Agricultural Fogging Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

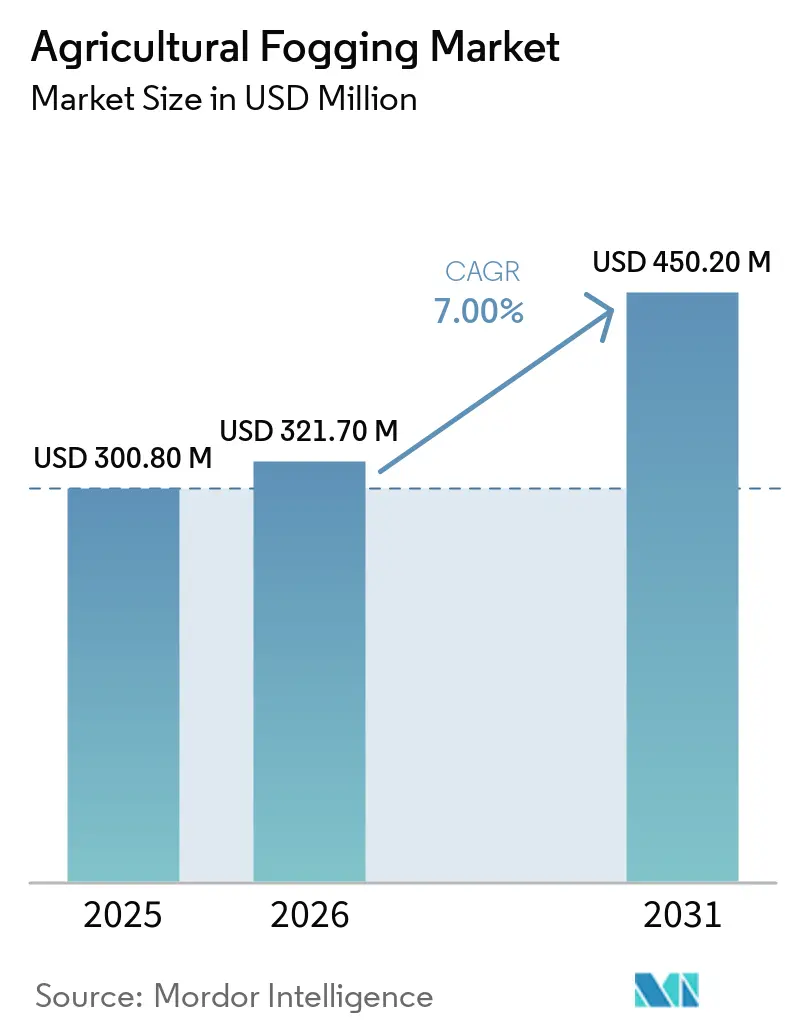

| Market Size (2026) | USD 321.70 Million |

| Market Size (2031) | USD 450.20 Million |

| Growth Rate (2026 - 2031) | 7.00% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Fogging Market Analysis by Mordor Intelligence

The agricultural fogging market size was valued at USD 300.80 million in 2025 and is projected to grow from USD 321.70 million in 2026 to USD 450.20 million by 2031, registering a CAGR of 7.0% during the forecast period from 2026 to 2031. The demand for agricultural fogging equipment remains steady as growers face increasing pressure to control pests and diseases with greater precision while minimizing chemical waste in high-value crop systems. Protected cultivation significantly supports the agricultural fogging market, particularly in the Asia-Pacific region, where greenhouse infrastructure is already extensive and continues to expand in several countries. The product mix in the market is evolving, with cold and electrostatic platforms gaining preference due to their compatibility with water-based and biological formulations, which may lose effectiveness under heat. Regulatory pressures concerning pesticide use, worker exposure, and residue control are driving the demand for machines that enhance on-target deposition and enable safer applications in enclosed spaces. Competitive positions are strongest among engineering-focused suppliers. However, the market faces challenges such as uneven adoption of premium equipment due to rising price competition in Asia and cost sensitivity among smallholder growers.

Key Report Takeaways

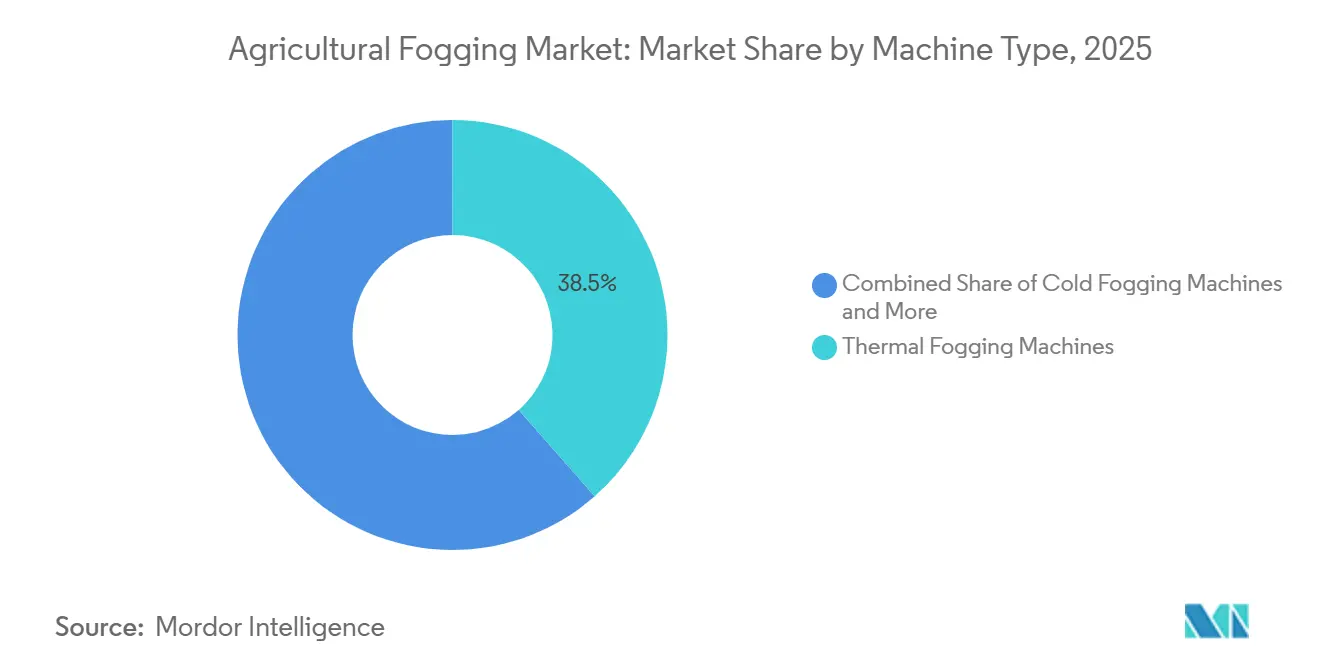

- By machine type, the agricultural fogging market share for thermal fogging machines accounted for the largest 38.5% in 2025, while cold fogging machines are projected to grow at the fastest 8.1% CAGR from 2026 to 2031.

- By power source, fuel-powered machines held the largest 42.0% share in 2025, while the battery-powered systems are forecast to grow at the fastest 11.4% CAGR from 2026 to 2031.

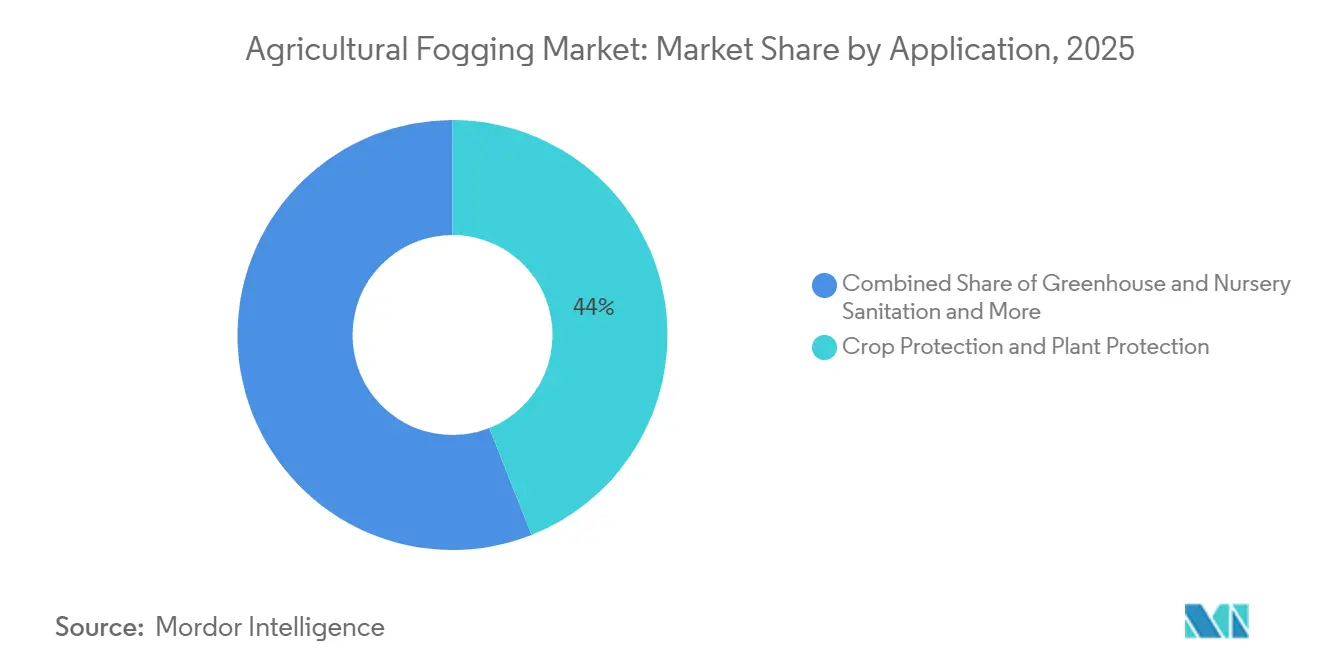

- By application, crop protection and disease management accounted for the largest 44.0% of the agricultural fogging market share in 2025, while the greenhouse and nursery sanitation market size is projected to grow at the fastest 9.2% CAGR from 2026 to 2031.

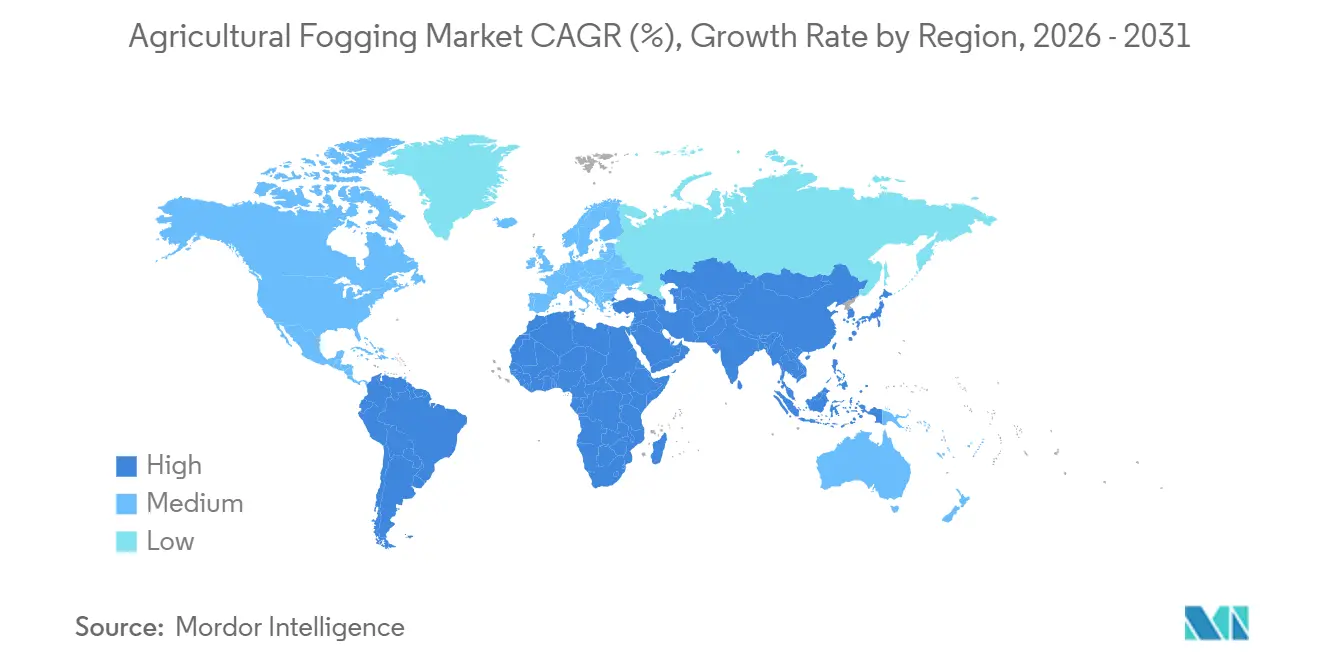

- By geography, Asia-Pacific accounted for the largest 42.3% of the agricultural fogging market size in 2025, and the Asia-Pacific market is projected to grow at the fastest 7.5% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agricultural Fogging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision pest and disease control demand | +1.2% | Global, with stronger intensity in North America, Europe, and East Asia | Medium term (2-4 years) |

| Expansion of greenhouse and protected cultivation | +1.5% | Asia-Pacific core, with spillover into the Middle East and Europe | Long term (≥ 4 years) |

| Mechanization to offset farm labor shortages | +1.3% | North America, Western Europe, Japan, and Australia | Medium term (2-4 years) |

| Need to reduce chemical volume and improve coverage consistency | +1.0% | Europe and North America, with rising importance in South America | Medium term (2-4 years) |

| Re-entry interval and worker-exposure compliance favor remote and automated fogging | +0.8% | North America, Europe, and Australia | Short term (≤ 2 years) |

| Rising adoption of biopesticides and water-based formulations in high-value horticulture | +0.9% | Global, with higher intensity in the Netherlands, California, and Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Precision Pest and Disease Control Demand

The agricultural fogging market is experiencing growth due to the rising demand for precision pest and disease control in crops such as berries, protected vegetables, citrus, and ornamental plants, where the quality of spray coverage significantly impacts treatment effectiveness. A 2024 study published in the Centre for Agriculture and Bioscience International (CABI) Agriculture and Bioscience journal highlighted that electrostatic spraying achieved 327 deposits/cm² on adaxial leaf surfaces, compared to 102 deposits/cm² with conventional spraying systems under identical operating conditions. This higher deposition efficiency is driving the adoption of electrostatic and cold fogging systems, as growers aim for improved canopy penetration, reduced chemical wastage, and more consistent application performance within integrated pest management programs.

Expansion of Greenhouse and Protected Cultivation

Protected cultivation is a key driver for the agricultural fogging market, as greenhouse production necessitates regular sanitation, crop treatment, and environmental control during each growing cycle. According to a 2025 review published in the International Journal of Research in Agronomy, China led the protected cultivation area, reaching 2.76 million hectares in 2024[1]Source: Agronomy Journal, “Protected Cultivation Development and Greenhouse Expansion in China,” agronomyjournals.com. The expansion of greenhouse infrastructure has significantly increased the demand for fogging systems used in crop protection, humidity management, and disease control. Suppliers with robust greenhouse-focused product portfolios are benefiting from the growing intensity of protected cultivation and the rising frequency of production cycles in commercial horticulture operations.

Mechanization to Offset Farm Labor Shortages

The agricultural fogging market is supported by increasing farm labor shortages and rising wage pressures in specialty crop production systems. According to the United States Department of Agriculture National Agricultural Statistics Service, the average gross wage rate for hired farmworkers in the United States reached USD 19.52 per hour in April 2025, reflecting a 3% increase from April 2024[2]Source: United States Department of Agriculture National Agricultural Statistics Service, “Farm Labor Report, May 2025,” nass.usda.gov. The rise in labor costs is driving growers to adopt programmable and semi-automated fogging systems, which reduce the need for manual spraying and enhance operational efficiency. These systems are particularly beneficial in greenhouse nurseries, floriculture, berry cultivation, and horticulture operations, where recurring treatment cycles create consistent labor demands.

Need to Reduce Chemical Volume and Improve Coverage Consistency

Agricultural operators are progressively adopting application systems designed to enhance coverage consistency while minimizing chemical and water usage in crop protection activities. Farmers are increasingly utilizing advanced cold fogging and precision fogging technologies due to their ability to achieve finer droplet distribution, better canopy penetration, and more uniform application across greenhouse, horticulture, and specialty crop cultivation. This shift is further driven by a growing emphasis on sustainable pesticide management, reduced input wastage, and adherence to residue-control regulations. Consequently, equipment that enables efficient low-volume application and consistent deposition performance is becoming more favored in commercial agricultural operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront and maintenance costs for professional systems | -1.5% | Asia-Pacific smallholder markets, Sub-Saharan Africa, and South America | Long term (≥ 4 years) |

| Tightening pesticide-use and residue compliance | -0.8% | North America, Europe, and Australia | Medium term (2-4 years) |

| Heat and formulation incompatibility limits some active ingredients in thermal systems | -0.6% | Global, with higher relevance in high-value horticulture | Medium term (2-4 years) |

| Greenhouse sealing, ventilation, and droplet-calibration demands raise failure risk for smaller growers | -0.5% | Europe, North America, and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront and Maintenance Costs for Professional Systems

High upfront and maintenance costs remain a significant barrier to adoption in the agricultural fogging market, particularly for small- and medium-scale farming operations facing financial constraints. According to the United States Department of Agriculture Economic Research Service, total farm sector production expenses are projected to rise from USD 473.1 billion in 2025 to USD 477.7 billion in 2026. Increasing operating costs are limiting growers' capacity to invest in advanced fogging systems, which require additional expenditures on fuel, maintenance, spare parts, and chemical handling infrastructure. Consequently, equipment replacement cycles are slower in cost-sensitive agricultural operations.

Tightening Pesticide-Use and Residue Compliance

Stricter pesticide-use and residue compliance requirements are posing operational challenges in the agricultural fogging market, particularly for smaller growers without precision application and monitoring capabilities. The European Union Regulation (EU) 2025/115 introduced updated maximum residue levels for various pesticide active substances across agricultural commodities in January 2025. This enhanced residue-control framework is driving the need for accurately calibrated fogging systems that enable controlled droplet application and effective drift management. Consequently, compliance-related operational demands are raising equipment costs and hindering adoption among cost-sensitive agricultural operations with limited technical infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Cold Foggers and Electrostatic Systems Reshape the Platform Mix

The agricultural fogging market share for thermal fogging machines held the largest 38.5% in 2025. These systems maintain strong demand due to their extensive use in open-field crop protection, livestock buildings, storage sanitation, and large-scale agricultural treatments requiring dense fog penetration and broad-area coverage. Factors such as an established supply chain, operator familiarity, and relatively lower equipment costs support their adoption, particularly in developing agricultural economies. Fuel-based thermal systems are especially suitable for outdoor and high-throughput applications where mobility and treatment speed are critical. This category continues to benefit from its widespread application in conventional agricultural pest and disease management practices.

The agricultural fogging market size for cold fogging machines is projected to advance at the fastest 8.1% CAGR from 2026 to 2031. These systems are increasingly adopted due to their compatibility with water-based formulations, biological crop protection products, and controlled droplet application, particularly in greenhouse and horticulture operations. Growers favor cold fogging machines for their ability to ensure precise deposition, minimize chemical wastage, and manage residues effectively. Additionally, electrostatic fogging technologies are driving adoption in precise cultivation environments by enhancing canopy penetration and application consistency. The shift toward sustainable crop protection programs and the need for biological-input compatibility continue to drive demand for advanced cold fogging equipment in commercial agriculture.

By Power Source: Battery-Operated Segment Outpaces All Others

The fuel-powered machines accounted for the largest 42.0% share in 2025. These systems remain widely adopted due to their strong mobility, high output capacity, and operational flexibility, particularly in open-field agriculture and remote farming locations without reliable electricity access. Their use across orchards, broadacre farming, livestock facilities, and large treatment areas ensures stable demand in commercial agricultural operations. Additionally, fuel-based platforms are essential in regions requiring portable, high-capacity equipment for recurring pest control and sanitation activities. The category benefits from established operator familiarity and the widespread availability of equipment through agricultural machinery distribution networks.

The battery-powered systems are projected to grow at the fastest 11.4% CAGR from 2026 to 2031. These systems are increasingly preferred in greenhouse, nursery, and enclosed agricultural operations due to their lower emissions, quieter operation, and ease of handling. The shift is further driven by rising labor-efficiency requirements and a growing interest in portable equipment with reduced maintenance complexity. Advancements in lithium-ion technology, improved runtime performance, and lightweight designs are enhancing the appeal of battery-operated foggers. Additionally, the increasing demand for indoor crop protection and controlled-environment agriculture applications is driving the adoption of battery-powered fogging systems in commercial agricultural operations.

By Application: Crop Protection Anchors and Disease Management Demand While Sanitation Drives Future Growth

The crop protection and disease management segment held the largest 44.0% share in 2025. This segment remains the primary demand category as fogging systems enable fine droplet penetration and efficient chemical dispersion across dense crop canopies. These systems are extensively utilized in fruit, vegetable, greenhouse, and specialty crop cultivation, where consistent treatment coverage is essential for recurring pest and disease management cycles. Additionally, agricultural fogging equipment offers reduced labor intensity and improved application efficiency compared to many conventional spraying methods. The demand is further driven by the increasing need to enhance crop quality, protect yields, and ensure consistent treatment across commercial agricultural operations.

The greenhouse and nursery sanitation market size is forecast to advance at the fastest 9.2% CAGR from 2026 to 2031. This growth is attributed to the rising need for recurring disinfection, humidity control, and biological-input dispersion. Growers are increasingly adopting fogging systems to enhance sanitation efficiency, prevent diseases, and manage controlled environments within enclosed cultivation structures. The demand is further supported by the expansion of greenhouse vegetable production, ornamental cultivation, and nursery activities in commercial horticulture operations. Additionally, the increasing use of biological crop protection products and sanitation-focused cultivation practices continues to drive the adoption of fogging equipment in controlled-environment agricultural systems.

Geography Analysis

Asia-Pacific accounted for the largest 42.3% of the agricultural fogging market share in 2025 and is projected to grow at the fastest CAGR of 7.5% from 2026 to 2031. The region continues to lead demand because greenhouse expansion and mechanized crop protection practices are increasing rapidly across China, India, and Southeast Asia. The expanding greenhouse base is strengthening demand for agricultural fogging systems used in crop protection, sanitation, and environmental management across commercial horticulture operations.

North America and Europe continue to represent technologically advanced regions for agricultural fogging systems, where growers increasingly prioritize precision application and residue management. Commercial greenhouse operators and specialty crop growers across these regions continue adopting advanced fogging systems capable of supporting controlled droplet application and biological-input compatibility. The regions also benefit from stronger regulatory oversight related to pesticide application practices and worker-safety requirements, encouraging use of calibrated fogging technologies with improved operational control.

Europe is a key growth region for agricultural fogging systems due to the ongoing expansion of greenhouse cultivation and the adoption of biological crop protection in commercial horticulture. According to Statistics Netherlands, biological pest control agents were utilized in 94.4% of the greenhouse-cultivated area in the Netherlands in 2024[3]Source: Statistics Netherlands, “Biological Pest Control Used in Greenhouse Cultivation,” cbs.nl. The growing reliance on biological crop protection is driving demand for precision fogging systems that enable controlled droplet application and uniform treatment coverage across greenhouse vegetables, floriculture, and nursery cultivation systems.

Competitive Landscape

The agricultural fogging market remains fragmented, with key players including Igeba Gerätebau GmbH, Micron Sprayers Limited (Goizper Group), B&G Equipment Company, Inc. (Pelsis Group), pulsFOG Dr. Stahl & Sohn GmbH, and Swingtec GmbH. Competition is divided between premium engineering-focused manufacturers and price-driven regional suppliers. European companies maintain strong positions in precision fogging technologies, while Asian manufacturers compete through broader equipment availability and lower-cost product offerings. Market participants are increasingly differentiating through application precision, droplet control, greenhouse compatibility, and operational reliability across diverse agricultural environments. Distribution networks, technical support, and maintenance services are also critical competitive factors, as growers prioritize long-term equipment durability and consistent treatment performance. The competitive landscape continues to evolve with the rise of greenhouse cultivation and the adoption of biological inputs in commercial agriculture.

Competitive strategies in the agricultural fogging market are increasingly focused on precision application capabilities, greenhouse compatibility, and the integration of advanced sanitation technologies. Manufacturers are developing adaptable fogging and spraying systems that enhance deposition quality, canopy penetration, and application efficiency in specialty agriculture environments such as vineyards, berry farms, nurseries, and greenhouse cultivation. Product development efforts emphasize electrostatic application technologies, controlled droplet systems, and automation-ready equipment configurations to support biological crop protection requirements. Suppliers are also enhancing their competitive positioning by designing equipment that minimizes chemical wastage, improves residue management, and aligns with sustainable agricultural practices.

Manufacturers are further strengthening their market position by incorporating automation compatibility, residue-control capabilities, and integration with controlled-environment agricultural systems. Growers increasingly demand fogging equipment that supports recurring sanitation cycles, biological-input application, and precision crop protection while adhering to strict operational compliance requirements. Product development continues to prioritize reduced maintenance needs, improved droplet consistency, and compatibility with enclosed cultivation structures, where treatment accuracy significantly impacts crop quality and disease management. The market offers opportunities for suppliers capable of delivering reliable hardware performance combined with automation support, environmental control integration, and application-tracking capabilities for commercial greenhouse and horticulture operations.

Agricultural Fogging Industry Leaders

Igeba Gerätebau GmbH

Micron Sprayers Limited (Goizper Group)

B&G Equipment Company, Inc. (Pelsis Group)

pulsFOG Dr. Stahl & Sohn GmbH

Swingtec GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: pulsFOG Dr. Stahl & Sohn GmbH introduced the Turbo-MAX SERIES, its first battery-powered cold foggers, utilizing 2×18V CAS battery technology for cordless applications in agriculture, greenhouses, and livestock hygiene fogging.

- March 2024: Shenzhen Longray Technology Co., Ltd. has launched an upgraded range of thermal fogger machines designed for agricultural crop protection and pest control. The new portfolio emphasizes enhanced fogging efficiency, ease of portability, and broader applicability in greenhouse and farming operations.

Global Agricultural Fogging Market Report Scope

An agricultural fogger is a mechanized device designed to disperse pesticides, disinfectants, biological agents, or sanitizing solutions into fine droplets or mist, ensuring uniform coverage across crops, greenhouses, storage facilities, and livestock environments. It is commonly utilized for crop protection, greenhouse sanitation, pest control, humidity management, and post-harvest treatment, where accurate and efficient chemical distribution is essential. The agricultural fogging market report is segmented by machine type (thermal fogging machines, cold fogging machines, and electrostatic fogging machines), by power source (fuel-powered, electric corded, and battery-powered), by application (crop protection and disease management, greenhouse and nursery sanitation, storage and post-harvest protection, and livestock and poultry house hygiene), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Thermal Fogging Machines |

| Cold Fogging Machines |

| Electrostatic Fogging Machines |

| Fuel-powered |

| Electric corded |

| Battery-powered |

| Crop Protection and Disease Management |

| Greenhouse and Nursery Sanitation |

| Storage and Post-harvest Protection |

| Livestock and Poultry House Hygiene |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Italy | |

| Spain | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Thailand | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Morocco | |

| Rest of Africa |

| By Machine Type | Thermal Fogging Machines | |

| Cold Fogging Machines | ||

| Electrostatic Fogging Machines | ||

| By Power Source | Fuel-powered | |

| Electric corded | ||

| Battery-powered | ||

| By Application | Crop Protection and Disease Management | |

| Greenhouse and Nursery Sanitation | ||

| Storage and Post-harvest Protection | ||

| Livestock and Poultry House Hygiene | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| Spain | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Morocco | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2031 value forecast for agricultural fogging?

The agricultural fogging market size is forecast to reach USD 450.2 million by 2031.

Which region leads demand for agricultural fogging equipment?

Asia-Pacific held the largest 42.3% agricultural fogging market share in 2025.

Which machine category is growing fastest in agricultural fogging?

Cold Fogging Machines are projected to be the fastest-growing machine type, registering a CAGR of 8.1% from 2026 to 2031.

Why are battery-operated foggers gaining traction?

Battery-powered systems are projected to grow at the fastest CAGR of 11.4% from 2026 to 2031, driven by increasing demand for safer enclosed-space operations, lower direct emissions, and ease of use in greenhouse environments.

Page last updated on: