Anesthesia Monitoring Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

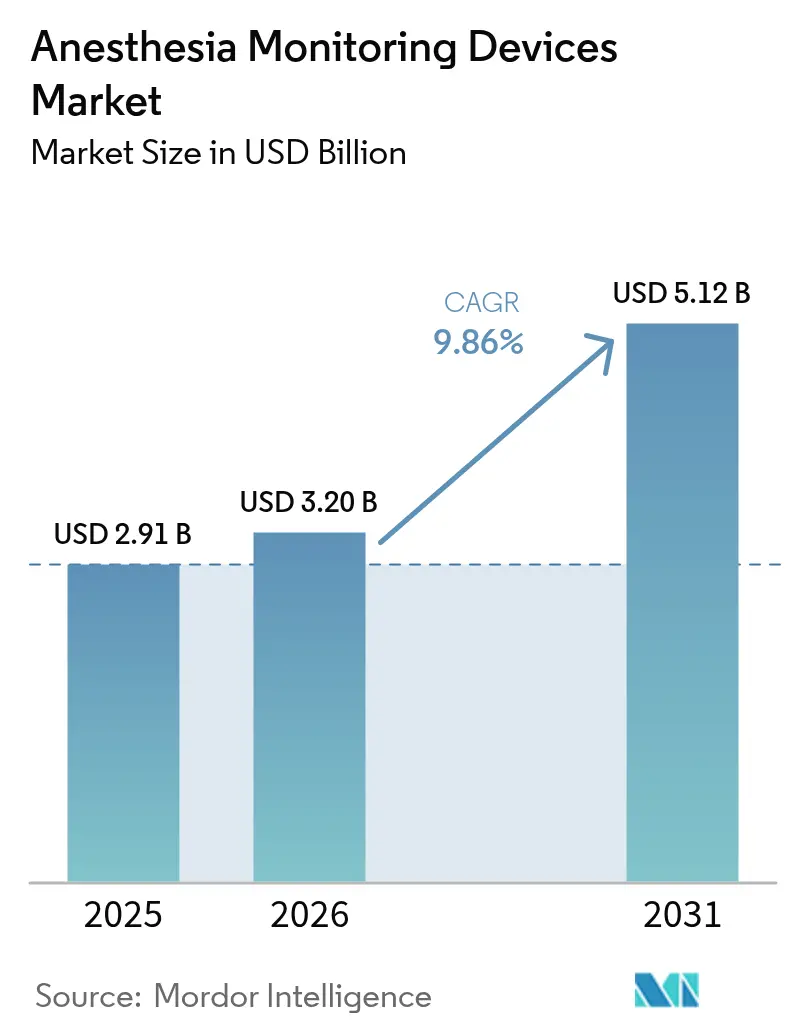

| Market Size (2026) | USD 3.2 Billion |

| Market Size (2031) | USD 5.12 Billion |

| Growth Rate (2026 - 2031) | 9.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anesthesia Monitoring Devices Market Analysis by Mordor Intelligence

The anesthesia monitoring devices market size was valued at USD 2.91 billion in 2025 and estimated to grow from USD 3.2 billion in 2026 to reach USD 5.12 billion by 2031, at a CAGR of 9.86% during the forecast period (2026-2031). Growth rests on higher surgical volumes, artificial-intelligence-enabled predictive analytics, and an aging population that requires deeper perioperative vigilance. Integrated workstations remain the backbone of the anesthesia monitoring devices market because they blend ventilation, gas delivery, and multi-parameter tracking in one footprint, streamlining operating-room workflows. At the same time, AI-enhanced advanced monitors are pulling demand toward specialized applications such as brain activity and nociception tracking, signalling a shift from reactive to anticipatory care. Outpatient migration is another catalyst; portable systems that meet hospital-grade accuracy standards are critical as procedures move to ambulatory surgery centers (ASCs). Regionally, North America supplies stability through reimbursement and early technology uptake, but Asia-Pacific is the fastest-growing zone thanks to policy-backed localization drives that cut import dependency.

Key Report Takeaways

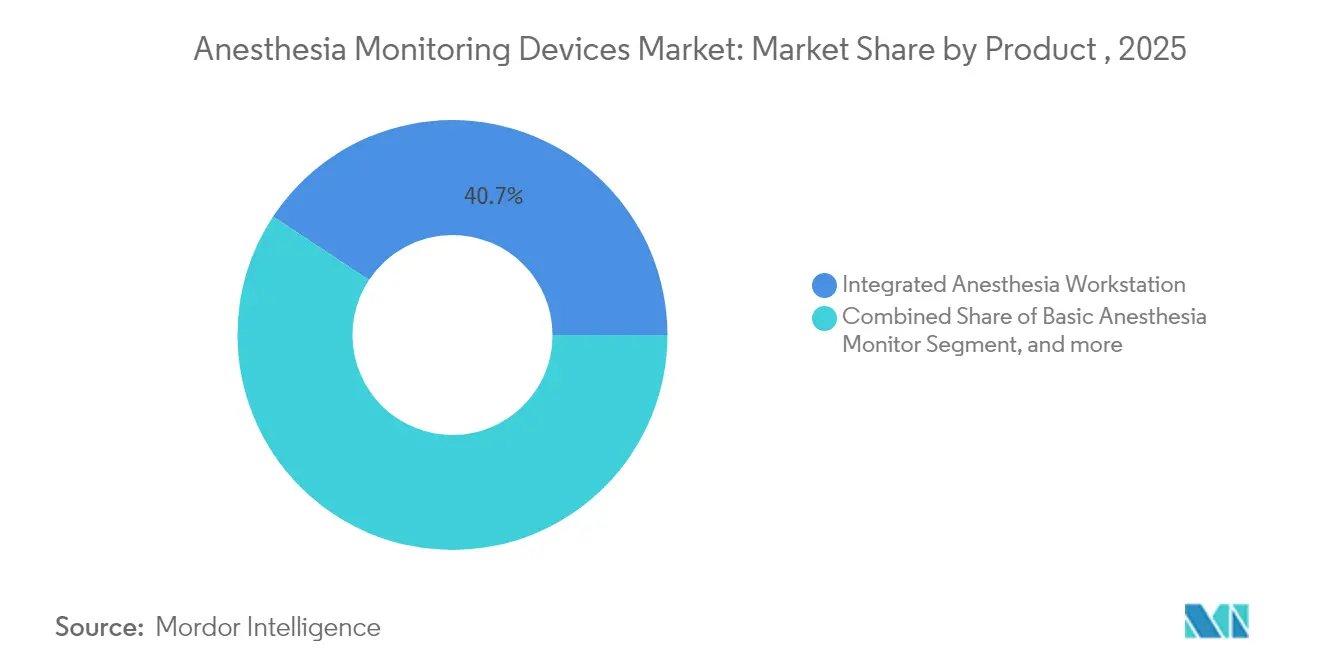

- By product, integrated anesthesia workstations held 40.72% of the anesthesia monitoring devices market share in 2025, while advanced anesthesia monitors are on track for a 10.62% CAGR through 2031.

- By parameter monitored, EtCO₂ ventilation devices secured 55.12% share of the anesthesia monitoring devices market size in 2025; EEG/BIS brain monitors are rising at 10.74% CAGR to 2031.

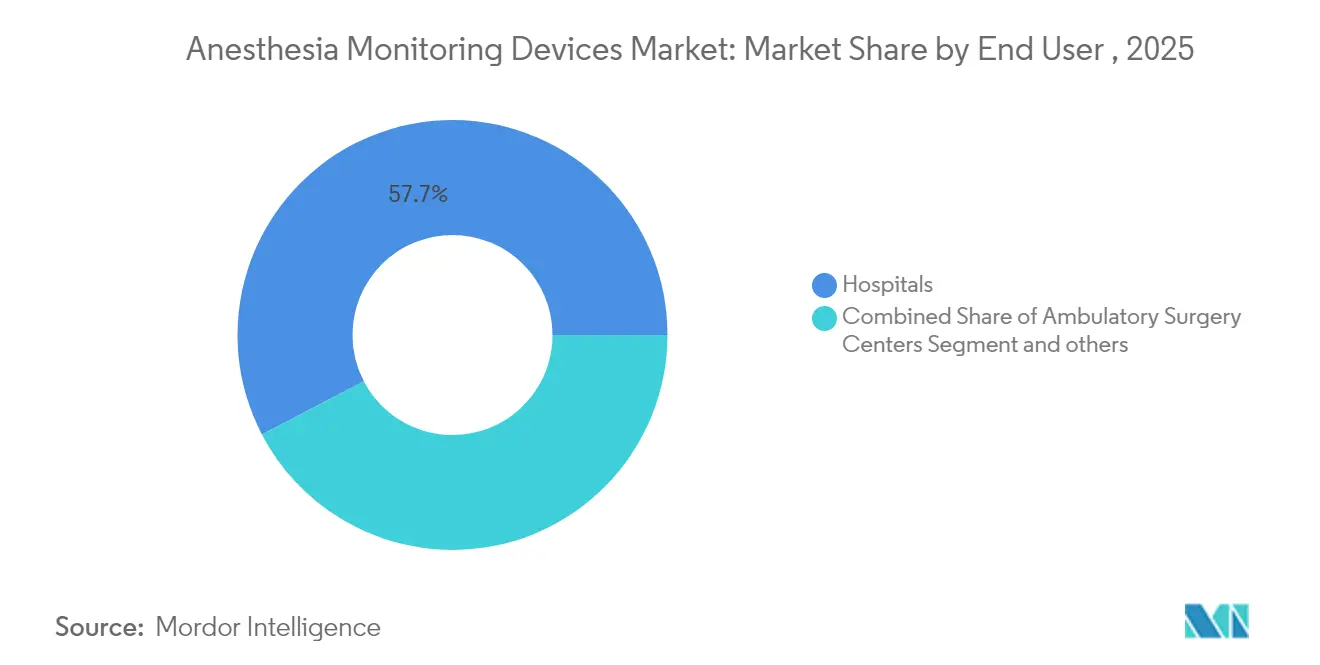

- By end user, hospitals commanded 57.65% of the anesthesia monitoring devices market size in 2025, whereas ASCs will grow the fastest at 10.48% CAGR.

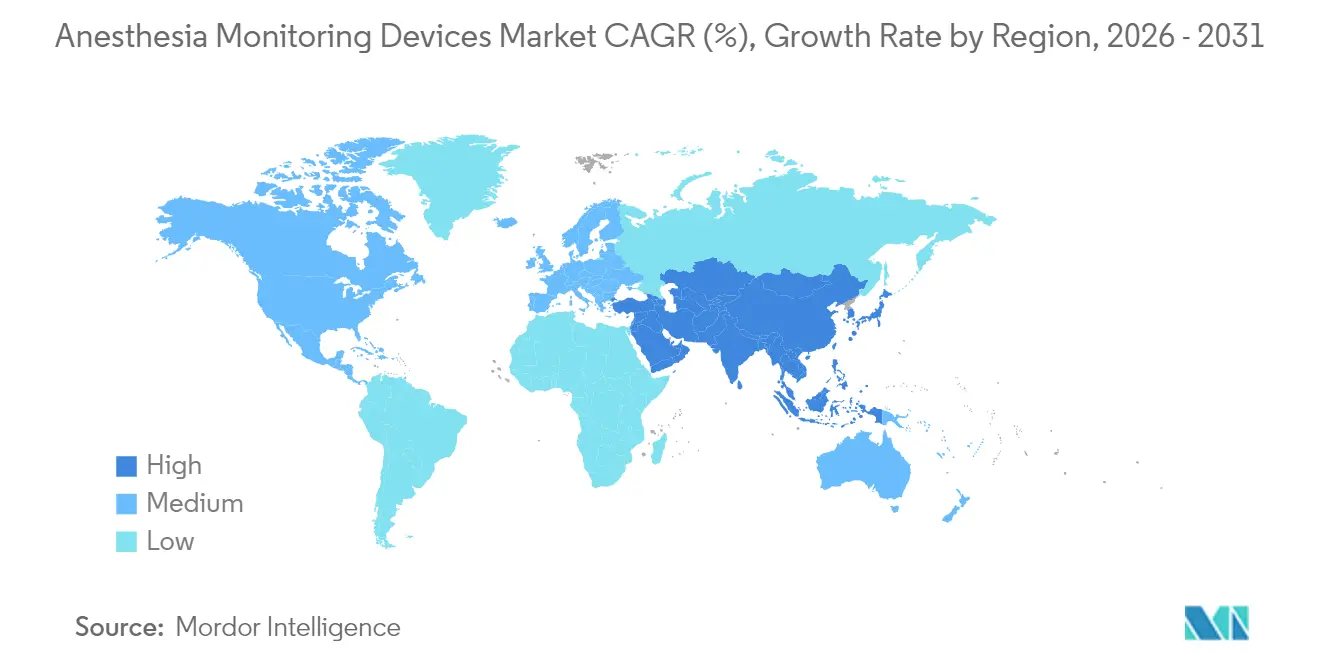

- By geography, North America contributed 38.15% revenue in 2025; Asia-Pacific leads with a projected 10.69% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Anesthesia Monitoring Devices Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Surgical Volumes from Aging Population | 2.3% | Global, peak impact in Asia-Pacific & North America | Long term (≥ 4 years) |

| Development in Anesthesia Technology & Automated Record-keeping | 2.1% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Increasing Demand for Pain-free Surgeries | 1.8% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| AI-driven Predictive Analytics for Intra-operative Monitoring | 1.7% | North America & EU core, expansion to APAC | Medium term (2-4 years) |

| Opioid-sparing Protocols Driving Nociception Monitoring | 1.2% | North America & EU, limited APAC penetration | Short term (≤ 2 years) |

| Portable Monitors for Decentralized Ambulatory Settings | 1.4% | Global, accelerated in North America ASC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Development in Anesthesia Technology & Automated Record-keeping

Automated anesthesia information management systems (AIMS) slash manual charting errors by 40%, freeing clinicians to focus on patient care . Philips’ IntelliSpace Critical Care and Anesthesia illustrates this trend with touch-optimized dashboards that feed real-time vitals directly into electronic health records . Closed-loop controllers already outmatch manual titration for hemodynamic stability, setting the stage for precision protocols driven by historical machine-learning feedback . Such gains meet a dual objective: higher safety margins and lower clinician burnout tied to administrative load. As a result, hospitals treat integrated AIMS as the core of a data-rich anesthesia monitoring devices market strategy.

Increasing Demand for Pain-free Surgeries

Patient expectations around rapid, opioid-sparing recovery are fueling multimodal techniques that hinge on objective nociception metrics. The NOL Index® finger probe converts four photoplethysmography channels into a 0–100 pain score, assisting anesthesiologists in tailoring analgesia . Validation studies confirm uniform accuracy across racial groups because infrared wavelengths and personalized algorithms normalize individual responses, answering equity concerns in perioperative care. In ASCs, where same-day discharge is the norm, NOL monitoring dovetails with ERAS pathways to curb respiratory depression and hasten mobilization. Consequently, pain-free protocols bolster the anesthesia monitoring devices market as facilities invest in sensors that align with patient-centric outcomes.

Rising Surgical Volumes from Aging Population

Median surgical age climbed from 56 to 59 years between 2008 and 2020, and comorbidity profiles point to heavier monitoring loads. Elderly patients experience longer PACU stays and more complications, requiring continuous vigilance that detects subtle physiologic drift. High-risk cases for those ≥65 grew 48.3%, especially in cardiovascular interventions that necessitate sophisticated hemodynamic and neurological oversight. These demographics create fertile ground for AI-enabled depth-of-anesthesia and hypotension prediction tools, reinforcing demand across the anesthesia monitoring devices market.

AI-driven Predictive Analytics for Intra-operative Monitoring

BD’s HemoSphere Alta™ pairs Acumen Hypotension Prediction Index with a Cerebral Autoregulation module, shrinking time-weighted MAP < 65 mmHg from 0.37 mmHg to 0.02 mmHg in controlled studies. Hybrid LSTM-Transformer models now achieve mean-squared-error rates of 0.0062 when forecasting anesthetic depth, eclipsing conventional regression. The payoff is clear: fewer alarms, earlier interventions, and an anesthesiology workforce empowered to supervise more rooms concurrently. Predictive analytics therefore represent a pivotal lever for value creation inside the anesthesia monitoring devices market.

Restraints Impact Analysis of Anesthesia Monitoring Devices Market*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost & Preference for Conventional Techniques | -1.6% | Global, pronounced in developing markets | Medium term (2-4 years) |

| Shortage of Skilled Anesthesiologists in Developing Regions | -1.3% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Cyber-security Risks in Networked Anesthesia Workstations | -0.9% | Global, critical in developed markets | Short term (≤ 2 years) |

| Accuracy Limitations in Obese Patients Discouraging Adoption | -0.7% | Global, correlated with obesity prevalence | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost & Preference for Conventional Techniques

Economic assessments show BIS monitoring costs USD 10,000–25,000 per avoided recall event, potentially adding USD 1 billion in annual spend if universally adopted. TIVA also presents higher variable expenses than low-flow inhalational strategies, leading resource-constrained systems to favor legacy monitors. Budget pressures, training overhead, and regulatory inertia slow advanced-device uptake, placing a drag on the anesthesia monitoring devices market where basic monitors suffice for routine cases.

Shortage of Skilled Anesthesiologists in Developing Regions

Provider deficits escalated to 78% of facilities by late 2024, with only 1,695 residency slots for 2024 and 44% of applicants unmatched. Projected shortfalls of up to 86,000 professionals by 2036 mean sophisticated monitors risk under-utilization in low-staff regions. Burnout among 56% of CRNAs compounds retention issues, restricting market growth where human expertise is essential to interpret high-resolution data streams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Anesthesia Monitoring Devices Market Segment Analysis

By Product:

Workstation Integration Drives Market ConsolidationIntegrated workstations dominated with 40.72% share of the anesthesia monitoring devices market in 2025 as hospitals demanded single-console solutions that house gas delivery, ventilators, and monitors. Advanced monitors, though smaller in installed base, expand 10.62% CAGR by 2031, leveraging AI modules for brain and pain metrics that retrofit onto existing theaters. Basic monitors and consumables sustain the lower-cost layer, particularly in emerging markets and as redundancy backups. GE Healthcare’s Aisys™ CS² automates fresh-gas delivery, illustrating how workstation platforms integrate sustainability and cost savings, making them indispensable anchors within the anesthesia monitoring devices market.

Consumables show steady growth tied to procedure counts rather than capital cycles. Cyber-security is shaping purchase criteria; unified workstations reduce attack surfaces compared with disparate single-parameter devices. Consequently, procurement teams increasingly assess cyber-resilience alongside clinical performance, further buttressing integrated solutions’ appeal in the anesthesia monitoring devices industry.

By Parameter Monitored:

Ventilation Dominance Challenged by Neurological MonitoringEtCO₂ capnography held 55.12% share of the anesthesia monitoring devices market size in 2025, reflecting its universal role in airway verification and ventilation analysis. Medtronic’s Microstream™ technology exemplifies maturity, adding Smart Capnography™ algorithms that filter nuisance alarms to preserve clinician focus. EEG/BIS platforms register the fastest 10.74% CAGR as opioid-sparing and depth-targeted protocols take hold, shifting spend toward neurological insights. Traditional circulation monitors continue as bedrock tools, but quantitative neuromuscular monitors gained momentum after the 2023 ASA guideline update recommending objective TOF ratios.

Pulse oximetry remains mandatory yet faces scrutiny for pigmentation bias, prompting FDA workshops on accuracy improvements. The trend points to multi-modal consoles that merge ventilation, circulation, and neurological data, reinforcing integrated-analytics demand within the anesthesia monitoring devices market.

By End User:

ASC Growth Reshapes Market DynamicsHospitals owned 57.65% of anesthesia monitoring devices market share in 2025, sustained by high-acuity case volumes and capital budgets for integrated suites. ASCs, however, are expanding at 10.48% CAGR as payers push procedures to outpatient venues, saving Medicare USD 4.2 billion annually versus hospital outpatient departments. This shift favors portable, battery-efficient monitors that retain hospital-grade precision yet fit tight ASC floorplans. Office-based surgical suites and specialty clinics represent an emergent tier, especially in ophthalmology and dermatology, where lighter sedation regimes still mandate robust monitoring to meet regulatory standards.

Manufacturers bundle service contracts and cloud analytics to appeal to ASC buyers who lack in-house biomed teams, closing capability gaps and embedding recurring revenue into the anesthesia monitoring devices market size trajectory.

Geography Analysis

North America Anesthesia Monitoring Devices Market

North America generated 38.15% revenue for the anesthesia monitoring devices market in 2025 on the back of early AI adoption, reimbursement coverage, and a consolidated supplier base. Regulatory clarity and cybersecurity guidance from agencies such as CISA speed procurement decisions, while major vendors leverage domestic manufacturing footprints to navigate supply-chain shocks.

APAC Anesthesia Monitoring Devices Market

Asia-Pacific leads with a 10.69% CAGR through 2031 as China and India escalate localization. China’s device market is slated to climb from USD 36.35 billion in 2024 to USD 55.67 billion by 2029, supported by Made in China 2025 incentives that cut import reliance from 85% toward sub-50% thresholds. India restricts refurbished imports and aims for a USD 50 billion MedTech sector by 2030, opening avenues for indigenous anesthesia monitoring platforms. These moves enlarge the anesthesia monitoring devices market size across regional OEMs and global joint-venture partners.

EMEA and South America Anesthesia Monitoring Devices Market

Europe maintains mid-single-digit growth under the EU Medical Device Regulation, which nudges suppliers toward eco-design and post-market surveillance that strengthen buyer confidence. Middle East and Africa attract hospital-build projects tied to medical tourism corridors in the Gulf, spawning demand for integrated workstations with multilingual user interfaces. South America shows pockets of acceleration in Brazil and Argentina as public hospitals modernize, yet currency volatility keeps procurement cycles uneven. Altogether, geographic diversification cushions the anesthesia monitoring devices market against region-specific shocks and sustains double-digit global expansion.

Regulatory Landscape

In the United States, anesthesia monitoring devices typically follow FDA medical device pathways. Quality system compliance is now anchored by the FDA Quality Management System Regulation (QMSR), which became fully effective on February 2, 2026, aligning expectations more closely with ISO 13485-style lifecycle controls. The FDA also continued to clarify classification and special controls for anesthesia-adjacent monitoring modalities; effective June 1, 2026, the agency issued final orders classifying an adjunctive pain measurement device for anesthesiology and a real-time ultrasound anatomy visualization and labeling device for ultrasound-guided regional anesthesia as Class II (special controls). This provides clearer 510(k) routes for these monitoring-driven workflows.

Across global markets, standards and post-market obligations shape design, validation, and upgrade cycles for integrated workstations and connected monitors. For example, ISO 80601-2-13 (particular requirements for basic safety and essential performance of an anaesthetic workstation) continues to anchor workstation safety expectations, and an amendment (Amd 1) progressed to the International Standard publication stage in April 2026. That progression reinforces the need for standards-aligned verification for workstation platforms that combine gas delivery, ventilation, and multiparameter monitoring in a single footprint.

Value Chain Analysis

The value chain begins with specialized component inputs (medical-grade display panels, high-reliability gas and physiologic sensors, embedded compute and connectivity modules) and software or firmware that must be maintained under regulated change control. OEMs such as Medtronic, GE HealthCare, Philips, Dragerwerk, and Getinge integrate these components into monitors and integrated anesthesia workstations, then complete verification and validation under ISO 13485-aligned quality systems and region-specific regulatory requirements. Because component substitutions and software updates can trigger re-validation across the full monitoring system, supplier qualification, configuration management, and cybersecurity patching have become core value-creation steps, not only compliance tasks.

Downstream, distribution flows through direct sales to hospital groups, group purchasing organizations, and channel partners, supported by field service networks for installation, calibration, and spare-parts logistics. Hospital demand for fewer vendors and standardized fleets is reinforcing platform-centric partnerships. In March 2026, Medtronic and GE HealthCare expanded their collaboration to integrate Medtronic technologies (including pulse oximetry, brain monitoring, and capnography) into additional GE monitoring platforms, and Philips and Getinge formed a commercial partnership in October 2025 to integrate Philips IntelliVue monitoring with Getinge Flow Family anesthesia delivery systems. Supply resilience and continuity planning are also gaining attention, with EU MDR Article 10a introducing advance notification requirements around potential device shortages. That requirement is pushing manufacturers to tighten demand planning, component buffers, and regional supply options.

Competitive Landscape

Moderate consolidation defines the anesthesia monitoring devices market, with top vendors enhancing portfolios through M&A that fuses hardware and predictive analytics. BD paid USD 4.2 billion for Edwards Lifesciences’ Critical Care line, instantly gaining the Acumen HPI algorithm and broadening its critical-care reach[2]Becton Dickinson Newsroom, “BD completes acquisition of Edwards Lifesciences Critical Care,” bd.com. The move reflects a wider pivot from commodity monitors to decision-support ecosystems that blend sensors, software, and cloud dashboards.

Platform leaders—GE Healthcare, Medtronic, Philips—push all-in-one workstations, packaging cybersecurity patches and remote fleet management to lock in hospital-wide contracts[3]GE Healthcare Press, “Aisys CS² with ecoFLOW technology,” gehealthcare.com. Parameter specialists—Masimo for SpO₂ and Nihon Kohden for EEG—compete by embedding AI into niche monitors that integrate seamlessly with leading anesthesia information systems. White-space entrants pursue zero-trust network architectures after CISA flagged authentication flaws that permit remote setting changes on legacy workstations[4]Cybersecurity & Infrastructure Security Agency, “Alert AA24-027A: Anesthesia workstation vulnerabilities,” cisa.gov.

Product differentiation now hinges on human-machine interface refinements such as voice commands, gesture controls, and augmented-reality overlays for catheter placement guidance. Patent filings cluster around sensor miniaturization and closed-loop algorithms, aligning with the anesthesia monitoring devices market trend toward lighter, smarter, and safer systems. Intensifying R&D investment coupled with rising demand keeps competitive rivalry high, yet entry barriers around regulatory clearance and clinical validation sustain moderate concentration.

Anesthesia Monitoring Devices Industry Leaders

Drägerwerk AG & Co. KGaA

Masimo

Medtronic Plc.

GE Healthcare

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Anesthesia Monitoring Devices Market Companies Covered in this Report

- Medtronic

- GE HealthCare Technologies Inc.

- Koninklijke Philips

- Dragerwerk

- Masimo

- Nihon Kohden

- Mindray Bio-Medical Electronics Co., Ltd.

- Smiths Group plc (Smiths Medical)

- B. Braun

- Getinge

- Infinium Medical Inc.

- Schiller

- Fukuda Denshi Co., Ltd.

- Shenzhen Comen Medical Instruments Co., Ltd.

- Criticare Systems Inc.

- Spacelabs Healthcare

- EIZO Corporation

- Heyer Medical

- SternMed

- RWD Life Science Co., Ltd.

- Axcent Medical GmbH

Market Opportunities and Future Outlook

Clearer regulatory classifications and special controls are creating more defined pathways for newer anesthesia-adjacent monitoring categories. That can reduce uncertainty for product developers and hospital adopters. In June 2026, the FDA classified a monitor for opioid-induced impairment of oxygenation as a Class II device under special controls, signaling a more standardized route for objective monitoring tools that support opioid-sparing and safety-focused perioperative protocols. The FDA action effective June 1, 2026 on Class II (special controls) for adjunctive pain measurement devices also adds an anchor for objective nociception and pain-assessment approaches that complement traditional hemodynamic surrogates.

Hospital system standardization and outpatient migration create whitespace for portable, interoperable, and service-supported monitoring fleets that maintain hospital-grade performance within ASC workflows. Evidence of fleet expansion shows up in neuromuscular monitoring. In April 2026, Senzime expanded an agreement with a southeastern US hospital system to deploy 65 additional TetraGraph neuromuscular monitors, taking the installed base in that network to more than 160 units, which points to active procurement for objective TOF and neuromuscular transmission monitoring. Regional manufacturing investment may also support availability and cost structure in emerging markets; in July 2026, Tatweer Medical Industries (linked to El Ezaby Medical and Mindray) announced plans to invest over USD 100 million over three years to expand medical technology manufacturing in Badr City, Egypt, supporting localization-driven purchasing programs and faster delivery for capital equipment and monitoring platforms.

Recent Industry Developments in Anesthesia Monitoring Devices Market

- June 2026: Senzime AB reported that its TetraGraph neuromuscular transmission monitoring system received regulatory approval from Brazils ANVISA. The approval broadens access in Latin America for objective TOF monitoring and supports multi-country standardization for hospital groups that procure monitoring fleets across regions.

- September 2025: Medasense Biometrics expanded US positioning for its PMD-200 monitor featuring NOL (Nociception Level Index) technology for nociception monitoring in adult patients under general anesthesia. This strengthens the clinical toolset for opioid-sparing protocols by adding objective pain-related metrics alongside ventilation and hemodynamic parameters.

- September 2024: BD closed its acquisition of Edwards Lifesciences Critical Care business and formed BD Advanced Patient Monitoring. The integration brought algorithms and hemodynamic monitoring capabilities under a larger platform vendor, raising the competitive bar for decision-support features bundled with perioperative and intraoperative monitoring ecosystems.

Anesthesia Monitoring Devices Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the anesthesia monitoring devices market covers revenues from new electronic monitors and integrated anesthesia workstations used to track patient status during anesthesia, including oxygen saturation, capnography, circulation, neuromuscular transmission, and depth of anesthesia in surgical or procedural care.

Scope exclusions: This scope excludes service contracts, consumables and disposables, refurbished units, stand-alone anesthesia delivery machines, and anesthesia information management software.

Segments Covered in This Report

- By Product

- Basic Anesthesia Monitor

- Integrated Anesthesia Workstation

- Advanced Anesthesia Monitor

- Consumables & Accessories

- By Parameter Monitored

- Oxygenation (SpO₂)

- Ventilation (EtCO₂)

- Circulation (BP/ECG)

- Neuromuscular Transmission (EMG/TOF)

- Brain Activity (EEG/BIS)

- By End User

- Hospitals

- Ambulatory Surgery Centers

- Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries and build the first pass of the demand and supply picture before speaking with experts. We relied on public and official sources such as World Health Organization publications, Centers for Disease Control and Prevention resources, OECD health statistics, and anesthesia or perioperative care association websites to understand procedure volumes and the safety practices used during anesthesia.

To make assumptions practical, we also reviewed medical device regulator databases and guidance notes (for example, FDA and similar agencies), peer-reviewed clinical journals for anesthesia monitoring adoption patterns, and customs or trade statistics where available to sanity check cross-border flows. Company annual reports, investor presentations, and reputable press were used to map product portfolios and typical selling models, and a paid subscription database for company financials, patent activity, and news helped validate timelines and track major product updates. These desk sources are not exhaustive, and other public references were also used for data collection, validation, and clarification as questions came up.

Primary Interviews and Surveys

Primary work was used to confirm what is really being bought and used in operating rooms and procedural settings, and to resolve gaps that public sources cannot answer cleanly. We spoke with a mix of manufacturers, distributors, biomedical engineering teams, anesthesia clinicians, and procurement leaders across APAC, EMEA, and the Americas, so assumptions on monitoring mix, replacement cycles, and average selling prices could be checked and adjusted.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | APAC: 47% |

| Mid tier: 47% | Functional/Unit leaders: 27% | EMEA: 35% |

| Smaller Players: 20% | Managers: 60% | Americas: 18% |

Market-Sizing & Forecasting

Sizing started from a top-down build where surgery and procedure volumes were translated into an addressable monitoring need using anesthesia safety guidelines and typical monitoring protocols, and then converted into device demand through penetration and replacement assumptions. The output was then corroborated with selective bottom-up approximations, such as sampling average selling prices by device class and applying them to estimated unit demand, followed by channel checks to keep the totals realistic.

The model is guided by a few practical inputs that can be defended on a client call. We used indicators such as annual surgical and interventional procedure counts, the share of cases requiring capnography and multi-parameter monitoring, typical capital replacement cycles for monitors and workstations, price mix shifts between basic monitors and advanced depth-of-anesthesia monitoring, and hospital versus ambulatory surgery center adoption patterns. Where unit data was not consistently available across countries, gaps were handled by using regional proxy ratios anchored to procedure volumes and then rechecked through interviews.

For forecasting, scenario analysis was applied around procedure growth, monitoring penetration improvements, and expected price progression, and then smoothed using time-series checks so short-term spikes did not overstate the trend. Assumptions were aligned to what practitioners expect to change in practice, such as tighter safety compliance in procedural sedation settings and gradual upgrades to integrated systems.

Data Validation & Update Cycle

Validation was done through multiple passes so the numbers are not dependent on one assumption. We checked outputs against independent signals such as procedure growth, installed base replacement logic, and the implied share of capital budgets that anesthesia monitoring would consume, and then flagged any country or region values that moved outside plausible ranges.

Before sign-off, the model goes through analyst review steps where inputs are rechecked, arithmetic is audited, and any large variance is traced back to a specific driver. If an outlier cannot be explained, experts are re-contacted to confirm whether it reflects a real change, such as new monitoring mandates or unusual purchasing cycles. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Anesthesia Monitoring Devices Market Size Compared Against Other Published Estimates

Published market values for anesthesia monitoring devices can look different even when they sound like they measure the same thing, because the boundary of what counts as a device sale is not consistent. In our work, we tried to keep the estimate tied to repeatable signals, and then we stress-tested it through expert checks so the market does not get overstated by adjacent revenues.

Procedure volume trends, anesthesia safety monitoring norms, and replacement-led demand checks are the evidence points that keep Mordor Intelligence's estimate anchored to new hardware revenue for anesthesia monitoring, instead of blending in disposables, service, or broader anesthesia delivery equipment.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.2 B (2026) | |

| Industry Publication A | USD 2.79 B (2024) | Uses an earlier base year and appears to bundle a wider product set around anesthesia monitoring without clearly separating hardware-only revenue from supporting software, services, or broader anesthesia workstation value in all regions. |

| Research Firm B | USD 3.10 B (2025) | Takes a different base year and may include integrated workstations more broadly as complete anesthesia platforms, which can pull in adjacent delivery components rather than counting only the monitoring-focused hardware. |

Across the three figures, most of the spread comes from what is included in an integrated system and how the base year is chosen. By keeping scope tight to new monitoring hardware and then cross-checking results against procedure-led demand and replacement behavior, the estimate stays easier to trace and update in a repeatable way.

Key Questions Answered in the Report

What is the current size of the anesthesia monitoring devices market?

The anesthesia monitoring devices market is valued at USD 3.2 billion in 2026 and is projected to reach USD 5.12 billion by 2031.

Which product segment leads the anesthesia monitoring devices market?

Integrated anesthesia workstations hold 40.72% share, making them the leading product category.

Why are ambulatory surgery centers important for future growth?

ASCs are expanding at 10.48% CAGR because payers favor cost-effective outpatient procedures, driving demand for portable monitors.

Which region shows the fastest market growth?

Asia-Pacific posts the highest CAGR at 10.69% through 2031, propelled by localization policies in China and India

How is artificial intelligence influencing anesthesia monitoring?

AI tools such as the Hypotension Prediction Index enable predictive alerts that reduce intraoperative complications and support precision anesthesia.

What are the main restraints facing the market?

High capital costs and a global shortage of trained anesthesiologists limit advanced device adoption, especially in developing regions.

Page last updated on: