Colombia Agriculture Market Analysis by Mordor Intelligence

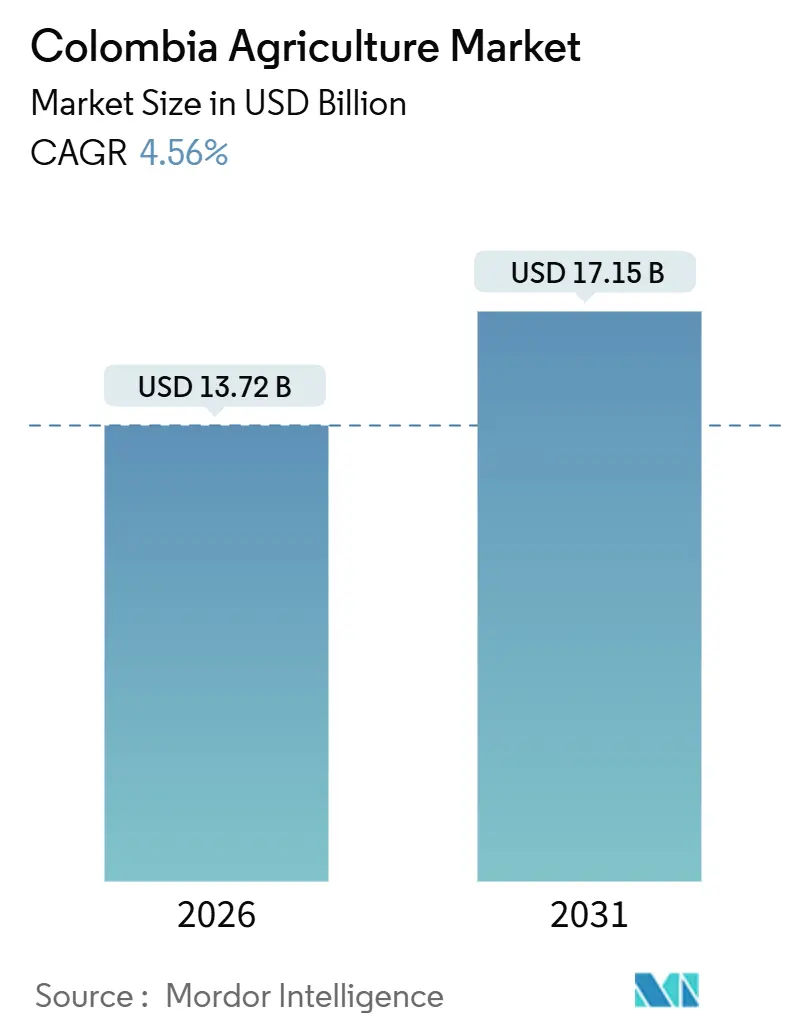

The Colombia agriculture market size is estimated to be USD 13.72 billion in 2026 and is projected to grow to USD 17.15 billion by 2031, with a compound annual growth rate (CAGR) of 4.56%. Growth drivers include increasing demand for climate-smart commodities, recovery in coffee yields following the 2024 drought, biodiesel mandates for palm oil, and strong export performance in Hass avocados. The market faces challenges such as structural land tenure issues, growing feed-grain deficits, and climate variability associated with the El Niño and La Niña cycles. Multinational processors are strengthening partnerships focused on traceability and biodiversity-positive supply chains, while public-private irrigation initiatives in Orinoquia are expanding agricultural opportunities. Additionally, fluctuations in voluntary carbon credit prices and parametric insurance pilot programs are influencing producer investment decisions. Despite these challenges, the Colombia agriculture market is projected to achieve steady growth, driven by productivity improvements that mitigate logistical and climate-related obstacles.

Key Report Takeaways

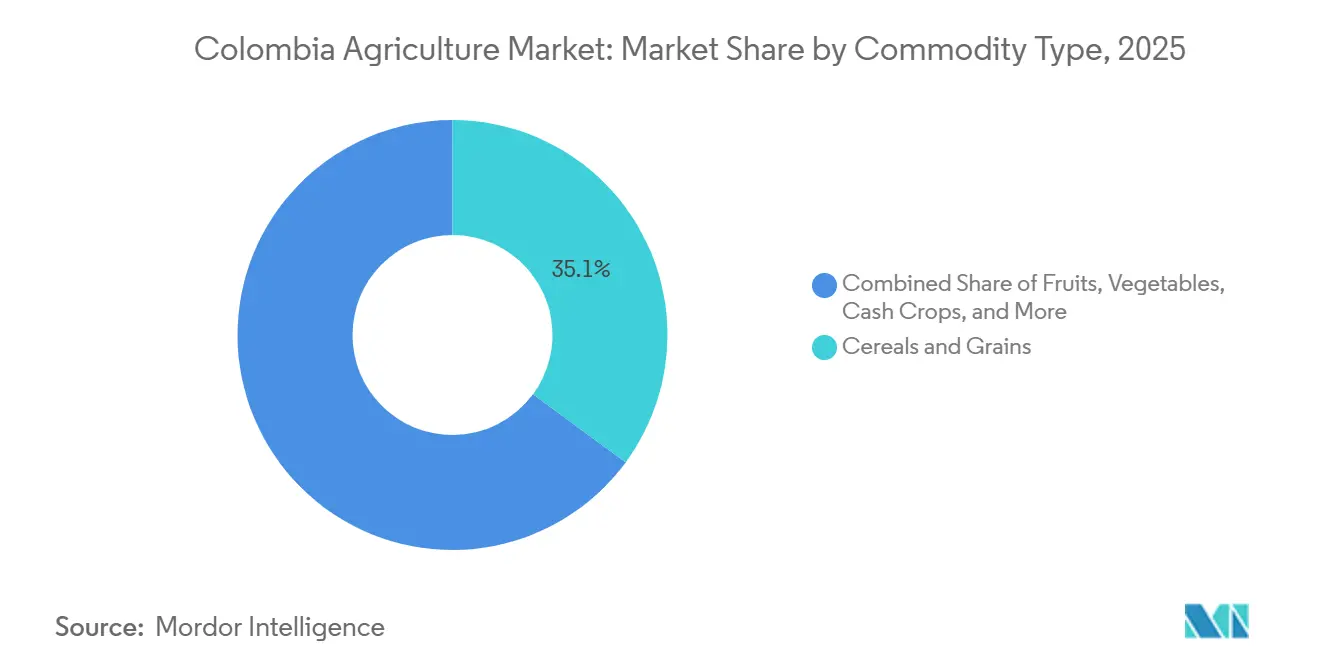

- By commodity type, cereals and grains accounted for 35.1% of the Colombia agriculture market share in 2025. Oilseeds and pulses are forecast to post the highest 5.1% CAGR, making them the fastest-growing segment of the market through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Colombia Agriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust global appetite for specialty coffee and cacao | +0.7% | Antioquia, Huila, Santander, and Arauca | Medium term (2-4 years) |

| Carbon-smart certification premiums for zero-deforestation supply | +0.6% | Orinoquia, Amazon piedmont, and Pacific coast palm zones | Long term (≥ 4 years) |

| Scaling irrigation in Orinoquia savanna through public-private partnerships | +0.5% | Meta, Casanare, and Vichada | Long term (≥ 4 years) |

| Growing corporate demand for biodiversity-positive ingredients | +0.4% | Nationwide, early in export-oriented fruit and cacao sectors | Medium term (2-4 years) |

| Direct-to-roaster and farm-to-table export platforms boosting farmer margins | +0.2% | Coffee zones of Huila, Nariño, and Cauca; emerging avocado and cacao regions | Short term (≤ 2 years) |

| Crop-loss parametric insurance backed by multilateral climate funds | +0.1% | Nationwide pilot programs in coffee and rice regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust Global Appetite for Specialty Coffee and Cacao

Specialty-grade coffee accounts for approximately 40% of Colombia's national coffee output, driven by smallholder investments in wet mills and varietal improvements that consistently achieve cupping scores exceeding 80 points [1]Source: United States Department of Agriculture Foreign Agricultural Service, “Coffee Annual – Colombia 2024,” USDA.GOV. Colombian Milds futures reached a peak of USD 7,040 per metric ton in January 2025, influenced by drought conditions in Brazil that reduced arabica inventories. Fine-flavor cacao initiatives in Meta and Santander have achieved premiums of 20% to 30% over commodity-grade beans, supported by georeferenced traceability systems that comply with European Union regulations on deforestation. Exporters benefit as roasters in North America and Europe increasingly favor transparent, single-origin lots that emphasize farm-level climate resilience. As a result, the Colombian agriculture market secures higher average unit prices for coffee and cacao, contributing to improved rural incomes and greater reinvestment capacity.

Carbon-Smart Certification Premiums for Zero-Deforestation Supply

The Roundtable on Sustainable Palm Oil (RSPO) certification has become a standard requirement for Colombian exporters seeking to target biodiesel sales in the European Union. Early adopters, such as Daabon Organic and Oleoflores, have focused on protecting high-conservation-value areas. In the Orinoquia region, 3,800 hectares of cacao agroforestry have been established since 2020 with support from the International Finance Corporation's technical assistance program, integrating carbon sequestration with increased farmer income [2]Source: International Finance Corporation, “Orinoquia Cacao Program,” IFC.ORG. Despite voluntary carbon credit prices declining to USD 3-5 per metric ton in 2024, global companies like Nestlé continue to include zero-deforestation clauses in their contracts. Additionally, the Colombian government's emphasis on climate-smart agriculture within the 2024-2027 World Bank framework further drives demand for certifications. These factors collectively support growth in Colombia's agriculture market, even as carbon revenue remains limited.

Scaling Irrigation in Orinoquia Savanna Through Public-Private Partnerships

The Meta, Casanare, and Vichada departments encompass 25 million hectares of flat savanna, which can achieve grain yields comparable to those of the Cerrado region once soil acidity is addressed. In August 2024, a USD 99.9 million funding agreement was signed between the Colombian government and the Corporación Andina de Fomento (CAF) Development Bank to expedite canal construction and soil amendment initiatives. Pilot plots for rice and corn have already achieved yield levels comparable to those of leading Brazilian benchmarks, and double-cropping is becoming viable with the availability of dry-season water. Additionally, improved road infrastructure under the fourth-generation infrastructure program has reduced haulage times to Caribbean ports, supporting the diversification of Colombia's agriculture market beyond the highland zones, which face land constraints.

Growing Corporate Demand for Biodiversity-Positive Ingredients

Major buyers, such as Cargill, Incorporated, are now monitoring on-farm habitat indicators and incentivizing producers who meet canopy and buffer zone requirements. Through its Intel4Value initiative, Cargill trained over 1,100 palm growers in 2024 on establishing riparian buffers and implementing integrated pest management practices. This initiative not only enhances sustainable farming practices but also contributes to long-term environmental conservation. Additionally, the reVive Hub, launched by the IDH Sustainable Trade Initiative, aims to restore 3,000 hectares of degraded land while involving 9,500 farmers across coffee, palm, and cacao supply chains. The program focuses on enhancing soil health, promoting biodiversity, and fostering sustainable livelihoods for farmers. The steep altitudinal gradients of Colombian landscapes enable farms to support the recovery of endemic species, providing the Colombian agricultural market with a competitive advantage in niche ingredients favored by premium food brands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented land titles limiting collateralization for credit | -0.5% | Nationwide, acute in Caquetá, Putumayo, and Chocó | Long term (≥ 4 years) |

| Exposure to La Niña and El Niño yield volatility | -0.7% | Coffee zones of Huila, Cauca, Nariño; rice belts of Tolima and Meta | Short term (≤ 2 years) |

| Rising rural security costs in post-peace-deal zones | -0.3% | Caquetá, Putumayo, Norte de Santander, and Arauca | Medium term (2-4 years) |

| Uncertain carbon price trajectories in voluntary markets | -0.4% | Nationwide, affecting agroforestry and REDD Plus economics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Land Titles Limiting Collateralization for Credit

Approximately 40% of rural parcels in Colombia lack registered deeds, which limits farmers' ability to use their land as collateral for loans [3]Source: World Bank, “Colombia Country Partnership Framework 2024–2027,” WORLDBANK.ORG. This issue significantly impacts access to formal credit, forcing commercial lenders to rely on Banco Agrario’s subsidized credit lines, while informal lenders charge interest rates exceeding 30% annually, further burdening farmers. In 2023, a land formalization plan allocated USD 4.25 billion for land purchase and redistribution, but progress has been hindered by cadastral backlogs and overlapping land claims in post-conflict regions, which have delayed the intended benefits. The average coffee farm size is just 1.5 hectares, restricting mechanization, economies of scale, and access to bulk-input discounts, which are critical for cost efficiency. Until land titling efforts accelerate and address these challenges, credit penetration in Colombia's agriculture market will remain below that of regional counterparts, limiting the sector's growth potential.

Exposure to La Niña and El Niño Yield Volatility

The 2023-2024 El Niño drought reduced coffee flowering, significantly impacting production levels. The subsequent 2024-2025 La Niña rains exacerbated the situation by triggering fungal outbreaks, which further decreased November 2025 production by 28% to 1.26 million bags. In addition to coffee, rice paddies in Tolima and Meta suffered from nutrient leaching during floods, leading to reduced soil fertility and lower yields. Similarly, palm bunch yields in Magdalena declined during dry periods, highlighting the vulnerability of key crops to climatic variations. Climate models indicate stronger oscillations in the future, which are projected to intensify risks for the Colombian agriculture market. To mitigate these challenges, the widespread adoption of drought-tolerant seeds, shade trees, and micro-irrigation systems will be critical for ensuring agricultural resilience and sustainability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Commodity Type: Cereals Anchor Value While Oilseeds Accelerate

Cereals and grains accounted for the largest share, representing 35.1% of the Colombia agriculture market size in 2025, driven by strong feed demand from industrial poultry and swine operations. According to the United States Department of Agriculture, domestic rice production reached 2.05 million metric tons in 2024, supported by milling clusters located in Tolima and Meta. However, wheat remains almost entirely reliant on imports. Tariffs on milled rice help stabilize farm prices but contribute to higher consumer costs. With limited potential for arable land expansion in traditional grain-producing regions, future growth in cereals will depend on productivity improvements and the development of the Orinoquia region.

Oilseeds and pulses are projected to grow at a compound annual growth rate (CAGR) of 5.1% from 2026 to 2031, making them the fastest-growing segment in Colombia’s agriculture market. Palm plantations, covering 590,000 hectares, produced approximately 1.8 million metric tons of oil in 2024, supporting a national biodiesel blend of 12%. In the same year, soybean meal imports totaled 1.2 million metric tons, primarily used in concentrated animal feed operations. Trials in the Orinoquia region aim to localize soybean supply in the future. While fruits like avocados are experiencing rapid growth, oilseeds benefit from policy mandates and increasing global demand for biofuels, positioning this segment for sustained growth within the overall Colombia agriculture market size.

Geography Analysis

Coffee and cacao dominate the Andean highlands, spanning Huila, Cauca, Nariño, Antioquia, and Santander. Production rebounded to 12.8 million bags in 2024 but remains vulnerable to climate fluctuations, as evidenced by the decline in November 2025 during the La Niña rains. Avocado orchards in Antioquia and Tolima benefit from off-season harvest periods that align with Northern Hemisphere demand. Additionally, silvopastoral dairy systems in Boyacá contribute to Alpina’s sustainability objectives. Land fragmentation, averaging below two hectares, limits mechanization but supports the cultivation of diverse specialty crops, strengthening the Colombia agriculture market.

The Orinoquia savanna, encompassing Meta, Casanare, and Vichada, represents Colombia’s agricultural frontier. Investments in public-private irrigation projects, lime application, and improved road infrastructure are transforming acidic oxisols into productive grain fields, with yields comparable to Brazil when inputs are optimized. The International Finance Corporation has supported cacao agroforestry, while the World Bank has allocated funds for climate-resilient agriculture through 2027. Although logistics costs remain higher than in coastal regions, enhanced connectivity is reducing this disparity, positioning Orinoquia as a critical area for future growth in the Colombia agriculture market.

Caribbean and Pacific coastal departments, including Magdalena, Cesar, Córdoba, and Nariño, primarily focus on the production of palm oil, bananas, and cacao. Compliance with Roundtable on Sustainable Palm Oil certification is increasingly important as European buyers demand zero-deforestation supply chains, prompting estates to formalize conservation zones. Banana exporters ship approximately 100 million boxes annually from Urabá and Magdalena, though stringent biosecurity measures are necessary to manage the risk of Tropical Race 4 fungus. In the Pacific region, heavy rainfall complicates harvest logistics, but biodiversity premiums for cacao and oil palm help offset some costs, ensuring the region's continued contribution to Colombia's agriculture market revenues.

Value Chain Analysis

Colombia's crop value chain starts with inputs (seeds, fertilizers, crop protection, machinery services) sourced through local ag-retail networks and, for several categories, through import-dependent channels that feed large grain and plantation crop areas. On-farm production remains dominated by smallholders in coffee and cacao, with the Federación Nacional de Cafeteros de Colombia acting as an organizing buyer and service platform, alongside more integrated plantation-style systems in palm and export fruits. National production reached 81.66 million tons in 2025, up 3.0% versus 2024, which points to sustained upstream demand for inputs, extension, and risk-management tools.

Midstream aggregation and first transformation center on wet mills and cooperative collection points in coffee, estate mills and biodiesel-linked assets in palm (for example, Oleoflores and Daabon Organic), and packhouses for export fruit. Grain and feed flows connect farms and imports to storage, mills, and livestock-feed demand, with multinational traders such as Cargill, Louis Dreyfus Company, and Olam operating through Caribbean nodes (Cartagena and Barranquilla) to balance domestic deficits. Downstream distribution spans wholesale markets, modern retail, and export channels. UPRA reported food supply in major wholesale markets rose 9.8% in March 2025 versus a year earlier. Export logistics are increasingly tied to traceability and sustainability requirements, reflected in partnerships such as Cargill and Solidaridad, which trained 880 palm growers through end-2026 on sustainability indices and carbon baselines, and Fresh Del Monte's August 2025 joint venture with Managro to expand avocado and lime packing for North American and European markets. Separately, 2025 agricultural and agroindustrial exports reached USD 15.317 million, up 33.5% in value versus 2024, raising throughput needs in cold chain, quality labs, and documentation.

Competitive Landscape

The Colombia agriculture market is moderately fragmented. The Federación Nacional de Cafeteros de Colombia operates a federated purchasing system that encompasses 540,000 families. This system stabilizes prices but restricts the entry of private processors. In the palm oil refining segment, there is moderate market concentration, with Grupo Nutresa S.A., Oleoflores S.A., and Daabon Organic S.A.S. managing integrated mills and biodiesel assets. Grupo Nutresa S.A. reported sales of COP 18.6 trillion (USD 4.6 billion) in 2024, with 60% of revenue generated from domestic operations. Additionally, multinational traders such as Cargill, Incorporated, Louis Dreyfus Company B.V., and Olam Group Limited operate grain terminals in Cartagena and Barranquilla, ensuring a consistent supply of corn and soy for feed mills.

Strategic initiatives in the market increasingly emphasize sustainability and traceability. In February 2025, Olam Group Limited agreed to sell a 64.57% stake in Olam Agri to Saudi Agricultural and Livestock Investment Company for USD 1.78 billion, a move that may shift procurement priorities toward Middle Eastern food security. Ecopetrol announced plans for a USD 700 million sustainable aviation fuel plant, which is projected to increase demand for domestic oilseeds starting in 2027. Furthermore, Cargill, Incorporated's Intel4Value program and the Federación Nacional de Cafeteros de Colombia georeferencing platform enhance supply chain transparency, which is becoming a critical competitive factor in the Colombia agriculture market.

Emerging disruptors in the market include blockchain-based coffee traceability pilots by Casa Luker and direct-trade networks supported by responsAbility at Procafecol. These models reduce intermediary margins and increase farmer earnings, fostering loyalty to platforms that provide both market access and certification services. Additionally, parametric insurance bundled with Banco Agrario credit reduces default risks, encouraging lenders to finance smallholder upgrades. Companies adopting regenerative practices are securing premium buyers, shifting the competitive focus from scale alone to verified environmental and social performance.

Market Opportunities and Future Outlook

Orinoquia remains the clearest expansion corridor where capital, land-use programs, and climate-smart practices intersect. The CAF-backed August 2024 agreement (USD 99.9 million) to accelerate irrigation canals and soil amendment in Meta, Casanare, and Vichada supports double-cropping economics and helps reduce dry-season yield volatility. New nature-based projects are also widening farm-system options: GeoPark and the Cataruben Foundation launched the Orinoquia Regenera initiative in January 2026 across 80,000 hectares in Meta and Casanare with USD 3 million financing from Bancolombia, centered on silvopastoral models and carbon-credit-linked land restoration. These programs translate into demand for lime, seeds, irrigation hardware, farm services, and measurement, reporting, and verification (MRV) capabilities tied to biodiversity and carbon claims.

Digitization and differentiated export supply chains are also creating openings beyond traditional spot-market selling. MinTIC and the Ministry of Agriculture's AGROTECH program targets 14 departments with digital tools, satellite monitoring, and training, while private technical-assistance models continue to scale (Precisagro reported digital monitoring and assistance across 216,992 hectares in May 2026). In export-oriented horticulture, financing is extending from production into packing infrastructure, shown by Grupo Cartama's USD 119 million project finance package (May 2025) to expand avocado capacity and facilities, alongside new avocado processing investments entering the country. On the policy side, CONPES 4184 (February 2026) earmarks COP 18.6 trillion over 2026-2036 for agrarian reform focused on land and water redistribution, which raises the emphasis on formalization, irrigation governance, and producer services for converting redistributed or regularized land into bankable, market-connected crop output.

Recent Industry Developments

- July 2026: Baika opened a new avocado plant in Colombia, adding in-country capacity for handling and preparing export-grade fruit. The expansion is intended to help Colombia meet tighter destination-market specifications for Hass avocado supply chains.

- June 2026: Yara Colombia announced an expansion of its Mamonal plant in Cartagena to raise annual NPK fertilizer output by 80,000 tons and lift total capacity by 25%. The capacity addition is aimed at improving local availability of blended nutrients used in yield recovery for grains, coffee renovation, and export fruit productivity programs.

- May 2025: Grupo Cartama secured a USD 119 million project finance package from Bancolombia, Banco Davivienda, and BBVA to expand avocado production and infrastructure. The funding supports orchard development and packhouse-linked investments as Colombia builds more scaled, export-aligned horticulture value chains.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the farm-gate value generated from crop production within Colombia, where volumes harvested are converted into value using producer price signals and then consolidated into one national total.

Scope exclusions: livestock, aquaculture, forestry outputs, and downstream food or biofuel processing margins are excluded.

Segmentation Overview

- By Commodity Type

- Cereals and Grains

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Oilseeds and Pulses

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Fruits

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Vegetables

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Cash Crops

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Cereals and Grains

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to anchor the model on observable supply, price, and trade signals for Colombia crops. We relied on public agricultural statistics such as national crop production and farm price series from government sources, FAOSTAT crop balance views, and trade flows from UN Comtrade style customs datasets for key export crops.

To keep assumptions consistent across crops, we also reviewed sources such as producer price indices and inflation series from official statistics, agronomy and yield papers from peer reviewed journals, and local association publications for plantation crops (for example coffee and bananas). Company filings, investor presentations, and reputable press were used mainly to cross-check major acreage shifts, weather impacts, and farm input tightness. Where needed, we used paid subscription databases for shipment level trade checks and for patent and technology scanning to validate directionality rather than to set final values. The sources listed here are illustrative, and many other public and paid references were used during data collection, clarification, and validation.

Primary Interviews and Surveys

Primary work focused on confirming what actually moved the market in the last two to three seasons, and on stress testing the price and yield assumptions used in the model. We spoke with growers, exporters, processors close to procurement, input distributors, and advisors. Coverage was balanced across major producing zones and trading corridors, so gaps from desk research could be closed in a practical way.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 20% | |

| Mid tier: 46% | Functional/Unit leaders: 30% | |

| Smaller Players: 21% | Managers: 50% |

Market-Sizing & Forecasting

The core sizing logic is top-down and built from crop level production volumes and harvested area, which are then paired with producer price series to reconstruct farm-gate value for the country. We corroborate totals using selective bottom-up approximations, including sampled price per ton checks from buyer and exporter discussions, and simple volume roll ups for the largest plantation crops where reporting is more consistent.

Key inputs include harvested area trends by crop, yield per hectare movement, weather and climate disruption patterns that affect seasonality, export share for cash crops, and producer price behavior in local currency. These variables help separate whether growth comes from real output changes, a crop mix shift, or a price cycle, since agriculture value can increase even when volumes are flat.

Forecasting uses scenario analysis supported by short ARIMA based smoothing on producer prices and output series, then the scenarios are adjusted using primary feedback on expected acreage, input affordability, and likely yield recovery or pressure. When public reporting is weak for a crop in a given year, we fill gaps using nearby crop proxies and trade signals, and then reconcile the result back to national totals during the final review.

Data Validation & Update Cycle

Validation is done in steps, starting with internal consistency checks across volumes, prices, and implied value per ton. We then compare results against independent signals such as export volumes, farm price indices, and major event timelines like droughts or disease outbreaks. When large variances are seen, assumptions are revisited, and we re contact a small set of primary respondents to confirm whether the issue is a data break, a crop mix change, or a temporary pricing spike.

Before sign off, another analyst reviews model logic, unit conversions, and currency handling so totals remain traceable to the same input series. Reports are refreshed annually, and interim updates are triggered when there are material shocks such as sharp currency moves, policy shifts affecting exports, or a major production disruption. Right before delivery, a final pass is performed so clients receive the latest version of key series and conclusions.

Mordor Intelligence's Colombia Agriculture Market Size Versus Other Published Estimates

It is normal to see different published market sizes for Colombia agriculture because teams do not always value the same thing at the same point in the chain. Differences usually come from what is included (only crops vs crops plus livestock), whether values are counted at farm gate or later in processing, and how currency conversion and price averages are applied.

Another driver is refresh cadence and the timing of price series, since agriculture values can change quickly with FX and season level producer prices. In this study, producer prices are updated to the most recent available season and converted using consistent currency timing, and those checks are refreshed during the review cycle. That approach helps explain why the headline value can sit away from older snapshots, which is a practice used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.72 B (2026) | |

| Global Research Publisher A | USD 9.77 B (2024) | Uses an earlier base year snapshot and can reflect different currency timing, which matters when local prices and FX move quickly. The scope description is broad, and it may not match a strict farm-gate crop-only valuation approach. |

| Regional Consultancy B | USD 18.70 B (2026) | Often applies a wider scope that can fold in livestock or agro-processing linked value, which pushes totals up versus a crop farm-gate definition. The longer horizon and faster growth setup can also embed more aggressive price and productivity assumptions. |

Taken together, the spread is mainly explained by timing and boundary choices, not one single arithmetic difference. By keeping the valuation tied to crop volumes and producer prices, and then re checking the implied value per ton against trade and primary feedback, we provide a practical number that can be repeated year after year with the same inputs.

Key Questions Answered in the Report

How large is the Colombia agriculture market in 2026?

The Colombia agriculture market size is USD 13.72 billion in 2026 and is projected to reach USD 17.15 billion by 2031.

What commodity holds the largest share of the market?

Cereals and grains lead with 35.1% of Colombia agriculture market share in 2025, mainly because of heavy corn and rice consumption.

Which segment is growing the fastest?

Pulses and oilseeds are forecast to expand at a 5.1% CAGR through 2031, lifted by biodiesel mandates and rising soybean-meal demand.

What regions offer the biggest expansion opportunities?

The Orinoquia savanna is the top frontier, supported by USD 99.9 million in irrigation funding and improving road links that unlock large-scale grain and oilseed farming.

Page last updated on: