Analytical Instrumentation In Life Science Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

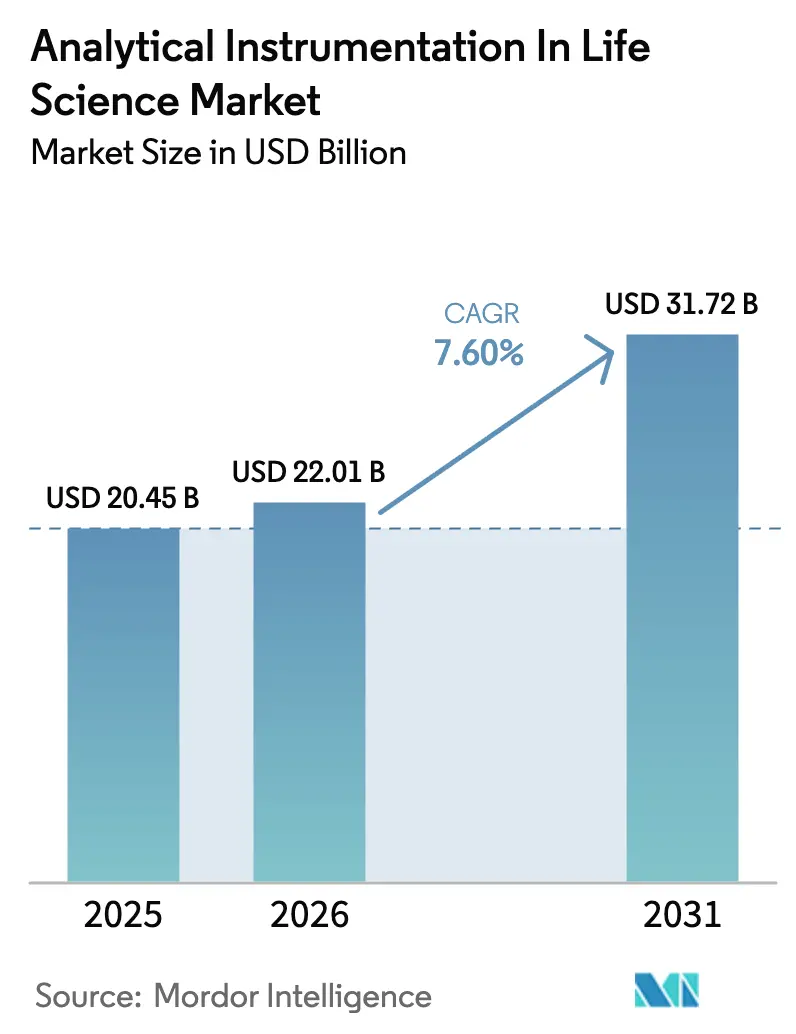

| Market Size (2026) | USD 22.01 Billion |

| Market Size (2031) | USD 31.72 Billion |

| Growth Rate (2026 - 2031) | 7.60% CAGR |

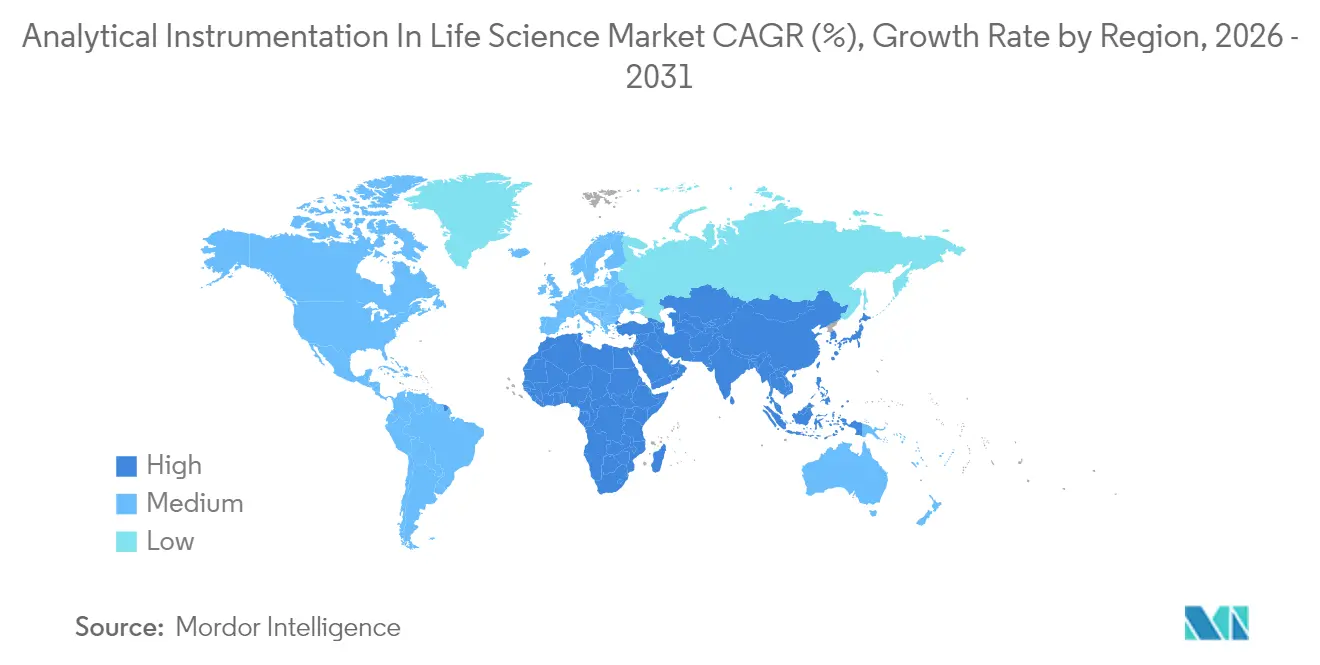

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

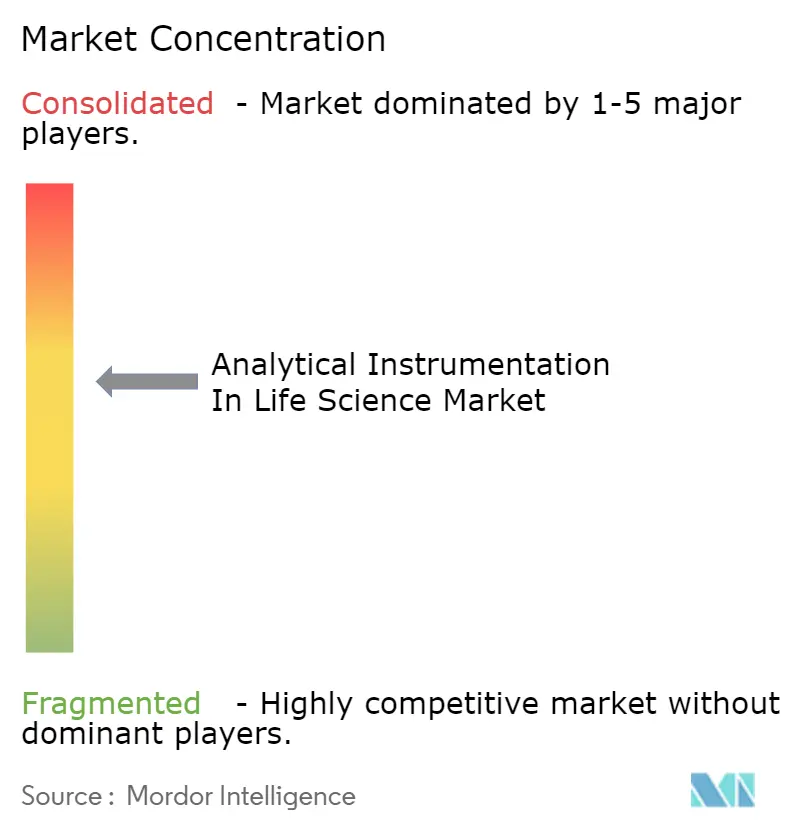

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analytical Instrumentation In Life Science Market Analysis by Mordor Intelligence

The analytical instrumentation in life science market size is expected to grow from USD 20.45 billion in 2025 to USD 22.01 billion in 2026 and is forecast to reach USD 31.72 billion by 2031 at 7.60% CAGR over 2026-2031. Heightened biologics development, stricter regulatory expectations for real-time process control, and accelerating precision-medicine programs are the primary engines behind this expansion.[1]FDA, “Content and Review of CMC Information for Human Somatic Cell Therapy INDs,” fda.gov Growing demand for high-resolution mass spectrometry, chromatography innovations that support continuous manufacturing, and artificial-intelligence-powered data analytics continue to widen the application scope of next-generation instruments. Asia-Pacific records the fastest uptake as regional CDMOs standardize high-throughput screening, while North America capitalizes on its established R&D infrastructure to maintain value leadership.[2]ISPE, “Navigating the Asia Pacific Pharmaceutical Landscape for Global Impact,” ispe.org Competitive activity is typified by scale-building acquisitions that bundle instruments, software, and consumables into integrated workflow solutions.

Key Report Takeaways

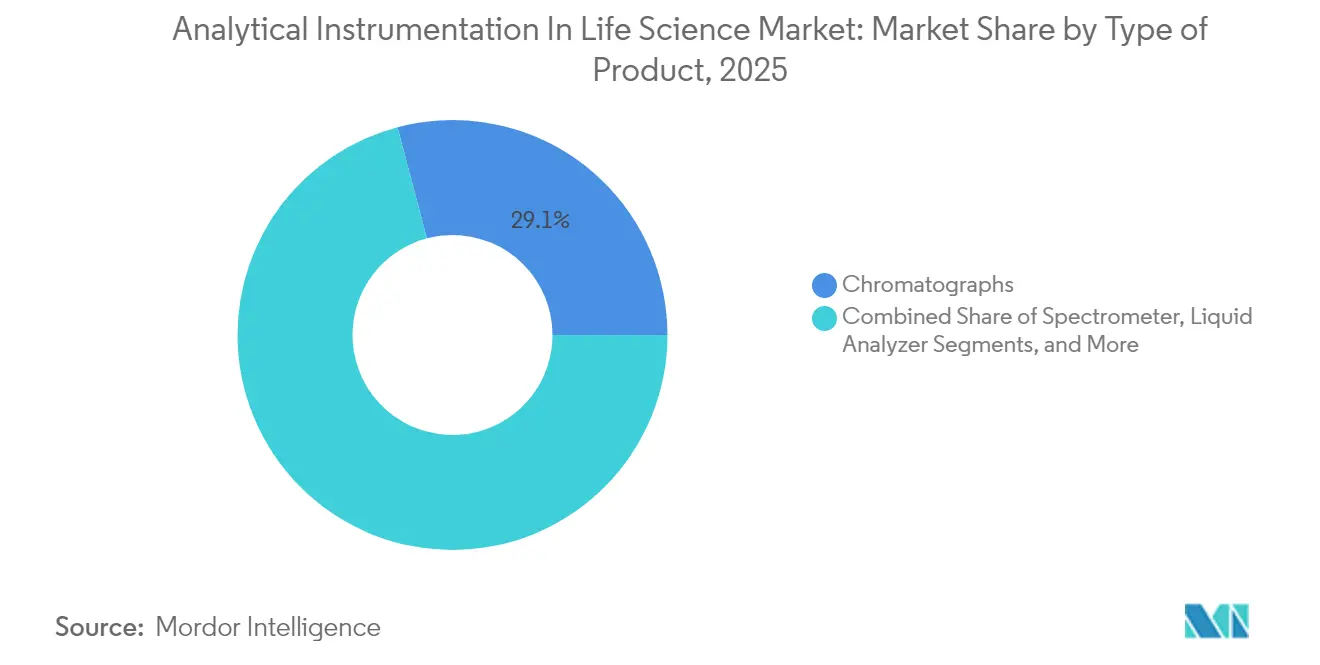

- By product type, chromatographs led with 29.12% revenue share in 2025, while spectrometers are tracking the highest 8.06% CAGR through 2031.

- By end-user, the pharmaceutical segment held 59.35% of the analytical instrumentation in life science market share in 2025; biopharmaceutical and nutraceutical applications are advancing at a 8.74% CAGR.

- By geography, North America commanded 38.95% revenue in 2025, whereas Asia-Pacific is projected to expand at a 9.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Analytical Instrumentation In Life Science Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Demand of Analytical Instrumentation in Pharmaceutical Industry | +1.8% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Expansion of Cell and Gene Therapy Pipeline Necessitating High-Resolution Characterization | +1.5% | North America & EU core, expanding to APAC | Long term (≥ 4 years) |

| Regulatory Push for In-Line Process Analytical Technology (PAT) in Continuous Manufacturing | +1.2% | Global, led by FDA and EMA jurisdictions | Medium term (2-4 years) |

| Growing Public-Private Funding in Omics and Biomarker Research | +1.0% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Rising Potency of Novel Drug Modalities Requiring Ultra-Sensitive Detection | +0.9% | Global, concentrated in major pharma hubs | Medium term (2-4 years) |

| Accelerated Adoption of High-Throughput Screening by Asian CDMOs | +0.7% | APAC core, spill-over to global supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in demand for analytical instrumentation in pharmaceutical manufacturing

The FDA’s 2025 update to 21 CFR 211.110 formalizes expectations for continuous processing, elevating process-analytical-technology (PAT) systems from optional enhancements to essential control tools. Harmonized ICH Q2(R2) and Q14 guidelines allow platform methods to be validated across multiple products, shrinking timelines and creating sustained pull for multi-attribute chromatography and mass-spectrometry solutions. Manufacturers now rely on real-time attribute measurements to release batches in hours rather than days, a shift that materially increases the installed base of high-performance instruments across development and commercial sites.

Expansion of cell and gene therapy pipeline

Regulators now highlight empty-capsid control and post-translational-modification monitoring as critical quality attributes for viral vectors, pushing biopharma firms toward orbitrap-class mass spectrometry and high-resolution chromatography.[3]BioProcess International, “Measure Twice, Treat Once: Assay Development in CGT,” bioprocessintl.com Samsung Biologics reduced protein variant analysis from 6-8 weeks to 1-2 weeks by integrating LC-MS/MS with multiplexed workflows, demonstrating the productivity gains attached to next-generation platforms. As global gene-therapy trials multiply, demand for sensitive, high-throughput characterization tools cements spectrometers as pivotal growth engines in the analytical instrumentation in life science market.

Regulatory push for in-line PAT in continuous manufacturing

Quality-by-design paradigms require real-time parameter monitoring; magnetic-sector MS and Raman spectroscopy are being embedded into bioreactors and solvent-recovery loops to guide instantaneous feedback control. Europe’s PIC/S alignment is now mirrored by Singapore and South Korea, enabling vendors to deliver standardized PAT suites across multiple jurisdictions, accelerating global market penetration.

Growing public-private funding in omics and biomarker research

Thermo Fisher’s USD 3.1 billion Olink acquisition underscores the commercial weight of high-throughput proteomics in precision medicine. AI-driven Raman spectroscopy maps tumor-immune microenvironments with single-cell resolution, confirming how machine learning augments instrument value and widens clinical utility. Robust funding pipelines drive labs to invest in multiplexed mass-spectrometry and imaging platforms that accommodate integrated genomics–proteomics workflows, reinforcing long-term equipment outlays.[4]CACLP, “Thermo Fisher Scientific Reports Q1 2025 Results,” caclp.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Cost | -1.4% | Global, particularly impacting emerging markets | Medium term (2-4 years) |

| Shortage of Skilled Analytical Chemists and Data Scientists | -1.1% | Global, acute in North America & EU | Long term (≥ 4 years) |

| Data Integrity and Validation Compliance Burden (ALCOA+ requirements) | -0.8% | Global, concentrated in regulated markets | Medium term (2-4 years) |

| Complex Preventive Maintenance Leading to Higher Downtime Costs | -0.6% | Global, affecting high-throughput facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High initial cost

Capital budgets remain tightly controlled; 64% of laboratories report difficulty approving new instrument purchases, and consumables can consume up to 80% of lifetime costs. Instrument-as-a-service models and shared-facility consortia are emerging to offset cash-flow barriers, while miniaturized handheld spectrometers projected to reach USD 4 billion by 2030 offer tailored, lower-priced alternatives for niche assays.[5]Spectroscopy Online, “Applications of Micro X-Ray Fluorescence Spectroscopy,” spectroscopyonline.com

Shortage of skilled analytical chemists and data scientists

The fusion of AI with analytical workflows demands hybrid skills that remain scarce; universities underutilize advanced mass-spectrometry equipment, leaving graduates underprepared for industry roles. Median analytical-chemist salaries stalled at USD 105,000 in 2024, prompting talent migration toward higher-paying tech sectors and sustaining a structural labor deficit. Vendors are countering with intuitive software and remote-support platforms, yet complex data interpretation still requires expert oversight, prolonging the skills bottleneck.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Product: Spectrometers drive innovation beyond traditional boundaries

The spectrometer category contributed USD 7.1 billion to the analytical instrumentation in life science market size in 2025 and is set to grow at an 8.06% CAGR through 2031. Liquid chromatographs preserved a 66.85% slice of chromatography revenue, but ion chromatographs now register 8.1% growth on the back of trace-impurity testing mandates. Orbitrap Astral Zoom debuted in 2025 with 35% faster scan rates, enabling real-time peptide-mapping of complex biologics and cementing high-resolution MS as the preferred platform for cell-therapy analytics. Gas-chromatography vendors respond to helium shortages by integrating hydrogen-safety interlocks and nitrogen-switch kits, limiting carrier-gas costs for QC labs. Micro-XRF instruments gain traction for non-destructive elemental mapping in controlled-release tablet coatings, extending their reach beyond traditional materials science. Novel gas analyzers oriented toward bioprocess monitoring now post 8.92% annual growth, reflecting the shift toward continuous biomanufacturing workflows that rely on in-line CO₂ and O₂ analytics.

Second-generation spectrometers further reduce acquisition costs per data point, widening adoption in mid-tier firms without diluting analytical power. As instrument throughput rises, consumable vendors bundle ultralow-void columns and high-capacity trapping cartridges, creating a holistic ecosystem that enhances vendor lock-in. The analytical instrumentation in life science market therefore benefits from hardware, software, and reagent co-development that optimizes complete workflows rather than isolated instrument performance.

By End User Vertical: Biopharmaceuticals reshape analytical requirements

The pharmaceutical segment captured 59.35% revenue in 2025, but biopharmaceutical manufacturing is projected to outpace it, expanding at 8.74% CAGR and lifting the collective analytical instrumentation in life science market size for biologics to USD 13.42 billion by 2031. API producers still account for 63.15% of pharmaceutical purchases, yet outsourcing to contract development and manufacturing organizations (CDMOs) is accelerating at 9.68%, creating distributed demand across North American and Asian service hubs.

WuXi Biologics expanded Worcester capacity to 36,000 liters, underlining the scale of analytical demand embedded in multiproduct biologics sites. Samsung Biologics’ 784,000-liter campus exemplifies how mega-facilities integrate hundreds of chromatography, spectroscopy, and in-line PAT stations to maintain consistent viral-vector output. Nutraceutical producers increasingly adopt pharmaceutical-grade validation, leveraging mid-range LC-MS and FT-IR instruments for ingredient authentication and micro-contaminant surveillance. The convergence of end-user requirements encourages platform instrument designs that deliver compliance flexibility across a spectrum of therapeutic and wellness products.

Geography Analysis

North America retained 38.95% of 2025 revenue behind its advanced biomanufacturing infrastructure and earliest adoption of continuous-processing guidance. The region’s regulatory rigor drives consistent upgrades to high-resolution instruments, and domestic stimulus packages direct USD-scale investments toward on-shore manufacturing resilience.

Asia-Pacific is the fastest-growing territory, operating at a 9.03% CAGR to 2031 as CDMOs scale capacity and governments offer tax incentives for single-use bioreactors and PAT equipment. India’s generics sector and Singapore’s biologics corridor draw multinational firms that demand standardized QC platforms compatible with global filings, lifting the analytical instrumentation in life science market across the region. China’s CRO industry exceeded CNY 64.77 billion in 2023 and continues to import premium LC-MS and UHPLC systems to service complex molecule pipelines.

Europe holds steady growth as PIC/S alignment simplifies multinational instrument validation. Waters’ USD 45 million Longbridge plant triples local orbitrap component capacity, underscoring sustained European demand for precision manufacturing inputs. South America is an emerging buyer base; Shimadzu’s Mexico subsidiary seeks 150% sales growth by 2028, signalling regional appetite for tier-one instruments. Middle East and Africa remain early-stage but attract pilot-scale investments tied to vaccine self-sufficiency programs, foreshadowing incremental instrument shipments aligned to GMP facility buildouts.

Competitive Landscape

The analytical instrumentation in life science market is moderately consolidated; the top five suppliers control 49% of 2024 global revenue, with Thermo Fisher holding 23%. Multi-year acquisition pipelines aim to secure integrated software, consumables, and services that elevate switching costs. Thermo Fisher’s USD 4.1 billion purchase of Solventum’s purification unit extends its downstream-processing footprint and reinforces cross-selling of chromatography and filtration consumables. Agilent’s USD 925 million BioVectra buy-out strengthens the firm’s RNA-based therapeutics service offering, pairing sample-prep instrumentation with custom manufacturing capacity.

Waters, Danaher, and Bruker focus on differentiated high-resolution MS, GC-MS, and FT-IR systems, embedding AI-driven analytics to boost operator productivity. Waters’ BioResolve Protein A column achieves 7× sensitivity gains, underscoring how consumables innovation supports hardware competitiveness. Bruker integrates DART ionization for faster therapeutic-drug monitoring, broadening clinical applicability of its timsTOF platform. Medium-sized specialists leverage modular designs to serve niche workflows such as in-line gas analysis and mini-XRF food testing, cultivating defensible positions despite scale disadvantages.

Platform-level digital ecosystems emerge as the next battleground. Vendors that couple secure cloud data lakes with predictive-maintenance algorithms create visible ROI for labs facing skilled-labor shortages. Continuous expansion of subscription-based software revenue shields margin in an environment where instrument hardware is incrementally commoditizing.

Analytical Instrumentation In Life Science Industry Leaders

Agilent Technologies

Thermo Fisher Scientific

Waters Corporation

Bruker Corporation

Shimadzu Scientific

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Thermo Fisher unveiled Orbitrap Astral Zoom and Orbitrap Excedion Pro, increasing scan speeds by 35% and multiplexing by 50%, targeting biopharma and omics workflows.

- June 2025: Waters introduced BioResolve Protein A columns with MaxPeak Premier to boost antibody-titer sensitivity 7× and enable aggregate analyses.

- June 2025: Bruker showcased DART integration and timsMetabo for PFAS detection, expanding routine clinical and environmental applications.

- April 2025: Thermo Fisher committed USD 2 billion to U.S. innovation, allotting USD 500 million to R&D for next-generation analytical platforms.

- April 2025: QIAGEN outlined three sample-prep instrument launches by 2026 to enhance lab automation and reduce plastic waste

- February 2025: Thermo Fisher agreed to acquire Solventum’s purification and filtration business for USD 4.1 billion, aiming for mid-to-high single-digit organic growth.

Global Analytical Instrumentation In Life Science Market Report Scope

Analytical instrumentation in the life science industry helps analyze the materials, establish the composition, quality control, drug discovery, and research and development. The scope of the study includes the revenue accrued from the sale of various types of analytical instruments for various applications in the life sciences industry. This segment includes industries such as pharmaceuticals and biopharmaceuticals - establishments engaged in manufacturing medicinal and pharmaceutical products.

The analytical instrumentation market in the lifesciences industry is segmented by type of product (chromatographs, spectrometer (mass, elemental analysis, and molecular analysis), gas analyzer, liquid analyzer, and analytical x-ray instrumentation and analytical microscopes), end-user vertical (the biopharmaceutical and nutraceutical, and pharmaceutical) and geography (North America, Europe, Asia-Pacific, Rest of the World). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Chromatographs | Gas Chromatographs (GC) | |

| Liquid Chromatographs (HPLC, UHPLC) | ||

| Ion Chromatographs | ||

| Spectrometer (Mass, Elemental Analysis and Molecular Analysis) | Mass Spectrometry | LC-MS |

| GC-MS | ||

| MALDI-TOF | ||

| Elemental Analysis | ICP-MS | |

| ICP-OES | ||

| Molecular Analysis | FT-IR | |

| Raman | ||

| UV-Vis | ||

| Gas Analyzer | Laser-Based Gas Analyzers | |

| Electrochemical Gas Analyzers | ||

| Photoacoustic Gas Analyzers | ||

| Liquid Analyzer | pH/ORP Analyzers | |

| Dissolved Oxygen (DO) Analyzers | ||

| Conductivity and Total Organic Carbon (TOC) Analyzers | ||

| Analytical X-ray Instrumentation and Analytical Microscopes | X-ray Diffraction (XRD) | |

| X-ray Fluorescence (XRF) | ||

| Electron Microscopes (SEM, TEM) | ||

| Atomic Force Microscopes (AFM) | ||

| Biopharmaceutical and Nutraceutical | Biologics Manufacturers |

| Nutraceutical Producers | |

| Pharmaceutical | Active Pharmaceutical Ingredient (API) Manufacturers |

| Contract Research and Manufacturing Organizations (CROs/CDMOs) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Type of Product | Chromatographs | Gas Chromatographs (GC) | |

| Liquid Chromatographs (HPLC, UHPLC) | |||

| Ion Chromatographs | |||

| Spectrometer (Mass, Elemental Analysis and Molecular Analysis) | Mass Spectrometry | LC-MS | |

| GC-MS | |||

| MALDI-TOF | |||

| Elemental Analysis | ICP-MS | ||

| ICP-OES | |||

| Molecular Analysis | FT-IR | ||

| Raman | |||

| UV-Vis | |||

| Gas Analyzer | Laser-Based Gas Analyzers | ||

| Electrochemical Gas Analyzers | |||

| Photoacoustic Gas Analyzers | |||

| Liquid Analyzer | pH/ORP Analyzers | ||

| Dissolved Oxygen (DO) Analyzers | |||

| Conductivity and Total Organic Carbon (TOC) Analyzers | |||

| Analytical X-ray Instrumentation and Analytical Microscopes | X-ray Diffraction (XRD) | ||

| X-ray Fluorescence (XRF) | |||

| Electron Microscopes (SEM, TEM) | |||

| Atomic Force Microscopes (AFM) | |||

| By End User Vertical | Biopharmaceutical and Nutraceutical | Biologics Manufacturers | |

| Nutraceutical Producers | |||

| Pharmaceutical | Active Pharmaceutical Ingredient (API) Manufacturers | ||

| Contract Research and Manufacturing Organizations (CROs/CDMOs) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the analytical instrumentation in life science market?

The analytical instrumentation in life science market reached USD 22.01 billion in 2026 and is projected to expand to USD 31.72 billion by 2031.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing region, posting a 9.03% CAGR through 2031 due to expanding CDMO capacity and government incentives.

Which product segment shows the highest growth?

Spectrometers, particularly high-resolution mass-spectrometry platforms, are forecast to grow at an 8.06% CAGR through 2031 as biologics characterization needs intensify.

Who are the leading companies in this market?

Thermo Fisher Scientific leads with 23% revenue share, followed by Agilent Technologies, Waters Corporation, Danaher, and Bruker.

How is regulation influencing instrument demand?

Stricter FDA and EMA guidance on continuous manufacturing and PAT drives real-time analytical adoption, boosting demand for in-line chromatography and mass-spectrometry systems.

What key challenge could slow market growth?

High capital expenditure and a shortage of skilled analytical chemists remain significant barriers, potentially curbing instrument deployment in resource-constrained settings.

Page last updated on: