Cancer Monoclonal Antibodies Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

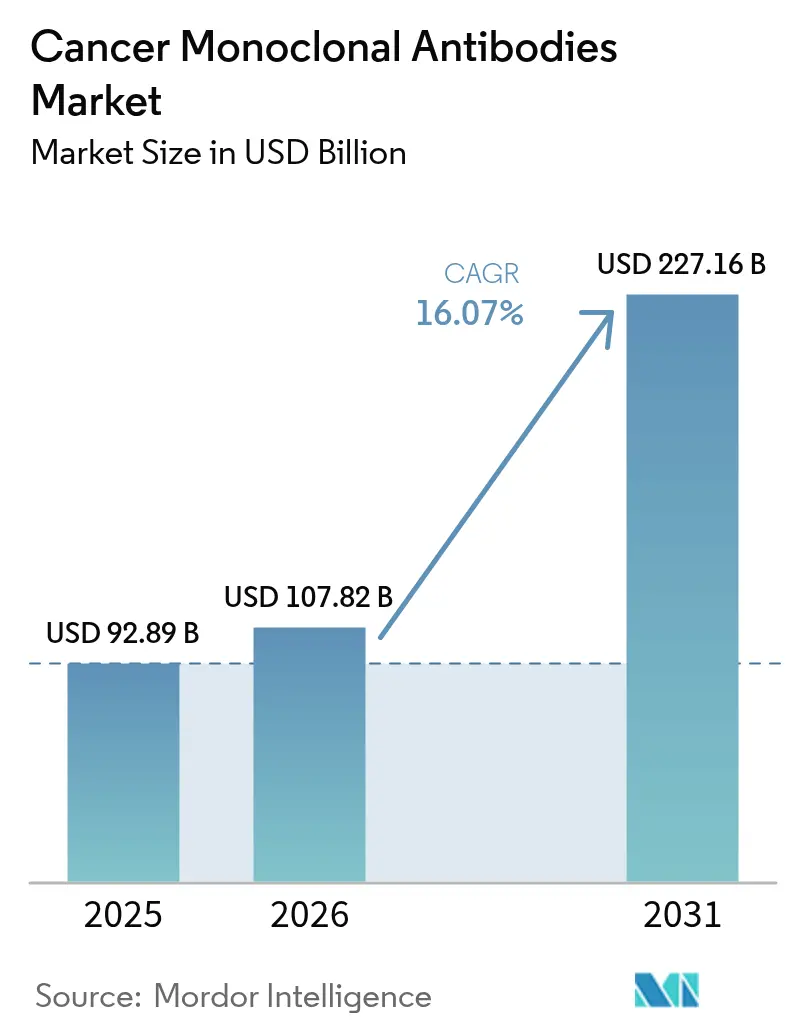

| Market Size (2026) | USD 107.82 Billion |

| Market Size (2031) | USD 227.16 Billion |

| Growth Rate (2026 - 2031) | 16.07% CAGR |

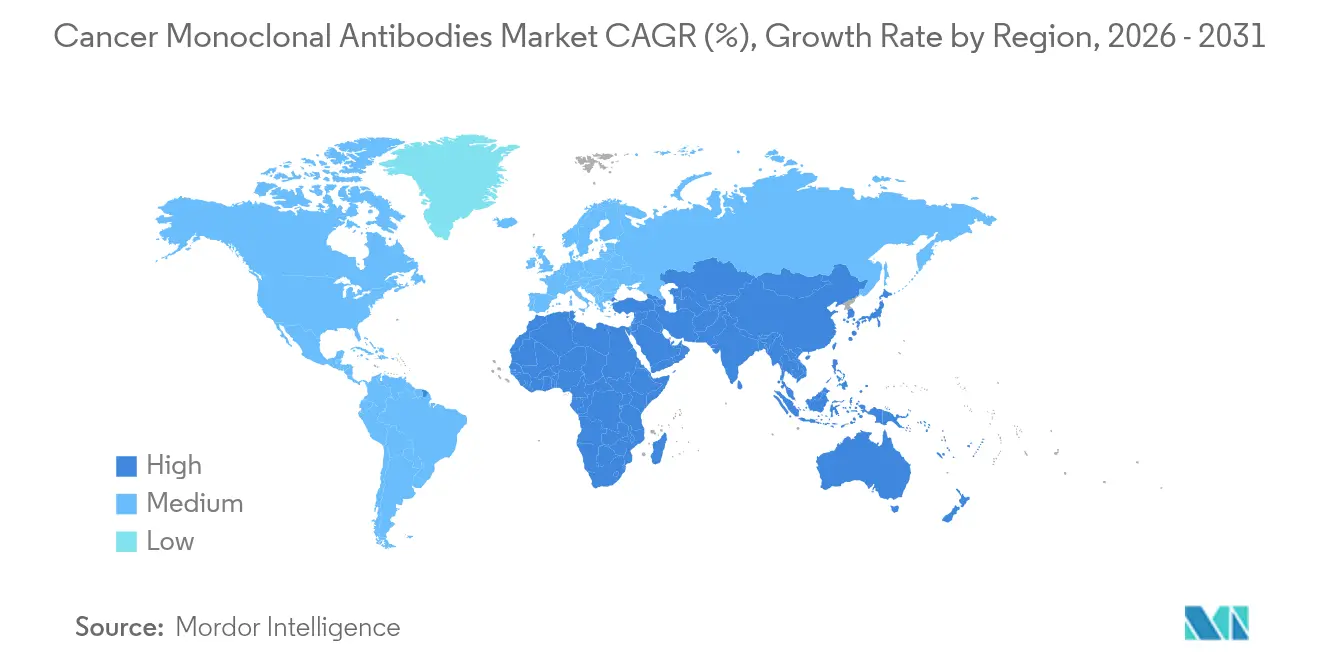

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cancer Monoclonal Antibodies Market Analysis by Mordor Intelligence

The Cancer Monoclonal Antibodies market size is expected to grow from USD 92.89 billion in 2025 to USD 107.82 billion in 2026 and is forecast to reach USD 227.16 billion by 2031 at 16.07% CAGR over 2026-2031.

Rapid gains stem from artificial-intelligence-enabled antibody design, a faster regulatory path for bispecific antibodies, and wider adoption of antibody-drug conjugates that together expand therapeutic breadth and boost revenue visibility. Capacity expansions by contract manufacturers, the shift toward value-based oncology care, and breakthrough clinical data from Chinese biotechnology firms further reshape competitive dynamics while keeping pipeline productivity high. Headline risks include bioreactor bottlenecks, stringent safety monitoring, and competition from CAR-T and gene-editing modalities, yet companies that integrate AI-driven engineering and flexible manufacturing retain strategic advantage.

Key Report Takeaways

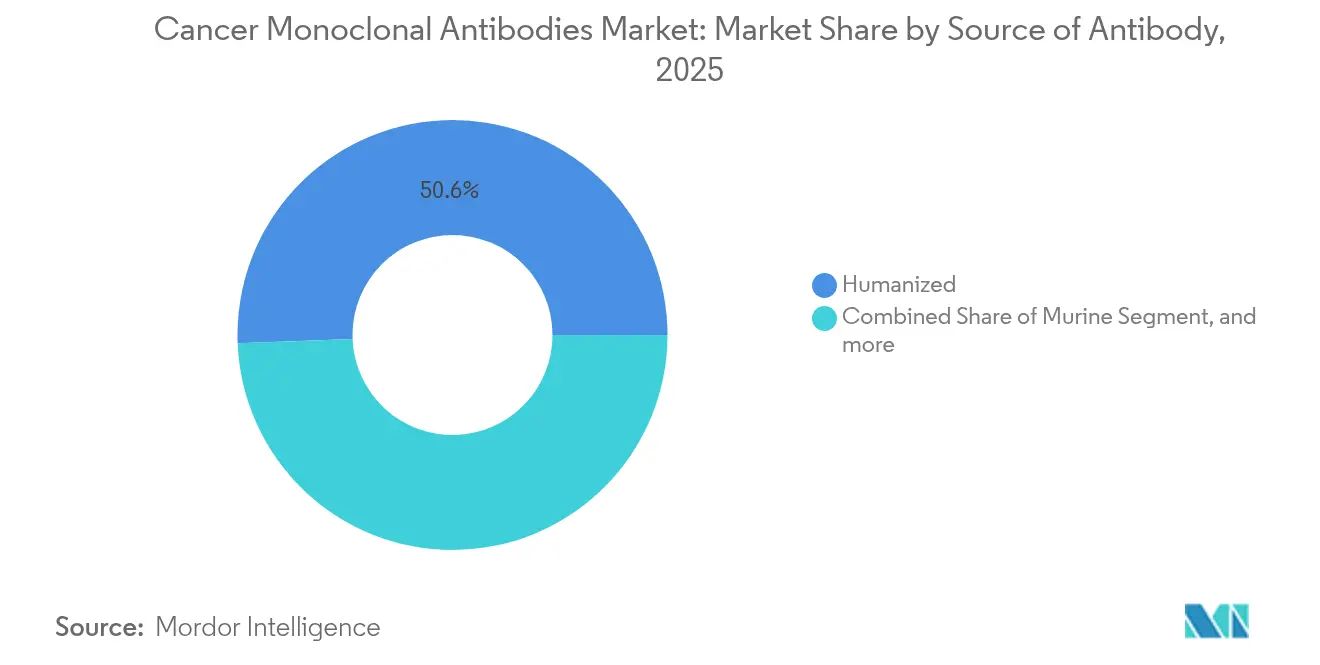

- By source of antibody, humanized antibodies led with 50.62% of cancer monoclonal antibodies market share in 2025, while fully-human antibodies post the fastest 18.59% CAGR through 2031.

- By therapy, trastuzumab commanded 16.72% share of the cancer monoclonal antibodies market size in 2025; the “Others” category grows at a 20.61% CAGR between 2026-2031.

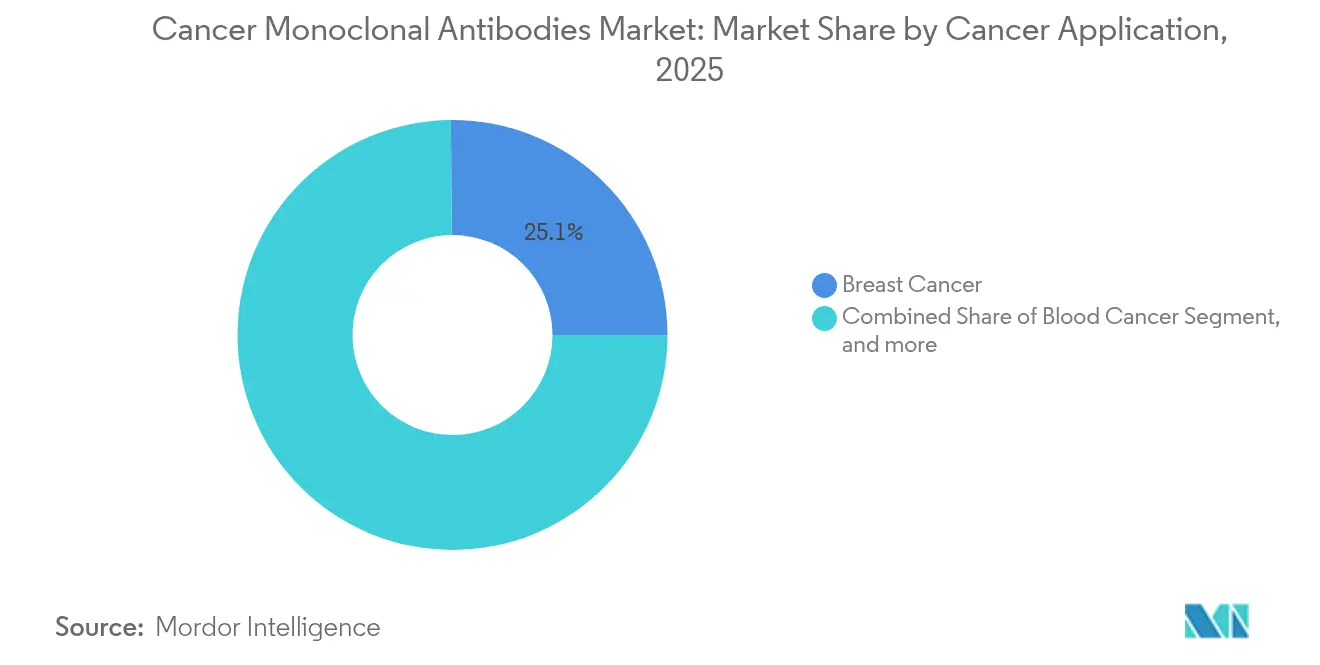

- By application, breast cancer held 25.12% share of the cancer monoclonal antibodies market size in 2025, whereas liver and gastrointestinal cancers advance at 16.41% CAGR to 2031.

- By distribution channel, hospital pharmacies controlled 52.24% revenue in 2025, and online pharmacies record the highest 17.95% CAGR to 2031.

- By geography, North America retained 41.78% cancer monoclonal antibodies market share in 2025, while Asia-Pacific expands the quickest at 18.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cancer Monoclonal Antibodies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global cancer incidence | +3.2% | Global with highest pull in Asia-Pacific | Long term (≥ 4 years) |

| Increasing allocation to oncology R&D | +2.8% | North America & EU; spill-over to Asia-Pacific | Medium term (2–4 years) |

| Proven clinical success of humanized and fully-human mAbs | +2.1% | Global, early use in developed markets | Short term (≤ 2 years) |

| Emergence of bispecific antibodies and ADCs | +4.3% | Global, China leads trials | Medium term (2–4 years) |

| Adoption of AI-driven antibody engineering | +1.9% | North America & EU, expanding in Asia-Pacific | Long term (≥ 4 years) |

| Shift toward value-based oncology models | +1.3% | North America & EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Global Cancer Incidence

Cancer incidence climbs from 20 million cases in 2022 to a projected 35 million in 2050, a 77% jump that expands patient pools across lung, breast, and colorectal cancers.[1]American Cancer Society Staff, “Cancer Facts & Figures 2025,” American Cancer Society, cancer.org Aging populations in developed regions and lifestyle changes in emerging economies intensify demand for targeted biologics. The cancer monoclonal antibodies market benefits as monoclonal antibodies deliver tumor-specific action that aligns with precision oncology protocols. Low- and middle-income countries witness the fastest case growth, creating access challenges yet opening underserved markets for cost-optimized biosimilars. This demographic surge sustains top-line growth well beyond current forecast windows.

Increasing Allocation to Oncology R&D

Oncology commands the highest share of biopharmaceutical R&D budgets, and 35% of oncology trials now involve antibody-drug conjugates or multispecific constructs. Improved development productivity and blockbuster acquisitions, Bristol Myers Squibb’s USD 5.8 billion Mirati buyout, Eli Lilly’s USD 1.4 billion Point Biopharma deal strengthen late-stage pipelines. Capital flows foster robust partnership activity that injects technical know-how and de-risks innovation, allowing the cancer monoclonal antibodies market to secure continual first-in-class launches.

Proven Clinical Success of Humanized and Fully-Human mAbs

Regulators cleared 25 new oncology biologics in 2024, many built on humanized or fully-human formats that lower immunogenicity.[2]United States Food and Drug Administration, “Oncology Approvals 2024,” FDA, fda.gov Subcutaneous dosing trims chair time to under five minutes, improving patient adherence and freeing infusion capacity. Broadening indications, such as penpulimab-kcqx in nasopharyngeal carcinoma, add new revenue streams. Robust biosimilar uptake saved payers USD 7 billion in 2023, proving therapeutic value and driving volume expansion that compensates for price erosion.

Emergence of Bispecific Antibodies and Antibody-Drug Conjugates

Fourteen bispecific antibodies had secured global approval by end-2023 and together with marketed ADCs may top USD 26 billion revenue by 2028. Partnerships such as BioNTech and Bristol Myers Squibb’s USD 1.5 billion collaboration on BNT327 highlight strong capital commitment.[3]Bristol Myers Squibb Communications, “BNT327 Collaboration Announcement,” bms.com Complex manufacturing raises entry barriers and protects innovators yet propels contract manufacturing demand, a structural tailwind for supply-side specialists.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory and safety monitoring | -2.1% | Global, strongest in developed markets | Short term (≤ 2 years) |

| High clinical attrition and long cycles | -1.8% | Global, burdens smaller firms | Long term (≥ 4 years) |

| Manufacturing bottlenecks in bioreactors and raw materials | -2.3% | Global, acute for Asia-Pacific build-out | Medium term (2–4 years) |

| Growing competition from advanced modalities | -1.4% | North America & EU, extending worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Safety Monitoring

Agencies demand integrated safety data for bispecifics and ADCs, adding pediatric study rules and comparative-effectiveness reviews that stretch timelines and cost outlays. European joint clinical assessments further raise evidence thresholds. Small companies face resource gaps, nudging them into licensing deals or M&A with larger players that possess the regulatory infrastructure.

Manufacturing Bottlenecks in Bioreactor and Raw Material Supply

Global bioreactor volume hit 17.4 million L in 2024, yet demand growth still outruns capacity. Shortages of cell-culture media and single-use bags drive lead-time inflation. Samsung Biologics, Fujifilm Diosynth, and Lonza announced multi-billion-dollar expansions, but new plants need three to five years to reach commercial output. The imbalance elevates contract manufacturing costs and can delay product launches, especially for firms without secured slots.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source of Antibody: Humanized Dominance Faces Fully-Human Disruption

Humanized antibodies delivered 50.62% of 2025 revenue, underscoring their heritage in blockbuster oncology regimens. The cancer monoclonal antibodies market now witnesses accelerated uptake of fully-human antibodies, which post a 18.59% CAGR through 2031 on the back of superior safety and rising use in combination protocols. Manufacturing process simplicity and favorable regulatory profiles position fully-human constructs to migrate from niche to mainstream over the forecast period.

Pipeline platforms leverage transgenic mice and phage display to generate diversified fully-human candidates that tackle traditionally hard targets. Lower immunogenicity cuts retreatment risk and improves quality-of-life scores. As costs fall, payers gain comfort funding earlier-line use, reinforcing trajectory. Murine and chimeric formats lose ground except in specialized settings where rapid clearance confers benefit. Firms pivoting rapidly to fully-human candidates are likely to outpace rivals in the cancer monoclonal antibodies market.

By Monoclonal Antibody Therapy: Trastuzumab Leadership Challenged by Innovation Pipeline

Trastuzumab held 16.72% of cancer monoclonal antibodies market share in 2025 owing to deep physician familiarity and robust evidence in HER2-positive breast cancer. However, an innovation wave centered on ADCs and bispecifics fuels the “Others” bucket, which grows 20.61% annually. New approvals, such as trastuzumab deruxtecan for HER2-low disease, extend benefit to broader patient subsets. Epcoritamab-bysp posted an 82% response rate in follicular lymphoma, proving bispecific potency and drawing attention away from older single-target constructs.

Strategic layering of antibodies with checkpoint inhibitors or small molecules enhances depth of response, widening the revenue base for next-generation agents. Biosimilar erosion trims trastuzumab value but drives volume, cushioning segment revenue. The end result is a diversified therapy mix in which novel mechanisms progressively tilt market share yet established brands conserve relevance through life-cycle management.

By Cancer Application: Breast Cancer Dominance Meets Liver & GI Acceleration

Breast cancer generated 25.12% of the 2025 cancer monoclonal antibodies market size due to entrenched HER2-targeted regimens and growing adoption in hormone-receptor-positive settings. Liver and gastrointestinal cancers, while smaller, register a 16.41% CAGR through 2031 as emerging targets such as TROP2 and EGFR variants move into late-stage trials. High prevalence in Asia and Latin America propels the addressable population, making these malignancies prime expansion niches.

Blood cancers maintain healthy contribution through bispecific T-cell engagers that match CAR-T efficacy yet offer outpatient dosing convenience. Lung cancer therapies evolve via checkpoint-antibody combinations that extend progression-free survival. Together, these shifts dilute single-tumor dependency and spread revenue risk across multiple disease sites.

By Distribution Channel: Hospital Pharmacies Lead While Online Channels Surge

Hospital pharmacies accounted for 52.24% of 2025 worldwide sales since many monoclonal antibodies still require supervised infusion. Subcutaneous formulations, however, catalyze 17.95% CAGR in online pharmacy turnover as patients embrace self-administration. Specialty retail programs extend cold-chain reach, while insurers reimburse home-based care to curb facility overheads. As digital prescription platforms mature, payers and providers collaborate on remote monitoring tools that safeguard safety without forcing hospital visits.

Hospitals respond by bundling infusion services with genomic testing and real-time outcome tracking, reinforcing their central role in complex oncology regimens. The dual-channel model enlarges overall access, especially in geographies where clinic density lags patient demand, thereby sustaining cancer monoclonal antibodies market expansion.

Geography Analysis

North America maintains first place with 41.78% of global revenue in 2025, helped by robust clinical-trial ecosystems and favorable payer policies. Real-world evidence requirements gain traction, prompting life-science firms to set up longitudinal patient registries that support value-based contracts. Subcutaneous pembrolizumab approval exemplifies the region’s push for patient-centric dosing that trims facility burden and supports tele-oncology rollouts.

Asia-Pacific records the fastest growth at 18.92% CAGR to 2031, reflecting bigger oncology budgets, demographic aging, and regulator-backed accelerated pathways. China’s Akeso produced ivonescimab, which outperformed Keytruda in time-to-progression, strengthening domestic confidence and luring capital into local antibody platforms cnn.com. Commercial health insurance penetration widens affordability, while public-private partnerships finance biomanufacturing parks near major urban centers.

Europe pursues balanced access through joint clinical assessments that streamline approvals yet guard budgets. Conditional marketing authorizations for breakthrough antibodies, including linvoseltamab, showcase agility in addressing high unmet need. High biosimilar uptake pressures prices, but volume increases maintain therapy availability and free funds for next-generation constructs.

Middle East & Africa and South America add incremental upside as governments prioritize oncology in universal-health-coverage blueprints. Foreign direct investment flows into fill-and-finish plants that shorten import cycles. Flexible pricing and patient-assistance programs mitigate affordability barriers, expanding therapy reach without compromising fiscal prudence. Collectively, these moves broaden the geographic footprint of the cancer monoclonal antibodies market.

Competitive Landscape

The cancer monoclonal antibodies market shows moderate consolidation. Top Western firms still command large portfolios, yet rising Asian biotechnology companies disrupt with competitive clinical data and lower development costs. Overall, contract manufacturing penetration and high discovery complexity erect entry barriers that partially offset fragmentation pressure.

Strategic M&A and licensing dominate growth plays. Pfizer sealed a USD 1.25 billion global deal with 3SBio for a PD-1/VEGF bispecific, demonstrating appetite for external innovation pfizer.com. BioNTech and Bristol Myers Squibb committed USD 1.5 billion upfront to co-develop BNT327, boosting multispecific capabilities. Large players integrate AI tools, invest in continuous bioprocessing, and roll out patient-support ecosystems that improve adherence and differentiate service quality.

Chinese firms like Akeso leverage government grants, fast-track reviews, and deep local patient pools to deliver pivotal data quicker and at lower cost. Ivonescimab’s trial success against Keytruda expands their bargaining power in global partnerships. Western incumbents respond by establishing joint ventures and research hubs within China to capture local insight and preserve share.

Cancer Monoclonal Antibodies Industry Leaders

Amgen Inc

Eli Lilly and Company

F. Hoffmann-La Roche Ltd (Genentech Inc)

Merck & Co., Inc

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BioNTech and Bristol Myers Squibb announced a global strategic partnership to co-develop BNT327, a bispecific antibody targeting PD-L1 and VEGF-A, with USD 1.5 billion upfront payment and potential milestone payments totaling USD 7.6 billion. The collaboration aims to accelerate regulatory approval and market launch for multiple solid tumor indications

- June 2025: Roche reported positive Phase III IMforte study results showing Tecentriq combined with lurbinectedin significantly improved survival in extensive-stage small cell lung cancer, reducing disease progression risk by 46% and death risk by 27% compared to Tecentriq.

- May 2025: Pfizer entered an exclusive global licensing agreement with 3SBio for SSGJ-707, a bispecific antibody targeting PD-1 and VEGF, with USD 1.25 billion upfront payment and potential milestone payments up to USD 4.8 billion for non-small cell lung cancer and other solid tumors.

- April 2025: FDA approved penpulimab-kcqx for non-keratinizing nasopharyngeal carcinoma, demonstrating median progression-free survival of 9.6 months for combination therapy and receiving fast track, breakthrough, and orphan drug designations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the cancer monoclonal antibodies (mAbs) market as all prescription-grade antibody molecules whose primary, regulator-approved indication is the diagnosis or treatment of solid tumors or hematologic malignancies, regardless of source class or mode of action. According to Mordor Intelligence, values reflect ex-factory revenues earned from first-line through salvage settings across hospital, retail, and digital pharmacy channels.

Scope exclusion: supportive biologics used only for anemia, neutropenia, or autoimmune disorders are outside this assessment.

Segmentation Overview

- By Source of Antibody

- Murine

- Chimeric

- Humanized

- Fully-Human

- By Monoclonal Antibody Therapy

- Bevacizumab

- Trastuzumab

- Rituximab

- Cetuximab

- Daratumumab

- Others

- By Cancer Application

- Breast Cancer

- Blood Cancer

- Colorectal Cancer

- Lung Cancer

- Liver & GI Cancer

- Other Solid Tumour

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with oncologists, hospital pharmacists, payers, and regional distributors spanning North America, Europe, Asia-Pacific, and Latin America. Insights covered line-of-therapy mix shifts, off-label use, tender prices, and real-world penetration of biosimilars, allowing us to validate desk-driven ratios and refine forecast inflection points.

Desk Research

We began by mapping the disease burden using open datasets such as WHO GLOBOCAN, CDC SEER incidence tables, and OECD Health Stats, which anchor patient pools and diagnostic uptake. Approval pipelines, label extensions, and trial attrition rates were traced through the US FDA Biologics License Application portal, EMA's EPAR, and ClinicalTrials.gov. Financial clues around dosing volume and average selling price (ASP) were extracted from company 10-Ks, investor decks, and, for cross-checks, D&B Hoovers and Dow Jones Factiva snapshots. Patent life and biosimilar entry windows were screened through Questel. These sources are illustrative; many additional feeds informed our desk work.

Market-Sizing & Forecasting

A blended top-down, bottom-up model was built. Starting with incident and prevalent cancer cases, we applied therapy-eligible proportions and mAb penetration rates, which are then multiplied by course intensity and ASP to derive 2025 revenue. Selective supplier roll-ups and channel checks served as reasonableness tests. Key variables include: 1) annual incidence of HER2-positive breast and PD-1-responsive tumors, 2) biosimilar share ramp, 3) median ASP erosion post-patent, 4) treatment duration drift toward shorter cycles, and 5) regional reimbursement coverage scores. Multivariate regression on these drivers, supplemented by scenario analysis for rapid ADC adoption, generated the 2025-2030 trajectory while gap-filled volumes followed peer-weighted averages from primary calls.

Data Validation & Update Cycle

Outputs pass three layers of variance screening, peer review, and senior analyst sign-off. Models refresh every twelve months, with mid-cycle tweaks after material approvals, pricing resets, or reimbursement shocks, so clients always receive the latest vetted baseline.

Why Mordor's Cancer Monoclonal Antibodies Baseline Commands Reliability

Published estimates differ because firms pick dissimilar product baskets, price points, and refresh rhythms; understanding these levers is vital before decisions are taken.

Key gap drivers revolve around whether pipeline assets are monetized early, how aggressively biosimilar erosion is modeled, and the breadth of country coverage adopted. Mordor reports current-market value only for commercialized labels and updates currency and ASP inputs each fiscal year, whereas others may annualize trial drugs or hold static price decks for longer.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 92.89 B (2025) | Mordor Intelligence | - |

| USD 125.10 B (2025) | Regional Consultancy A | Includes pipeline antibodies and assumes flat ASP growth through 2034 |

| USD 86.06 B (2025) | Trade Journal B | Excludes biosimilars and covers only 25 countries |

| USD 48.30 B (2024) | Industry Association C | Older base year and omits hospital-only purchasing in Asia-Pacific |

In sum, the disciplined scoping, annually refreshed variables, and cross-confirmed assumptions applied by Mordor Intelligence yield a balanced, transparent baseline that users can retrace and replicate with confidence.

Key Questions Answered in the Report

What is the current size of the cancer monoclonal antibodies market?

The market reaches USD 107.82 billion in 2026 and is projected to rise to USD 227.16 billion by 2031 at a 16.07% CAGR.

Which geographic region is growing the fastest?

Asia-Pacific posts the highest 18.92% CAGR through 2031, driven by China’s large clinical-trial pipeline and expanding manufacturing capacity.

Which antibody source segment leads, and which is expanding the quickest?

Humanized antibodies hold 50.62% revenue share, while fully-human antibodies grow the fastest at 18.59% CAGR thanks to lower immunogenicity and broader combination use.

What are the top drivers behind market growth?

Key growth factors include rising global cancer incidence, increased oncology R&D budgets, adoption of bispecific antibodies and antibody-drug conjugates, and AI-enabled antibody engineering.

How are distribution channels evolving?

Hospital pharmacies remain dominant with 52.24% share, but online pharmacies record an 17.95% CAGR because subcutaneous formulations support home administration.

What major challenges could slow adoption?

Stringent regulatory reviews, bioreactor and raw-material shortages, and competition from CAR-T and gene-editing therapies can temper the otherwise strong growth trajectory.

Page last updated on: