Agricultural Surfactants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

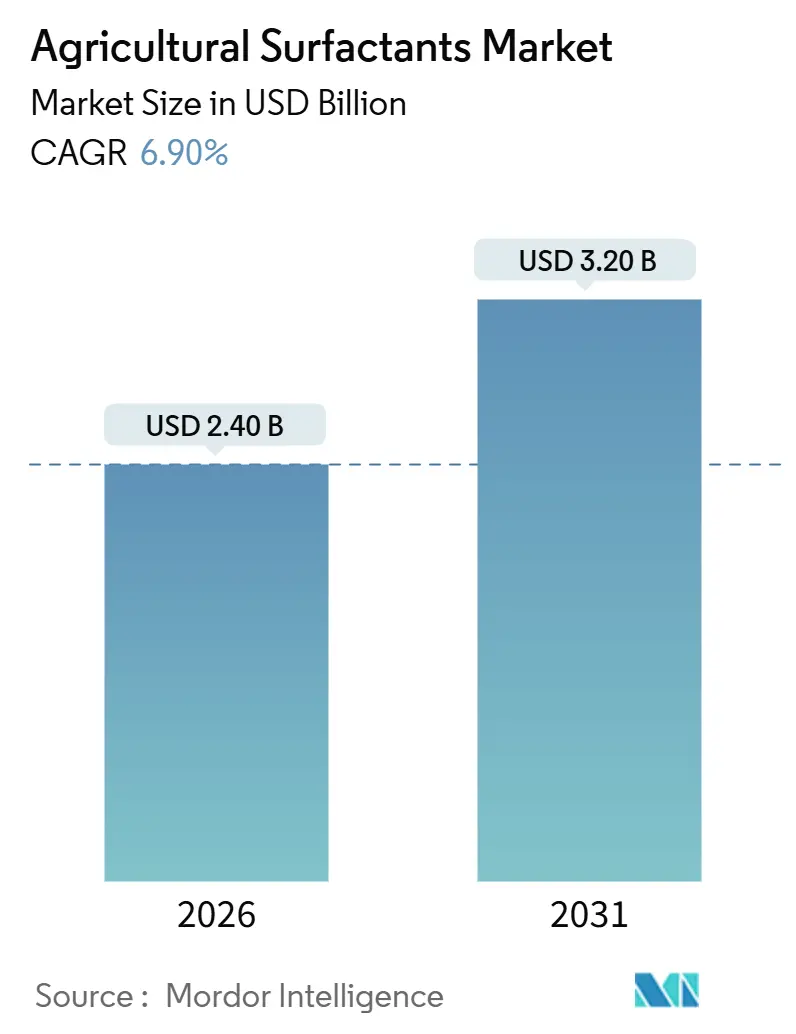

| Market Size (2026) | USD 2.40 Billion |

| Market Size (2031) | USD 3.20 Billion |

| Growth Rate (2026 - 2031) | 6.90% CAGR |

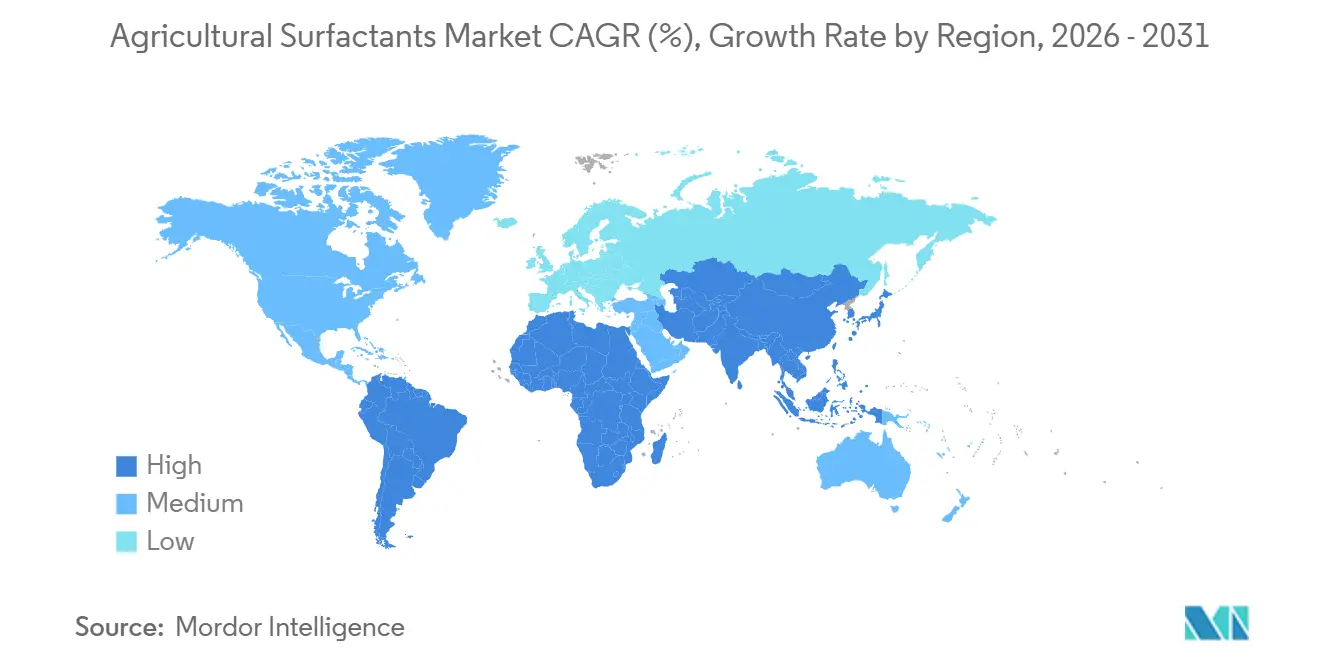

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Surfactants Market Analysis by Mordor Intelligence

The agricultural surfactants market size stood at USD 2.4 billion in 2025 and is anticipated to reach USD 3.2 billion by 2031, reflecting a 6.9% CAGR for 2026-2031. Climate volatility, pest resistance, shrinking arable land, and precision-spray technology are prompting growers to boost adjuvant loads, lifting the agricultural surfactants market in every major crop and geography. Nonionic chemistries, bio-based feedstocks, and ultra-high-concentration drone sprays are reshaping product strategy, while regulatory mandates in Europe and North America accelerate the pivot toward biodegradable ingredients. Competitive tactics now revolve around nano-emulsion platforms that lower active-ingredient doses, partnerships with biological input suppliers, and digital integrations that prescribe surfactant blends in real time. Supply risks tied to palm-derived fatty alcohols and ethylene oxide continue to compress margins, yet investment in fermentation-derived substrates and humidity-responsive nano-formulations is expanding the addressable agricultural surfactants market.

Key Report Takeaways

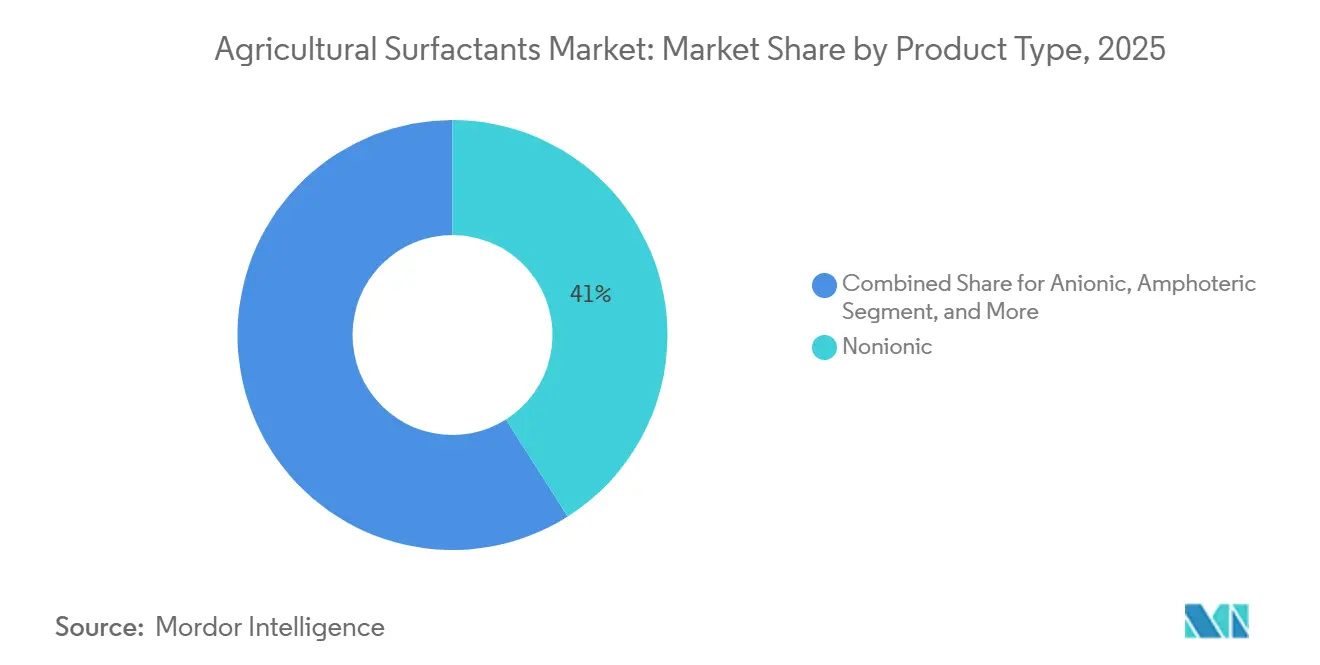

- By product type, nonionic surfactants led with 41% of the agricultural surfactants market share in 2025, while oil-based variants are advancing at a 13.2% CAGR through 2031.

- By application, herbicides accounted for 46% of consumption in 2025, whereas fungicide-compatible adjuvants are projected to expand at a 12.4% CAGR through 2031.

- By substrate, synthetic inputs held a 64% share in 2025, yet bio-based substrates are forecast to grow at a 18.1% CAGR through 2031.

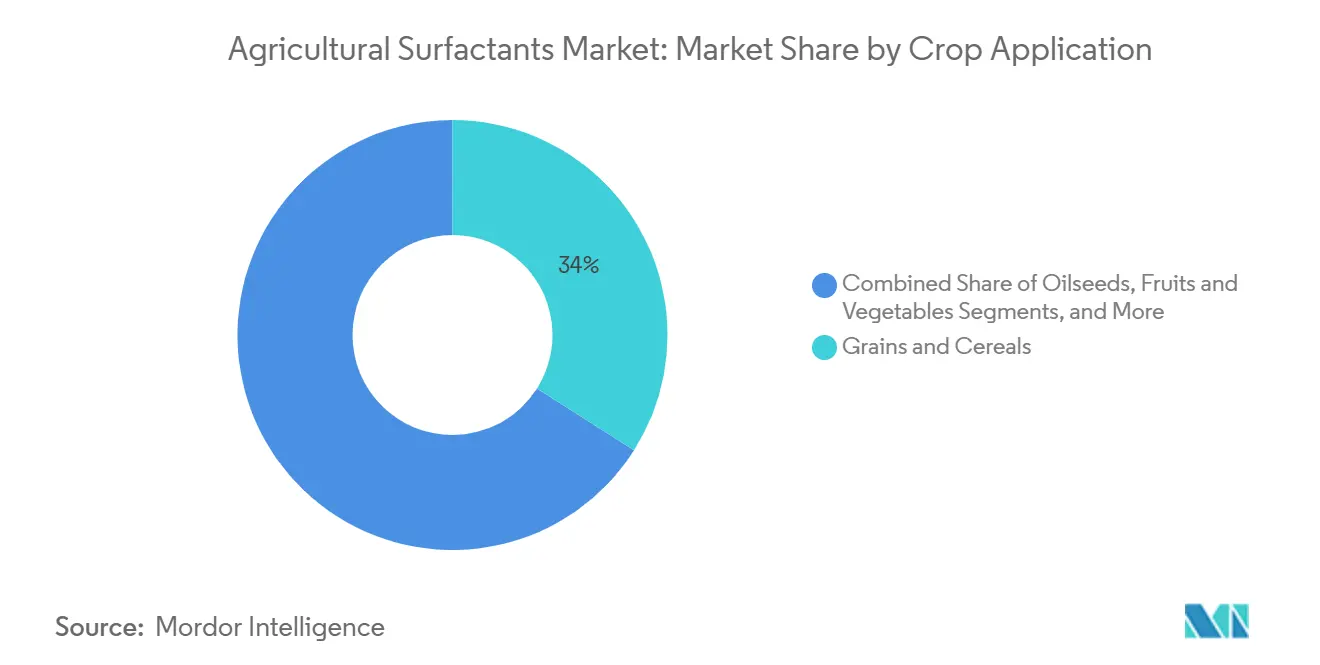

- By crop application, the crop-based segment accounted for a 34% share in 2025 and is anticipated to outpace the market at a 11.7% CAGR from 2025 to 2031.

- By form, liquid formulations captured 68% share in 2025, and are projected to rise at 10.3% CAGR through 2031.

- By function, wetting agents led with 55% share in 2025, whereas penetrant and adjuvant formulations are expanding at 14.9% CAGR through 2031.

- By geography, North America commanded 38% of revenue in 2025, but Asia-Pacific is forecast to register an 11.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agricultural Surfactants Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for agrochemicals to boost crop yield | +2.1% | Global, with intensity peaks in Asia-Pacific, Africa, and South America | Medium term (2-4 years) |

| Precision-farming adoption increasing surfactant usage | +1.8% | North America and Europe core, spill-over to Australia and Brazil | Medium term (2-4 years) |

| Growing focus on sustainable and bio-based surfactants | +1.5% | Europe and North America lead, regulatory pull in Asia-Pacific | Long term (≥ 4 years) |

| Nano-surfactant innovations enabling ultra-low doses | +1.3% | Asia-Pacific core, early trials in North America and Europe | Long term (≥ 4 years) |

| Biological crop-protection compatibility requirements | +1.0% | Global, with accelerated adoption in Europe and North America organic segments | Medium term (2-4 years) |

| Ultra-high-concentration formulations for drone spraying | +0.9% | Asia-Pacific leads, emerging in Brazil and select North American states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Agrochemicals to Boost Crop Yield

Climate swings and pest resistance necessitate multiple spray passes each season, resulting in increased surfactant kilograms per hectare. Brazil cleared 100 new crop-protection products in August 2024, which is anticipated to lift demand for soybean and corn adjuvants[1]Source: Brazilian Ministry of Agriculture, “New Crop-Protection Registrations,” gov.br. India’s pesticide sales increased significantly in 2024, with surfactants outpacing actives due to challenges in penetrating hard water. China experienced growth in herbicide sales in 2025, amid labor shortages in rice and wheat, which led to increased demand for chemical weed control that relies on adjuvants for leaf adhesion. The spike in post-emergence herbicides that need surface tension below 30 dynes/cm favors nonionic and oil-based chemistries on smallholder farms.

Precision-Farming Adoption Increasing Surfactant Usage

Variable-rate sprayers now modulate adjuvant dose by canopy density, soil moisture, and wind speed. North American farm penetration increased in 2024, and algorithms showcased by Corteva in November 2024 recommend bespoke surfactant blends, trimming total spray volume by 20% and extending equipment uptime. Europe’s drift-reduction rules accelerate investment in nozzle technology and adjuvant formulations that hold droplet size within tight bands. Australia’s grain belt links GPS booms with inline surfactant injectors, cutting adjuvant waste by 15% per season.

Growing Focus on Sustainable and Bio-Based Surfactants

Retailer policies and ESG targets push formulators to replace petroleum-based inputs despite 25%-40% cost premiums. BASF rolled out Sokalan CP 301 in April 2025, a plant-derived dispersant that meets EU Ecolabel criteria. Nouryon followed with Adsee Flex 960, posting a 35% greenhouse-gas reduction versus conventional ethoxylates. REACH and EPA Safer Choice certifications reward suppliers that demonstrate biodegradability and low aquatic toxicity.

Nano-Surfactant Innovations Enabling Ultra-Low Doses

Particle sizes below 10 nanometers improve cuticle penetration by 50% and cut active-ingredient rates by up to 40%. Field data from 2024 rice and soybean trials confirm faster systemic translocation, making nano-emulsions attractive where new actives face regulatory delays. Phytotoxicity under 85% relative humidity remains a hurdle, prompting humidity-responsive designs that alter droplet coalescence in tropical climates.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost of bio-based raw materials | -1.4% | Global, with acute margin pressure in Europe and North America | Medium term (2-4 years) |

| Stringent regulations on chemical residues | -1.2% | Europe and North America lead, cascading to export-oriented Asia-Pacific producers | Long term (≥ 4 years) |

| Feed-stock supply volatility for specialty ethoxylates | -0.9% | Global, with supply-chain bottlenecks in Southeast Asia | Short term (≤ 2 years) |

| Phytotoxicity concerns with nano-formulations in humid tropics | -0.7% | South America, Africa, and Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production Cost of Bio-Based Raw Materials

Fermentation-derived fatty alcohols raise costs by up to 40% versus petroleum feedstocks. Palm oil rose 22% in early 2025 after Indonesia tightened exports, inflating nonionic input costs. Ethylene oxide volatility of 30-35% from 2024-2025 hampered small formulators that lack long contracts, undermining competitiveness against integrated majors. Price spikes in palm and soybean oil cascade through the value chain, lifting contract prices for bio-surfactant intermediates by double digits within a single quarter. Formulators without vertical integration must absorb this volatility or pass it to growers, a strategy that erodes demand in price-sensitive row crops.

Stringent Regulations on Chemical Residues

REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals), and the United States Pesticide Registration Improvement Act, enforce residue limits and now require inert-ingredient disclosure. Compliance per active costs USD 2-5 million, including toxicology and field trials. Export-oriented producers in India and China are reformulating to avoid bans in premium markets. Toxicology, environmental fate, and multi-crop field residue studies stretch registration timelines by 24 to 30 months, delaying revenue from new launches. Failure to meet emerging limits can trigger border rejections that halt exports overnight, an acute threat for Indian and Chinese formulators serving premium fruit and vegetable chains.

Segment Analysis

By Product Type: Nonionic Dominance Faces Bio-Based Disruption

Nonionic chemistries controlled 41% share in 2025, favored for broad compatibility and hard-water tolerance. Oil-based alternatives rise at 13.2% CAGR as post-emergence herbicides need deeper cuticle penetration. Regulatory phase-outs of nonylphenol ethoxylates open a USD 180-220 million replacement pool. Bio-based nonionics, such as BASF’s Sokalan CP 301, anchor the pivot toward renewable content.

The agricultural surfactants market benefits from synthetic robustness in early-season cold spells, while hybrid blends balance cost and sustainability. Amphoteric and cationic options stay niche yet grow with aquatic weed programs and pH-buffered tank mixes. Innovation continues in dispersants like Clariant’s Dispersogen TP 100 T for wettable powders, which is a nonionic dispersant for wettable powders, underscores ongoing innovation in this mature segment, while Ashland's easy-wet 300 n super wetting agent, commercialized in September 2024, targets low-surface-tension applications in precision spraying.

Note: Segment shares of all individual segments available upon report purchase

By Application: Herbicide Leads, Fungicide Compatibility Accelerates

Herbicide applications commanded 46% of surfactant consumption in 2025, reflecting the dominance of glyphosate, glufosinate, and dicamba programs in row-crop agriculture. Fungicide-friendly adjuvants grow at 12.4% CAGR driven by late-season disease pressure in high-value crops and the proliferation of biological fungicides that demand non-ionic, low-toxicity adjuvants to preserve microbial viability. Insecticide adjuvants rise in Asia-Pacific cotton and rice, where integrated pest management boosts coverage needs.

BASF's October 2024 partnership with AgroSpheres on bioinsecticide delivery platforms illustrates the strategic importance of surfactant compatibility in biological crop protection, a segment forecast to reach USD 12 billion globally by 2030. Compatibility with triazole and strobilurin fungicides steers product design, as evidenced by Nouryon’s Adsee Flex 960. Drone sprayers elevate systemic herbicide needs, reinforcing demand for penetrant agents. Tank-mix simplicity also drives multipurpose formulations that combine wetting, penetration, and drift control.

By Substrate: Synthetic Volume Meets Bio-Based Velocity

Synthetic substrates held 64% market share in 2025, anchored by petroleum-derived ethoxylates and sulfonates that offer predictable performance and cost advantages of 25-40% over bio-based alternatives. Bio-based substrates are projected to grow at a 18.1% CAGR to 2031, driven by retailer sourcing mandates, corporate ESG commitments, and regulatory incentives in Europe and North America that favor renewable carbon inputs. Price parity edges closer as fermentation technology scales, with Clariant’s Synergen Soil matching synthetic benchmarks in Europe.

Hybrid blends with 30-50% renewable carbon content strike a middle ground, meeting ESG goals without compromising performance. Cold-weather viscosity challenges persist for bio-based ethoxylates, keeping synthetic anchors in early-season sprays. Carbon taxes and supply-chain emission tracking further tilt adoption toward plant-based feedstocks. The substrate segmentation is evolving toward hybrid blends that combine synthetic performance with bio-based content sufficient to meet sustainability thresholds, a strategy that balances cost, efficacy, and regulatory compliance.

By Crop Application: Crop-based Grains Anchor, Fruits and Vegetables Surge

Crop-based segment absorbed 34% of surfactant volume in 2025 due to vast wheat, corn, rice, and soybean acreage. The segment also outpaced at 11.7% CAGR, reflecting premium pricing for residue-free produce and growing biological fungicide use. Oilseeds, including canola, sunflower, and rapeseed, account for approximately 20% of crop-based demand and are expanding in Eastern Europe and Australia as growers diversify rotations to manage herbicide-resistant weeds.

Residue concerns in fresh produce push non-phytotoxic wetting agents. Early-season vegetable programs adopt Clariant’s Synergen Guard 100 for low-temperature efficacy. Large-acreage grains leverage economies of scale, lowering per-hectare adjuvant cost to USD 2-4, yet rely on penetrant surfactants for resistant weeds in dicamba and glyphosate programs. Turf and ornamental applications prioritize low-phytotoxicity formulations that preserve visual quality, a requirement that limits surfactant selection to nonionic and amphoteric chemistries with proven safety profiles on sensitive species.

Note: Segment shares of all individual segments available upon report purchase

By Form: Liquid Convenience Dominates Powder Niches

Liquid formulations commanded 68% share in 2025, enabling real-time metered injection in precision sprayers. Drone adoption and automation drive a 10.3% CAGR for liquids. Powders appeal in regions lacking cold-chain logistics, as they resist phase separation under temperature swings. These products, offer logistical advantages in remote geographies with limited cold-chain infrastructure, as powder forms tolerate temperature extremes that cause liquid surfactants to gel or separate. Preparation time and labor requirements limit powder uptake in large United States and European farms.

Clariant’s Dispersogen TP 100 T shores up the wettable powder segment, ensuring particle suspension in hard water. South America and Africa still favor powders for cost containment, though liquids dominate biological inputs where dust can damage microbial spores. Liquid surfactants are also preferred in biological crop protection, as powder forms can generate dust that damages microbial viability during handling.

By Function: Wetting Agents Lead, Penetrants Gain Traction

Wetting agents held 55% share in 2025 by reducing surface tension to 25-30 dynes/cm. Penetrants grow at 14.9% CAGR, vital for systemic herbicides and ultra-concentrated drone sprays. They enable active ingredients to breach cuticle barriers within 30 to 60 minutes of application, a speed advantage that reduces vulnerability to rain washoff and extends application windows in regions with unpredictable weather. Dispersants remain essential for powder formulations in niche herbicide blends.

Ashland’s easy-wet 300 n drops tension to 22 dynes/cm, aiding onion and brassica coverage. Nouryon's Adsee Flex 960, launched in April 2025, combined wetting and penetrant functions in a single formulation, simplifying tank-mix protocols and reducing adjuvant inventory for growers managing multiple herbicide chemistries. Multifunctional surfactants that merge drift control with wetting and penetration lead new product pipelines across the agricultural surfactants market.

Geography Analysis

North America dominated with 38% share in 2025. Large row-crop operations embrace precision sprayers that align adjuvant dose with canopy maps, reducing water use by up to 30%. Regulatory influence from the EPA's Pesticide Registration Improvement Act is forcing reformulation of legacy surfactants. Mexico's agricultural sector is expanding surfactant usage in avocado and berry production, where export markets demand residue-free produce that meets stringent maximum residue limits.

Asia-Pacific represents the fastest expansion at 11.5% CAGR. India’s hard-water conditions and China’s labor shortages elevate adjuvant requirements, and drone programs compress payload volume by 75%. Ultra-high-concentration formulations for drone spraying are advancing rapidly in China, where regulatory approvals for aerial application were streamlined in 2024. Humidity-driven phytotoxicity in tropical zones slows nano-emulsion rollouts but accelerates development of moisture-responsive blends suited for rice and soybean[3]Source: Indian Crop Protection Association, “Pesticide Market Growth 2024,” cropprotection.org.in.

Europe advances, guided by REACH and carbon taxes that reward biodegradable inputs. Germany, France, and the United Kingdom lead investments in drift-control technology. South America is growing as Brazil adds crop-protection registrations and pushes systemic herbicide penetration in its expanded soybean acreage. Africa and the Middle East's growth is supported by intensification and precision irrigation.

Competitive Landscape

Market concentration is moderate, with the top five suppliers capturing a significant share of 2025 revenue. BASF is leveraging vertical feedstock integration and EU-compliant biodegradable launches[2]Source: BASF, “AgroSpheres Collaboration Announcement,” basf.com. Corteva couples adjuvants with its digital platform, creating switching costs for growers. Solvay rounds out the tier-one group, pursuing bio-based and nano-emulsion innovation. Strategic patterns center on vertical integration of bio-based feedstocks, nano-emulsion platform development, and partnerships with biological-input suppliers to capture adjacency opportunities in crop protection.

White-space potential lies in humidity-responsive nano-surfactants that prevent leaf burn, particularly in tropical soybeans and rice. Smaller challengers such as Marubeni Corporation, LLC, Clarinat, and Nouryon disrupt through rapid launch cycles and renewable content. Ashland and Bionema focus on specialty niches like low-tension wetters for onions and biological-compatible adjuvants. They are targeting bio-based and precision-farming segments where legacy players lack differentiated offerings.

Regulatory compliance costs favor integrated majors with captive toxicology labs. Digital agronomy partnerships shape future competition as algorithms prescribe adjuvant blends by microclimate. The competitive landscape is bifurcating into scale players that compete on cost and distribution reach, and innovation specialists that capture premium pricing through differentiated performance in niche applications like drone spraying and biological inputs.

Agricultural Surfactants Industry Leaders

BASF SE

Corteva Agriscience

Nouryon

Solvay SA

Marubeni Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: BASF launched Sokalan CP 301, a biodegradable dispersant derived from plant-based feedstocks, designed for tank-mix compatibility with biological fungicides and meeting EU Ecolabel criteria. This product addresses the phase-out of nonylphenol ethoxylates and targets European markets where REACH compliance costs favor renewable-carbon inputs.

- April 2025: Nouryon introduced Adsee Flex 960, a renewable-carbon tank-mix adjuvant that reduces greenhouse gas emissions by 35% compared to conventional ethoxylates. The product was formulated for compatibility with triazole and strobilurin fungicides, addressing grower concerns about antagonistic interactions in disease-control programs.

- March 2025: Clariant unveiled four surfactant lines, including Synergen Soil for soil-applied herbicides, Synergen Guard 100 for low-temperature spray conditions, Dispersogen TP 100 T for wettable powder formulations, and the Sapogenat T range for precision-farming applications. These launches target bio-based and specialty segments where legacy products face regulatory headwinds.

- September 2024: Ashland commercialized easy-wet 300 n super wetting agent, achieving surface tensions below 22 dynes per centimeter for improved coverage on difficult-to-wet crops like onions and brassicas. The product targets precision-spraying applications in North America and Europe.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study, according to Mordor Intelligence, counts every formulated anionic, non-ionic, cationic, or amphoteric surfactant that is intentionally added to crop-care sprays to improve wetting, spreading, retention, or penetration across field and specialty crops worldwide.

Scope exclusion: we leave out surfactants sold solely for livestock hygiene, post-harvest washes, or general household cleaning.

Segmentation Overview

- By Product Type

- Anionic

- Nonionic

- Cationic

- Amphoteric

- Oil-based Surfactants

- By Application

- Herbicide

- Insecticide

- Fungicide

- Other Applications

- By Substrate

- Synthetic

- Bio-based

- By Crop Application

- Crop-based

- Grains and Cereals

- Oilseeds

- Fruits and Vegetables

- Non-crop-based

- Turf and Ornamental Grass

- Other Crop Applications

- Crop-based

- By Form

- Liquid

- Powder/Granular

- By Function

- Wetting Agent

- Dispersant

- Penetrant/Adjuvant

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed formulators, adjuvant blenders, agronomists, and large growers across North America, Brazil, France, India, and Australia to validate desk findings, sense-check bio-based adoption rates, and discuss typical dose rates in herbicide programs. Follow-up surveys with distributor purchase managers helped us refine regional price spreads.

Desk Research

We first mapped the value chain through open datasets from agencies such as FAO, USDA, Eurostat, and OECD that report pesticide usage volumes. We then cross-checked trade flows on Volza and customs dashboards to spot import gaps. Regulatory release notes from US EPA and EFSA, patent families on Questel, and technical papers in journals like Crop Protection enriched functional performance benchmarks. Company 10-Ks and investor decks provided average selling prices. These publicly available sources, supplemented by D&B Hoovers for supplier revenues, laid the factual bedrock; many additional databases were also reviewed, though not all are listed here.

Market-Sizing & Forecasting

We deploy a top-down build that converts herbicide-treated hectares, average spray concentration, and typical surfactant inclusion rates into a demand pool, which is then value-translated with regional ASPs. Select bottom-up supplier roll-ups and channel checks confirm the totals.

Input variables include:

1. Share of non-ionic surfactants in glyphosate blends;

2. Bio-based surfactant penetration by substrate cost differential;

3. Annual change in cereal acreage requiring post-emergent sprays.

A multivariate regression model links these drivers to observed historical sales and projects the market through 2030, with scenario analysis used where regulation may tighten ethoxylate limits.

Data gaps in supplier volumes are bridged with price-volume proxy ranges collected during interviews.

Data Validation & Update Cycle

Each iteration is peer-reviewed, anomaly flags trigger re-contact with sources, and variance beyond three percentage points versus independent indicators is escalated. Reports refresh yearly and are re-checked for material events before client delivery.

Why Mordor's Agricultural Surfactants Baseline Deserves Confidence

Published estimates differ because firms pick dissimilar functional scopes, currency years, and refresh schedules.

By anchoring totals to treated-hectare math and live ASP interviews, our baseline remains closely tethered to market fundamentals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.10 B (2025) | Mordor Intelligence | - |

| USD 1.56 B (2025) | Regional Consultancy A | Excludes adjuvants used in seed treatments, narrower functional scope |

| USD 1.70 B (2023) | Trade Journal B | Older base year and constant-price currency treatment |

| USD 1.56 B (2024) | Global Consultancy A | Omits synthetic-bio blend volumes and applies single global ASP |

Taken together, the comparison shows that when scope breadth, current pricing, and annual refresh discipline align, as in Mordor's model, decision makers receive a balanced, transparent baseline they can readily audit and reuse.

Key Questions Answered in the Report

What is the projected value of the agricultural surfactants market by 2030?

It is projected to reach USD 3.2 billion by 2031, growing at a 6.9% CAGR.

Which region will grow the fastest through 2031?

Asia-Pacific is anticipated to register the highest CAGR at 11.5% as smallholders adopt drone spraying and precision farming.

Which product type currently leads the market?

Nonionic surfactants hold the largest share at 41% because of its broad compatibility with herbicides, insecticides, and fungicides.

How are regulations influencing product development?

REACH and EPA residue limits are accelerating the shift to biodegradable, bio-based ingredients and prompting reformulation of legacy ethoxylates.

What technology trend is reshaping surfactant usage?

Real-time digital agronomy platforms now prescribe surfactant blends based on canopy density and weather, lowering spray volume by up to 30%.

Which companies dominate the competitive landscape?

BASF, Corteva, Marubeni Corporation, LLC, Nouryon, and Solvay collectively control significant share of global revenue.