Kuwait Fisheries And Aquaculture Market Analysis by Mordor Intelligence

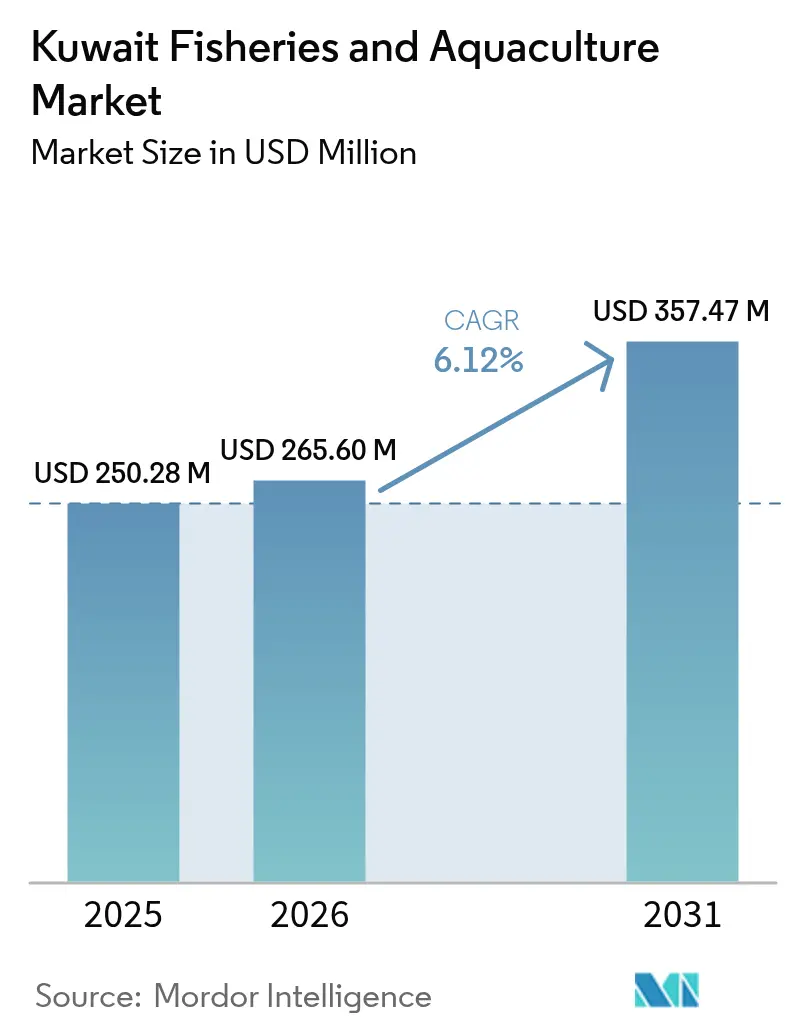

The Kuwait fisheries and aquaculture market size was valued at USD 250.28 million in 2025 and estimated to grow from USD 265.6 million in 2026 to reach USD 357.47 million by 2031, at a CAGR of 6.12% during the forecast period (2026-2031). This steady rise reflects a national policy shift from import dependence toward homegrown output, underpinned by state-funded hatchery construction, liberalized broodstock rules, and the early commercial success of recirculating aquaculture systems that function reliably in desert conditions. Consumption growth is a second pillar, as younger Kuwaitis replace red meat with protein-rich seafood while processors roll out convenient, value-added formats that lift margins. Capital deployment is also tilting toward land-based and offshore projects because coastal cage farms face risks related to temperature, salinity, and brine discharge that constrain their expansion. Finally, cross-border corridors enabled by the Gulf Cooperation Council’s food-security program are channeling technology and investment into Kuwait, accelerating farm mechanization, genetics upgrades, and Internet of Things (IoT)-enabled water-quality controls.

Key Report Takeaways

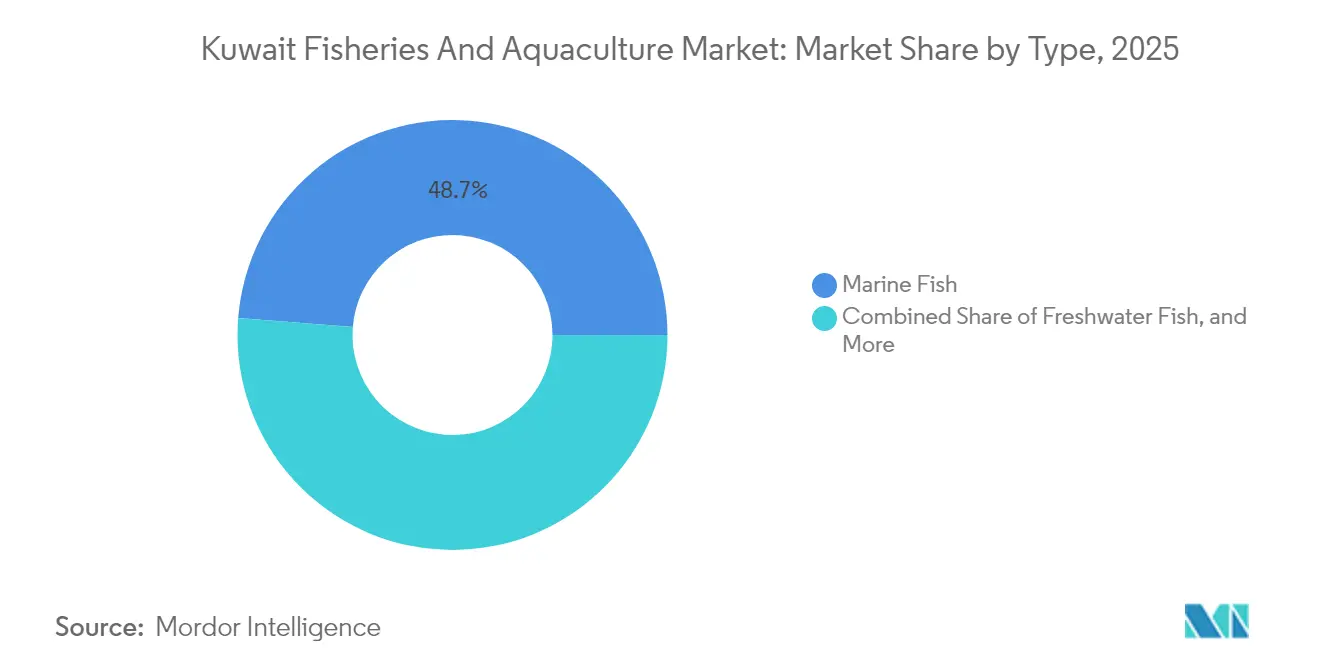

- By type, marine fishes held 48.74% of the Kuwait fisheries and aquaculture market share in 2025. Freshwater fishes are forecast to expand at a 8.95% CAGR from 2026 to 2031, the fastest rate among all segments in the Kuwait fisheries and aquaculture market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kuwait Fisheries And Aquaculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust government investment in inland hatchery expansion | +1.2% | National, with early gains in coastal governorates | Medium term (2-4 years) |

| Rising per-capita seafood intake among Kuwaitis | +0.9% | National | Long term (≥ 4 years) |

| Liberalized import policy for broodstock and feed inputs | +0.8% | National, spill-over to GCC trade corridors | Short term (≤ 2 years) |

| Shift from capture to aquaculture to lower import dependency | +1.3% | National | Medium term (2-4 years) |

| Adoption of bio-floc and RAS technologies in desert aquaculture | +1.5% | National, concentrated in inland zones | Medium term (2-4 years) |

| State-backed offshore mariculture projects | +0.8% | Coastal zones, potential northern offshore sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Government Investment in Inland Hatchery Expansion

Kuwait’s Public Authority for Agriculture Affairs and Fish Resources is channeling capital into inland hatcheries that can produce seed year-round, independent of coastal salinity swings. USD 347 million investment made earlier in Saudi Arabia, now delivering commercial shrimp output, serves as a regional benchmark that underscores the potential payoff from similar programs in Kuwait. Peer-reviewed trials have demonstrated that bio-floc tanks filled with local groundwater can sustain high Nile tilapia survival rates, providing evidence that desert hatcheries can operate profitably without relying on imported water. Shorter growth cycles, 20 to 30 days less than conventional pond schedules, allow operators to harvest extra cohorts each year, boosting fixed-asset returns. Genetics partnerships with overseas breeders are also in place, targeting families that tolerate Kuwait’s high-salinity aquifers and elevated summer temperatures.

Rising Per-Capita Seafood Intake Among Kuwaitis

The average seafood consumption in Gulf Cooperation Council nations was 14.4 kg per capita in 2024, and Kuwait is trending upward as urban professionals opt for protein-dense seafood dishes[1]Source: Food and Agriculture Organization of the United Nations, “Kuwait | Family Farming Knowledge Platform,” FAO.ORG. Public-health drives now position fish as the preferred alternative to red meat in school cafeterias and hospital menus, generating predictable offtake agreements that de-risk producer cash flow. Ready-to-cook fillets, marinated portions, and frozen meal kits are expanding shelf space in hypermarkets, supporting margin growth beyond commodity whole-fish sales. Because import-route disruptions through the Red Sea continue to inflate landed costs, locally farmed products enjoy freshness advantages and lower cold-chain losses, widening the price-value gap in favor of domestic supply. As dietary diversification accelerates, the Kuwait fisheries and aquaculture market gains a structural demand floor that emboldens investors and lenders.

Liberalized Import Policy for Broodstock and Feed Inputs

Customs clearance for certified broodstock and specialty feed ingredients has been simplified, and tariffs have been reduced in line with broader GCC trade facilitation goals [2]Source: World Economic Forum, “The GCC is increasing food security through innovation,” WEFORUM.ORG. A February 2024 agreement with Ukraine opened a new lane for frozen finfish and potential live broodstock, diversifying Kuwait’s sourcing mix beyond traditional Asian suppliers. The Organisation for Economic Co-operation and Development, and the Food and Agriculture Organization of the United Nations (OECD-FAO) outlook forecasts a decline in the real price of fishmeal by 2030, which is projected to alleviate variable costs for Kuwait’s shrimp and marine-fish farmers, who currently import up to 80% of their feed [3]Source: OECD and FAO, “OECD-FAO Agricultural Outlook 2024-2033,” OECD.ORG. Access to niche formulations designed for hypersaline water further sharpens feed conversion and reduces nitrogen discharge. Smaller and mid-sized farms, once hampered by limited bargaining power, now leverage streamlined logistics, which lower unit costs and enable faster scale-up.

Shift from Capture to Aquaculture to Lower Import-Dependency

Wild capture landings have flattened due to stock stress and an aging artisanal fleet, compelling capital reallocation toward controlled-environment farming. Aquaculture allows Kuwait to domestically supply premium seabream, kingfish, and white shrimp that otherwise arrive frozen from Asia or Europe. A seasonality study shows November-to-March landings account for most finfish catch, leaving a summer deficit that land-based systems can fill consistently. The World Bank’s AquaInvest platform demonstrates that, once externalities are priced in, aquaculture generates higher wealth per tonne than capture fisheries, strengthening the rationale for subsidy shifts. Shipping disruptions in the Red Sea during 2024 magnified these strategic vulnerabilities, accelerating government and private timetables for new onshore ponds and offshore cages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extreme seawater temperature and salinity swings | -0.7% | Coastal zones, northern offshore sites | Short term (≤ 2 years) |

| Declining artisanal fisheries labor force | -0.5% | National, concentrated in coastal communities | Long term (≥ 4 years) |

| Stringent brine-discharge rules near desalination outfalls | -0.6% | Coastal zones adjacent to desalination plants | Medium term (2-4 years) |

| Limited genetic diversity of local broodstock lines | -0.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Extreme Seawater Temperature and Salinity Swings

Summer surface readings can exceed 35 °C, and salinity may spike beyond 45 ppt near desalination outfalls, conditions that depress feed intake by up to 30% and elevate cortisol levels in marine finfish. Elevated turbidity and nutrient loading during warm months further tax immune systems, forcing farms to harvest early or invest in shade nets, subsurface cages, and mechanical aeration, all of which raise capital expenditures (capex) by 15-20%. Climate models project that heat extremes will intensify, making site selection, depth refuges, and energy-efficient cooling essential design criteria for future marine cages.

Declining Artisanal Fisheries Labor Force

An aging skipper cohort and the career preferences of younger Kuwaitis have shrunk the artisanal fleet, reducing the capture sector’s ability to exploit seasonal pelagic booms, especially for kingfish and mackerel. The labor shortfall also disrupts shore-based processing schedules, increasing reliance on imports and eroding economies of scale. Although land-based Recirculating Aquaculture System (RAS) farms require fewer workers, they demand higher technical skills, which adds training costs that deter small entrepreneurs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Freshwater Fishes Lead Growth Trajectory

Marine fish, despite holding 48.74% of the Kuwait fisheries and aquaculture market share in 2025, face mixed dynamics. Wild landings of pelagic species, such as kingfish and mackerel, remain seasonally concentrated, leaving processors with raw material shortfalls each summer that they increasingly cover with imports. Offshore cage pilots targeting seabream, hamour, and kingfish now test deeper, cooler waters to stretch the production window, yet capex remains high because of robust mooring systems and disease-monitoring gear. Nonetheless, premium pricing for locally farmed marine fish in hotel and food-service outlets incentivizes private investment. Crustaceans, led by white shrimp, represent the next frontier. Inland pond trials indicate that Kuwait can leverage brackish aquifers and avoid costly seawater pumping; however, success hinges on a pathogen-free post-larvae supply, reliable aeration, and tight biosecurity checks, all of which add to working-capital needs.

Freshwater fish are forecast to grow at a 8.95% CAGR from 2026 to 2031, the highest rate in the Kuwait fisheries and aquaculture market, as RAS and bio-floc units scale across inland deserts. Tilapia dominates because it thrives in brackish groundwater and commands steady retail demand, making it a reliable cash-flow anchor for new farms. Pilot IoT-enabled RAS projects have cut water use and achieved densities of 30 kg per m³ while maintaining survival, proving that technologically intensive freshwater farming is commercially viable under extreme heat. Operators also value the year-round harvest schedule, which smooths summer supply gaps that plague the capture sector. Feed-conversion improvements, aided by specialized formulations for hypersaline conditions, further widen margins and draw investor attention to this segment within the broader Kuwait fisheries and aquaculture market.

Geography Analysis

Northern coastal governorates host the bulk of capture operations because proximity to Kuwait Bay and offshore pelagic grounds minimizes steaming time and fuel costs. Commercial landings reach a seasonal high between November and March, then decline by 40-50% when surface temperatures exceed 35 °C, forcing processors to either pivot to imports or tap into inland aquaculture harvests. Inland governorates, where brackish groundwater intersects with affordable land parcels, anchor most new RAS and bio-floc projects. Government hatchery grants are explicitly designed to favor these zones, aiming to avoid brine-discharge hotspots and spread employment beyond the shoreline, thereby reinforcing balanced regional development.

Policy alignment within the Gulf Cooperation Council amplifies geographic opportunities for the Kuwaiti fisheries and aquaculture market. The bloc’s USD 30.5 billion food-security blueprint mobilizes USD 3.8 billion for agri-food technology, opening up cross-border funding and technical advisory channels that Kuwaiti farms can tap into to import equipment duty-free and secure concessional loans. Case studies from Saudi Arabia’s 80,000 metric ton NEOM project and the UAE’s 1.1-km² KEZAD zone inform Kuwait’s own site selection and permitting roadmaps, fostering knowledge spillovers and supply chain synergies with neighboring states.

Offshore expansion prospects center on deeper northern waters where stronger currents improve oxygenation and dissipate waste. Bathymetric surveys are under way to map suitable depths and substrata for large-volume cages. Real-time telemetry, as mandated by the Food and Agriculture Organization of the United Nations (FAO) biosecurity guidelines, will feed data into a proposed national disease-response center. While capex remains steep, the promise of cooler, more stable water columns and the absence of land-use conflicts make offshore mariculture a strategic hedge against onshore environmental and regulatory constraints. Together, these coastal, inland, and offshore vectors underpin a diversified production mosaic that positions the Kuwait fisheries and aquaculture market to meet rising domestic demand and to tap niche export opportunities.

Competitive Landscape

Sector structure is best described as moderately fragmented. The government-linked Kuwait Institute for Scientific Research serves as a technology incubator, conducting pilot hatchery genetics, species trials, and remote-sensor analytics to de-risk concepts before they are adopted by the private sector. Established private players, such as Kuwait Aquaculture Company and Gulf Fisheries Company, have staked early claims in marine-cage farming and feed-mill joint ventures, aiming to replicate the 90,000 metric ton scale achieved by Saudi Arabia’s NAQUA, which already exports shrimp to Kuwait. These incumbents are integrating upstream into broodstock and feed to secure critical inputs, and downstream into branded retail lines to capture value.

A second tier of startups is harnessing RAS and bio-floc technologies to produce tilapia and seabream in land-locked governorates. They differentiate through organic certification, traceability apps, and direct-to-consumer subscriptions, appealing to health-conscious urban families. Feed innovators are formulating diets rich in locally sourced protein concentrates that perform well in hypersaline water, trimming reliance on imported fishmeal. Genetics ventures are partnering with Nordic and Thai hatcheries to import pathogen-screened, saline-tolerant broodstock, accelerating performance gains.

Strategically, mergers and acquisitions are gaining traction. Saudi state investor SALIC’s USD 32.62 million stake sale in Saudi Fisheries during 2024 set valuation benchmarks that Kuwait firms use in their own capital-raising pitches. Investors increasingly ask for life-cycle assessments and ESG disclosures, pushing farms to quantify water use, carbon intensity, and effluent profiles. As scale economies favor vertically integrated models, joint ventures between Kuwaiti producers and GCC logistics or retail players are likely to proliferate, tightening the competitive landscape while delivering larger product volumes and more reliable supply to domestic consumers.

Recent Industry Developments

- February 2025: The Gulf Cooperation Council has announced a unified regional food-security strategy targeting USD 30.5 billion in agricultural and fishery output, supported by USD 3.8 billion in food-technology investment. This strategy aims to create cross-border partnerships and technology-transfer corridors that Kuwait operators can leverage for scaling aquaculture infrastructure and accessing regional funding mechanisms.

- November 2024: The World Bank published a procurement plan for the Program on Sustainable Fishery Development in the Red Sea and Gulf of Aden, a regional initiative that may provide technical assistance and capacity-building opportunities for Kuwait's fisheries sector, particularly in stock assessment, ecosystem-based management, and regional cooperation frameworks.

- December 2023: EnerTech Holding Company and Aqua Bridge Group unveiled their joint venture at COP28, aiming to decarbonize Kuwait's food supply chains. This initiative aims to lessen Kuwait's dependence on imports and strengthen its aquaculture and fisheries industries. These efforts align with the state's national food security goals, emphasizing the creation of a resilient and sustainable agri-food system capable of withstanding global economic shocks and disruptions.

Kuwait Fisheries And Aquaculture Market Report Scope

Aquaculture is aqua farming of fish, crustaceans, mollusks, aquatic plants, algae, and other organisms. It is the breeding, rearing, and harvesting fish, shellfish, algae, and other organisms in all water environments. The Kuwaiti fisheries and aquaculture market is segmented by type into freshwater fishes and marine fishes. The report includes production (volume), consumption (volume and value), import (volume and value), export (volume and value), and price trend analysis. The report offers market estimation and forecasts in value (USD) and volume (metric tons) for the above segments.

By Type

| Freshwater Fishes | |

| Diadromous Fishes | |

| Crustaceans | Shrimp |

| Marine Fishes | Pelagic Fish |

| Tuna | |

| Other Marine Fishes |

| By Type | Freshwater Fishes | |

| Diadromous Fishes | ||

| Crustaceans | Shrimp | |

| Marine Fishes | Pelagic Fish | |

| Tuna | ||

| Other Marine Fishes | ||

Key Questions Answered in the Report

What is the current value of the Kuwait fisheries and aquaculture market?

The Kuwait fisheries and aquaculture market size is USD 265.6 million in 2026.

How fast is the sector projected to grow by 2031?

Market value is projected to reach USD 357.47 million by 2031, implying a CAGR of 6.12%.

Which product segment shows the strongest growth momentum?

Freshwater fishes, led by tilapia cultured in RAS and bio-floc systems, are forecast to grow at a 8.95% CAGR.

What share of the market do marine fishes currently hold?

Marine fishes accounted for 48.74% of Kuwait fisheries and aquaculture market share in 2025.

How are rising temperatures affecting marine cage farms?

Summer surface temperatures above 35 °C suppress feed intake and require costly cooling or deeper cage deployment to maintain survival.

Which policy change most influences future investment?

Kuwait's 2024 ratification of the World Trade Organization (WTO) Agreement on Fisheries Subsidies redirects state support toward sustainable aquaculture infrastructure, bolstering private project viability.

Page last updated on: