Europe Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

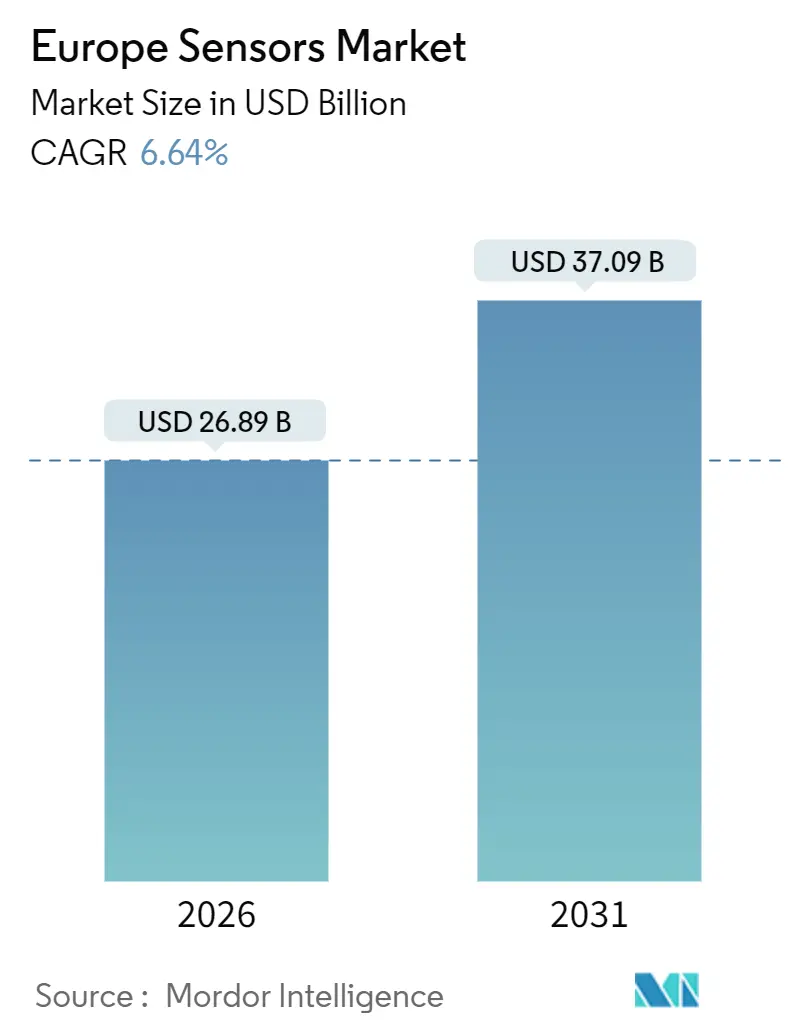

| Market Size (2026) | USD 26.89 Billion |

| Market Size (2031) | USD 37.09 Billion |

| Growth Rate (2026 - 2031) | 6.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Sensors Market Analysis by Mordor Intelligence

The Europe sensors market size stood at USD 26.89 billion in 2026 and is projected to reach USD 37.09 billion by 2031, advancing at a 6.64% CAGR during 2026-2031. A sustained policy push to digitize infrastructure, stricter emissions-reporting rules, and the automotive sector’s rapid electrification are moving sensors from discretionary add-ons to mandatory design wins. Edge-AI processing is gaining favor because it addresses GDPR-related data-sovereignty concerns, trimming cloud costs and latency. Reshoring incentives in the European Chips Act are encouraging domestic fabs, yet near-term supply remains tight, prompting design teams to dual-source analog front ends. LiDAR modules priced below USD 1,000 are expanding beyond passenger vehicles into warehouse robots, while MEMS investment cycles are shortening as Bosch and STMicroelectronics ramp 300-millimeter capacity. These shifts collectively underpin mid-single-digit growth even as legacy process-control and consumer-electronics avenues mature.

Key Report Takeaways

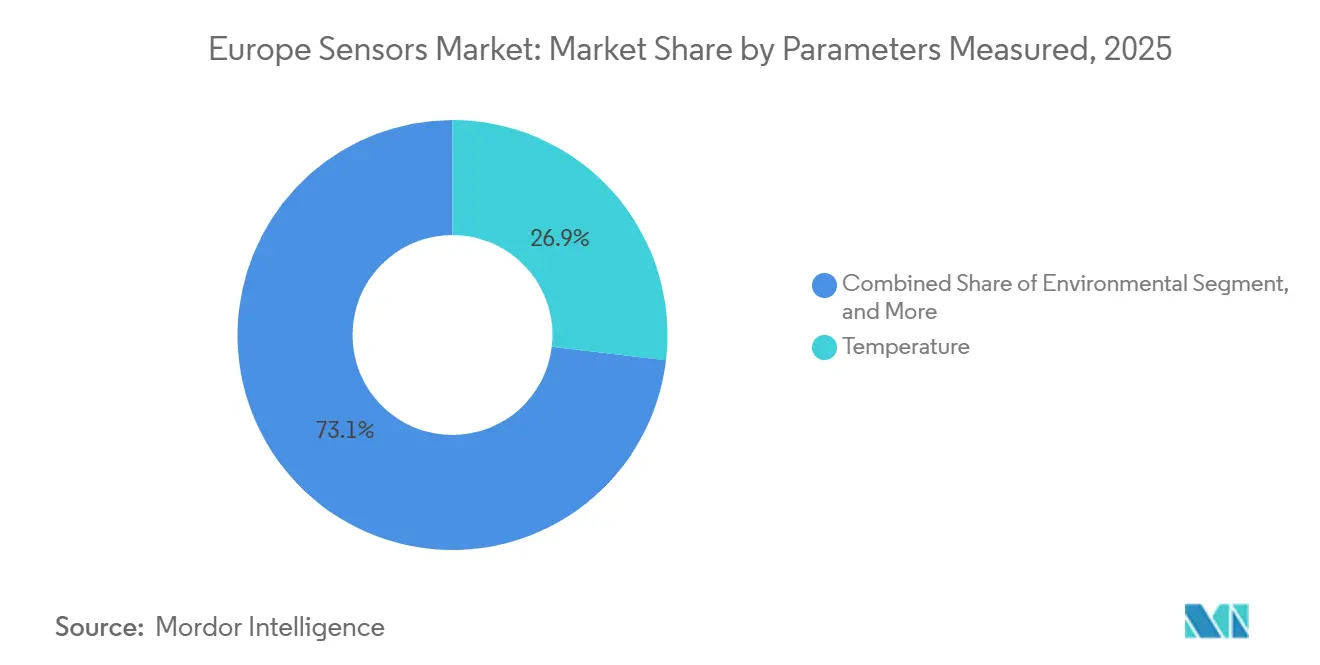

- By parameters measured, temperature sensors commanded 26.87% of Europe sensors market share in 2025, while environmental sensors are poised to grow at an 8.61% CAGR through 2031.

- By mode of operation, optical sensors led with 19.16% revenue share in 2025; LiDAR modules are projected to expand at an 8.43% CAGR to 2031.

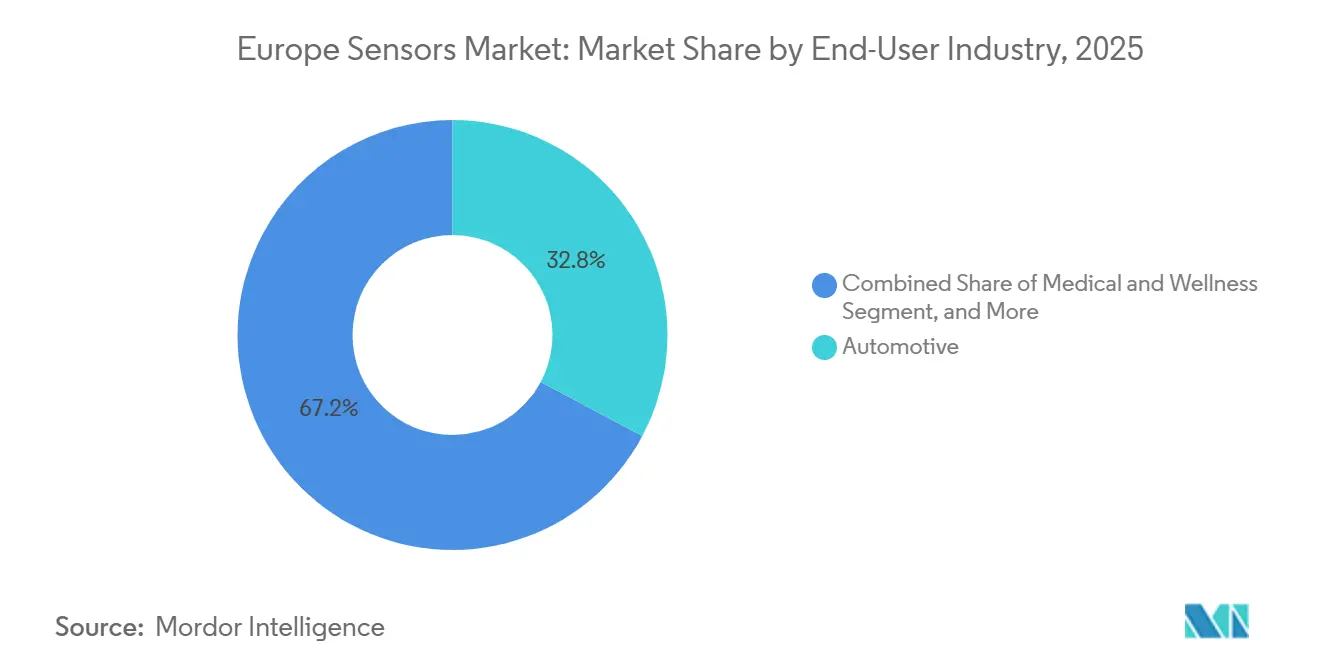

- By end-user industry, automotive applications accounted for 32.78% of demand in 2025, whereas medical and wellness deployments are advancing at an 8.26% CAGR through 2031.

- By sensor technology, MEMS devices captured 53.44% of the Europe sensors market in 2025 and are forecast to grow at a 6.83% CAGR through 2031.

- By geography, Germany accounted for 27.89% of the Europe sensors market in 2025, while Poland is projected to register an 8.29% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global valuation is built by aggregating outputs from multiple regions, with Europe forming one of the important contributors. Mordor Intelligence's global sensors market size report represents that cumulative total.

Europe Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand in Automotive Sector | +1.8% | Germany, France, Italy, Spain | Medium term (2-4 years) |

| Proliferation of Industry 4.0 Smart Factories | +1.5% | Germany, Netherlands, Poland | Long term (≥ 4 years) |

| Acceleration of Electric-Vehicle Adoption | +1.2% | Germany, United Kingdom, France, Netherlands | Medium term (2-4 years) |

| Rapid Uptake of Industrial IoT Edge-AI Sensors | +1.1% | Germany, United Kingdom, France | Long term (≥ 4 years) |

| Mandatory EU Climate-Monitoring Regulations | +0.7% | Pan-European | Short term (≤ 2 years) |

| Growth of Smart Infrastructure (Rail, Energy) | +0.6% | Germany, France, United Kingdom, Spain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand in the Automotive Sector

European automakers integrated 150-200 sensors per 2026 model, up from roughly 100 in 2020, a jump driven by Euro NCAP protocols that make advanced driver-assistance systems standard fitment.[1]Euro NCAP, “2025 Protocols Elevate ADAS to Standard Fitment,” euroncap.com Radar, ultrasonic, and camera arrays dominate the bill of materials, yet cost-reduced solid-state LiDAR, such as Valeo’s SCALA 3 at sub-USD 1,000, has begun enabling Level 3 highway autonomy. Additional content stems from battery-management sensors monitoring thermal runaway in 800-volt packs. Continental’s 2025 acquisition of silicon carbide signals vertical integration in high-temperature current sensing. Together, these trends lift unit volumes and average selling prices, reinforcing the growth trajectory of the Europe sensors market.

Proliferation of Industry 4.0 Smart Factories

More than 2 million industrial IoT nodes were deployed in 2025, each bundling 3-5 sensors for vibration, temperature, and energy data.[2]European Commission, “Digital Europe Program IoT Node Statistics,” digital-strategy.ec.europa.eu Predictive maintenance reduces unplanned downtime by up to 30%, justifying retrofit costs within 2 years. Siemens’ Xcelerator platform posted 40% annual growth in connected assets as tier-one suppliers demanded real-time quality traceability. The pivot to edge inference boosts demand for smart sensors with 16-bit ADCs and on-board DSPs, typified by Bosch Sensortec’s BHI360 launch in October 2025. These deployments underpin long-run demand visibility for the Europe sensors market.

Acceleration of Electric-Vehicle Adoption

Registrations of battery-electric vehicles climbed to 2.8 million units in 2025, up 35% year on year, following tightening fleet-average CO₂ penalties.[3]ACEA, “Battery-Electric Vehicle Registrations 2025,” acea.auto Each EV uses 30-50 incremental sensors, spanning high-voltage current shunts to coolant-flow meters. STMicroelectronics reported a 28% spike in automotive-sensor revenue in 2025, driven by supplying VN9D30Q8F drivers for inductive position sensing. Hall-effect devices with 1,500-volt isolation are becoming standard as premium brands shift to 800-volt powertrains. These dynamics raise the sensor-content ceiling and help sustain a robust outlook for the Europe sensors market.

Rapid Uptake of Industrial IoT Edge-AI Sensors

Roughly 1.2 million edge-AI nodes capable of local neural network inference were installed in 2025, especially in pharma and aerospace plants that restrict cloud uploads for sovereignty and latency reasons. Texas Instruments’ MSPM0 MCU enables 10-year coin-cell operation, illustrating the power-budget breakthroughs fueling adoption. NXP’s i.MX RT1180 crossover processor brings 0.5 TOPS NPU performance into defect-inspection cameras. Demand for co-packaged sensors with retrainable AI cores positions MEMS suppliers to capture recurring software value, bolstering the revenue base of the Europe sensors market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Integration Costs | -0.9% | Southern and Eastern Europe | Short term (≤ 2 years) |

| Semiconductor Supply-Chain Disruptions | -0.7% | Pan-European | Medium term (2-4 years) |

| Skills Gap in Sensor Fusion Engineering | -0.5% | Germany, France, United Kingdom | Long term (≥ 4 years) |

| GDPR-Driven Data-Governance Complexity | -0.3% | Pan-European | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Integration Costs

Retrofitting legacy equipment costs EUR 5,000-15,000 per asset, a hurdle for SMEs operating on sub-10% margins. Integration fees for ERP mapping range from EUR 50,000 to EUR 100,000, stretching payback timelines. Pressure and temperature loops often remain analog, forcing either rip-and-replace or edge-digitization middleware. Endress+Hauser’s Heartbeat Technology is gaining traction as a cost-effective compromise that defers capital replacement. Until hardware prices drop further, cost sensitivities will curb uptake and slightly temper the Europe sensors market CAGR.

Semiconductor Supply-Chain Disruptions

Lead times for automotive-grade MCUs were still 26-40 weeks in early 2026, versus 12-16 weeks pre-2020. Mature-node fabs run at full allocation, delaying sensor-module builds and inflating prices by 15-25%. GlobalFoundries’ EUR 2 billion Dresden expansion will not be completed until 2027, and the ESMC joint venture will only begin pilot production in late 2027. The resulting volatility forces manufacturers to build buffer inventory, tying up working capital and marginally dragging on the growth of the Europe sensors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Parameters Measured: Environmental Sensors Capitalize on Emissions Mandates

Environmental devices are forecast to grow at 8.61% during 2026-2031 as the Corporate Sustainability Reporting Directive phases in third-party-verified Scope 1-3 disclosures. The Europe sensors market for this sub-segment is expanding rapidly because particulate-matter, NOx, and VOC analyzers now feed continuous-emissions-monitoring systems across chemical and metallurgical sites. Satellite feedback from ESA’s Sentinel-5, launched in August 2025, improves ground-station calibration and extends sensor life. Temperature sensors, at 26.87% share in 2025, remain indispensable in custody-transfer flows across energy and food processing. Flow instruments are rising as utilities deploy smart meters to spot leaks, while proximity sensors meet IEC 61496 redundancy rules in collaborative robots.

Combination modules that measure temperature, humidity, and pressure in a single package reflect a trend toward convergence that rewards suppliers skilled in multi-chip packaging. Chemical sensors are moving from niche to mainstream as pharmaceutical bioreactors demand real-time glucose and pH monitoring. Magnetic sensors embedded in brushless DC motors continue to proliferate as industrial electrification advances. Overall, diversified use cases ensure the parameters-measured category remains a steady volume driver within the Europe sensors market.

By Mode of Operation: LiDAR Modules Disrupt Optical Dominance

Optical devices retained a 19.16% share in 2025, driven by safety curtains, fiber-optic strain sensors, and spectrometry modules. However, solid-state LiDAR is tracking an 8.43% CAGR as sub-USD 500 pricing opens warehouse automation and agricultural machinery opportunities. Electrical-resistance sensors like thermistors continue to serve legacy HVAC and force applications but face a margin squeeze. Biosensors for glucose and lactate now achieve clinical accuracy in handhelds, setting the stage for multi-analyte wearables. Capacitive and piezoelectric sensors serve touch and ultrasonic applications, though growth is modest given the technology's maturity.

Radar, both 24 GHz short-range and 77 GHz long-range, remains standard in blind-spot and adaptive-cruise systems, with NXP and Infineon leading chipset supply. As autonomous platforms demand redundancy, perception stacks increasingly fuse camera, radar, and LiDAR data, thereby increasing the need for synchronized, time-stamped outputs. Suppliers offering turnkey sensor suites enjoy a competitive edge in the Europe sensors market.

By End-User Industry: Medical and Wellness Outpaces Automotive

Medical and wellness deployments are pacing at an 8.26% CAGR because national health systems now reimburse remote patient monitoring solutions. Movesense’s MD-grade ECG module showcases how Bluetooth-enabled wearables stream 3-lead data for arrhythmia detection without clinical supervision. Consumer trust rose after a 2025 peer review validated sub-3% error rates with hospital-grade devices. Automotive, despite holding a 32.78% share in 2025, is entering an optimization phase as OEMs consolidate sensors into zonal architectures to manage their bill of materials.

Energy utilities deploy voltage and current sensors to stabilize grids as they move toward 40% renewables by 2030. Industrial actors embrace vibration and temperature probes for predictive maintenance, while construction and agriculture see sporadic adoption tied to regional connectivity gaps. Defense and aerospace remain high-value niches immune to consumer-cycle volatility. Together, these verticals diversify demand and reinforce resilience in the Europe sensors market.

By Sensor Technology: MEMS Consolidates Leadership

MEMS claimed 53.44% of the Europe sensor market share in 2025 and is projected to grow at a 6.83% CAGR as 300-millimeter fabs, such as Bosch’s Dresden plant, add 30% capacity. Silicon micromachining now spans microphones, gas sensors, and micro-mirror arrays, lowering unit costs under USD 1 for high-volume lines. STMicroelectronics is co-developing MEMS ultrasonic sensors for Euro NCAP’s 2026 child-presence mandate, underscoring automotive pull-through. Hybrid MEMS-quartz modules target navigation-grade inertial guidance in GPS-denied zones, widening application scope.

As integration tightens among mechanical structures, analog conditioning, and edge ML, MEMS vendors are poised to extract greater value from software ecosystems tied to the Europe sensors market.

Geography Analysis

Germany captured 27.89% of the Europe sensors market in 2025, buoyed by the automotive triad, which ordered more than 500 million sensors for vehicle production and aftermarket service. Bosch’s new wafer fab and Siemens’ Xcelerator rollouts strengthen local ecosystems, while universities provide a steady stream of engineering talent. The United Kingdom and France leverage aerospace clusters where Rolls-Royce embeds 10,000 sensors per Trent XWB engine, and Thales integrates millimeter-wave radar into air-traffic networks. Italy and Spain focus on smart-grid and renewable energy deployments, but lag behind Germany in automation penetration.

Poland is expected to log an 8.29% CAGR through 2031, the fastest in the bloc, after Intel’s USD 2.1 billion packaging plant and L3Harris’s sensor assembly site both opened in 2025. The Netherlands’ Eindhoven corridor hosts over 50 photonics startups commercializing coherent LiDAR and integrated spectrometers, reinforcing regional specialization. While EU Chips Act subsidies total EUR 43 billion, new fabs will not meaningfully ease supply until 2027, leaving short-run allocations tight.

Eastern European nations attract greenfield plants through labor arbitrage and proximity to Western OEMs, yet Germany’s incumbency in automotive engineering remains difficult to replicate. Reshoring favors suppliers co-locating packaging near fabs for traceability, an increasingly stringent requirement in safety-critical sectors. Collectively, geographic dynamics diversify revenue streams and lower systemic risk in the Europe sensors market.

Coverage of the sensors market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Asia, alongside detailed country-level intelligence for China, Japan, South Korea, Taiwan, and United States, each shaped by local operating conditions.

Competitive Landscape

The top five suppliers, Bosch, Siemens, STMicroelectronics, Infineon, and TE Connectivity, command roughly a 35-40% share, indicating moderate concentration within the Europe sensors market. Bosch is injecting EUR 3 billion into Dresden to build 300-millimeter MEMS capacity, while Siemens has folded edge-gateway software into its Xcelerator stack to provide sensor-to-cloud continuity. Specialists such as Sick AG and Pepperl+Fuchs thrive in safety-rated proximity and explosion-proof niches that larger players overlook.

Technology leadership is trending toward embedded intelligence; ABB’s Ability platform registered 25% growth in connected industrial assets during 2025 by pairing sensors with digital twins. Patent filings for MEMS microphones, capacitive fingerprint readers, and time-of-flight imaging rose 12% in 2025, underlining the importance of IP portfolios. Compliance with the forthcoming EU AI Act nudges vendors to adopt explainable-AI firmware, increasing software R&D overhead but offering a differentiation path.

White-space opportunities include sub-USD 500 solid-state LiDAR, continuous metabolic biosensors, and emissions-grade environmental modules. Startups bundle pre-calibrated sensors with firmware, lowering integration barriers for customers lacking in-house sensor-fusion talent. As software differentiation eclipses hardware alone, partnerships between chipmakers and algorithm vendors will shape future competitive positioning in the Europe sensors market.

Europe Sensors Industry Leaders

Texas Instruments Incorporated

TE Connectivity Ltd

Honeywell International Inc.

Rockwell Automation Inc.

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: L3Harris inaugurated a USD 120 million sensor-assembly facility in Katowice, Poland, to supply infrared imaging modules and millimeter-wave radar components for NATO programs.

- August 2025: The European Space Agency launched Sentinel-5, carrying a hyperspectral imager that provides 7 km spatial-resolution pollutant data for sensor calibration.

- June 2025: Valeo rolled out the SCALA 3 LiDAR at sub-USD 1,000 bill-of-materials cost, enabling Level 3 highway automation for a German premium OEM.

- May 2025: STMicroelectronics partnered with a European tier-1 supplier to co-develop MEMS ultrasonic sensors for in-cabin child-presence detection.

Europe Sensors Market Report Scope

The Europe Sensors Market Report is Segmented by Parameters Measured (Temperature, Pressure, Level, Flow, Proximity, Environmental, Chemical, Inertial, Magnetic, Vibration), Mode of Operation (Optical, Electrical Resistance, Biosensor, Piezoresistive, Image, Capacitive, Piezoelectric, LiDAR, Radar), End-User Industry (Automotive, Consumer Electronics, Energy, Industrial, Medical and Wellness, Construction, Agriculture and Mining, Aerospace, Defense), Sensor Technology (MEMS, Non-MEMS), and Geography (Germany, United Kingdom, France, Italy, Spain, Netherlands, Poland, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Temperature |

| Pressure |

| Level |

| Flow |

| Proximity |

| Environmental |

| Chemical |

| Inertial |

| Magnetic |

| Vibration |

| Optical |

| Electrical Resistance |

| Biosensor |

| Piezoresistive |

| Image |

| Capacitive |

| Piezoelectric |

| LiDAR |

| Radar |

| Automotive |

| Consumer Electronics |

| Energy |

| Industrial |

| Medical and Wellness |

| Construction, Agriculture and Mining |

| Aerospace |

| Defense |

| MEMS |

| Non-MEMS |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Poland |

| Rest of Europe |

| By Parameters Measured | Temperature |

| Pressure | |

| Level | |

| Flow | |

| Proximity | |

| Environmental | |

| Chemical | |

| Inertial | |

| Magnetic | |

| Vibration | |

| By Mode of Operation | Optical |

| Electrical Resistance | |

| Biosensor | |

| Piezoresistive | |

| Image | |

| Capacitive | |

| Piezoelectric | |

| LiDAR | |

| Radar | |

| By End-User Industry | Automotive |

| Consumer Electronics | |

| Energy | |

| Industrial | |

| Medical and Wellness | |

| Construction, Agriculture and Mining | |

| Aerospace | |

| Defense | |

| By Sensor Technology | MEMS |

| Non-MEMS | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe sensors market?

The market was valued at USD 26.89 billion in 2026 and is forecast to reach USD 37.09 billion by 2031.

Which segment is growing fastest within the market?

Environmental sensors lead growth at an 8.61% CAGR because EU emissions-reporting rules spur demand for particulate-matter and gas analyzers.

How large is automotive’s share in regional demand?

Automotive applications accounted for 32.78% of demand in 2025, reflecting continued electrification and ADAS uptake.

Why are MEMS sensors so dominant?

MEMS captured 53.44% share in 2025 due to scalable 300-millimeter wafer production that lowers costs and integrates on-board processing.

Which country will grow fastest through 2031?

Poland is projected to advance at an 8.29% CAGR, driven by new semiconductor packaging and sensor-assembly investments.

What supply-chain risk should buyers monitor?

Lead times for automotive-grade microcontrollers remain 26-40 weeks, keeping component availability the primary operational risk through 2027.

Page last updated on: