Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.12 Billion |

| Market Size (2026) | USD 1.16 Billion |

| Market Size (2031) | USD 1.39 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Argentina Food Sweetener Market Analysis by Mordor Intelligence

The Argentine sweeteners market size is expected to grow from USD 1.12 billion in 2025 to USD 1.16 billion in 2026 and is forecast to reach USD 1.39 billion by 2031 at 3.62% CAGR over 2026-2031. The growing demand for food sweeteners in Argentina is being driven by a societal shift towards healthier lifestyles, proactive regulatory reforms, and robust industry innovations. As awareness of diet-related ailments such as obesity, diabetes, and cardiovascular diseases rises, Argentine consumers are increasingly turning to low- or zero-calorie sweeteners. Options like stevia, erythritol, sucralose, and aspartame are becoming preferred substitutes for traditional sugar. Highlighting this trend, the Pan American Health Organization (PAHO) reported in 2022 that 68.4% of Argentina's adult population was classified as obese. Furthermore, government measures, including sugar taxes and mandatory “front-of-package” warning labels, have intensified the shift away from high-sugar products. These initiatives are nudging both consumers and manufacturers towards healthier alternatives. On a related note, policy changes like the January 2025 elimination of sugar export taxes, are altering the dynamics of raw-material flows. This not only fortifies domestic supply chains but also enhances cost competitiveness.

Key Report Takeaways

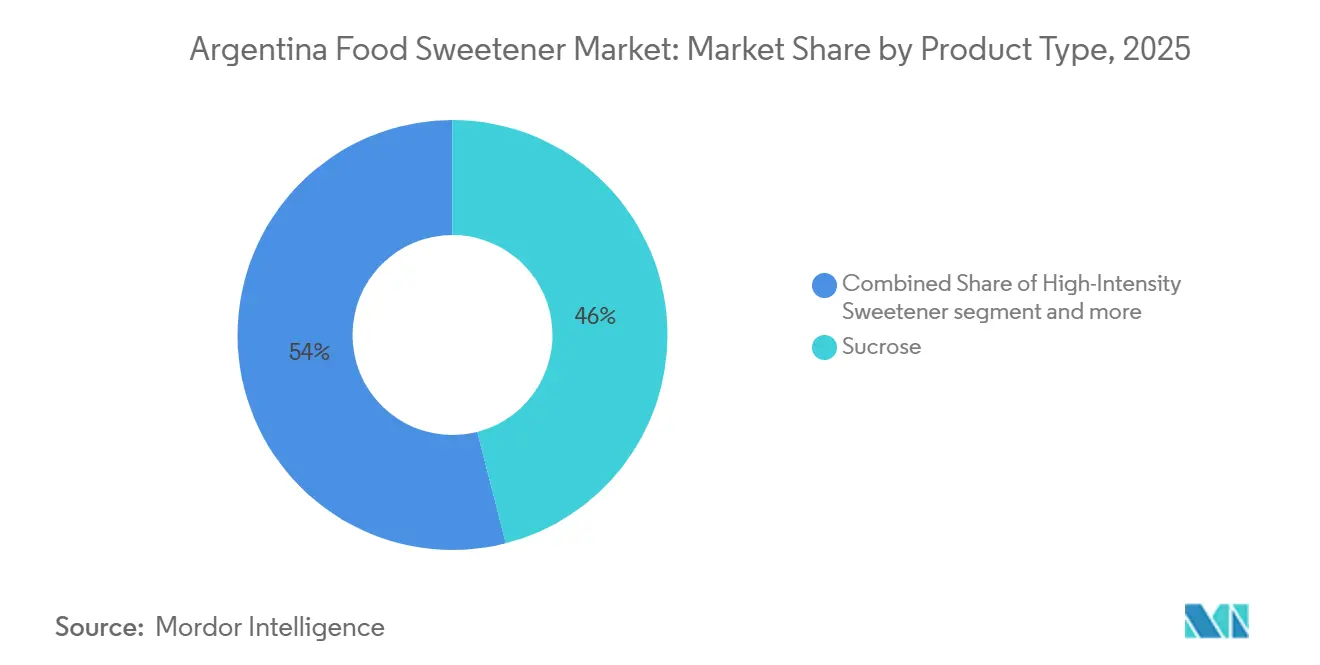

- By product type, sucrose led with 46.02% of Argentina's sweeteners market share in 2025; high-intensity sweeteners are projected to expand at a 4.32% CAGR to 2031.

- By application, beverages accounted for 36.78% of the Argentine sweeteners market size in 2025, while dairy and desserts post the fastest 4.12% CAGR through 2031.

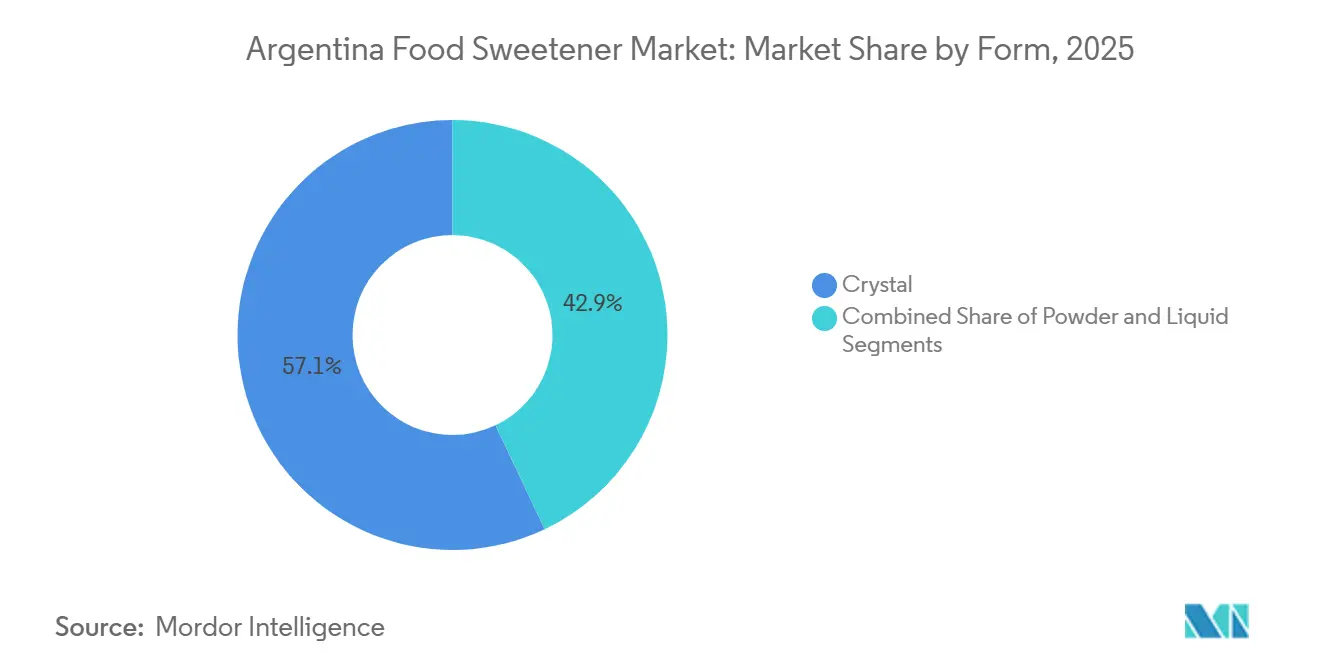

- By form, crystal sweeteners captured 57.06% revenue in 2025; liquid form is set to grow at a 4.61% CAGR over the same period.

- By category, conventional products held 79.74% share in 2025, yet organic variants are forecast to climb at a 5.29% CAGR toward 2031.

- By geography, Buenos Aires Province commanded 55.72% of Argentina's sweeteners market size in 2025, whereas the Central Region records the strongest 4.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Food Sweetener Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising obesity and diabetes rates | +1.2% | National; sharpest pressure in Buenos Aires Province | Medium term (2-4 years) |

| Government push for sugar reduction | +0.8% | National law applies to every province | Short term (≤ 2 years) |

| Growing consumer demand for low-calorie and natural sweeteners | +0.9% | National, strongest uptake in Buenos Aires and Central Region | Medium term (2-4 years) |

| Growing adoption in functional food and beverage | +0.6% | Buenos Aires Province and Central Region | Long term (≥ 5 years) |

| Beverage reformulations by global brands | +0.7% | Urban centers nationwide | Short term (≤ 2 years) |

| Clean-label preference for plant-based sweeteners | +0.5% | Buenos Aires Province and Central Region | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Rising obesity and diabetes rates

In Argentina, surging rates of obesity and diabetes are driving a heightened demand for sweeteners, particularly organic and natural alternatives. As the adult population grapples with rising obesity rates and soaring diabetes cases, the nation confronts a significant health crisis, intensifying the push for natural sweetener substitutes. For instance, the International Diabetes Federation reported that in 2024, Argentina was home to 4.34 million diabetics [1]International Diabetes Federation, "Number of adult population with diabetes", idf.org. As public awareness grows, many Argentinians are swapping high-calorie sugars for low- or zero-calorie sweeteners, with a pronounced preference for natural options like stevia and organic monk fruit. These natural sweeteners resonate with health-conscious consumers who prioritize “clean-label” ingredients. In response, both regulators and food companies are reformulating products to align with these health trends. Thus, the pervasive challenges of obesity and diabetes are catalyzing a pronounced shift towards healthier sweetening solutions in Argentina's food and beverage landscape.

Government push for sugar reduction

Argentina's government, driven by the 2020 Healthy Eating Law and a 2022 decree, has intensified its focus on sweeteners. The law mandates black octagon warnings on products high in sugar, fat, sodium, or calories, and requires products with sweeteners to display a cautionary label: “contains sweeteners, not recommended for children.” These measures, along with marketing restrictions targeting minors and a sales ban in schools, are prompting manufacturers to reformulate products to avoid negative labels. In December 2024, ANMAT (Argentina’s food and drug regulator) introduced Provisions 11378/2024 and 11362/2024, refining Decree 151/2022. These provisions demand clearer labeling to differentiate between naturally occurring and added sugars and impose stricter advertising restrictions on products with warning labels, particularly for children and adolescents. Research shows many companies have reduced sugar content in key categories like ice cream, chocolate, biscuits, and snacks, often replacing it with alternative sweeteners. This regulatory push is driving demand for artificial sweeteners (sucralose, aspartame, cyclamate) and natural ones (stevia, erythritol, monk fruit), reshaping the food and beverage market towards healthier formulations.

Growing demand for low-calorie and natural sweeteners

Amid rising concerns over obesity and diabetes, Argentina is shifting towards healthier, low-calorie lifestyles, driving demand for natural sweeteners like stevia, erythritol, monk fruit, and sorbitol. These sweeteners, valued for their zero-calorie or low-glycemic properties, align with the nation's clean-label trends and wellness-focused diets. Stevia stands out, supported by government initiatives and regulatory frameworks that expedite approvals and subsidize local production. In 2024, Argentina's Ministry of Agriculture allocated approximately USD 45 million to natural sweetener programs, with 30% directed towards stevia development. Production subsidies for stevia farmers rose by 65%, while SENASA accelerated stevia-related approvals by 42% compared to artificial sweeteners. Certified organic stevia has gained traction among health-conscious and environmentally-aware consumers, driven by a shift towards plant-based and organic products. Technological advancements in extraction and flavor enhancement have further boosted the appeal of natural sweeteners in beverages, confections, and baked goods. With growing consumer preferences for low-calorie, natural, and organic solutions, Argentina's alternative sweeteners market is set for significant growth.

Beverage reformulations by global brands

In Argentina, beverage giants like Coca-Cola, PepsiCo, and Nestlé are reformulating their flagship drinks to meet changing regulatory standards and consumer preferences. This shift has increased demand for alternative sweeteners, especially natural and organic options. Companies are replacing full-sugar recipes with low- or zero-calorie substitutes, blending artificial sweeteners like aspartame and ace-K with natural ones such as stevia, erythritol, and monk fruit. For example, Guaraná Antarctica Zero, a sugar-free version of the popular Brazilian soda, is gaining popularity as consumers prefer no-sugar carbonated options. Ingredient suppliers like ADM and Sensient are supporting this trend by offering stevia extracts like Reb M and blends that mimic sugar's mouthfeel. These reformulation efforts are driving demand for organic, plant-based, and cleaner-label sweeteners in Argentina.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of natural and imported sweeteners | -0.9% | National, greatest pressure in Central Region and interior provinces | Medium term (2-4 years) |

| Consumer skepticism toward artificial sweeteners | -0.6% | National, most evident in Buenos Aires Province | Short term (≤ 2 years) |

| Formulation challenges in certain food categories | -0.4% | Buenos Aires Province and Central Region | Long term (≥ 5 years) |

| Volatility in raw-material prices | -0.7% | National; sugar- and corn-based supply centered in northern provinces | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cost of natural and imported sweeteners

In 2024, Argentina grapples with economic volatility, currency devaluation, and persistent inflation, driving up the costs of imported ingredients. High-purity stevia extracts, monk fruit, and erythritol sourced predominantly from China and the U.S. have seen notable price hikes. For context, the Instituto Nacional de Estadística y Censos (Argentina) reported that Argentina's Consumer Price Index (CPI) in April 2024 surged by 289% compared to the same month the previous year. Domestic production of natural sweeteners in Argentina is limited and lacks the economies of scale to compete with cheaper, mass-market artificial alternatives like cyclamate and saccharin. Consequently, many manufacturers are leaning towards more affordable synthetic sweeteners or are curtailing reformulation efforts to keep retail prices stable. In Argentina's lower-income demographics, concerns about affordability often overshadow health considerations, leading to diminished demand for premium natural or organic sweeteners. Thus, despite a rise in health awareness and regulatory pressures, cost challenges continue to temper the growth of Argentina's natural sweetener market.

Consumer skepticism toward artificial sweeteners

In Argentina, heightened public scrutiny over synthetic sweeteners like aspartame, saccharin, and cyclamate has emerged, often tied to media narratives linking them to cancer risks or metabolic disruptions. This growing concern has prompted many Argentine consumers to meticulously examine ingredient labels, steering clear of products with artificial additives. Argentina's stringent front-of-package labeling laws further amplify this skepticism. These laws mandate clear warnings on products with non-nutritive sweeteners, particularly those aimed at children. Consequently, many consumers now associate "sugar-free" labels with "chemically altered" products, leading to a decline in purchases of these artificially sweetened items, even if they boast fewer calories. This wariness is notably stronger among health-conscious individuals and younger consumers, who lean towards natural alternatives or reduced-sugar options devoid of synthetic ingredients. Thus, while regulatory and health trends push for a reduction in sugar use, the prevailing negative sentiment towards artificial sweeteners is hindering their broader acceptance in Argentina's food and beverage sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sucrose Dominants, While High-Intensity Sweeteners is Growing

In 2025, sucrose commanded a 46.02% share of Argentina's sweeteners market, buoyed by strong cane yields and the 2025 abolition of sugar export taxes. Sucrose's demand in Argentina spans industries from bakery and confectionery to dairy and processed foods thanks to its versatility, accessibility, and cost-effectiveness. Beyond just sweetness, sucrose is pivotal for texture, preservation, and browning in food manufacturing, making its large-scale replacement challenging. Illustrating this demand, Argentina's sucrose imports rose from 281 tons the previous year to 472 tons in 2024, as per ITC Trademap .

Meanwhile, high-intensity sweeteners (HIS) are on the rise, expanding at a 4.32% CAGR, driven by mandates for calorie reduction and a growing emphasis on consumer wellness. As sucrose remains entrenched, there's a notable uptick in demand for high-intensity sweeteners (HIS). This shift is largely attributed to heightened health concerns, escalating rates of obesity and diabetes, and stringent sugar-reduction regulations. Sweeteners such as stevia, sucralose, and aspartame are increasingly favored in beverages, sugar-free snacks, and functional foods, delivering sweetness without the calories. This evolving landscape showcases a market in flux: while sucrose continues to hold its ground, there's a pronounced tilt towards low- and zero-calorie alternatives, especially in health-centric and reformulated products. Thus, the Argentine sweeteners market is broadening: upholding a robust demand for sucrose while swiftly embracing HIS for reformulation and compliance with health regulations.

By Application: Beverages Lead, While Dairy Accelerates

In 2025, beverages accounted for 36.78% of Argentina's sweeteners market, bolstered by the country's leading soft-drink volumes. Argentine beverage manufacturers favor sucrose not just for its sweetness, but for its mouthfeel, body, and flavor balance attributes, especially prized in traditional soft drinks, fruit juices, and flavored waters. Despite facing regulatory scrutiny and a consumer shift towards sugar reduction, many established beverages continue to lean on sucrose for consistency and familiar taste. Concurrently, Argentina's burgeoning beverage production bolsters the usage of sweeteners in beverages and this segment. For instance, the Instituto Nacional de Estadística y Censos reported the industrial production index (IPI) of beverages at 135.6 points in August 2024 .

Meanwhile, the dairy and dessert sectors are projected to grow at a brisk 4.12% CAGR through 2031, spurred by Arcor's increased stake in Mastellone, paving the way for new yogurt and flavored-milk innovations. Argentina's dairy sector, especially in yogurt, flavored milk, and desserts, is pivoting towards alternative sweeteners. This shift comes as manufacturers adapt to heightened health awareness and new labeling laws. Dairy producers are increasingly adopting both artificial and natural high-intensity sweeteners, such as sucralose, stevia, and erythritol. These choices enable them to craft reduced-sugar or sugar-free products that align with consumer demands for wellness and transparency. This trend underscores a complex landscape in Argentina's sweeteners market: while the beverage sector clings to sucrose for its traditional recipes, the dairy industry is charting a new course, championing innovative sweeteners to cater to health-focused consumers.

By Form: Crystal Dominates, While Liquid Innovation is On the Rise

Crystal forms dominate the market, accounting for 57.06% of sales, supported by established sucrose logistics and storage infrastructures at mills like La Providencia. Beverage OEMs prefer these forms for their inline dosing capabilities and reduced dust exposure. In Argentina, food and beverage manufacturers favor crystal-formed sweeteners for their ease of handling, extended shelf life, and compatibility with dry formulations such as baked goods and powdered drink mixes. Crystalline sweeteners, including sucrose, stevia powder, and select sugar alcohols, are valued for enhancing texture, providing bulk, and maintaining heat stability during processing. As Argentina increases food and beverage production, demand for these sweeteners grows. The Instituto Nacional de Estadística y Censos (Argentina) reported a 2022 gross production value (GPV) of 2.6 trillion Argentine pesos for the food service industry, a 144% rise from the previous year.

Liquid formats, growing at a 4.61% CAGR, are gaining traction, particularly in beverage manufacturing, dairy applications, and processed foods. Their advantages—precise dosing, rapid solubility, and easy mixing—are driving demand. Sweeteners like liquid stevia, glucose syrup, and agave nectar ensure uniform sweetness distribution and support health-driven reformulations in ready-to-drink beverages and yogurts. This trend highlights Argentina's sweeteners market dynamics, where liquid sweeteners are carving a niche in health-focused and high-volume processing sectors, while crystalline forms dominate traditional applications.

By Category: Conventional Leads, as Organic Accelerates

In 2025, conventional offerings made up 79.74% of the market volume. In Argentina, food and beverage manufacturers favor conventional sweeteners for their cost-effectiveness, wide availability, and proven functionality in mass-market products. Ingredients such as sucrose, glucose syrup, and high-fructose corn syrup play a pivotal role in producing baked goods, soft drinks, dairy items, and processed snacks. These ingredients deliver consistent performance and a familiar taste profile at a low cost, a crucial factor in a price-sensitive market grappling with inflation and currency fluctuations. To illustrate, Argentina imported USD 7.9 million worth of sucralose in 2024, underscoring the demand for conventional sweeteners.

Organic variants are on the rise, boasting a robust 5.29% CAGR, driven by a surge in organic food shoppers, who have doubled in number over the past five years. As consumer preferences evolve towards clean-label, health-focused, and eco-friendly products, the demand for organic sweeteners is steadily rising. Heightened awareness of wellness and nutrition, coupled with regulatory and marketing pushes for natural ingredients, has led many manufacturers to explore organic options. Ingredients like certified organic stevia, coconut sugar, and agave syrup are being adopted to set their offerings apart and cater to premium market segments. Although challenges like cost and limited local production hinder widespread adoption, the growing interest in organic alternatives indicates a notable shift in Argentina’s sweetener landscape. While conventional options still hold sway, organic sweeteners are carving out a niche, aligning with changing consumer values and global food trends.

Geography Analysis

In 2025, Buenos Aires Province seized a commanding 55.72% share of Argentina's sweeteners market, bolstered by its dense food-processing hubs and efficient port logistics for ingredient imports. Beverage titans are setting up bottling lines close to urban demand, while ingredient suppliers are strategically placing bulk-storage terminals in docklands for liquid glucose and fructose. Echoing national sugar-reduction goals, provincial health policies are hastening product reformulations and boosting local demand for premium sweeteners.

The Central Region is emerging as the fastest-growing area, with a projected 4.92% CAGR through 2031, thanks to its proximity to corn and cane feedstocks within a convenient trucking radius. New investments in Córdoba and Santa Fe are establishing starch-sweetener plants, capitalizing on grain silos for a more integrated supply chain. With regional incentives and less congestion than Buenos Aires, mid-scale enterprises are seizing opportunities in natural HIS extraction. In 2025, pilot formulations of monk fruit were introduced, aiming at dairy and sports-drink manufacturers based in Córdoba, further emphasizing local value addition.

Tucumán, Jujuy, and Salta, the northern provinces, account for a staggering 99.5% of Argentina's sugar production. Ethanol mandates, which elevate gasoline blends to 12%, bolster cash-flow stability for cane mills, thereby indirectly supporting sweetener co-production. In Misiones, stevia plantations cater to both domestic and international markets, with companies like Yevia collaborating with agronomic institutes to cultivate high-Reb M varieties. Thanks to infrastructure enhancements on Route 34, haulage costs to refiners in the Central Region have diminished, streamlining the supply chain across Argentina's sweeteners market.

Competitive Landscape

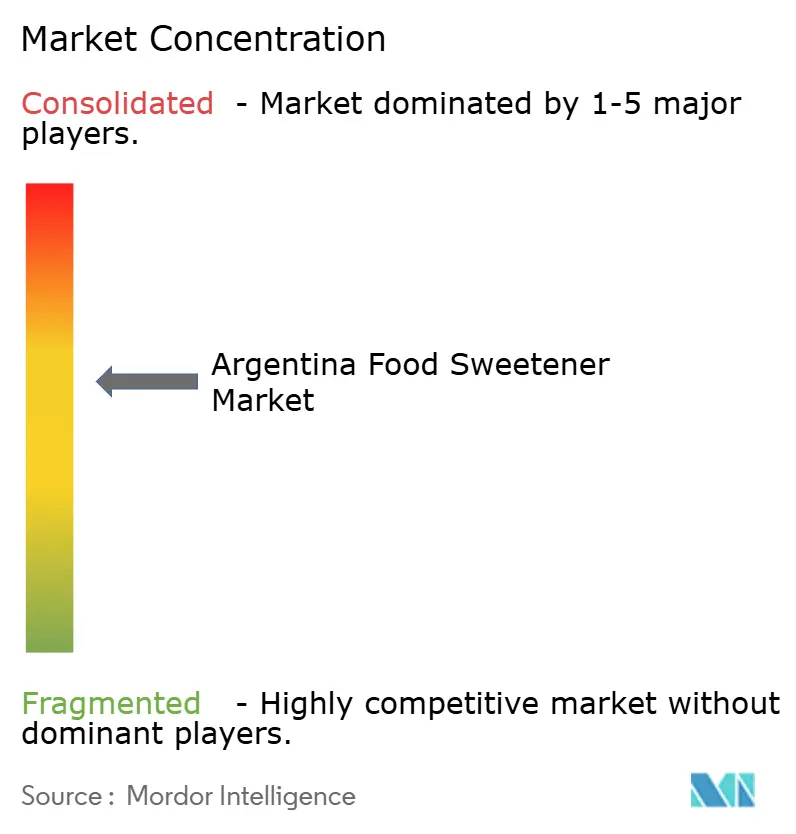

Argentina's food sweetener market demonstrates moderate consolidation, with major players including Tate & Lyle PLC, Cargill, Incorporated, Archer Daniels Midland Company, Ingredion Incorporated, and International Flavors & Fragrances Inc. These companies maintain significant market share through exclusive high-intensity sweetener formulations and technical service laboratories in Greater Buenos Aires.

Strategic initiatives emphasize natural sweeteners and fortifying supply chains in the market. In April 2025, Arca Continental's investment in AI-driven Sensify, aimed at enhancing cooler uptime, underscores a push for better distribution efficiency. Ingredion's increased stake in PureCircle, now at 88%, bolsters its bioconversion capabilities for premium steviol glycosides. SWT Stevia, championing a seed-to-shelf certification, collaborates with mate-tea brands to market monk-fruit/stevia blends, eyeing clean-label premiums.

While import challenges boost localized production, benefiting domestic players with raw-material security, global suppliers leverage their scale and research and development prowess, offering technical support and value-added solutions to maintain their market share. The organic segment presents a lucrative avenue for nimble entrants, albeit with certification challenges. Thus, the competitive landscape is shaped by innovation, cost management amidst peso fluctuations, and timely front-label reformulations.

Argentina Food Sweetener Industry Leaders

-

Tate & Lyle PLC

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Ingredion Incorporated

-

International Flavors and Fragrances Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Tate & Lyle and Manus have partnered to ensure a secure and sustainable supply of Reb M. The Natural Sweetener Alliance aims to provide scalable, sustainable, and reduced-calorie sweeteners. They plan to achieve this by harnessing Tate & Lyle's expertise in sugar reduction and Manus' bio-conversion technology, sourcing from an all-Americas supply chain that includes Argentina.

- March 2024: Ingredion reported USD 8.2 billion net sales for 2023 and raised PureCircle ownership to 88% to strengthen its natural sweeteners platform. Ingredion’s earlier joint venture with Grupo Arcor in Argentina and neighboring countries links its global sweetener innovations directly to local production facilities in Chacabuco, Baradero, Lules, and Córdoba. The PureCircle-backed technologies can now be leveraged through these established channels, speeding formulation and distribution of natural sweetener blends in the Argentine market.

- January 2023: Sweegen expanded its bioconversion stevia portfolio (Rebaudiosides E and I) in Latin America following regulatory approval in Colombia. Though Argentina-specific, this rollout establishes a foundation for new stevia-infused formulations across the region, including potential launches in Argentina using these new extracts.

Argentina Food Sweetener Market Report Scope

Food sweeteners are classified as food additives that are used or intended to be used as tabletop sweeteners or to give meals a sweet flavor.

Argentina's Food Sweetener Market is segmented by Type (Sucrose, Starch Sweeteners, and Sugar Alcohols (Dextrose, High Fructose Corn Syrup, Maltodextrin, Sorbitol, Xylitol, and Others) and High-intensity Sweeteners (Sucralose, Aspartame, Saccharin, Cyclamate, Ace-K, Neotame, Stevia, and Others)) and Application (Dairy, Bakery, Soups, Sauces and Dressings, Confectionery, Beverages, and Other Applications). The report offers the market size and forecasts in value (USD million) for all the above segments.

By Product Type

| Sucrose | ||

| Starch Sweeteners and Sugar Alcohols | Dextrose | |

| High Fructose Corn Syrup (HFCS) | ||

| Maltodextrin | ||

| Sorbitol | ||

| Xylitol | ||

| Other Starch Sweeteners and Sugar Alcohols | ||

| High-Intensity Sweeteners | Artificial High-Intensity Sweeteners | Sucralose |

| Aspartame | ||

| Saccharin | ||

| Neotame | ||

| Cyclamate | ||

| Acesulfame Potassium (Ace-K) | ||

| Other Artificial HIS | ||

| Natural High-Intensity Sweeteners | Stevia Extract | |

| Monk Fruit Extract | ||

| Other Natural HIS | ||

| Other Sweeteners | ||

By Application

| Bakery and Confectionery |

| Dairy and Desserts |

| Beverages |

| Soups, Sauces, and Dressings |

| Other Applications |

By Form

| Powder |

| Liquid |

| Crystal |

By Category

| Conventional |

| Organic |

By Region

| Buenos Aires Province |

| Central Region |

| Others |

| By Product Type | Sucrose | ||

| Starch Sweeteners and Sugar Alcohols | Dextrose | ||

| High Fructose Corn Syrup (HFCS) | |||

| Maltodextrin | |||

| Sorbitol | |||

| Xylitol | |||

| Other Starch Sweeteners and Sugar Alcohols | |||

| High-Intensity Sweeteners | Artificial High-Intensity Sweeteners | Sucralose | |

| Aspartame | |||

| Saccharin | |||

| Neotame | |||

| Cyclamate | |||

| Acesulfame Potassium (Ace-K) | |||

| Other Artificial HIS | |||

| Natural High-Intensity Sweeteners | Stevia Extract | ||

| Monk Fruit Extract | |||

| Other Natural HIS | |||

| Other Sweeteners | |||

| By Application | Bakery and Confectionery | ||

| Dairy and Desserts | |||

| Beverages | |||

| Soups, Sauces, and Dressings | |||

| Other Applications | |||

| By Form | Powder | ||

| Liquid | |||

| Crystal | |||

| By Category | Conventional | ||

| Organic | |||

| By Region | Buenos Aires Province | ||

| Central Region | |||

| Others | |||

Key Questions Answered in the Report

What is the current size of the Argentina sweeteners market?

The market stands at USD 1.16 billion in 2026 and is projected to reach USD 1.39 billion by 2031.

Which segment holds the largest Argentina sweeteners market share?

Sucrose leads with 46.02% share in 2025, reflecting Argentina’s strong cane-sugar base.

What category is growing fastest within the Argentina sweeteners market?

Organic sweeteners post the fastest 5.29% CAGR 2026-2031, buoyed by expanding clean-label demand.

Which region is the most lucrative for sweetener players in Argentina?

Buenos Aires Province captures 55.72% of market value thanks to dense processing capacity and consumer concentration.

How is government policy influencing Argentina sweeteners market size?

Front-of-pack warning labels, sugar-tax debate and the sugar export-tax repeal together propel reformulation and raw-material availability, supporting steady 3.62% annual growth.

Page last updated on: