Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

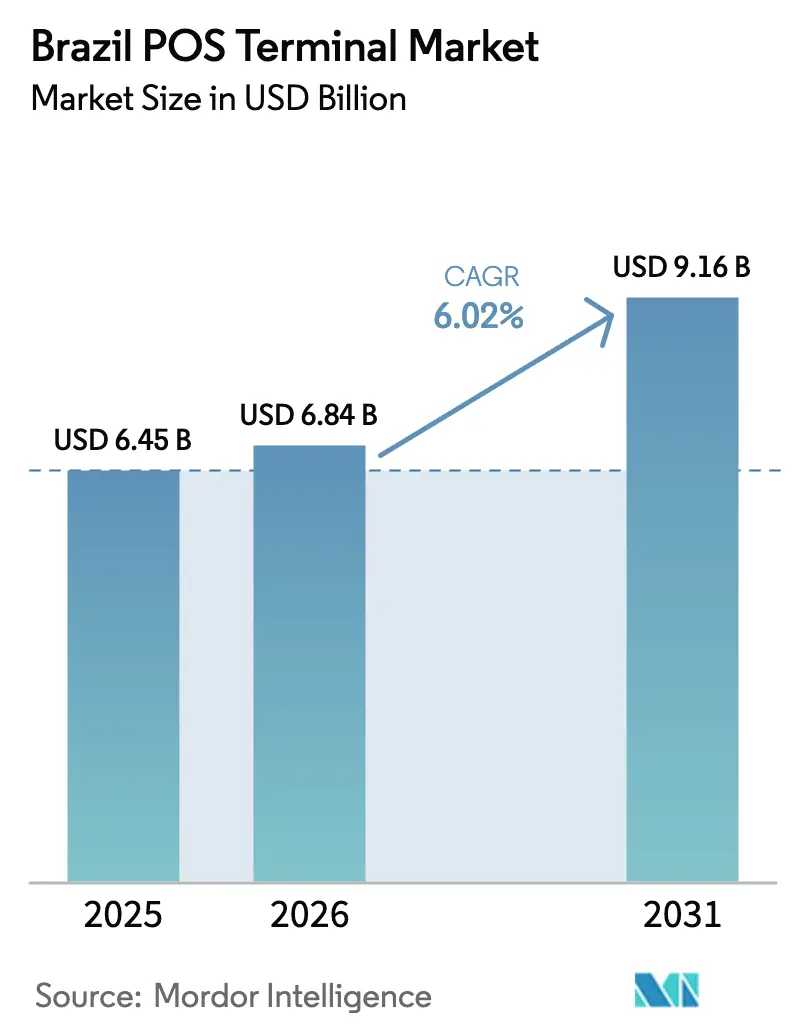

| Base Year Market Size (2025) | USD 6.45 Billion |

| Market Size (2026) | USD 6.84 Billion |

| Market Size (2031) | USD 9.16 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

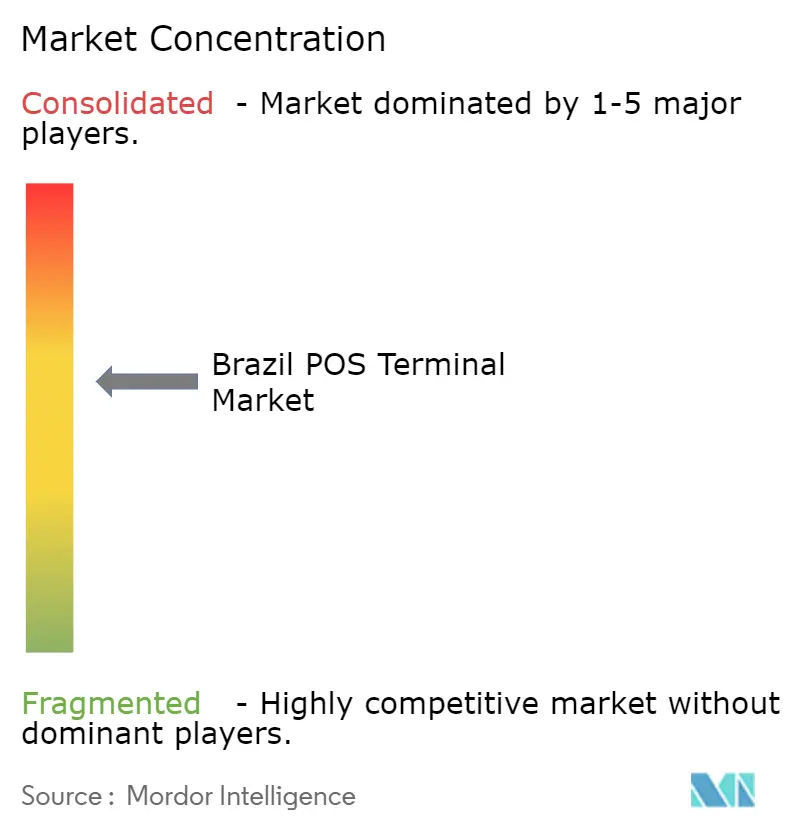

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil POS Terminal Market Analysis by Mordor Intelligence

The Brazil POS terminal market size is expected to grow from USD 6.45 billion in 2025 to USD 6.84 billion in 2026 and is forecast to reach USD 9.16 billion by 2031 at 6.02% CAGR over 2026-2031. Robust consumer acceptance of tap-to-pay cards, the rollout of Pix by Proximity, and an accelerating replacement cycle for legacy fixed devices collectively support persistent double-digit unit demand. Acquirers are shifting capital toward Android smart terminals that converge EMV contactless and Pix NFC payloads, allowing merchants to reconcile real-time and card transactions in a single ledger. Fintech acquirers deepen distribution by subsidizing hardware in exchange for data-driven lending rights, tying device adoption to embedded working-capital offers. At the same time, card networks and the central bank mandate full contactless enablement, compressing the useful life of contact-only estates and enlarging the serviceable base for next-generation hardware.

Key Report Takeaways

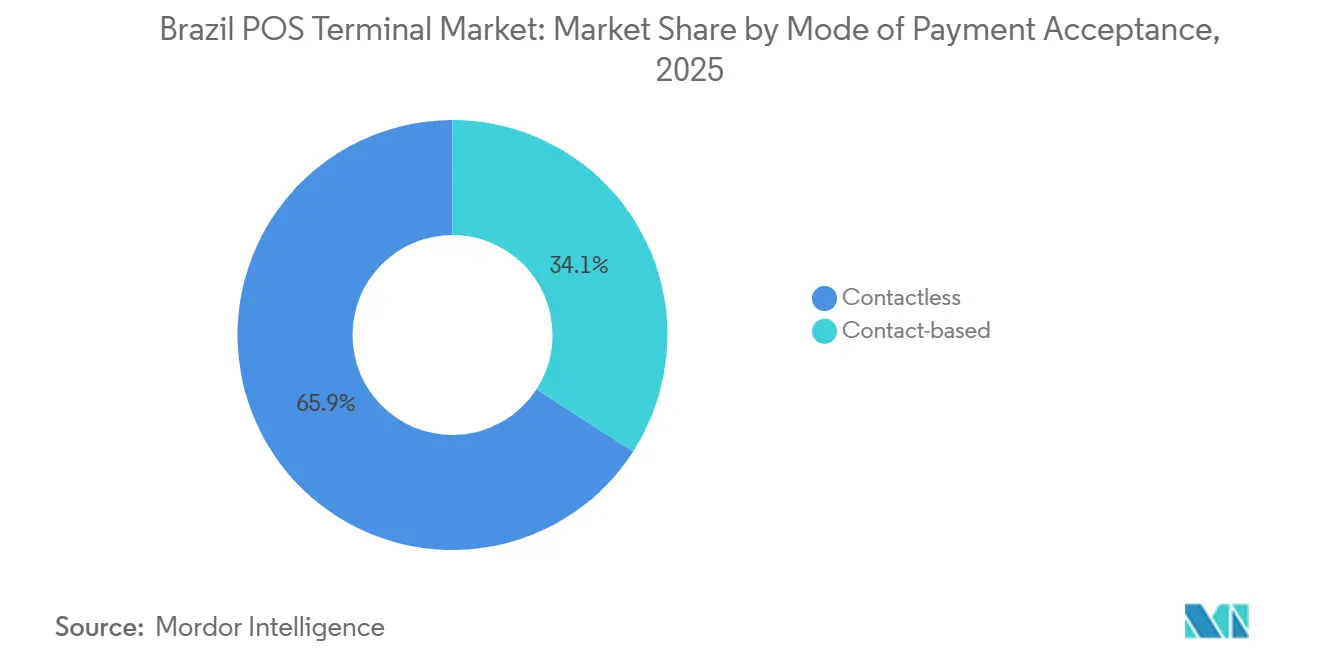

- By mode of payment acceptance, contactless commanded 65.89% of the Brazil POS terminal market share in 2025 and is projected to expand at a 6.48% CAGR through 2031.

- By POS type, mobile and portable devices held 53.97% share of the Brazil POS terminal market size in 2025 while posting the fastest expected CAGR of 6.54% over 2026-2031.

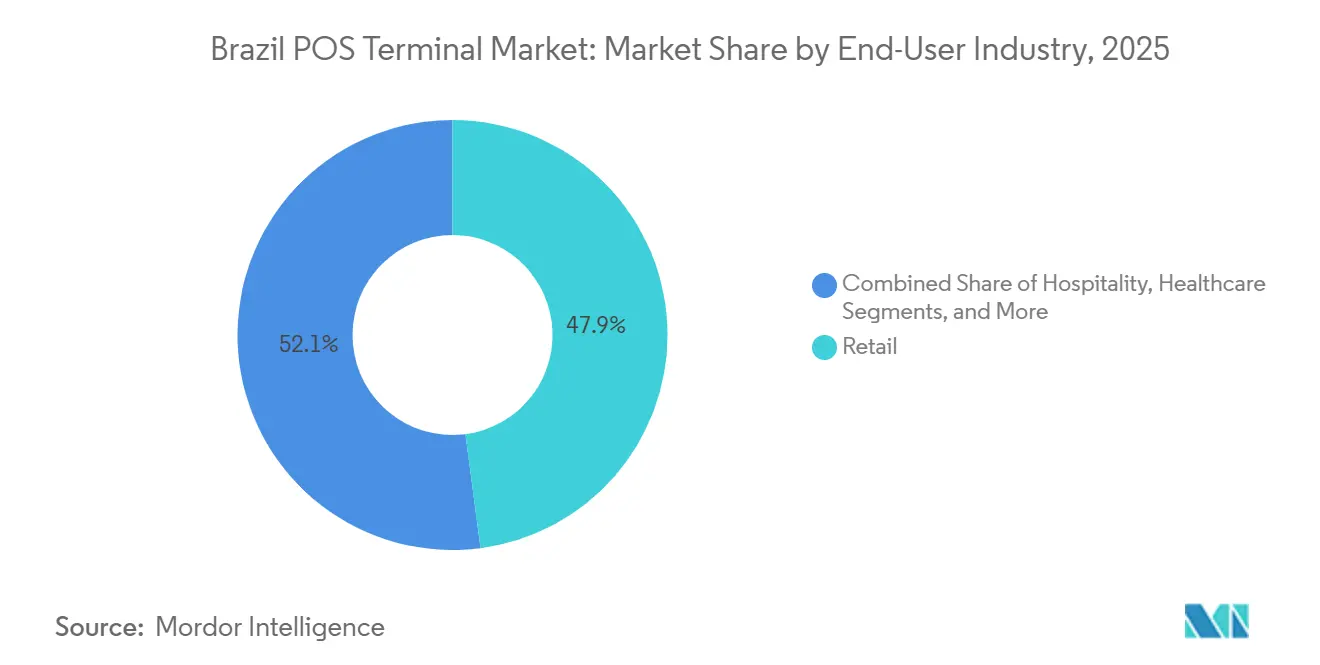

- By end-user industry, retail led with 47.92% revenue share in 2025 whereas healthcare is forecast to advance at a 7.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil POS Terminal Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Contactless and NFC Adoption | +1.8% | National, early lead in Southeast, growing in Northeast tourism corridors | Medium term (2-4 years) |

| Rapid Expansion of mPOS Among SMEs | +1.5% | National, strongest in Southeast and South | Short term (≤ 2 years) |

| Pix-by-Proximity Integration Driving Hybrid Terminals | +1.3% | National, led by large urban centers | Medium term (2-4 years) |

| Regulatory Mandates for EMV and PCI Compliance | +0.9% | National | Long term (≥ 4 years) |

| Unified-Commerce Demand for Real-Time Data Loops | +0.7% | Southeast and South | Medium term (2-4 years) |

| Cloud-Managed POS Enabling AI Merchant Scoring | +0.6% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Contactless and NFC Adoption

Contactless card payments reached 67.2% of all in-person card transactions by December 2024, fueled by dual-interface card reissuance and pandemic-era habit formation.[1]Abecs, “Abecs Statistics and Normatives”, abecs.org.br Pix by Proximity, launched in February 2025, now extends the same tap gesture to instant payments, letting merchants favor real-time settlement at lower fees. Terminal vendors consequently bundle dual-mode NFC chipsets that read EMV credentials and Pix payloads without separate peripherals. Mastercard’s acceptance mandate obliges acquirers to retrofit or replace non-NFC estates, shortening upgrade cycles. The resulting hardware refresh accelerates revenue visibility for manufacturers while raising the performance baseline for future-proof devices.

Rapid Expansion of mPOS Among SMEs

Micro-merchants gravitate to low-capex acceptance, and mPOS solutions addressed 4.125 million Stone clients by year-end 2024, processing USD 96 billion in volume. Tap-on-phone software converts off-the-shelf Android handsets into terminals, eliminating upfront hardware spend and enabling same-day onboarding. Fintech acquirers incentivize adoption through instant settlement and algorithmic credit offers, monetizing data flows rather than per-transaction fees. Open APIs released by the central bank reduce certification friction, inviting a long tail of developers to ship niche vertical apps. As subscriptions and lending replace device margin, platform depth becomes the primary SME buying criterion.

Pix-by-Proximity Integration Driving Hybrid Terminals

Resolutions 406 and 407 permit NFC-initiated Pix transfers that settle in real time at roughly one-third of the debit-card fee.[2]Priscilla Santos and Ingrid Pistili, “PIX and Open Finance: What Is Coming Next?”, Tauil & Chequer, tauilchequer.com.br Merchants can now apply dynamic checkout pricing, steering price-sensitive shoppers toward Pix while preserving card rails for high-ticket or installment sales. Worldline’s Yooz and Verifone’s latest Android lines integrate Payment Transaction Initiation Service APIs, assuring compliance while simplifying merchant reconciliation. Smaller OEMs struggle with the certification overhead, widening the capability gap. Acquirers are ready to capture hybrid firmware-switching demand as merchants sunset single-rail equipment.

Regulatory Mandates for EMV and PCI Compliance

Banco Central do Brasil enforces recurring firmware updates, including new application identifiers for the Trilho Voucher network that must be live by November 2025. Non-compliance risks fines and higher chargeback exposure, incentivizing acquirers to deploy devices supporting remote key injection and cloud updates. Bradesco’s deployment of AI fraud scoring on nearly one billion Pix transactions per month shows how compliance investments can also lift approval rates and customer trust. Vendors embedding secure elements and hardware encryption earn preference among regulated merchants, anchoring premium pricing tiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Security and Cyber-Fraud Incidents | -1.2% | National, highest in digital-first urban hubs | Short term (≤ 2 years) |

| High Up-Front Hardware Costs For Micro-Merchants | -0.8% | National, acute in less-dense regions | Medium term (2-4 years) |

| Margin Squeeze From Zero-Fee Pix | -1.1% | National | Medium term (2-4 years) |

| Semiconductor Module Supply Volatility | -0.5% | Global supply, national impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Security and Cyber-Fraud Incidents

Pix fraud losses hit USD 1.2 billion in 2024, an 80% jump from the prior year, with 4.7 million confirmed cases. Social-engineering scams and malware such as Prilex exploit legacy firmware that blocks NFC to coerce chip insertion, siphoning credentials.[3]G1, “Prilex Malware Targeting POS Terminals”, g1.globo.com Acquirers respond by accelerating migrations to cloud-managed devices featuring end-to-end encryption and biometric operator login. However, retrofitting those controls onto installed bases strains capital budgets. Liability pressures, therefore, slow procurement among price-sensitive merchants and elongate decision cycles.

High Up-Front Hardware Costs For Micro-Merchants

Merchants frequently route customers to personal Pix keys to avoid person-to-business fees, eroding acquirer revenue tied to MDR. InfinitePay countered by offering fee-free Pix acceptance and monetizing through AI-driven lending, a tactic that raised business-account consent share to 19.5% by August 2025. As rivals copy the playbook, terminal hardware risk becomes a subsidized entry point for cross-selling credit and analytics, compressing standalone device profitability. The June 2025 debut of Automatic Pix, which facilitates unattended recurring debits, further shifts value toward ancillary services, challenging acquirers reliant on pure processing margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode Of Payment Acceptance: Contactless Uptake Reshapes Hardware Strategy

Contactless acceptance represented 65.89% of the Brazil POS terminal market share in 2025 and is on track to post a 6.48% CAGR through 2031, a trajectory that underscores the convergence of card and Pix tap experiences. The Brazil POS terminal market size attached to contactless-enabled units will therefore rise faster than the overall installed base, forcing acquirers to prioritize devices with integrated dual-interface antennas. Rising consumer comfort with tap-to-pay encourages merchants to streamline checkout flows, lowering average queue times and boosting basket conversion. Pix by Proximity extends these gains by guaranteeing real-time settlement without invoking card authorization holds, giving retailers the confidence to eliminate surcharge differentials. Mastercard’s national mandate cements contactless capability as a non-negotiable purchase criterion, relegating contact-only terminals to obsolescence. Vendors that master simultaneous EMV kernel and Pix NFC payload processing gain a defensible position, since certification windows for dual-mode devices remain resource-intensive.

Despite its shrinking share, chip-and-PIN retains relevance for high-value or installment purchases where customers prefer perceived extra security. However, the maintenance burden of dual firmware paths is prompting acquirers to consolidate SKUs around Android smart terminals capable of fallback to contact authentication. PAX Technology’s A920 Pro, Worldline’s Yper, and Verifone’s Engage lines already ship with standardized contactless stacks, easing fleet management for nationwide retailers that run mixed loyalty and inventory applications. As greenfield merchants subscribe directly through fintech apps, first-time hardware purchases increasingly default to contactless, further entrenching the modality and ensuring that replacement cycles skew toward hybrid-capable devices.

By POS Type: Mobile And Portable Units Capture SME Wallet

Mobile and portable solutions accounted for 53.97% of the Brazil POS terminal market size in 2025 and are projected to deliver the highest 6.54% CAGR to 2031. Their dominance stems from a pay-as-you-go cost structure paired with same-day settlement that appeals to restaurants, street vendors, and service professionals. Fintech acquirers bundle instant merchant onboarding, real-time dashboards, and automated tax reporting, making the offer compelling even for previously cash-only micro-enterprises. Android form factors support inventory apps, delivery integrations, and conversational commerce, embedding the terminal into daily operations rather than treating it as a commodity peripheral. Subscription bundles thus anchor multi-year stickiness while opening upsell lanes for working-capital loans.

Fixed systems continue to serve supermarkets, fuel chains, and healthcare clinics that value ruggedized hardware, high transaction throughput, and back-office integration. NCR Voyix Pulse illustrates the trend by syncing e-commerce carts, inventory files, and in-store transactions within a single data layer, thereby enabling click-and-collect services. Although capital-intensive, these smart counters tie acceptance to broader omnichannel strategies, justifying premium pricing. Dual deployment models will co-exist, yet unit growth will skew toward mobile devices as smartphone penetration widens and 4G coverage expands into the North and Central-West. Vendors offering modular portfolios that bridge both segments insulate revenue against cyclical swings in either channel.

By End-User Industry: Healthcare Digitization Outpaces Retail

Retail delivered 47.92% revenue share in 2025 by virtue of Brazil’s dense merchant footprint, but healthcare is projected to record a 7.27% CAGR through 2031, the fastest across verticals. Hospitals and clinics embed contactless terminals in reception areas, pharmacies, and telemedicine portals, enabling patients to tokenize cards or Pix keys for co-pay settlement aligned with electronic health records. LGPD compliance drives demand for devices housing dedicated secure elements that segregate patient identifiers from payment credentials, a feature set that commands higher average selling prices. Insurance reimbursements tied to instant confirmation reinforce the business case, elevating payment orchestration from back-office task to strategic imperative.

Hospitality and tourism, fuelled by 6.6 million international arrivals in 2024, sustain a parallel upgrade wave as hotels and restaurants pivot to tip-adjusted contactless workflows. Transportation, logistics, and professional services collectively embrace mPOS for on-the-go billing, but adoption ratios vary with local connectivity. Retail itself faces saturation risk yet unlocks incremental terminal demand by moving toward unified commerce that harmonizes curbside pickup, online reservations, and store inventory through cloud APIs. The interplay of vertical-specific compliance, workflow integration, and financing incentives will dictate vendor share in each segment of the Brazil POS terminal market.

Geography Analysis

The Southeast anchored the largest share of the Brazil POS terminal market in 2025, propelled by São Paulo’s diversified retail base and Rio de Janeiro’s tourism flows. Fintech giants Stone, PagSeguro, and InfinitePay pilot most product releases in this corridor, ensuring early merchant exposure to Android smart terminals, Open Finance consent frameworks, and Pix upsell programs. Intense rivalry, however, compresses MDR, prompting acquirers to differentiate via reconciliation automation, AI credit scores, and embedded payroll modules rather than price.

The Northeast is emerging as the fastest-growing region, catalyzed by revival in coastal tourism destinations such as Salvador and Fortaleza. Government financial-inclusion subsidies and smartphone-based mPOS bundles reduce hardware barriers for micro-merchants. Real-time analytics reveal that average daily Pix ticket sizes in beach districts now exceed card averages, nudging proprietors toward dual-mode devices tuned for offline QR fallback in spots with patchy cellular coverage. Terminal vendors that invest in Portuguese-only remote support, split settlement for tour aggregators, and anti-saltwater housing win disproportionate contracts in this market.

Southern, Central-West, and Northern states collectively represent a smaller installed base but display divergent needs. Agribusiness exporters in the South favor fixed Android counters integrated with ERP so they can reconcile B2B Pix flows that accounted for 42% of Pix value in March 2024. Central-West pharmacies and petrol stations embrace solar-powered mPOS to hedge intermittent grid supply, whereas the North relies on satellite backhaul and offline credential vaulting. Regional customization of connectivity, battery endurance, and climatic resilience therefore shapes procurement more than headline features, underscoring the geographic complexity inside the Brazil POS terminal market.

Competitive Landscape

Global OEMs Worldline, Verifone, and PAX Technology compete head-on with domestic brands Gertec, Elgin, and Bematech, yet ecosystem-oriented fintech acquirers now set the pace. InfinitePay issued more than USD 200 million in SME credit by October 2024 and reached 19.5% of Open Finance business consents by August 2025, signaling that underwriting agility can attract merchants faster than hardware innovation. Stone replicates the model with Tap Ton, while PagSeguro wraps working-capital advances around Point Smart 2 terminals. Device margin therefore compresses, and manufacturers offset by partnering with ERP suites, loyalty apps, and fraud engines to sell value-added subscriptions.

Worldline’s Yper and Yooz portfolios add 5G, Android 11, and over-the-air compliance patching, features that appeal to enterprise retailers subject to frequent regulatory updates. Verifone leverages its gateway footprint to pioneer International Pix routing, enabling multi-currency settlement for U.S. merchants catering to Brazilian travelers.[4]Verifone, “International Pix Partnership with PagBrasil”, verifone.com PAX Technology emphasizes open SDKs and third-party app stores, courting independent software vendors that bundle industry-specific tools onto the terminal. Domestic players differentiate through localized support, lower logistics costs, and willingness to certify niche voucher schemes.

Regulatory cadence acts as a competitive moat. Vendors that quickly embed Trilho Voucher AIDs, Automatic Pix mandates, and future cross-border Nexus APIs secure replacement contracts from acquirers wary of compliance fines. Meanwhile, white-label solutions from cloud startups threaten to erode OEM market share at the low end by turning smartphones into software POS. The balance of power will hinge on which cohort monetizes transaction data most effectively through credit, insurance, and analytics overlays inside the Brazil POS terminal market.

Brazil POS Terminal Industry Leaders

Worldline SA (Ingenico)

Verifone Systems LLC

PAX Technology Limited

NCR Voyix Corporation

Gertec Brasil Ltda.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: CloudWalk’s InfinitePay captured 19.5% of Open Finance business-consent share, up 97% since May.

- July 2025: Verifone partnered with PagBrasil to support International Pix acceptance for U.S. merchants targeting Brazilian shoppers.

- June 2025: Cielo confirmed 80% of its estate is Pix Automático ready ahead of the June 16 rule change.

- May 2025: Bradesco deployed FICO’s AI fraud platform on nearly one billion monthly Pix transactions, trimming false positives by 50%.

Brazil POS Terminal Market Report Scope

The Brazil POS Terminal Market Report is Segmented by Mode of Payment Acceptance (Contact-based, Contactless), POS Type (Fixed Point-of-Sale Systems, Mobile and Portable Point-of-Sale Systems), End-User Industry (Retail, Hospitality, Healthcare, Transportation and Logistics, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Mode of Payment Acceptance

| Contact-based |

| Contactless |

By POS Type

| Fixed Point-of-Sale Systems |

| Mobile and Portable Point-of-Sale Systems |

By End-User Industry

| Retail |

| Hospitality |

| Healthcare |

| Transportation and Logistics |

| Other End-User Industries |

| By Mode of Payment Acceptance | Contact-based |

| Contactless | |

| By POS Type | Fixed Point-of-Sale Systems |

| Mobile and Portable Point-of-Sale Systems | |

| By End-User Industry | Retail |

| Hospitality | |

| Healthcare | |

| Transportation and Logistics | |

| Other End-User Industries |

Key Questions Answered in the Report

How big is the Brazil POS terminal market today?

It stood at USD 6.84 billion in 2026 and is projected to reach USD 9.16 billion by 2031.

Which payment method drives most terminal upgrades in Brazil?

Contactless acceptance, now covering 65.89% of in-person payments, leads upgrade demand thanks to EMV tap cards and Pix by Proximity.

What segment is growing fastest within Brazilian POS hardware?

Mobile and portable devices aimed at SMEs are forecast to grow at a 6.54% CAGR through 2031.

Why are healthcare providers adopting new POS devices quickly?

Data-privacy rules and the rise of telemedicine push clinics to formalize digital payments, giving healthcare a projected 7.27% CAGR.

How are acquirers mitigating margin pressure from zero-fee Pix?

They bundle POS hardware with AI-driven working-capital loans and analytics, shifting revenue toward financial services rather than MDR.

Page last updated on: