Market Overview

| Study Period | 2019 - 2031 |

|---|---|

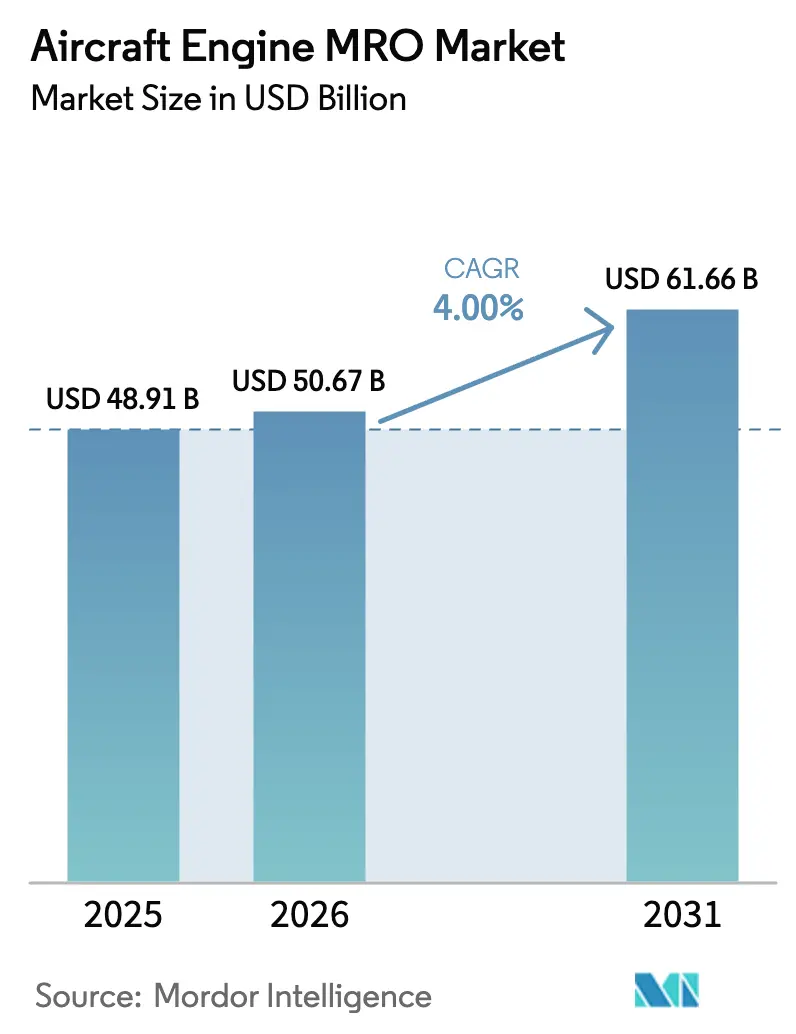

| Market Size (2026) | USD 50.67 Billion |

| Market Size (2031) | USD 61.66 Billion |

| Growth Rate (2026 - 2031) | 4.00% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Engine MRO Market Analysis by Mordor Intelligence

The aircraft engine mro market size is expected to grow from USD 48.91 billion in 2025 to USD 50.67 billion in 2026 and is forecasted to reach USD 61.66 billion by 2031 at a 4.00% CAGR over 2026-2031. This growth unfolds while operators struggle with powder-metal contamination in Pratt & Whitney GTF disks that lengthens shop visits to 250-300 days. Dust-related turbine-blade erosion on LEAP engines in desert environments has prompted CFM International to develop retrofit durability kits. Spare-engine lease rates have climbed to USD 200,000-350,000 per month, signaling tight capacity and lifting margins for lessors. OEMs defend high aftermarket profitability by restricting access to technical data and tooling, while additive manufacturing can shorten lead times by up to 90% for selected hot-section parts. Digital-twin analytics, led by Rolls-Royce and Airbus, now extend time-on-wing by nearly 50%, cutting unscheduled removals and reshaping competitive dynamics.

Key Report Takeaways

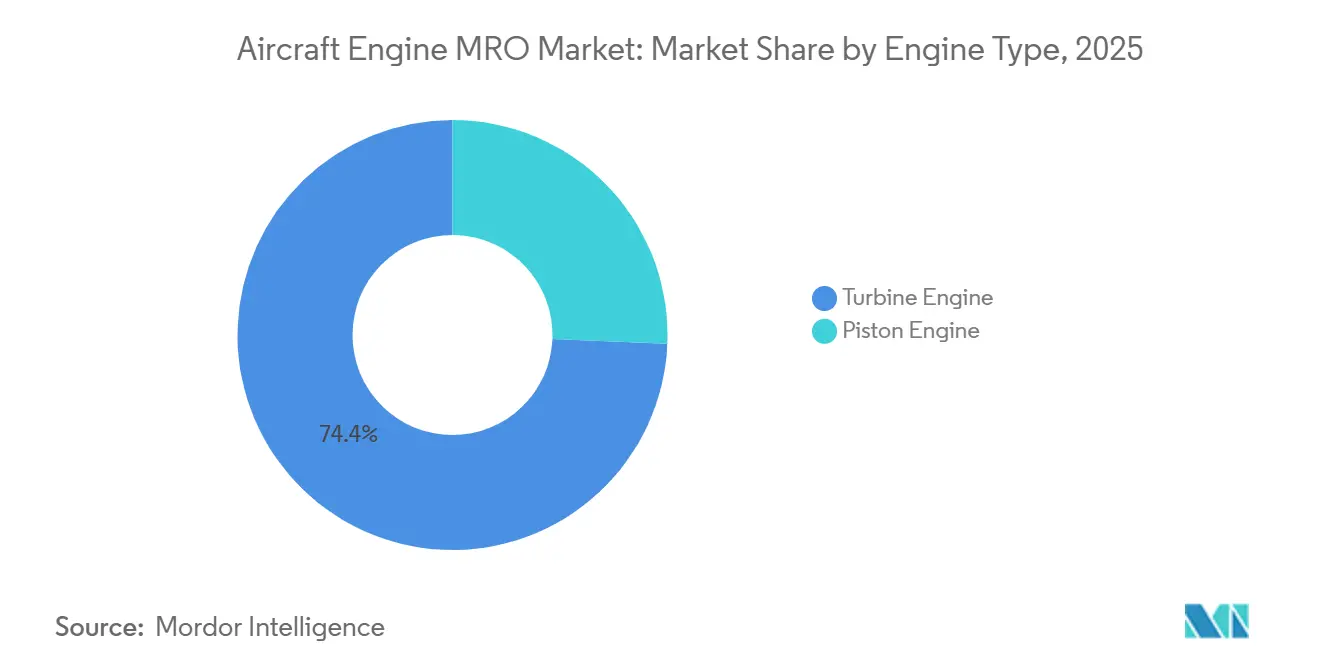

- By engine type, turbine engines accounted for 74.36% of the aircraft engine MRO market share in 2025 and are forecasted to expand at a 5.32% CAGR through 2031.

- By aviation, commercial aviation accounted for 62.67% of spending in 2025, whereas unmanned aerial vehicles are projected to grow at a 7.38% CAGR through 2031.

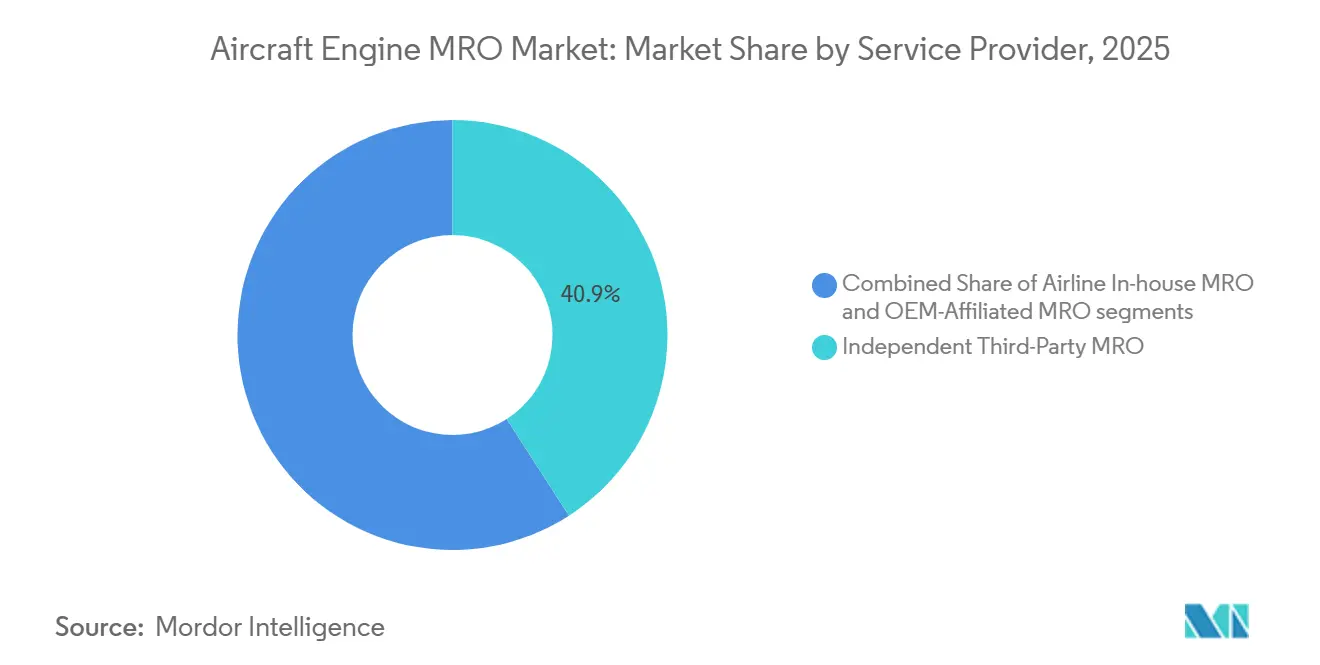

- By service providers, independent MROs accounted for 40.89% of shop visits in 2025; however, OEM-affiliated networks are projected to show the highest CAGR at 5.12% through 2031.

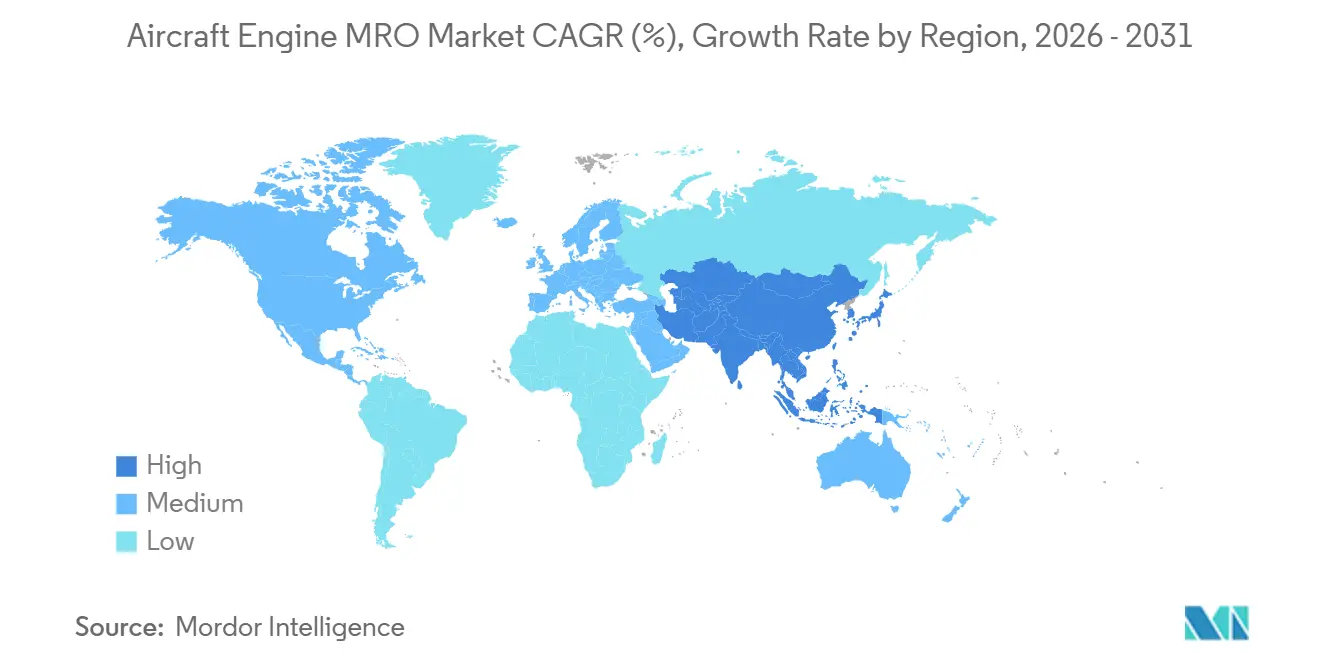

- By geography, the Asia-Pacific region is expected to deliver the fastest regional growth at a 6.65% CAGR, driven by more than USD 600 million in new capacity additions in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aircraft Engine MRO Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging narrow-body fleet growth and high flight-cycle utilization | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| OEM-mandated teardowns for LEAP and GTF durability fixes | +0.9% | Global, acute in Middle East, South Asia, North America | Short term (≤ 2 years) |

| Used-serviceable-material scarcity inflating shop-visit pricing | +0.6% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Digital-twin-based predictive maintenance adoption cuts unscheduled removals | +0.5% | North America, Europe, Asia-Pacific hubs | Long term (≥ 4 years) |

| Green-time leasing boom amid engine capacity bottlenecks | +0.4% | Global, led by North America and Europe lessors | Short term (≤ 2 years) |

| 3D-printed hot-section parts slash turnaround time | +0.3% | North America, Europe, select Asia-Pacific facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Narrow-Body Fleet Growth and High Flight-Cycle Utilization

Airbus reported 19,233 A320-family orders, with 7,262 units still undelivered. Notably, 72% of this backlog consists of A321neo variants, which accumulate 3,000-3,500 flight hours per year. Boeing 737 MAX operators in Asia-Pacific and Latin America routinely fly 11-12 block hours daily, shortening first shop-visit intervals on LEAP-1A and -1B engines to 8,000-9,000 cycles. This compression forces MROs to invest in modular tooling and flexible bays that absorb unpredictable surges, as demonstrated by Lufthansa Technik and ST Engineering facilities commissioned in 2024. Certification under FAA and EASA Part 145 remains essential to scale these high-cycle workloads. Consequently, the aircraft engine MRO market increasingly rewards providers that can synchronize manpower, tooling, and parts logistics without extending turnaround times.

OEM-Mandated Teardowns for LEAP and GTF Durability Fixes

Pratt & Whitney’s powder-metal contamination has sidelined more than 1,200 GTF engines, stretching shop visits to 250-300 days and grounding up to 12% of the active fleet. CFM International is simultaneously rolling out ceramic-matrix-composite shrouds and advanced coatings to fight blade erosion in dusty regions, compelling airline budgets to include inspections every 4,000-5,000 cycles.[1]Tony Osborne, “LEAP Blade Erosion Spurs Retrofit Kits,” aviationweek.com Delta TechOps increased GTF throughput by 30% to 450 annual shop visits after investing USD 50 million in tooling and additional staff. Pratt & Whitney has earmarked USD 3 billion for accelerating parts production and establishing regional repair hubs in Singapore and Poland. This mandatory work injects near-term volume but also heightens dependency on OEM-owned technical data, intensifying competition inside the aircraft engine MRO market.

Used-Serviceable-Material Scarcity Inflating Shop-Visit Pricing

AerFin logged a 50% increase in demand for rotable modules, as aircraft retirements decreased to 400 units in 2024, limiting the feedstock for teardown. Discounts on USM parts narrowed to 70-85% of new-part prices, resulting in reduced savings for airlines. PMA suppliers such as Heico and AAR responded by expanding FAA-approved parts that undercut OEM pricing by up to 40%. OEMs countered by bundling warranty coverage only with genuine parts, locking independents into higher material costs. The outcome is a 15-20% rise in average shop-visit invoices across the aircraft engine MRO market since 2023.

Digital-Twin Predictive Maintenance Adoption Cuts Unscheduled Removals

Rolls-Royce digital-twin algorithms have lengthened time-on-wing by 48% and cut unscheduled downtime by 30% on Trent and Pearl engines.[2]Rolls-Royce, “Digital-Twin Maintenance Performance,” rolls-royce.com Airbus Skywise aggregates operational data on more than 12,000 aircraft, enabling airlines to benchmark engine health in real-time. A study in the Journal of Air Transport Management found that digital twins reduce unplanned events by 7 hours per 1,000 flight hours, resulting in an annual savings of USD 210,000 per aircraft. OEM-affiliated MROs enjoy privileged access to telemetry that independents lack, creating data asymmetry within the aircraft engine MRO market. Independent providers are responding by recruiting data scientists and entering into direct feed agreements with airline operations centers, although progress remains gradual.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic global shortage of licensed engine technicians | -0.7% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Long-lead forgings and castings create prolonged TATs | -0.5% | Global, supply concentrated in North America | Medium term (2-4 years) |

| OEM aftermarket lock-ins squeeze independent MRO margins | -0.4% | Global, particularly impacting independent third-party MROs | Long term (≥ 4 years) |

| Escalating ESG compliance costs for chemical processing | -0.2% | Europe, North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Global Shortage of Licensed Engine Technicians

Boeing forecasts a need for 132,000 new maintenance personnel by 2043, while US retirements reach 14,500 annually against 6,000-8,000 graduates from FAA-approved schools.[3]Boeing, “Pilot and Technician Outlook 2024,” boeing.com European data indicate that 20% of mechanics are over 55, with limited cross-border mobility due to EASA Part 66 regulations. Starting salaries of USD 45,000-55,000 trail those of the technology sector, fueling attrition. MROs are automating borescope inspections and AI-assisted defect detection, but regulators still require human sign-offs, capping productivity gains. Labor scarcity, therefore, hinders the growth trajectory of the aircraft engine MRO market.

Long-Lead Forgings and Castings Prolong Turnaround

Titanium compressor disks now require 18-24 months to procure, up from 12-15 months before the pandemic. Nickel-superalloy single-crystal blades need 9-12 months, delaying engine re-delivery. Pratt & Whitney disclosed that forging bottlenecks slow GTF spare-engine deliveries by up to 90 days, and CFM faces similar delays on LEAP parts. GE Aerospace acquired additional forging capacity through a partnership with Arconic, while Rolls-Royce invested £90 million in its Rotherham plant to gain machining headroom. Independents, lacking capital for vertical integration, rely on consignment inventory, which erodes their pricing power within the aircraft engine MRO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Type: Turbine Engines Lead a Diverse Fleet

Turbine engines captured 74.36% of the aircraft engine MRO market share in 2025, with a projected annual growth rate of 5.32% during the forecast period, driven by their widespread use across commercial, military, and business jet fleets. Turbofan families, such as the CFM56, LEAP, Trent, and GEnx, generate the majority of shop visits, supported by high cycle counts on the A320 and 737 fleets. Turboprop demand follows regional aviation use of Pratt & Whitney Canada PT6 powerplants that exceed 400 million flight hours, turboshaft engines power over 20,000 UH-60 and AH-64 helicopters with GE T700 variants, keeping rotorcraft MRO steady.

Piston engines are projected to rise at a moderate CAGR as general aviation and UAV fleets expand; overhauls occur every 500-1,000 hours on delivery drones, bringing new revenue streams. Standardization under ASTM F3201 is expected to streamline the approval process for UAV maintenance. This trend positions niche providers to anchor specialization within the aircraft engine MRO market size for smaller propulsion categories.

By Aviation: Commercial Dominates While UAVs Accelerate

Commercial aviation accounted for 62.67% of 2025 spending, driven by narrow-body engines that face first-run overhauls at 8,000-10,000 cycles. Wide-body overhauls, although less frequent, are more expensive due to the replacement of fan blades and high-pressure turbine modules on GE90, Trent XWB, and GEnx engines.[4]Lufthansa Technik, “Widebody Engine MRO,” lufthansa-technik.com Regional jets comply with updated ICAO Annex 16 noise and emissions limits, sustaining moderate MRO volume.

Military budgets contribute USD 8-9 billion yearly, with the F135 depot network supporting 6,000-hour overhauls on the expanding F-35 fleet. Transport aircraft, such as the C-130J and C-17, operate under performance-based logistics that guarantee availability. UAVs remain the fastest-growing slice of the aircraft engine MRO market, advancing at a 7.38% CAGR through 2031 as defense ministries and logistics firms expand their drone fleets.

By Service Provider: OEM Networks Extend Control

Independent MROs accounted for 40.89% of shop visits in 2025 by pricing 10-15% below OEM rates, utilizing PMA parts and DER repairs. Yet OEM-affiliated networks from GE, Rolls-Royce, Pratt & Whitney, and Safran grow at a 5.12% CAGR by leveraging embedded telemetry and warranty bundling. Airline in-house arms such as Delta TechOps and Lufthansa Technik absorb excess capacity, selectively serving third-party customers for margin diversification.

Tooling outlays of USD 5-10 million per engine type, plus annual data fees of USD 50,000-200,000, restrict independent entry into next-generation platforms. Niche expertise in directed-energy deposition blade repairs at AAR or legacy CFM56 overhauls at Magnetic MRO exemplifies the survival strategies employed by independent companies in the aircraft engine MRO market.

Geography Analysis

North America accounted for 29.91% of 2025 revenues, with mature commercial and military fleets serviced by Delta TechOps, StandardAero, and AAR facilities that manage over 1,000 annual shop visits. Technician shortages, however, push wages higher and limit expansion pace, while proximity to GE, Pratt & Whitney, and Honeywell sustains rapid parts logistics.

Asia-Pacific, advancing at a 6.65% CAGR, recorded more than USD 600 million of investment in 2024 alone, including GAMECO’s USD 500 million LEAP and Trent project in China and Pratt & Whitney’s USD 200 million joint venture with Air India.[5]Financial Times, “Asia-Pacific MRO Investments,” ft.com ST Engineering has committed USD 100 million to developing wide-body capability in Singapore, while Rolls-Royce operates a Trent hub there. The regional fleet is forecast to exceed 17,000 aircraft by 2043, reinforcing long-term workload within the aircraft engine MRO market.

Europe’s established players, Lufthansa Technik, Air France-KLM, and SR Technics, continue to expand; Lufthansa Technik has invested USD 150 million in Poland for Trent XWB and GEnx work. Safran doubled LEAP capacity in Morocco, illustrating a southward shift toward cost-competitive labor. The Middle East leverages state backing at Sanad and Turkish Technic to capture regional workloads. South America and Africa remain under-served, forcing operators to ferry engines abroad and inflating logistics costs, an imbalance that signals future white-space within the aircraft engine MRO market.

Competitive Landscape

OEM-affiliated networks collectively manage 35-40% of global shop visits and earn 25-30% operating margins through data exclusivity and proprietary tooling. GE Aerospace expanded MRO sites in Poland and India, Rolls-Royce invested GBP 90 million (USD 120.69 million) in Rotherham machining, and Pratt & Whitney formed a USD 200 million Indian joint venture, strengthening footholds in growth regions.

Independent providers counter with specialization. StandardAero guarantees 120-day turnarounds under performance-based contracts, AAR offers rapid blade repairs, and ST Engineering integrates predictive analytics to offset data gaps. PMA suppliers, such as Heico, penetrate the market at price points 30-40% below OEM parts, exerting downward pressure on material margins. Additive manufacturing reshapes competitive edges; GE has already cut lead times by 90% on selected components, and MTU won EASA approval for 3D-printed blade repairs.

Regulatory compliance under FAA and EASA Part 145 ensures that quality systems scale with volume, serving as a barrier to new entrants. The aircraft engine MRO market, therefore, balances between capital-intensive OEM franchises and agile independents that exploit niche technologies or legacy platforms to sustain their share.

Aircraft Engine MRO Industry Leaders

General Electric Company

Safran SA

Lufthansa Technik AG

Rolls-Royce Holdings plc

RTX Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Air Arabia and Lufthansa Technik signed a long-term contract for comprehensive engine MRO (Maintenance, Repair, and Overhaul) services for the CFM56-5B engines powering the airline's fleet of 43 Airbus A320ceo aircraft.

- March 2025: MTU Maintenance Zhuhai and All Nippon Airways (ANA) signed a contract for the maintenance, repair, and overhaul (MRO) of the CFM56-7B engines powering ANA's fleet of 47 Boeing 737NG aircraft. This agreement highlights the long-standing collaboration between Japan's largest airline and Asia's leading provider of customized MRO solutions for aero engines.

- October 2024: ST Engineering's Commercial Aerospace division signed a 15-year MRO contract with Indian carrier Akasa Air to provide MRO services for the LEAP-1B engines powering its Boeing 737 MAX fleet.

- January 2026: GE Aerospace secured a USD 1.4 billion contract from the US Navy to supply T408 engines for the CH-53K Stallion helicopters. These engines will address new deliveries, replacements, and sustainment needs.

Global Aircraft Engine MRO Market Report Scope

Engine maintenance, repair, and overhaul (MRO) involves the repair, servicing, or inspection of engines to ensure the safety and airworthiness of the aircraft in accordance with international standards.

The aircraft engine MRO market is segmented by engine type, aviation, service providers, and geography. By engine type, the market is segmented into turbine engines and piston engines. The turbine engine is further segmented into turbofan engines, turboprop engines, turboshaft engines, and turbojet engines. By aviation, the market is segmented into commercial aviation, military aviation, general aviation, and UAVs. Commercial aviation includes narrowbody, widebody, and regional jets. The military aviation segment encompasses combat, transport, special mission, and helicopter operations. General aviation covers business jets and commercial helicopters. The market is segmented into airline in-house MRO, independent third-party MRO, and OEM-affiliated MRO, as provided by service providers.

The report offers the market size and forecasts for major countries across the regions. For each segment, the market sizing and projections were made based on value (USD).

By Engine Type

| Turbine Engine | Turbofan Engine |

| Turboprop Engine | |

| Turboshaft Engine | |

| Turbojet Engine | |

| Piston Engine |

By Aviation

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Combat |

| Transport | |

| Special Mission | |

| Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters | |

| Unmanned Aerial Vehicles (UAVs) |

By Service Providers

| Airline In-house MRO |

| Independent Third-Party MRO |

| OEM-Affiliated MRO |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | Egypt | |

| Rest of Africa | ||

| By Engine Type | Turbine Engine | Turbofan Engine | |

| Turboprop Engine | |||

| Turboshaft Engine | |||

| Turbojet Engine | |||

| Piston Engine | |||

| By Aviation | Commercial Aviation | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military Aviation | Combat | ||

| Transport | |||

| Special Mission | |||

| Helicopters | |||

| General Aviation | Business Jets | ||

| Commercial Helicopters | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By Service Providers | Airline In-house MRO | ||

| Independent Third-Party MRO | |||

| OEM-Affiliated MRO | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | Egypt | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the aircraft engine MRO market be by 2031?

It is expected to reach USD 61.66 billion by 2031 on a 4.00% CAGR trajectory.

Which engine type draws the most maintenance spending?

Turbine engines hold 74.36% of 2025 value, reflecting their use across commercial, military, and business-jet fleets.

Why are spare-engine lease rates so high in 2026?

Extended shop-visit times for GTF and LEAP engines have driven monthly lease prices to USD 200,000-350,000 as operators secure additional coverage.

Which region is expanding maintenance capacity fastest?

Asia-Pacific leads with a 6.65% CAGR and more than USD 600 million invested in new facilities during 2024.

How is additive manufacturing changing overhaul economics?

How is additive manufacturing changing overhaul economics?

Page last updated on: