China Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

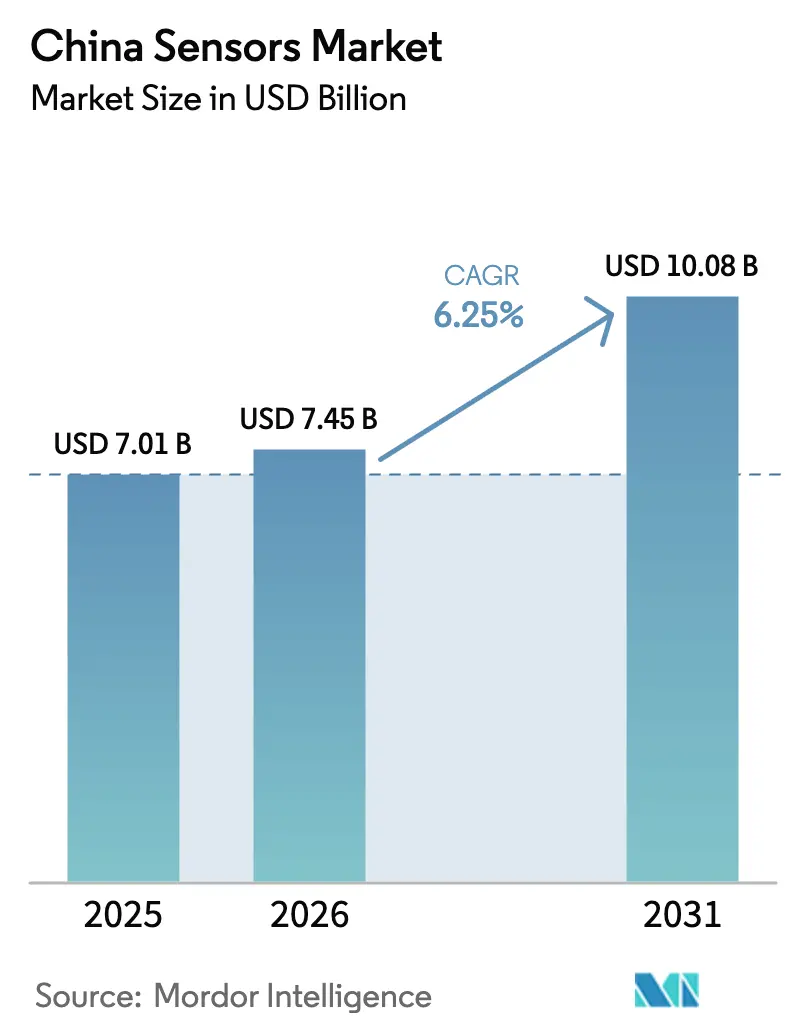

| Base Year Market Size (2025) | USD 7.01 Billion |

| Market Size (2026) | USD 7.45 Billion |

| Market Size (2031) | USD 10.08 Billion |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Sensors Market Analysis by Mordor Intelligence

China sensors market size in 2026 is estimated at USD 7.45 billion, growing from 2025 value of USD 7.01 billion with 2031 projections showing USD 10.08 billion, growing at 6.25% CAGR over 2026-2031. Unit shipments are projected to climb from 14.59 billion to 27.68 billion units over the same period, a 13.66% volume CAGR that underscores intensifying price pressure as production scales. Policy-driven localization, rapid electric-vehicle (EV) build-out, and large-scale consumer-electronics manufacturing continued to stimulate demand, while falling 8-inch MEMS wafer costs widened addressable end-markets. Competitive dynamics shifted as domestic suppliers leveraged government incentives, wafer cost advantages, and proximity to downstream assemblers to close technology gaps with multinational incumbents. Geographically, Pearl River Delta consumer-electronics clusters, Yangtze River Delta smart-manufacturing hubs, and Beijing-Tianjin-Hebei research corridors remained the three principal engines of growth.

Key Report Takeaways

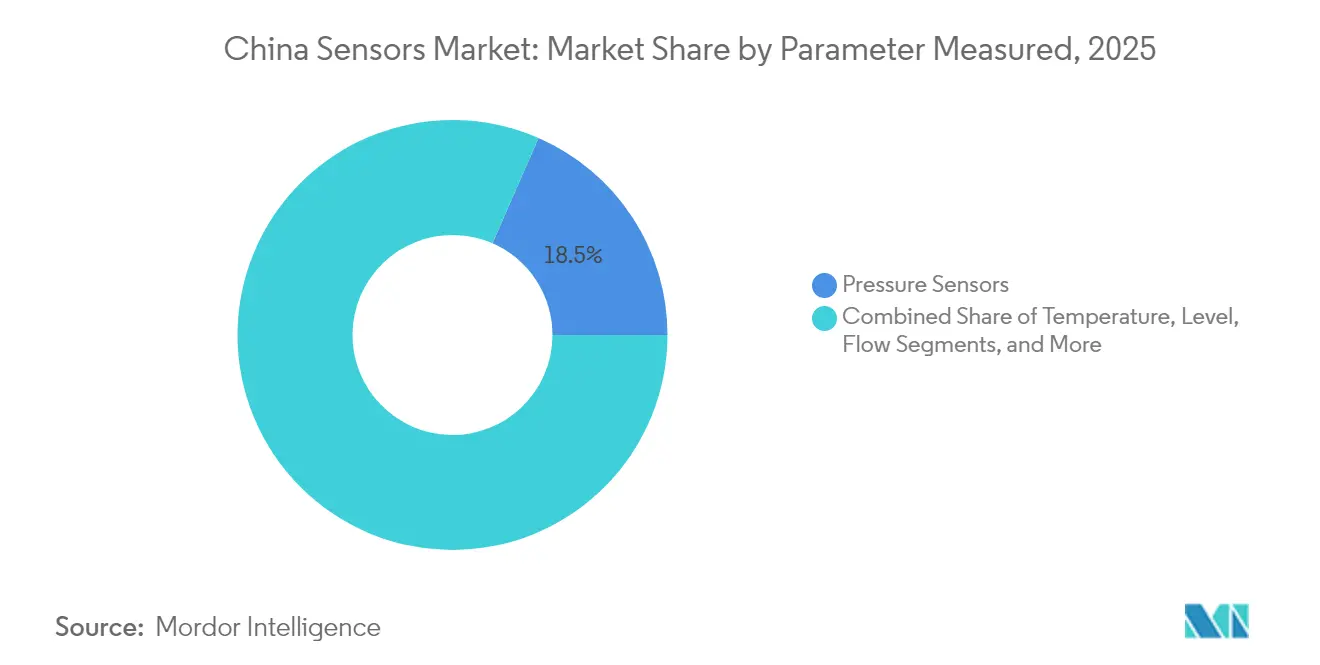

- By parameter measured, pressure sensors led with 18.45% of China sensors market share in 2025, whereas environmental sensors are on track for a 16.59% CAGR to 2031.

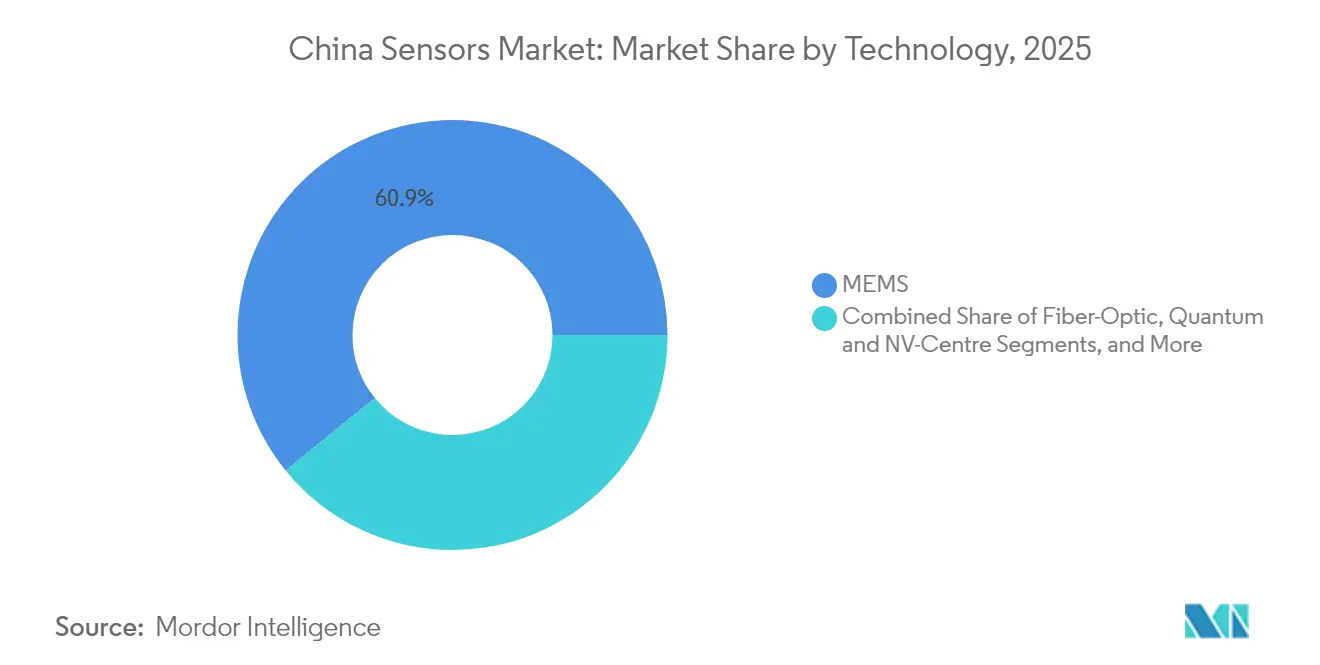

- By technology, MEMS held 60.85% of the China sensors market share in 2025, while quantum sensors are forecast to expand at 27.5% CAGR between 2026–2031.

- By mode of operation, piezoresistive devices commanded 31.75% of the China sensors market size in 2025; LiDAR is projected to grow at 21.53% CAGR through 2031.

- By end-user industry, consumer electronics captured 34.55% of the China sensors market size in 2025; automotive is the fastest-growing segment at 12.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China contributes to a system defined not by any single country or region but by the interaction of many. The global sensors market data by Mordor Intelligence represents that combined structure.

China Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led "Made in China 2025" localisation push for sensor supply chains | 1.8% | National, with a concentration in manufacturing hubs of Shenzhen, Shanghai, and Beijing | Long term (≥ 4 years) |

| EV production surge boosting demand for high-temperature, pressure, and current sensors | 1.5% | National, with a concentration in automotive manufacturing centres | Medium term (2-4 years) |

| Mass-manufacturing of smartphones and IoT wearables clustering in Guangdong raises MEMS volumes | 1.2% | Guangdong province, with spillover to Jiangsu and Zhejiang | Medium term (2-4 years) |

| Smart-factory retrofits across the Yangtze River Delta are accelerating industrial sensor uptake | 0.9% | Yangtze River Delta (Shanghai, Jiangsu, Zhejiang) | Medium term (2-4 years) |

| Rising adoption of remote patient monitoring and digital health platforms is driving the medical sensors market | 0.7% | Tier-1 and Tier-2 cities nationwide | Long term (≥ 4 years) |

| Falling 8-inch MEMS wafer costs from domestic foundries are widening sensor addressable markets | 0.6% | National, with a concentration in semiconductor manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-led “Made in China 2025” localization push

Large-scale fiscal incentives and mandated procurement preferences lifted domestic content in core sensor components toward 70% by 2025, compared with about 40% in 2020.[1]Molnar et al., “China’s Manufacturing Innovation Centers,” National Institute of Standards and Technology, nist.gov More than 33 Manufacturing Innovation Centres had been launched by early 2025, anchoring joint R&D between universities and enterprises. Preferential financing, expedited certification, and IP support further reduced entry barriers for local firms, fostering a vertically integrated value chain that now rivals overseas suppliers in pressure, environmental, and inertial categories.

EV production surge boosting demand for high-temperature, pressure, and current sensors

EV sales exceeded 3.5 million units in 2024, sustaining a triple-digit expansion from pre-2023 levels and lifting per-vehicle sensor content at an 8–10% annual pace. BYD bundled its ‘God’s Eye’ smart-driving platform across the full model line without extra cost, normalizing advanced thermal-management, battery-pressure, and current-measurement arrays even in mass-market cars. The trend strengthened order books for domestic MEMS and shunt-based current-sensor makers positioned closest to major assembly hubs.

Mass manufacturing of smartphones and IoT wearables clustering in Guangdong

Handset and wearable factories in Guangdong averaged 11–14 and 6–8 sensors per unit, respectively, in 2024, pushing annual MEMS output into the multi-billion range and lowering unit costs through shared tooling and logistics. Proximity between sensor fabs, module houses, and final assemblers accelerated engineering cycles, enabling rapid incorporation of novel barometric, optical, and inertial elements. The cluster effect also encouraged foreign OEMs to dual-source from local fabs, reinforcing regional economies of scale.

Smart-factory retrofits across the Yangtze River Delta are accelerating industrial sensor uptake

The 14th Five-Year Plan prioritized digitalization, prompting factories to install dense sensor networks for asset tracking, energy optimization, and predictive maintenance. Industrial sensor deployments in Shanghai-Jiangsu-Zhejiang grew at 15–18% annually in 2024, nearly double the global average, aided by provincial subsidies for retrofit projects. Customizable modules that interface with legacy PLCs offered local vendors a differentiation avenue versus imported turnkey systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on imported specialty wafers creates supply-chain risk | -0.9% | National, with the highest impact on advanced sensor manufacturing | Medium term (2-4 years) |

| A fragmented IP landscape is triggering cross-licensing disputes with incumbents | -0.7% | Global, affecting Chinese manufacturers' export capabilities | Medium term (2-4 years) |

| Price wars among local vendors are eroding R&D budgets | -0.6% | National, particularly affecting smaller domestic manufacturers | Short term (≤ 2 years) |

| China's Cybersecurity Law complicates the deployment of cloud-connected industrial sensors | -0.4% | National, with particular impact on foreign vendors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dependence on imported specialty wafers creates supply-chain risk

Despite domestic fabs adding mature-node capacity, China still relied on overseas suppliers for SOI, SiC, and GaN wafers used in high-temperature and photonic sensors. Renewed export-control measures on advanced substrates in 2024 heightened procurement uncertainty and forced buffer-stock policies, increasing working-capital needs. Resulting lead-time volatility constrained the production of cutting-edge automotive and medical devices.

Fragmented IP landscape triggering cross-licensing disputes

Accelerated patent filings by Chinese sensor firms collided with legacy portfolios held by established multinationals, leading to a rise in SEP-related arbitration when exporting to Europe and North America. License fees and litigation added overheads that smaller entrants struggled to absorb, while uncertainty around cross-jurisdiction enforcement slowed time-to-market for novel connected-sensor modules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Parameter Measured: Environmental sensors surged amid regulatory push

Pressure sensors accounted for 18.45% of China's sensor market share in 2025, reflecting established automotive, industrial, and handset integration footprints. Environmental sensors represented a smaller base yet posted the fastest 16.59% CAGR forecast, propelled by stricter National Ambient Air Quality Standards and municipal PM2.5 monitoring mandates.

Rapid air-quality site build-outs in Tier-1 cities stimulated demand for micro-precision gas and particulate sensors, pushing the China sensors market size for environmental categories at a significant rate during the forecast period. Consumer IoT air-purifiers and smart-home devices further broadened volume. Meanwhile, flow and level sensors advanced steadily in chemical processing and water-utilities projects, while vibration and magnetic devices gained traction in structural health and autonomous navigation use cases.

By Mode of Operation: LiDAR revolutionized automotive safety systems

Piezoresistive components retained a 31.75% revenue share in 2025, anchored by mature packaging lines and well-established design IP. LiDAR units, however, are projected for a 21.53% CAGR through 2031 as ADAS penetration in mid-range EVs climbs. Hesai and RoboSense jointly shipped more than 520,000 automotive LiDARs in 2024, equal to one-third of global deliveries.

The China sensors market size for LiDAR is expected to approach USD 1.42 billion by 2031 on the strength of national standards such as GB/T 45500-2025 that codify performance metrics. Complementary radar, capacitive-touch, and optical imagers sustained double-digit growth, serving consumer devices and industrial robots that require multi-modal perception arrays.

By Technology: Quantum sensors emerged as a disruptive force

MEMS retained a dominant 60.85% share of the China sensors market size in 2025, helped by falling 8-inch wafer costs and mature-process expansions at SMIC and HuaHong. Quantum devices using nitrogen-vacancy centres in diamond are forecast to scale at 27.5% CAGR, aided by heteroepitaxial growth breakthroughs that allow wafer-level production.

First commercial deployments target EV battery diagnostics and precision navigation. CMOS/IC, thin-film, and fiber-optic platforms expanded in applications ranging from flexible wearables to distributed infrastructure monitoring, further diversifying supply-chain demand inside the China sensors market.

By End-user Industry: The Automotive sector drove an innovation wave

Consumer electronics absorbed 34.55% of 2025 sales through high-volume phones and wearables. The automotive vertical is anticipated to generate the highest incremental revenue, rising at 12.71% CAGR as sensor content per EV surpasses 250 units. The China sensors market size for automotive applications is expected to grow at a rapid rate by 2031, supported by mandatory ADAS regulations and export ambitions of Chinese OEMs.

Industrial, medical, and energy segments each logged double-digit gains as factories digitized operations, health systems embraced continuous monitoring, and utilities rolled out smart-grid hardware. Aerospace and defense procurement remained steady, underpinned by long-cycle programs in civil aviation and satellite remote-sensing.

Geography Analysis

The Pearl River Delta accounted for the major national production value in 2024, giving the region a significant market share thanks to Guangzhou-Shenzhen consumer-electronics clusters that consumed the bulk of MEMS output. Robust handset and wearable demand pushed the local China sensors market size for pressure, proximity, and ambient-light devices at a prominent rate in 2025, and Honeywell’s 2024 decision to expand its Guangdong plant reinforced the zone’s importance to multinational supply chains. Short design-iteration loops, dense subcontractor networks, and export-oriented logistics lowered time-to-market for domestic startups, allowing Guangdong vendors to win follow-on orders from foreign smartphone brands. Provincial incentives that reimburse up to 15% of capital expenditures on new sensing lines further cemented the Pearl River Delta’s leadership position.

The Yangtze River Delta is another prominent region in China's sensors market, as Shanghai, Jiangsu, and Zhejiang factories are retrofitting with smart-manufacturing sensor suites. Mature-node foundries such as SMIC and HuaHong ramped 8-inch MEMS capacity in 2025, slashing die costs and lifting regional shipments of pressure and inertial parts. Local governments offered subsidies that covered 20% of automation-equipment purchases, accelerating edge-connected sensor deployments on legacy production lines. The region also houses leading automotive-electronics campuses, which pulled in high-temperature and current-measurement devices for EV platforms assembled in nearby Ningbo and Changzhou.

The Beijing-Tianjin-Hebei corridor captured nominal share of 2024 revenue yet punched above its weight in R&D, spearheading quantum-sensor breakthroughs that aim to commercialize nitrogen-vacancy diamond devices for navigation and battery diagnostics. Government laboratories in Beijing partnered with universities to secure national-science grants that finance pilot fabrication lines, while Tianjin aerospace suppliers validated radiation-hardened MEMS for satellite constellations. Policy proximity enabled rapid alignment with “Made in China 2025” localization quotas, ensuring preferential procurement for locally developed high-end sensors. The corridor’s focus on early-stage innovation complements high-volume production in the southern deltas, rounding out China’s full-stack sensing ecosystem.

The sensors market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Asia and Europe. This is complemented by country-specific insights for South Korea, Taiwan, Japan, and United States, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The competitive structure of the China sensors market blended concentrated leadership in emerging niches with fragmentation in mature categories. International firms such as Bosch, STMicroelectronics, and Honeywell preserved strong positions in high-precision pressure, temperature, and industrial sensors by leveraging decades of process know-how. Domestic champions Goertek, AAC Technologies, MEMSensing, Hesai, and RoboSense narrowed technology gaps through state incentives, cooperative R&D, and proximity to downstream assemblers.

Strategic positioning diverged between volume-driven players focused on smartphone MEMS and specialists targeting premium automotive or quantum segments. Hesai secured a critical standards advantage in May 2025 by leading the drafting of GB/T 45500-2025 for automotive LiDAR, locking its design parameters into national procurement frameworks.[4]Auto Tech News, “Hesai Leads Development of China’s Automotive LiDAR Standard GB/T 45500-2025,” auto-tech-news.com Mercedes-Benz formalized a partnership with Hesai the following month to co-develop global smart-car platforms, validating Chinese LiDAR technology for export markets. RoboSense built scale by shipping 519,800 automotive LiDAR units in 2024 and captured 26% of the global passenger-car segment, highlighting the speed at which local suppliers can reach international volume leaders. BYD’s choice to bundle its ‘God’s Eye’ sensor suite across all vehicle trims without a premium forced tier-1 vendors to reprice ADAS hardware and stimulated downstream demand.

Cost leadership remained pivotal, with domestic fabs cutting 8-inch MEMS wafer pricing and permitting vertical integration from wafer to module assembly. Bosch reacted by forming a joint venture with Element Six in April 2025 to accelerate commercialization of diamond-based quantum sensors, aiming to differentiate on performance rather than cost. Honeywell’s sensing division returned to growth in late 2024 after expanding local production, demonstrating that multinational incumbents can still compete on scale and service when they localize manufacturing. Even so, a fragmented intellectual-property landscape and escalating cross-licensing costs continued to siphon resources from R&D and posed a barrier for smaller sensor startups seeking export certifications.

China Sensors Industry Leaders

Bosch Sensortec GmbH

STMicroelectronics NV

Honeywell International Inc.

Will Semiconductor Co. Ltd.

Omron Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hesai led the development of China’s automotive LiDAR standard GB/T 45500-2025.

- April 2025: RoboSense ranked first in global passenger-car LiDAR with 26% share after shipping 519,800 units in 2024.

- April 2025: Bosch and Element Six formed a joint venture to scale quantum-sensing technologies.

- March 2025: Mercedes-Benz partnered with Hesai to co-develop smart cars for worldwide markets.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines China's sensors market as the annual, ex-factory revenue earned from finished sensing elements and integrated sensor modules, whether MEMS, CMOS, optical, magnetic, or piezoelectric, that convert a physical stimulus into an electrical signal for downstream processing. Values are expressed in constant 2024 US dollars and cover shipments into every domestic demand center, from automotive to consumer electronics, regardless of import origin.

Scope Exclusions: Pure-play analytics software, intangible licensing fees, and discrete passive components are not counted.

Segmentation Overview

- By Parameter Measured

- Temperature

- Pressure

- Level

- Flow

- Proximity

- Environmental (Air-quality, Gas)

- Chemical

- Inertial (Accel/Gyro)

- Magnetic

- Vibration

- Other Parameters

- By Mode of Operation

- Optical

- Electrical Resistance

- Biosensors

- Piezoresistive

- Image

- Capacitive

- Piezoelectric

- LiDAR

- Radar

- Other Modes

- By Technology

- MEMS

- CMOS / IC Sensors

- Fiber-Optic

- Quantum and NV-Centre

- Others (O-NEMS, Thin-Film)

- By End-user Industry

- Automotive

- Consumer Electronics

- Smartphones

- Tablets, Laptops and PCs

- Wearables

- Smart Home Devices

- Other Consumer Electronics

- Energy (Generation and Storage)

- Industrial and Manufacturing

- Medical and Wellness

- Construction, Agriculture and Mining

- Aerospace and Defense

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews and short surveys with fabless chip designers, Tier-1 module suppliers, system integrators, and procurement managers across East China, the Pearl River Delta, and the Beijing-Tianjin corridor. These discussions validated shipment run-rates, ASP ranges, localization progress, and demand inflection points that secondary sources only hinted at.

Desk Research

We began with macro indicators, industrial output, fixed-asset investment, and electronic component export data from sources such as the National Bureau of Statistics, the General Administration of Customs, and MIIT reports. Industry bodies like the China Semiconductor Industry Association and Shenzhen Sensor Standards Alliance supplied volume trends, while peer-reviewed articles and patent analytics from Questel highlighted emergent quantum and NV-center sensing breakthroughs. Financial filings, investor decks, and press releases were sifted to capture average selling prices (ASP) shifts and factory utilization changes. Finally, company intelligence from D&B Hoovers and news feeds pulled through Dow Jones Factiva framed competitive footprints. This list is illustrative; many other open and paid repositories informed fact-checks and clarifications.

Market-Sizing & Forecasting

A top-down build starts from domestic production plus net imports, reconstructed through trade codes and factory gate indices, then calibrated against penetration-rate based demand pools in automotive ECUs, smartphones, and industrial controllers. Select bottom-up rollups, sampled supplier revenues and channel checks, test the totals before adjustment. Key variables modeled include smartphone output, NEV production, smart-factory robot shipments, 5G base-station rollouts, and policy incentives under 'Made in China 2025'. Multivariate regression, supported by ARIMA for short-term smoothing, projects each driver, while expert consensus guides scenario bounds. Data gaps in supplier rollups are bridged with weighted averages derived from disclosed gross margins and unit mixes.

Data Validation & Update Cycle

Outputs pass anomaly checks against historical series and independent proxy indicators, followed by multi-level analyst review. The dataset refreshes annually; material events, policy shifts, or large fab capacity additions trigger interim revisions. A final pre-publication pass ensures clients receive the freshest view.

Why Mordor's China Sensors Baseline Commands Reliability

Published estimates often diverge because analysts choose different product baskets, pricing assumptions, or refresh cadences.

Key gap drivers here include broader industrial sensor inclusion by some publishers, unvetted ASP inflation, and less frequent model refreshes that miss 2024's currency realignment and subsidy cuts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.01 B (2025) | Mordor Intelligence | - |

| USD 8.53 B (2024) | Regional Consultancy A | Includes gray-channel proximity switches; limited primary vetting |

| USD 21.58 B (2024) | Global Consultancy B | Aggregates embedded sensor dies and modules, uses desktop projections, refresh lag >18 months |

Taken together, the comparison shows that Mordor's disciplined scope selection, annual refresh, and dual-track validation yield a balanced, transparent baseline that decision-makers in policy, procurement, and strategy teams can readily trace back to observable variables.

Key Questions Answered in the Report

What is the current value of the China sensors market?

The market was valued at USD 7.45 billion in 2026 and is projected to reach USD 10.08 billion by 2031.

Which segment holds the largest China sensors market share by parameter measured?

Pressure sensors led with an 18.45% share in 2025.

How fast is LiDAR growing inside the China sensors market?

LiDAR revenue is forecast to expand at a 21.53% CAGR between 2026 and 2031.

Why are MEMS devices dominant in the China sensors market?

Mature 8-inch wafer lines, falling fabrication costs, and high consumer-electronics volumes kept MEMS at 60.85% of 2025 revenue.

Page last updated on: