Anime Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

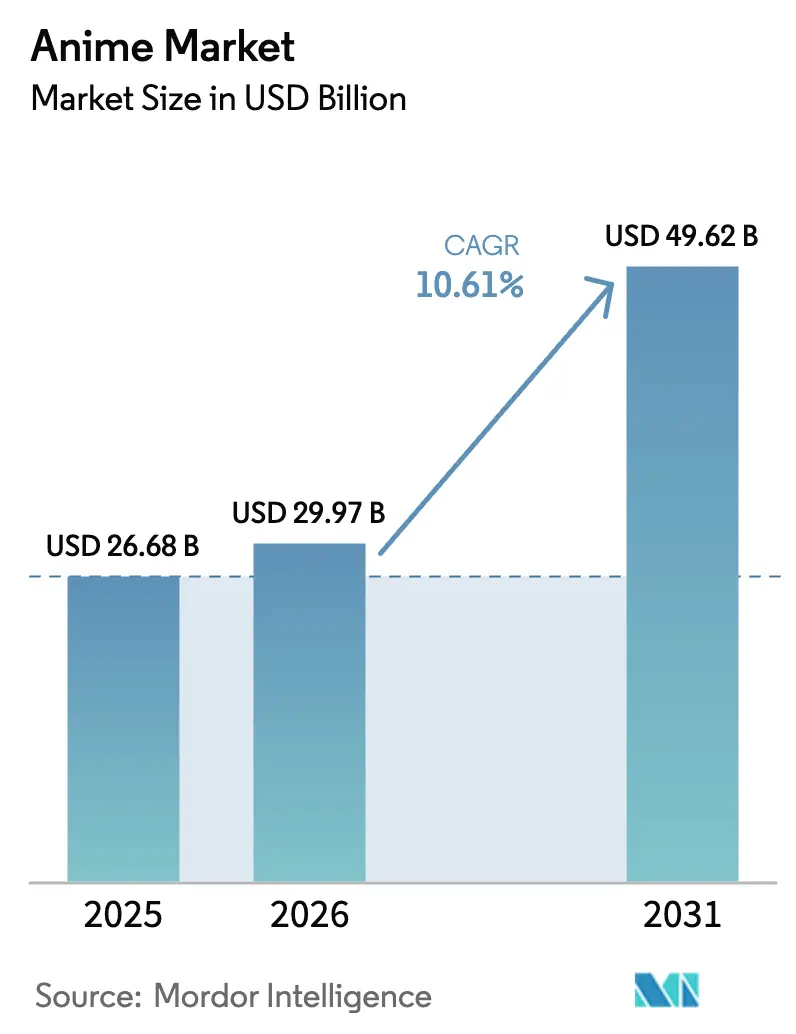

| Market Size (2026) | USD 29.97 Billion |

| Market Size (2031) | USD 49.62 Billion |

| Growth Rate (2026 - 2031) | 10.61% CAGR |

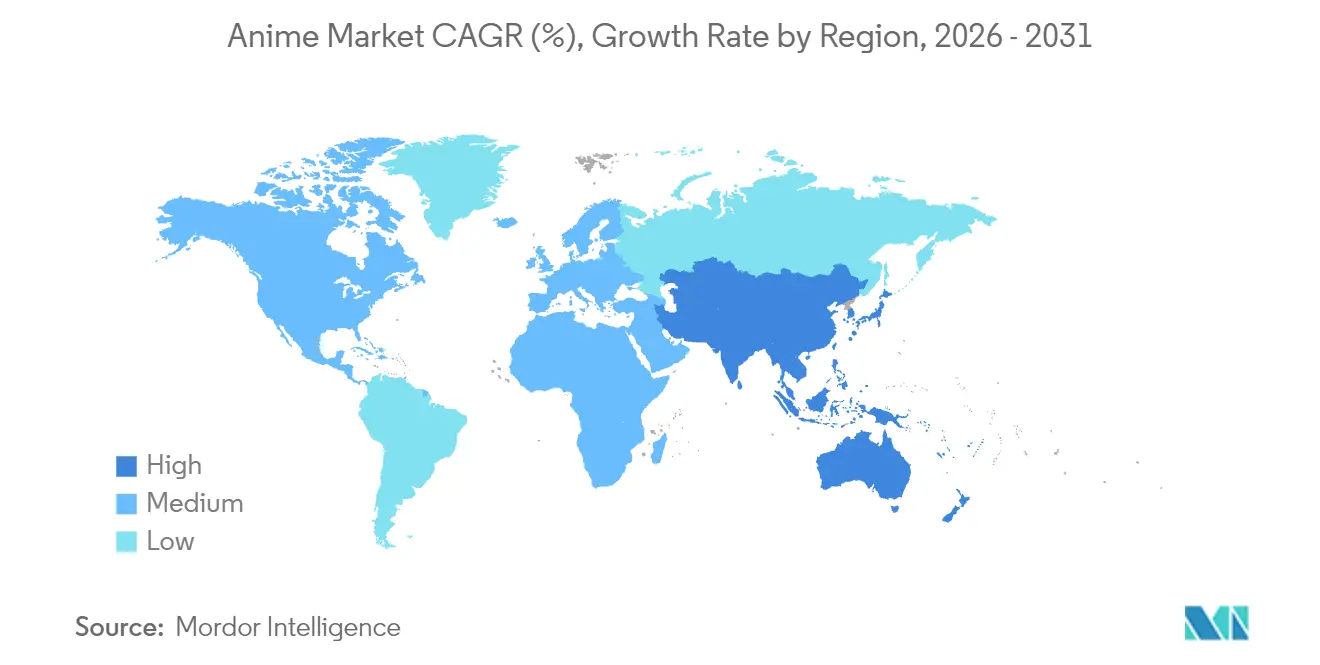

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

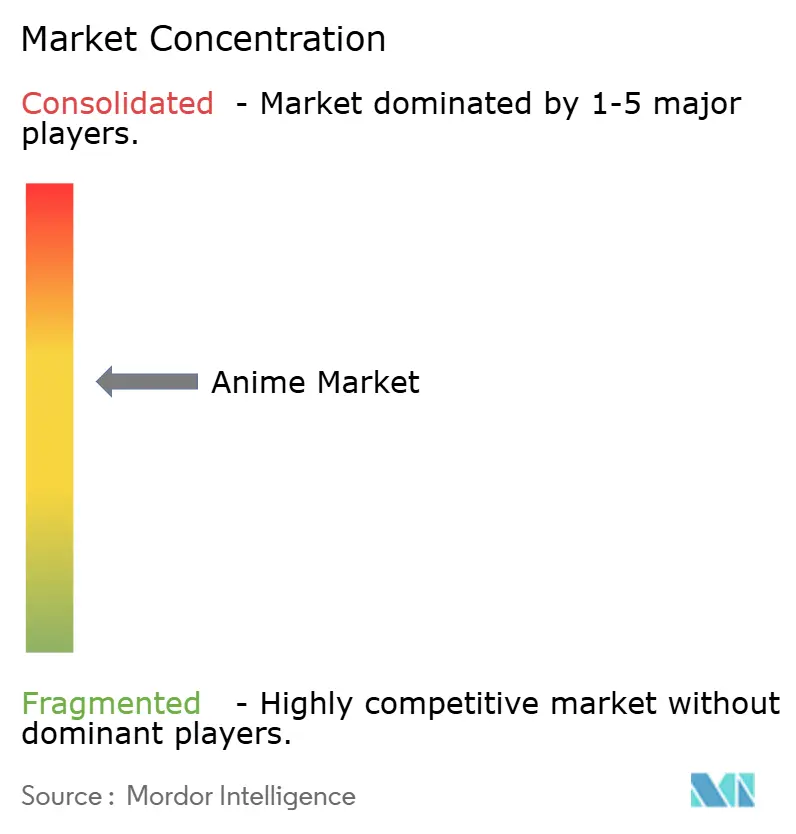

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anime Market Analysis by Mordor Intelligence

The Anime Market size is expected to grow from USD 26.68 billion in 2025 to USD 29.97 billion in 2026 and is forecast to reach USD 49.62 billion by 2031 at a 10.61% CAGR over 2026-2031. Momentum comes from platform-native distribution that eliminates geographical release gaps, while merchandising, theatrical events, and live experiences combine to extend intellectual-property lifecycles. Streaming services monetize global day-and-date releases, premium collectibles capture adult discretionary spending, and cross-media franchise engineering maximizes lifetime value. Generative AI enhances production efficiency, though talent shortages and piracy pressures temper the upside potential. Government export programs, growing Arabic and Portuguese dubbing libraries, and record-breaking box-office performances reinforce the trajectory of the anime market.

Key Report Takeaways

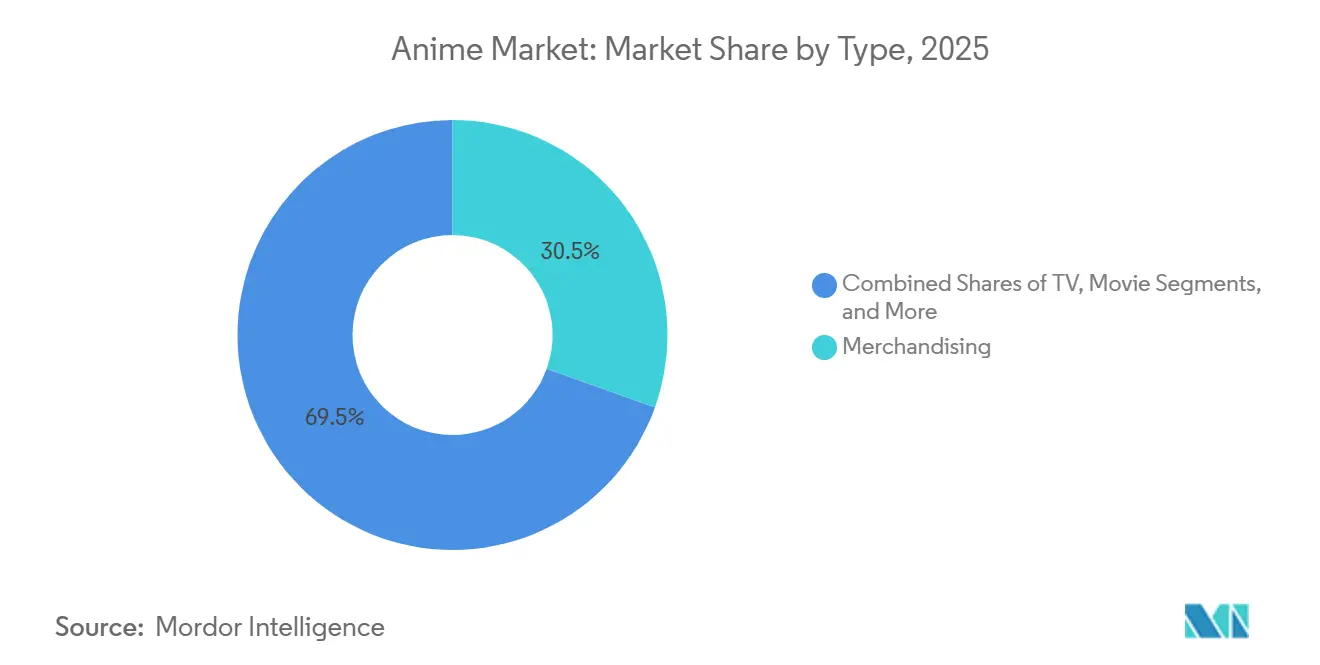

- By type, merchandising led with 30.47% revenue share in 2025, whereas Internet Distribution is projected to advance at a 12.18% CAGR through 2031.

- By genre, Action and Adventure captured 33.54% of the 2025 revenue mix, while Sci-Fi and Fantasy is set to expand at an 11.98% CAGR to 2031.

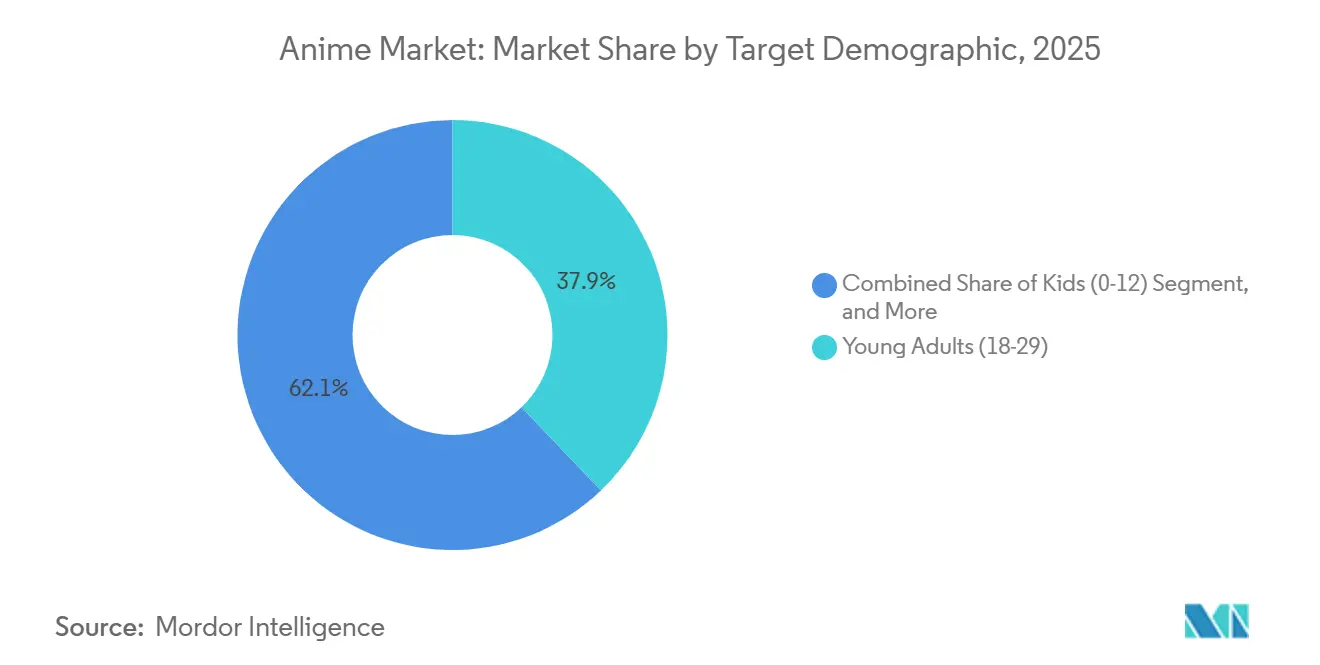

- By target demographic, Young Adults aged 18-29 held 37.86% share in 2025, yet the Teens segment aged 13-17 is on course to grow at an 11.58% CAGR between 2026-2031.

- By geography, Asia-Pacific accounted for 27.43% revenue in 2025 and is poised to post the fastest 11.63% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anime Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Popularity of Global Streaming Simulcasts | +2.8% | Global, strongest in North America and Europe | Short Term (≤ 2 Years) |

| Expansion of High-Value Collectible Merchandising Lines | +2.1% | Japan, North America, China | Medium Term (2–4 Years) |

| Cross-Media Franchise Strategies Boosting Lifetime IP Value | +1.9% | Asia-Pacific and North America | Long Term (≥ 4 Years) |

| Generative AI Accelerating Pre-Production Workflows | +1.5% | Japan, South Korea, China, India | Medium Term (2–4 Years) |

| Localization Investments Unlocking Non-Traditional Regions | +1.3% | Middle East, South America, Africa | Long Term (≥ 4 Years) |

| Government Support for Cultural Export Programs | +0.9% | Japan, South Korea, ASEAN | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Rising Popularity of Global Streaming Simulcasts

Simulcast distribution delivers episodes worldwide within hours of the Japanese airing, eliminating the 6-12-month localization lag that historically fueled piracy. Crunchyroll surpassed 15 million paid subscribers in 2025 after amplifying its simulcast slate, proving that immediacy converts casual viewers into recurring revenue.[1]Crunchyroll, “Company Information and Subscriber Data,” CRUNCHYROLL.COM Netflix disclosed 4.4 billion anime viewing hours during the first half of 2025, a growth rate that outpaced its general catalog tenfold and prompted 40 new greenlights for 2026. Platforms use global rights bundles to hedge against foreign-exchange swings and lower per-territory transaction costs, but smaller distributors struggle to match the speed of localization. Simulcasts also compress marketing timelines, with social media chatter peaking around synchronized releases, creating efficient word-of-mouth. As a result, the anime market gains worldwide day-one revenues that were previously unattainable.

Expansion of High-Value Collectible Merchandising Lines

Adults with disposable income are driving premium figure sales priced above USD 100, shifting merchandising from volume to value. Good Smile Company launched 87 Nendoroid and Figma figures in 2025, and limited editions sold out in 48 hours, later reselling at 200-300% premiums. Bandai Namco’s Hobby Division earned JPY 45 billion (USD 300 million) operating income in fiscal 2025, largely from collectible Gundam kits. Rapid 3D-printing prototyping cuts development cycles to nine months, allowing manufacturers to seize short-lived hype waves. Social-media unboxing videos deliver organic promotion that traditional toy lines lack, reinforcing the anime market momentum among collectors. However, reliance on Chinese factories introduces tariff exposure and variable quality control, which could suppress margins.

Cross-Media Franchise Strategies Boosting Lifetime IP Value

Publishers seed intellectual property through manga and light novels, gauge fan traction, then escalate into anime, mobile gaming, and live events. KADOKAWA logged JPY 180 billion (USD 1.2 billion) in fiscal-2025 revenue by orchestrating such cascades, using print as a low-risk incubator for animated adaptations.[2]KADOKAWA Corporation, “FY-2025 Results and IP Strategy,” KADOKAWA.CO.JPFrieren: Beyond Journey’s End exemplifies the model, debuting in manga, securing an anime adaptation, and launching a mobile RPG inside five years. Cross-media engineering amplifies merchandise demand, prolongs subscription life, and offsets single-season volatility, lifting the broader anime market. Because development costs distribute across multiple media, franchises achieve higher return on capital than stand-alone TV properties, incentivizing committees to prioritize IP universes that translate across formats.

Generative AI Accelerating Pre-Production Workflows

Studios deploy AI systems for background art, in-betweening, and color correction, trimming lead times and reallocating animators toward creative keyframes. Toei Animation recorded a 35% reduction in background preparation for One Piece after rolling out AI tools in 2025.[3]Toei Animation, “AI-Assisted Production,” TOEI-ANIM.CO.JP KADOKAWA’s partnership with startup Kamikai generates rough animation from storyboards, allowing directors to iterate before investing human labor. As production budgets top JPY 300 million (USD 2 million) per episode, these efficiencies are crucial for profitability. Guilds demand transparency on AI usage, requiring minimum human headcounts to safeguard jobs, yet adoption spreads because the anime market rewards faster content cycles. Long term, AI may democratize small-studio output if regulatory clarity emerges around training-data rights.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Talent Shortages and Burnout | -1.8% | Japan, South Korea, Southeast Asia | Short Term (≤ 2 Years) |

| Escalating Production Budgets Outpacing Revenue Growth | -1.5% | Japan and North America | Medium Term (2–4 Years) |

| Piracy and Illicit Streaming Undermining Monetization | -1.2% | Southeast Asia, Africa, South America, Middle East | Medium Term (2–4 Years) |

| Fragmented Intellectual Property Rights Across Markets | -0.9% | China, Middle East, South America | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Persistent Talent Shortages and Burnout

Japanese animators earned an average of 4.4 million JPY (USD 29,000) in 2025, 35% below the national median, discouraging new entrants.[4]Japan Animation Creators Association, “2025 Animator Income Survey,” JANICA.JP Turnover hit 20%, pushing studios to outsource in-betweening to Southeast Asia, where language barriers and time-zone gaps lengthen feedback loops. Government-mandated 60-hour weekly caps exist, but freelance contracts circumvent them, so overwork remains endemic. Keyframe artists, whose quality anchors viewer satisfaction, are irreplaceable, meaning shortages directly constrain output. Unless wages rise or automation matures, supply limits could temper the anime market expansion despite robust demand.

Escalating Production Budgets Outpacing Revenue Growth

Episodes now cost USD 2-3 million to deliver theatrical-grade visuals, yet non-exclusive streaming fees linger around USD 300,000, leaving a financing gap. Voice-actor rates doubled since 2020, while inflation lifts energy and rent costs, squeezing margins. Studios lacking merchandise hits depend on sequels to proven franchises to de-risk budgets, reducing creative variety. Platforms leverage monopsony buying power to cap fee escalation, creating uneven bargaining positions. Rising costs without proportional revenue escalation can slow greenlights and elongate recoupment periods, challenging the anime market profitability model.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Internet Distribution Reshapes Revenue Timing

Internet Distribution is forecast to post a 12.18% CAGR during 2026-2031 as on-demand libraries accumulate and consumers abandon linear television. Merchandising retained 30.47 of % anime market share in 2025, confirming that tangible goods still deliver near-term cash flow. TV viewership among under-35 audiences fell by double digits, while theatrical anime surpassed USD 400 million in worldwide receipts during 2025, proving event cinema’s resilience. Pachinko, confined to Japan, secured roughly 8-10% of revenue from machine licenses, whereas Live Entertainment rebounded 15% year over year, with conventions such as Anime Expo drawing 115,000 attendees. Video discs continue to contract, but digital soundtrack streams partially offset the decline. Broadly, the anime market pivots to subscription revenues that arrive upfront, smoothing studio cash flow.

The streaming explosion fragments viewership across services, compelling enthusiasts to juggle multiple subscriptions and inflating churn risk. Exclusive licensing transfers catalog power from broadcaster syndication to tech platforms, placing pressure on independent distributors. Merchandising provides hedge revenue as figures launch in sync with episode releases, amplifying demand spikes. The anime market size for streaming formats will expand fastest, but long-tail physical formats still generate collector premiums. Linear broadcasting remains relevant for older demographics and advertisers that value weekly tune-in, illustrating that revenue diversification mitigates segment volatility.

By Genre: Sci-Fi and Fantasy Gains on Formulaic Efficiency

Action and Adventure owned 33.54% of 2025 revenues, anchored by shonen flagships. However, Sci-Fi and Fantasy is predicted to advance at an 11.98% CAGR across 2026-2031 due to isekai formulas that recycle world-building assets. Sports titles like Blue Lock rode soccer’s global footprint to penetrate Europe and South America, showing that genre freshness can unlock new geographies. Romance and Drama grow steadily among older women but offer modest merchandising upside relative to action franchises. Horror remains niche because content rating restrictions impede ad monetization, though streaming midnights preserve cult appeal.

Formulaic isekai lowers script risk, allowing committees to greenlight titles with preexisting light-novel fandoms. Streaming algorithms promote microgenres, enabling small but global communities to generate sufficient views for profitability. Action remains merchandising king, yet overreliance on legacy franchises risks audience fatigue. Studios experiment with hybrid genres, pairing sports with supernatural elements to diversify revenue streams. Overall, cross-genre adaptation accelerates because the anime market rewards IP that travels across borders and product categories.

By Target Demographic: Teens Drive Incremental Growth

Teens aged 13-17 are projected to grow by 11.58% annually through 2031, driven by algorithmic recommendations that blend anime with Western animation feeds. Young Adults aged 18-29 maintained a 37.86% share in 2025 and remain the backbone of premium subscription and collectibles purchases. Kids under 12 stay underserved, giving Western studios dominance in preschool programming. Seinen and josei segments appeal to adults seeking mature narratives; although smaller, they command higher ad CPMs and boutique-figure sales. Advertising brands target teen fandom because 59% of U.S. adolescents self-identify as anime fans, with gender parity challenging stereotypes.

Platform rating systems influence production themes, as teen-safe edits unlock broader reach but may dilute plot intensity. Live conventions cater to teen cosplay culture, monetizing ticketing and merchandise on-site. Seinen titles experiment with psychological drama, broadening demographic diversity. As parental control tools improve, studios can tailor age-specific catalog zones, enhancing discoverability and retention. The anime market thus widens its demographic funnel while preserving core adult spend.

Geography Analysis

Asia-Pacific held 27.43% revenue in 2025 and is forecast to climb at 11.63% CAGR through 2031, reflecting Japan’s creative dominance, China’s consumption surge, and Southeast Asia’s mobile broadband boom. Bilibili registered 341 million monthly users in Q4-2025, with anime consuming 35% of watch hours. China’s regulators approved 47 Japanese titles in 2025, up from 28 in 2023, signaling détente and expanding import windows. Outsourcing hubs in Vietnam and the Philippines absorb in-betweening to counter Japan’s workforce gap, while South Korea leverages webtoons for original adaptations. India registers double-digit view growth as budget carriers enable affordable mobile internet. Asia-Pacific’s market balance shifts from export-oriented production to balanced indigenous demand, lifting regional licensing fees and collaborating with local telcos to integrate anime bundles.

North America ranks second in absolute revenue. Theatrical releases surpassed USD 50 million in domestic grosses, a figure considered implausible pre-2020, and Crunchyroll counts 15 million U.S. and Canadian subscribers, proving mainstream acceptance. Streaming fragmentation compels multi-service households, while brick-and-mortar retailers expand anime figure aisles. Canada’s bilingual market opens opportunities for French dubs, mirroring European practices. Mexico and other South American nations see anime viewership climbing as Spanish and Portuguese dubs roll out, although payment-processing gaps hamper ARPU growth.

Europe demonstrates mature fandoms, with Germany, France, and the United Kingdom leading. French box office topped USD 150 million in 2025 for anime releases. Localized dubbing in German, French, and Italian lifts completion rates. The Middle East emerges as a high-growth frontier as streaming services invest in Arabic tracks, and youth-dense Gulf nations host conventions that draw 50,000-plus attendees. Africa remains nascent because piracy eclipses paid platforms, yet smartphone adoption seeds future potential. Collectively, geographic expansion broadens the anime market revenue base, reducing overreliance on Japan and the United States.

Competitive Landscape

The anime market remains moderately fragmented. Japanese studios such as Toei Animation, MAPPA, and Ufotable control high-end production, but global streamers wield negotiating clout through scale. Netflix’s exclusive six-series pact with MAPPA, valued at above USD 150 million in 2026, illustrates direct pipeline financing. Crunchyroll’s integration under Sony synchronizes production, theatrical distribution, and merchandising, tightening margins for independents. Bandai Namco and Good Smile dominate collectibles, owing to decades of tooling expertise and IP relationships that deter entrants. Technology differentiates players, with Ufotable partnering Epic Games on real-time rendering that trims compositing by 25%.

AI adoption shifts cost structures. Studios deploying generative tools shorten schedules, sparking a productivity arms race. Patent filings rose to 127 animation-tech inventions in 2025, underscoring innovation intensity. Vertical integration is accelerating, as Bandai Namco purchased a 35% stake in Sunrise Beyond for JPY 12 billion (USD 80 million), locking in capacity for Gundam adaptations. Cooperative deals such as Bilibili-Crunchyroll’s 50-title exchange signify pragmatic coexistence where exclusivity fails to monetize fully.

Regulatory versatility becomes competitive armor. Studios skilled at region-specific edits secure approvals quicker in China and the Middle East. Payment-plan experimentation, such as ad-supported tiers, helps platforms penetrate price-sensitive markets. Talent retention differentiates studios; those offering profit-share and remote options attract scarce key animators. Overall, while no single entity dominates, converging ownership between production and distribution narrows independent leverage, shaping future consolidation.

Anime Industry Leaders

Crunchyroll LLC

Bandai Namco Filmworks Inc.

Toei Animation Co., Ltd.

Netflix, Inc. (Anime Division)

Studio Ghibli, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Netflix entered a multi-year agreement with MAPPA to produce six original series, earmarking more than USD 150 million.

- January 2026: Crunchyroll unveiled simultaneous releases in 15 new languages, investing USD 50 million to expand global reach.

- December 2025: Bandai Namco acquired 35% of Sunrise Beyond for JPY 12 billion (USD 80 million).

- November 2025: Toei Animation inaugurated a Manila facility employing 300 animators at a cost of USD 25 million.

Global Anime Market Report Scope

The Anime Market Report is Segmented by Type (TV, Movie, Video, Internet Distribution, Merchandising, Music, Pachinko, Live Entertainment), Genre (Action and Adventure, Sci-Fi and Fantasy, Romance and Drama, Sports, Horror, Slice of Life, Others), Target Demographic (Young Adults 18-29, Teens 13-17, Kids 0-12, Seinen, Josei), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| TV |

| Movie |

| Video |

| Internet Distribution |

| Merchandising |

| Music |

| Pachinko |

| Live Entertainment |

| Action and Adventure |

| Sci-Fi and Fantasy |

| Romance and Drama |

| Sports |

| Horror |

| Slice of Life |

| Others Genre |

| Young Adults (18-29) |

| Teens (13-17) |

| Kids (0-12) |

| Seinen (Adult Males 20-40) |

| Josei (Adult Females 20-40) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | Japan |

| China | |

| South Korea | |

| India | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Type | TV | |

| Movie | ||

| Video | ||

| Internet Distribution | ||

| Merchandising | ||

| Music | ||

| Pachinko | ||

| Live Entertainment | ||

| By Genre | Action and Adventure | |

| Sci-Fi and Fantasy | ||

| Romance and Drama | ||

| Sports | ||

| Horror | ||

| Slice of Life | ||

| Others Genre | ||

| By Target Demographic | Young Adults (18-29) | |

| Teens (13-17) | ||

| Kids (0-12) | ||

| Seinen (Adult Males 20-40) | ||

| Josei (Adult Females 20-40) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | Japan | |

| China | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the anime market by 2031?

It Is Projected to Reach USD 49.62 Billion by 2031, Expanding at a 10.61% CAGR From 2026–2031.

Which Segment Is Growing Fastest Within Streaming Formats?

Internet Distribution Leads All Segments With a Forecast 12.18% CAGR During 2026–2031.

Which Genre Is Expected to Outperform Through 2031?

Sci-Fi and Fantasy Is Set to Grow at an 11.98% CAGR as Isekai Narratives Proliferate Globally.

Where Is Geographic Growth Strongest?

Asia-Pacific Is Predicted to Record the Fastest 11.63% CAGR, Driven by China and Southeast Asia.

How Are Production Studios Addressing Talent Shortages?

They Outsource In-Betweening to Southeast Asia, Invest in AI Tools, and Open Overseas Facilities to Secure Animators.

What Drives Premium Merchandising Sales?

Collectible Figures Priced Above USD 100 Attract Adult Fans, Aided by Rapid 3D-Printing and Social-Media Virality.

Page last updated on: