Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

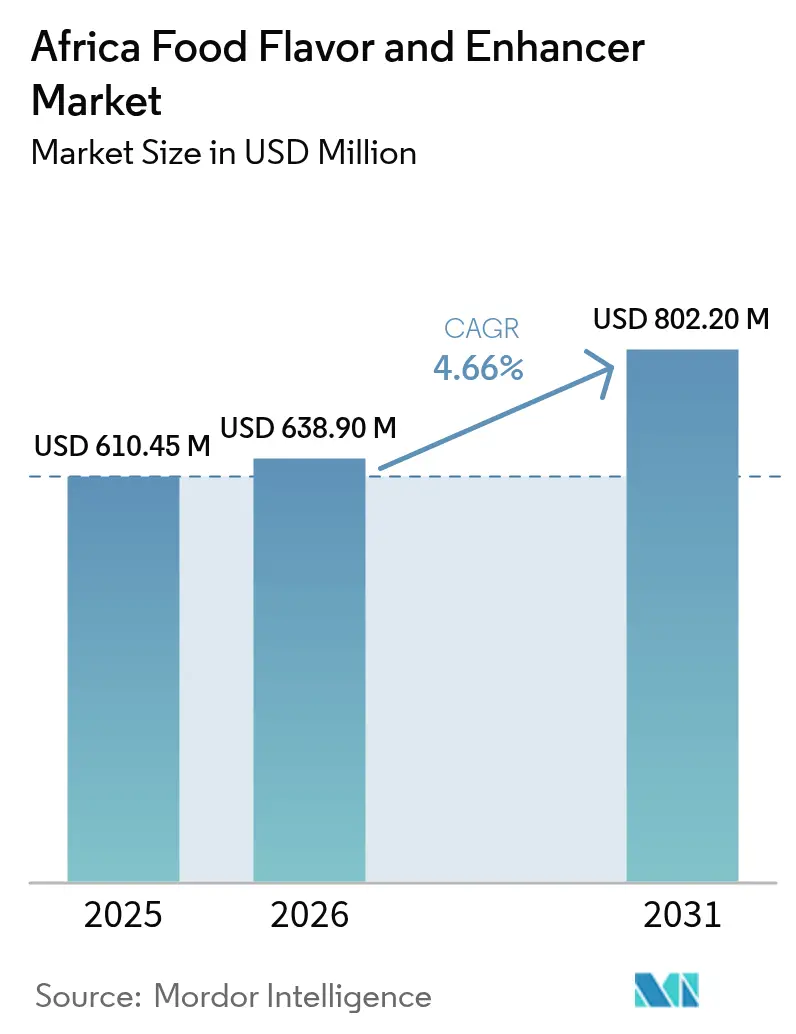

| Base Year Market Size (2025) | USD 610.45 Million |

| Market Size (2026) | USD 638.9 Million |

| Market Size (2031) | USD 802.2 Million |

| Growth Rate (2026 - 2031) | 4.66% CAGR |

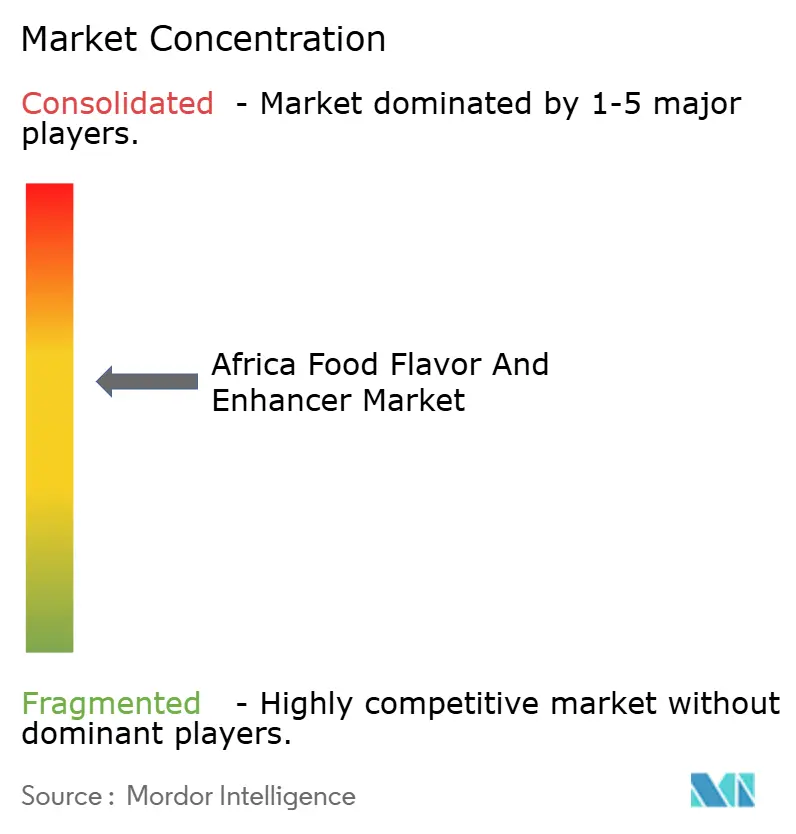

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Africa Food Flavor And Enhancer Market Analysis by Mordor Intelligence

The Africa food flavor and enhancer market size is expected to grow from USD 610.45 million in 2025 to USD 638.9 million in 2026 and is forecast to reach USD 802.2 million by 2031 at 4.66% CAGR over 2026-2031. Consumers are increasingly seeking sophisticated flavor profiles as urban incomes rise and modern retail expands, with global cuisines significantly influencing their preferences. Multinational flavor houses are actively establishing regional hubs to meet this growing demand, while local specialists are leveraging their cost agility to effectively serve smaller processors. Regulatory authorities are intensifying scrutiny on sodium and artificial additives, prompting manufacturers to shift towards natural extracts and clean-label formulations. Although logistics challenges, raw material price volatility, and competition from traditional herbs present obstacles, they also create opportunities for innovation, particularly in encapsulated formats and sodium-reduction technologies, which address evolving consumer and regulatory demands.

Key Report Takeaways

- By product type, food flavor held 78.02% of the Africa food flavor and enhancer market share in 2025; food enhancers are advancing at a 5.26% CAGR through 2031.

- By type, synthetic ingredients captured 74.55% of the Africa food flavor and enhancer market size in 2025, while natural ingredients are forecast to expand at a 6.05% CAGR to 2031.

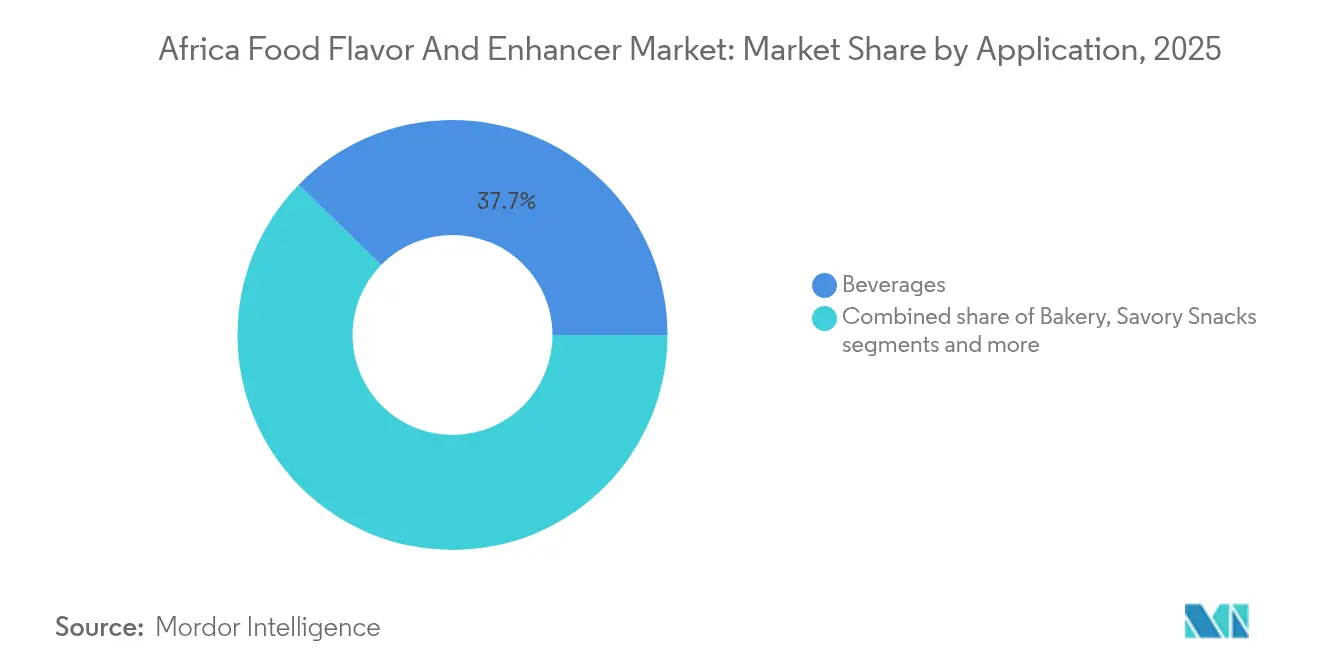

- By application, beverages led with 37.68% revenue share in 2025 and are growing at a 6.12% CAGR through 2031.

- By form, liquid formats accounted for 66.95% share of the Africa food flavor and enhancer market size in 2025; powder formats post the fastest CAGR at 5.42% to 2031.

- By geography, South Africa commanded 41.85% of the Africa food flavor and enhancer market share in 2025, whereas Morocco records the highest projected CAGR at 5.31% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Food Flavor And Enhancer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing preference for diverse and sophisticated taste experiences | +0.9% | South Africa, Nigeria, Morocco | Medium term (2-4 years) |

| Shift toward clean-label, natural, and plant-based ingredients | +1.1% | South Africa, Morocco, Egypt, export-oriented processors | Long term (≥ 4 years) |

| Popularity of flavored beverages, snacks, and ready-to-eat meals | +1.3% | Nigeria, South Africa, urban centers across Africa | Short term (≤ 2 years) |

| Growth of the food and beverage industry | +0.8% | Global, with concentration in Nigeria, South Africa, Egypt | Medium term (2-4 years) |

| Product premiumization and brand differentiation via unique flavors | +0.7% | South Africa, Morocco, Nigeria, Ghana | Medium term (2-4 years) |

| Technological innovation in flavor and enhancer delivery systems | +0.6% | South Africa, Egypt, Morocco, Kenya | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing preference for diverse and sophisticated taste experiences

The Africa food flavor and enhancer market is driven by a growing consumer preference for diverse and sophisticated taste experiences. Increasing urbanization and rising disposable incomes have raised demand for bold, unique, and authentic flavors across beverages, bakery, confectionery, and savory snacks. African consumers, especially in urban centers, seek flavor profiles that extend beyond traditional seasonings, influenced by exposure to global cuisines through digital media and international travel. In South Africa, the carbonated soft drink market grew 8% year-on-year between 2022 and 2023, boosted by limited-edition flavors and AI-assisted formulation, which accelerate product development cycles [1]Source: Food Export, "Market Assessments", foodexport.org. This trend is particularly strong among younger demographics who value experimentation and premiumization. Flavor enhancers are also gaining traction for their ability to deepen taste complexity without increasing sodium levels. Consequently, manufacturers are intensifying research and development investments to meet these evolving and nuanced flavor demands.

Shift toward clean‑label, natural, and plant‑based ingredients

The Africa food flavor and enhancer market is increasingly driven by a shift toward clean-label, natural, and plant-based ingredients. Consumers across the continent are becoming more health-conscious and environmentally aware, prompting demand for products with transparent ingredient lists free from artificial additives. Natural flavors and enhancers sourced from botanicals and sustainable agriculture gain preference, particularly in urban centers. Morocco's World Bank-backed USD 250 million Transforming Agri-food Systems Program, approved in December 2024, targets organic farming expansion to 100,000 hectares by 2030, creating a domestic supply base for natural flavor precursors[2]Source: World Bank, "New Program will Boost Climate Resilience of Agriculture and Quality of Food Production in Morocco", worldbank.org. This trend aligns with global movements toward wellness and sustainability, influencing product development and marketing strategies. Manufacturers are responding by innovating with plant-based extracts and natural antioxidant solutions to meet these preferences. Regulatory frameworks and export requirements further encourage adoption of clean-label formulations.

Popularity of flavored beverages, snacks, and ready-to-eat meals

The rising popularity of flavored beverages, snacks, and ready-to-eat meals across Africa drives the food flavor and enhancer market, fueled by rapid urbanization, expanding middle-class incomes, and shifting lifestyles toward convenience. Beverages lead demand with innovative ready-to-drink options like energy drinks and flavored waters requiring diverse enhancers to meet evolving tastes. Savory snacks show high growth as urban youth seek on-the-go premium varieties amid modern retail expansion. RTE meals surge due to busy schedules boosting needs for consistent natural flavor solutions in processed foods. This trend amplifies enhancer adoption with manufacturers innovating clean-label options to differentiate in competitive segments. Overall these categories reflect a broader appetite for sensory-rich convenient foods spurring market expansion.

Growth of the food and beverage industry

The growth of Africa's food and beverage industry propels the food flavor and enhancer market as rapid population expansion urbanization and rising middle-class incomes fuel demand for processed convenient products. This demographic shift transforms traditional diets into packaged staples dairy beverages and value-added items requiring consistent appealing flavors to suit urban lifestyles. Beverages exhibit accelerated expansion driven by functional drinks and premium options while food segments like bakery confectionery and RTE meals surge with modern retail penetration. Manufacturers respond by scaling production of natural synthetic and enhancer solutions to meet volume growth and taste innovation needs. Strategic investments in local facilities by global players further support this momentum enhancing supply chain efficiency. Overall the industry's projected robust CAGR underscores sustained demand for flavors that differentiate products in competitive dynamic markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High import dependence for advanced flavor ingredients | -0.8% | Nigeria, Kenya, Ghana, East and West Africa | Medium term (2-4 years) |

| Infrastructure and logistics bottlenecks across the supply chain | -0.6% | Nigeria, Kenya, Tanzania, Uganda, landlocked countries | Long term (≥ 4 years) |

| Price volatility and supply risk for natural raw materials | -0.5% | Global, with acute impact in South Africa, Morocco, Egypt | Short term (≤ 2 years) |

| Competition from local seasonings, herbs, and spices as substitutes | -0.4% | Nigeria, Ghana, Kenya, Ethiopia, rural and peri-urban areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High import dependence for advanced flavor ingredients

Africa's food flavor and enhancer market faces a significant restraint due to high import dependence on advanced flavor ingredients. Local production of specialized and high-quality flavor compounds remains limited, forcing manufacturers to rely heavily on imports, which increases costs and supply chain vulnerabilities. Import tariffs, fluctuating currency exchange rates, and logistical challenges further exacerbate the cost burden. This dependence also limits the agility of manufacturers to innovate quickly and respond to evolving consumer preferences. Moreover, the lack of local infrastructure and technical expertise hampers the development of domestic flavor manufacturing capabilities. These factors collectively constrain market growth and competitiveness. Reducing import reliance through local capacity building remains a critical challenge for the sector.

Infrastructure and logistics bottlenecks across the supply chain

Infrastructure and logistics bottlenecks remain a significant restraint on Africa's food flavor and enhancer market, driven by poor transportation networks, inadequate storage facilities, and unreliable power supply that increase operational costs and delay ingredient sourcing and product distribution. While programs like Morocco's FAO and EBRD-backed urban agrilogistics modernization, launched in May 2024, target reducing post-harvest losses and enhancing cold-storage capacity, full implementation will take several years [3]Source: Food and Agriculture Organization, "FAO and EBRD launch urban agrilogistics programme in Morocco", fao.org. Limited cold chain infrastructure complicates handling of temperature-sensitive flavor compounds, and fragmented regional regulations create additional challenges, prolonging lead times and increasing import costs. These ongoing inefficiencies affect product freshness and quality, deter investment, and limit scalability for local manufacturers, making supply chain improvements essential for market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Enhancers Gain as Umami Demand Rises

Food flavors hold the dominant position in the Africa food flavor and enhancer market, capturing 78.02% market share in 2025. This substantial lead stems from their essential role in enhancing taste profiles across a wide array of applications, including beverages, bakery products, confectionery, and dairy items. Manufacturers rely heavily on food flavors to meet consumer demands for diverse and appealing sensory experiences in everyday processed foods. The versatility of flavors allows seamless integration into both sweet and savory formulations, solidifying their market leadership. Urbanization and rising disposable incomes in key African markets like South Africa further amplify adoption in ready-to-eat products.

Food enhancers emerge as the fastest-growing segment in the Africa market, projected to expand at a 5.26% CAGR through 2031. This robust growth trajectory reflects manufacturers' increasing focus on achieving umami depth and improved mouthfeel in formulations. Enhancers enable sodium reduction without compromising flavor intensity, aligning with global health trends gaining traction in Africa. Demand surges particularly in savory snacks, meat products, and beverages where clean-label claims drive innovation. Regulatory shifts favoring low-sodium alternatives in processed foods accelerate enhancer penetration across the region. As processed food consumption rises with population growth, enhancers position for significant market expansion by 2031.

By Type: Natural Ingredients Outpace Synthetic Despite Cost Gap

Synthetic ingredients command 74.55% of the market share in the Africa food flavor and enhancer market in 2025. Their dominance arises from significant cost advantages, typically 40-60% lower than natural equivalents, enabling broad accessibility for manufacturers. Established supplier networks spanning key African hubs like South Africa ensure reliable supply chains and scalability for mass production. These cost efficiencies support widespread use in high-volume applications such as beverages, bakery, and savory snacks. Synthetic options deliver consistent performance and shelf stability, critical for processed foods in emerging markets. Overall, entrenched economics and infrastructure position synthetics as the market leader amid regional growth.

Natural ingredients represent the fastest-growing segment in the Africa food flavor and enhancer market, expanding at a 6.05% CAGR through 2031. This acceleration stems from stringent export-market requirements demanding clean-label certifications for shipments to Europe and North America. Consumer willingness to pay premiums for natural products fuels adoption, particularly among urban health-conscious demographics. Regulatory pressures favoring botanicals and allergen-free profiles further boost natural penetration in dairy and confectionery. Rising investments in local sourcing of herbs and spices enhance supply viability across Nigeria and Egypt. By 2031, naturals will capture greater share as sustainability trends reshape formulation strategies.

By Application: Beverages Lead Share and Growth Velocity

Beverages command the largest application share in the Africa food flavor and enhancer market, holding 37.68% in 2025. This dominance reflects their pivotal role in delivering sensory appeal through diverse flavor profiles tailored to regional tastes. Urbanization across Africa drives demand for convenient, flavored ready-to-drink options consumed daily by growing middle classes. Manufacturers prioritize beverages due to high-volume production and distribution networks in key markets like South Africa and Nigeria. Beverages also emerge as the fastest-growing application segment, projected to expand at a 6.12% CAGR through 2031, surpassing the overall market rate. This accelerated growth stems from the proliferation of energy drinks, flavored waters, and functional beverages targeting health-aware urban consumers.

Savory snacks represent a critical growth area within the Africa food flavor and enhancer market, fueled by urbanization and snacking culture. Enhancers deliver umami and crunch enhancement essential for extruded chips, nuts, and puffed products popular in informal retail channels. Demand surges with youth demographics seeking bold, spicy profiles using synthetic and natural blends. Local manufacturers in Egypt and South Africa leverage cost-effective enhancers to compete with imports. Regulatory focus on sodium reduction accelerates adoption of clean-label alternatives in this segment. Overall, savory snacks position for strong volume gains through 2031 amid convenience food trends.

By Form: Powder Gains on Encapsulation Advances

Liquid formats hold the dominant position in the Africa food flavor and enhancer market, securing 66.95% market share in 2025. Their prevalence stems from superior ease of dispersion in diverse formulations, ensuring uniform flavor distribution. Manufacturers favor liquids for precise dosing capabilities, minimizing waste in large-scale production. Compatibility with high-speed filling lines accelerates adoption in beverage applications across urban processing hubs. Liquids integrate seamlessly into ready-to-drink products, aligning with Africa's expanding packaged goods sector. This entrenched utility cements liquids as the leading form amid rising processed food demand.

Powder formats emerge as the fastest-growing segment in the Africa food flavor and enhancer market, advancing at a 5.42% CAGR through 2031. Advancements in encapsulation technologies enhance stability against oxidation and moisture exposure. These innovations extend shelf life critical for distribution in Africa's hot, humid climates spanning Nigeria to South Africa. Powders offer cost-effective bulk handling for bakery and savory snacks, reducing logistics challenges. Improved solubility supports versatile use in dry mixes and instant products gaining traction regionally. By 2031, powders will capture expanded share as infrastructure supports ambient-stable solutions.

Geography Analysis

South Africa dominates the Africa food flavor and enhancer market, capturing 41.85% market share in 2025. This leadership position relies on well-established food-processing clusters concentrated in Gauteng and the Western Cape regions. Stringent compliance frameworks, including ISO 22000 and FSSC 22000 certifications, attract multinational flavor houses to establish operations there. A mature retail landscape enables premium brands to secure price premiums through innovative flavor offerings. High urbanization rates and sophisticated consumer preferences further reinforce South Africa's central role in regional demand. Overall, these structural advantages sustain its top position amid continental market expansion.

Morocco stands out as the fastest-growing country in the Africa food flavor and enhancer market, projected to advance at a 5.31% CAGR through 2031. Rapid industrialization of its food processing sector drives demand for advanced flavor solutions in exports to Europe. Government incentives for agro-processing in coastal hubs like Casablanca accelerate infrastructure development. Rising tourism and urban consumption patterns favor diverse flavor profiles in beverages and confectionery. Strategic trade agreements enhance access to natural ingredient sourcing from the Mediterranean region. By 2031, Morocco will significantly narrow the gap with leaders through sustained investment momentum.

Nigeria maintains a significant share in the Africa food flavor and enhancer market, positioning it as a key battleground for flavor innovation. Despite persistent infrastructure bottlenecks, local manufacturers innovate with cost-effective synthetic blends for savory snacks and beverages. Heavy import dependence on flavors underscores opportunities for regional suppliers amid population-driven demand. Youth demographics fuel experimentation with bold, ethnic-inspired profiles in urban centers like Lagos. Efforts to localize production through policy reforms could mitigate logistics challenges over time. Nigeria's scale ensures its enduring relevance despite operational hurdles.

Competitive Landscape

The Africa food flavor and enhancer market displays moderate fragmentation, where global giants such as Givaudan, dsm-firmenich, Symrise, IFF, and Kerry collectively control an estimated 50-60% market share. These multinational leaders leverage unparalleled scale advantages, enabling cost-efficient production and distribution across key hubs like South Africa and Nigeria. Deep R&D capabilities allow them to innovate with region-specific profiles, such as tropical fruit blends for beverages and umami enhancers for savory snacks tailored to African palates. Long-standing relationships with multinational food and beverage customers ensure priority access to high-volume contracts in modern trade channels. Certifications like ISO 22000 and Halal compliance further solidify their foothold in regulated markets.

Regional distributors play a pivotal role in bridging gaps for mid-tier manufacturers, capturing a substantial portion of the remaining market share through agile operations. Operating from strategic locations in Morocco, Egypt, and Kenya, these entities offer flexible minimum order quantities that suit smaller production runs common among local brands. Faster payment terms and localized logistics mitigate cash flow challenges prevalent in emerging African economies. They specialize in blending global ingredients with indigenous spices, creating hybrid solutions for ethnic foods like jollof rice seasonings and maamoul flavors.

Local specialists round out the competitive landscape, serving niche segments with customized, rapid-turnaround solutions for small-to-medium enterprises. Firms in South Africa and Nigeria excel in natural flavor extraction from regional botanicals, aligning with clean-label demands amid export regulations. Their intimate knowledge of consumer preferences enables hyper-local innovations, such as low-sodium enhancers for West African stews. Proximity reduces lead times and freight costs, providing a competitive edge in volatile supply chains. Collaborations with agro-cooperatives bolster sourcing of sustainable raw materials like baobab and moringa.

Africa Food Flavor And Enhancer Industry Leaders

-

International Flavors & Fragrances Inc.

-

Givaudan S.A,

-

Symrise AG

-

Kerry Group plc

-

Dsm-Firmenich AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Symrise signed a contract for a 30,000 m² land plot in Giza, Egypt, within an industrial complex developed by Industrial Development Group (IDG). - The move to site e2 in Giza's 6th of October Industrial City supports its growth plans in Africa and the Middle East. - The new site will integrate production and innovation capabilities to enhance collaboration. Symrise Egypt currently operates two production sites, an innovation center, a quality control lab, and sales & marketing offices, serving customers in over 22 markets.

- September 2024: Syensqo introduced Riza, a 100% plant-based range of rosemary-derived antioxidants and natural flavors for food preservation, following its acquisition of a majority stake in Moroccan rosemary extractor Azerys. The rosemary is ethically sourced from Morocco's Atlas Mountains, ensuring a pesticide-free and heavy metal-free supply with reliable endemic species. Riza preserves omega-3 fatty acids like DHA, stabilizes flavors and colors, and extends shelf life. Available in powder and liquid forms with varying carnosic acid contents, including pure rosemary and blends, it is suitable for applications in meat, bakery, instant meals, oils, pet foods, feeds, and beverages.

- June 2024: Symrise Nigeria, subsidiary of global flavors and fragrance leader Symrise, inaugurated upgraded application laboratories in Lagos' Ikeja area. Operating in Nigeria for over 30 years, the company positions the country as a strategic growth pathway for Central, East, and West Africa.

Africa Food Flavor And Enhancer Market Report Scope

The Africa food flavor and enhancer market is segmented by type into food flavors (natural, synthetic and natural identical flavors) and enhancers. Moreoever, by application he market is segmented into bakery, confectionery, processed food, beverage, dairy product and geography (Africa).

Product Type

| Food Flavor |

| Food Enhancer |

Type

| Natural |

| Synthetic |

Appication

| Dairy |

| Bakery |

| Confectionery |

| Savory Snacks |

| Meat |

| Beverages |

| Other Appications |

Form

| Powder |

| Liquid |

| Others |

Country

| South Africa |

| Nigeria |

| Morocco |

| Rest of Africa |

| Product Type | Food Flavor |

| Food Enhancer | |

| Type | Natural |

| Synthetic | |

| Appication | Dairy |

| Bakery | |

| Confectionery | |

| Savory Snacks | |

| Meat | |

| Beverages | |

| Other Appications | |

| Form | Powder |

| Liquid | |

| Others | |

| Country | South Africa |

| Nigeria | |

| Morocco | |

| Rest of Africa |

Key Questions Answered in the Report

What is the projected value of the Africa food flavor and enhancer market in 2031?

The market is forecast to reach USD 802.2 million by 2031, growing at a 4.66% CAGR.

Which segment records the fastest growth within the market?

Food enhancers are advancing at a 5.26% CAGR through 2031 as brands seek umami depth with lower sodium.

Why are natural flavors gaining share despite higher costs?

Export regulations and consumer demand for clean-label products are driving a 6.05% CAGR for natural ingredients, narrowing the gap with synthetic alternatives.

Which country shows the highest growth rate?

Morocco posts the fastest national CAGR at 5.31% through 2031, buoyed by World Bank-backed agri-food reforms and cold-chain upgrades.

What role does encapsulation play in product stability?

Advances in microencapsulation extend shelf life under high heat and humidity, allowing powder flavors to grow at a 5.42% CAGR across the continent.

Page last updated on: