Business Process Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

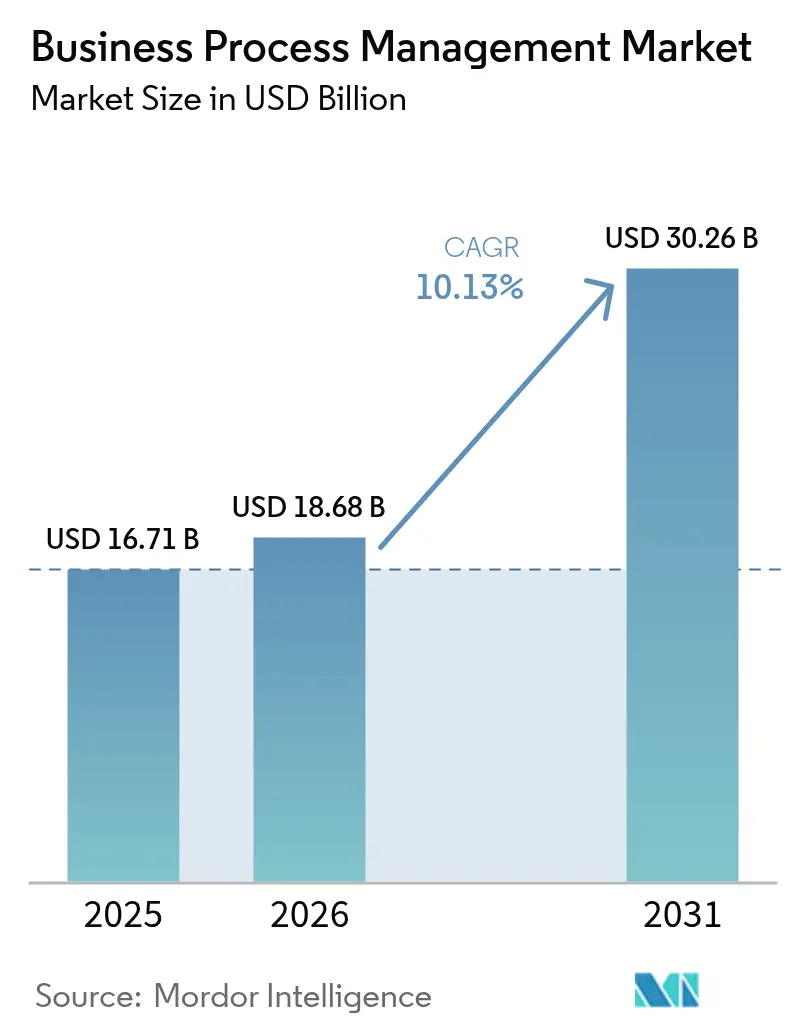

| Market Size (2026) | USD 18.68 Billion |

| Market Size (2031) | USD 30.26 Billion |

| Growth Rate (2026 - 2031) | 10.13% CAGR |

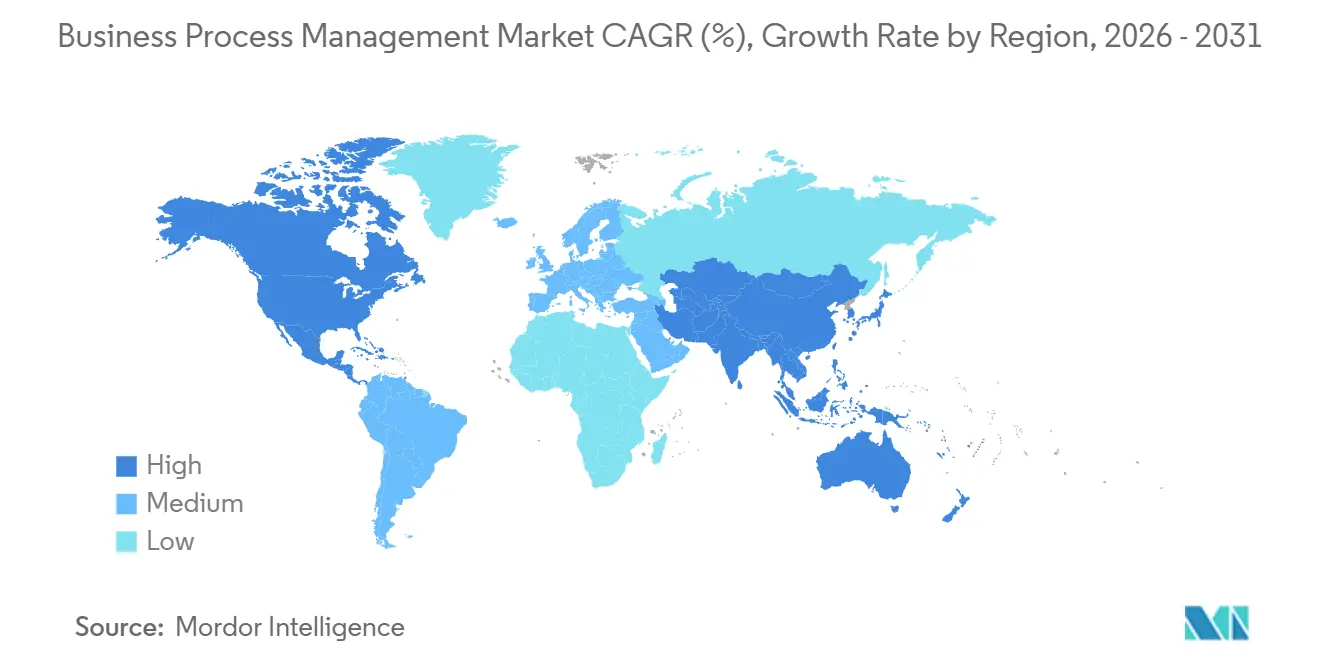

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Business Process Management Market Analysis by Mordor Intelligence

The Business Process Management market size is projected to expand from USD 16.71 billion in 2025 and USD 18.68 billion in 2026 to USD 30.26 billion by 2031, registering a CAGR of 10.1% between 2026 and 2031. Demand is shifting from basic workflow automation toward agentic orchestration, where autonomous AI agents coordinate multi-step processes in cloud-native environments while embedding compliance logic required by banking and healthcare regulators. 81% of IT leaders surveyed in early 2026 identified agent-centric orchestration as essential, and 79% intend to increase automation budgets by at least 20% through 2028, confirming that process intelligence is now a board-level priority. Cloud deployments continued to dominate revenue in 2025, yet hybrid models are expanding rapidly as data-sovereignty laws tighten and enterprises seek elasticity without forfeiting on-premise control. Parallel momentum surrounds process mining because digital-twin simulations surface bottlenecks before they escalate into service-level breaches, a capability that resonates strongly across manufacturing and financial-services workflows.

Key Report Takeaways

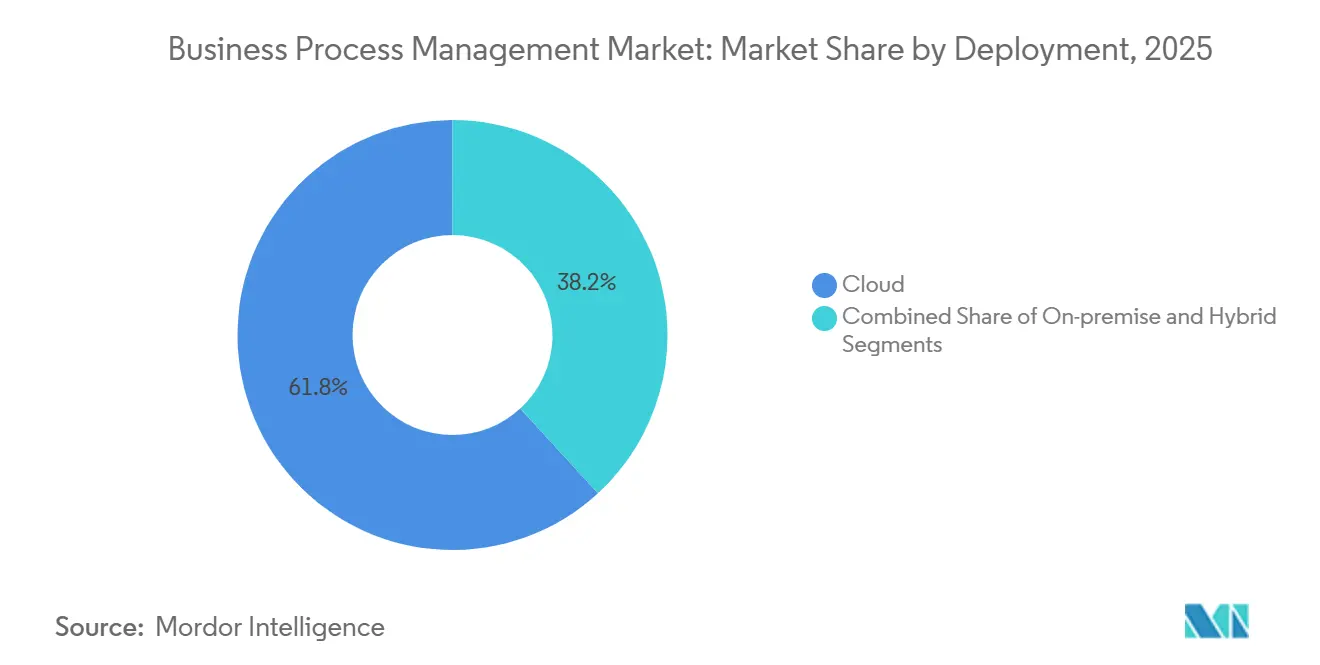

- By deployment, cloud led with 61.83% of Business Process Management market share in 2025, while hybrid configurations are forecast to grow at a 10.2% CAGR through 2031.

- By solution, process automation commanded 27.64% of the Business Process Management market size in 2025 and process mining is advancing at a 10.2% CAGR over 2026–2031.

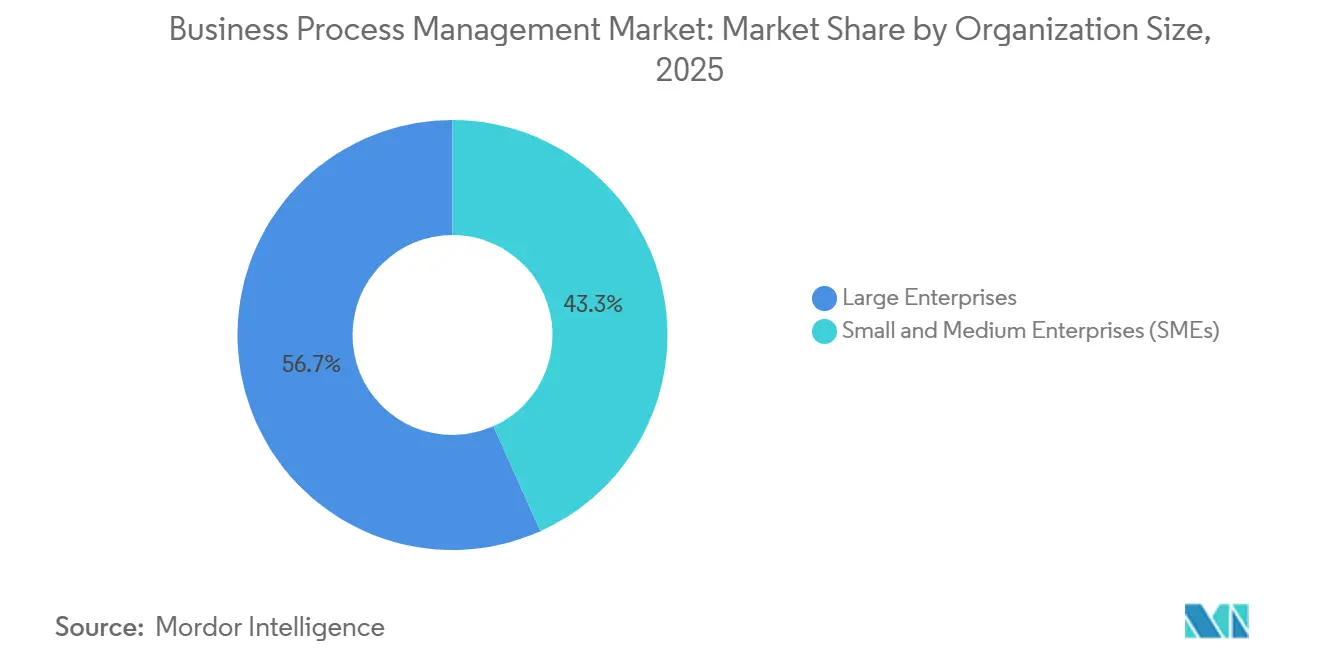

- By organization size, large enterprises held 56.71% spending share in 2025, whereas SMEs represent the fastest growth at a 10.3% CAGR through 2031.

- By end-user, BFSI led with 21.92% share in 2025, yet healthcare and life sciences will expand the fastest at a 10.6% CAGR to 2031.

- By geography, North America retained 34.48% revenue share in 2025, while Asia-Pacific is projected to record the highest 10.8% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Business Process Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Adoption of Low-Code/No-Code BPM Suites | +2.1% | Global, with early gains in North America and Western Europe | Short term (≤ 2 years) |

| Growing Demand For Cloud-Native Process Automation Platforms | +1.8% | Global, APAC core with spill-over to Middle East | Medium term (2-4 years) |

| Expansion Of Hyper-Automation Initiatives Integrating RPA and AI | +2.3% | North America and EU, expanding to APAC manufacturing hubs | Medium term (2-4 years) |

| Compliance-Driven Digital Transformation Across BFSI and Healthcare | +1.6% | EU (DORA, CSRD), North America (HIPAA, SEC), APAC (local data-residency laws) | Long term (≥ 4 years) |

| Emergence Of Process-Mining-Driven Digital Twins For Optimisation | +1.4% | Global, with concentration in manufacturing regions (Germany, China, Japan) | Long term (≥ 4 years) |

| Embedded ESG Reporting Workflows Within BPM Solutions | +0.9% | EU (CSRD mandatory), North America (voluntary SEC disclosure), emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of Low-Code or No-Code BPM Suites

Low-code BPM suites achieved 86% enterprise adoption in 2025 as drag-and-drop modelers shortened build cycles from months to weeks, enabling business teams to automate approvals and document routing without code. The surge democratizes development but raises shadow-IT risks because citizen developers may bypass version control, leaving auditors unable to trace changes. Vendors have responded by embedding role-based access controls and automated policy checks, though enforcement across multi-tenant clouds remains inconsistent. Strategic success therefore hinges on pairing low-code flexibility with centralized process repositories and mandatory peer reviews, repositioning IT from gatekeeper to curator. Organizations that strike this balance report faster release velocity without compromising compliance with SOX and ISO 9001.[1]Kissflow, “Low-Code Statistics,” kissflow.com

Growing Demand for Cloud-Native Process Automation Platforms

Cloud-native architectures that run on Kubernetes and event-driven messaging are displacing monolithic on-premise suites as firms seek horizontal scalability and zero-downtime upgrades. Camunda 8’s Zeebe engine partitions workflow state across distributed clusters that process millions of instances per second, a capability that proved vital during 2025 peak-season surges in e-commerce and logistics. Hybrid patterns are becoming durable rather than transitional, with sensitive credit-decision processes kept on-premise while customer-facing workflows burst into public clouds. Achieving genuine cloud-native status demands asynchronous event streams, infrastructure-as-code pipelines, and blue-green releases, reducing deployment risk and accelerating feature delivery.

Expansion of Hyper-Automation Initiatives Integrating RPA and AI

Hyper-automation now blends process mining, RPA, and machine learning into unified programs. Twenty-five percent of enterprises already feed AI insights into production workflows, and 74% plan to do so by 2027. UiPath’s generative-AI upgrades allow bots to interpret unstructured emails and launch end-to-end processes without rules-based triggers. The shift from deterministic to adaptive automation delivers resilience but complicates auditability, prompting firms to adopt explainable-AI tooling that logs predictions and confidence scores for regulators such as the European Banking Authority under DORA.[2]European Banking Authority, “Digital Operational Resilience Act,” eba.europa.eu Successful rollouts therefore couple AI models with transparent governance to sustain trust.

Compliance-Driven Digital Transformation Across BFSI and Healthcare

Regulators increasingly embed operational-resilience, data-protection, and ESG reporting mandates directly into law, compelling banks and hospitals to codify compliance inside process models. The Digital Operational Resilience Act in the EU and updated HIPAA rules in the United States both require continuous monitoring and auditable workflows. Businee Process platforms automate incident reporting, third-party risk reviews, and consent-management tasks, cutting manual effort and reducing fines. Because new mandates typically allow multi-year transition periods, investment occurs steadily over the long term, sustaining demand beyond cyclic IT budgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Integration Complexity in Heterogeneous IT Landscapes | -1.2% | Global, acute in enterprises with legacy ERP systems (North America, Europe) | Medium term (2-4 years) |

| High Upfront Costs And Uncertain ROI For Enterprise-Wide Roll-Outs | -1.5% | Global, particularly impacting mid-market and SMEs in cost-sensitive regions | Short term (≤ 2 years) |

| Skills Shortage to Govern Citizen-Developer BPM Initiatives | -0.8% | Global, with talent concentration in North America and Western Europe | Medium term (2-4 years) |

| Vendor Lock-In Risks From Proprietary Process-Model Standards | -0.6% | Global, affecting enterprises with multi-vendor IT strategies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Integration Complexity in Heterogeneous IT Landscapes

Enterprises run hundreds of SaaS applications alongside legacy ERP and mainframe systems, forcing teams to wire disparate authentication schemes, data models, and error protocols into a single orchestration layer. BPM platforms promise universal connectors, yet many brownfield systems expose only batch files or SOAP endpoints, so integration engineers resort to custom middleware that increases technical debt. Every minor workflow tweak can ripple across adapters, schemas, and downstream apps, stretching release cycles and raising regression risk. Modernizing core platforms with API-first designs and adopting event-driven architectures reduce coupling, but large estates require sustained investment in integration-platform-as-a-service offerings that centralize monitoring and trim engineering overhead.

High Upfront Costs and Uncertain ROI for Enterprise-Wide Rollouts

Comprehensive BPM programs involve six-figure software licenses, multi-year consulting engagements, and resilient cloud or on-premise clusters, pushing total cost of ownership well into the millions before live value accrues. Intangible returns such as reduced compliance risk are harder to quantify than direct cost savings, complicating budget approvals. Failed change-management efforts often erode projected efficiency gains when staff circumvent new workflows to preserve informal routines. Best-practice adopters stage deployments, beginning with high-volume, low-complexity tasks that deliver measurable savings inside 12 months, then recycle gains into more complex automations while pairing technical workstreams with stakeholder engagement that clarifies how automation augments rather than replaces human roles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Hybrid Architectures Balance Sovereignty and Elasticity

Cloud maintained 61.83% Business Process Management market share in 2025, but hybrid configurations are climbing a 10.2% CAGR through 2031 as data-residency rules proliferate. Banks run credit-scoring engines on private clouds to satisfy operational-resilience principles, while shifting customer onboarding to public clouds that offer global scalability.[3]Bank for International Settlements, “Principles for Operational Resilience,” bis.org Active-active replication across regions now enables seamless failover, a capability validated during the 2025 US-East-1 outage when hybrid customers rerouted workflows to on-premise clusters within minutes.

Hybrid patterns have become an endpoint, not a bridge. Containerized process engines packaged via Kubernetes allow identical deployment across environments, eliminating configuration drift. Enterprises also leverage service meshes and zero-trust security to ensure consistent policy enforcement. As a result, the Business Process Management market size attached to hybrid deployments is forecast to expand steadily, reflecting long-term coexistence of on-premise and multicloud estates rather than eventual full public-cloud migration.

By Solution: Process Mining Delivers Data-Driven Differentiation

Process automation held 27.64% revenue in 2025, yet process mining and analytics are growing at 10.2% CAGR as firms prioritize discovery and optimization before scaling execution. Platforms like Celonis reconstruct actual flows from ERP and CRM logs, exposing rework loops and violations, then simulate fixes inside digital twins to validate savings prior to code changes.

Process improvement, content management, case management, business rules, and integration suites remain essential but are increasingly converging within unified stacks. Vendors embed document processing and rules engines within broader platforms to simplify procurement. Consequently, organisations view process mining as the strategic front-end while automation handles fulfilment, creating a feedback loop that continuously tunes processes. This coupling underpins sustained demand, ensuring that the Business Process Management market continues to prioritize insight before execution.

By Organization Size: Cloud Democratizes BPM for SMEs

Large enterprises captured 56.71% of spending in 2025, supported by centers of excellence that standardize process governance. However, SMEs are registering a 10.3% CAGR as SaaS pricing aligns cost with usage and low-code studios remove the need for specialist integration teams. Pre-built connectors to QuickBooks and Shopify eliminate middleware overhead, enabling rapid deployment of procurement and customer-support workflows.

SMEs still face governance gaps, so leading vendors incorporate automated security scans and mandatory backups into subscription tiers. This risk-mitigated packaging accelerates adoption without proportional headcount growth, broadening the Business Process Management market size among firms previously priced out of enterprise-grade platforms. Continued SME uptake is expected to add diversification and volume growth for vendors through 2031.

By End-User Industry: Healthcare Gains Momentum on Patient-Journey Orchestration

BFSI led with 21.92% spend in 2025, driven by DORA and anti-money-laundering mandates that demand auditable, resilient workflows. Healthcare and life sciences, however, are forecast to grow at 10.6% CAGR as hospitals orchestrate appointments, diagnostics, and billing in real time under renewed HIPAA guidance that stresses interoperability and patient consent tracking.

Government agencies digitize citizen services under Digital India grants, retail integrates e-commerce, WMS, and last-mile logistics for same-day delivery, and manufacturing ties IoT sensors into predictive-maintenance workflows. These diverse use cases reinforce that the Business Process Management industry offers horizontal applicability across sectors that run repeatable, multi-step operations.

Geography Analysis

North America accounted for 34.48% Business Process Management market share in 2025, benefiting from deep venture capital funding and early enterprise adoption of hyper-automation suites. United States regulations such as SOX and HIPAA have long required granular audit trails, making BPM a compliance staple. Canada and Mexico contribute incremental growth, with Mexican manufacturers using BPM to streamline nearshore operations amid shifting supply-chain geographies.

Europe remains a significant revenue contributor, propelled by the Digital Operational Resilience Act and the Corporate Sustainability Reporting Directive, which require companies to embed ICT risk governance and ESG reporting directly into business processes. Germany, France, and the United Kingdom spearhead industrial and financial-services use cases, while Italy and Spain channel EU recovery funds into public-sector digitization programs that rely on BPM to accelerate citizen-service delivery.

Asia-Pacific is the fastest-growing region at a 10.8% CAGR, anchored by China’s 14th Five-Year Plan investments in smart manufacturing, India’s Digital India subsidies for cloud BPM in government, and Japan’s Society 5.0 push to offset labor shortages with automated services. South Korea and Southeast Asian economies deploy cloud-first BPM stacks that leapfrog legacy systems, while Middle East markets invest in process orchestration to support smart-city projects. South American and African uptake is smaller but rising as banks, telecom operators, and public utilities deploy BPM to improve operational resilience and customer experience.

Competitive Landscape

The Business Process Management market is moderately concentrated. Incumbents such as IBM, SAP Signavio, Pegasystems, and Oracle retain large installed bases through decades-long ERP and middleware relationships, yet face disruption from process-mining leaders like Celonis and open-source orchestrators such as Camunda that decouple process logic from proprietary run-times. Vendors are expanding horizontally by integrating RPA, AI, and low-code capabilities into single suites. IBM’s Cloud Pak for Business Automation couples workflow orchestration with content management on Kubernetes, offering hybrid portability. SAP Signavio embeds process intelligence inside S/4HANA, enabling customers to optimize core ERP flows without third-party tools.

Horizontal platforms compete with domain-specific solutions. ServiceNow, Appian, and Pegasystems emphasize low-code design and pre-built connectors across IT, HR, and customer-service domains. UiPath evolved from RPA to full-stack orchestration after acquiring process-mining assets, while Microsoft integrated Copilot into Power Automate to translate natural-language prompts into executable workflows. White-space continues to open in micro-verticals such as clinical-trial orchestration and energy trading, where startups build agentic BPM that self-optimizes resource allocation.

Pricing pressures intensify as open-source alternatives lower entry costs. Camunda offers a community edition that eliminates license fees, redirecting budgets toward implementation support. Bonitasoft and other open-source providers follow similar models, broadening vendor choice and preventing lock-in. Partnerships between BPM vendors and hyperscalers also influence strategy, with AWS, Microsoft Azure, and Google Cloud offering marketplace integrations that bundle infrastructure credits with process-automation deployments.

Business Process Management Industry Leaders

IBM Corporation

Pegasystems Inc.

Appian Corporation

Oracle Corporation

Software AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Camunda released its 2026 Process Orchestration Report, showing 81% of IT leaders deem agentic orchestration essential and 79% intend to lift automation budgets by at least 20% over two years.

- December 2025: UiPath reported annual recurring revenue of USD 1.57 billion, highlighting uptake of its AI-powered automation suite that unifies RPA, process mining, and document understanding.

- November 2025: ServiceNow embedded generative AI into the Now Platform, enabling natural-language process design and intelligent task routing for business users.

- October 2025: Microsoft added Copilot-driven workflow generation to Power Automate, letting users describe processes in plain language and receive runnable templates.

Global Business Process Management Market Report Scope

Business process management (BPM) is a discipline that involves a combination of process modeling, automation, execution, control, measurement, and optimization of business process flows to align with enterprise goals, spanning systems, employees, customers, and business partners.

The Business Process Management Market Report is Segmented by Deployment (Cloud, On-Premise, and Hybrid), Solution (Process Improvement, Process Automation, Content and Document Management, Case Management, Business Rules Management, Integration and Optimisation, and Process Mining and Analytics), Organization Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (BFSI, Government and Public Sector, Healthcare and Life Sciences, IT and Telecommunication, Retail and Consumer Goods, Manufacturing and Industrial, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-premise |

| Hybrid |

| Process Improvement |

| Process Automation |

| Content and Document Management |

| Case Management |

| Business Rules Management |

| Integration and Optimisation |

| Process Mining And Analytics |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| Government and Public Sector |

| Healthcare and Life Sciences |

| IT and Telecommunication |

| Retail and Consumer Goods |

| Manufacturing and Industrial |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Deployment | Cloud | |

| On-premise | ||

| Hybrid | ||

| By Solution | Process Improvement | |

| Process Automation | ||

| Content and Document Management | ||

| Case Management | ||

| Business Rules Management | ||

| Integration and Optimisation | ||

| Process Mining And Analytics | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By End-user Industry | BFSI | |

| Government and Public Sector | ||

| Healthcare and Life Sciences | ||

| IT and Telecommunication | ||

| Retail and Consumer Goods | ||

| Manufacturing and Industrial | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Business Process Management market by 2031?

The market is forecast to reach USD 30.26 billion by 2031, expanding at a 10.1% CAGR from 2026.

Which deployment model will grow the fastest through 2031?

Hybrid architectures are expected to post the highest 10.2% CAGR as firms balance data sovereignty with cloud elasticity.

Why is healthcare adopting BPM more rapidly than other industries?

Updated HIPAA interoperability rules and patient-journey orchestration needs push healthcare BPM spending at a 10.6% CAGR.

How are SMEs overcoming historical BPM cost barriers?

SaaS pricing tied to transaction volumes and low-code studios with pre-built connectors let SMEs deploy workflows without large IT teams.

Which region shows the highest growth potential?

Asia-Pacific leads with a projected 10.8% CAGR thanks to government digitalization programs and smart-manufacturing investments.

Page last updated on: