Algae Products Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

| Market Size (2025) | USD 3.85 Billion |

| Market Size (2030) | USD 5.56 Billion |

| Growth Rate (2025 - 2030) | 7.64% CAGR |

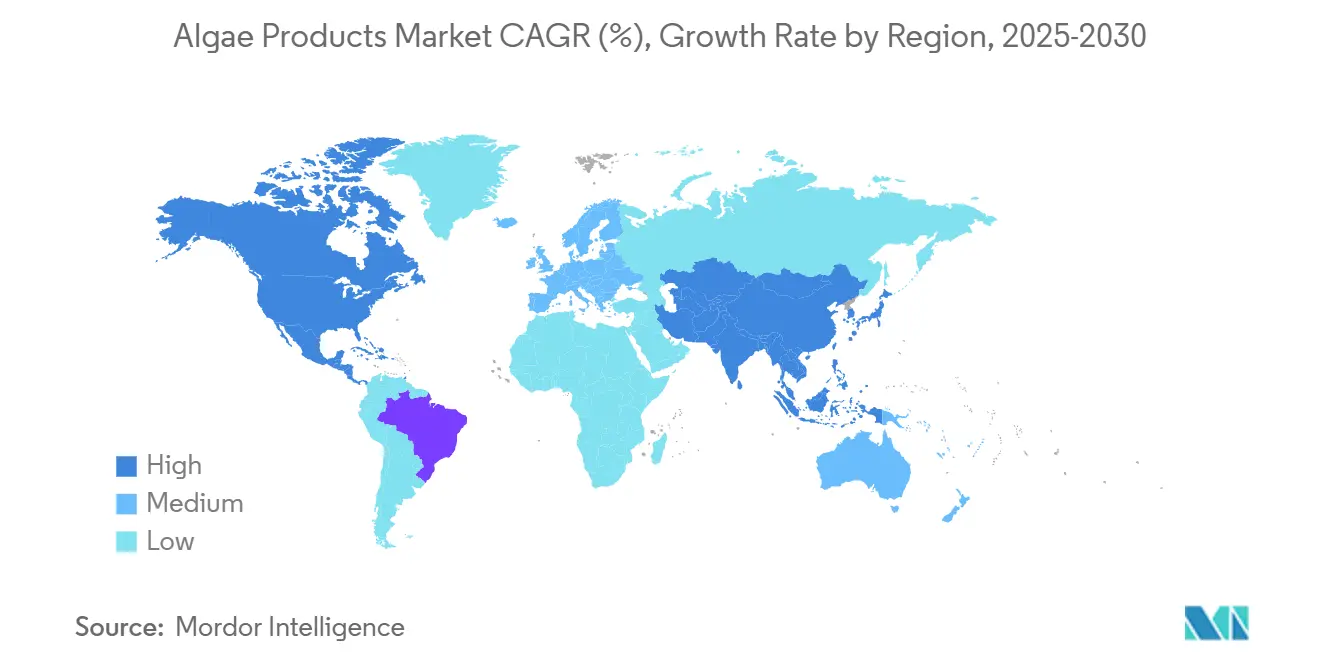

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Algae Products Market Analysis by Mordor Intelligence

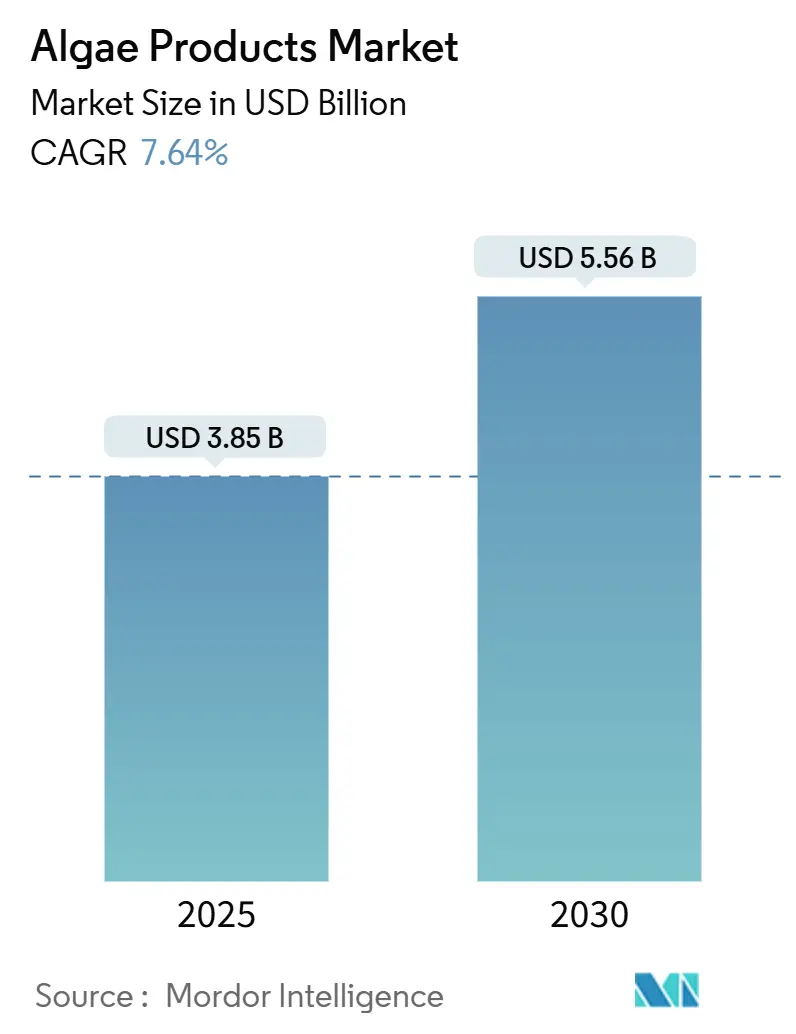

The algae products market size is estimated at USD 3.85 billion in 2025 and is expected to reach USD 5.56 billion by 2030, at a CAGR of 7.64% during the forecast period (2025-2030). Regulatory approvals are broadening ingredient options, shifting commercial momentum from niche applications to mainstream adoption. A prime example is the FDA's approval of Galdieria extract blue in May 2025, according to the Federal Register[1]Source: Federal Register, "approval of Galdieria extract blue" www.federalregister.gov. As demand surges for natural colorants, plant-based proteins, and sustainable lipids, capital is increasingly funneled into advanced photobioreactor capacities. Concurrently, cost-reduction initiatives aimed at enhancing support-structure efficiency are successfully narrowing the gap with conventional ingredients as per Pacific Northwest National Laboratory (PNNL)[2].Source: Pacific Northwest National Laboratory (PNNL), "cost-reduction initiatives", www.pnnl.gov North America maintains its leadership, bolstered by consistent safety frameworks. In contrast, Asia-Pacific is witnessing the fastest growth, driven by a booming aquaculture sector and government mandates for biofuels. While competitive intensity is moderate, there's enough rivalry to fuel innovation. Yet, this landscape also allows established players to fortify their positions through scale and patents.

Key Report Takeaways

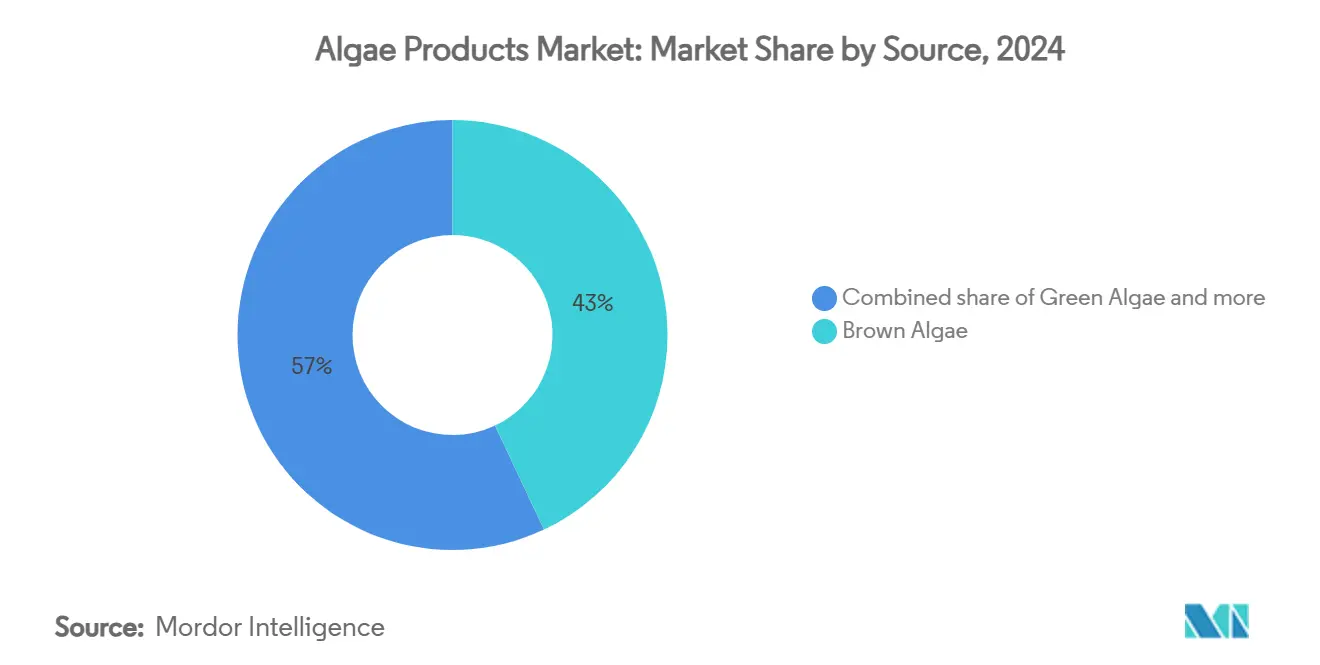

• By source, brown algae led with 43.01% of algae products market share in 2024; green algae is forecast to expand at a 9.36% CAGR through 2030.

• By product type, hydrocolloids commanded 45.93% share of the algae products market size in 2024, whereas carotenoids are projected to grow at a 10.80% CAGR to 2030.

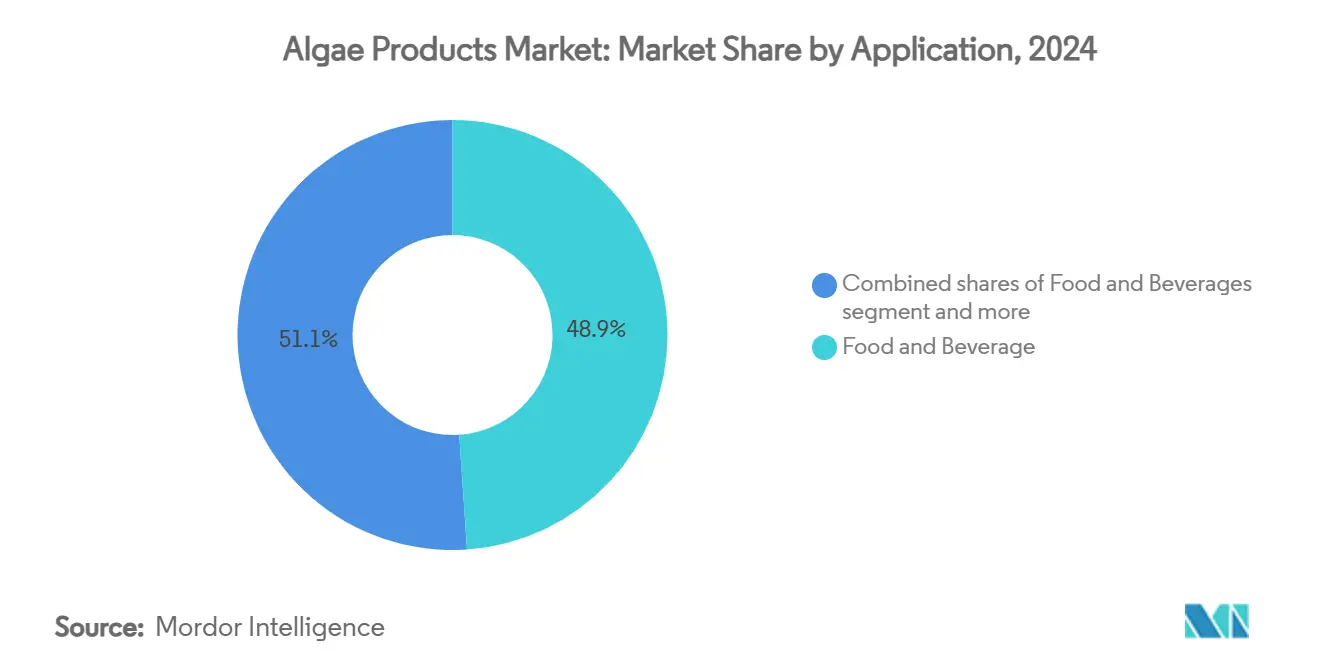

• By application, food and beverage accounted for 48.93% of the algae products market size in 2024 and is advancing at an 8.22% CAGR through 2030.

• By geography, North America held 34.54% of the algae products market share in 2024, while Asia-Pacific is set to post an 8.98% CAGR to 2030.

Global Algae Products Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for plant-based protein ingredients | +1.8% | Global, North America and Europe focus | Medium term (2-4 years) |

| Increasing use of natural food colorants and texturants | +1.5% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Technological advancements in algae cultivation and processing | +1.2% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Support from organic farming and circular economy initiatives | +0.9% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Broadening applications across diverse industries | +1.1% | Global | Medium term (2-4 years) |

| Rising investments in algae-based biofuel development | +0.8% | Asia-Pacific core, North America secondary | Long term (≥ 4 years) |

Source: Mordor Intelligence

Growing Demand for Plant-Based Protein Ingredients

Microalgae, particularly Spirulina and Chlorella, are gaining traction in sports nutrition, meat alternatives, and infant formulas due to their high protein content, reaching up to 70% of their dry weight. A 2024 study from the University of Exeter highlighted Spirulina's muscle-boosting protein, comparable to mycoprotein. AlgaeCore Technologies secured USD 19 million to refine its Simplii Texture process, which eliminates off-notes and creates fibrous structures without extrusion, as per the Pacific Northwest National Laboratory (PNNL). Brevel's Israeli facility is producing neutral-flavor microalgae protein using sugar-based fermentation, reducing the cost gap with soy and pea proteins. Rising demand for sustainable, plant-based proteins is driving innovation and scaling efforts in the microalgae market.

Increasing Use of Natural Food Colorants and Texturants

In a notable policy shift, the FDA approved four algae-derived pigments in 2025, including the Galdieria extract blue. This move accelerates the market entry of natural alternatives. Notably, the spirulina extract benefits from a certification exemption, sidestepping the periodic batch fees associated with synthetic dyes. At the same time, advancements in fermentation are enhancing pigment heat stability. This allows confectionery and baking companies to seamlessly transition from synthetic blues and reds, without compromising on hue intensity. Additionally, the growing consumer demand for clean-label and plant-based products is further driving the adoption of algae-derived pigments. The increasing focus on sustainability and reducing reliance on synthetic ingredients also aligns with the broader industry trends, making algae products a preferred choice. Collectively, these developments are elevating algal carotenoids from niche ingredients to essential components, driving the growth of the algae products market.

Support from Organic Farming and Circular Economy Initiatives

Industrial CO₂ emissions are now being directly channeled into algae units, thanks to circular-economy pilots by the U.S Department of Energy[4]Source: U.S Department of Energy, "Circular Economy Initiatives", www.energy.gov. These units are strategically located at cement and steel plants, generating carbon-credit revenue streams that enhance project IRRs. Backed by a USD 46 million funding pool from the Department of Energy, waste-to-algae fuel projects are integrating wastewater polishing. These projects boast impressive metrics: achieving 99% ammonia removal and 83% orthophosphate uptake, all while producing saleable biomass. In addition to environmental benefits, these initiatives are driving innovation in algae-based biofuels, creating opportunities for sustainable energy solutions. Furthermore, the integration of algae systems into industrial processes is reducing dependency on fossil fuels, contributing to long-term carbon neutrality goals. In the EU, Horizon programs, operating under the "Blue bioeconomy" initiative, are promoting algae cultivation on non-arable land. This move not only aligns with agronomy and climate objectives but also bolsters the competitive edge of the algae products market over traditional crops.

Broadening Applications Across Diverse Industries

Chlorella vulgaris, a microalgae, is making waves in the sunscreen industry, offering SPF 8 through its naturally occurring mycosporine-like amino acids. This innovation aligns with reef-safe regulations, notably in states like Hawaii. On the pharmaceutical frontier, Chlamydomonas is being harnessed to express recombinant vaccine antigens. This approach capitalizes on eukaryotic glycosylation, achieving results at a fraction of traditional mammalian-cell costs. In the realm of packaging, algae-derived biopolymers are stepping into the spotlight. They're being piloted for single-use packaging, boasting biodegradability and carbon capture features that outshine conventional petrochemical plastics. Additionally, algae-based products are gaining traction in the food and beverage industry, offering sustainable and nutrient-rich alternatives to traditional ingredients. The growing focus on environmental sustainability and regulatory support for bio-based products further accelerates the adoption of algae-derived solutions. With a diverse array of end-markets, the algae products market is cushioned against volatility, paving the way for stable long-term growth.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure for photobioreactor scale-up | -1.4% | Global, acute in emerging markets | Medium term (2-4 years) |

| Regulatory ambiguities for novel algae-based foods in emerging economies | -0.8% | Asia-Pacific emerging markets, Latin America | Short term (≤ 2 years) |

| Supply-chain constraints for algae raw materials | -0.6% | Global, regional variations | Short term (≤ 2 years) |

| High production costs versus conventional alternatives | -1.2% | Global | Medium term (2-4 years) |

Source: Mordor Intelligence

Regulatory Ambiguities for Novel Algae-Based Foods in Emerging Economies

India's Food Safety and Standards Authority has yet to provide a definitive direction for algal proteins, leaving companies to navigate a maze of inconsistent approvals at the state level. In contrast, the EU (European Union) took decisive action in 2024, incorporating 20 algae species into its Novel Food Status Catalogue. This strategic move not only spared companies a significant EUR 10 million in administrative costs but also underscored a widening market gap. India's regulatory uncertainties have hampered the uptake of algae-based products, curtailing their domestic market potential. Meanwhile, the EU's forward-thinking stance has made it a magnet for investment and innovation in the algae sector. Consequently, global producers are increasingly favoring regions with clearer approval processes, leading to a slowdown in technology transfers to more budget-friendly areas.

Supply-Chain Constraints for Algae Raw Materials

Shortages in feedstock, including CO₂, essential nutrients, and premium seawater, threaten the consistent production of algae products. For instance, coastal facilities in Chile have had to scale back operations due to seasonal fluctuations in industrial CO₂ off-take agreements, highlighting the delicate supply chains the algae products market relies on. While there's ongoing investment in nutrient recycling and direct-air-capture CO₂ solutions, these efforts are still at a nascent stage. Additionally, the high costs associated with developing and implementing these technologies pose a significant challenge to scalability. The lack of standardized infrastructure for nutrient recycling further exacerbates the issue, creating inefficiencies in the supply chain. Addressing these constraints is critical to ensuring the long-term growth and stability of the algae products market.

Segment Analysis

By Source: Brown Algae Dominance Faces Green Innovation

In 2024, brown algae commanded a dominant 43.01% share of the algae products market, bolstered by established carrageenan and alginate supply chains in coastal regions of Asia and South America. Decades of infrastructure development, coupled with stringent specification standards, have cemented customer loyalty, particularly in dairy gelling and wound-care dressing applications. However, the segment's reliance on largely wild-harvested cultivation leaves it vulnerable to climate-induced fluctuations in biomass. Additionally, the limited scalability of wild-harvest methods poses challenges in meeting the growing global demand. Efforts to transition toward controlled aquaculture systems are underway, but widespread adoption remains slow due to high initial investment costs.

Green algae, on the other hand, is emerging as the fastest-growing segment, projected to maintain a robust 9.36% CAGR through 2030. This growth is driven by strains like Chlorella and Chlamydomonas, achieving impressive yields exceeding 0.3 g L⁻¹ day⁻¹. By employing fermentation-based processes, producers sidestep photosynthetic challenges, enabling them to position plants closer to renewable energy sources. Innovations in recombinant platforms are paving the way for lucrative pharmaceuticals, and ProFuture’s development of a flavor-neutral Chlorella addresses past sensory limitations. Furthermore, green algae's versatility in applications such as biofuels and animal feed enhances its market potential. The segment's rapid advancements are attracting significant investments, further accelerating its growth trajectory.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Hydrocolloids Lead While Carotenoids Surge

In 2024, hydrocolloids dominated the algae products market, accounting for 45.93% of the market size. These hydrocolloids provide shelf-stable viscosity to plant-based cheeses, yogurts, and deli meats. Demand for these products remains price-inelastic, as synthetic substitutes struggle to replicate the necessary thermal gel strength and pH tolerance. Furthermore, capacity rationalization among the top three carrageenan firms has led to disciplined pricing, bolstering profit margins.

Carotenoids, with a robust growth rate of 10.80% CAGR, are benefiting from increasing regulatory challenges faced by synthetic azo dyes. Haematococcus astaxanthin, prized for its antioxidant potency, commands a premium price of USD 7,000 per kg. This high value enables producers to recover their significant capital investments within just five years. In the cosmetics industry, formulators are increasingly turning to beta-carotene for its ability to deliver natural sun-kissed shades. This trend not only diversifies revenue streams but also elevates the overall profile of carotenoids in the algae products market.

By Application: Food Dominance Extends Across Segments

In 2024, food and beverage applications command a dominant 48.93% market share and are also the fastest-growing segment, boasting an 8.22% CAGR through 2030. This surge was driven by launches in dairy alternatives, confectionery, and savory snacks, all harnessing the power of clean-label pigments and texturants. Recognizing the nutritional density of microalgae, product developers are now integrating microalgae powder into bars and drinks aimed at boosting immunity. Additionally, a swift regulatory process has eased the challenges of reformulation. The growing consumer demand for plant-based and sustainable ingredients further supports the adoption of algae products in this sector. Companies are also leveraging algae's versatility to create innovative textures and flavors in food applications.

Moving beyond the culinary realm, personal-care brands are turning to algal polysaccharides for their moisture-barrier creams. Meanwhile, sunscreens are incorporating mycosporine-like amino acids, ensuring reef-safe UVA absorption. The use of algae-derived ingredients aligns with the rising trend of eco-friendly and sustainable personal care products. Furthermore, advancements in algae cultivation techniques are enabling the production of high-quality ingredients tailored for the cosmetics industry. In the aquafeed sector, Veramaris’s plant in Nebraska plays a crucial role, supplying algal oil that caters to 15% of the global salmon industry's omega-3 requirements.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

In 2024, North America held a commanding 34.54% share of the algae products market. Multinationals find reassurance in the FDA's clear stance on color additives and its Generally Recognized as Safe (GRAS) processes. Meanwhile, public-private funding, exemplified by the Department of Energy's USD 20.2 million investment in algae-to-fuel consortia, bolsters technical advancements. In Alberta, pilots of cold-climate photobioreactors showcase potential cost parity, even at latitude 53°, expanding the region's agricultural possibilities. The region's focus on innovation and regulatory clarity has attracted significant investments from both domestic and international players. Additionally, advancements in photobioreactor technology are expected to further enhance production efficiency and scalability.

Asia-Pacific, projected to grow at an 8.98% CAGR through 2030, reaps benefits from China's mandates on microalgae biodiesel and its integrated aquaculture initiatives. Coastal provinces are incentivizing onshore raceway ponds, linking them to wastewater remediation goals, which in turn reduces input expenses. While Japan and South Korea focus on supplying high-purity strains for the cosmetics industry, ASEAN countries are capitalizing on their year-round sunlight to cultivate protein biomass for export. The region's diverse climatic conditions and government support create a conducive environment for algae cultivation. Furthermore, increasing demand for sustainable and renewable resources is driving innovation and partnerships across the Asia-Pacific algae products market.

Europe marries its sustainability agenda with robust research and development. The EU's 2024 inclusion of 20 new algae species in its Novel Food Catalogue accelerates commercial ventures. The Carbon Border Adjustment Mechanism is motivating steel producers to establish algal units on-site, allowing them to harness flue gas CO₂ and generate protein-rich biomass for animal feed. Additionally, Horizon Europe grants are fueling the expansion of integrated biorefineries, solidifying the continent's technological dominance in the global algae products arena. The region's commitment to reducing carbon emissions aligns with its push for algae-based solutions in various industries. Moreover, collaborations between academia and industry are fostering innovation and ensuring the scalability of algae-based technologies.

Note: Segment shares of all Individual segments will be available upon report purchase

Competitive Landscape

The algae products market is moderately consolidated. Companies like DSM-Firmenich, Corbion, and Cargill, Incorporated, leverage vertical integration, spanning from strain libraries to downstream formulation expertise. DSM-Firmenich has introduced Life’ DHA B54-0100, boasting a potency of 545 mg g¹DHA, which cuts capsule counts by 40%. This innovation not only alleviates consumer pill fatigue but also boosts retailer demand. Meanwhile, Corbion’s AlgaPrime DHA fermentation platform has secured multi-year supply contracts with producers of Chilean salmon, ensuring guaranteed off-take volumes.

Strategic partnerships are on the rise. Veramaris, a collaboration between DSM and Evonik, has poured USD 200 million into a Nebraska facility. This move aims to reduce reliance on fish-oil supply chains and achieve certification from the Aquaculture Stewardship Council. In another venture, PETRONAS and Euglena are teaming up in Malaysia to establish a biorefinery with a capacity of 650,000 t/y¹. Their focus on sustainable aviation fuel underscores a strategic move into high-value energy markets.

New entrants, driven by technology, are carving out unique niches. AlgaeCore has developed a spirulina-based smoked salmon, utilizing a proprietary decolorization method. This innovation allows them to replicate fish flesh without synthetic flavorings, positioning them for premium listings in delicatessens. On another front, Algenuity, a vendor of modular photobioreactors, has licensed its hydrogel-encapsulation technology to firms specializing in microalgae drug delivery. This partnership ensures Algenuity a steady annuity revenue from the reactors in use. Such diverse strategies are shaping a vibrant, albeit moderately concentrated, market for algae products.

Algae Products Industry Leaders

-

Cargill, Incorporated

-

Corbion

-

BASF

-

Archer Daniels Midland Company

-

DSM-Firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: FDA approved Galdieria extract blue as a color additive exempt from certification, derived from unicellular red algae Galdieria sulphuraria. The approval expands natural colorant options for food manufacturers and validates algae-derived ingredients for mainstream applications.

- October 2024: Dsm-firmenich launched life's DHA B54-0100, a high-potency algal oil containing 545mg DHA and 80mg EPA per gram, enabling smaller supplement capsules and addressing omega-3 deficiency gaps. The product launch represents a significant advancement in algae-derived omega-3 technology and supports the company's expansion in North American markets.

- October 2024: Algiecel secured EUR 6.5 million equity funding to scale microalgae production for feed and food industries, targeting CO2-emitting industries for bioreactor feedstock while producing high-value biomass and bio-oil.

- April 2024: European Commission approved beta-glucan from Euglena gracilis microalgae as a novel food, with Kemin Foods receiving five-year exclusivity for its applications in cereal bars, yogurts, and meal replacement beverages. The approval opens immunity supplement markets for algae-derived beta-glucan.

Global Algae Products Market Report Scope

Algae products, derived from single-celled aquatic organisms, boast a rich nutritional profile. These products find applications in dietary supplements, personal care, and pharmaceuticals.

The algae products market is categorized by source, product type, application, and geography. Sources include Brown Algae, Red Algae, Green Algae, and Blue-green Algae. Product types encompass Algal Protein, Alginate, Carrageenan, Carotenoids, Lipids, and other variants. Applications range from Personal Care, Food and Beverage, Dietary Supplements, and Pharmaceuticals to Animal Feed and Others. The report also provides a geographical analysis of the market, focusing on both developed and emerging regions, namely North America, Europe, Asia Pacific, South America, and the Middle East and Africa.

Market sizing is presented in USD value terms for all segments mentioned above.

| By Source | Brown Algae | ||

| Red Algae | |||

| Green Algae | |||

| Blue-green Algae | |||

| By Product Type | Hydrocolloids | Carrageenan | |

| Alginate | |||

| Others | |||

| Algal Protein | |||

| Carotenoids | |||

| Lipids | |||

| Other Product Types | |||

| By Application | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| Dietary Supplements | |||

| Pharmaceuticals | |||

| Animal Feed | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| Brown Algae |

| Red Algae |

| Green Algae |

| Blue-green Algae |

| Hydrocolloids | Carrageenan |

| Alginate | |

| Others | |

| Algal Protein | |

| Carotenoids | |

| Lipids | |

| Other Product Types |

| Food and Beverage |

| Personal Care and Cosmetics |

| Dietary Supplements |

| Pharmaceuticals |

| Animal Feed |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current size and growth trajectory of the global algae products market?

The global algae products market is valued at USD 3.85 billion in 2025 and is projected to reach USD 5.56 billion by 2030, exhibiting a compound annual growth rate of 7.64%.

Which product segments offer the highest growth potential?

Carotenoids represent the fastest-growing product segment at 10.80% CAGR through 2030. While hydrocolloids maintain market dominance with 45.93% share, carotenoids benefit from premium pricing and FDA initiatives to phase out synthetic food dyes.

Who are the key players in Algae Products Market?

Cargill, Incorporated, Corbion, BASF, Archer Daniels Midland Company, DSM-Firmenich are the major companies operating in the Algae Products Market.

What are the primary applications driving market demand?

Food and beverage applications dominate with 48.93% market share while simultaneously representing the fastest-growing segment at 8.22% CAGR.

Which region has the biggest share in Algae Products Market?

In 2024, the North America accounts for 34.54% of the algae products market.

What characterizes the competitive dynamics in the algae products market?

The market exhibits moderate concentration with a 6/10 concentration index, indicating sufficient competition to drive innovation while allowing established players to maintain strategic advantages.

Page last updated on: July 3, 2025