Nigeria Data Center Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

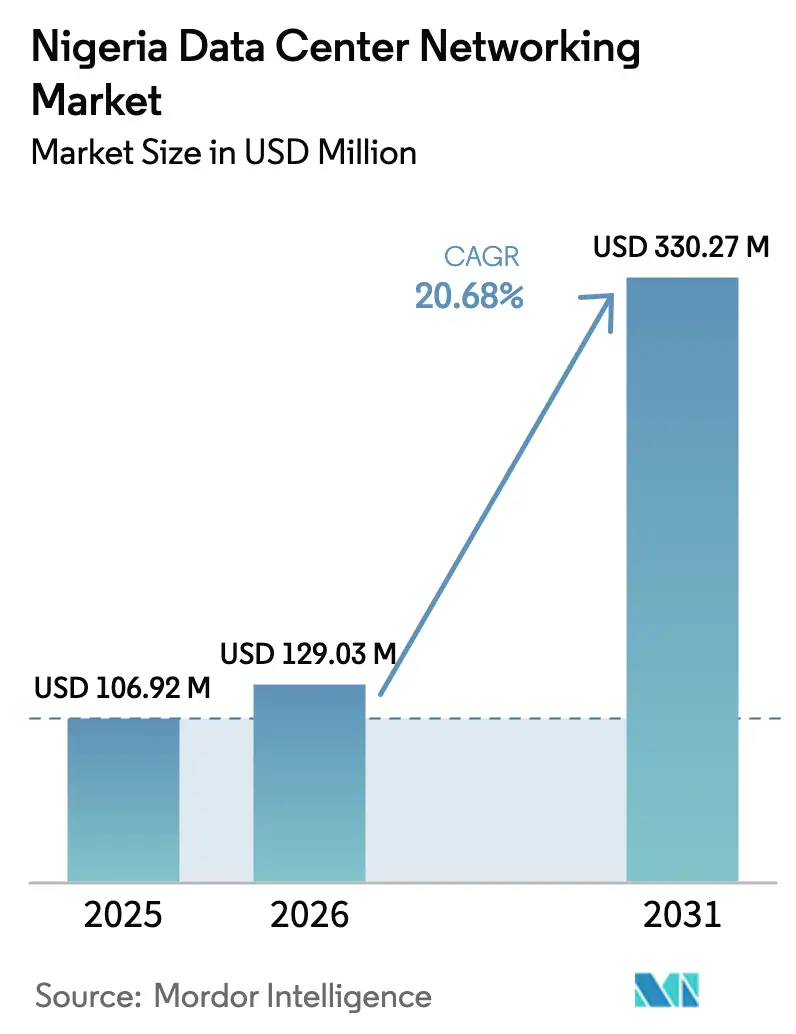

| Base Year Market Size (2025) | USD 106.92 Million |

| Market Size (2026) | USD 129.03 Million |

| Market Size (2031) | USD 330.27 Million |

| Growth Rate (2026 - 2031) | 20.68% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Nigeria Data Center Networking Market Analysis by Mordor Intelligence

Nigeria data center networking market size in 2026 is estimated at USD 129.03 million, growing from 2025 value of USD 106.92 million with 2031 projections showing USD 330.27 million, growing at 20.68% CAGR over 2026-2031. Momentum is fueled by cloud migration, 5G roll-outs, and data-sovereignty mandates that require critical workloads to remain inside national borders. Lagos and Abuja anchor most build-outs, yet secondary cities are steadily adding edge capacity as fintech, media streaming, and e-commerce traffic spreads inland. Spending continues to flow toward leaf-spine topologies, 400G/800G optics, and software-defined tools that tame multi-vendor environments. Vendors that marry high-performance hardware with managed services gain an edge because operators face both power-grid volatility and a shortage of certified network engineers. International capital commitments crossing USD 630 million underscore long-term confidence, even as operators wrestle with elevated OPEX linked to diesel generation and import tariffs on optical gear.

Key Report Takeaways

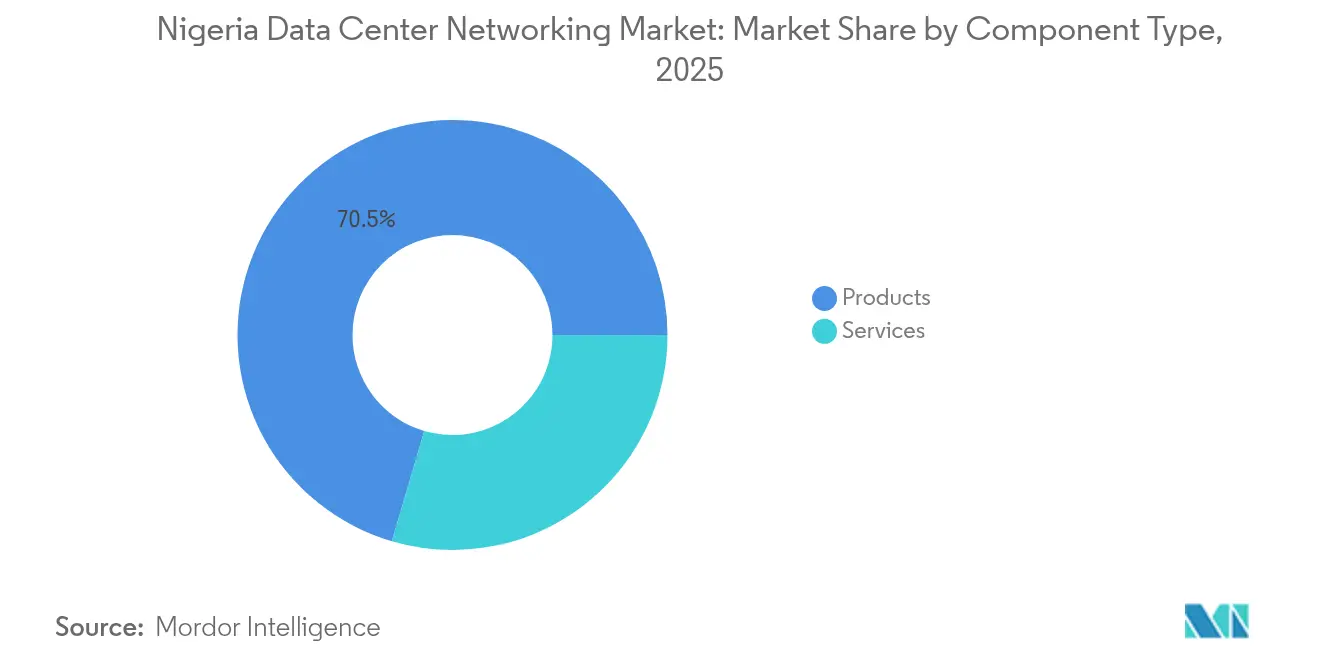

- By component, products led with 70.45% of Nigeria data center networking market share in 2025; services post the fastest 23.35% CAGR through 2031.

- By end-user, IT & telecommunications commanded 37.85% revenue share in 2025, while healthcare & life sciences expand at a 24.55% CAGR to 2031.

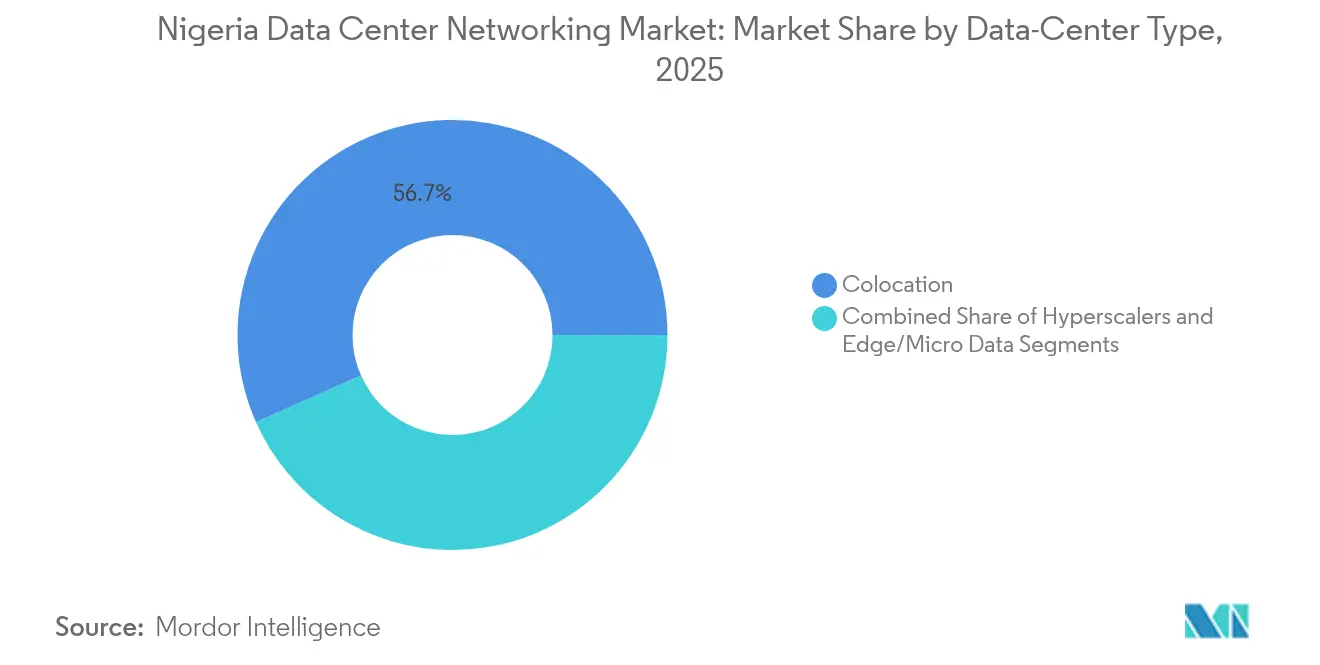

- By data-center type, colocation captured 56.65% of the Nigeria data center networking market size in 2025; hyperscalers grow at a 25.1% CAGR to 2031.

- By bandwidth, 50-100 GbE links held 33.65% revenue share in 2025; >100 GbE upgrades progress at a 22.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Relative standing becomes clear only when country-level and regional contributions are evaluated alongside one another at a global level. Mordor Intelligence's data center networking market share coverage captures this comparative structure.

Nigeria Data Center Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in cloud service adoption and local data sovereignty push | +4.2% | National, with concentration in Lagos, Abuja | Medium term (2-4 years) |

| 5G-driven low-latency demand elevating networking capacity | +3.8% | National, with early deployment in Lagos, Port Harcourt | Medium term (2-4 years) |

| Hyperscale and colocation capital inflows | +3.1% | Lagos, Abuja, with spillover to Port Harcourt | Short term (≤ 2 years) |

| Government incentives via National Broadband Plan 2025 | +2.9% | National, prioritizing underserved regions | Long term (≥ 4 years) |

| Rapid adoption of liquid and immersion cooling enabling 400G fabrics | +2.4% | Lagos, Abuja data center clusters | Medium term (2-4 years) |

| AI workloads requiring 800G leaf-spine architectures in fintech clusters | +1.8% | Lagos financial district, emerging fintech hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in cloud service adoption & data-sovereignty push

Mandated domestic hosting of financial, health, and citizen data compels enterprises to shift workloads to local clouds, sparking immediate upgrades to carrier-neutral facilities that can deliver sub-millisecond latency. Banks in Lagos now specify redundant spine-leaf fabrics for real-time clearing systems, while domestic cloud start-ups tout compliance as a competitive moat. The regulatory stance keeps traffic onshore, driving fresh purchases of high-port-density switches and application delivery controllers. Operators that bundle managed security with ultra-low-latency connectivity become preferred partners for highly regulated sectors.

5G-driven low-latency demand elevating networking capacity

The regulator awarded 3.5 GHz spectrum and declared the backbone 97% ready for nationwide launch. Mobile operators respond with micro-data centers near towers so that IoT and AR/VR sessions avoid long round-trip times.[1]Nigerian Communications Commission, “NCC Announces Nigeria’s 5G Readiness Status,” ncc.gov.ng These edge nodes feed metro facilities by 400G wave-division links, which in turn push backbone requirements beyond 800 G. MTN Nigeria’s 1,400-rack Tier 4 build illustrates the scale required to backhaul 5G traffic peaks. Optical vendors that can integrate coherent pluggables into existing routing shelves gain a pricing advantage.

Hyperscale & colocation capital inflows

Equinix’s USD 320 million MainOne acquisition and IFC’s USD 100 million investment in Raxio validate Nigeria’s location as West Africa’s cloud gateway.[2]Equinix Inc., “Equinix Completes Acquisition of MainOne,” equinix.com Each project demands high-density switches, automated fabric management, and direct-to-cloud exchange points. Operators aim to lift revenue per rack by weaving 400G leaf uplinks with liquid cooling so tenants can host AI accelerators without thermal risk. Fast-tracked deployments shorten payback periods but intensify the scramble for skilled installers.

Government incentives via National Broadband Plan 2025

The plan targets 70% internet penetration and 120,000 km of new fibre, unlocking fiscal perks and zero right-of-way charges for carriers that extend routes into underserved zones. The framework catalyzes metro aggregation builds that link rural POPs to Lagos cores through resilient ring topologies.[3]Office of the Minister of Communications, Innovation and Digital Economy, “National Broadband Plan 2025 Update,” fmcide.gov.ng Vendors able to ruggedise 100 Gbps optics for tropical conditions see early uptake in northern corridors.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unreliable power grid inflating OPEX | -2.8% | National, acute in northern regions | Short term (≤ 2 years) |

| Shortage of certified data-center network engineers | -1.9% | National, concentrated in Lagos, Abuja | Medium term (2-4 years) |

| Delays in metropolitan fiber right-of-way permits | -1.4% | Lagos, Abuja, Port Harcourt metropolitan areas | Short term (≤ 2 years) |

| High import tariffs on greater than100G optics and NICs | -1.1% | National, affecting all data center operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Unreliable power grid inflating OPEX

Grid output frequently slips below 5,000 MW, forcing data centers to run diesel generators that add significant cost per kilowatt-hour. Power volatility also complicates the adoption of high-density 800G switches, which draw more amperage and demand tighter thermal envelopes. Operators increasingly pivot to immersion cooling and on-site gas turbines to tame utility disruptions, yet capital outlays stretch project timelines.

Shortage of certified data-center network engineers

The “Japa” talent exodus drains mid-career professionals skilled in 400G optics, SDN, and fabric automation. Local curricula lag behind hyperscale design practices, leaving integrators to import contractors at a premium. Wages climb, deployment schedules stretch, and managed-service vendors with regional training pipelines clinch multi-year contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Scale on Skills Gaps

Products still command 70.45% revenue in 2025 as operators acquire leaf-spine switches, routers, and coherent optics to migrate from legacy 10 GbE. Services, however, sprint at a 23.35% CAGR, lifted by complexity that forces enterprises to outsource design, integration, and day-two operations. Managed network services capture workloads from fintechs that must run 24/7 yet lack in-house engineers. Consulting and training engagements rise as operators prepare for liquid cooling and 800G road maps. Consequently, suppliers that wrap lifecycle services around hardware record stickier revenues in the Nigeria data center networking market.

A parallel trend is the pivot to software-defined overlays that abstract vendor heterogeneity. Controllers optimize traffic flows across both 100 GbE and 400 GbE links while exposing north-bound APIs for DevOps teams. This transition underpins demand for high-availability professional services, keeping the Nigeria data center networking market on an upward trajectory despite macro headwinds.

By End-User: Healthcare Picks Up Pace

IT & telecom retains 37.85% spending in 2025, but digital-health initiatives push healthcare to a 24.55% CAGR through 2031. Tele-ICU platforms move clinical data among hospitals, cloud AI engines, and insurers, requiring secure L2-L3 fabrics plus application firewalls. Fintechs that handle 42% of continental deal flow remain voracious network buyers for high-frequency trading and instant payment settlement. The government modernises tax and identity systems, adopting private-cloud stacks inside classified facilities. Media outlets deploy content-delivery nodes to keep streaming latency below 50 ms during live sports. All together, these verticals sustain equipment refresh cycles, keeping the Nigeria data center networking market expanding even as economic volatility lingers.

Healthcare’s momentum is most visible in teaching hospitals that now back-haul radiology images to Lagos AI clusters for diagnostics, leaning on 50-100 GbE uplinks and redundant BGP routes. Compliance with new patient-data laws accelerates encryption appliance demand. These upgrades underscore how vertical diversification shields the Nigeria data center networking industry from sector-specific shocks.

By Data-Center Type: Hyperscale Growth Outpaces Colocation

Colocation retains 56.65% share in 2025 because enterprises prize carrier-neutral facilities such as Rack Centre for multi-cloud interconnection. Still, hyperscale campuses post a 25.1% CAGR as Microsoft and Google deploy availability zones to satisfy data-sovereignty clauses. Project pipelines nearing 60 MW in aggregate will swell the Nigeria data center networking market size for hyperscale builds at least through 2031.

Operators blur lines by launching hybrid offers that let tenants mix shared MMR space with reserved suites. These models need high-port-count leaf switches and micro-segmentation firewalls. Edge and micro-data centers emerge along 5G corridors, using modular containers with ruggedised 25 GbE TOR switches to keep back-haul efficient. Such diversification ensures that investment cycles overlap rather than peak simultaneously, smoothing capex volatility in the Nigeria data center networking market.

By Bandwidth: 400G-Plus Moves Mainstream

The lion’s share of 2025 revenue stays with 50-100 GbE because many enterprise workloads remain VM-centric. Yet >100 GbE links grow 22.2% annually as AI clusters, online trading engines, and streaming transcoders exceed 30 Gbps per server. Early 800G pilots in Lagos fintech racks rely on immersion-cooled chassis that offset 35 W per optical module. Vendors supplying low-power DSPs capture orders as clients chase lower PUE.

Conversely, ≤10 GbE uplinks decline, surviving only in branch offices. Secondary cities adopt 25-40 GbE for edge compute nodes that aggregate IoT sensor feeds. These shifts collectively elevate average port speeds, pushing the Nigeria data center networking market toward higher ASPs even as unit volumes level off.

Geography Analysis

Lagos anchors nearly every hyperscale launch thanks to proximity to subsea cables, Nigeria Stock Exchange, and the fintech corridor. The metro’s carrier hotels already land traffic from more than 40 regional ISPs, uplifting cross-connect volumes and boosting Nigeria data center networking market demand for 400G optical backbones. Abuja forms the governmental compute enclave, driven by e-governance applications and National Broadband Plan incentives that subsidise fibre laterals into underserved districts. Port Harcourt now attracts edge nodes that serve oil-and-gas telemetry and 5G small-cell aggregation. Northern states lag on utility stability, yet recent solar-farm PPAs could unlock captive micro-grid data centers. Across all regions, new fibre commitments of 90,000 km aim to raise household internet penetration from 42% to 70% by 2025, laying fresh conduits for high-capacity inter-data-center routes.

Cross-border connectivity improves as new subsea systems land in Lagos, cutting latencies to Europe to below 90 ms and positioning Nigeria as a regional handoff point. Traffic from Ghana and Côte d’Ivoire increasingly hairpins through Lagos exchange points, further enlarging the Nigeria data center networking market. With right-of-way fees lifted in multiple states, metro loops proliferate, yet permitting delays still cause schedule overruns in congested urban zones.

Analysis of the data center networking market by Mordor Intelligence spans multiple other regional evaluations across Africa, Europe, and North America, supported by country-level insights for South Africa, Austria, United States, Brazil, Saudi Arabia, and Mexico, wherein local market conditions keep varying from one country to another.

Competitive Landscape

Global OEMs such as Cisco, Huawei, and Dell maintain brand pull, bolstered by end-to-end portfolios and channel financing. Juniper and Arista specialise in high-density leaf-spine fabrics, securing AI and HFT projects that require deterministic latency. Ciena’s WaveLogic 6 Nano pluggables push coherent 800G onto compact chassis, winning metro back-haul slots. Local integrators fill a critical gap by offering compliance alignment, customs clearing, and on-site support, which international vendors sometimes deliver only remotely.

Technology differentiation increasingly revolves around software-defined orchestration tied to AI-driven telemetry that predicts congestion and power anomalies. Vendors that bundle network-aware liquid cooling carve out margin because customers want a single throat to choke. Edge deployments in secondary cities open a white-space market for ruggedised switches rated for high humidity and temperature swings. Over the forecast period, competitive intensity should remain moderate as capacity additions stay ahead of demand, keeping pricing stable but rewarding service-rich offers.

Nigeria Data Center Networking Industry Leaders

-

Cisco Systems Inc.

-

Huawei Technologies Co. Ltd.

-

Dell Technologies Inc.

-

Oracle Corporation

-

Juniper Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Equinix expanded its Lagos operations, boosting neutral interconnection capacity for cloud providers.

- May 2025: Schneider Electric released new power and cooling suites tailored to Nigeria’s grid volatility.

- April 2025: Rack Centre commissioned its 12 MW LGS2 facility with region-leading PUE, aimed at fintech and e-commerce tenants.

- April 2025: IFC injected USD 100 million into Raxio to speed Nigerian and regional data-center builds

- April 2025: Equinix completed a USD 140 million southern Nigeria expansion, enhancing interconnection density.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Nigeria data-center networking market as all physical and software solutions that move packets inside or between local data-center facilities, including Ethernet switches, routers, application delivery controllers, SAN fabrics, and associated support services sold to third-party colocation, enterprise, hyperscale, and edge sites across the country. According to Mordor Intelligence, values reflect factory-gate revenues plus recurring maintenance recognized inside Nigeria during calendar year 2025.

Scope exclusion: We do not count spend on consumer CPE, wide-area carrier transport, or cloud provider backbone gear installed outside Nigerian borders.

Segmentation Overview

-

By Component

-

Products

- Ethernet Switches

- Routers

- Storage Area Network (SAN)

- Application Delivery Controllers (ADC)

- Network Security Appliances

- Software-Defined Networking (SDN) Controllers

- Optical Interconnects

-

Services

- Installation and Integration

- Training and Consulting

- Support and Maintenance

- Managed Network Services

-

Products

-

By End-User

- IT and Telecommunications

- Banking, Financial Services and Insurance (BFSI)

- Government and Defense

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Other End-Users

-

By Data-Center Type

- Colocation

- Hyperscalers/Cloud Service Providers

- Edge/Micro Data Centers

-

By Bandwidth

- LessThan equals to 10 GbE

- 25–40 GbE

- 50–100 GbE

- Greater Than 100 GbE

Detailed Research Methodology and Data Validation

Primary Research

Conversations with network architects at colocation operators, carrier procurement leads in Lagos and Abuja, and regional value-added distributors helped us vet uplink mix, price erosion, and service attach rates. Inputs from OEM field engineers clarified adoption timing for 100 GbE and 400 GbE fabrics, which our desk research could not quantify with certainty.

Desk Research

We started with public sources such as the Nigerian Communications Commission statistical bulletins, National Bureau of Statistics trade tables, and industry briefs from the Africa Data Centres Association. Trade filings, import records on Volza, and patents extracted via Questel added device flow and technology cadence. Company 10-Ks plus press releases supplied baseline pricing and capacity announcements, while Dow Jones Factiva helped track fresh buildouts. This list is indicative; many additional open datasets informed gap checks.

A second sweep covered paid repositories that Mordor analysts access. D&B Hoovers gave vendor financials, Marklines confirmed hyperscale expansion vehicles entering Lagos, and Global Security flagged government cloud contracts influencing demand. These blocks anchored historical shipments before our team moved to interviews.

Market-Sizing & Forecasting

A top-down model begins with active rack counts and power draw published by operators, which are then converted into port demand using validated ports-per-rack ratios and typical utilization. Results are corroborated through selective bottom-up roll-ups of switch shipments and average selling prices collected in primary calls. Key variables like mobile data traffic growth, cloud seat penetration, fiber-kilometer rollout, average rack density, and import tariff swings drive yearly adjustments. We employ multivariate regression to project each driver through 2030, before scenario analysis fine-tunes our base case. Where shipment data were incomplete, interpolation used three-year moving averages and price bands discussed with channel partners.

Data Validation & Update Cycle

Outputs pass two internal reviews, variance checks against external data cues, and a reconciliation call with at least one earlier respondent. Mordor refreshes this model annually and issues mid-cycle updates when currency shocks, spectrum auctions, or material hyperscale deals shift baselines.

Why Mordor's Nigeria Data Center Networking Baseline Rings True

Published figures often differ because studies apply dissimilar product baskets, price curves, and refresh cadences.

Our disciplined blend of local primary insight, tariff-adjusted pricing, and annually updated driver sets narrows those gaps for decision makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 106.92 M (2025) | Mordor Intelligence | - |

| USD 88.19 M (2025) | Global Consultancy A | Hardware only, excludes services and support; limited local channel checks |

| USD 60.00 M (2023) | Trade Journal B | Older baseline, no 5G traffic uplift, scope stops at <=25 GbE switches |

The comparison shows that when scope is narrow or data are stale, totals swing widely. By grounding every assumption in fresh Nigerian rack counts, tariff-adjusted ASPs, and on-the-ground expert views, Mordor Intelligence delivers a balanced, transparent benchmark that clients can replicate and trust.

Key Questions Answered in the Report

What is the current size of the Nigeria data center networking market?

The market is valued at USD 129.03 million in 2026 and is on track to hit USD 330.27 million by 2031.

Which segment grows fastest in the Nigeria data center networking market?

Services expand at a 23.35% CAGR as enterprises outsource complex network design, integration, and operations.

How will 5G affect the Nigeria data center networking industry?

5G roll-outs trigger edge-data-center builds and require 400G/800G back-haul links to handle low-latency traffic.

What is the biggest restraint for operators?

Unreliable power infrastructure forces heavy reliance on diesel generators, inflating operating costs and complicating high-density equipment deployments

Why are hyperscale investments accelerating?

Data-sovereignty rules, rising cloud adoption, and new subsea cables make Nigeria a strategic hub, prompting global players to commit multi-hundred-million-dollar campuses.

Page last updated on: