Market Overview

| Study Period | 2021 - 2031 |

|---|---|

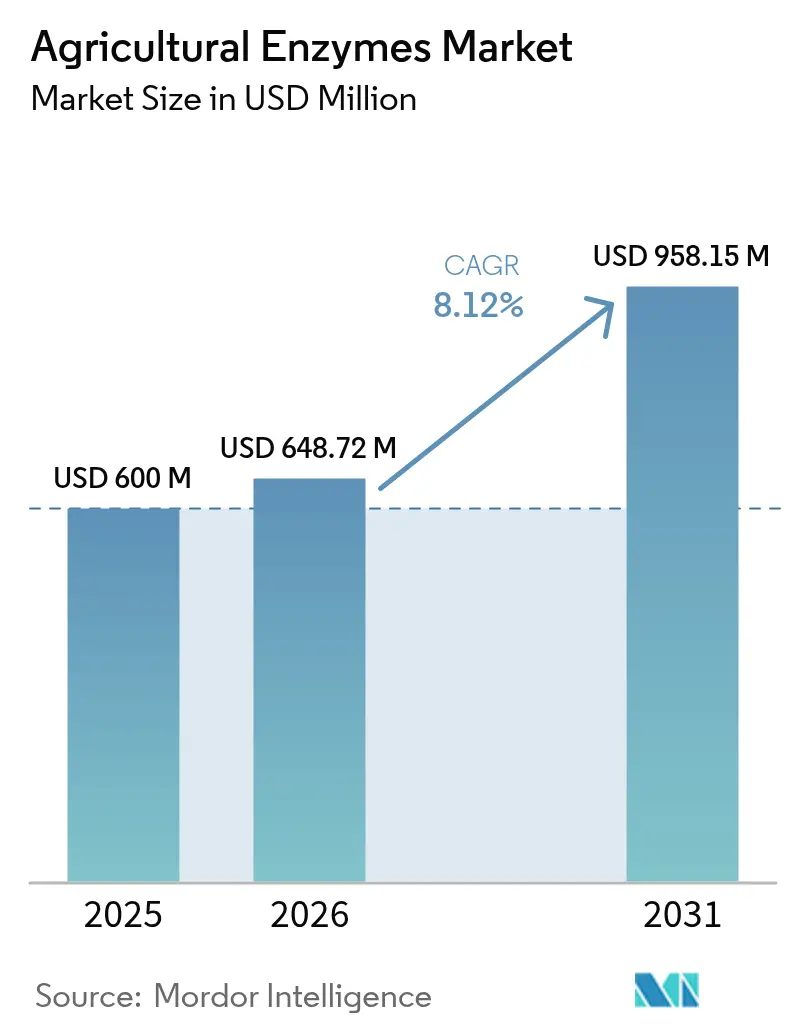

| Market Size (2026) | USD 648.72 Million |

| Market Size (2031) | USD 958.15 Million |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

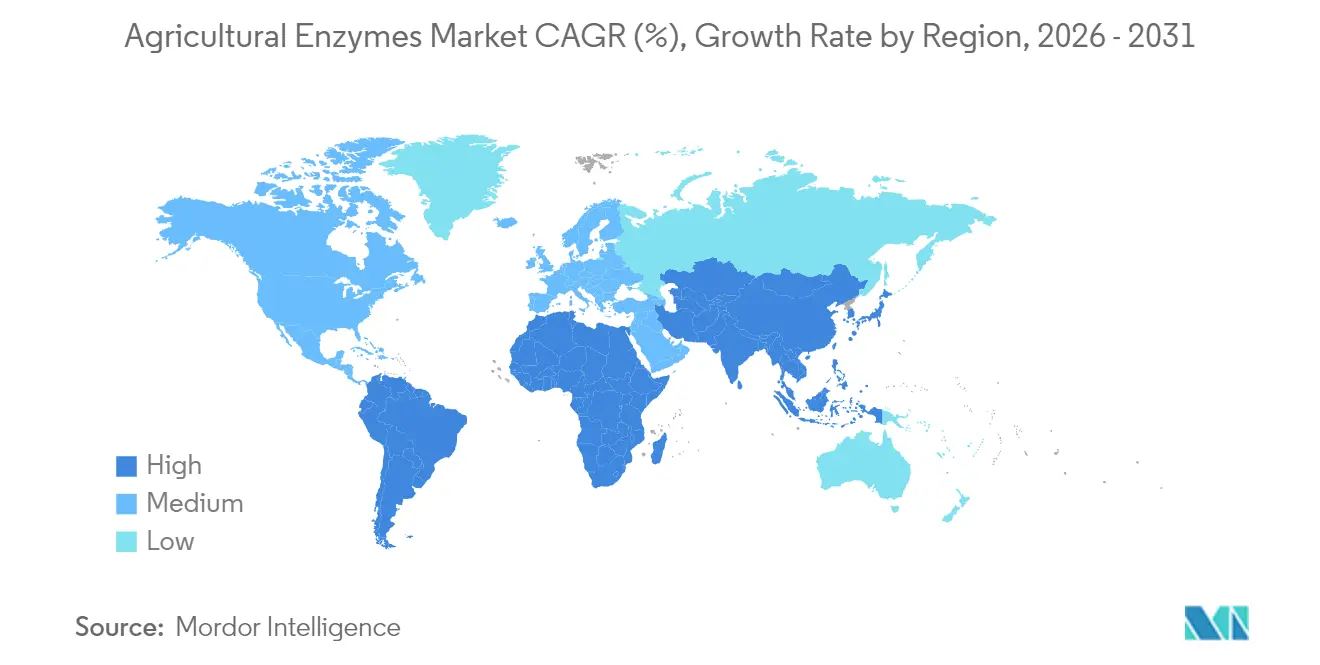

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

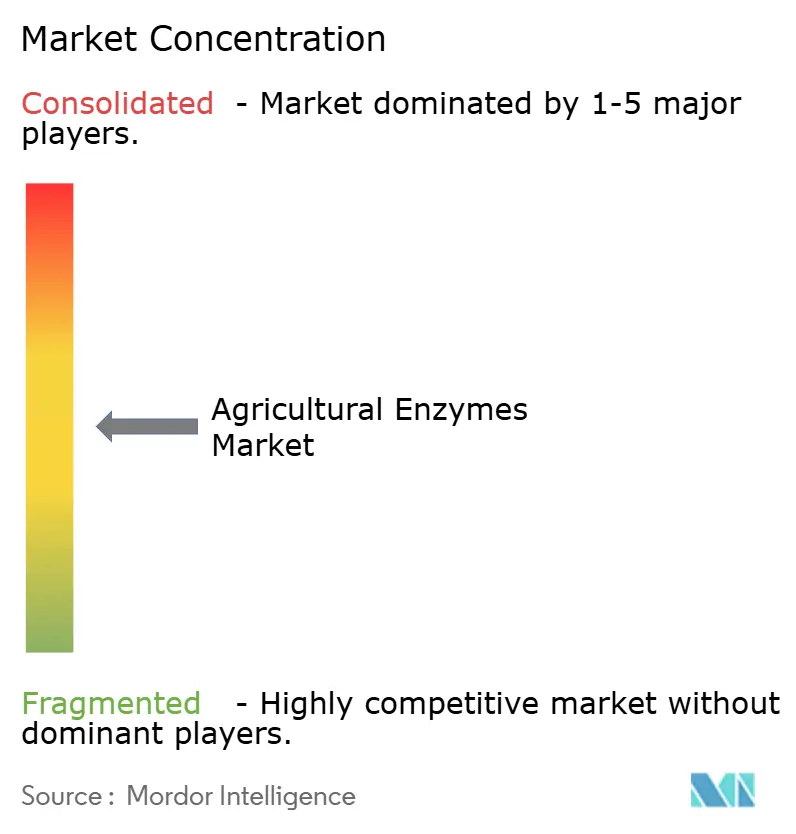

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Enzymes Market Analysis by Mordor Intelligence

The Agricultural Enzymes Market size was valued at USD 600 million in 2025 and estimated to grow from USD 648.72 million in 2026 to reach USD 958.15 million by 2031, at a CAGR of 8.12% during the forecast period (2026-2031). This growth reflects the tightening of regulations on synthetic chemicals, a greater consumer appetite for residue-free food, and steady advances in enzyme formulation and delivery technologies. Commercial growers in mature markets are replacing a share of conventional inputs with enzyme-based biologicals, while smallholders in Asia-Pacific are moving toward yield-boosting biologicals supported by targeted subsidy programs. Parallel advances in precision fermentation and AI-driven protein design are reducing product-development cycles, while long-term carbon-credit programs are generating new revenue streams for farmers who deploy regenerative enzyme solutions. Competitive intensity is rising as agrochemical majors strengthen biological portfolios through partnerships and acquisitions, and specialized biotechnology firms race to commercialize next-generation multi-enzyme cocktails.

Key Report Takeaways

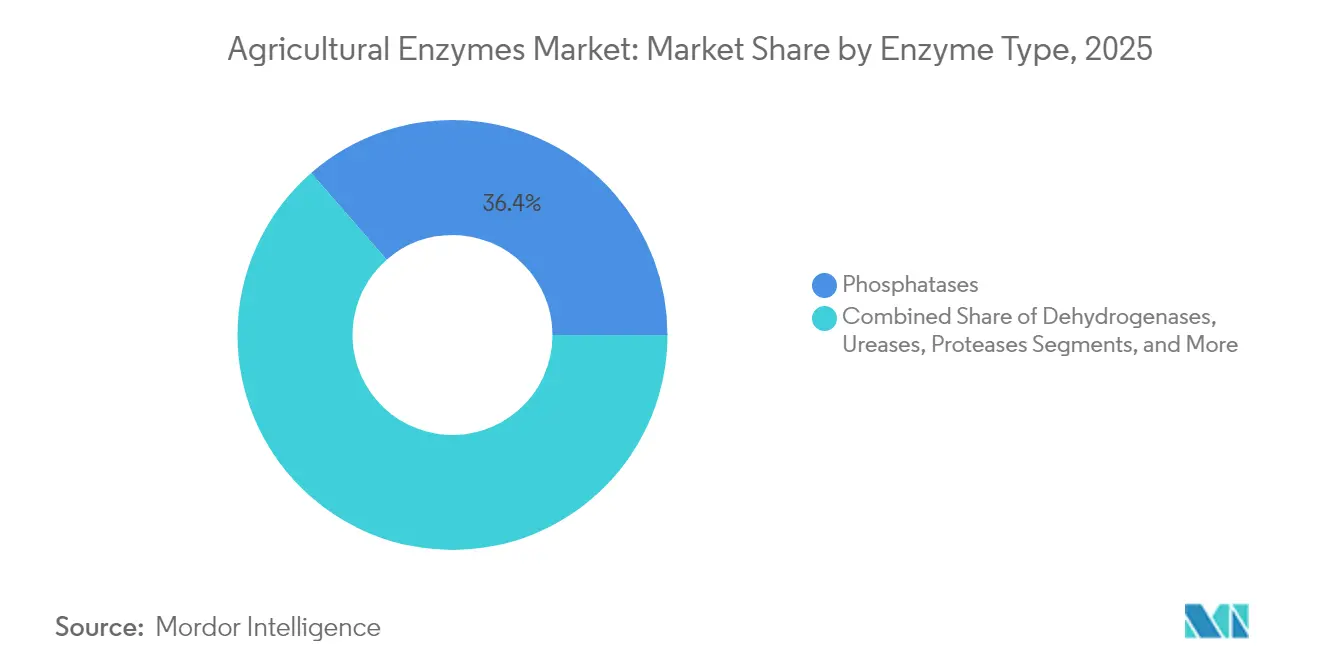

- By enzyme type, phosphatases led with 36.42% agricultural enzymes market share in 2025, while cellulases are forecast to advance at a 13.05% CAGR to 2031.

- By formulation, liquid products accounted for 45.55% of the agricultural enzymes market size in 2025; granular formats are projected to grow at 11.72% CAGR through 2031.

- By application, fertility enhancement commanded 40.35% of the agricultural enzymes market size in 2025, whereas crop protection is set to expand at an 11.32% CAGR between 2026-2031.

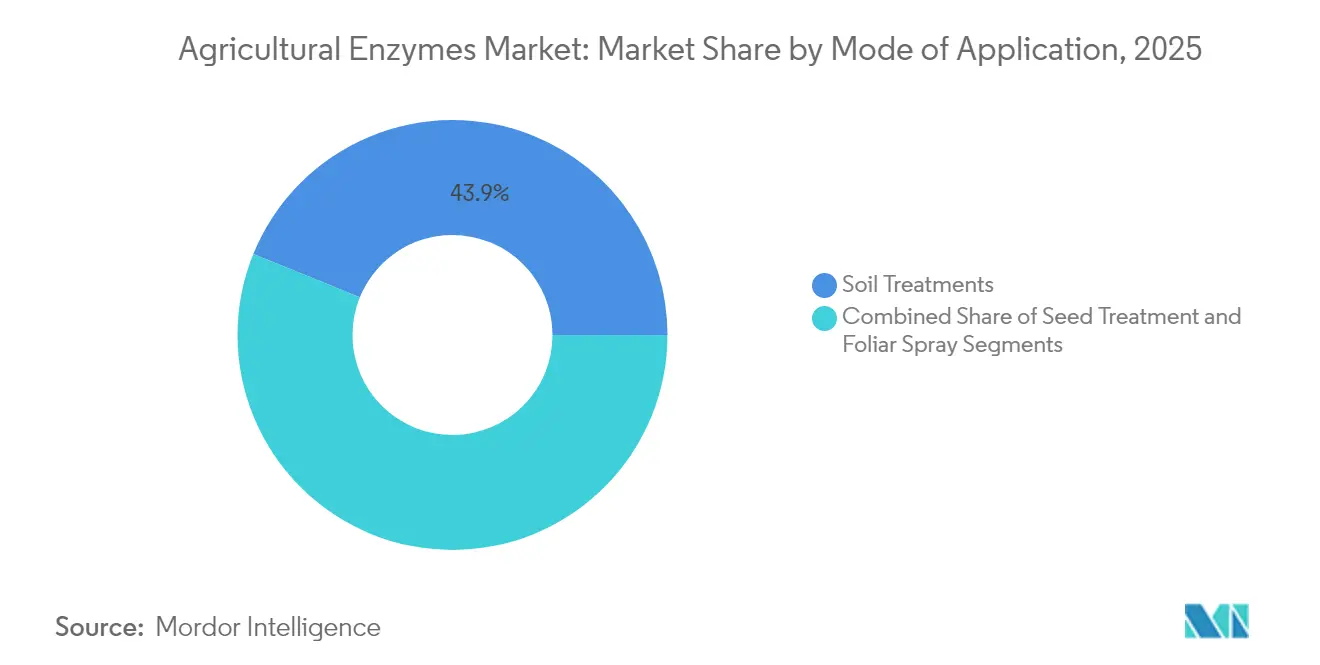

- By mode of application, soil treatments held 43.86% agricultural enzymes market share in 2025, while seed treatments are anticipated to post a 10.24% CAGR to 2031.

- By crop type, cereals and grains secured 39.15% of the agricultural enzymes market size in 2025; fruits and vegetables represent the fastest-growing crop segment at a 10.18% CAGR.

- By geography, North America dominated with roughly 34.62% agricultural enzymes market share in 2025, whereas Asia-Pacific is projected to register a 9.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agricultural Enzymes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Organic and residue-free food demand | +1.8% | Global, concentrated in North America and EU | Medium term (2-4 years) |

| Biological input adoption surge | +2.1% | Global, led by Asia-Pacific and Brazil | Short term (≤ 2 years) |

| Intensified Research and Development, and product innovation | +1.4% | North America and EU core, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Seed-coating micro-dose delivery | +0.9% | North America and Brazil, expanding to Asia-Pacific | Medium term (2-4 years) |

| Regenerative-ag carbon-credit programs | +1.2% | North America and EU, pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| On-farm enzyme fermentation units | +0.6% | Developed markets initially, scaling to emerging regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Organic and Residue-free Food Demand

Global spending on organic produce is climbing as retailers tighten residue thresholds, and the EU Farm to Fork Strategy mandates a 50% cut in chemical pesticide use by 2030. Farmers gain 20–30% price premiums in certified organic channels, offsetting the transition costs of adopting enzymes that mobilize nutrients without chemical residues. Enzyme-embedded programs help close yield gaps in organic systems by enhancing phosphorus and nitrogen availability, fortifying plant defense pathways, and improving soil microbiome balance. Commercial orchard operators in Spain reported a 9% yield uplift after switching from phosphate fertilizers to a blended phosphatase-urease granule in 2024, demonstrating clear economic returns. Similar outcomes are now driving uptake in greenhouse vegetables across Canada, where liquid cellulase blends shorten crop cycles by improving biomass breakdown between rotations.

Biological Input Adoption Surge

Brazil has adopted biological crop-protection solutions on a significant portion of its cultivated land, surpassing adoption rates in the European Union and the United States. Mounting resistance to synthetic herbicides and fungicides is accelerating the search for new modes of action, positioning agricultural enzymes as synergistic companions to biocontrol microbes. Row-crop growers in Mato Grosso logged a 4.6% corn-on-corn yield gain in the 2024/25 season after integrating a seed-treatment cocktail containing lipase and mannanase enzymes. Similar momentum is unfolding in India, where state-level subsidy programs cover up to 30% of enzyme input costs, catalyzing smallholder adoption and fueling double-digit market growth.

Intensified Research and Development, and Product Innovation

The discovery of the CelOCE cellulase in 2025 highlights advancements in enzyme engineering, enhancing glucose release from residues for improved applications. Venture funding is reflecting this trend Arzeda secured USD 38 million in October 2024 to enhance generative AI protein design for improved enzyme performance. Precision fermentation platforms are lowering production costs, and encapsulation technologies now protect enzymes against ultraviolet degradation in the field. These advances enable custom formulations tailored to crop stage, soil pH, and climate, expanding addressable acres for the agricultural enzymes market.

Seed-coating Micro-dose Delivery

Micro-dose seed-coating systems position enzymes directly on the seed surface, synchronizing activation with germination. Meristem’s HOPPER THROTTLE MAXSTAX Soybean, introduced for the 2025 United States season, integrates multiple inputs, including lipase and mannanase, into a single pass, simplifying the application process. Trials in Iowa demonstrated notable yield improvements compared to untreated checks. Similar micro-dose platforms are being developed for sorghum and wheat, and research on nano-DAP seed coatings in India has shown significant yield enhancements in sunflower, underscoring the technology’s adaptability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented regulatory approvals | -1.1% | Global, especially EU and emerging markets | Short term (≤ 2 years) |

| Soil and climate-based performance variability | -0.8% | Tropical and semi-arid regions | Medium term (2-4 years) |

| Cold-chain gaps in tropical regions | -1.3% | Asia-Pacific, Africa, South America | Medium term (2-4 years) |

| Invisible short-term Return on Investment vs chemicals | -0.7% | Global, pronounced in price-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Regulatory Approvals

Biological input developers still navigate divergent approval timelines, with the EU requiring multiple dossiers depending on product classification. The new United States Unified Website for Biotechnology Regulation improves domestic transparency, yet global harmonization remains distant.[1] U.S. Department of Agriculture, Environmental Protection Agency, and Food and Drug Administration, “Unified Website for Biotechnology Regulation,”Delays add 18–24 months to average commercialization cycles, inflating compliance costs and prompting some firms to prioritize fewer, high-value markets. Smaller innovators struggle most, often partnering with larger agrochemical companies for regulatory support, which can limit independent go-to-market strategies.

Cold-chain Gaps in Tropical Regions

Liquid enzymes typically demand refrigerated storage, but cold-chain shortfalls reach 80% in India’s dairy sector and 90% in fisheries, reflecting broader infrastructure gaps.[2]World Bank, “Food Cold Chain Logistics in Emerging Economies,” worldbank.org Up to 25% of agricultural produce is lost annually in similar markets, underscoring logistical constraints for temperature-sensitive inputs. Solar-powered micro cold-stores and water-dispersible granules are emerging solutions, yet implementation costs and financing hurdles remain. These conditions favor granular enzyme formats that tolerate ambient distribution, shaping product-development priorities for companies targeting tropical climates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enzyme Type: Phosphatases Lead, Cellulases Accelerate

Phosphatases captured 36.42% of the agricultural enzymes market in 2025 by unlocking immobilized soil phosphorus that otherwise reaches 80% of applied fertilizer. As fertilizer prices remain volatile, demand for phosphorus-mobilizing solutions stays strong across cereals and oilseeds. The agricultural enzymes market size for phosphatases is, therefore, set to maintain a dominant revenue position through 2031. Cellulases, propelled by CelOCE and related innovations, top the growth chart at a 13.05% CAGR. These enzymes deconstruct crop residues, releasing sugars that fuel beneficial microbes and improve soil structure. Ureases, lyases, and proteases round out the portfolio, with cocktail products increasingly combining complementary activities to match complex field conditions.

The shift toward multi-enzyme blends is pronounced in high-value horticulture, where growers demand precise nutrient mobilization and stress-response enhancement in one pass. Start-ups are developing on-farm fermentation kits that allow growers to brew fresh cellulase-rich mixes, avoiding shelf-life concerns and reducing costs. Larger players integrate phosphatase-urease synergies to improve nitrogen use efficiency and mitigate volatilization in paddy fields, reflecting a broadening solution set within the agricultural enzymes market.

By Formulation: Liquid Dominance Meets Granular Innovation

Liquid products retained 45.55% of the agricultural enzymes market size in 2025, primarily due to their compatibility with existing spraying equipment and efficient foliar absorption. Yet logistics costs and cold-chain dependency are steering product managers toward more temperature-tolerant technologies. Granular products, advancing at 11.72% CAGR, now embed “bioreactor-in-a-granule” architectures that stabilize enzymes for up to 24 months while enabling timed release after soil contact.

Powder formulations occupy a cost-efficient middle ground, but require dedicated mixing equipment. Hybrid water-dispersible granules blur these lines, providing liquid-like convenience with granular durability. Expect competitive differentiation to hinge on formulation versatility, particularly for companies pursuing growth in the Asia-Pacific and African tropics where cold-chain gaps persist.

By Application: Fertility Enhancement Anchors Growth

Fertility enhancement held 40.35% of the agricultural enzymes market size in 2025, reflecting the universal need to stretch every kilogram of fertilizer. Enzyme programs that mobilize locked nutrients and improve microbial cycling cut input bills and advance sustainability metrics. The segment further benefits from government-linked carbon-credit schemes that reward measurable emissions reductions tied to nutrient-use efficiency.

Crop protection, rising at 11.32% CAGR, leverages enzymes for novel modes of action against pests and pathogens. Lipase-based biofungicides are already demonstrating double-digit yield gains in citrus groves, while chitinase-fortified bacterial consortia suppress soil-borne diseases in greenhouse tomato. Over the next five years, formulations that combine fertility and protection attributes are anticipated to command premium pricing and broaden the agricultural enzymes market.

By Mode of Application: Soil Treatment Foundation, Seed Treatment Momentum

Soil treatments formed the backbone with 43.86% agricultural enzymes market share in 2025, aligning neatly with regenerative farming practices that emphasize microbial health and organic matter turnover. Conservation-till systems in the US Corn Belt show a 0.4 percentage jump in soil organic carbon after two seasons of phosphatase-urease applications.

Seed treatments deliver the fastest momentum, clocking a 10.24% CAGR. By packaging enzymes in micro-doses, companies ensure activation occurs close to germination, avoid foliar re-entry intervals, and reduce application labor. Foliar sprays remain essential for high-value crops requiring rapid, in-season adjustments, while root-drip injectables are preferred in arid orchards where water efficiency is critical.

By Crop Type: Cereals Foundation, Fruits and Vegetables Expansion

Cereals and grains dominated with a 39.15% market share in 2025, driven by scale efficiencies across corn, wheat, and rice. Their established distribution networks, alongside integrated pest-management protocols, create a ready channel for enzyme add-ons. The rapid adoption of fertility programs in Brazilian soy and the United States corn underscores sustained demand.

Fruits and vegetables post the briskest growth at 10.18% CAGR, buoyed by higher price realization for residue-free produce. European greenhouse operators deploy cellulase-laced drip systems to accelerate root turnover and decrease disease cycles. Oilseeds and pulses benefit from enzyme-enhanced nitrogen fixation, while turf and ornamentals, though niche, secure premium margins through aesthetic performance.

Geography Analysis

North America, holding about 34.62% of the agricultural enzymes market in 2025, benefits from robust distribution infrastructure and rapid regulatory clearance for biological inputs. Canadian growers planted 11.8 million hectare of genetically engineered crops last season, creating a receptive environment for complementary enzyme programs. The United States biostimulant segment is equally vibrant, with enzyme‐infused foliar sprays gaining traction among almond and tomato producers.

Asia-Pacific is the fastest-growing region, on track for a 9.56% CAGR through 2031. India’s BioAgri segment reached USD 12.4 billion in 2023, and state subsidies now cover up to 30% of enzyme costs, accelerating adoption among smallholders. Cold-chain gaps remain a material hurdle, 80% of the required capacity is still absent across India’s dairy sector, prompting manufacturers to emphasize granular products. China’s land-transfer reforms encourage larger farm units, improving the business case for enzyme technologies that can be applied at scale.

Europe retains a strong foothold due to stringent pesticide-reduction goals under the Green Deal. Biocontrol active substances climbed from 120 in 2011 to almost 220 in 2022, doubling revenue to EUR 1.549 billion (1.784 billion) in that period. South America, led by Brazil’s trail-blazing 60% biological adoption, remains a mature yet expanding arena, particularly for enzyme-enhanced seed treatments in soy and corn. The Middle East and Africa show emerging promise, though growth hinges on regulatory clarity and cold-chain investment, with South Africa and the Gulf states spearheading early adoption.

Competitive Landscape

The agricultural enzymes market maintains moderate fragmentation, with increasing consolidation as major agrochemical companies pursue biological growth opportunities. Novenesis Group, Elemental Enzymes, and Infinita Biotech Pvt. Ltd. are the major companies that are partnering with Chemical companies to expand their products. In May 2025, UPL established an exclusive agreement with Elemental Enzymes for the Brazilian market, with plans to replicate this model globally by 2027.

Technology development remains a key competitive factor. Arzeda's USD 38 million funding in 2024 supports AI-enabled protein design to develop enzyme variants with enhanced field stress resistance. AgroSpheres secured USD 37 million for developing nanocarrier technology that improves enzyme stability on leaf surfaces. Marrone Bio Innovations' patent applications demonstrate specific progress, with their water-dispersible granules showing 15% higher field efficacy than liquid formulations in high-humidity conditions.

The market presents growth potential in crop-specific enzyme solutions and localized production methods. Companies are testing containerized fermentation systems for on-site enzyme blend production, reducing transportation costs and enabling customization based on soil analysis. Market success depends on demonstrating scientific validity and providing a clear return on investment evidence that meets farmer requirements.

Agricultural Enzymes Industry Leaders

Elemental Enzymes

Infinita Biotech Pvt. Ltd

Enzyme Solutions Inc.

Bioworks Inc.

Novenesis Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: INRAE (National Research Institute for Agriculture, Food and Environment) has identified CelOCE (Cellulose Oxidative Cleaving Enzyme), a newly discovered cellulase. This enzyme increases cellulose degradation efficiency by 21%, facilitating improved biomass conversion for biofuel and bioprocessing applications.

- September 2024: AgIdea, which specializes in Research and Development services that transform pre-commercial technologies into solutions for safer and more eco-friendly agriculture, has partnered with Elemental Enzymes, known for its development of agricultural enzymes and biochemical solutions. The two companies have signed a three-year agreement to promote the screening of Elemental Enzymes' innovative technologies in the United States, with a particular focus on row crops.

- May 2024: Rizobacter BioSolucoes, a global leader in bio-innovation, has introduced 'RizoPower'. This product, designed for foliar application, is crafted from a blend of soy, corn, cotton, sugarcane, rice, and wheat. It features the innovative UBP molecule, a first in the bioactivator domain.

- February 2024: Novozymes and Chr. Hansen merged to create Novonesis, a global biosolutions company operating across 30 industries. The company develops enzymes, microbial technologies, and ingredients to support health, food production, and climate-neutral practices.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the agricultural enzymes market as farm-gate revenue from bio-proteins applied on soil, seed, or foliage to free nutrients, guard crops, or steer growth, supplied in liquid, powder, or granular form from microbial, plant, or animal sources.

Scope Exclusion: Inputs meant only for livestock feed, industrial processing, or biofuels are excluded.

Segmentation Overview

- By Enzyme Type

- Phosphatases

- Dehydrogenases

- Ureases

- Proteases

- Lyases

- Cellulases

- Other Enzyme Types

- By Formulation

- Liquid

- Powder

- Granular

- By Application

- Crop Protection

- Fertility Enhancement

- Plant Growth Regulation

- By Mode of Application

- Seed Treatment

- Foliar Spray

- Soil Treatment

- By Crop Type

- Cereals and Grains

- Oilseeds and Pulses

- Fruits and Vegetables

- Turf and Ornamentals

- Other Crops

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed agronomists, formulators, distributors, and growers on four continents and ran short surveys to confirm dose norms, price bands, and subsidy moves.

Desk Research

We mined FAO fertilizer tables, USDA organic acreage, Eurostat chemical dashboards, China MOA notes, and briefs from Biostimulants Europe and ABISOLO. Company 10-Ks in D&B Hoovers, Questel patent abstracts, and Factiva news traced suppliers, prices, and rule changes; the list is illustrative.

Market-Sizing & Forecasting

A top-down rebuild of treated cropland is priced with regional average selling values and checked with focused bottom-up shipment rolls. Four drivers, organic acreage share, dose per hectare, phosphatase prices, and drought index, feed a multivariate regression to 2030, while scenario tests add policy or weather shocks.

Data Validation & Update Cycle

Outputs are matched with customs codes, earnings hints, and satellite vigor maps. Variances prompt analyst review, and the model refreshes each year with interim tweaks after major events.

Why Mordor's Agricultural Enzymes Baseline Commands Confidence

Estimates diverge: a global consultancy quotes USD 600.3 million for 2024, whereas an industry body records USD 635.2 million for 2025. Scope drift, currency picks, and refresh speed explain the gap.

Mordor's clear scope and dual-source checks give decision-makers a dependable starting point.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 600 million (2025) | Mordor Intelligence | |

| USD 600.3 million (2024) | Global Consultancy A | Excludes Asia-Pacific acreage |

| USD 635.2 million (2025) | Industry Association B | Adds feed enzymes; flat ASP |

Mordor's clear scope and dual-source checks give decision-makers a dependable starting point.

Key Questions Answered in the Report

What is the current size of the agricultural enzymes market?

The agricultural enzymes market stands at USD 648.72 million in 2026 and is forecast to reach USD 958.15 million by 2031, implying an 8.12% CAGR.

Which enzyme type holds the largest share today?

Phosphatases lead with 36.42% agricultural enzymes market share in 2025, owing to their pivotal role in unlocking soil phosphorus for crops.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing region, projected to post a 9.56% CAGR through 2031, propelled by smallholder adoption programs and supportive government subsidies.

How are enzymes used in crop protection?

Enzyme-based bio fungicides and seed treatments deliver novel modes of action that complement microbial biocontrols, driving an 11.32% CAGR for the crop-protection application segment through 2031.

Page last updated on: