Agricultural Grade Zinc Chemicals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

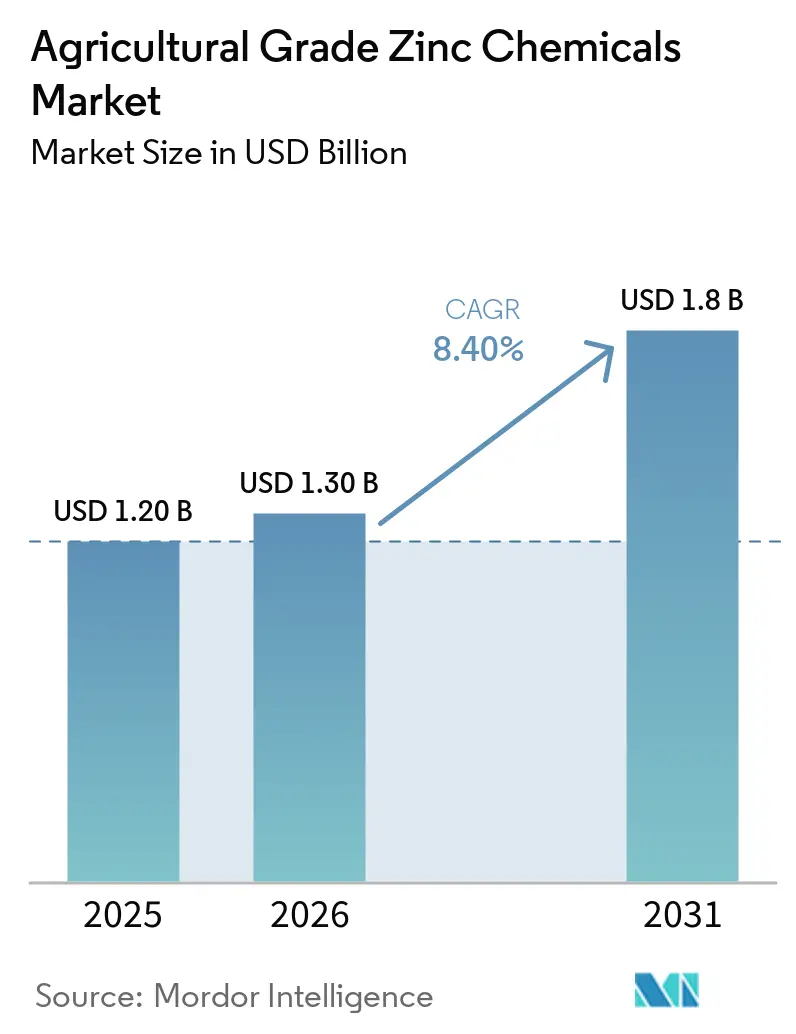

| Market Size (2026) | USD 1.30 Billion |

| Market Size (2031) | USD 1.8 Billion |

| Growth Rate (2026 - 2031) | 8.40% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Grade Zinc Chemicals Market Analysis by Mordor Intelligence

The agricultural grade zinc chemicals market size is anticipated to grow from USD 1.20 billion in 2025 to USD 1.30 billion in 2026 and is forecast to reach USD 1.80 billion by 2031 at 8.4% CAGR over 2026-2031. Expanded nutrient-deficiency testing programs, the acceleration of precision agriculture platforms, and new subsidy allocations from large grain-producing governments are turning zinc from a discretionary input into a mainstream component of balanced fertilization. Fertilizer blenders are embedding zinc sulfate monohydrate in compound NPK grades to comply with India’s January 2026 subsidy incentive, while growers in North America and Europe are shifting toward liquid and chelated forms that align with variable-rate technology. Regional capacity additions at Hindustan Zinc and Mosaic Company enhance supply security, yet imported low-cadmium concentrates remain critical for producers targeting stringent European Union quality standards. Suppliers that couple zinc offerings with data-enabled advisory services are expanding customer reach and defending margins against volatility in mined zinc prices.

Key Report Takeaways

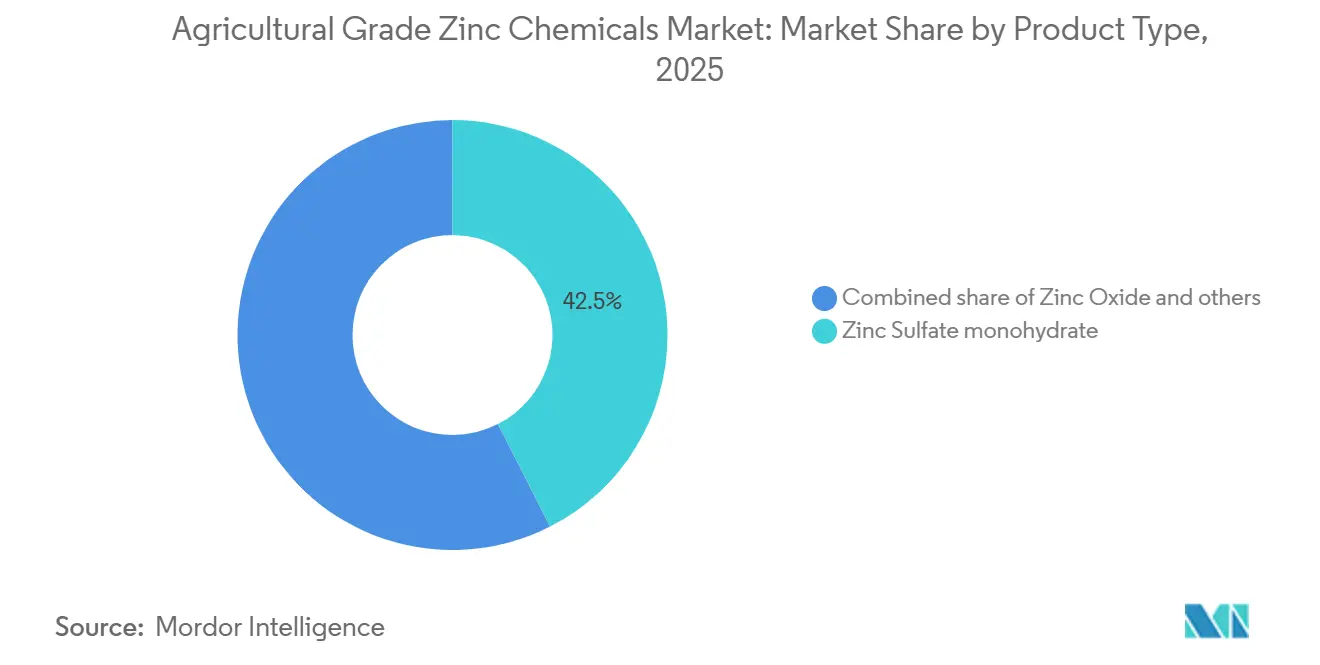

- By product type, zinc sulfate monohydrate held the largest share, accounting for 42.5% of the agricultural grade zinc chemicals market share in 2025, whereas chelated zinc is projected to record the fastest 12.8% CAGR between 2026 and 2031 within product types.

- By application, fertilizer blends commanded the largest 58.0% share of the agricultural grade zinc chemicals market in 2025, whereas soil amendments are forecast to post the fastest 11.7% CAGR over 2026 and 2031 within applications.

- By form, granular products captured the largest 47.0% share in 2025, whereas liquid formulations are anticipated to deliver the fastest 12.9% CAGR across 2026 and 2031.

- By crop type, cereals and grains represented the largest 41.5% share in 2025, whereas oilseeds and pulses are set to expand at the fastest 10.4% CAGR during 2026 and 2031 within crop types.

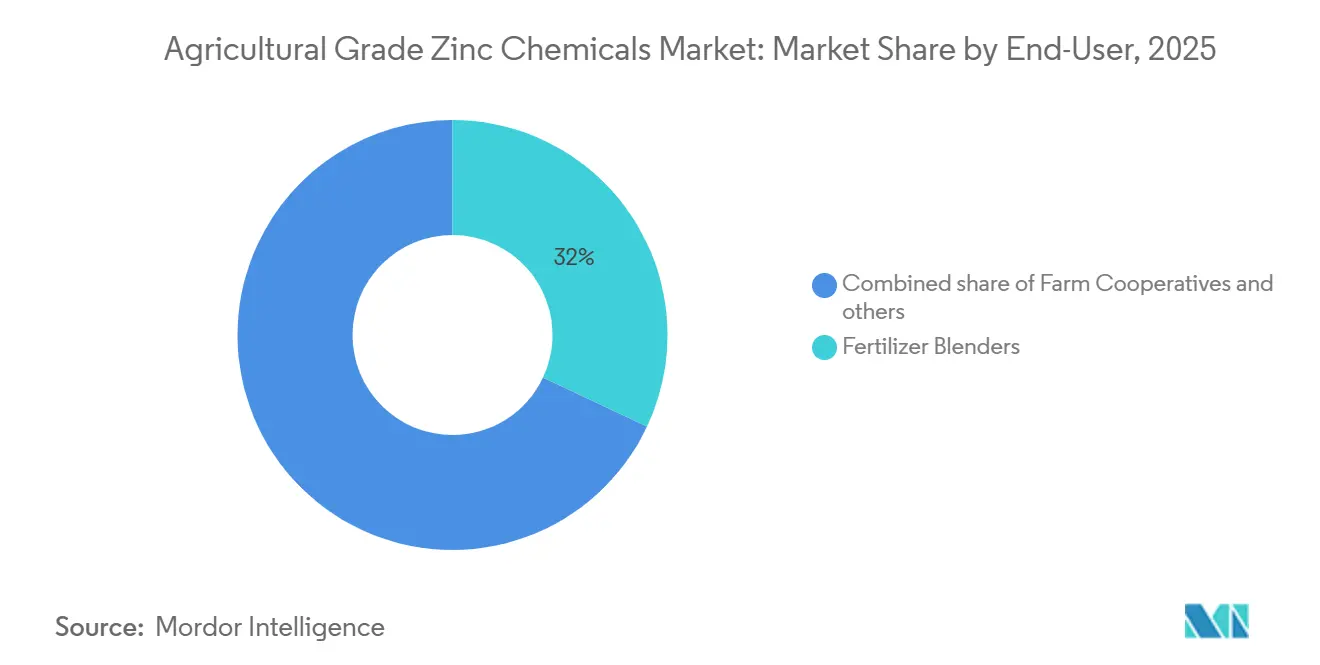

- By end-user, fertilizer blenders held the largest 35.2% share of the agricultural grade zinc chemicals market share in 2025, whereas farm cooperatives will witness the fastest 11.5% CAGR through 2026 and 2031.

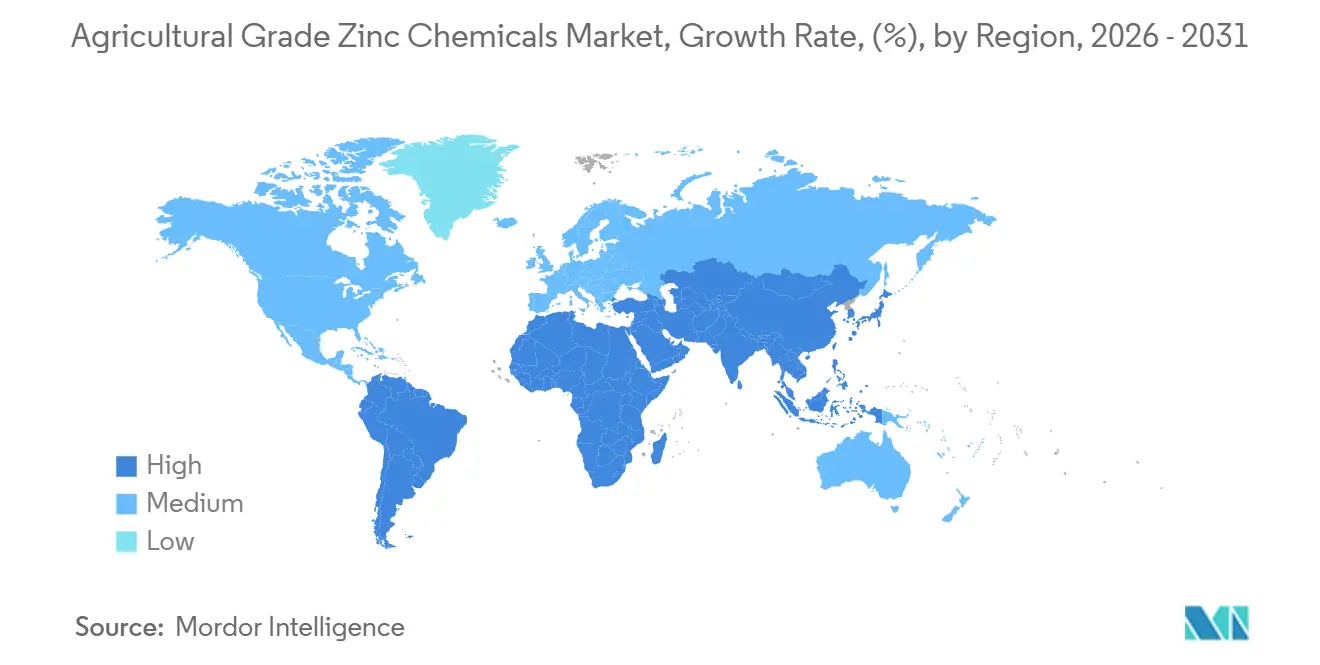

- By region, Asia-Pacific accounted for the largest 38.6% of the agricultural grade zinc chemicals market share in 2025, whereas Africa is projected to experience the fastest 10.5% CAGR across 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agricultural Grade Zinc Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Micronutrient Deficiency Awareness Campaigns | +1.8% | India, China, Ethiopia, Kenya, and Nigeria | Medium term (2-4 years) |

| Adoption of Precision Agriculture Nutrient Mapping | +1.5% | United States, Canada, France, Germany, and China | Short term (≤ 2 years) |

| Government Subsidies for Zinc-Enriched Fertilizers | +1.4% | India, Brazil, Vietnam, and Zambia | Medium term (2-4 years) |

| Commercial Launch of Nano-Chelated Zinc Foliar Sprays | +1.2% | United States, Spain, Japan, and India | Long term (≥ 4 years) |

| Integration of Zinc with Controlled-Release Coatings | +0.9% | United States, Australia, Japan, and South Korea | Long term (≥ 4 years) |

| Soil Microbiome Solutions Boosting Zinc Uptake | +0.6% | Brazil, India, and Kenya | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Micronutrient Deficiency Awareness Campaigns

National programs are uncovering widespread zinc scarcity in cropland soils and translating test results into policy mandates. India’s Soil Health Card initiative found zinc deficiency in 49% of sampled districts in 2025, triggering state procurement of zinc-fortified fertilizers[1]Source: Government of India, “Soil Health Card Portal,” soilhealth.dac.gov.in. Ethiopia mapped 2.3 million hectares of deficient wheat and teff zones in 2025 and partnered with the International Fertilizer Development Center to deliver zinc sulfate to cooperatives. A July 2024 meta-analysis in Nature Food reported grain zinc gains of 30-50% and benefit-cost ratios above 2.5 when 10-20 kilograms per hectare of zinc sulfate were applied. Extension agents now describe zinc as a co-priority with nitrogen and phosphorus in yield-focused fertilizer plans. As a result, blenders anticipate sustained volume growth in agricultural grade zinc chemicals market.

Adoption of Precision Agriculture Nutrient Mapping

Variable-rate platforms overlap satellite imagery, yield history, and soil electrical conductivity to isolate zinc hotspots. The United States Department of Agriculture Economic Research Service recorded adoption on 18% of corn and soybean hectares in 2025, up seven points since 2023[2]Source: United States Department of Agriculture Economic Research Service, “Precision Agriculture Adoption,” ers.usda.gov . European subsidy programs for precision equipment propelled similar uptake in France and Germany, where GPS-guided spreaders modulate zinc flow on the go. Precision agriculture favors liquid and chelate formulations because these formulations meter accurately at low volumes and avoid phosphorus antagonism. Recorded data trails also help growers meet environmental audit requirements, enhancing demand durability. Collectively, precision practices inject a data-driven pull into the agricultural grade zinc chemicals market.

Government Subsidies for Zinc-Enriched Fertilizers

Credit and reimbursement schemes neutralize the upfront cost premium of fortified blends. India set an incentive of INR 500 (USD 6) per metric ton in January 2026, prompting compounders to integrate zinc sulfate into popular diammonium phosphate blends[3]Source: Ministry of Chemicals and Fertilizers, “Nutrient Based Subsidy Rates for Rabi 2025-26,” fert.nic.in . Brazil’s 2025-2026 Plano Safra offered BRL 2.1 billion (USD 420 million) in low-interest micronutrient credit, and uptake surged in Mato Grosso soybean belts gov.br. Zambia distributed subsidized zinc fertilizer to 300,000 smallholders in 2025, doubling local demand. These measures compress payback periods for growers and guarantee a minimum offtake for processors. Subsidy-linked volumes underpin baseline growth of the agricultural grade zinc chemicals market size.

Commercial Launch of Nano-Chelated Zinc Foliar Sprays

Nanometer-scale chelates cross leaf cuticles rapidly and deliver two to three times higher bioavailability than bulk sulfates. A March 2026 Scientific Reports paper confirmed a 45% improvement in zinc use efficiency when alginate-coated nanoparticles were applied to sandy loam soils. Precision Labs released a nano-zinc seed coating in 2025 for United States corn growers, while Indian cooperative IFFCO launched a 1,000-ppm nano-zinc foliar liquid in 2025. California almond and Florida citrus producers pay premiums of 40-60% to secure consistent leaf concentrations above 25 milligrams per kilogram. Commercial traction is strongest in high-value horticulture, yet cereal programs are beginning to test split foliar applications to raise grain zinc levels for biofortification. These early adopters are expanding the specialty corner of the agricultural grade zinc chemicals industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Volatility of Mined Zinc Ores | -1.1% | Global with sharp exposure in China, Peru, and Australia | Short term (≤ 2 years) |

| Stringent Heavy-Metal Residue Regulations | -0.8% | European Union, United States, and export-oriented Asia | Medium term (2-4 years) |

| Supply Bottlenecks of Heptahydrate Crystallizer Units | -0.5% | United States, Belgium, and Canada | Medium term (2-4 years) |

| Farmer Perception of Chelate Cost Versus Yield | -0.7% | Sub-Saharan Africa, South Asia, and Andean region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Mined Zinc Ores

Spot zinc fluctuated between USD 2,400 and USD 3,200 per metric ton in 2025 due to Chinese smelter curtailments and labor actions in major mines. Processing margins for zinc sulfate average USD 150-250 per metric ton of contained zinc, so a 10% ore uptick can shave one-quarter of gross profit for merchants that lack hedging facilities. Old Bridge Chemicals reported lower 2025 earnings as ore costs rose faster than fertilizer sale prices. Hindustan Zinc, by contrast, offset volatility through captive smelter integration and announced a USD 216 million fertilizer plant in September 2025. Persistent swings deter independent processors from expanding capacity, limiting supply elasticity for the agricultural grade zinc chemicals market.

Stringent Heavy-Metal Residue Regulations

European Union Regulation 2019/1009 caps cadmium at 20 milligrams per kilogram in fertilizers, forcing producers to source premium low-cadmium concentrates or install purification units. Compliance upgrades cost USD 50-80 per metric ton, eroding exporters' margins in China and India. United States Environmental Protection Agency testing adds 8-12% to quality assurance expenses. Buyers in Germany and France pay price premiums of up to 8% for certified low-cadmium zinc sulfate. The additional cost narrows adoption among price-sensitive growers and constricts supply options inside the agricultural grade zinc chemicals industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Monohydrate Dominance Faces Chelate Disruption

Zinc sulfate monohydrate secured 42.5% agricultural grade zinc chemicals market share in 2025 on the back of affordable ex-works prices near USD 1,200-1,400 per metric ton and universal compatibility with NPK blending lines [industry pricing data]. The segment benefits from ongoing government mandates that specify minimum zinc inclusion rates. Chelated zinc, while below 10% in volume, is on track for the fastest 12.8% CAGR over 2026-2031 as premium horticulture and variable-rate farming value consistent uptake in high-pH soils. Heptahydrate’s roughly 18% share persists in Europe where storage stability is prized, yet new capacity is hampered by crystallizer shortages. Zinc oxide, at about 15%, remains concentrated in feed formulations.

Forward-looking product strategies separate commodity and specialty paths. Monohydrate producers such as Zinc Nacional and Old Bridge Chemicals are adding purification steps to hit low-cadmium targets demanded by European buyers. Chelate innovators backed by ICL Group are filing patents for alginate encapsulation that promises 40-60% dosage cuts. Nano-chelates, below 2% today, are piloted in California almonds and Indian vegetables with triple-digit demand growth off a small base. Controlled-release granules blend polymer coatings with monohydrate for high-value greenhouse crops, cost remains a barrier for broad-acre cereals. The split underscores an evolving pattern in the market for agricultural grade zinc chemicals, in which low-cost monohydrate carries volume, while chelates capture value.

By Application: Fertilizer Supremacy with Soil Amendment Surge

Fertilizer blends accounted for the largest share of 58.0% of agricultural grade zinc chemicals market size in 2025, as public subsidy schemes reimburse purchases that meet nutrient standards. Blenders incorporate 0.5-1.0% zinc sulfate by weight to unlock India’s payment incentive and mirror similar policies in Vietnam and Ethiopia. Soil amendment ranks second and is forecast to have the fastest growth rate of 11.7% CAGR over 2026-2031, propelled by targeted broadcast and incorporation rates of 10-25 kilograms per hectare in alkaline soils of the United States Great Plains and Australia. Seed treatment, accounting for only a limited share, is gaining attention among large corn and soybean farms adopting nano-zinc coatings that deliver early vigor. Feed and crop protection, while collectively holding significant potential, provide diversification opportunities.

Application preferences mirror the realities of technology and distribution. Soil health programs in Africa distribute standalone zinc sulfate through cooperatives, thereby supporting the use of amendments. Variable-rate rigs in North America favor a blend-ready schedule that combines nitrogen with liquid zinc, enabling one-pass savings of USD 8-12 per hectare. In Brazil, Mosaic Company is co-packing zinc and beneficial microbes in new fertilizer lines from its 2025 Palmeirante plant. Foliar spraying is emerging as a sub-segment that can raise grain zinc by 40% in cereals, supported by drip irrigation systems. These dynamics maintain fertilizer primacy while fostering growth pockets that expand the agricultural-grade zinc chemicals market.

By Form: Granular Incumbency Meets Liquid Momentum

Granular forms led with 47.0% share in 2025 because global blending infrastructure is calibrated for bulk dry inputs. They store well in humid tropical ports and remain dust-free during handling. Liquid zinc formulations are the fastest-growing segment, with a 12.9% CAGR over 2026-2031, aligned with fertigation in irrigated fruits and vegetables and with variable-rate side-dress rigs in Midwestern corn. Powder products hover near 35% share, serving resource-constrained blenders in South Asia that operate simple drum mixers, yet inconsistent dispersion sparks quality complaints. Hybrid pastes and gels are in the pilot stage for specialty greenhouse use.

Portfolio shifts trace application technology. Yara International introduced zinc-enriched granular NPK in Argentina during 2025 to address alkaline soils in Pampas cropland. Indorama Ventures announced a planned April 2026 liquid zinc sulfate line at its planned Egypt complex, aimed at Middle Eastern drip irrigation hubs. California vegetable growers inject 5-10% zinc solutions through drip lines and report uniform uptake and labor savings. Powder share is forecast to slip as regional blending upgrades in Africa add granulation equipment financed by multilateral banks. Form competition reinforces the multi-channel nature of the agricultural grade zinc chemicals market.

By Crop Type: Cereals Anchor Demand, Oilseeds Drive Growth

Cereals and grains, spanning wheat, rice, and maize, accounted for the largest 41.5% share of the agricultural-grade zinc chemicals market in 2025, as zinc deficiency causes visible yield losses of 10-20% and governments prioritize staple security. Oilseeds and pulses are on course for a fastest 10.4% CAGR through 2031 as Brazilian and Argentinian soybean farmers integrate zinc into fertility programs to sustain nitrogen fixation. Fruit and vegetable growers adopted chelated and nano forms to correct row setting and small fruit size in high-value orchards and greenhouses. Cotton, sugarcane, and forage compose the balance with localized but consistent zinc responses.

Crop rotation influences usage intensity. Soybean hectares require continuous zinc because higher soil phosphorus levels exacerbate micronutrient lockout. Wheat farmers in the Indo-Gangetic Plain are shifting to integrated mineral and organic zinc strategies after a January 2026 field trial showed 32% gains in grain zinc with combined applications. California citrus groves apply foliar chelates three times per season to maintain leaf tissue thresholds. Cotton in Texas receives granular zinc during pre-plant fertilizer passes to avoid boll abortion tied to deficiency. The spread of diversified farming systems underpins resilient growth in the agricultural grade zinc chemicals industry.

By End-User: Blenders Rule, Cooperatives Accelerate

Fertilizer blenders held the largest 35.2% share in 2025, purchasing bulk monohydrate or heptahydrate and custom-mixing for regional soil profiles. Integrated agri-input manufacturers such as Yara and Nutrien commanded 28% by controlling production through retail channels. Farm cooperatives, supported by donor programs and group purchasing, are slated for an 11.5% CAGR from 2026-2031, especially in East Africa, where cooperative networks now reach most maize smallholders. Large individual growers in the United States and Argentina directly source zinc in tote quantities, while research stations and specialty consultants make up the remainder.

Strategic mergers reinforce channel clout. ICL Group’s July 2024 purchase of Custom Ag Formulators added 15 United States blending plants and 8,000 farm clients to its footprint. Digital agriculture startups ship prescription zinc pack sizes directly to growers, slicing a small but growing niche. Cooperative feed loops in Zambia and Kenya are bundling zinc fertilizers with credit and insurance, bolstering uptake. Merchants that integrate financing and agronomic advice see higher retention rates and cross-sell potential. Audience diversity sustains volume and cushions risk for the agricultural grade zinc chemicals market.

Geography Analysis

Asia-Pacific retained the largest 38.6% share of the agricultural grade zinc chemicals market in 2025, supported by India’s January 2026 subsidy that reimburses INR 500 (USD 6) per metric ton for zinc-fortified fertilizers. Strong provincial mandates in China and capacity additions at Hindustan Zinc lift regional self-sufficiency and steady demand. Africa is projected to post the fastest CAGR of 10.5% over 2026-2031, as donor-funded soil health programs in Ethiopia, Kenya, and Nigeria embed zinc application into extension guidelines. Expanding inland blending plants and rising cooperative distribution underpin Africa’s growth momentum despite logistics constraints.

Europe, North America, and South America exhibit stable demand profiles shaped by precision agriculture and specialty product uptake. European cadmium limits create a premium tier for low-impurity zinc sulfate sourced from compliant concentrates. North American growers favor liquid and variable-rate applications that integrate zinc with side-dress nitrogen solutions. In South America, Mosaic Company’s 2025 micronutrient facility in Brazil shortens lead times for soybean and corn growers while Middle Eastern demand builds around Indorama Ventures’ Egypt complex and Oceania applies zinc to alkaline wheat soils.

Region-specific subsidy schemes, capacity expansions, and evolving agronomic practices are broadening the buyer base and improving supply resilience. Asia-Pacific producers are investing in purification to meet European import standards, potentially redirecting low-cadmium output to premium markets. African governments plan to scale up cooperative blending units that couple zinc with credit and advisory services, thereby boosting adoption among smallholders. Together, these initiatives are anticipated to enlarge the addressable market and sustain robust growth for agricultural grade zinc chemicals worldwide.

Competitive Landscape

The top five players accounted for a moderate share in 2025, confirming moderate concentration in the agricultural-grade zinc chemicals market. Zinc Nacional anchors this collective position through dedicated agricultural grade zinc sulfate monohydrate lines in Monterrey that supply long-term contracts across North and South America. EverZinc leverages its Belgian zinc oxide assets to secure European feed and fertilizer demand while pursuing capacity upgrades, financing them after the 2025 private-equity acquisition. Both leaders prioritize low-cadmium inputs and backward integration to insulate margins from price swings in mined zinc.

Old Bridge Chemicals expands domestic reach from its New Jersey refinery by pairing zinc metal refining with monohydrate crystallization, ensuring consistent purity for United States blenders. Yara International formulates zinc-enriched NPK blends in Argentina and co-markets liquid micronutrient packages with variable-rate advisory services. Nutrien scales specialty zinc blends through its retail footprint and digital agronomy platform, which cover core Corn Belt geographies. These three firms deepen channel access rather than chase commodity volume, reinforcing differentiated value propositions.

Capacity additions, targeted acquisitions, and technology partnerships are set to widen market opportunity. Top players are commissioning new crystallizers, embracing nanochelate patents, and integrating microbial solutions to boost zinc-uptake efficiency. Downstream moves, such as on-farm advisory bundles and cooperative financing, aim to lock customer loyalty while raising application rates. Collectively, these strategies are anticipated to extend market coverage and support sustained expansion for agricultural grade zinc chemicals over the 2026-2031 horizon.

Agricultural Grade Zinc Chemicals Industry Leaders

Zinc Nacional S.A. de C.V.

EverZinc Belgium NV

Old Bridge Chemicals, Inc.

Yara International ASA

Nutrien Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Indorama Ventures announced a USD 525 million integrated fertilizer complex in Ain Sokhna, Egypt, that will include liquid zinc sulfate lines for exports to the Middle East and North Africa. The additional capacity is set to shorten regional supply chains and accelerate liquid formulation adoption, lifting demand for agricultural grade zinc chemicals across irrigated farms.

- July 2025: Mosaic Company inaugurated an USD 84 million micronutrient blending plant in Palmeirante, Brazil with 1 million metric ton annual capacity. The facility increases local supply of zinc-fortified NPK for soybean and corn growers, reinforcing demand growth for agricultural grade zinc chemicals across South America.

- July 2024: ICL Group acquired Custom Ag Formulators for USD 60 million, adding 15 blending sites across the United States Corn Belt. The expanded footprint strengthens last-mile distribution of specialty zinc products and supports deeper penetration of premium agricultural grade zinc chemicals among large row-crop farms.

Global Agricultural Grade Zinc Chemicals Market Report Scope

Agricultural-grade zinc chemicals are specific zinc compounds, including zinc sulfate, zinc oxide, and EDTA-chelated zinc, utilized as fertilizers and micronutrient supplements. These chemicals address zinc deficiencies in soil and crops, improving yields and enhancing plant resistance to stress. The Agricultural Grade Zinc Chemicals Market is Segmented by Product Type (Monohydrate, Heptahydrate, Chelated, Oxide, Others), Application (Fertilizers, Feed, Crop Protection, Soil Amendment, Seed Treatment), Form (Powder, Granular, Liquid), Crop Type (Cereals, Oilseeds, Fruits and Vegetables, Others), End-user (Blenders, Manufacturers, Cooperatives, Farmers, Others), and Geography. Market Forecasts are in Value (USD).

| Zinc Sulfate Monohydrate |

| Zinc Sulfate Heptahydrate |

| Chelated Zinc (EDTA, DTPA) |

| Zinc Oxide |

| Others |

| Fertilizers |

| Animal Feed |

| Crop Protection |

| Soil Amendment |

| Seed Treatment |

| Powder |

| Granular |

| Liquid |

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Others |

| Fertilizer Blenders |

| Agri-input Manufacturers |

| Farm Cooperatives |

| Individual Farmers |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Zinc Sulfate Monohydrate | |

| Zinc Sulfate Heptahydrate | ||

| Chelated Zinc (EDTA, DTPA) | ||

| Zinc Oxide | ||

| Others | ||

| By Application | Fertilizers | |

| Animal Feed | ||

| Crop Protection | ||

| Soil Amendment | ||

| Seed Treatment | ||

| By Form | Powder | |

| Granular | ||

| Liquid | ||

| By Crop Type | Cereals and Grains | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Others | ||

| By End-user | Fertilizer Blenders | |

| Agri-input Manufacturers | ||

| Farm Cooperatives | ||

| Individual Farmers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the agricultural grade zinc chemicals market in 2031?

The agricultural grade zinc chemicals market size is forecast to reach USD 1.80 billion by 2031, expanding at a 8.4% CAGR over 2026-2031.

Which product type currently holds the largest share?

Zinc sulfate monohydrate commanded the largest 42.5% agricultural grade zinc chemicals market share in 2025.

Which segment is the fastest growing by form?

Liquid formulations are projected to grow at the fastest 12.9% CAGR between 2026-2031.

Why is Africa considered an attractive growth region?

Donor-backed soil health programs and new blending capacity are anticipated to drive the fastest 10.5% CAGR in Africa through 2026-2031.

How are regulations influencing product specifications in Europe?

European Union cadmium limits are pushing demand toward premium low-cadmium zinc sulfate, adding compliance costs but opening price-premium opportunities.

What strategic move exemplifies vertical integration in the market?

Hindustan Zinc's INR 1,800 crore (USD 216 million) investment in an integrated zinc sulfate plant announced in 2025 demonstrates vertical integration from smelting to fertilizer production.

Page last updated on: