Bitumen Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

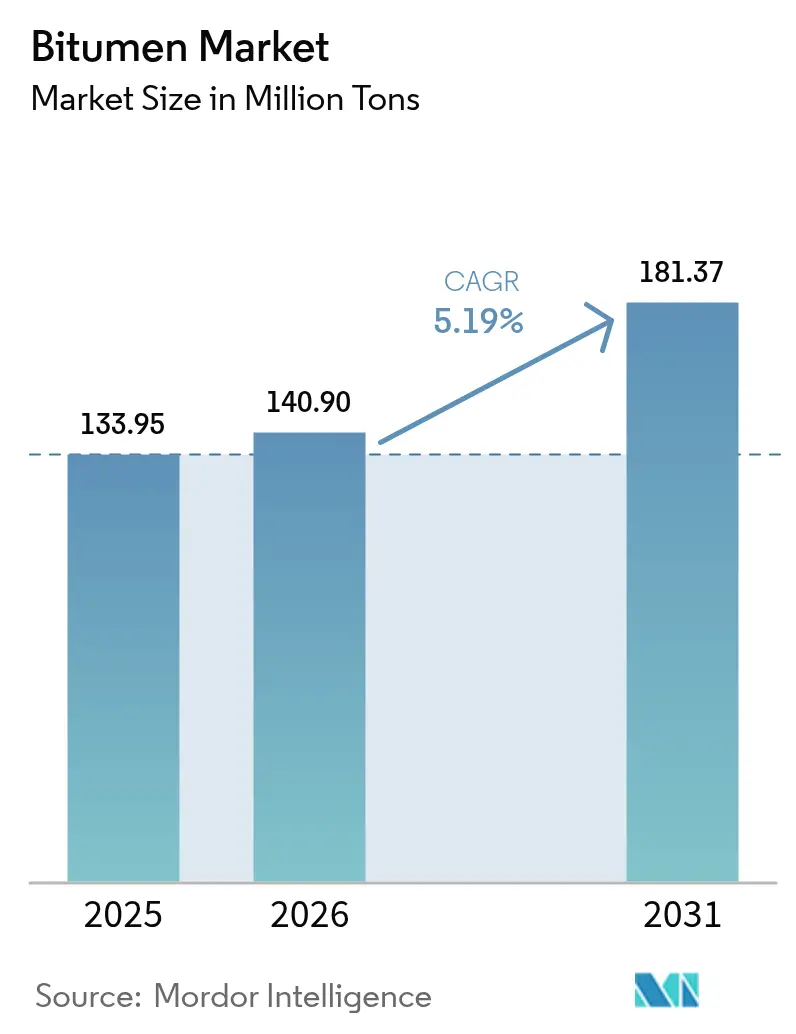

| Market Volume (2026) | 140.9 Million tons |

| Market Volume (2031) | 181.37 Million tons |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bitumen Market Analysis by Mordor Intelligence

The Bitumen Market size is expected to grow from 133.95 Million tons in 2025 to 140.9 Million tons in 2026 and is forecast to reach 181.37 Million tons by 2031 at 5.19% CAGR over 2026-2031. Heightened public‐sector spending on highways, airport runways, and climate-resilient pavements is sustaining long-run demand, while polymer-modified formulations open higher-margin niches. Stable crude-oil prices in 2024 created predictable feedstock economics, yet the projected slide to USD 66 per barrel by 2026 could both widen production margins and intensify price competition. Asia-Pacific remains the pivotal consumption hub, boosted by aggressive infrastructure outlays and flexible import strategies that exploit Middle-Eastern price discounts. Concurrently, environmental regulations accelerate the transition toward low-temperature emulsions and recycled asphalt technologies, subtly reshaping supply chains and product specifications within the bitumen market.

Key Report Takeaways

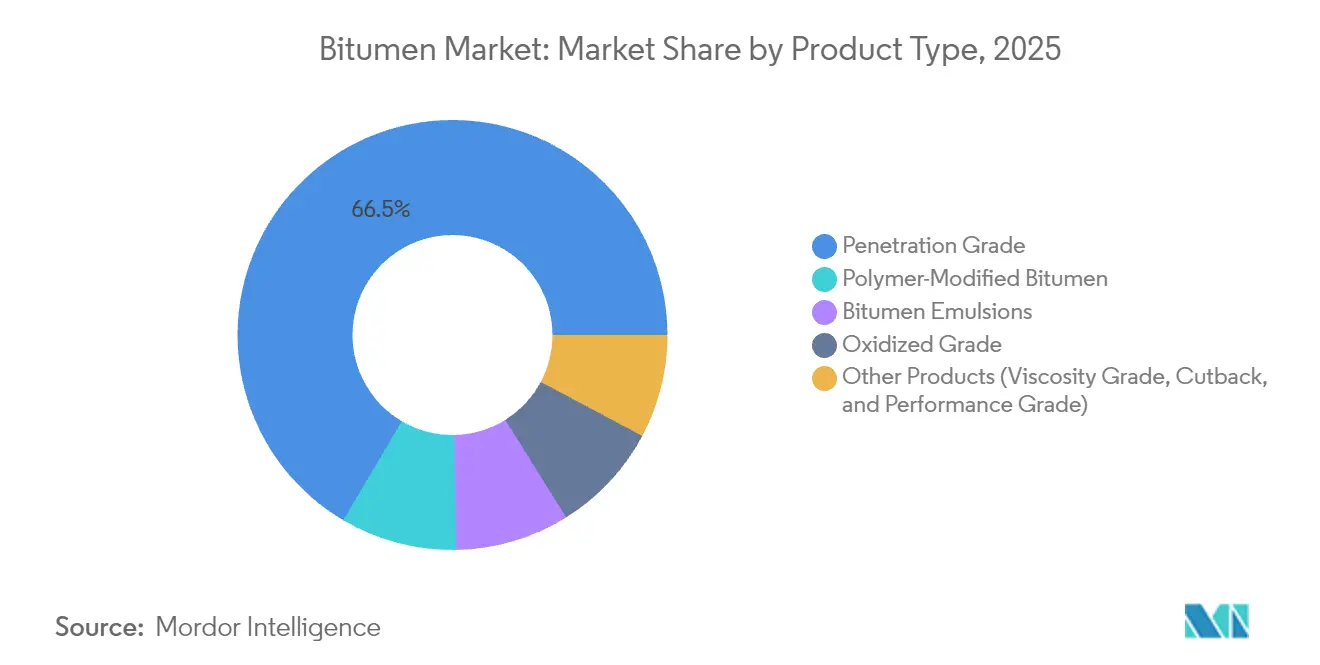

- By product type, penetration-grade bitumen captured 66.52% of the bitumen market share in 2025, and is advancing at the fastest 5.62% CAGR through 2031.

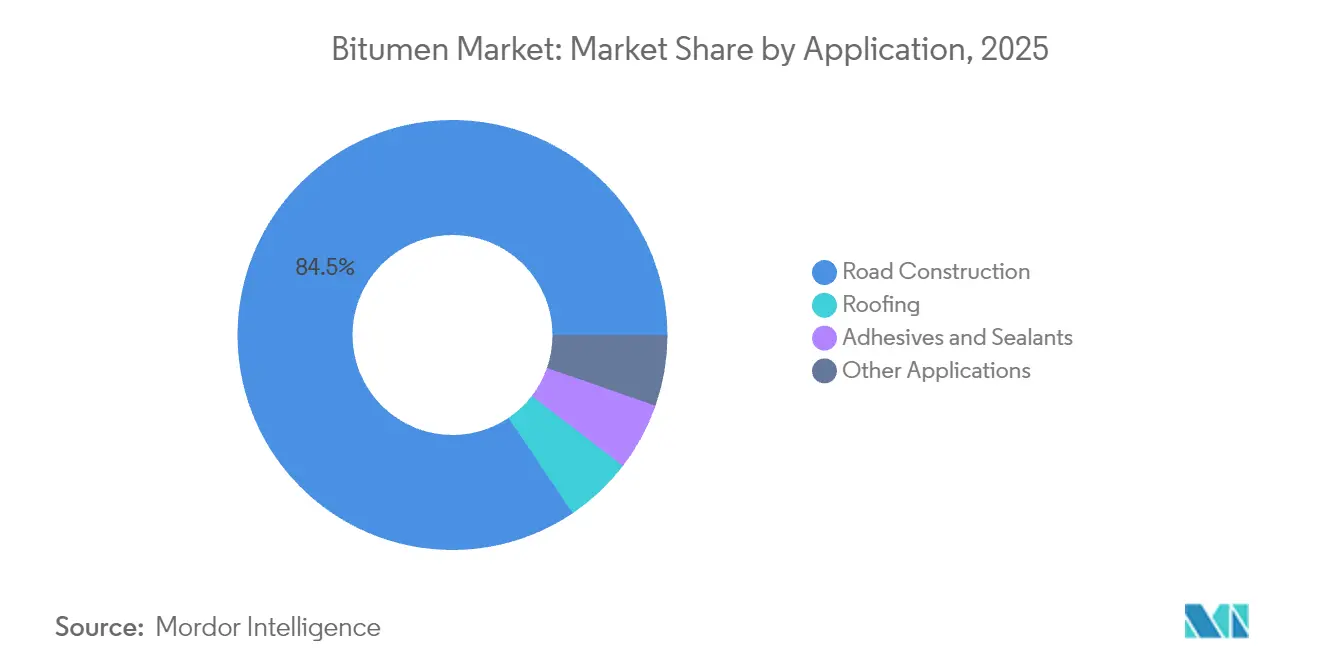

- By application, road construction accounted for 84.45% of the bitumen market size in 2025 and is projected to grow at a 5.56% CAGR through 2031.

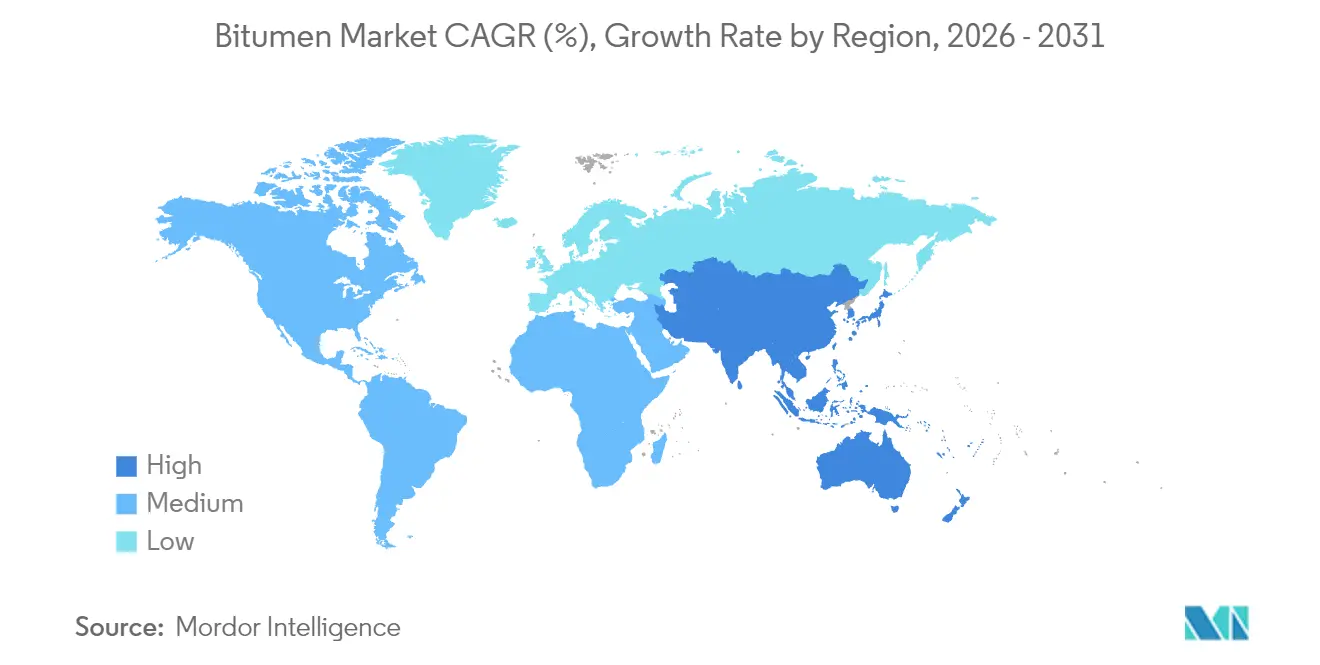

- By geography, Asia-Pacific led with 45.10% revenue share in 2025; the region is expanding at a 6.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bitumen Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing road and highway rehabilitation spend | +1.8% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Large-scale airport runway expansion programs | +0.7% | Global, particularly Middle East and Asia-Pacific hubs | Long term (≥ 4 years) |

| Government infrastructure stimulus in emerging economies | +1.2% | Asia-Pacific core, spill-over to Latin America and Africa | Short term (≤ 2 years) |

| Shift to polymer-modified bitumen for climate-resilient pavements | +0.9% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Circular-economy push for reclaimed asphalt pavement adoption | +0.6% | Europe and North America, gradual adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Road and Highway Rehabilitation Spend

Governments are reallocating budgets from new builds toward preservation, leading to steady recurrent consumption of penetration-grade binders and specialty surface treatments. The U.S. Infrastructure Investment and Jobs Act has already launched more than 60,000 construction projects, and Québec alone earmarked CAD 35.868 billion for roads in its 2025-2026 budget. Agencies recognize that every dollar invested in timely preservation avoids USD 4-7 in future reconstruction costs, locking in a virtuous cycle of maintenance demand. Germany’s EUR 500 billion modernization fund assigns 20% to asset optimization, embedding resilience criteria that further elevate specifications for climate-adaptive bitumen grades. As pavement management systems mature, procurement shifts from cyclical surges to predictable multi-year contracts, stabilizing volume offtake across the bitumen market.

Large-Scale Airport Runway Expansion Programs

Runway projects require premium binders that tolerate high wheel loads, shear stresses, and jet-fuel spills. Gulf and Asian hubs are leading a USD 730 billion capex wave through 2030, intertwining energy infrastructure with aviation build-outs. Frankfurt Airport’s two-year test strip using cashew-shell bio-bitumen illustrates airlines’ push for lower-carbon materials without performance sacrifice. Polymer-modified grades with styrene-butadiene-styrene command price premiums of 15-25%, lifting segment profitability even though volumes remain modest. Suppliers capable of certifying mix designs to International Civil Aviation Organization standards are positioned to capture long-run framework agreements, reinforcing vertical integration strategies within the bitumen market.

Government Infrastructure Stimulus in Emerging Economies

Strategic megaprojects in Asia-Pacific are tilting global trade flows. Indonesia’s National Strategic Projects scheme delivered 153 initiatives by 2022, creating procurement clusters that favor regional refiners with agile logistics. Gulf-Asia trade, projected at USD 682 billion by 2030, extends beyond hydrocarbons to include packaged polymer-modified binders, specialized emulsions, and rejuvenators[1]Asia House, “The Middle East Pivot to Asia 2024,” asiahouse.org . This interconnected landscape underpins Asia-Pacific’s leadership in the bitumen market and spurs investment in local upgrading facilities.

Shift to Polymer-Modified Bitumen for Climate-Resilient Pavements

Extreme temperature swings and heavier axle loads expose the limits of conventional binders. Field trials show Shell’s Cariphalte DM with 7% SBS triples fatigue life while reducing total lifecycle costs by 45%. Academic work indicates that 5% SBS optimizes elasticity, whereas 6% waterborne epoxy in micro-surface mixes boosts abrasion resistance under monsoon conditions. Public procurement increasingly stipulates performance-grade specifications, unlocking higher unit revenues and differentiating suppliers through formulation know-how. These advancements accelerate market segmentation within the bitumen market, creating premium subcategories that grow faster than base grades.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent GHG and PAH emission regulations on paving operations | -0.8% | Europe and North America, expanding globally | Short term (≤ 2 years) |

| Crude-oil price volatility impacting feedstock economics | -1.1% | Global, with acute effects in import-dependent regions | Medium term (2-4 years) |

| Rising share of concrete and composite pavements in urban projects | -0.4% | North America and Europe, selective adoption in Asia-Pacific urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent GHG and PAH Emission Regulations on Paving Operations

Regulators are tightening exposure limits for volatile organic compounds and polycyclic aromatic hydrocarbons. Canada will prohibit coal-tar sealants exceeding 1,000 ppm PAHs by October 2025, effectively removing a traditional product class and forcing reformulations[2]Canada Gazette, “Certain Products Containing Toxic Substances Regulations,” gazette.gc.ca. Predictive analytics using gas chromatography coupled with supervised learning now pinpoint odor-causing alkanes, offering compliance pathways but raising analytical costs that smaller producers must absorb. Agencies also favor warm-mix technologies that lower placement temperatures by up to 40 °C, reducing on-site emissions and tightening the operating envelope for hot-mix asphalt, thereby constraining volume expansion in the bitumen market.

Crude-Oil Price Volatility Impacting Feedstock Economics

The EIA forecasts Brent crude easing from USD 81 per barrel in 2024 to USD 66 in 2026, creating deflationary pressures on refinery netbacks. Refiners lacking downstream integration may shutter or convert units, as evidenced by multiple European closures slated for the next decade. OPEC+ production adjustments add uncertainty, complicating term supply contracts and inventory planning. Smaller regional suppliers face margin squeeze and potential capacity rationalization, heightening competitive intensity inside the bitumen market during commodity down-cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Penetration-Grade Dominance Drives Market Leadership

Penetration-grade binders held 66.52% of the bitumen market share in 2025 and are projected to grow at a 5.62% CAGR through 2031, sustained by compatibility with conventional hot-mix plants and broad climatic tolerance. Oxidized grades occupy niche waterproofing and roofing roles where oxidation stability justifies premium pricing. Bitumen emulsions, totaling 8 million tons globally, are gaining favor for chip seals and microsurfacing because they reduce energy use and lower work-zone emissions.

Innovation centers on viscosity control and ecological additives. Polyphosphoric acid at 1% dosage improves high-temperature stability, though concentrations beyond 2% can undermine storage stability. Bio-based modifiers such as Iranian natural asphalt enhance viscosity and thermoplasticity, extending service life and reducing reliance on synthetic polymers. These incremental gains sustain penetration-grade primacy but gradually shift value toward specialty formulations inside the bitumen market.

By Application: Road Construction Maintains Overwhelming Market Control

Road building consumed 84.45% of global volume in 2025 and is growing at a 5.56% CAGR, fueled by USD 9 trillion annual infrastructure spending targets. Preventive maintenance strategies have doubled lane-kilometer resurfacing frequencies in several North American states, embedding recurring demand for tack coats, rejuvenators, and micro-surfacing emulsions.

Roofing is driven by urbanization and building-code enhancements that demand higher wind uplift and insulation performance. Adhesives and sealants remain low-volume but high-margin segments due to tight performance specifications and limited supplier competition. Industrial uses span canal linings, tank pads, and ballast stabilization, representing less than 2% of the bitumen market yet offering customization opportunities.

Geography Analysis

Asia-Pacific led with 45.10% share in 2025 and is advancing at a 6.31% CAGR to 2031, anchored by synchronized infrastructure programs across China, India, and Southeast Asia. China’s processing of 14.8 million barrels per day of crude in 2023 underpins both domestic asphalt supply and export capabilities.

North America balances robust rehabilitation budgets with evolving environmental mandates. The IIJA pipeline stabilizes demand, but Canada’s impending PAH restrictions catalyze a shift to emulsions and cold processes. Europe confronts refinery rationalization; closures tighten regional supply yet open market space for bio-based alternatives. The bitumen market size in Europe could contract marginally in tonnage yet expand in value as specialty grades outpace generic ones.

The Middle East leverages abundant feedstock and strategic shipping lanes to supply Asia. Trade between Gulf producers and Asian buyers is forecast to touch USD 682 billion by 2030, with finished binders and modifiers joining crude flows.

Africa and South America remain emergent, characterized by episodic megaprojects that create demand surges. Suppliers attuned to flexible logistics and rapid deployment can gain traction as these regions scale connectivity investments.

Mordor Intelligence provides coverage of the bitumen market across other key regional markets, including Asia, Africa, and Europe, each with their regulatory frameworks and demand patterns.

Regulatory Landscape

Bitumen regulation is increasingly shaped by chemical safety oversight and road-agency sustainability requirements. In Europe, asphalt and bitumen substances fall under the EU REACH framework administered by the European Chemicals Agency (ECHA), which adds chemical identity and safety expectations alongside traditional binder test parameters. Separately, CEN published sustainability guidance for bitumens and bituminous binders (CEN/TR 18114:2025, adopted nationally via bodies such as SIS), supporting procurement language that links product selection to documented environmental performance.

At the project-delivery level, requirements are tightening around environmental documentation and emissions exposure controls. Transport Infrastructure Ireland (TII) requires an Environmental Product Declaration (EPD) for bituminous mixtures used on national roads, and the Dutch Environmental Database released PCR Asphalt 3.0 in July 2026 (effective January 1, 2027) to update calculation rules aligned with EN 15804+A2. In emerging markets, formal oversight is expanding, with Ghana's National Petroleum Authority inaugurating a 16-member Bitumen Technical Committee in June 2026 to develop a regulatory framework for quality, importation, and distribution, signaling a shift toward more standardized market access and enforcement.

Value Chain Analysis

The bitumen value chain starts with crude oil refining (and, in some regions, oil sands and oil shale), where bitumen is produced as a vacuum residue stream or as a refinery blendstock. It is then upgraded via blowing, blending, or modification. Downstream manufacturing covers penetration and viscosity grades as well as higher-value polymer-modified bitumen (PMB) and emulsions, which require additive supply, formulation control, and product certification. Distribution then runs through heated storage terminals, inland transport (road tankers, rail, and barges), and supply to asphalt mix plants and contractors serving road construction, roofing, waterproofing, and other industrial uses.

The main constraints are concentrated in logistics and infrastructure, including limited heated tank storage, terminal and port congestion, and forecasting mismatches that increase project-delivery risk when paving windows are narrow. Company actions in 2025 highlighted how distribution hubs and storage can reduce lead times, including OMV Petrom partnering to expand bitumen storage capacity in Galati and organizing PMB supply collaborations to shorten delivery cycles. More sustainability-linked partnerships are also showing up upstream of the contractor interface, including a November 2025 MoU by AIZO Group with K2 Bitumen to develop a green bitumen facility in Sarawak focused on crumb rubber modified bitumen, reflecting how performance and environmental requirements are pulling more value into modification and technical services.

Competitive Landscape

The bitumen market is moderately fragmented. Integrated majors such as ExxonMobil, Shell, BP, and TotalEnergies capitalize on refinery proximity and logistics scale to maintain cost leadership, even as they pivot toward petrochemicals and energy-transition assets. Technology-driven challengers are carving niches. Modern Hydrogen’s carbon-sequestered asphalt, backed by Bill Gates, claims 20% cost savings and lower lifecycle emissions, earning pilot approvals from multiple U.S. state DOTs. Volatile crude-oil margins encourage portfolio optimization and selective divestments rather than broad-based consolidation. Nevertheless, regional bolt-on acquisitions continue, exemplified by Canadian Natural Resources’ synthetic crude expansion through an asset purchase in late 2024.

Bitumen Industry Leaders

BP p.l.c.

Shell plc

TotalEnergies

China Petroleum and Chemical Corporation (Sinopec)

Exxon Mobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity is to build corridor-level supply resilience using port-based terminals, bulk dispatch systems, and regional storage, which de-risks deliveries for large road programs where import dependence is higher. In India, bulk bitumen dispatches began from Indian Oil Corporation's Pipavav bitumen cell in June 2026, operated by Amron Oil Resources (a JV of GP Petroleums and West Coast Oils LLP), reflecting buyer preference for dedicated logistics nodes that can support public-works demand with tighter lead times. Similar whitespace exists for suppliers that can pair storage with assured quality compliance and third-party testing, consistent with procurement that increasingly requests documented performance and traceability.

Product-side headroom is concentrated in higher-performance and lower-temperature systems that target durability and worksite emissions constraints, including PMB and CRMB capacity, emulsions for maintenance treatments, and recycled-asphalt enabling additives and processes. Equipment and project activity supports this shift, including high-capacity PMB plant deployments for Vietnam's North-South Expressway (Feiteng, April 2026), which shows how megaproject schedules can draw in localized modification capability. Sustainability is also becoming more specification-driven through EPD/PCR frameworks in parts of Europe and through green-construction specifications such as Inner Mongolia's DB15/T 4260-2026, creating commercial space for producers that can deliver binder-plus-data packages (verified environmental declarations, mix design support, and recycling-compatible formulations) rather than commodity-only volumes.

Recent Industry Developments

- June 2026: Bharat Petroleum Corporation Limited (BPCL) signed a joint venture and share subscription agreement to acquire a 40% equity stake in Tiki Tar and Shell India Private Limited (TTSIPL) for INR 85 crore. The agreement strengthens BPCL's position in value-added bitumen solutions and expands access to established capabilities and channels for advanced binders aligned with road durability needs.

- June 2026: Indian Oil Corporation flagged off the first bulk bitumen dispatch from the Pipavav Bitumen Cell in Gujarat, operated by Amron Oil Resources (a joint venture involving GP Petroleums) under the SPRINT 2026 Mission Excellence initiative. The port-linked dispatch model improves supply reliability for large road programs by combining import and storage infrastructure with dedicated distribution execution.

- December 2024: Mangalore Refinery and Petrochemicals Limited commissioned a 150,000-ton bitumen unit using Biturox technology, doubling its bitumen capacity to serve India's highway demand. The upgrade expands regional availability of paving-grade material and increases competitive pressure on suppliers relying on longer-haul sourcing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the bitumen market covers supply of petroleum-based bitumen sold into paving and non-paving construction uses (such as roads, roofing, and waterproofing) across major regions, counted at the point of product sale.

Scope exclusions: natural asphalt and other non-petroleum binders, along with on-site paving labor and road construction services, are not counted as part of this market.

Segmentation Overview

- By Product Type

- Penetration Grade

- Oxidized Grade

- Bitumen Emulsions

- Polymer-Modified Bitumen

- Other Products (Viscosity Grade, Cutback, and Performance Grade)

- By Application

- Road Construction

- Roofing

- Adhesives and Sealants

- Other Applications (Coatings in Sectors such as Oil and Gas, Canal Lining, Tank Foundation, Railway Ballast Treatment, and Others)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to frame the demand pool and keep the assumptions grounded before forecasting. The approach relied on public sources such as national road statistics and government infrastructure budgets (for lane-km additions and resurfacing plans), energy and refinery indicators from agencies like the IEA and EIA, and trade data from UN Comtrade for asphaltic material flows.

To connect demand with supply, we also reviewed publications from road and asphalt associations, standards bodies that track paving grades and performance requirements, and peer-reviewed journals covering asphalt mix design and recycling trends. Company annual reports, investor presentations, and refinery updates were used to understand capacity and product mix changes. For selective cross-checks in key markets, we used a paid subscription for company financials and an import or export shipment-level database to confirm directionality. The sources listed here are illustrative and not exhaustive, and additional references were used for collection, validation, and research clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to validate gaps that desk sources rarely quantify well, especially the paving versus non-paving split, grade shifts (penetration grade, emulsions, polymer-modified), and how price pass-through behaves through distribution channels. We spoke with participants across production and distribution, asphalt mix producers, contractors, and public or private buyers, and kept the respondent mix balanced across APAC, EMEA, and the Americas so regional seasonality and specification differences were captured.

These discussions were also used to confirm binder-intensity assumptions, check trade-flow interpretations, and pressure-test the timing of tender cycles and inventory movements that can shift annual consumption.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 16% | APAC: 47% |

| Mid tier: 43% | Functional/Unit leaders: 25% | EMEA: 33% |

| Smaller Players: 19% | Managers: 59% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand reconstruction, where roadwork activity and infrastructure budgets are translated into asphalt mix volumes, then into binder demand using typical binder content ranges and local specification norms. The model keeps volume and price logic separate and recombines them after cross-checks, since crude-linked volatility can distort value trends.

Key inputs include road construction and resurfacing intensity (lane-km, project pipeline, and tender calendars), refinery throughput and yield signals, import and export movement patterns, product mix trends across penetration grade, emulsions, and polymer-modified grades, and crude and fuel price movements that influence bitumen pricing. Forecasting uses scenario analysis reflecting expected infrastructure funding cycles and grade adoption, followed by smoothing to reduce one-off swings from monsoons, winter paving stoppages, and temporary inventory builds.

Results were corroborated with selective bottom-up approximations such as sampled country consumption (volume multiplied by an average realized price range) and supplier plus channel checks where coverage is available. Where smaller markets lacked continuous data, proxy ratios were applied using road network size and paving intensity, and the assumptions were re-tested with regional interview feedback before finalizing totals.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, including road spending direction, refinery operating rates, and trade balance movements, to flag overstatement in either volume growth or price progression. Outliers were reviewed at country and regional levels, and if a variance could not be explained by seasonality, regulation, or a known project cycle, the underlying assumption was revised and checked again.

Before sign-off, the model goes through multi-step analyst reviews, including calculation checks and logic checks against prior years and known market events. Reports are refreshed annually, with interim updates triggered when major policy shifts, refinery outages, or large infrastructure packages materially change demand expectations. Right before delivery, an analyst completes a final pass so clients receive the latest updated view.

Mordor Intelligence's Bitumen Market Size Measured Against Other Published Estimates

Published bitumen market sizes often differ because some sources report value in USD and others report physical volume, and the two do not move in the same way when feedstock prices change quickly. Another recurring driver is what gets counted as bitumen, since some totals fold in adjacent asphalt or roofing material categories that are not labeled consistently across countries.

The biggest gaps usually come from price handling (annual average pricing versus point-in-time pricing), differences in how paving grades, emulsions, and polymer-modified grades are grouped, and whether roadworks activity is used as the anchor demand signal. When the market is built from resurfacing and new-build activity and then reconciled to refinery and trade indicators, the year-to-year pattern tends to be steadier, which is why roadwork-driven tonnage checks sit at the center of the model used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 140.90 M (2026) | |

| Industry Publisher A | USD 73.35 B (2024) | This estimate is value-based and depends heavily on the assumed average selling price, which can swing with crude-linked movements and regional pricing lags. It also uses a different base year and can combine broader downstream uses into one value number, which makes reconciliation to binder demand in tons difficult. |

| Industry Publisher B | USD 75.30 B (2024) | This figure is also reported as global value and may apply broad growth rates across regions and types, which can overstate value growth when paving grades dominate and prices normalize. Differences can also come from how waterproofing and specialty grades are grouped and how currency conversion timing is treated across countries. |

Overall, the spread is explained more by unit choice and pricing conventions than by a single disagreement on end-use demand. By keeping the demand pool tied to roadworks intensity and product-grade mix first, and then layering pricing with cross-checks, the estimate remains traceable to clear drivers and repeatable steps.

Key Questions Answered in the Report

How large is the bitumen market in 2026?

The sector reached 140.9 million tons in 2026 and is forecast to expand to 181.37 million tons by 2031.

Which region leads demand for paving-grade bitumen?

Asia-Pacific holds 45.10% of global consumption thanks to aggressive infrastructure spending and flexible import options.

How will crude-oil prices influence bitumen economics?

The EIA projects Brent crude easing to USD 66 per barrel by 2026, which could widen production margins but heighten competition.

Which regulations most affect the sector near-term?

Canada's 2025 ban on high-PAH coal-tar sealants exemplifies tightening GHG and toxicity controls that push demand toward low-emission formulations.

Are recycled asphalt solutions gaining traction?

Yes. Government incentives and cost savings are accelerating reclaimed asphalt pavement adoption, especially in North America and Europe.

Page last updated on: