Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

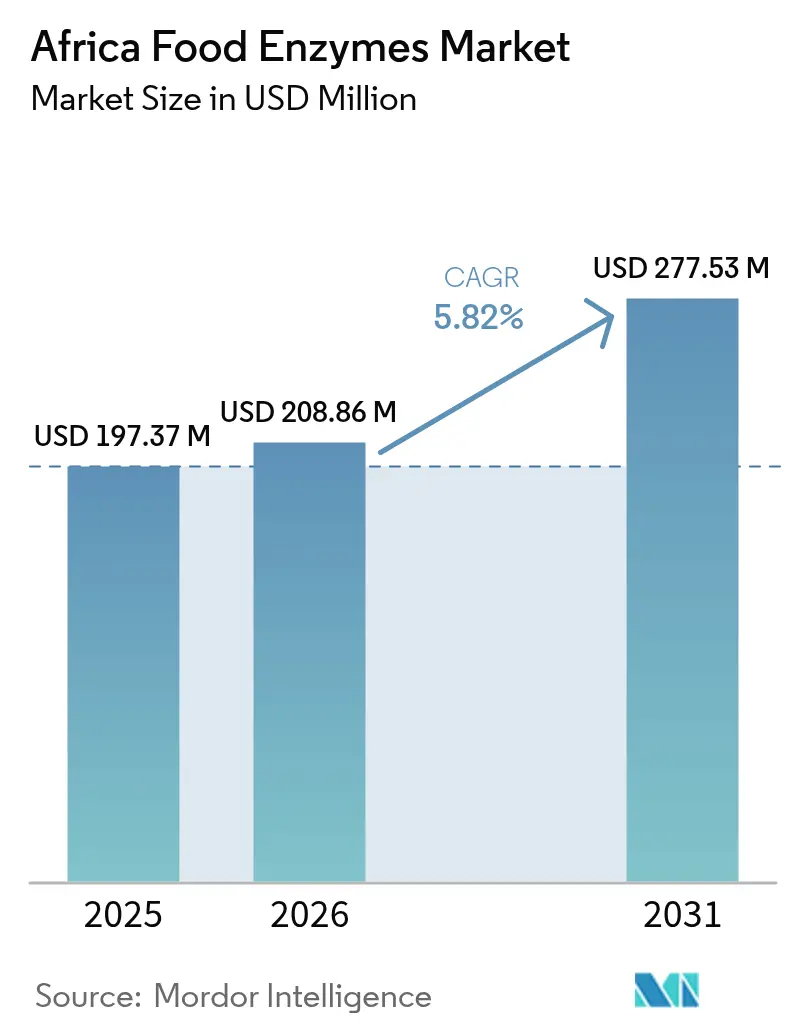

| Base Year Market Size (2025) | USD 197.37 Million |

| Market Size (2026) | USD 208.86 Million |

| Market Size (2031) | USD 277.53 Million |

| Growth Rate (2026 - 2031) | 5.82% CAGR |

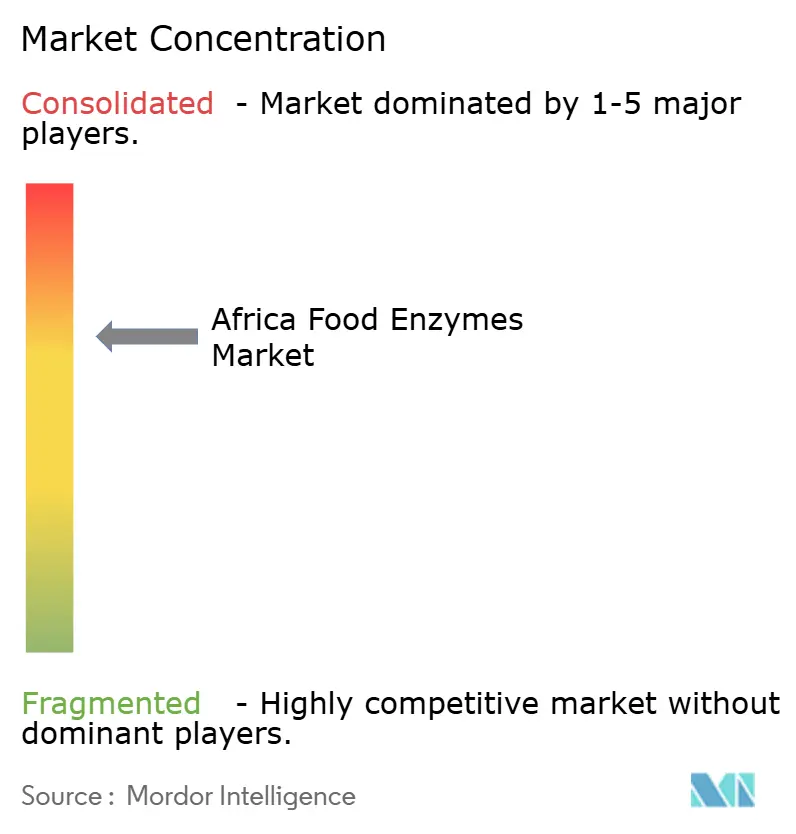

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Food Enzymes Market Analysis by Mordor Intelligence

The Africa food enzymes market size is expected to grow from USD 197.37 million in 2025 to USD 208.86 million in 2026 and is forecast to reach USD 277.53 million by 2031 at 5.82% CAGR over 2026-2031. Four key drivers fuel this growth: urban migration broadening the processed-food landscape, clean-label regulations replacing synthetic additives with biocatalysts, regional expansions in dairy capacity, and investments in modular fermentation reducing import dependencies. While multinational suppliers roll out thermostable amylases, lipases, and proteases suited for tropical supply chains, local institutes experiment with solid-state fermentation, utilizing cassava peel and rice bran feedstocks. Yet, despite this momentum, challenges arise: fragmented additive regulations, currency fluctuations, and cold-chain deficiencies limit the immediate addressable volume. As a result, suppliers pivot towards high-margin niches in bakery, dairy, and beverages, where premium pricing is more palatable. The competitive landscape is marked by localized formulations, mergers to consolidate intellectual property, and strategic acquisitions of specialty portfolios, including lactase for lactose-free dairy and pectinases for enhanced juice clarity.

Key Report Takeaways

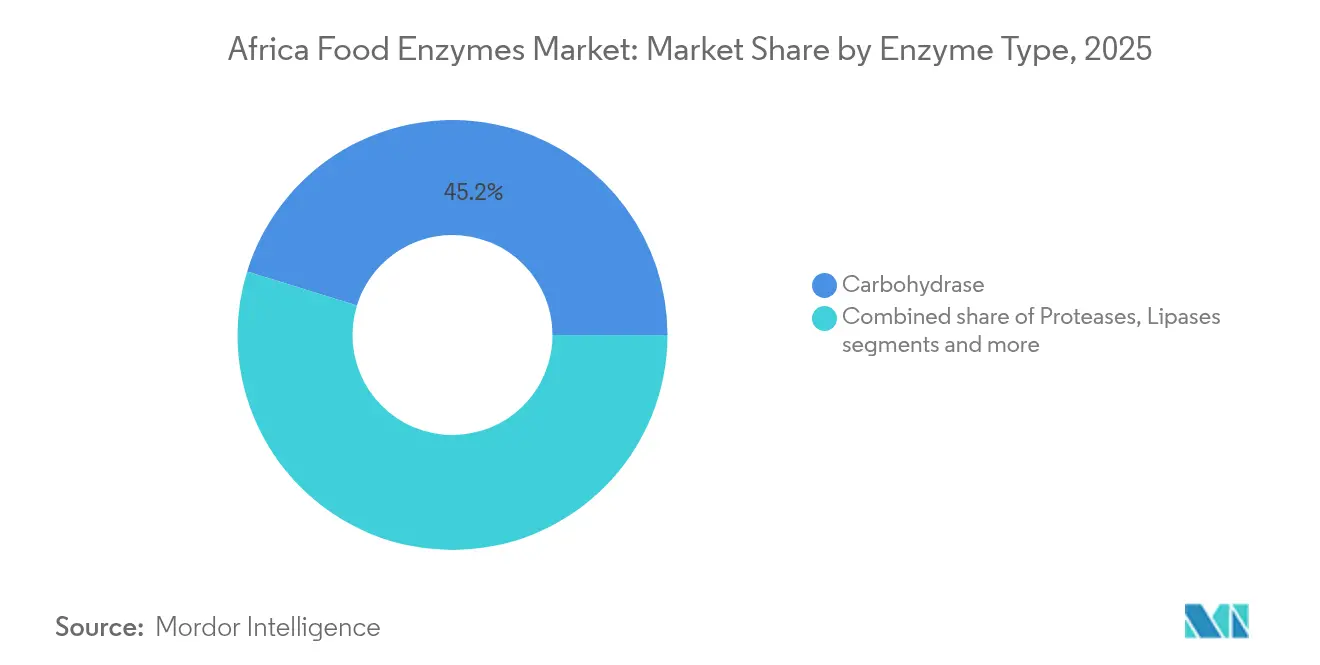

- By enzyme type, carbohydrases led with 45.22% Africa food enzymes market share in 2025; lipases are projected to advance at a 10.49% CAGR through 2031.

- By source, microbial preparations captured 67.03% of the Africa food enzymes market size in 2025, while plant-derived alternatives recorded the highest forecast CAGR at 9.74%.

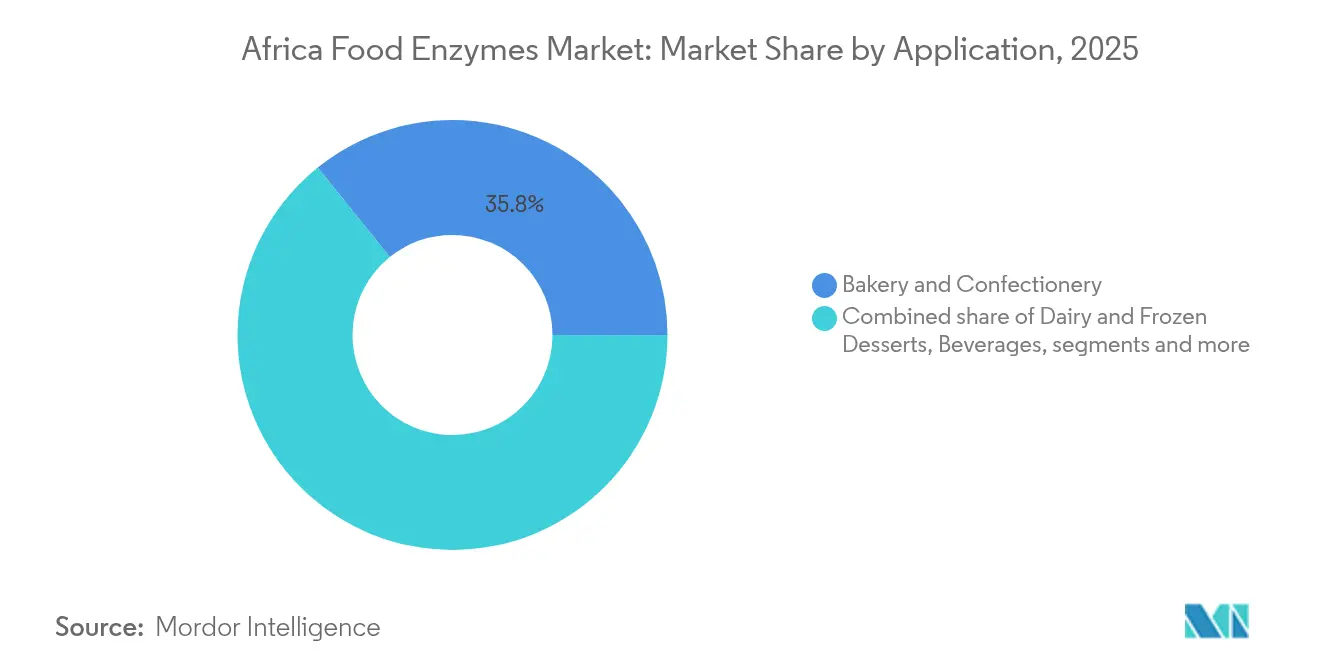

- By application, bakery and confectionery commanded 35.78% revenue share in 2025; dairy and frozen desserts are forecast to expand at a 10.08% CAGR to 2031.

- By geography, South Africa accounted for 48.17% of the Africa food enzymes market size in 2025, whereas Nigeria registers the fastest CAGR at 8.41% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Food Enzymes Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Processed-food boom in urban Africa | +1.2% | Nigeria, Kenya, Egypt, South Africa (Lagos, Nairobi, Cairo, Johannesburg) | Medium term (2–4 years) |

| Clean-label and natural-ingredient demand | +0.9% | South Africa, Egypt, Morocco; spillover to Nigeria, Ghana | Long term (≥ 4 years) |

| Expansion of regional dairy capacity | +0.8% | South Africa, Kenya, Egypt; Nigeria emerging | Medium term (2–4 years) |

| Cost-efficiency versus chemical additives | +0.7% | Pan-African bakery, beverage, starch-processing sectors | Short term (≤ 2 years) |

| Cassava- and sorghum-based beverage innovation | +0.6% | Nigeria, Ghana, Uganda, Tanzania | Long term (≥ 4 years) |

| Local modular fermentation build-outs | +0.5% | South Africa, Nigeria, Kenya, Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Processed-food boom in urban Africa

City dwellers in Africa are increasingly favoring packaged goods, shifting from traditional staples to items like bread, biscuits, juices, and dairy. From 2020 to 2024, as incomes rose and supermarket chains expanded, per-capita consumption of industrial bakery goods surged in Lagos and Abuja. In response to the inconsistent falling numbers in flours, industrial bakers are now turning to thermostable amylases and xylanases for smoother dough handling. The African Development Bank's Special Agro-Industrial Processing Zones program, has spurred factory expansions, adding hundreds of ovens, juice extractors, and cheese vats[1]Source: FAO/WHO, “JECFA Evaluations 2024,” fao.org. Enzyme vendors are adapting by launching pilot bakeries in Lagos and Nairobi, mimicking tropical humidity for on-site optimization, a move away from less effective European protocols suited for cooler climates. These trends signal a robust growth in bakery-grade carbohydrase volume projected through 2030.

Clean-label and natural-ingredient demand

In 2025, Nigeria's regulatory body imposed a ban on azodicarbonamide and designated enzymes as the favored processing aids, especially when used in baking. Following suit, South Africa exempted deactivated enzymes from being labeled as additives. This move expanded the compliance flexibility for both dough conditioners and juice-clarification agents. In 2024, JECFA reaffirmed the acceptable daily intake levels for various carbohydrases and proteases, streamlining the import registration process[2]Source: FAO/WHO, “JECFA Evaluations 2024,” fao.org. Export-driven processors in Morocco and Egypt, attuned to EU Regulation 1169/2011, have transitioned to using pectinases, moving away from chemical fining agents in juice production. Collectively, these regulatory shifts bolster the demand for microbial and plant enzymes, championing clean-label narratives devoid of E-numbers.

Expansion of regional dairy capacity

Between 2022 and 2024, processors in South Africa, Kenya, and Egypt ramped up dairy throughput by installing UHT lines and expanding cheese vat sizes to meet growing consumer demand and improve operational efficiency. In Kenya, cooperatives are now using lipase supplementation to cut cheddar ripening time from 90 days to just 55, significantly reducing inventory costs and freeing up stainless-steel capacity for additional production. Lactase is being harnessed to produce lactose-free milk and yogurt, effectively addressing the widespread lactase deficiency among African adults. This innovation not only meets consumer health needs but also justifies higher retail prices, creating a premium product segment. In 2024, Nigeria’s Anchor Borrowers’ Programme backed 12 new dairy clusters, each delving into transglutaminase applications to combat yogurt syneresis, a common issue that affects product quality and shelf life. Such investments are set to expand the dairy-enzyme landscape through 2030, enabling the industry to cater to evolving consumer preferences and

Cost-efficiency vs. chemical additives

West African bakeries demonstrate that enzyme-led dough conditioners can reduce the cost per loaf, mainly by substituting potassium bromate and ascorbic acid blends, which are traditionally used for dough strengthening and shelf-life improvement. In the juice sector, pectinase concentrates are replacing bentonite, a common clarifying agent, resulting in higher yields from mango and passion-fruit pulps by breaking down pectin more efficiently. Nigeria’s FIIRO has experimented with Aspergillus fermentation on cassava peel, hinting at a potential 40% reduction in import costs once scaled, as this process converts agricultural waste into valuable enzymes[3]Source: FIIRO, “Enzyme Technology Division,” fiiro.gov.ng. While the pilot output remains modest, the economic benefits underscore enzymes as a cost-effective solution for extending shelf life and ensuring process consistency across various applications.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented food-additive regulations | -0.6% | Nigeria, South Africa, Egypt, Kenya, Morocco | Medium term (2–4 years) |

| Cold-chain and logistics gaps | -0.5% | Sub-Saharan Africa rural distribution | Short term (≤ 2 years) |

| Tariff and FX volatility on enzyme imports | -0.4% | Nigeria, Egypt, Ghana | Short term (≤ 2 years) |

| Scarcity of enzymology talent | -0.3% | Continent-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented food-additive regulations

Nigeria's National Biotechnology Management Agency mandates a 270-day pre-import window and requires GMO labeling. In contrast, South Africa has its own thresholds, and Egypt maintains distinct purity dossiers to regulate enzyme imports. According to UNCTAD, these non-tariff measures inflate intra-African enzyme costs, creating additional financial and logistical burdens for businesses operating in the region. Suppliers typically register only in South Africa, Nigeria, or Egypt, as these are the larger markets, leaving smaller markets underserved and reliant on gray-market channels. These channels often bypass regulatory frameworks, leading to compromised quality oversight and potential risks for end-users. Without a unified enzyme monograph adopted by regional blocs, the duplication in compliance processes will continue to hinder market growth and integration across Africa.

Cold-chain and logistics gaps

Less than 30% of African processors have reliable cold storage, which significantly impacts the supply chain for temperature-sensitive products like enzymes. Road freight, averaging just 15 km/h, causes enzyme transit from port to factory to take over a week, further complicating logistics. When ambient temperatures exceed 35 °C, liquid enzyme concentrates degrade by 20–30% within two weeks, leading to quality issues. This degradation forces bakers to over-dose enzymes to maintain product quality, effectively erasing any potential cost savings. While dry-powder formats are more stable and can withstand such conditions, they come with a 30–40% price premium and require specialized blending equipment that many bakeries lack, adding another layer of complexity. Infrastructure upgrades, such as RCL Foods’ expanded Vector Logistics network, are still rare and insufficient to address the broader challenges. Until at least half of the processing nodes are equipped with refrigeration facilities, enzyme adoption will remain limited to urban centers where infrastructure is more developed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enzyme Type: Carbohydrases Hold Sway, Lipases Accelerate

In 2025, carbohydrases commanded a dominant 45.22% share of Africa's food enzymes market. This surge was largely propelled by amylases, which play a pivotal role in hydrolyzing damaged starch. These enzymes are integral, preventing staling in over 80% of industrial bread recipes. Notably, thermostable variants sourced from Bacillus licheniformis can withstand oven peaks of 90–95 °C. This resilience is crucial, given the high-heat tunnel ovens prevalent in bakeries across Johannesburg and Lagos. Meanwhile, cellulases and xylanases play a crucial role in breaking down non-starch polysaccharides. This process ensures a balanced water uptake in composite flours, especially those rich in sorghum and millet. In juice production, pectinases take center stage, boosting yields by an impressive 8–10% from mango and passion fruit pulps. Additionally, xylanases are making waves in sorghum brewing, where they effectively reduce the viscosity of the wort.

Looking ahead, lipases are projected to grow at a robust 10.49% CAGR through 2031. These enzymes are pivotal, catalyzing the release of flavors in cheese and modifying palm-kernel oil for use in ice cream. In a notable industry shift, Kenyan dairies have leveraged microbial lipases to slash cheddar maturation time from 90 days down to just 55. This halving not only accelerates production but also significantly reduces inventory overheads. Furthermore, in the realm of frozen desserts, lipase-interesterified fats are enhancing scoopability. This is particularly beneficial given the warmer freezer set points commonly found in African households. Collectively, these dynamics not only anchor carbohydrases as key revenue drivers but also spotlight lipases as the premium-growth narrative, propelling the overall expansion of Africa's food enzymes market.

By Source: Microbial Scale, Plant-Based Momentum

In 2025, microbial preparations dominated the sales landscape, capturing a significant 67.03% share. Their appeal lies in short fermentation cycles, GRAS status, and consistent batch quality. Suppliers can confidently guarantee the activity of amylases and pectinases, produced by Aspergillus niger and Bacillus subtilis strains in submerged tanks, even after transit through tropical regions. The 10,000-ton Sadat City plant of DSM-Firmenich, equipped with such fermentation capabilities, is strategically positioned to reduce lead times for deliveries into North Africa.

Plant-derived enzymes, with papain and bromelain leading the charge, are witnessing a robust expansion at a 9.74% CAGR. In Africa, growers are tapping into papaya and pineapple waste streams as valuable feedstock. Meanwhile, processors are making strategic moves, leveraging non-GMO certifications to secure a spot on organic shelves across Europe. However, challenges remain: while papain's stability falters above 70°C, its premium market positioning helps mitigate these limitations. On the other hand, recombinant and animal-based enzymes occupy a niche segment, constrained by regulatory scrutiny and religious dietary considerations. Yet, with innovation pipelines buzzing, there's a clear indication of a gradual diversification in source variety within Africa's food enzymes market.

By Application: Bakery Dominates, Dairy Surges

In 2025, bakery and confectionery claimed a 35.78% share, reflecting urban Africa's bread-centric diets. To counter low-protein wheat and inconsistent milling quality, every industrial loaf now incorporates at least one amylase or xylanase. These enzymes improve dough handling, enhance crumb structure, and ensure consistent product quality. Enzyme blends like Kerry’s Biobake Fresh Rich extend shelf life by 30%, a crucial advantage for retail models dependent on prolonged ambient display, especially in regions with limited cold chain infrastructure.

From 2025 to 2031, dairy and frozen desserts are set to expand at a robust 10.08% CAGR. While lipases elevate cheese flavor by breaking down milk fats into flavorful compounds, lactase introduces premium lactose-free options for lactose-intolerant adults, a growing consumer segment in Africa. Transglutaminase bolsters yogurt firmness, allowing Nigerian processors to tackle syneresis without resorting to stabilizer E-numbers, thereby meeting consumer demand for clean-label products. Although the meat, beverage, and fruit-processing sectors contribute smaller streams, they collectively enhance the functional breadth of Africa's food enzymes market by enabling innovations such as tenderized meat products, improved beverage clarity, and extended fruit shelf life.

Geography Analysis

In 2025, South Africa accounted for 48.17% of the region's revenue, bolstered by advanced cold chains and major players like bakery giants and dairy leaders Clover and RCL Foods. These companies are now incorporating lipases and lactase into their premium product lines to enhance functionality and cater to evolving consumer preferences. Retail giant Woolworths has committed to transitioning all its private-label bakery products to clean-label status by 2026, driving up the demand for enzymes as clean-label trends gain momentum. Additionally, the South African Bureau of Standards has provided regulatory clarity by exempting denatured enzymes from additive labeling, reducing compliance complexities and making adoption even more appealing for manufacturers.

Nigeria, boasting an 8.41% CAGR, benefits from processing zones backed by the AfDB and a vast consumer base of 200 million, which creates a robust demand for enzyme applications across industries. In Cross River’s new SAPZ, cassava starch plants will utilize amyloglucosidase for syrup production, supporting the growing demand for sweeteners in food and beverage sectors. Meanwhile, urban bakeries are replacing bromate with amylase blends, responding to tightened clean-label regulations from NAFDAC, which aim to improve food safety and align with global standards. Although FX volatility and 90-day LC cycles pose challenges for smaller importers, localized fermentation initiatives, such as pilot projects for enzyme production, suggest a promising future for supply stability and reduced dependency on imports.

Egypt, Morocco, and other African nations account for the remaining market share. DSM-Firmenich’s hub in Sadat City is providing pectinases and amylases to juice and bakery facilities across Egypt, supporting the growing demand for high-quality processed foods. Meanwhile, Morocco's focus on exports is driving enzyme adoption to align with EU labeling standards, ensuring compliance and competitiveness in international markets. In East Africa, Kenya's dairy sector is ramping up its use of lipases for faster ripening, enabling producers to meet increasing consumer demand for dairy products. However, cold-chain facilities outside Nairobi are yet to meet the desired benchmarks, which limits the scalability of enzyme applications in the region. While the harmonized EAC labeling introduced in 2024 is a step forward in standardizing regulations, inconsistent enforcement at ports is causing delays in clearing enzyme shipments, impacting supply chain efficiency.

Regulatory Landscape

Food-enzyme use in Africa is handled through a mix of country-specific additive and processing-aid rules, with Codex Alimentarius acting as a key reference point for safety and use conditions (including alignment work linked to the General Standard for Food Additives). In March 2025, the African Union adopted the statute establishing the African Food Safety Agency (AfFSA), which marks a push toward more harmonized food-safety policy and creates an intersecting agenda for enzyme registration and oversight.

Even with this harmonization direction, compliance pathways remain fragmented across major import markets. National bodies (such as Nigeria regulators and standards authorities like Kenya Bureau of Standards) apply different dossier, labeling, and pre-import or registration practices. Regional frameworks, including SADC food-safety regulatory guidelines, and ongoing Codex Africa (CCAFRICA) engagement, including workstreams tied to the Codex Strategic Plan 2026-2031 and committee deliberations relevant to additives, provide anchors for convergence. However, near-term market access still depends on meeting each country’s documentation and quality-system expectations (GMP/HACCP) for enzyme preparations.

Competitive Landscape

In the competitive landscape of the African food enzymes market, key players include Novozymes A/S, DSM-Firmenich, Kerry Group PLC, BASF SE, and IFF. In 2024, Novonesis emerged as a frontrunner after its merger with Chr. Hansen and, in 2025, its acquisition of DSM-Firmenich’s feed-enzyme unit for a hefty EUR 1.5 billion. This strategic move has significantly strengthened Novonesis's position in the animal enzymes segment. However, its concentrated focus on animal enzymes has created a noticeable gap in the specialty food enzyme segments, presenting opportunities for competitors to address unmet needs.

Following closely is Kerry Group, bolstered by its strategic EUR 150 million acquisition of lactase and the establishment of a new plant in Rwanda. This plant specializes in formulating bakery and dairy enzymes, customized to the region's raw materials, which positions Kerry Group to effectively cater to local market demands and expand its footprint in Africa. Completing the top tier are DSM-Firmenich, IFF, and AB Enzymes, all of whom are channeling investments into African application labs and forging partnerships with local millers and dairies. These initiatives aim to enhance product localization and strengthen relationships with key stakeholders in the value chain.

Mid-tier players like Sabinsa South Africa, catering to halal markets with plant protease blends, AEB Africa, supplying pectinases to juice SMEs, and Lesaffre with its expansive baking center network, are making their mark by addressing niche market requirements. Common strategies among these players emphasize thermostable variants, granular formats adept at withstanding tropical logistics, and innovative digital dosing systems to address the challenges of variable flour qualities. While modular fermentation pilots at FIIRO and the CSIR hint at a future of import substitution, they remain in the experimental phase and not yet commercially viable. These pilots, however, underscore the potential for local production capabilities to reduce dependency on imports in the long term.

Africa Food Enzymes Industry Leaders

Novozymes A/S

DSM-Firmenich

International Flavors and Fragrance Inc. (IFF)

Kerry Group PLC

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Industrial scale-up in enzyme-intensive downstream categories is broadening the addressable market for processing aids across bakery, beverages, and dairy. In Nigeria, demand signals are coming from new agro-processing assets, including Olam Agri’s USD 50 million soybean crushing and feed-milling complex in Ilorin (opened in April 2026, with 250,000 to 350,000 metric tonnes annual processing capacity), and the commissioning of a fruit concentrate plant in Makurdi in June 2026. These facilities increase the need for consistent process control, yield improvement, and raw-material variability management, which supports adoption of carbohydrases and pectinases across adjacent food and beverage value chains.

A second opportunity is the localization of technical support and formulation to account for Africa-specific constraints such as cold-chain gaps and variable flour, fruit, and milk quality. Steps including dsm-firmenich establishing an East Africa office and application center in Nairobi create a basis for on-site trials, training, and reformulation into more temperature-tolerant formats. This helps processors move from intermittent imports and overdosing toward calibrated dosing and more stable performance. Regulatory convergence efforts anchored by the AU’s AfFSA statute and Codex engagement also create room for suppliers to standardize documentation and provide multi-country compliance support, particularly for SMEs in secondary markets that are currently underserved by formal registrations.

Recent Industry Developments

- February 2026: dsm-firmenich opened a new office and application center in Nairobi, Kenya, to serve East Africa (including Kenya, Tanzania, Uganda, Ethiopia, and Rwanda). The expanded local footprint strengthens technical service for bakery, beverage, and dairy processors that need on-site troubleshooting and localized enzyme formulations suited to tropical logistics.

- February 2025: Novonesis agreed to acquire dsm-firmenich’s share of the Feed Enzyme Alliance for EUR 1.5 billion in an all-cash transaction. The deal consolidated capabilities in industrial biosolutions and reshaped competitive positioning and capital allocation across enzyme portfolios that also supply adjacent food and fermentation value chains.

- September 2024: dsm-firmenich inaugurated an animal nutrition and health manufacturing plant in Sadat City, Egypt, positioned to serve customers across Egypt and wider regional corridors. The facility reinforced North Africa as a production and distribution hub, supporting shorter lead times and improved supply reliability for enzyme-based solutions moving through the region.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Africa food enzymes market covers enzymes sold for use in food and beverage processing across African countries, measured as the value of products supplied to food manufacturers and processors within the year.

Scope exclusions: It excludes enzymes used mainly for animal feed, industrial biofuels, pharmaceuticals, and non-food technical applications.

Segmentation Overview

- By Enzyme Type

- Carbohydrases

- Amylase

- Cellulase

- Pectinase

- Xylanase

- Proteases

- Lipases

- Other Specialty Enzymes

- Carbohydrases

- By Source

- Microbial

- Plant

- Animal

- Recombinant / GMO

- By Application

- Bakery and Confectionery

- Bread

- Cakes and Pastries

- Cookies and Biscuits

- Dairy and Frozen Desserts

- Meat, Poultry and Seafood Processing

- Beverages

- Juices and Nectars

- Brewing and Malting

- Fruit and Vegetable Processing

- Functional and Specialty Foods

- Bakery and Confectionery

- By Geography

- South Africa

- Nigeria

- Egypt

- Morocco

- Rest of Africa

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used first to set the market boundaries and to build a common data backbone for food processing activity across Africa. We referenced public sources such as FAOSTAT and other FAO publications, UN Comtrade trade statistics, World Bank macro indicators, and country statistics portals for key food categories that typically use enzymes.

On top of that, we reviewed manufacturer and distributor websites, investor presentations, and public annual reports to understand product positioning and where demand is likely to be concentrated. In a few cases, patent databases and an import export shipment-level database were used to sanity check the direction of enzyme innovation and the movement of enzyme preparations into major ports. The desk sources listed here are illustrative, and many other public documents and datasets were also consulted to collect, cross-check, and clarify data points.

Primary Interviews and Surveys

Primary work was used to validate the demand signals behind enzyme use in bakery, dairy, beverages, and processed foods, and to pressure-test assumptions on pricing, formulation shifts, and supply routes. We spoke with a mix of ingredient suppliers, local distributors, and food processors across key African markets so the gaps from public datasets could be filled, then filtered using consistent rules.

For a regional market like this, the feedback covered major demand hubs as well as smaller import-led markets. When an interview view and a desk indicator did not align, follow-up questions were used to identify the reason, for example channel differences or timing of shipments.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | |

| Mid tier: 55% | Functional/Unit leaders: 36% | |

| Smaller Players: 17% | Managers: 50% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool reconstruction where food processing output, packaged food consumption trends, and trade flows were used to approximate enzyme-using volumes by application, then converted into value using typical dosage patterns and average selling price ranges. After shaping the regional total, we corroborated it with selective bottom-up checks, such as rolling up sampled supplier and distributor revenue splits, and cross-checking implied volumes against import patterns and channel feedback.

A few practical inputs that guided the model (illustrative) included growth in bakery and dairy production, expansion of packaged beverage output, local currency movement against the US dollar (which affects imported enzyme costs), adoption of clean-label processing aids, and cold-chain reliability for enzyme handling. Where data gaps existed for smaller countries, we used proxy ratios based on similar food industry structure and then adjusted the shares after expert review.

For forecasting, scenario analysis was used with a base case anchored in expected processed food growth and pricing progression, then stress-tested for currency volatility and slower regulatory approvals. The final forecast was signed off only after the trend direction matched what operators described for the next few years.

Data Validation & Update Cycle

Outputs were checked through triangulation across independent signals, and then variances were investigated before estimates were finalized. When the model implied an enzyme intensity that looked too high or too low for a specific application, the assumptions were revisited and follow-up calls were triggered to confirm what changed.

Before release, the numbers went through multi-step analyst reviews, including consistency checks across countries and across applications so totals reconcile cleanly. Reports are refreshed annually, and interim updates are made when a material event changes prices, trade movement, or demand outlook. Right before delivery, we run a fresh pass to make sure clients receive the latest updated view.

Mordor Intelligence's Africa Food Enzymes Market Market Size Versus Other Published Estimates

Published estimates for Africa food enzymes can differ a lot, even when they use similar market labels, because the included enzyme set, the pricing logic, and the time window are not always aligned. The table helps show how changes in scope and assumptions quickly widen the spread.

The table points to a large gap that is mostly explained by scope and price construction, and in Mordor Intelligence's model, the value is counted for food-grade enzyme preparations used in food and beverage processing within Africa, rather than folding in adjacent industrial enzymes or broader ingredient revenues that may sit outside food enzyme pricing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 208.86 M (2026) | |

| Global Consultancy A | USD 2.40 B (2024) | The estimate appears to use a wider definition that can blend food enzymes with broader ingredient or industrial enzyme revenues, and it also anchors to an earlier base year where currency conversion timing and price levels differ. |

| Industry Publisher B | USD 48.70 M (2026) | The lower figure likely reflects a narrower covered set of applications or countries, and it may rely on conservative adoption rates in bakery and dairy with limited adjustment for import-led supply and price bands. |

Taken together, the comparison shows that the largest swings come from what gets counted as a food enzyme sale, how Africa-wide coverage is handled, and how USD pricing is normalized across volatile currencies. By keeping the steps traceable to food processing activity, adoption levels, and realistic price ranges, the final number stays easier to reproduce and to update when new market signals appear.

Key Questions Answered in the Report

What is the current value of the Africa food enzymes market?

The market is valued at USD 208.86 million in 2026 and is forecast to reach USD 277.53 million by 2031.

Which enzyme type generates the most revenue?

Carbohydrases contribute 45.22% of 2025 sales, making them the largest revenue generator.

Which country provides the fastest growth momentum?

Nigeria shows the quickest expansion with an 8.41% CAGR through 2031, propelled by new processing zones.

Why are lipases gaining traction in African dairy?

Lipases shorten cheese maturation and tailor palm-kernel fats for clean-label ice cream, driving a 10.49% CAGR in this enzyme class.

Page last updated on: