Agricultural Chelates Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.38 Billion |

| Market Size (2031) | USD 2.07 Billion |

| Growth Rate (2026 - 2031) | 8.45% CAGR |

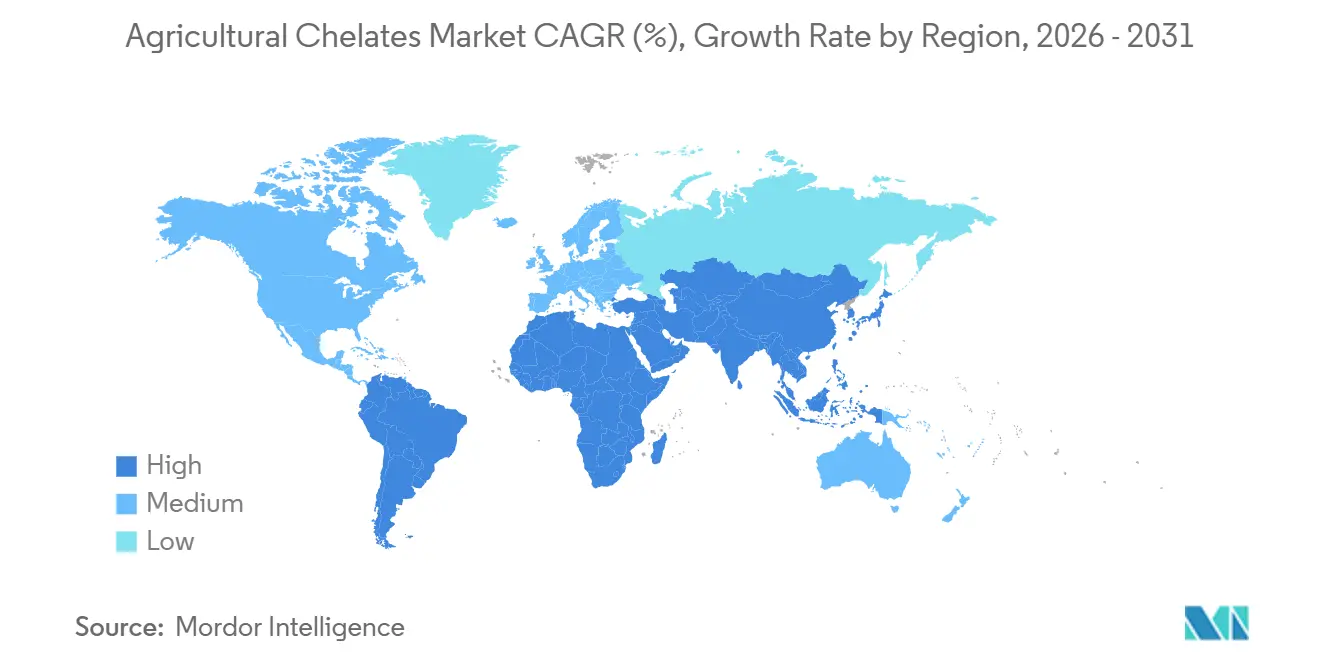

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

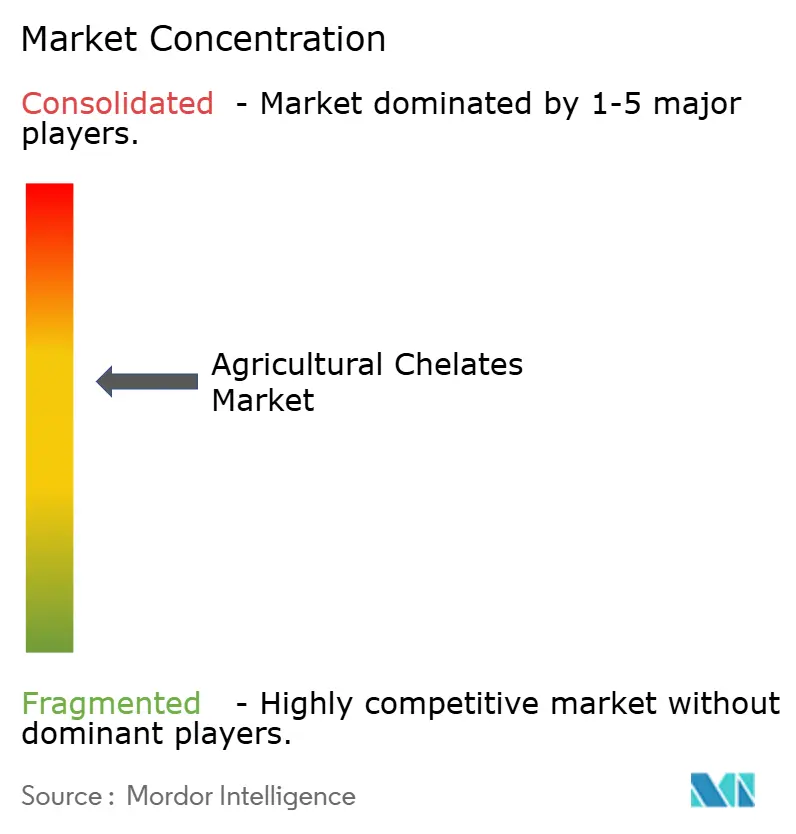

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Chelates Market Analysis by Mordor Intelligence

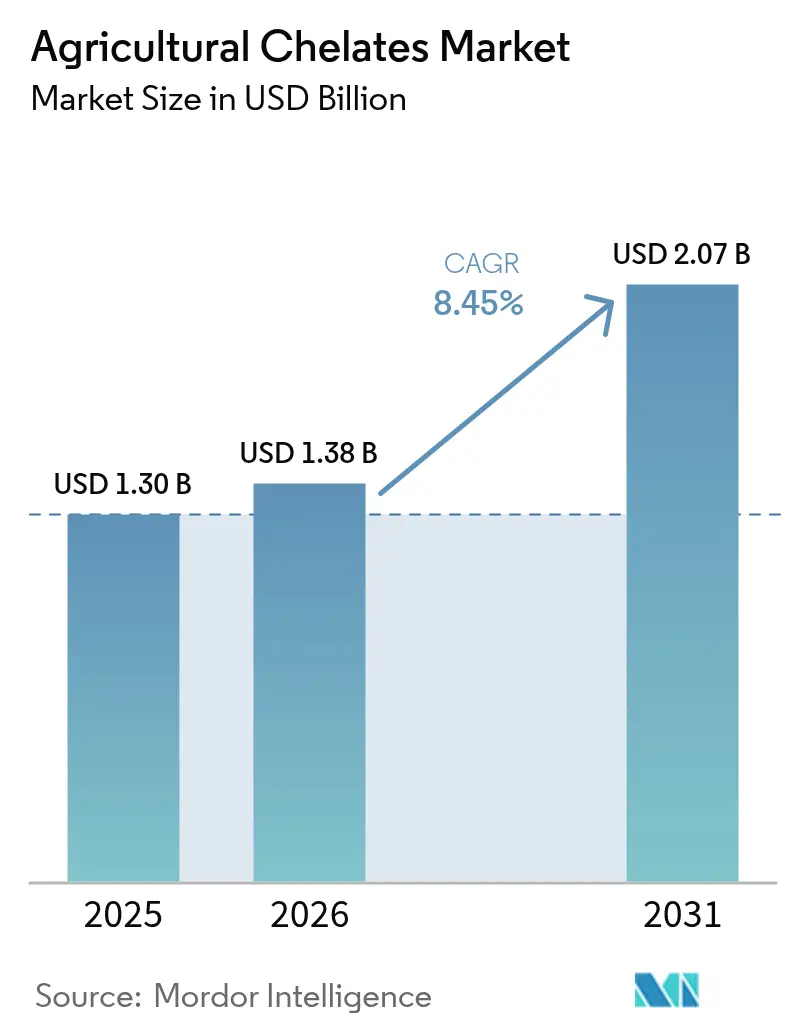

The agricultural chelates market size is projected to expand from USD 1.30 billion in 2025 and USD 1.38 billion in 2026 to USD 2.07 billion by 2031, registering a 8.45% CAGR between 2026 and 2031. Demand for high-efficiency micronutrient inputs is rising as growers face shrinking arable land and government biofortification mandates. Ethylenediaminetetraacetic Acid (EDTA) chelates led 2025 revenue, yet bio-based alternatives such as amino-acid and Iminodisuccinic Acid (IDHA) grades are scaling quickly under Europe’s regulatory scrutiny of persistent synthetic agents. Precision-agriculture investments, especially smart fertigation, are steering product design toward fully soluble, sensor-compatible formulations. Asia-Pacific remains the growth engine because widespread zinc and iron deficiencies coincide with public programs that subsidize fortified grains.

Key Report Takeaways

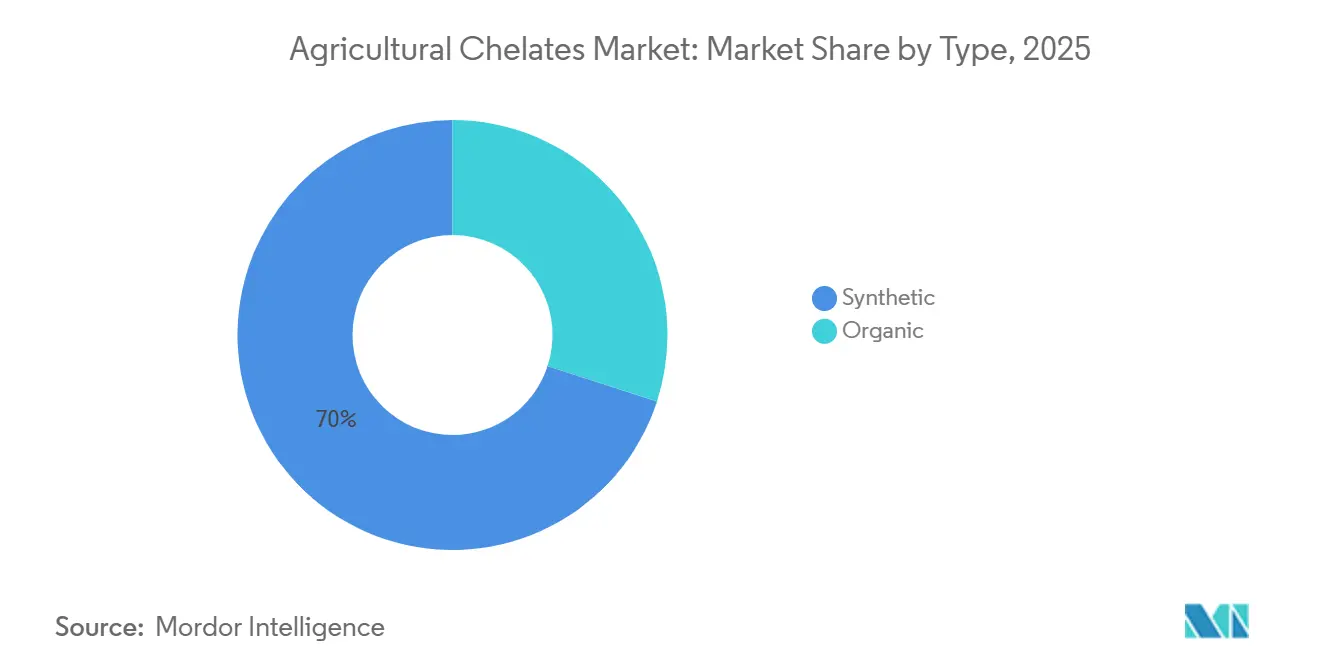

- By type, synthetic chelates held 70% agricultural chelates market share in 2025, while bio-based grades are advancing at a 9.5% CAGR through 2031.

- By application, soil methods held a 41% of the agriculture chelates market revenue lead in 2025, while fertigation is projected to accelerate at an 8.4% CAGR through 2031.

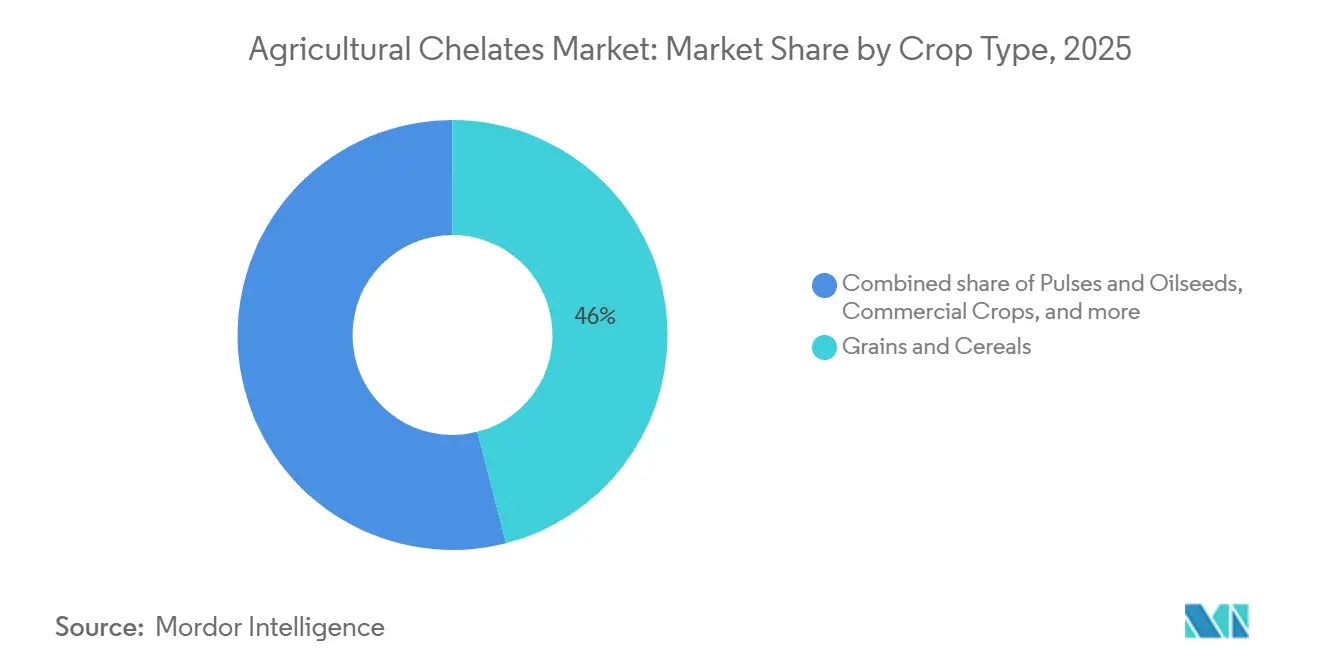

- By crop type, grains and cereals accounted for 46% of the agriculture chelates market size in 2025, and fruits and vegetables are growing at an 8.9% CAGR.

- By geography, Asia-Pacific contributed 53.4% of 2025 revenue and is expanding at an 8.8% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agricultural Chelates Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global food-security pressure amid shrinking arable land | +1.2% | Asia‑Pacific and Africa with global spillover | Medium term (2–4 years) |

| Widespread micronutrient deficiency in agricultural soils | +1.5% | Asia‑Pacific core, the Middle East, Africa, and South America | Long term (≥ 4 years) |

| Rising demand for nutritionally fortified and biofortified crops | +1.0% | Asia‑Pacific and Africa | Medium term (2–4 years) |

| Expansion of controlled-environment agriculture facilities | +0.9% | North America, Europe, and the Middle East | Short term (≤ 2 years) |

| Smart-fertigation-ready specialty chelates | +0.7% | North America, Europe, and the Middle East | Medium term (2–4 years) |

| Carbon-credit-linked nutrient-use-efficiency programs | +0.5% | Europe, North America, and Asia‑Pacific expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global Food-Security Pressure Amid Shrinking Arable Land

World farmland continues to decline by 12 million hectares each year, intensifying interest in inputs that raise yields per hectare, according to data from the United Nations Food and Agriculture Organization (FAO) and the UN Convention to Combat Desertification (UNCCD). Chelated micronutrients deliver three- to five-fold higher bioavailability than sulfate salts, helping growers meet nutrition targets on limited acreage. The Food and Agriculture Organization projects a 50% increase in cereal output by 2050, underscoring the role of chelates in yield-intensive systems[1]Source: Food and Agriculture Organization, “State of Food Security and Nutrition in the World,” fao.org. Asia-Pacific and Africa feel the greatest pressure, driving faster adoption in those regions. The impact remains significant through the medium term as governments allocate subsidies to high-efficiency fertilizers.

Widespread Micronutrient Deficiency in Agricultural Soils

Roughly half of global cereal soils are zinc-deficient, while iron chlorosis constrains horticultural output in calcareous zones such as the Mediterranean. The World Health Organization links soil deficiency to “hidden hunger,” which affects 2 billion people[2]Source: World Health Organization, “Micronutrients,” who.int. Chelates keep micronutrients available in alkaline soils where salts precipitate, making them critical to remediation. Large-scale rice and wheat belts in India and China use foliar chelated sprays to meet nutritional standards. This structural driver exerts a long-lasting influence on the agricultural chelates market.

Rising Demand for Nutritionally Fortified and Biofortified Crop

Government procurement programs now specify minimum levels of zinc and iron in subsidized cereals. HarvestPlus confirmed that biofortified varieties reached 100 million farm households in 2025, with chelates used during grain filling to raise micronutrient density[3]Source: HarvestPlus, “Biofortification Progress Briefs,” harvestplus.org. Foliar chelate treatments complement genetic biofortification, enabling farmers to meet targets when soils lack nutrients. Emerging mandates in Bangladesh and several African nations are anticipated to expand future demand. The driver remains strongest in the medium term as enforcement tightens.

Expansion of Controlled-Environment Agriculture Facilities

Greenhouse acreage worldwide increased by 8% in 2025, and hydroponic systems dominate new builds. In recirculating solutions, conventional salts cause emitter clogging, so growers turn to chelated forms. Dutch standards already require chelated blends, and adoption is rising in Saudi Arabia and the United Arab Emirates. Rapid build-outs create a short-term spike in demand, especially for high-purity grades tailored to drip irrigation. These facilities rely on closed-loop fertigation, underscoring the importance of stable micronutrient complexes to prevent nutrient lockout.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations on persistent synthetic chelating agents | −1.1% | Europe and North America | Short term (≤ 2 years) |

| High product cost versus conventional micronutrient salts | −1.3% | Africa, South America, and smallholder Asia‑Pacific | Medium term (2–4 years) |

| Emergence of next-generation bio-stimulant substitutes | −0.6% | North America and Europe premium segments | Medium term (2–4 years) |

| Supply-chain volatility for bio-based chelating ligands | −0.4% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulations on Persistent Synthetic Chelating Agents

Ethylenediaminetetraacetic acid (EDTA) is a widely used chelating agent in global agriculture but is under European Chemicals Agency (ECHA) assessment for low biodegradability. Although not classified as a Substance of Very High Concern (SVHC), the European market is shifting to biodegradable alternatives like Tetrasodium Glutamate Diacetate (GLDA) and Iminodisuccinic Acid (IDHA) to align with the European Union (EU) Green Deal’s zero-pollution goals. The United States Environmental Protection Agency is conducting parallel reviews, and draft assessments are anticipated in 2026. These actions force formulators to accelerate the adoption of biodegradable alternatives such as the International Diploma in Humanitarian Assistance (IDHA) and Ethylenediamine-N, N′-bis (2-hydroxyphenylacetic Acid) (EDDHA). Compliance costs and portfolio pivots compress margins and slow shipment volumes in the short run. The restraint will ease after new grades gain regulatory acceptance.

High Product Cost Versus Conventional Micronutrient Salts

Chelated zinc often sells at four to eight times the price of zinc sulfate, deterring cash-constrained smallholders. Extension agents in Sub-Saharan Africa and South Asia lack resources to demonstrate payback, so growers default to cheaper salts. Bulk soil applications compound the premium because they require higher volumes than targeted foliar sprays. Spot prices for chelated formulations also track petroleum-derived feedstocks, so spikes in energy markets quickly translate into higher retail prices. Currency fluctuations against the USD elevate landed costs for import-dependent African distributors and amplify pricing uncertainty at the farm gate. Without subsidy or credit schemes, adoption lags in cost-sensitive regions. The restraint is most pronounced through the medium term until financing tools spread.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Synthetic Dominance Faces Biodegradable Pressure

Synthetic chelates held a dominant 70% of agricultural chelates market share in 2025, benefiting from long-standing field validation and inclusion in government fertilizer subsidies. Bio-based chelates are the fastest-growing group and are advancing at a 9.5% CAGR through 2031 as European and United States regulators scrutinize persistent agents like Ethylenediaminetetraacetic Acid (EDTA). The price gap between the two groups is shrinking because fermentation capacity expansions, such as Mitsubishi Chemical’s 40% Tetrasodium Glutamate Diacetate (GLDA) boost in 2025, lower unit costs. Nouryon’s Glutamic Acid, N,N-Diacetic Acid, Tetrasodium Salt (Dissolvine GL) earned European Union (EU) Ecolabel certification in 2025, signaling that biodegradable grades can now replace Ethylenediaminetetraacetic Acid (EDTA) in fertigation without sacrificing performance.

Within bio-based offerings, lignosulfonates supply a budget option for pasture and forage crops but lack stability in alkaline soils. Amino-acid chelates made from glycine or glutamic acid deliver rapid foliar uptake for fruits and vegetables where visual quality drives premium pricing. Heptagluconates offer mid-range cost and stability for organic-certified soil programs, while citrate and gluconate complexes remain niche inputs in hydroponics where quick biodegradation prevents buildup. This diversification allows growers to tailor chelate choice to crop value, soil pH, and sustainability goals as the agricultural chelates market size continues to expand.

By Application: Soil Dominates, Smart Fertigation Gains Pace

Soil application accounted for 41% of the agricultural chelates market in 2025, as broad-acre cereals incorporate chelated zinc and iron into basal fertilizers. Fertigation is the fastest-growing channel, with an 8.4% CAGR through 2031, as drip and hydroponic systems require fully soluble formulations. Foliar sprays grow steadily at a decent CAGR, addressing mid-season deficiencies in high-value fruit and vegetable crops. The agricultural chelates market share for fertigation-grade products rises as controlled-environment farms invest in sensor-driven dosing.

Seed treatments and hydroponic concentrates remain smaller slices yet are strategically vital for specialty crops. Yara's YaraTera chelate range enhances precision irrigation by providing residue-free, fully soluble nutrients that prevent clogging in drip emitters, ensuring uniform water and nutrient distribution throughout the field. Adjuvant-enhanced foliar blends reduce labor by lowering application frequency. Application technology thus shapes product specifications and competitive positioning in the agricultural chelates market.

By Crop Type: Grains Hold Sway, Horticulture Sets the Pace

Grains and cereals accounted for 46% of the agricultural chelates market share in 2025 revenue because zinc drives grain filling and protein synthesis in wheat, rice, and maize. Fruits and vegetables expand at an 8.9% CAGR, driven by export-oriented horticulture that penalizes visual quality defects linked to micronutrient shortages. Pulses and oilseeds grow at a decent CAGR, leveraging chelated iron and zinc to improve nitrogen fixation and oil content. Commercial crops such as cotton and sugarcane add stable demand where fiber and sucrose quality matter.

Biofortification mandates in South Asia are driving demand for chelates in wheat, raising kernel zinc by up to 35% according to 2025 HarvestPlus field data. In horticulture, iron chelates prevent chlorosis in stone fruits and citrus grown on calcareous soils where ferrous sulfate fails. Turf and ornamental segments, though small, accept premium chelated blends to preserve aesthetics. Crop diversity, therefore, underpins resilience in the agricultural chelates market size.

Geography Analysis

Asia-Pacific held 53.4% of the agricultural chelates market share in 2025 and is forecast to expand at an 8.8% CAGR through 2031. Government biofortification mandates in India and China subsidize chelated zinc and iron, thereby accelerating adoption among smallholders. Domestic producers are scaling International Diploma in Humanitarian Assistance (IDHA) and amino-acid grades, trimming import dependency, and easing price pressures. Expansion of drip irrigation under national water-savings programs further elevates demand for fully soluble chelates.

Europe, North America, the Middle East, and Africa follow with varied growth paths. Europe pivots toward biodegradable ligands as Evaluation, Authorisation and Restriction of Chemicals (REACH) rules tighten, while Spain’s citrus industry anchors steady Ethylenediamine-N, N′-Bis (2-Hydroxyphenyl)Acetic acid (EDDHA)-iron consumption. North America benefits from the United States Department of Agriculture cost-share incentives that offset premium pricing for specialty crops and greenhouse vegetables. Middle East greenhouses rely on chelates to overcome the challenges of alkaline soils, and Africa’s commercial farms adopt targeted foliar sprays despite cost hurdles.

Regional adoption will deepen as controlled-environment facilities multiply and carbon-credit programs reward nutrient efficiency. Local manufacturing in India and China is anticipated to lower unit costs, widening access across South and Southeast Asia. European suppliers that secure eco-label certifications will capture price-insensitive organic segments. Public-sector extension services and precision-agriculture platforms will disseminate best practices, expanding the worldwide footprint of the agricultural chelates market.

Regulatory Landscape

Agricultural chelates sold into the European Union are governed by the EU Fertilising Products Regulation (EU) 2019/1009, which sets requirements for conformity assessment and CE marking, product function category rules, and labeling and safety documentation for input materials such as chelating and complexing agents. To improve technical consistency across fertilizers and related products, the European Commission issued Implementing Decision (EU) 2024/2387 (September 2024), referencing harmonized standards including EN 17816:2023 and EN 17817:2023 that suppliers use to support compliance files and product claims.

Environmental and chemicals oversight is also tightening on persistent synthetic chelants, reinforcing the shift away from EDTA toward biodegradable ligands in Europe under REACH-linked scrutiny and related policy pressure. In the United States, trade-policy uncertainty has influenced agricultural input planning; in February 2026, the US Supreme Court struck down presidential emergency tariffs that had affected agricultural inputs during 2025, prompting industry calls for more certainty in import costs and sourcing strategies for chelate raw materials and finished formulations.

Competitive Landscape

The top five players, including BASF SE, Yara International, ICL Group Ltd, Nouryon Chemicals Holdings B.V., and Haifa Group, together control a major share of the agriculture chelates market in 2025. BASF SE and Yara International ASA anchor the market through vertically integrated production and global agronomic advisory networks. Both companies bundle chelates with broader crop nutrition programs, defending share in high-volume cereal and specialty horticulture segments. Their scale advantages translate into competitive pricing and rapid regulatory compliance for new biodegradable ligands.

Nouryon Chemicals Holding B.V., ICL Group Ltd., and Haifa Group round out the leading cohort, each with a focused strategy. Nouryon leverages European Union (EU) Ecolabel certification on its dissolvine line to penetrate organic and sustainability-driven niches. ICL Group Ltd. expanded its Mediterranean reach by acquiring a Spanish Ethylenediamine-N, N′-Bis (2-hydroxyphenyl)Acetic Acid (EDDHA)-iron producer, adding 12,000 metric tons of capacity. Haifa differentiates through nano-chelated foliar nutrients that cut spray frequency in high-value fruit crops.

Capacity additions, biodegradable ligand rollouts, and digital agronomy partnerships will shape future rivalry. Under the Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) framework, BASF and Mitsubishi Chemical have increased production of Glutamic Acid Diacetate (GLDA) and Iminodisuccinic Acid (IDHA). These biodegradable chelating agents will replace Ethylenediaminetetraacetic Acid (EDTA) in European and North American markets by 2026. Yara and Trimble embed chelate prescriptions into cloud platforms, locking products into precision-fertigation routines. Smaller innovators that tailor crop-specific blends or secure carbon-credit alignment are anticipated to chip away at established positions, broadening the agricultural chelates market.

Agricultural Chelates Industry Leaders

Nouryon Chemicals Holding B.V.

BASF SE

Yara International ASA

Haifa Group

ICL Group Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory-driven reformulation and premium compliance pathways continue to create openings for biodegradable chelates in fertigation and controlled-environment agriculture, where fully soluble, low-residue micronutrients help reduce precipitation and emitter clogging. This direction is visible in supplier portfolios: BASF launched Trilon G (GLDA-based) in April 2025, aligning biodegradable ligand supply with customer demand influenced by EU Green Deal and REACH scrutiny of persistent agents. In parallel, certification and sustainability labeling are increasingly used as purchase criteria, illustrated by Nouryon securing ISCC PLUS certification (January 2025) at its Herkenbosch, Netherlands site for biodegradable chelates with renewable-carbon attributes.

Product differentiation is also moving beyond classic EDTA and EDDHA positioning toward dual-function and biologically derived complexes, leaving room for chelate-plus-biostimulant concepts in specialty crops and high-value horticulture programs. A specific example is ICLs Bioz Kellus launch (April 2026), positioned around peptide-based molecules and organic acids to improve nutrient uptake and biodegradation outcomes, which aligns with growers adopting precision nutrition and sustainability-linked agronomy. On the demand side, large correction programs for zinc and iron deficiencies in broad-acre systems (including Brazil and Asia-Pacific grain and soybean belts) continue to support high-stability chelates in soil and foliar programs, while concentration of key ligands and isomers increases the value of localized formulation, sourcing diversification, and region-specific technical support.

Recent Industry Developments

- June 2026: BASF SE announced a price increase for select Trilon chelating agents in North America, effective July 1, 2026, covering a broad portfolio that includes Trilon B, BD, BS, BX, C, D, G, and food-grade variants. The change reflects cost and supply dynamics across established synthetic and biodegradable chelant value chains and can affect formulation economics for micronutrient blends and fertigation-grade products. The adjustment also highlights the importance of alternative ligands and optimized dosing programs when growers and distributors face higher per-kilogram input costs.

- November 2025: Nouryon opened an innovation center in Shanghai, China, to accelerate localized innovation and customer collaboration across multiple end markets, including agriculture. The facility supports application-development capacity closer to Asia-Pacific demand, where chelated micronutrients are used to address widespread zinc and iron deficiencies and to support higher-efficiency fertilizer programs. Faster iteration and regional technical service can reduce time from ligand selection to field-ready formulations.

- April 2025: BASF SE introduced Trilon G, a GLDA-based biodegradable chelating agent positioned to meet readily biodegradable performance thresholds while supporting renewable-carbon goals. The launch expanded BASFs sustainable chelant offering for customers seeking to replace or reduce persistent synthetic agents in regulated markets. It also pointed to faster commercialization of biodegradable ligands that can be incorporated into micronutrient chelates designed for precision fertigation and higher-purity applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the agricultural chelates market covers chelated micronutrient products used in farming to improve nutrient availability and uptake in crops, where a chelating agent binds a micronutrient ion and helps reduce losses in soil and water.

Scope exclusions: We exclude non-chelated micronutrient salts and non-agricultural chelating uses (such as industrial, water treatment, or animal nutrition applications).

Segmentation Overview

- By Type

- Synthetic

- Ethylenediaminetetraacetic Acid (EDTA)

- Ethylenediamine-N, N-bis(2-hydroxyphenylacetic Acid (EDDHA)

- Diethylenetriaminepentaacetic Acid (DTPA)

- Iminodisuccinic Acid (IDHA)

- Other Synthetic Types

- Organic

- Lignosulfonates

- Amino Acids

- Heptagluconates

- Other Organic Types

- Synthetic

- By Application

- Soil Application

- Foliar Application

- Fertigation

- Other Applications

- By Crop Type

- Grains and Cereals

- Pulses and Oilseeds

- Commercial Crops

- Fruits and Vegetables

- Turfs and Ornamentals

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Spain

- United Kingdom

- France

- Germany

- Russia

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure of the market and to keep the assumptions tied to measurable farm activity. We relied on public and official references such as FAOSTAT for crop area and production signals, USDA and Eurostat for agriculture and fertilizer-related statistics, and trade indicators from UN Comtrade where product mapping was relevant.

To translate those demand signals into a workable revenue model, we also reviewed sources such as IFA and national agriculture ministry publications, alongside company annual reports, investor presentations, and credible industry press that discuss micronutrient programs and formulation shifts. When available, we used subscription databases focused on company financials and patents to cross-check product focus and technology direction. These examples are not exhaustive, and many other public and paid sources were used to collect data, validate numbers, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on practical checks that are hard to confirm from public sources alone, including typical price bands by chelate type, channel margins, and how application trends are changing across soil, foliar, and fertigation use. We spoke with a mix of manufacturers, distributors, agronomists, and large farm input buyers across major consuming regions, which helped close gaps in adoption assumptions and confirm the direction of the final totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 20% | APAC: 37% |

| Mid tier: 43% | Functional/Unit leaders: 30% | EMEA: 37% |

| Smaller Players: 22% | Managers: 50% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable demand pool from crop activity and micronutrient intensity, then narrows it to chelated formats based on observed usage patterns in each region. In practice, the model links planted area and crop mix to application routes (soil, foliar, fertigation) and then applies chelate penetration and typical treatment frequency, converting into value using type-level pricing.

The totals shift most with a few inputs, including the share of high-value crops, expansion of fertigation and protected cultivation, soil pH constraints that favor specific chelates (for example, EDDHA use in alkaline conditions), and changes in regulations affecting persistent synthetic chelators. Raw material driven price movement also changes average selling prices by grade. To keep results realistic, we corroborate the top-down output with selective bottom-up checks, such as sampled price lists, distributor channel checks, and limited roll-ups of supplier revenues where reporting is clear, and we handle gaps by applying conservative coverage factors rather than forcing full company mapping.

For forecasting, we primarily use scenario analysis supported by trend smoothing on key variables, since adoption and pricing can move differently by region and crop season. The scenarios are anchored in expert views on micronutrient program expansion, expected mix shift between synthetic and organic chelates, and how quickly price changes pass through the channel.

Data Validation & Update Cycle

Outputs are checked through several steps so the final numbers stay consistent with real-world signals. We compare implied consumption intensity against independent indicators such as crop area shifts, fertilizer spending direction, and trade movement where classification allows a reasonable proxy, then investigate large variances before sign-off.

If an assumption changes meaningfully, such as a sharp raw material swing that impacts chelate pricing or a regulation update that affects permitted chemistries, we re-contact relevant respondents and re-run the affected modules. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery review is done so clients receive the most current view available.

Mordor Intelligence's Agricultural Chelates Market Size Compared Against Other Published Estimates

Published market sizes for agricultural chelates often differ, even when the references point to the same product family, because timing and modeling choices are not always aligned. Differences commonly come from what is counted as chelated value, how prices are averaged across grades and channels, and which year and currency conversion date are used.

A frequent gap driver is refresh cadence, since chelate prices can move quickly with raw material costs and regional mix, and older assumptions can lag the current selling environment. Currency timing also matters because revenues are earned in local currencies and converted for reporting, and small conversion differences can add up in a global total. Some estimates also blend adjacent micronutrient products that are not truly chelated, or they apply a single blended ASP across types. In contrast, our model refreshes ASP bands by chelate type and region before conversion, and it is cross-checked through repeat validation calls, which explains much of the spread around the Mordor Intelligence value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.30 B (2025) | |

| Global Consultancy A | USD 1.03 B (2025) | Uses a longer forecast window with a slower growth path, and the 2025 value appears to reflect a more conservative ASP set that is not clearly adjusted for grade mix and channel pass-through. |

| Industry Publisher B | USD 0.79 B (2025) | Likely applies a narrower product boundary or excludes parts of synthetic chelates, and it appears to rely on a lower average price level that can understate value in regions with higher chelate adoption and stronger fertigation demand. |

Looking across the figures, the spread is mostly explained by how current the pricing and conversion assumptions are, followed by whether the definition captures the full chelated micronutrient basket used in agriculture. By keeping the scope tied to chelated products only and using repeatable demand indicators with practical price checks, the resulting number stays transparent and easier to reconcile with what buyers and sellers observe in the market.

Key Questions Answered in the Report

What is the current value of the Agricultural chelates market and its projected 2031 size?

The market is valued at USD 1.38 billion in 2026 and is projected to reach USD 2.07 billion by 2031.

Which region shows the fastest market growth?

Asia-Pacific is expanding at an 8.8% CAGR through 2031, driven by soil micronutrient deficiencies and subsidy programs.

Why are bio-based chelates gaining share?

Regulatory pressure on persistent synthetic agents and demand for sustainable labels push growers toward biodegradable amino-acid and IDHA grades.

How does smart fertigation influence chelate demand?

Sensor-driven fertigation favors fully soluble chelates that resist precipitation, boosting sales of high-purity liquid grades.

What is the competitive outlook for small innovators?

Moderate concentration and regulatory shifts create openings for niche players offering specialized biodegradable ligands and digital agronomy integration.

Page last updated on: