Antiblock Additive Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

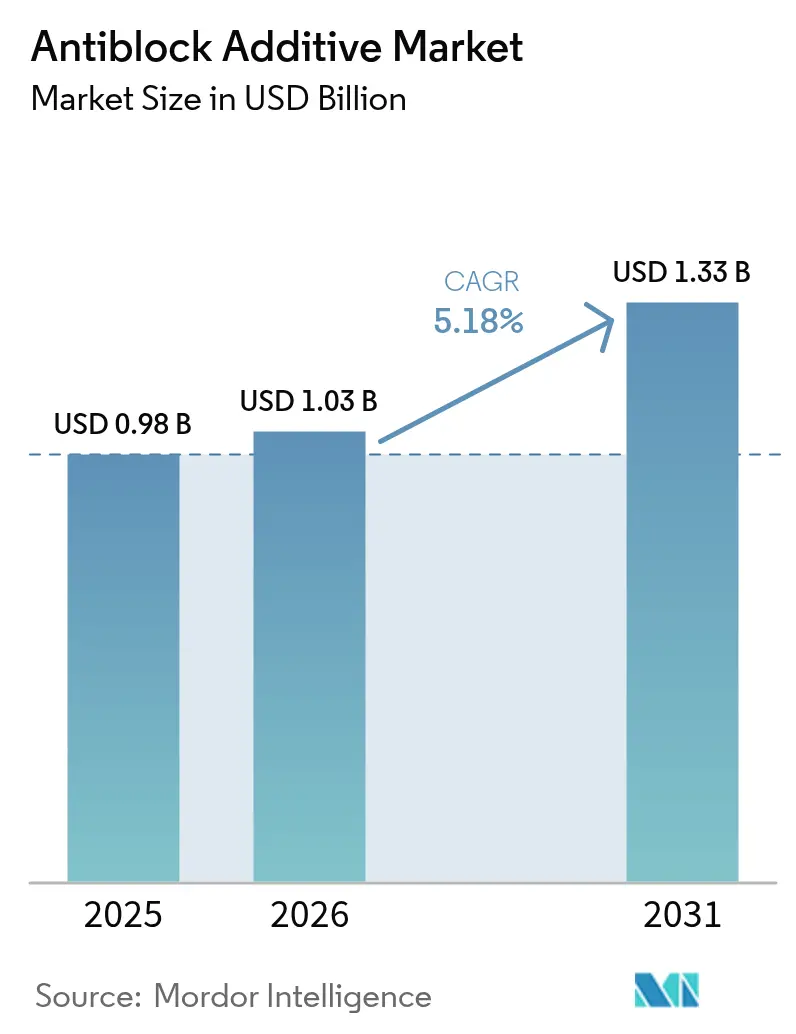

| Market Size (2026) | USD 1.03 Billion |

| Market Size (2031) | USD 1.33 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antiblock Additive Market Analysis by Mordor Intelligence

The Anti-block Additive market size in 2026 is estimated at USD 1.03 billion, growing from 2025 value of USD 0.98 billion with 2031 projections showing USD 1.33 billion, growing at 5.18% CAGR over 2026-2031. Demand strength arises from the expansion of e-commerce packaging, greenhouse agriculture, and mono-material recyclable films, each relies on anti-block technology to prevent film blocking, preserve optical clarity, and maintain line throughput. Brand-owner sustainability targets accelerate the shift from mineral to bio-based chemistries, while regulatory scrutiny of crystalline and amorphous silica puts pressure on traditional inorganic offerings. Meanwhile, Asia-Pacific retains its position as the largest production and consumption base, underpinned by integrated polymer value chains in China and India and supported by multinational investments in specialty chemical plants. Supply-side consolidation around semiconductor-grade silica and sodium-based agents raises input-cost volatility and compels formulators to qualify alternative raw materials that can pass Food and Drug Administration (FDA), European Union (EU), and China GB standards without compromising performance.

Key Report Takeaways

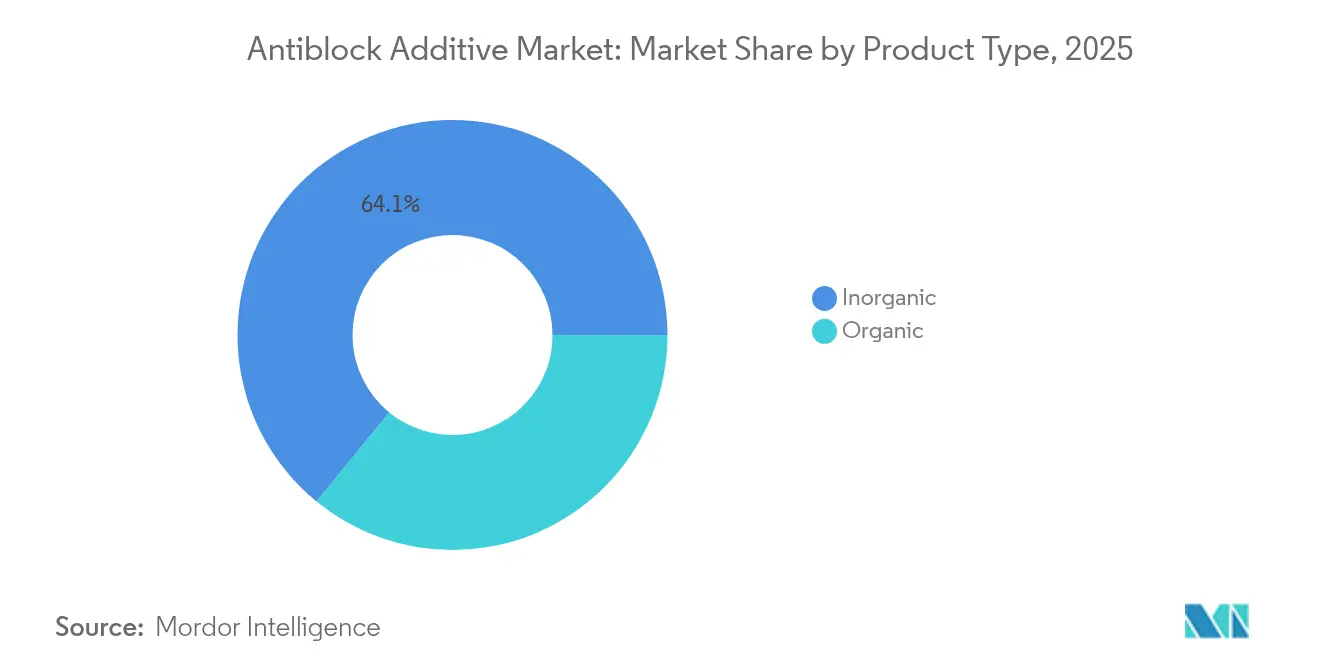

- By product type, inorganic additives led with 64.10% of the Anti-block Additives market share in 2025, while organic formulations are set to advance at a 6.00% CAGR through 2031.

- By polymer type, low-density polyethylene held 38.05% of the Anti-block Additives market size in 2025, whereas biaxially-oriented polypropylene is projected to be the fastest-growing polymer segment at a 6.17% CAGR to 2031.

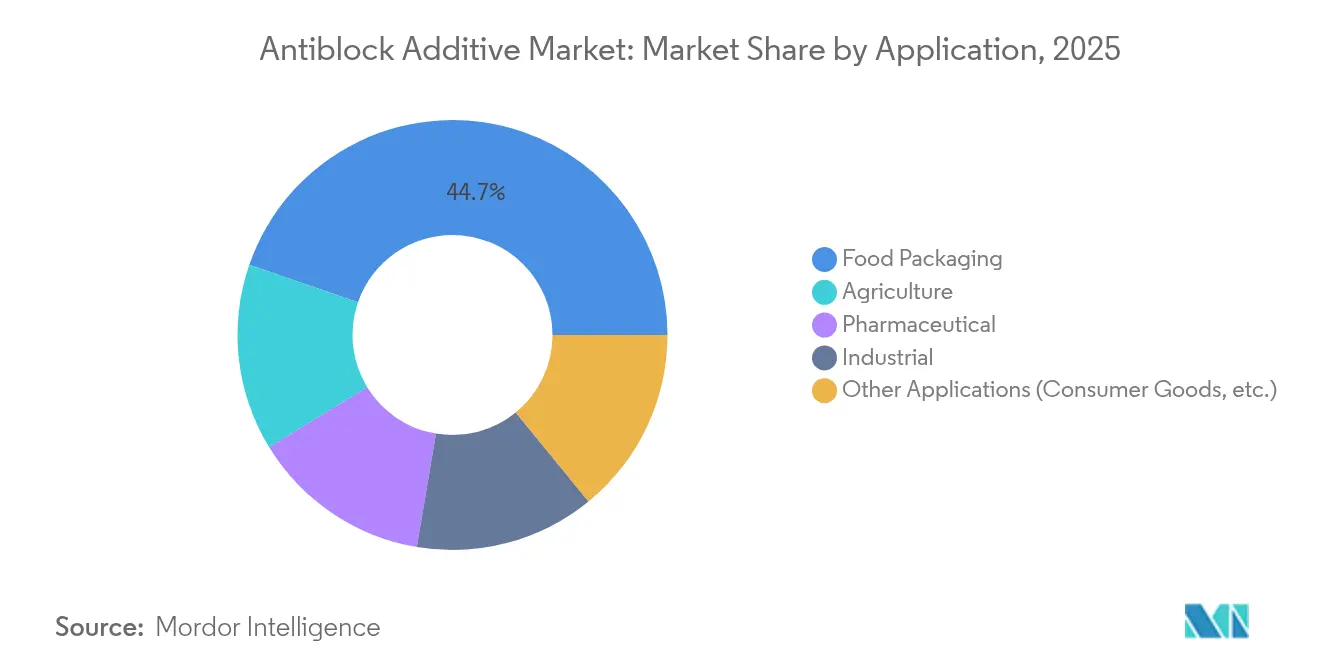

- By application, food packaging accounted for 44.70% revenue share of the Anti-block Additives market size in 2025; agricultural films are expected to expand at a 6.22% CAGR during the same period.

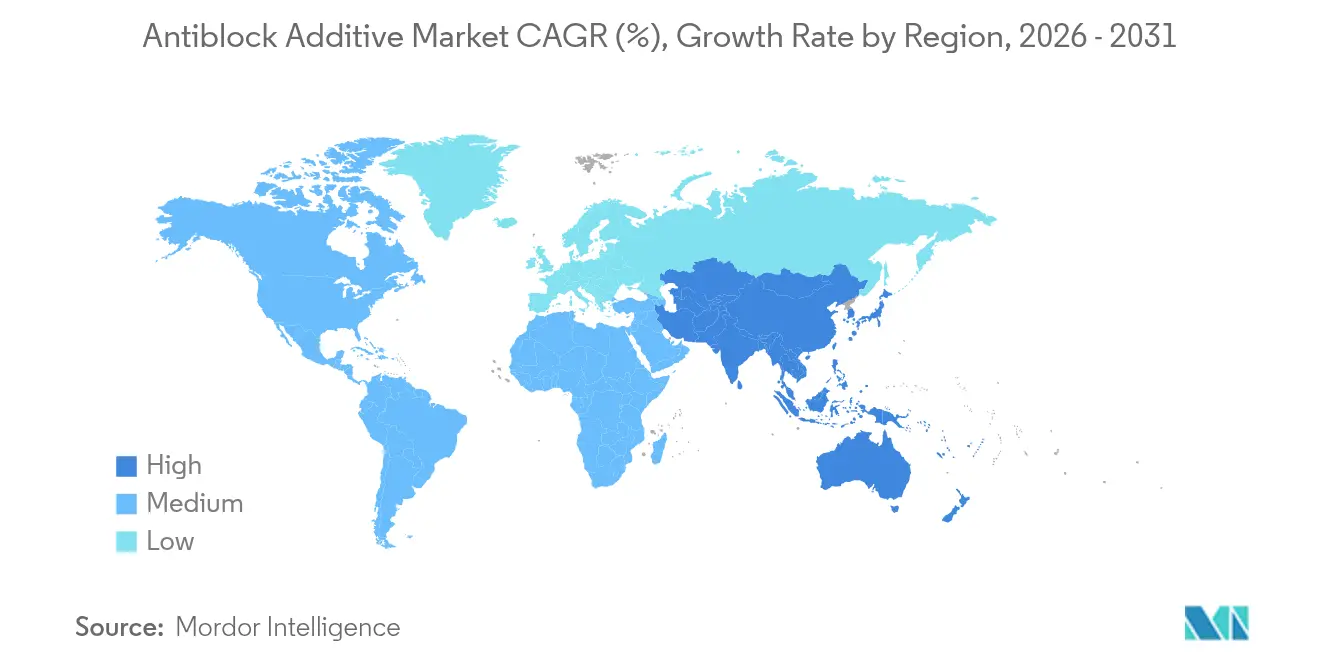

- By geography, Asia-Pacific commanded 30.30% of the Anti-block Additives market share in 2025 and is forecast to grow at a 6.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Antiblock Additive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Flexible and Rigid Food Packaging Film Demand | +1.8% | Global, with concentration in APAC and North America | Medium term (2-4 years) |

| Expansion of Greenhouse and Mulch-film Agriculture | +1.2% | APAC core, spill-over to Europe and North America | Long term (≥ 4 years) |

| Rapid Growth of High-clarity BOPP Lines | +1.0% | Global, led by Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Brand-owner Shift Toward Mono-material Recyclability | +0.9% | Europe and North America, expanding to APAC | Medium term (2-4 years) |

| Expansion of E-commerce Sector Creating Non-sticking Packaging Films Demand | +0.7% | Global, concentrated in urban markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Flexible and Rigid Food Packaging Film Demand

Food manufacturers continue to accelerate flexible and rigid film adoption to support ready-to-eat and portion-controlled product lines. Modern high-speed form-fill-seal equipment requires antiblock agents that keep film layers separate without impairing clarity or sealability; bio-based Optislip grades demonstrate how surface-migration layers reduce blocking at lower loadings [1]Cargill, “Optislip™ Bio-based Additives,” cargill.com. Thinner gauge initiatives heighten surface-to-surface contact, further elevating the importance of controllable surface roughness. Global ready-meal sales growth and regulatory pushes for extended shelf life collectively intensify demand for premium antiblock systems that withstand repeated temperature cycling. Consequently, anti-block additives transition from a cost item to a performance enabler, allowing suppliers to defend higher price points in value-added packaging contracts.

Expansion of Greenhouse and Mulch-film Agriculture

Precision farming and climate-controlled cultivation spur rapid uptake of greenhouse covers and mulch films that rely on anti-block technology to ease roll-out and retrieval. Optical transmittance must remain high to optimize photosynthesis; therefore, agents such as rice-husk-ash silica are gaining traction despite requiring 2,000–3,000 ppm (parts per million) loading, as they match the blocking resistance of commercial silica while supporting waste-valorization goals. Biodegradable mulch films create an attractive niche for organic antiblock solutions that integrate seamlessly into soil-degradable polymer matrices. Market expansion in India, China, and Gulf Cooperation Council states underscores the long-term nature of this driver as governments seek food-security gains.

Rapid Growth of High-clarity BOPP Lines

Brand owners migrating from polyethylene Terephthalate (PET) to clear biaxially oriented polypropylene (BOPP) for improved stiffness-to-weight ratios are installing new tenter and sequential-stretch units across Asia. High-clarity film grades demand anti-block particles small enough to minimize haze yet large enough to create effective micro-asperities; talc-based Optibloc formulations deliver sub-1% haze at 500 ppm dosage while ensuring line productivity. Electronics producers also adopt capacitor-grade BOPP, necessitating ultra-pure anti-block choices free from ionic contaminants. The tight technical window has lifted specialty additive margins and spurred research and development (R&D) into nano-silica and bio-wax hybrids capable of balancing thermal stability with dielectric integrity.

Brand-owner Shift Toward Mono-material Recyclability

European extended-producer-responsibility directives and North American retail commitments will soon target 100% recyclable packaging. Eliminating multi-layer structures places more onus on anti-block additives to deliver slip, clarity, and seal strength within a single polymer family. Clariant’s AddWorks PKG 158 stabilizer shows how synergistic packages can withstand multiple mechanical-recycling loops while preserving film color. Formulators now screen anti-block candidates for in-use performance and compatibility with optical sorters and re-melt rheology. These new selection criteria open market space for organic waxes and calcium-carbonate-coated starches that leave no residue in regrind streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Haze and Gloss Deterioration in Optical Films | –0.8% | Global premium packaging markets | Short term (≤ 2 years) |

| Stringent Migration Limits in Pharmaceutical Blister Packs | –0.6% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Supply Risk of High-purity Sodium-based Inorganic Agents | –0.4% | Global, specialty applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Haze and Gloss Deterioration in Optical Films

High-end display and transparent barrier films tolerate negligible haze, forcing antiblock loadings well below standard industrial levels. Conventional silica or talc particles scatter visible light, and interactions with erucamide can form discoloring complexes that reduce shelf appeal. Electronics laminates require dual-function formulations that offset the loss of surface asperities with advanced low-migration slip aids, yet the R&D cost and qualification timelines slow commercialization. This constraint disproportionately affects the premium segment, dampening additive volume growth despite healthy unit economics.

Stringent Migration Limits in Pharmaceutical Blister Packs

Regulatory authorities enforce tight extractable and leachable thresholds under 21 CFR 178, mandating full toxicological dossiers before new anti-block chemistries can be adopted for pill cavities and sachets [2]US FDA, “Indirect Food Additives: Polymers,” fda.gov. Nanoparticle-based systems face extra scrutiny because analytical methods to verify particle migration remain under debate. As a result, drug companies maintain legacy silica grades already granted Drug Master File status, limiting upgrade opportunities for suppliers and elongating conversion cycles to alternative solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Organic Formulations Challenge Inorganic Dominance

In 2025, inorganic agents captured 64.10% of the global Anti-block Additives market share, largely through cost-effective silica, diatomite, and talc solutions that blend readily into polyethylene and polypropylene. However, the segment faces regulatory headwinds as the European Chemicals Agency (ECHA) weighs stricter crystalline-silica exposure limits. Organic solutions, fatty-acid amides, plant waxes, and starch-calcium carbonate composites are advancing at a 6.00% CAGR, closing the performance gap as suppliers refine particle morphology and surface energy. Hybrid systems combining micronized shell-based wax with nano-silica illustrate how formulators can cut mineral loading by 30% without losing blocking resistance or optical clarity. Film recyclers favor these bio-based alternatives because they leave no residual abrasion in regrind, supporting circular-economy targets. Consequently, organic share gains are expected across commodity and premium applications, narrowing volume spreads even as total demand expands.

Organic momentum is further fueled by improved dispersion techniques such as reactive-extrusion grafting that locks fatty-acid chains onto polymer backbones, limiting migration and bloom. Cost parity is becoming reachable at crude-oil price levels above USD 75/bbl, where petrochemical feedstocks inflate inorganic processing costs. The antiblock additives market therefore exhibits a gradual but irreversible tilt toward organics, especially in regions with robust recycling mandates or consumer eco-label programs.

By Polymer Type: LDPE Leadership Faces BOPP Challenge

Low-density polyethylene (LDPE) maintained a 38.05% share of the Anti-block Additives market size in 2025, owing to its prevalence in grocery sacks, stretch hooders, and agricultural covers. LDPE’s amorphous morphology allows uniform silica dispersion, creating micro-asperities that prevent film fusion during roll-winding. Yet biaxially-oriented polypropylene is gathering pace, forecast to post a 6.17% CAGR through 2031 as converter investments in high-clarity lines multiply across Asia and Eastern Europe. BOPP’s rising acceptance in capacitor, confectionery, and tobacco overwraps increases demand for ultra-pure antiblock particles that do not impede dielectric performance. Linear Low-Density Polyethylene (LLDPE) and High-Density Polyethylene (HDPE) continue steady penetration in heavy-duty sacks and industrial liners, whereas Polyvinyl Chloride (PVC) has lost ground due to chlorine-content concerns.

Polymer-specific needs shape additive selection: LDPE tolerates coarser particles, allowing lower-cost diatomite, while BOPP requires sub-3 µm mean diameters. Hybrid multilayer barrier films are being replaced by recyclable mono-material laminates, often Polypropylene (PP) or Polyethylene (PE), shifting additive buyers toward chemistries compatible with mechanical reprocessing. Therefore, suppliers offering tailored masterbatches aligned with polymer rheology maintain competitive edge.

By Application: Food Packaging Dominance Challenged by Agriculture

Food packaging absorbed 44.70% of global anti-block demand in 2025 due to high-volume snack, dairy, and ready-meal segments needing slip and antifog in addition to antiblock. Startup craft-food brands choosing transparent stand-up pouches reinforce this base. Agricultural films, however, will grow the fastest at a 6.22% CAGR as governments subsidize greenhouse expansion and biodegradable mulch adoption. Agricultural needs revolve around consistent optical transmission, dust resistance, and ease of field deployment, pushing innovation toward higher-load organic agents that balance cost and performance.

Pharmaceutical blister and sachet films remain a lucrative niche because of stringent purity norms, enabling premium pricing for United States Pharmacopeia (USP)-class silica. Though volumes are modest, industrial liners for construction and automotive interior skins utilize antiblock additives for processability during thermoforming. Consumer-goods shrink film increasingly adopts bio-based antiblock to safeguard recyclability claims printed on the pack. Application diversity cushions overall demand swings tied to any single end-use sector.

Geography Analysis

Asia-Pacific recorded 30.30% of the global Antiblock Additives market share in 2025 and is advancing at a 6.05% CAGR, driven by China’s integrated resin-to-film clusters and India’s e-commerce boom. Local supply of ethylene, propylene, and mineral fillers provides structural cost advantages, while domestic brands upgrade to thinner gauges, lifting unit additive consumption. Multinationals such as Evonik invested USD 200 Million in Nanjing specialty amine capacity to secure regional availability of raw materials for organo-modified additives.

North America exhibited steady mid-single-digit growth in 2025 as frozen-food producers switched to lighter bags and pharmaceutical packagers maintained stringent specification lock-ins. FDA compliance requirements favor incumbents, giving US-based masterbatch companies stable margins. The region also pioneers post-consumer-recycled (PCR) film loops, which require robust antiblock packages tolerant to reprocessing heat histories.

Europe’s antiblock demand climbed modestly despite stringent REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) documentation burdens that raise testing costs. Packaging recyclability goals are accelerating the adoption of bio-wax solutions, and ECHA’s proposed silica limits intensify this pivot. Western European converters lead mono-material laminate adoption, fostering collaboration between additive suppliers and recycling consortia to validate downstream process compatibility.

South America saw rising agricultural film consumption, notably in Brazil’s protected horticulture projects. Import dependence remains high for specialized antiblock grades, exposing converters to currency fluctuations. Middle East & Africa, though smaller in value, enjoy strong greenhouse adoption in Gulf states and North African citrus regions. Regional resin capacities in Saudi Arabia support film plants that increasingly source additives locally to manage lead times.

The geographic mosaic underscores how proximity to raw materials, regulatory regimes, and end-use industries shapes demand trajectories, reinforcing Asia’s volume leadership while Europe and North America steer sustainability-driven innovation.

Competitive Landscape

The Antiblock Additives market is moderately consolidated. Ampacet Corporation leverages a broad color and functional portfolio to bundle antiblock with slip and antifog, enhancing wallet share among flexible-packaging clients. Evonik Industries AG capitalizes on its organomodified siloxane and amine chemistry platforms to tailor hybrid organo-inorganic particles, addressing clarity-sensitive BOPP needs. LyondellBasell Industries Holdings B.V. integrates resin and additive supply to guarantee secure sourcing for multinational converters. Joint-venture activity centers on Asian masterbatch tolling, enabling Western formulators to localize production without heavy capital outlays. Short supply events in quartz and sodium trisilicate have raised the strategic importance of vertical integration and multi-sourcing, potentially spurring consolidation over the next five years.

Antiblock Additive Industry Leaders

Ampacet Corporation

ATLANTA

Avient Corporation

Tosaf Compounds Ltd.

Sukano

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The European Chemicals Agency proposed stricter regulations for silicon dioxide compounds due to health risks associated with crystalline and amorphous forms. This move can potentially affect the antiblock additive formulations that rely on silica-based agents.

- April 2023: Cargill, Incorporated announced renaming the Crodamide brand of slip and anti-blocking additives to Optislip. This move aims for a name that resonates more with the advantages and performance the products offer to the plastics sector.

Global Antiblock Additive Market Report Scope

The antiblock additive market report includes:

| Organic |

| Inorganic |

| Low Density Polyethylene (LDPE) |

| Linear Low-density Polyethylene (LLDPE) |

| High-density polyethylene (HDPE) |

| Biaxially-oriented Polypropylene (BOPP) |

| Polyvinyl Chloride (PVC) |

| Other Polymer Types (Polyethylene Terephthalate (PET), etc.) |

| Food Packaging |

| Pharmaceutical |

| Industrial |

| Agriculture |

| Other Applications (Consumer Goods, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Organic | |

| Inorganic | ||

| By Polymer Type | Low Density Polyethylene (LDPE) | |

| Linear Low-density Polyethylene (LLDPE) | ||

| High-density polyethylene (HDPE) | ||

| Biaxially-oriented Polypropylene (BOPP) | ||

| Polyvinyl Chloride (PVC) | ||

| Other Polymer Types (Polyethylene Terephthalate (PET), etc.) | ||

| By Application | Food Packaging | |

| Pharmaceutical | ||

| Industrial | ||

| Agriculture | ||

| Other Applications (Consumer Goods, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Anti-block Additives market?

The Anti-block Additives market size reached USD 1.03 Billion in 2026 and is projected to grow to USD 1.33 Billion by 2031.

Which region leads global demand for anti-block additives?

Asia-Pacific holds the largest share at 30.30% and is forecast to grow at a 6.05% CAGR through 2031 due to strong film manufacturing bases in China and India.

Which polymer segment is expected to grow the fastest?

Biaxially-oriented polypropylene is projected to post the highest CAGR of 6.17% through 2031, driven by demand for high-clarity packaging and capacitor films.

Why are bio-based anti-block additives gaining traction?

Regulatory pressure on silica exposure and increased focus on mono-material recyclability push converters toward bio-based solutions that maintain performance without mineral drawbacks.

How will tighter silica regulations in Europe affect the market?

Proposed ECHA limits could raise compliance costs for inorganic additives, accelerating the shift toward organic alternatives and hybrid formulations.

Page last updated on: