Aliphatic Hydrocarbon Solvents And Thinners Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

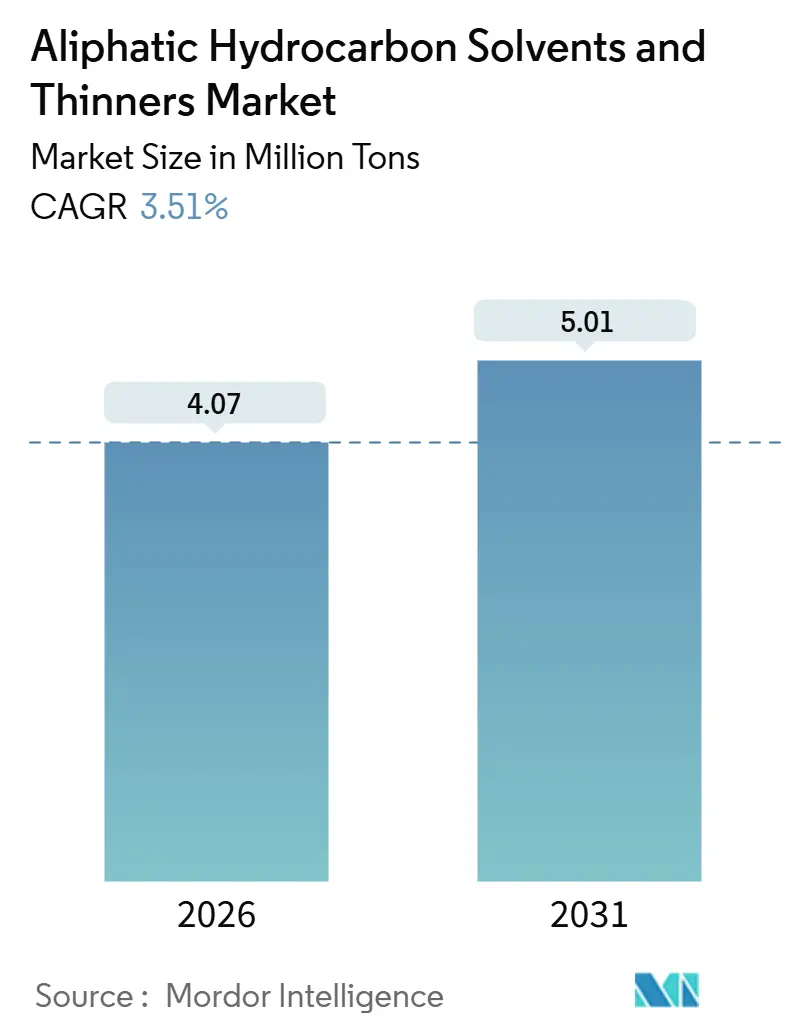

| Market Volume (2026) | 4.07 Million tons |

| Market Volume (2031) | 5.01 Million tons |

| Growth Rate (2026 - 2031) | 3.51% CAGR |

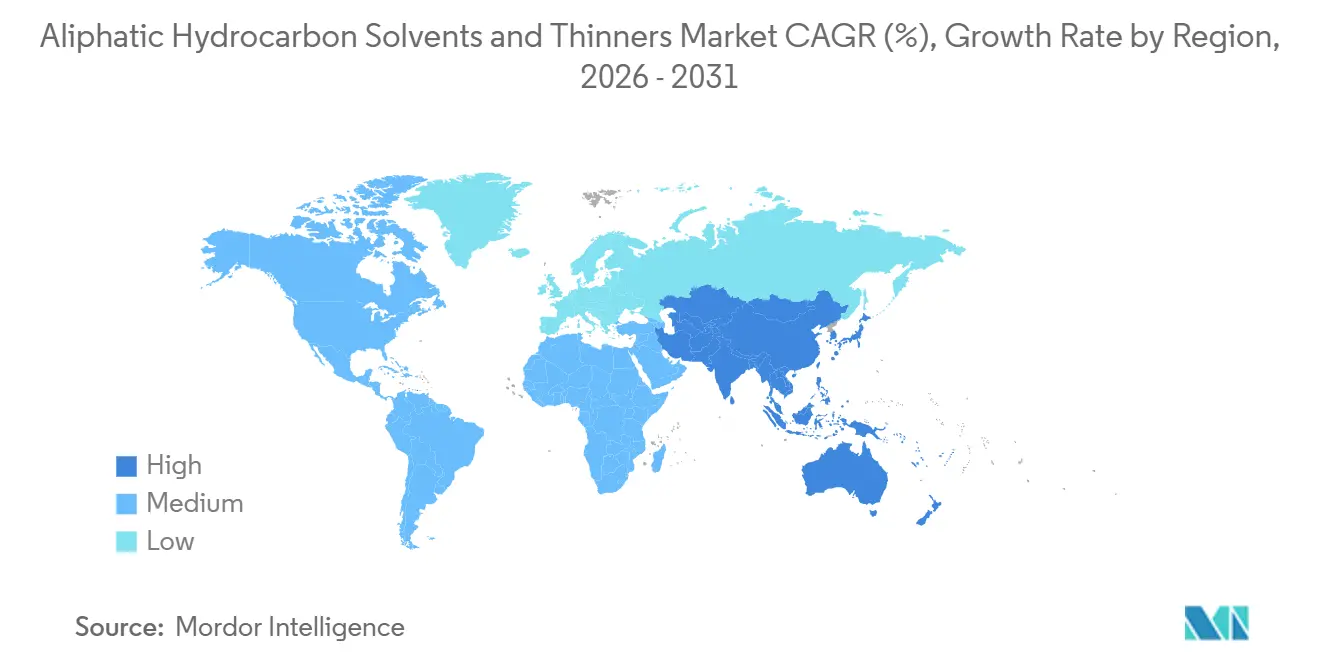

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aliphatic Hydrocarbon Solvents And Thinners Market Analysis by Mordor Intelligence

The Aliphatic Hydrocarbon Solvents And Thinners Market size is estimated at 4.07 Million tons in 2026, and is expected to reach 5.01 Million tons by 2031, at a CAGR of 3.51% during the forecast period (2026-2031). Demand progresses in line with repainting cycles, automotive‐refinishing throughput, adhesive‐formulation adjustments, and a measured shift toward lower‐aromatic grades rather than radical technology change. Hexane remains the single largest solvent, anchored by edible-oil extraction and rubber polymerization, while paints and coatings continue to absorb the lion’s share of volume as industrial maintenance cycles outpace new construction. Regulatory initiatives limit aromatics and total VOCs, stimulating preference for C6-C8 paraffins and positioning low-aromatic mineral spirits as substitutes for higher-toxicity aromatics. Feedstock-supply swings driven by naphtha inventories, crude-to-chemicals projects, and refinery operating decisions reward integrated producers with captive refining capacity. Geographic momentum favors Asia-Pacific, where urbanization, infrastructure build-outs, and rapid vehicle‐parc expansion bolster solvent demand ahead of North America and Europe.

Key Report Takeaways

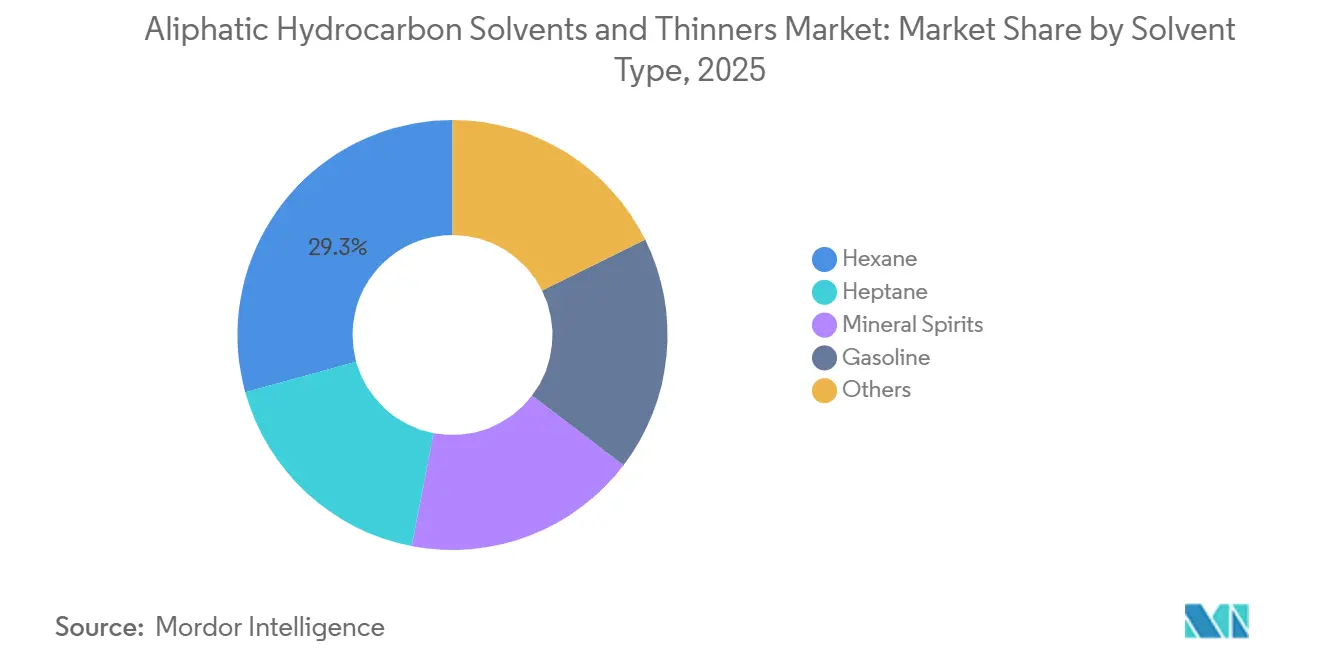

- By solvent type, hexane accounted for 29.30% of the aliphatic hydrocarbon solvents and thinners market share in 2025 and heptane is forecast to post the fastest growth, expanding at a 4.38% CAGR to 2031.

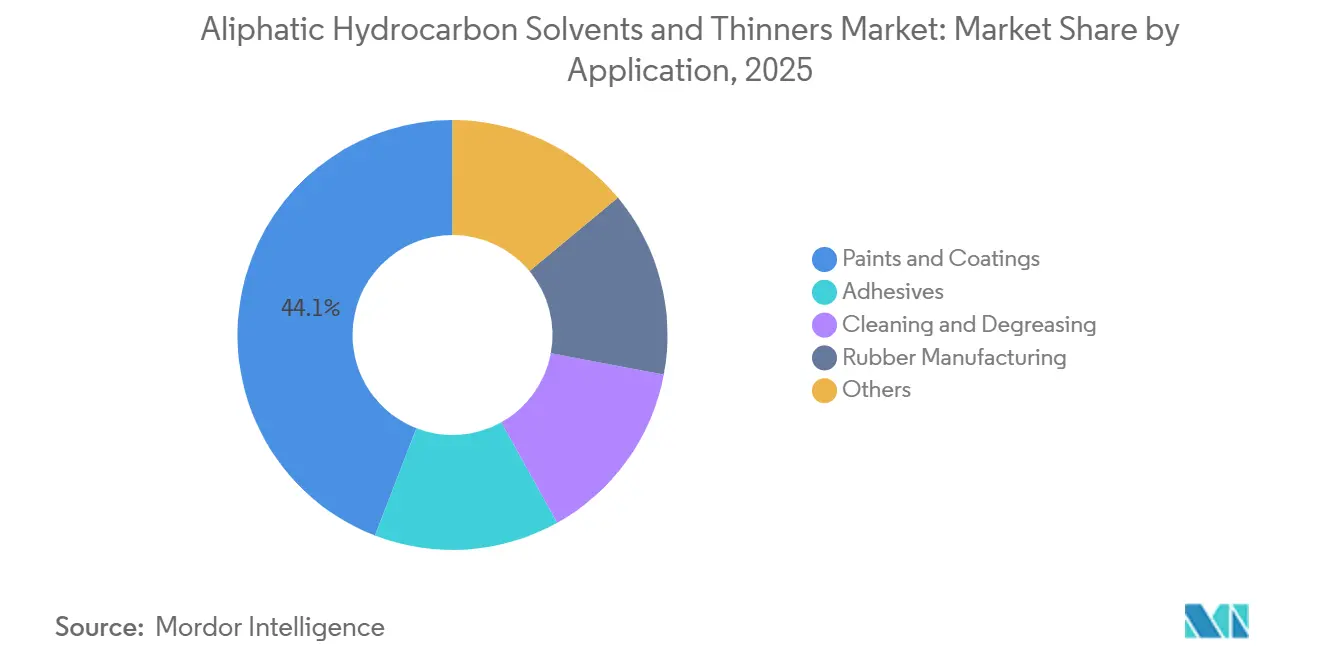

- By application, paints and coatings held 44.14% of the aliphatic hydrocarbon solvents and thinners market size in 2025 and rubber manufacturing is projected to advance at the quickest pace, registering a 4.02% CAGR through 2031.

- By geography, Asia-Pacific led with 41.08% volume share in 2025, while the region is also expected to log the strongest 4.32% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aliphatic Hydrocarbon Solvents And Thinners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Application in Paints and Coatings | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Expanding Demand from Adhesives and Sealants | +0.7% | Asia-Pacific core, spill-over to Middle East and Latin America | Long term (≥ 4 years) |

| Growth in Construction Activities Globally | +0.9% | Asia-Pacific, Middle East, selective North American metros | Medium term (2-4 years) |

| Rising Automotive Refinishing Volumes | +0.5% | North America, Europe, emerging in China and India | Short term (≤ 2 years) |

| Shift Toward Low-Aromatic Health-Safer Grades | +0.6% | Europe and North America, gradual adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Application in Paints and Coatings

Global paint output climbed to 48.3 million tons in 2024, and solvent-borne formulations still represented 38% of that total despite continued water-borne gains. Capacity additions—such as BASF’s 50,000-ton-per-year alkyd-resin line in Shanghai—specifically target OEM primers and metal topcoats that require aliphatic thinners to remain within China’s GB 24409-2020 VOC limits[1]BASF, “BASF expands alkyd resin capacity in Shanghai,” basf.com . Maintenance repainting, rather than new construction, increasingly drives tonnage because older assets need higher film-build and multi-coat systems. In India, organized producers lifted manufacturing capacity by 1.2 million liters per day through 2025, translating into incremental solvent demand that supports local suppliers. Yet policy developments, including California’s proposed 2027 limit of 100 g/L VOC in industrial maintenance coatings, foreshadow lower solvent intensity in western U.S. markets. Formulators therefore walk a tightrope: maximize solvency and dry-time performance while staying under tightening VOC ceilings.

Expanding Demand from Adhesives and Sealants

Solvent-based adhesive systems retain niche relevance wherever extended open time, rapid green-strength, and low-temperature application remain mandatory. A hexane-heptane blend released by Henkel in 2024 cut cure time by 30% and lifted laminating line speeds to 325 m/min, illustrating how incremental solvent chemistry advances can unlock throughput gains without new equipment. Rapid parcel growth in Asia-Pacific keeps pressure-sensitive label and tape output rising, thereby sustaining mineral-spirits demand. The Middle East’s USD 2.8 trillion active project pipeline underpins polyurethane-sealant volumes, and each square meter of curtain wall still requires solvent-containing sealant. Although water-borne acrylics nibble at construction segments, solvent formulations continue to dominate demanding façade and expansion-joint jobs where bond reliability outweighs VOC considerations.

Growth in Construction Activities Globally

Asia-Pacific accounted for 45% of worldwide construction spending in 2024, and infrastructure programs, rather than residential real estate, supplied the bulk of new surface-area to coat. India’s National Highways Authority awarded 8,500 km of road contracts in fiscal 2025, consuming road-marking paint dependent on mineral spirits carriers. Saudi Arabia’s NEOM project specified solvent-borne epoxies for steel exposed to Red Sea humidity, proving that extreme environments still favor aliphatic thinners despite low-VOC aspirations. North American renovation spending rose 6.8% in 2024, and repainting requires 2.3 times more paint per square meter than new construction. Consequently, stable solvent demand persists even when housing starts stall.

Rising Automotive Refinishing Volumes

The global vehicle parc touched 1.5 billion units in 2024, with an aging U.S. fleet averaging 12.6 years. North American collision-repair centers processed 18.2 million claims, driving solvent-borne refinish consumption because clearcoats and primers largely remain beyond water-borne capability. In China, luxury-vehicle share reached 14.2%, triggering demand for multi-stage metallic systems that employ heptane thinners for flow and leveling. These dynamics decouple refinishing from new-vehicle sales, making solvent demand resilient through economic cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and Hazardous-Air-Pollutant Regulations | -0.8% | North America and Europe, emerging in China and India | Short term (≤ 2 years) |

| Growing Adoption of Water-Borne and High-Solids Coatings | -0.6% | Global, with fastest penetration in North America and Europe | Medium term (2-4 years) |

| Volatility in Naphtha-Based Feedstock Supply | -0.4% | Global, with acute impact in import-dependent Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent VOC and Hazardous-Air-Pollutant Regulations

The U.S. EPA slashed VOC limits on architectural finishes to 50 g/L for flat paints and 150 g/L for non-flat coatings in December 2024, cutting solvent loading to roughly 15 wt %[2]U.S. Environmental Protection Agency, “National VOC Emission Standards for Architectural Coatings,” epa.gov . California doubled down, imposing a 10 g/L ceiling on interior flats through SCAQMD Rule 1113, effectively banning solvents in the largest local market. China followed suit with GB 30981.1-2025, capping aromatic content in industrial cleaning solvents at 0.5 wt %. Compliance costs escalate; a mid-sized German paint maker spent USD 2.5 million in 2024 on reformulations alone, underscoring how regulatory stringency erodes demand even where low-aromatic grades offer interim relief.

Growing Adoption of Water-Borne and High-Solids Coatings

Water-borne architectural coatings captured 62% of North American volume in 2025 as major producers resigned solvent lines to meet odor and VOC expectations. High-solids technology offers another pathway by boosting non-volatile content above 70 wt %, evidenced by PPG’s Delfleet Evolution truck coating that cut solvent usage 40% per vehicle while meeting 250 g/L VOC. Yet conversion is capital intensive; retrofitting a 50-million-L plant may require USD 25 million in new dispersion, pH-control, and effluent systems—hurdles smaller regional players struggle to overcome. Performance gaps linger in chemical-resistant spaces, preserving a floor for solvent demand, but the trajectory clearly shifts away from traditional mineral spirits in mass-market interior paints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solvent Type: Hexane Strength Persists Amid Heptane Upside

Hexane commanded 29.30% of the aliphatic hydrocarbon solvents and thinners market in 2025, owing to its indispensability in oilseed extraction and synthetic-rubber workflows. Global usage in edible-oil processing reached 1.18 million tons in 2024 following capacity additions across Brazil, Argentina, and the U.S. Midwest. Heptane, while smaller, is forecast to post the fastest 4.38% CAGR through 2031 because pharmaceutical synthesis values its higher flash point and lower toxicity. Mineral spirits remain the workhorse of paint thinning and industrial cleaning but must absorb incremental hydrotreatment costs to comply with Europe’s ultra-low-aromatic thresholds. Gasoline’s share continues to slide as occupational-safety rules favor higher-flash-point alternatives. Specialty blends, including VM&P naphtha and odorless variants, supply niche printing-ink and aerosol-propellant segments, adding diversity but limited incremental growth.

Mineral-spirits suppliers pursue differentiation via purity. ShellSol D60’s aromatic content below 1 wt % achieved 18% penetration in European industrial cleaning in 2024. ExxonMobil’s Baytown retrofit underscores the drive to cut naphthalene content under 10 ppm, opening pharmaceutical and food-contact markets. As solvent-quality specifications tighten, players with hydrotreating assets can command premiums, keeping this segment profitable despite volume headwinds.

By Application: Paints and Coatings Dominate, Rubber Manufacturing Accelerates

Paints and coatings absorbed 44.14% of demand in 2025, and the aliphatic hydrocarbon solvents and thinners market size linked to the category will continue expanding on maintenance cycles even as water-borne systems encroach. Industrial‐maintenance coatings, comprising nearly 28% of segment volume, rely on aliphatic thinners for single-coat 40-60 μm film thickness that water-borne products cannot duplicate. Rubber manufacturing, buoyed by Asia-Pacific tire production exceeding 2.1 billion units in 2024, will rise at a 4.02% CAGR, driven by solution-styrene-butadiene production that consumes hexane as the polymerization medium. Adhesives and sealants grow steadily as flexible packaging proliferation and automotive interiors need balanced open time and bond strength profiles that solvent systems still deliver. Solvent cleaning steadily declines outside aerospace and precision machining, where residue-free finishing remains essential.

Looking forward, formulators must balance performance, cost, and compliance. Water-borne penetration will continue, but high-solids and exempt-solvent blends are likely to maintain a solvent baseline in heavy-duty applications. Rubber manufacturing stands out for solvent resilience, underpinned by polymer-grade purity requirements that aqueous alternatives cannot meet at scale.

Geography Analysis

Asia-Pacific accounted for 41.08% of 2025 volume, and the aliphatic hydrocarbon solvents and thinners market in the region is projected to post a 4.32% CAGR through 2031. China leads on urban facade repainting and industrial infrastructure, generating steady offtake. India’s 5.9 million vehicle output plus ongoing road‐building propel solvent demand, and organized paint capacity expansions promise downstream pull. Mature markets Japan and South Korea grow modestly on automotive refinishing, while ASEAN members register mid-single-digit gains tied to electronics assembly and construction.

North America’s share masks diverging patterns. The United States uses solvent-borne paints mainly in exterior wood, high-gloss, and specialty primers, but Step-change VOC rules steadily erode per-liter solvent intensity. Canada leverages colder climates that favor solvent-borne curing. Mexico gains from automotive nearshoring and maintains stricter fire-code allowances for mineral-spirits cleaning.

Europe faces the toughest VOC regimes. Germany’s usage slipped as automotive lines switched to water-borne basecoats. The United Kingdom preserved demand in marine and offshore protective coatings. Nordic countries defend mineral-spirits wood-finishing traditions, while Eastern Europe remains a pocket of growth where regulatory alignment lags. Russia grew on local refining and import-substitution policies.

South America is dominated by Brazil, tied to construction and vehicle refinishing. Argentina’s contraction was mitigated by lithium-brine extraction, which employs hexane for lithium chloride separation. The Middle East and Africa combined delivered substantial growth, led by Saudi Arabia’s megaprojects and South Africa’s aging vehicle parc requiring solvent-rich refinish systems.

Competitive Landscape

The aliphatic hydrocarbon solvents and thinners market features moderate concentration. Integrated players—BASF, ExxonMobil, Shell, TotalEnergies, and Chevron Phillips—collectively held 38% global share in 2025, backed by captive naphtha supply and multi-site logistics. Shell’s Pernis and ExxonMobil’s Baytown complexes each top 200,000 t/y of aliphatic capacity, capturing economies of scale and hydro-processing synergies that push cash costs under USD 420 per ton. BASF’s 35,000 t/y ultra-low-aromatic line in Shanghai addresses high-purity niches willing to pay 15-20% premiums.

Strategic moves highlight low-aromatic expansion and bio-feed integration. Shell’s 2025 arrangement with Neste will redirect 50,000 t/y of HVO-based naphtha into solvent production, offering customers a 60-70% greenhouse-gas reduction. Smaller regional suppliers—Gandhar Oil Refinery in India and SK geocentric in South Korea—compete on lead time, flexible packaging, and localized technical service. Technology differentiation remains incremental, focusing on additive packages that lower odor and improve storage stability like Honeywell’s Hydrofluor line that doubles shelf life in steel drums.

The aliphatic hydrocarbon solvents and thinners industry maintains price discipline through feedstock linkage; however, merchant blenders without refining integration remain exposed to naphtha volatility, reinforcing gradual consolidation as scale economies widen.

Aliphatic Hydrocarbon Solvents And Thinners Industry Leaders

Exxon Mobil Corporation

Shell plc

BASF

Chevron Phillips Chemical Company LLC

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Shell plc completed the acquisition of Raj Petro Specialities, enhancing its lubricants portfolio and expanding its customer base. This acquisition is expected to impact the aliphatic hydrocarbons and thinners market by increasing the availability of specialized products and strengthening supply chains.

- February 2025: The European Chemicals Agency (ECHA) completed an assessment of regulatory needs for fluorinated aliphatic hydrocarbons, a group of 28 substances used in manufacturing, electronics, and industrial cleaning. The review identified potential hazards related to carcinogenicity, reproductive toxicity, endocrine disruption, and environmental persistence. However, no immediate EU-wide regulatory risk management measures were proposed.

Global Aliphatic Hydrocarbon Solvents And Thinners Market Report Scope

Aliphatic hydrocarbon solvents and thinners are petroleum-derived organic liquids composed of carbon-hydrogen chains, which can be straight, branched, or cyclic but do not include aromatic rings such as benzene. These solvents are commonly used for dissolving substances, thinning paints and coatings, degreasing, and as cleaning agents. They are recognized for their effectiveness, relatively lower toxicity compared to aromatic solvents, and high flammability.

The aliphatic hydrocarbon solvents and thinners market is segmented by solvent type, application, and geography. By solvent type, the market is segmented into hexane, heptane, mineral spirits, gasoline, and others. By application, the market is segmented into paints and coatings, adhesives, cleaning and degreasing, rubber manufacturing, and others. The report also covers the market size and forecasts for aliphatic hydrocarbon solvents and thinners in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Hexane |

| Heptane |

| Mineral Spirits |

| Gasoline |

| Others |

| Paints and Coatings |

| Adhesives |

| Cleaning and Degreasing |

| Rubber Manufacturing |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Solvent Type | Hexane | |

| Heptane | ||

| Mineral Spirits | ||

| Gasoline | ||

| Others | ||

| By Application | Paints and Coatings | |

| Adhesives | ||

| Cleaning and Degreasing | ||

| Rubber Manufacturing | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current volume of the aliphatic hydrocarbon solvents and thinners market?

The market totals 4.07 million tons in 2026 and is on course to reach 5.01 million tons by 2031.

Which solvent type holds the largest share?

Hexane leads with 29.30% of global volume in 2025, thanks to its role in edible-oil extraction and rubber polymerization.

Which region is growing fastest?

Asia-Pacific combines the largest 41.08% share in 2025 with a 4.32% forecast CAGR through 2031.

How are VOC regulations affecting demand?

Stricter VOC caps in the United States, Europe, and China are reducing solvent loading in coatings and encouraging low-aromatic grades.

Page last updated on: