Africa Bitumen Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

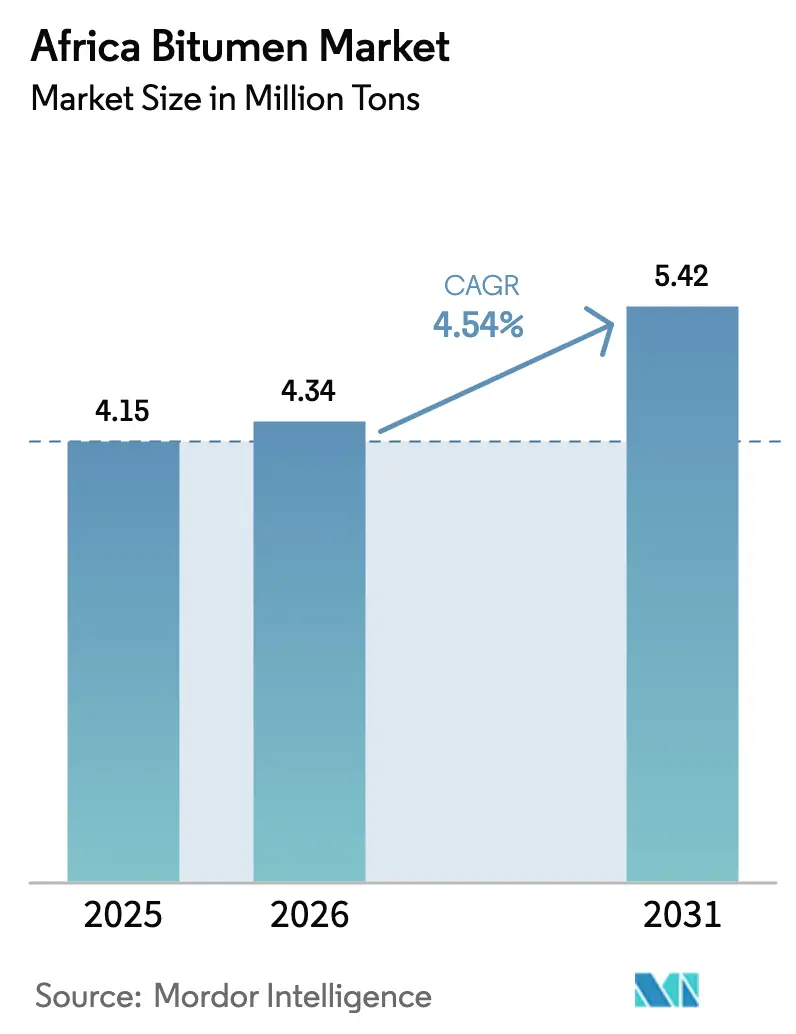

| Base Year Market Size (2025) | 4.15 Million tons |

| Market Volume (2026) | 4.34 Million tons |

| Market Volume (2031) | 5.42 Million tons |

| Growth Rate (2026 - 2031) | 4.54% CAGR |

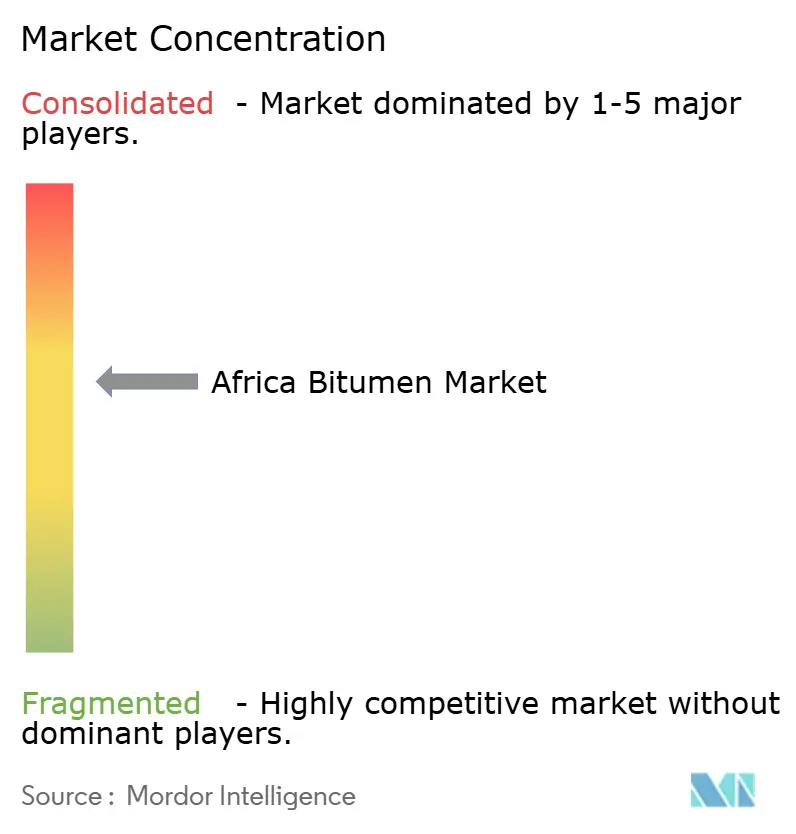

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Bitumen Market Analysis by Mordor Intelligence

The Africa Bitumen Market size is expected to grow from 4.15 Million tons in 2025 to 4.34 Million tons in 2026 and is forecast to reach 5.42 Million tons by 2031 at 4.54% CAGR over 2026-2031.The combination of rapid urban population growth, record public-sector spending on roads, and a gradual pivot toward specialty binders positions the Africa bitumen market for lengthy expansion even as sovereign balance sheets tighten. Polymer-modified and emulsified grades are capturing procurement share because performance-based specifications now dominate large contracts, while cost-inflating carbon rules force refiners to innovate their feedstock slates. Strategic opportunities arise where governments require longer-lasting pavements, where private developers standardize waterproofing membranes, and where indigenous ore-grade bitumen deposits promise import substitution. Competitive intensity is fragmenting as international oil majors sell refining stakes, inviting local blenders to integrate storage terminals with on-site modification units to shorten lead times and lift margins. Downside risk remains tethered to crude-oil price spikes, tighter greenhouse-gas caps, and concrete or block-paver substitution on high-visibility urban arterials.

Key Report Takeaways

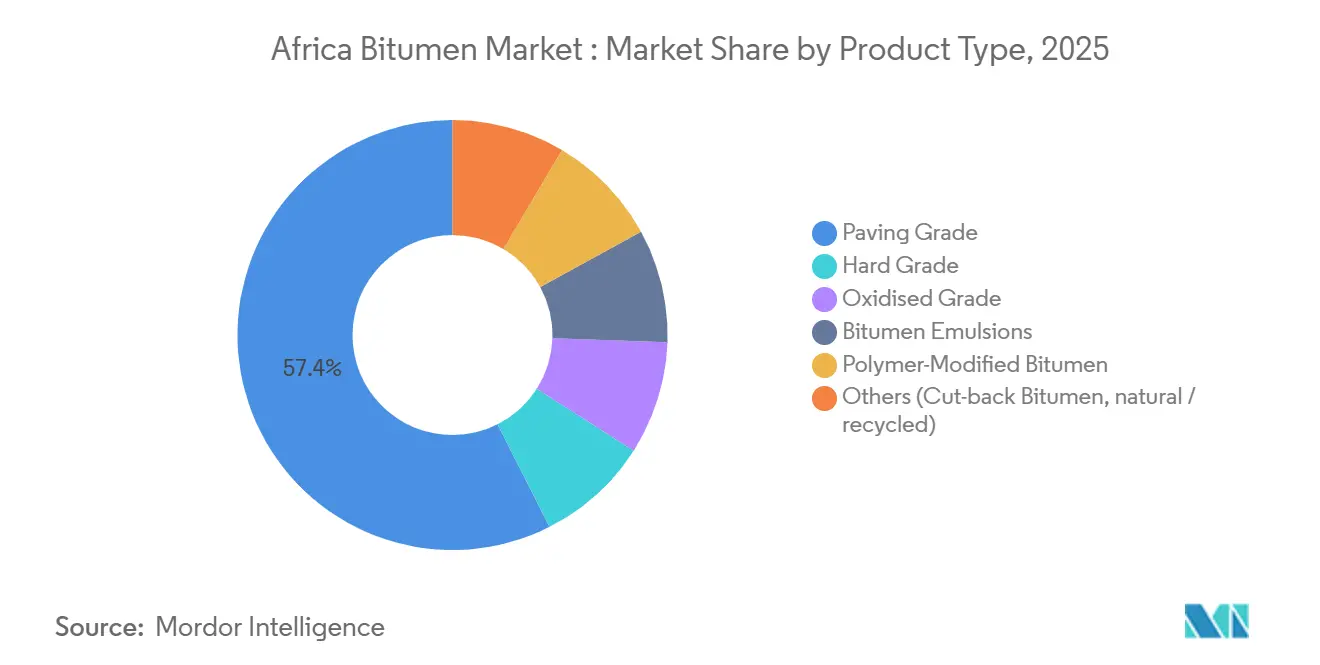

- By product type, paving-grade captured 57.45% of Africa bitumen market share in 2025 and polymer-modified grades are advancing at a 7.12% CAGR, the fastest rate through 2031.

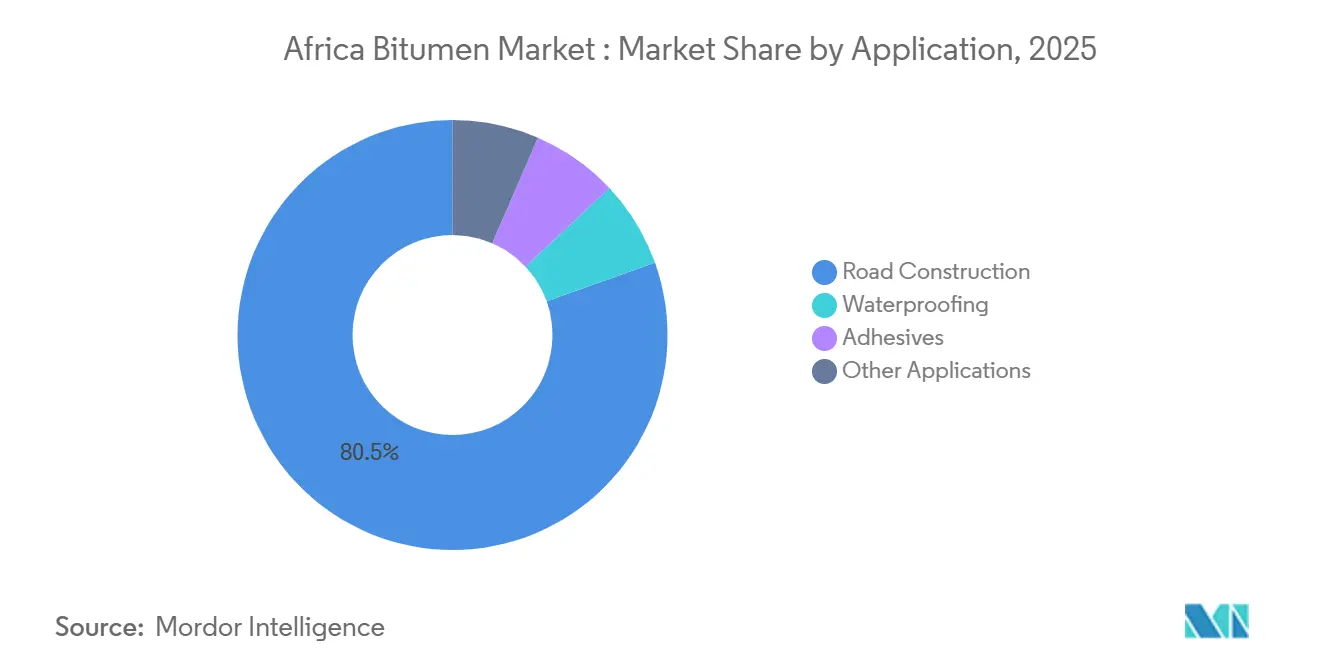

- By application, road construction held 80.47% of Africa bitumen market size in 2025, while other applications are poised for a 6.83% CAGR to 2031.

- By geography, South Africa led with 25.29% of 2025 volume, while Nigeria is poised for a 6.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa contributes to a system defined not by any single geography but by the interaction of many. The global bitumen market data by Mordor Intelligence represents that combined structure.

Africa Bitumen Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Government-Funded Road-Network Expansion | +1.8% | Nigeria, Kenya, Egypt, Algeria, Morocco | Medium term (2-4 years) |

| Accelerating Demand for Waterproofing and Roofing Membranes | +0.6% | South Africa, Nigeria, Egypt, Kenya | Long term (≥ 4 years) |

| Rapid Adoption of Polymer-Modified and Emulsified Bitumen | +1.2% | South Africa, Kenya, Ghana, Ethiopia | Medium term (2-4 years) |

| Urbanization-Led Road Maintenance and Rehabilitation Spend | +0.7% | Global, with early gains in Lagos, Nairobi, Johannesburg | Long term (≥ 4 years) |

| Commercialization of Nigeria's Native Bitumen Reserves | +0.3% | National, concentrated in Ondo, Ogun, Edo States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Government-Funded Road-Network Expansion

Between 2024 and 2026, African sovereigns earmarked more than USD 25 billion for strategic highway corridors, a fiscal commitment that elevates the addressable volume for the Africa bitumen market. Nigeria’s Lagos–Calabar coastal highway alone is budgeted at USD 2 billion and will consume roughly 180,000 tons of polymer-modified binder annually before commissioning in 2029. Kenya secured USD 3.6 billion in blended finance for the 440-kilometer Usahihi Expressway, unlocking a 2026 ground-breaking that embeds warm-mix-asphalt clauses into bid documents. Algeria’s Chiffa–Berrouaghia stretch of the North-South highway, opened in July 2025, demonstrated how Belt and Road Initiative capital prefers asphalt over concrete in hot, arid micro-climates. Morocco’s Guercif–Nador link received a EUR 246 million African Development Bank loan, ensuring freight traffic from the Nador West Med port will ride on performance-graded asphalt by 2028. Because multilateral lenders now require lifecycle-cost models, most engineering contracts justify premium polymer-modified overlays that double pavement life, adding structural demand even where headline budgets stay flat.

Accelerating Demand for Waterproofing and Roofing Membranes

Sub-Saharan cities are adding residents at 3.5% per year, propelling a surge in mid-rise concrete structures that specify atactic-polypropylene (APP) or styrene-butadiene-styrene (SBS) membranes over outdated tar-paper. The South African Council for Scientific and Industrial Research reported in 2024 that nano-modified emulsions lower rooftop surface temperatures by up to 18%, prompting Johannesburg developers to standardize reflective coatings that extend roof life from 10 to 25 years. Nigeria’s real-estate sector grew 6.2% in 2024, and builders in Lagos now specify self-adhesive membranes capable of resisting saline groundwater, a chronic problem on reclaimed land. Kenya’s 2025 building code mandates waterproofing for any structure exceeding three stories, automatically granting bitumen membrane suppliers a captive urban client base. Because waterproofing revenue is relatively immune to public-budget cycles, refiners that diversify into membranes cushion volatility when highway allocations are delayed.

Rapid Adoption of Polymer-Modified and Emulsified Bitumen

Polymer-modified grades are expanding at a 7.12% CAGR, outpacing the broad Africa bitumen market by 258 basis points. South Africa’s Sabita Manual 35, revised in 2024, requires SBS or EVA modification for routes exceeding 3 million equivalent standard axles, automatically reserving 40% of national-route tonnage for high-value binders. Ghana’s GOIL-SMB venture brought a USD 40 million plant online in September 2024, giving West Africa a 7,500-ton storage hub with in-line dosing that cuts regional trucking costs 15%. Ethiopia tendered 12 performance-based contracts that specify polymer-modified binders for high-altitude frost zones, a specification shift that alone adds 22,000 tons of incremental demand by 2028. Sasol’s SASOBIT additive enables warm-mix asphalt at 120-140 °C, lowering carbon output 30% and keeping paving crews active during Highveld winter nights, a productivity bonus that most agencies price into bid assessments.

Urbanization-Led Road Maintenance and Rehabilitation Spend

African megacities spend an increasing share of transport budgets on resurfacing and rehabilitation rather than new alignments, a pivot that boosts emulsified and polymer-modified grades. Lagos, Nairobi, and Johannesburg each recorded more than 4,000 pothole complaints in 2025, forcing municipal engineers to adopt micro-surfacing treatments that extend service life 5–7 years at one-third the overlay cost. Cold-in-place recycling with cationic emulsions now dominates Johannesburg’s winter maintenance schedule, lifting demand for rapid-setting products that were niche five years earlier. In Nairobi, Bus Rapid Transit lanes receive SBS chip seals to prevent rutting under articulated buses, further expanding the specialty-binder footprint. The maintenance-led model reinjects steady volume into the Africa bitumen market even when macro headwinds curb capital budgets for greenfield expressways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening VOC / GHG Emission Regulations | -0.5% | South Africa, Kenya, Egypt | Short term (≤ 2 years) |

| Concrete and Block-Paving Substitution in Urban Arterials | -0.3% | Ghana, Kenya, Nigeria (urban centers) | Medium term (2-4 years) |

| Crude Oil Price Volatility Inflating Feedstock Costs | -0.4% | Global, acute in import-dependent markets (Ghana, Kenya, Tanzania) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening VOC / GHG Emission Regulations

South Africa’s Climate Change Act imposes a carbon-budget system that forces asphalt producers to trim plant-level emissions 2–3% annually until 2030, a rule that directly inflates production costs for penetration-grade bitumen[1]South African Department of Forestry, Fisheries and the Environment, “Climate Change Act 2024,” dffe.gov.za . The Carbon Tax Act further levies ZAR 190 per ton CO₂e, calculated at 3.15 tons CO₂e per ton of bitumen, and the rate escalates at inflation plus 2% every April. Kenya’s National Environment Management Authority capped stack VOCs at 50 mg/m³ in 2025, triggering retrofit bills topping USD 500,000 for every plant in Nairobi’s industrial belt. Egypt’s environment ministry now requires continuous emissions monitors on every distillation column producing bitumen, effectively sidelining small private refiners that cannot justify USD 1 million of compliance gear. The resulting compliance arbitrage encourages blenders to relocate to Mozambique and Tanzania, then back-haul finished product into regulated markets, fragmenting supply chains and undermining in-country investment.

Concrete and Block-Paving Substitution in Urban Arterials

Ghanaian engineers documented in 2024 that interlocking concrete pavers cut lifecycle costs by up to 20% on steep city arteries where asphalt rutting accelerates during monsoon seasons. Kenya’s cost manual pegs installed concrete blocks at KES 1,200 per m² versus KES 1,350 for warm-mix asphalt adjusted for recent bitumen spikes, a saving that has already converted 12 roundabouts in Nairobi’s CBD. Lagos State Public Works piloted permeable pavers on 8 km of secondary roads, slashing storm-runoff 40% and eliminating repetitive crack sealing - a result that garners political favor in flood-prone suburbs. While rural corridors favor bitumen’s rapid construction speed, urban show-case projects shape engineer preferences, risking erosion of bitumen’s brand equity where public scrutiny is highest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialty Grades Capture Margin Premium

Paving-grade binder retained 57.45% Africa bitumen market share in 2025, satisfying lowest-cost bids on long-haul highways across Algeria, Egypt, and Tanzania. Yet polymer-modified grades are registering a 7.12% CAGR, redefining specifications for corridors in South Africa and Kenya. Emulsions are climbing steadily because cationic surface dressing extends pavement life five years for one-third of overlay cost. Oxidized-grade demand tracks roofing cycles in Nigeria and Egypt, while hard-grade remains a niche used in pipe coating. Sasol’s lignin-enhanced bio-binder trial, swapping 15% of bitumen for bagasse derivatives, hints at future blends that satisfy carbon levies without sacrificing rut resistance.

Price realization differs markedly: paving-grade trades at vacuum-residue parity; polymer-modified grades fetch premiums of USD 140–180 per ton; emulsions deliver USD 110 margins when sold with turnkey micro-surfacing service contracts. Because carbon taxes apply per ton of binder, specialty grades amortize levies over longer pavement cycles, giving polymer-modified suppliers pricing power even when crude swings. Investors gauge project returns not only on throughput but also on additive-line optionality; Tema’s new 7,500-ton storage hub illustrates how in-line dosing can pivot between SBS and EVA modifiers in under an hour, maximizing asset utilization.

By Application: Maintenance Spend Diversifies Revenue

Road construction absorbed 80.47% of 2025 demand, buoyed by the 1.2 million-ton combined requirement of Nigeria’s coastal highway, Kenya’s Usahihi Expressway, and Algeria’s trans-Atlas segments. Yet other applications collectively clock a 6.83% CAGR, outpacing greenfield alignments. Surface-dressing programs in Ghana, Sierra Leone, and Côte d’Ivoire prefer emulsified binders because they can heal cracked pavements in dry seasons when hot-mix plants sit idle. Automotive hot-melt adhesives remain niche but lucrative: tier-one suppliers to South Africa’s BMW and Ford plants buy stabilized oxidized bitumen at twice paving-grade margins.

Fiscal austerity elevates maintenance budgets because low-traffic rural roads can be rejuvenated for USD 35,000 per km using slurry seals versus USD 140,000 for full-depth reconstruction, making emulsified products politically attractive during election cycles. As a result, specialty blenders hedge volatility by courting both highway-agency tenders and property-developer orders, an operational model that smooths revenue cycles and encourages investment in dual-purpose storage tanks and small-batch reactors.

Geography Analysis

South Africa contributed 25.29% of overall 2025 volume, anchored by SANRAL’s predictable tender calendar and by Sasol-operated Natref’s on-spec output despite a January 2025 distillation-unit fire that squeezed short-term supply. Imports filled the gap, climbing to 200,000 tons in 2024 and eroding coastal price discounts. Nigeria’s 6.36% CAGR positions it as the growth engine of the Africa bitumen market; the Lagos–Calabar highway alone demands 180,000 tons annually, while planned mining of native deposits promises to displace 50% of imports by 2030.

Egypt’s National Road Project, bankrolled at EGP 175 billion, already added 7,000 km of lanes and continues to specify 50/70 penetration grade except on Cairo ring-road ramps where polymer-modified dictates dowel-bar retrofits. Algeria’s July 2025 opening of the 53-km Chiffa–Berrouaghia section consumed a large amount of paving-grade, confirming Belt and Road contractors’ preference for bitumen in arid corridors. Morocco’s Guercif–Nador link will finalize the trans-Maghreb corridor, cementing an asphalt route from Tunis to Casablanca by 2028.

East Africa commands a smaller but accelerating share. Kenya’s USD 3.6 billion Usahihi Expressway, financed in May 2025, aligns moderate polymer-modified demand with a 36-month build window. Ethiopia’s ETB 3 trillion transport plan intends to boost the paved network from 144,000 km to 246,000 km, of which at least 25% requires polymer-modified binder for high-altitude freeze-thaw cycles. Tanzania’s infrastructure diversification, showcased by the Standard Gauge Railway and the Julius Nyerere hydro project, siphons budget share away from roads, explaining subdued bitumen imports relative to peers.

West Africa’s supply chain is redrawing itself around new coastal terminals. Ghana’s Tema plant exports emulsions and PMB across ECOWAS in ISO tanks, trimming voyage times to Abidjan to under 16 hours. Cameroon’s All Bitumen refinery, under construction in Kribi, will add 250,000 tons of annual capacity, reducing landed costs in landlocked Chad by an expected 30% once trucking corridors are synchronized with rail extensions.

The bitumen market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Asia and Europe.

Competitive Landscape

Africa hosts a moderately fragmented supplier matrix. TotalEnergies, Shell, and BP managed 32% of 2025 refining throughput, but repeated divestments are shrinking their footprint. TotalEnergies sold its 50% Natref stake and exited Côte d’Ivoire’s SIR in 2024, yet expanded its branded-station network to 4,520 outlets across 30 countries to monetize non-fuel retail and lubricants[2]TotalEnergies SE, “Annual Report 2024,” totalenergies.com . Shell exited onshore SPDC assets in Nigeria in March 2025, freeing capital for LNG and lubricants, leaving local terminals to import finished binder.

Regional challengers exploit the vacuum. GOIL-SMB’s USD 40 million Tema hub co-locates import jetty, polymer-mod lines, and ISO-tank loading, slicing logistics costs 15% and granting West African contractors 48-hour order-to-dispatch cycles. All Bitumen Cameroon’s CFA 161 billion Kribi refinery will supply 250,000 tons per year, coupling a 10,000-bpd mini-refinery with PMB reactors to feed Central and landlocked Sahel demand. Sasol controls the warm-mix niche via SASOBIT additive, bundling chemical supply with design-build paving contracts that lock in downstream binder volume.

Innovation hotspots center on bio-binders and rubber-crumb. South Africa’s CSIR tests showed 15% lignin substitution cut carbon intensity 22% without rutting degradation, aligning with pending Scope 3 reporting rules. Kenyan startups blend tire-derived rubber into 70/100 penetration binder, achieving 25% lifecycle-cost gains on Nairobi’s freight corridors. These novel blends fit under carbon-tax exemptions for recycled content, hinting at competitive upside for first-movers.

Africa Bitumen Industry Leaders

Exxon Mobil Corporation

Shell plc

TotalEnergies

BP p.l.c.

THE Bouygues group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: All Bitumen Cameroon signed a memorandum of understanding with the government of Cameroon to accelerate the development of an integrated bitumen production plant. The XAF 161 billion project is expected to produce 230,000 liters of diesel per day and 250,000 tons of bitumen annually, addressing the increasing demand for bitumen in road construction across West and Central Africa

- September 2024: The African Bitumen Terminal (ABT) in Tema, a joint venture between GOIL PLC and Ivory Coast's SMB, was inaugurated to supply high-quality bitumen for road construction in the region. The facility provides storage, laboratory testing, and production of various bitumen grades (AC10, AC20) and emulsions, enhancing economic ties between Ghana and Côte d'Ivoire.

Africa Bitumen Market Report Scope

Bitumen is a black or dark brown non-crystalline soil or viscous material having adhesive properties. It is derived from petroleum crude either naturally or through refinery processes. Bitumen is commonly used as a binder in the construction of roads, runways, and platforms, and for waterproofing and adhesive applications in residential and commercial construction.

The Africa Bitumen Market is segmented by product type, application, and geography. By product type, the market is segmented into paving grade, hard grade, oxidized grade, bitumen emulsions, polymer modified bitumen, and others (cut-back bitumen and natural / recycled bitumen). By application, the market is segmented into road construction, waterproofing, adhesives, and other applications (road maintenance and rehabilitation, industrial coatings, etc.) The report also covers the market size and forecasts for the Africa Bitumen Market in 10 countries across the African region. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Paving Grade |

| Hard Grade |

| Oxidised Grade |

| Bitumen Emulsions |

| Polymer-Modified Bitumen |

| Others (Cut-back Bitumen, natural / recycled) |

| Road Construction |

| Waterproofing |

| Adhesives |

| Other Applications (Road Maintenance and Rehabilitation, Industrial Coatings, etc.) |

| South Africa |

| Nigeria |

| Egypt |

| Algeria |

| Morocco |

| Kenya |

| Ghana |

| Ethiopia |

| Tanzania |

| Côte d’Ivoire |

| Rest of Africa |

| By Product Type | Paving Grade |

| Hard Grade | |

| Oxidised Grade | |

| Bitumen Emulsions | |

| Polymer-Modified Bitumen | |

| Others (Cut-back Bitumen, natural / recycled) | |

| By Application | Road Construction |

| Waterproofing | |

| Adhesives | |

| Other Applications (Road Maintenance and Rehabilitation, Industrial Coatings, etc.) | |

| By Geography | South Africa |

| Nigeria | |

| Egypt | |

| Algeria | |

| Morocco | |

| Kenya | |

| Ghana | |

| Ethiopia | |

| Tanzania | |

| Côte d’Ivoire | |

| Rest of Africa |

Key Questions Answered in the Report

What is the projected size of the Africa bitumen market in 2031?

Volume is forecast to reach 5.42 million tons by 2031, up from 4.34 million tons in 2026.

Which product type is expanding the quickest across the region?

Polymer-modified grades are advancing at a 7.12% CAGR, the fastest rate among all binders through 2031.

How much share did paving-grade bitumen command in 2025?

Paving-grade held 57.45% of total volume in 2025.

Why is Nigeria seen as the fastest-growing geography for bitumen demand?

The Lagos–Calabar coastal highway and planned mining of 42 billion tons of native reserves are driving a 6.36% CAGR through 2031.

Page last updated on: