Agentic AI Applications In Vector Database Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

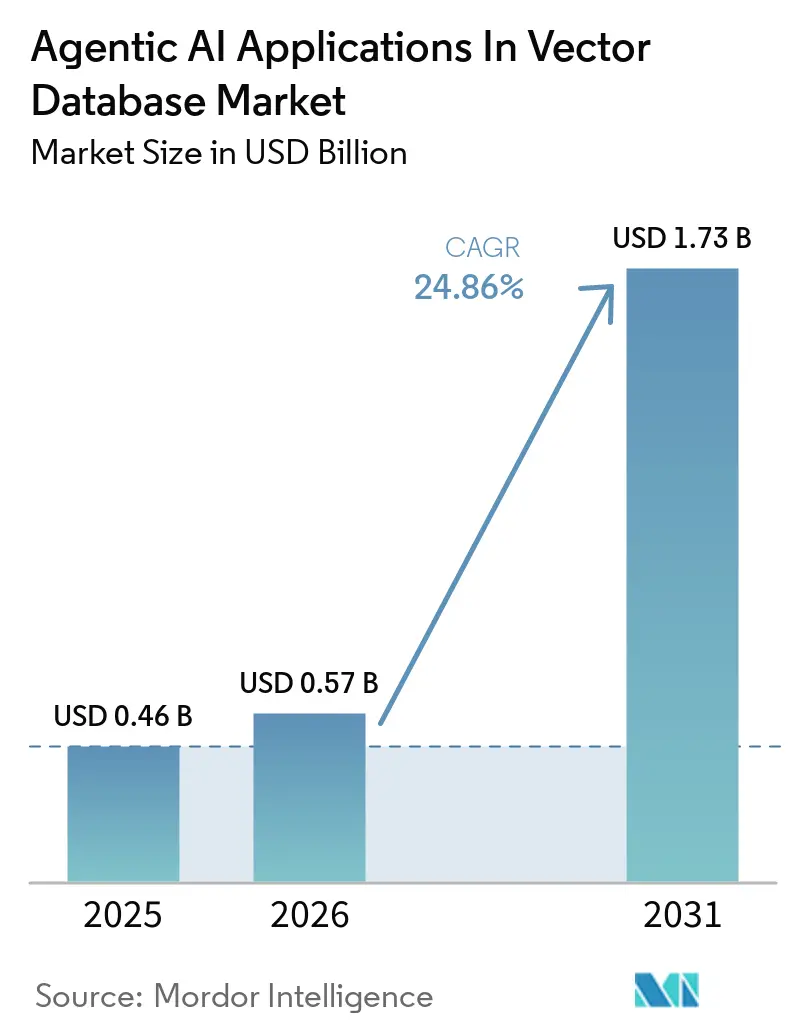

| Market Size (2026) | USD 0.57 Billion |

| Market Size (2031) | USD 1.73 Billion |

| Growth Rate (2026 - 2031) | 24.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI Applications In Vector Database Market Analysis by Mordor Intelligence

The agentic AI applications market size in the vector database market is expected to grow from USD 0.46 billion in 2025 to USD 0.57 billion in 2026, and is forecast to reach USD 1.73 billion by 2031 at a 24.86% CAGR over 2026-2031. The market is moving beyond isolated retrieval-augmented generation pilots and toward persistent memory layers that support production agent workflows across multiple sessions. Demand is rising because multi-agent systems issue far more vector queries per workflow than conventional RAG systems and therefore place greater value on low-latency retrieval, durable memory, and stable indexing at scale. Native vector capabilities in cloud platforms and enterprise databases are also changing buyer behavior, as they reduce integration work and make vector search part of a broader AI infrastructure stack. At the same time, the market is splitting into read-heavy semantic retrieval environments and write-intensive agent memory environments, and that split is creating distinct requirements for performance, governance, and deployment. Compliance deadlines, data residency rules, and sovereign cloud mandates are also opening the door to hybrid and bring-your-own-cloud models, even as hyperscaler offerings expand.

Key Report Takeaways

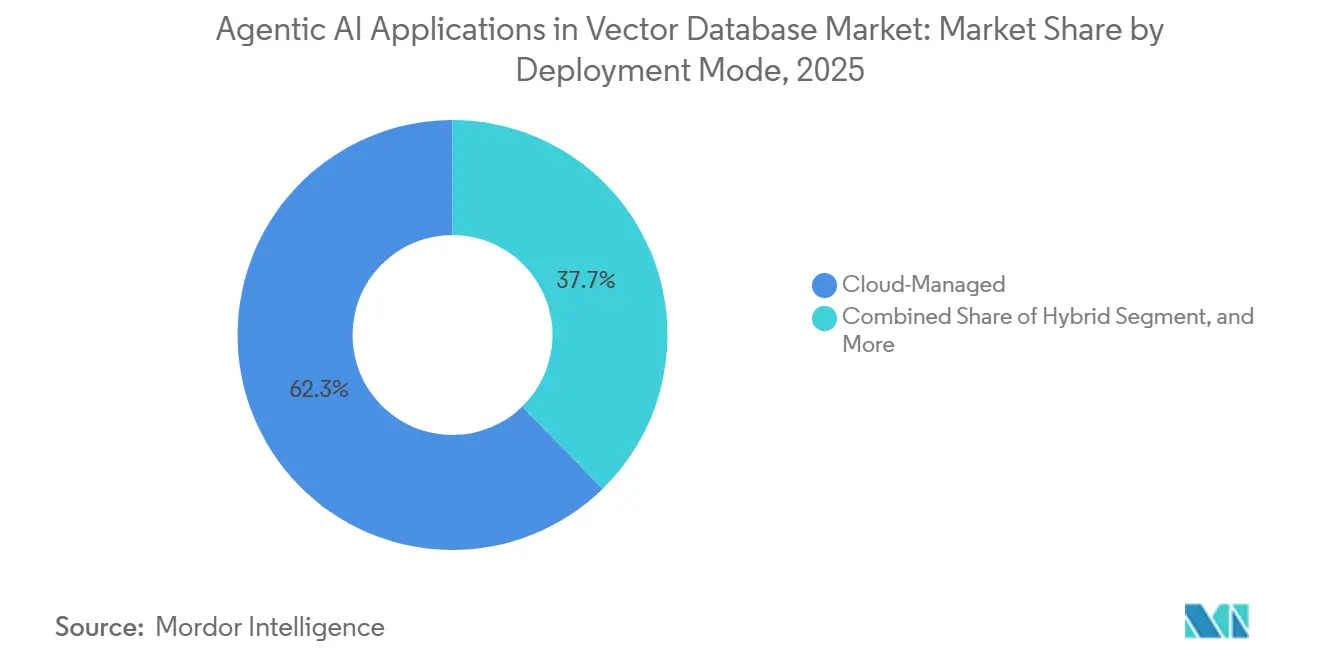

- By deployment mode, cloud-managed deployments led with a 62.31% share of the agentic AI applications in the vector database market in 2025, while hybrid deployments are projected to expand at a 24.81% CAGR through 2031.

- By vector database type, purpose-built vector databases held 55.73% share in 2025, while embedded and edge vector stores recorded the highest projected CAGR at 28.33% through 2031.

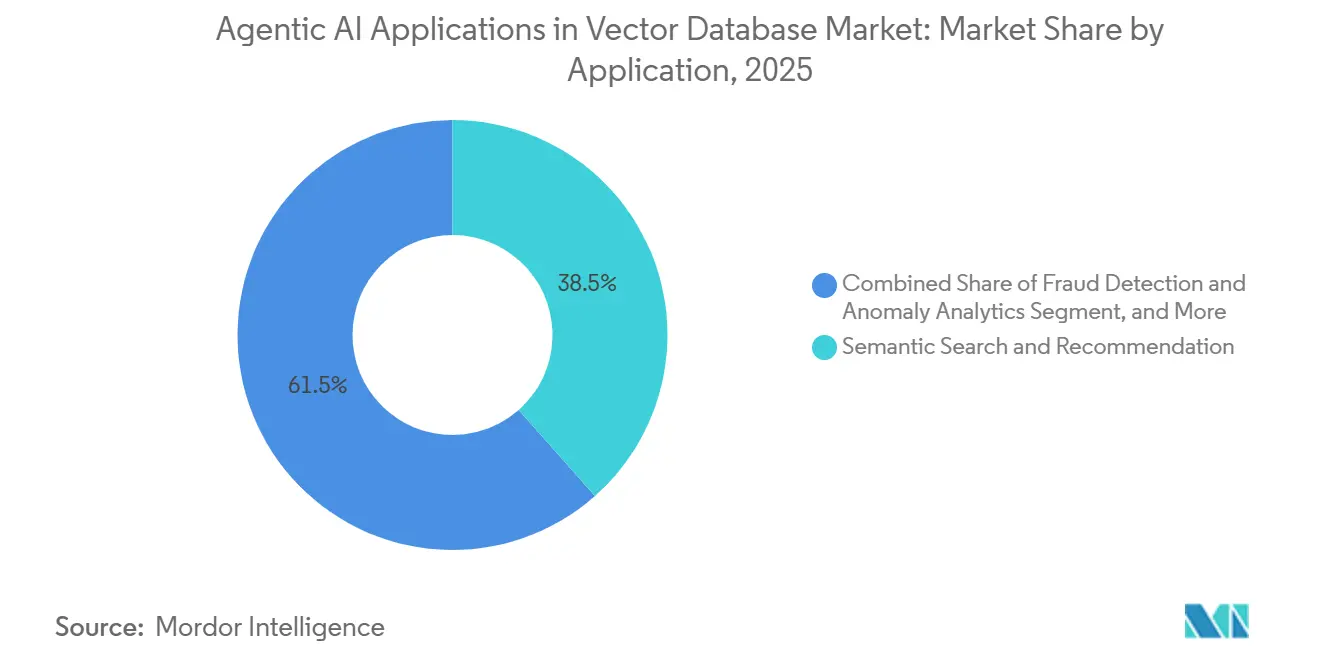

- By application, semantic search and recommendation accounted for 38.47% of the market in 2025, while autonomous agents and workflow orchestration are forecast to grow at a 29.54% CAGR through 2031.

- By end-user industry, IT and telecom captured 29.78% of the market in 2025, while healthcare and life sciences are advancing at a 26.71% CAGR through 2031.

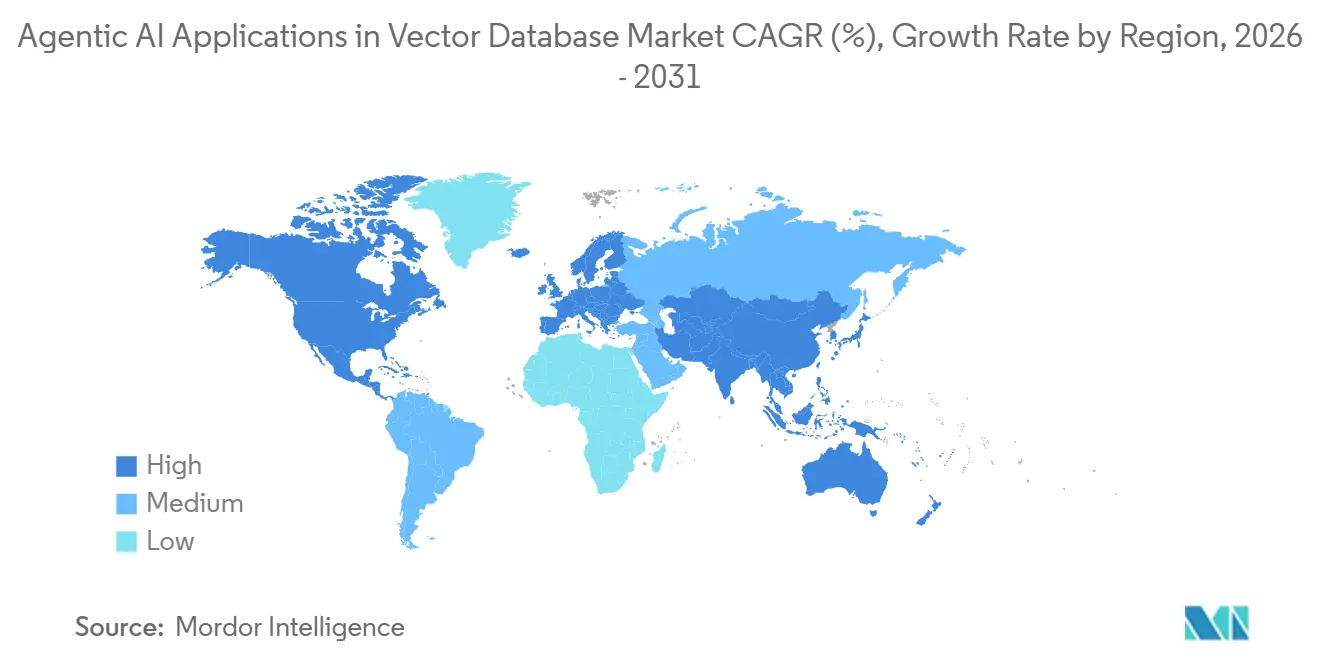

- By geography, North America held 41.11% share in 2025, while the Asia-Pacific is projected to expand at a 25.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agentic AI Applications In Vector Database Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation Of Large Language Models Driving High-Dimensional Retrieval | +6.2% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Rise Of Agentic AI Architectures Necessitating Persistent Memory Stores | +5.8% | Global, with early production gains in North America, early-stage in APAC | Medium term (2-4 years) |

| Cloud Providers Embedding Native Vector Capabilities Into AI Stacks | +4.3% | Global, dominant in North America and Asia-Pacific | Short term (≤ 2 years) |

| Open-Source Vector Engines Lowering Total Cost Of Ownership | +3.1% | Global, with outsized impact in Europe and APAC due to data sovereignty priorities | Medium term (2-4 years) |

| Edge AI Adoption Spurring Demand For Embedded Vector Stores | +2.4% | APAC core, spill-over to Middle East and Africa and Europe | Long term (≥ 4 years) |

| Venture Capital Influx Accelerating Product Innovation | +1.9% | North America primary, Europe secondary | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation Of Large Language Models Driving High-Dimensional Retrieval

Agentic AI applications in the vector database market are benefiting from the shift of large language models from experimentation to production infrastructure. Each enterprise pipeline that combines LLM inference with live internal data requires a vector index that can handle large embedding volumes with low, stable retrieval latency. The pressure is increasing because many organizations are no longer standardizing on a single model and are instead supporting several models that operate in different embedding spaces. That forces them to maintain multiple indexes and raises storage, orchestration, and compute demand inside the same environment. MongoDB introduced 5 Voyage 4 embedding models in January 2026, including a multimodal option with video capability, and integrated them into Atlas Vector Search to reduce dependence on external embedding calls. That kind of integration shows how the agentic AI applications in the vector database market are expanding alongside model diversity rather than around a single retrieval pattern.

Rise of Agentic AI Architectures Necessitating Persistent Memory Stores

The agentic AI applications in the vector database market are also being pushed forward by agentic systems that plan, retrieve, reason, and act across multiple sessions. These workloads differ from static RAG because they can execute thousands of vector lookups for one task and also write new memory back into the system while the task is still active. Qdrant stated in April 2026 that production agent loops generate multi-thousand queries per workflow, while traditional RAG workloads remain much lighter. Enterprises also expect full observability, audit trails, and access controls because every agent action must be explainable to internal governance teams. Amazon Bedrock AgentCore reached general availability in October 2025, introducing persistent memory, semantic retrieval, and native OpenTelemetry observability, raising the baseline for enterprise deployments. As a result, the agentic AI applications in the vector database market are favoring providers that combine performance with governance rather than solely on retrieval speed.

Cloud Providers Embedding Native Vector Capabilities Into AI Stacks

The agentic AI applications in the vector database market are being reshaped by hyperscalers that are placing vector search inside existing storage and database products. This reduces service sprawl and lets enterprises keep semantic retrieval inside the same cloud stack as data storage, orchestration, and model serving. Amazon S3 Vectors expanded to 31 AWS Regions by March 2026 and supported up to 2 billion vectors per index with a 100-millisecond query latency target for frequently accessed workloads. Snowflake Cortex Search reached general availability in March 2026 with multi-index querying and custom vector embedding support inside the Snowflake platform.[1]Snowflake, “Cortex Search - Multi-Index and Custom Embedding General Availability,” Snowflake Documentation, docs.snowflake.com Native services reduce switching costs because vector spending stays within the same cloud billing envelope, avoiding additional data movement across systems. Zilliz responded to this shift with bring-your-own-cloud and customer-managed key options that let buyers preserve control while retaining managed operations.

Open-Source Vector Engines Lowering Total Cost of Ownership

The agentic AI applications in the vector database market are also opening up through open-source engines that reduce licensing friction and support deployment on existing hardware or customer-controlled cloud environments. Open-source options are especially relevant for enterprises that want to limit ongoing query fees and avoid early lock-in while they refine production workloads. Zilliz announced general availability of Milvus 2.6.x in January 2026 with tiered storage and JSON path indexing, which it said improved storage efficiency and metadata filtering performance. Open-source adoption also aligns with sovereignty priorities because buyers can keep vector data in controlled jurisdictions and add governance layers around it. Qdrant reported more than 250 million cumulative downloads and 29,000 GitHub stars in April 2026, indicating a strong developer reach before enterprise conversion begins. This keeps the agentic AI applications in the vector database market open to new entrants even as native cloud services expand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Compute And Storage Costs For Billion-Scale Indexes | -3.2% | Global, with acute pressure in cost-sensitive APAC and emerging markets | Medium term (2-4 years) |

| Lack Of Standardized Benchmarks And Interoperability | -2.4% | Global, particularly in North America and Europe where multi-vendor procurement is common | Medium term (2-4 years) |

| Data-Sovereignty Regulations Restricting Cross-Border Vector Sharing | -1.8% | Europe, Middle East and APAC regulatory-heavy markets | Long term (≥ 4 years) |

| Scarcity Of Skilled Vector Similarity Engineers | -1.5% | Global, with greatest scarcity in South America, Middle East and Africa, and Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Compute And Storage Costs For Billion-Scale Indexes

Agentic AI applications in the vector database market face a real cost ceiling as deployments move from millions of vectors to billions. HNSW indexes remain memory-intensive, and a 1-billion-vector dataset with 1,536 dimensions requires substantial RAM before quantization is even applied. That pushes managed cloud spending to levels that can weaken the business case for mid-market users and for enterprises testing multiple agent workflows simultaneously. Qdrant highlights binary quantization that cuts memory use by 32x while preserving more than 95% recall, but the tradeoff still depends on workload design and tolerance for retrieval drift. The pressure is sharper for agent memory systems because frequent writes increase rebuild frequency and infrastructure load compared with static retrieval systems. Tencent Cloud said its enterprise vector database handled more than 850 billion daily retrieval requests across internal Tencent businesses in 2025, which shows how scale efficiency remains concentrated among the largest operators.

Lack of Standardized Benchmarks And Interoperability

The agentic AI applications in the vector database market are also slowed by the lack of benchmark standards that reflect real production conditions. Common tests still focus on static nearest-neighbor recall and do not capture concurrent writes, memory updates, or latency stability under mixed read-and-write loads. That gives vendors room to highlight favorable benchmark settings, making buyer comparisons more difficult during procurement. Interoperability is another issue because embeddings generated by one model family do not transfer cleanly into another semantic space without re-embedding. A Milvus GitHub issue from February 2026 explicitly requested data lineage, access labels, and audit logging features to support EU AI Act and GDPR-related obligations.[2]GitHub Milvus-Io, “Issue 47812, EU AI Act Compliance Requirements for Data Lineage and Audit Logging,” GitHub, github.com Regulated enterprises, therefore, end up building extra governance layers around the stack, which slows deployment speed across the agentic AI applications in the vector database market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Hybrid Models Bridge Sovereignty And Scale

Within the agentic AI applications market for vector databases, cloud-managed deployments held a 62.31% share in 2025, as buyers favored elasticity, managed availability, and low infrastructure overhead. Cloud-managed services shorten deployment time for AI teams by handling indexing, scaling, failover, and routine maintenance within the platform. The model also fits enterprise buying behavior because vector retrieval is increasingly bundled into broader AI subscriptions rather than purchased as a separate system. Amazon Bedrock AgentCore reinforced that pattern in 2025 by combining persistent memory and semantic retrieval inside a managed service stack.

In the agentic AI applications market for vector databases, self-hosted deployments remain relevant in healthcare, government, and heavily regulated enterprise environments where residency and control remain central. Hybrid deployments are projected to expand at a 24.81% CAGR through 2031 as organizations seek cloud-like operations without losing control of the execution environment. Zilliz positioned directly into that demand with BYOC-I and BYOC Azure options that let customers keep the engine inside their own tenant while retaining vendor support and managed updates. That makes hybrid less of a compromise and more of a default architecture for the agentic AI applications in the vector database market across multi-region enterprises.

By Vector Database Type: Purpose-Built Engines Hold The Core Workloads

Within the vector database market, purpose-built vector databases captured 55.73% of the agentic AI applications share in 2025 because they are designed from the ground up for high-dimensional similarity search. Their value is strongest where latency targets are tight, index sizes are large, and retrieval quality must remain stable under production load. Qdrant reported p50 query latency of 3 milliseconds and p99 latency of 14 milliseconds for 1 million vectors at 768 dimensions, which illustrates why purpose-built engines remain attractive for core workloads. Vector-enabled relational and document stores still matter because they let enterprises add semantic retrieval to existing application databases without introducing another infrastructure layer.

In the agentic AI applications market for vector databases, embedded and edge vector stores are forecast to grow at a 28.33% CAGR through 2031 as AI inference moves closer to the point of action. Qdrant launched Qdrant Edge in July 2025 as an in-process vector library for mobile devices, robots, and resource-constrained hardware. Actian followed in April 2026 with VectorAI DB, aimed at environments ranging from Raspberry Pi systems to enterprise edge servers. This segment is gaining ground in the agentic AI applications market for the vector databases because local search reduces latency, supports offline execution, and meets data minimization requirements.

By Application: Semantic Search Leads While Agent Memory Scales Faster

Within the agentic AI applications in the vector database market, semantic search and recommendation accounted for a 38.47% share in 2025, as it was the earliest large-scale enterprise use case. E-commerce discovery, media recommendation, and enterprise knowledge retrieval created a broad installed base before autonomous agent systems reached production. That base remains important, but it is also more mature because hybrid retrieval patterns are reducing the uniqueness of standalone vector search for standard search tasks. Conversational AI and RAG are another major use case because enterprises continue to rely on vector retrieval to ground model outputs in internal content.

Within the agentic AI applications in the vector database market, autonomous agents and workflow orchestration are the fastest-growing segments, and the market for these segments is projected to expand at a 29.54% CAGR through 2031. Growth is tied to the move from single-step retrieval to multi-step agents that need memory, tool use, and repeated retrieval during a single session. That shift requires stateful, version-aware memory behavior that conventional indexes were not originally designed to handle. The same market is also expanding into bioinformatics and scientific computing, where protein and genomic embeddings create a highly specialized demand for large-scale, high-recall retrieval systems.

By End-User Industry: IT And Telecom Leads While Healthcare Moves Up

Within the agentic AI applications in the vector database market, IT and telecom held 29.78% of the market share in 2025 because these buyers already had cloud-native architectures, internal AI talent, and large data flows. These companies can connect vector retrieval into customer support, software development assistance, and network operations without rebuilding their broader infrastructure stack. Telecom operators are also using vector-backed AI agents for incident similarity matching and faster root-cause analysis across historical records. BFSI, retail, and e-commerce follow closely because all depend on search quality, anomaly detection, and personalization at scale.

Within the agentic AI applications in the vector database market, healthcare and life sciences are projected to grow at a 26.71% CAGR through 2031 as buyers apply retrieval to clinical support, literature grounding, and research workflows. The pace is improving because synthetic embedding governance is clearer and because clinical and scientific data contain large amounts of unstructured information suited to similarity search. Pinecone's HIPAA compliance add-on in 2026 shows that vendors are adapting managed offerings to the specific governance expectations of this customer group. Media and entertainment remain smaller in terms of current share, but they are an active part of the agentic AI applications in the vector database market for multimodal discovery and copyright-sensitive search.

Geography Analysis

Within the agentic AI applications market for vector databases, North America held a 41.11% share in 2025 and remained the leading regional revenue base, as enterprise AI deployments moved into production earlier than in most other regions. The United States led regional spending through large rollouts across financial services, healthcare, and enterprise software, while Canada added support through its research clusters and startup ecosystem. Mexico also contributed through the expansion of nearshore technology services and the wider use of AI-enabled customer engagement platforms in regional delivery centers. The region's regulatory demands are also shaping product design, and managed vendors have already added healthcare-focused compliance features to support U.S. adoption.

Within the agentic AI applications in the vector database market, Asia-Pacific is the fastest-growing region, and the market size in the region is projected to grow at a 25.97% CAGR through 2031. China is a major demand center because domestic AI infrastructure investment is growing, and Tencent Cloud said its enterprise vector database handled more than 850 billion daily retrieval requests across internal Tencent businesses in 2025. Japan is building demand through large-enterprise knowledge management and compliance retrieval use cases that carry high contract value even when deployment counts remain lower. India is supporting growth through its large developer base and IT services sector, which is increasingly evaluating vector platforms for public and enterprise RAG programs. South Korea is strengthening the region's role in embedded deployment because manufacturers are using agentic AI for quality control and supply chain workflows that depend on local vector stores.

Europe has a distinct role in the agentic AI applications market for vector databases because GDPR and the EU AI Act are pushing buyers toward resident infrastructure and stronger governance features. Zilliz made BYOC Azure with customer-managed encryption keys generally available in March 2026, directly addressing those sovereignty requirements within customer-controlled environments.[3]Zilliz, “Milvus Multi-AZ Deployment and BYOC Azure with Customer-Managed Keys,” Zilliz, zilliz.com South America remains smaller, with Brazil as the main node, as cloud investment expands across the region. The Middle East and Africa are gaining momentum through sovereign AI programs, and the Stargate UAE project in Abu Dhabi is building a 1-gigawatt compute base, with an initial 200 MW phase expected to be operational in Q2 2026.

Competitive Landscape

The agentic AI applications market in the vector database space is moderately fragmented, with a 3-layer competitive structure comprising hyperscalers, purpose-built vector specialists, and incumbent database vendors that have extended existing platforms. Hyperscalers compete by bundling storage, compute, and retrieval within a single cloud environment. Pure-play vendors compete on performance, developer experience, compliance features, and deployment flexibility. Incumbent database providers defend their installed base by adding vector functions so customers can extend current systems rather than procure a separate stack.

Consolidation accelerated across the agentic AI applications in the vector database market in 2025 and 2026 as larger platform vendors moved to close product gaps. IBM announced the acquisition of DataStax in February 2025 to strengthen enterprise AI development through distributed vector-capable data infrastructure.[4]IBM, “IBM to Acquire DataStax to Accelerate Enterprise AI Development,” IBM Newsroom, newsroom.ibm.com Databricks agreed to acquire Neon in May 2025, which added serverless PostgreSQL with native pgvector support to its broader AI platform strategy. Oracle deepened its own position in April 2026 by adding partition-level HNSW index management and bitmap compression for sparse vectors in Oracle AI Vector Search. These moves reduced the need for customers to stitch together separate embedding, retrieval, and operational data layers inside the same enterprise architecture.

White space remains open in the agentic AI applications in the vector database market for agent-memory middleware, multimodal retrieval, and bioinformatics-focused search systems that require specialized indexing behavior. Qdrant added GPU-accelerated indexing, multi-availability-zone clusters, and audit logging in April 2026, which strengthened its appeal in regulated and large-scale production deployments. Weaviate released a native MCP server in April 2026, which reduced integration work for developers building agent frameworks that communicate directly with vector databases. Actian also entered the discussion with VectorAI DB in April 2026, showing that edge and operational niches remain open even as the largest providers expand across the broader market.

Agentic AI Applications In Vector Database Industry Leaders

Pinecone Systems Inc.

Zilliz Technology Inc.

Semi Technologies B.V. (Weaviate)

Elastic N.V.

Redis Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Pinecone launched a Frankfurt cloud region and unveiled Pinecone Nexus, a multi-region knowledge fabric that enables enterprise AI agents to perform consistent semantic retrieval across geographically distributed data-residency zones.

- April 2026: Qdrant Cloud shipped GPU-accelerated vector indexing, multi-availability-zone cluster support, and enterprise-grade audit logging in a single release. These features collectively address the 2 primary enterprise adoption barriers, index rebuild latency at billion-scale and compliance auditability, positioning Qdrant directly against hyperscaler-managed vector services in regulated industry procurement cycles.

- April 2026: Oracle released the April 2026 Release Update 23.26.2 for Oracle AI Vector Search, introducing partition-level HNSW index management and bitmap compression for sparse vector types.

- March 2026: Qdrant completed a USD 50 million Series B funding round, with proceeds earmarked for GPU infrastructure expansion, enterprise compliance certifications, and engineering headcount for multi-modal vector capabilities.

Global Agentic AI Applications In Vector Database Market Report Scope

The Agentic AI Applications in Vector Database Market refers to the global market for artificial intelligence applications and autonomous AI agents that leverage vector database technologies to enable advanced semantic understanding, contextual memory, intelligent retrieval, and autonomous decision-making. This market focuses on integrating agentic AI systems with vector databases to support real-time data retrieval, embedding storage, similarity search, knowledge augmentation, and multi-step reasoning across enterprise and consumer applications.

The Agentic AI Applications in Vector Database Market is Segmented by Deployment Mode (Cloud-Managed, Self-Hosted, and Hybrid), Vector DB Type (Purpose-Built Vector Databases, Vector-Enabled Relational/Document Stores, and Embedded/Edge Vector Stores), Application (Conversational AI and Retrieval-Augmented Generation, Autonomous Agents and Workflow Orchestration, Semantic Search and Recommendation, Fraud Detection and Anomaly Analytics, and Bioinformatics and Scientific Computing), End-User Industry (IT and Telecom, BFSI, Healthcare and Life Sciences, Retail and E-Commerce, and Media and Entertainment), Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Managed |

| Self-Hosted |

| Hybrid |

| Purpose-Built Vector Databases |

| Vector-Enabled Relational/Document Stores |

| Embedded/Edge Vector Stores |

| Conversational AI and Retrieval-Augmented Generation |

| Autonomous Agents and Workflow Orchestration |

| Semantic Search and Recommendation |

| Fraud Detection and Anomaly Analytics |

| Bioinformatics and Scientific Computing |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Media and Entertainment |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Mode | Cloud-Managed | ||

| Self-Hosted | |||

| Hybrid | |||

| By Vector Database Type | Purpose-Built Vector Databases | ||

| Vector-Enabled Relational/Document Stores | |||

| Embedded/Edge Vector Stores | |||

| By Application | Conversational AI and Retrieval-Augmented Generation | ||

| Autonomous Agents and Workflow Orchestration | |||

| Semantic Search and Recommendation | |||

| Fraud Detection and Anomaly Analytics | |||

| Bioinformatics and Scientific Computing | |||

| By End-User Industry | IT and Telecom | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Retail and E-Commerce | |||

| Media and Entertainment | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast size of the agentic AI applications in vector database market?

The market was valued at USD 0.46 billion in 2025, is expected to reach USD 0.57 billion in 2026, and is forecast to reach USD 1.73 billion by 2031 at a 24.86% CAGR.

Which deployment model currently leads adoption?

Cloud-managed deployments led with 62.31% share in 2025 because enterprises preferred managed elasticity, faster deployment, and lower infrastructure overhead.

Which application is growing the fastest through 2031?

Autonomous agents and workflow orchestration are the fastest-growing applications, with a projected 29.54% CAGR through 2031 as enterprises adopt persistent memory and multi-step agent workflows.

Which region offers the strongest growth outlook?

Asia-Pacific has the strongest growth outlook with a projected 25.97% CAGR through 2031, supported by domestic AI infrastructure investment and large-enterprise adoption across China, Japan, India, and South Korea.

Which end-user group generates the most revenue today?

IT and telecom led with 29.78% share in 2025 because these users already had cloud-native systems, large data volumes, and internal AI teams that could scale vector retrieval faster.

What is the main competitive challenge for standalone vector database vendors?

The main challenge is commoditization from hyperscalers and incumbent database vendors that are embedding vector capabilities into broader platforms, while buyers also expect stronger compliance, auditability, and residency controls.

Page last updated on: