Europe Bitumen Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

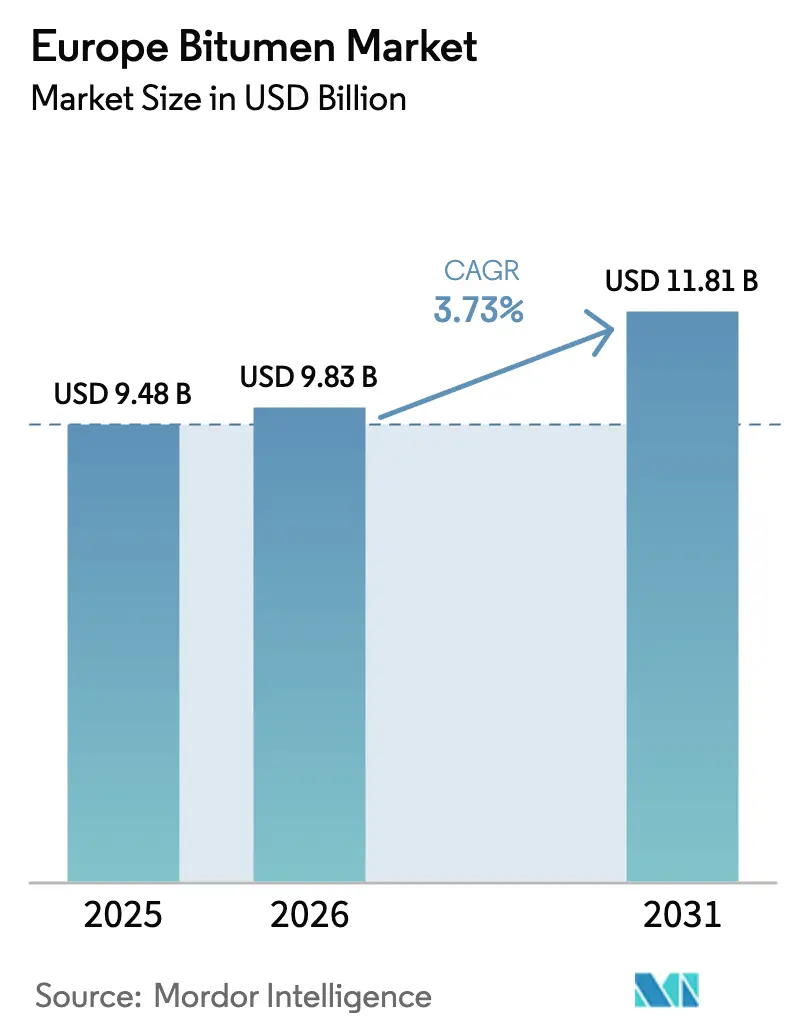

| Base Year Market Size (2025) | USD 9.48 Billion |

| Market Size (2026) | USD 9.83 Billion |

| Market Size (2031) | USD 11.81 Billion |

| Growth Rate (2026 - 2031) | 3.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Bitumen Market Analysis by Mordor Intelligence

Europe Bitumen Market size in 2026 is estimated at USD 9.83 billion, growing from 2025 value of USD 9.48 billion with 2031 projections showing USD 11.81 billion, growing at 3.73% CAGR over 2026-2031. This steady expansion is anchored in record public‐works allocations, accelerating polymer-modified binder adoption, and supply-chain realignment that channels Mediterranean refinery surpluses into Northwest Europe at lower freight cost. Warm-mix asphalt technologies are scaling quickly, helping plant operators curb energy use and comply with Fit-for-55 carbon limits. Builders of zero-energy commercial facilities are specifying premium SBS-modified membranes, while freight growth drives heavier truck loads that favor high-performance pavements. The Europe bitumen market also benefits from cohesive EN-series standards that harmonize product quality, yet it must navigate tightening emission caps and the encroachment of concrete alternatives in long-life motorway projects.

Key Report Takeaways

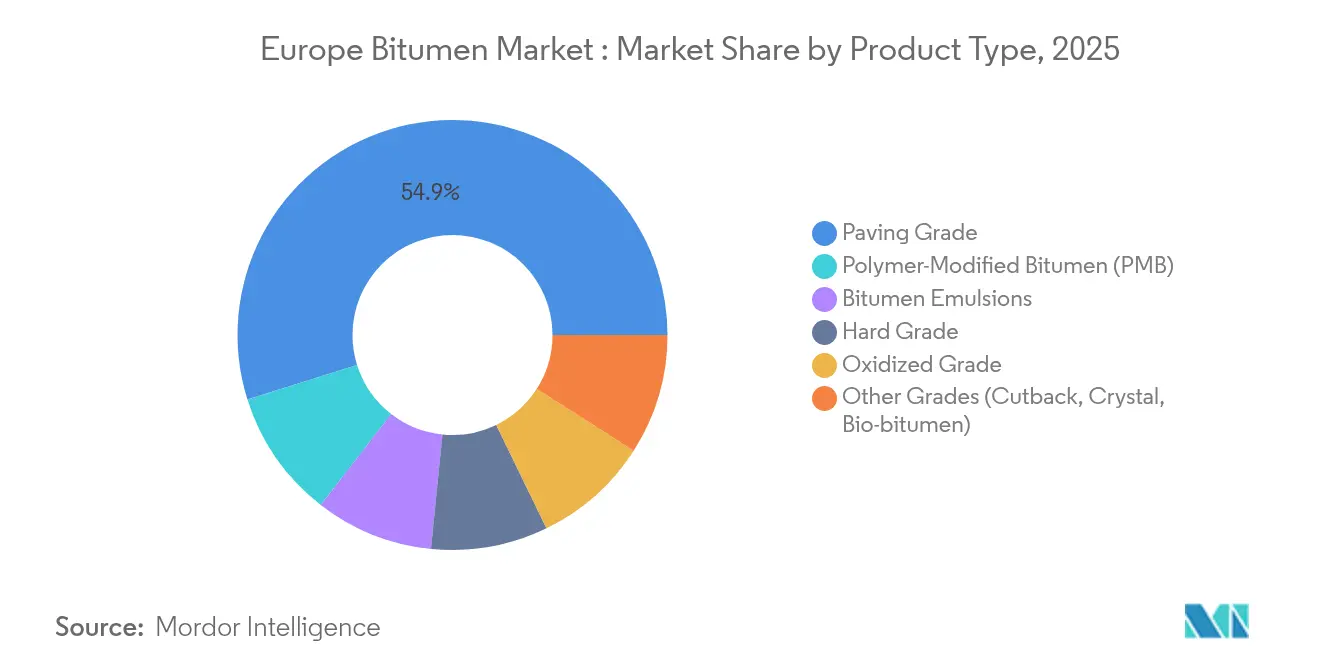

- By product type, paving grade held 54.85% of the Europe bitumen market share in 2025, while polymer-modified bitumen is projected to grow at a 4.27% CAGR through 2031.

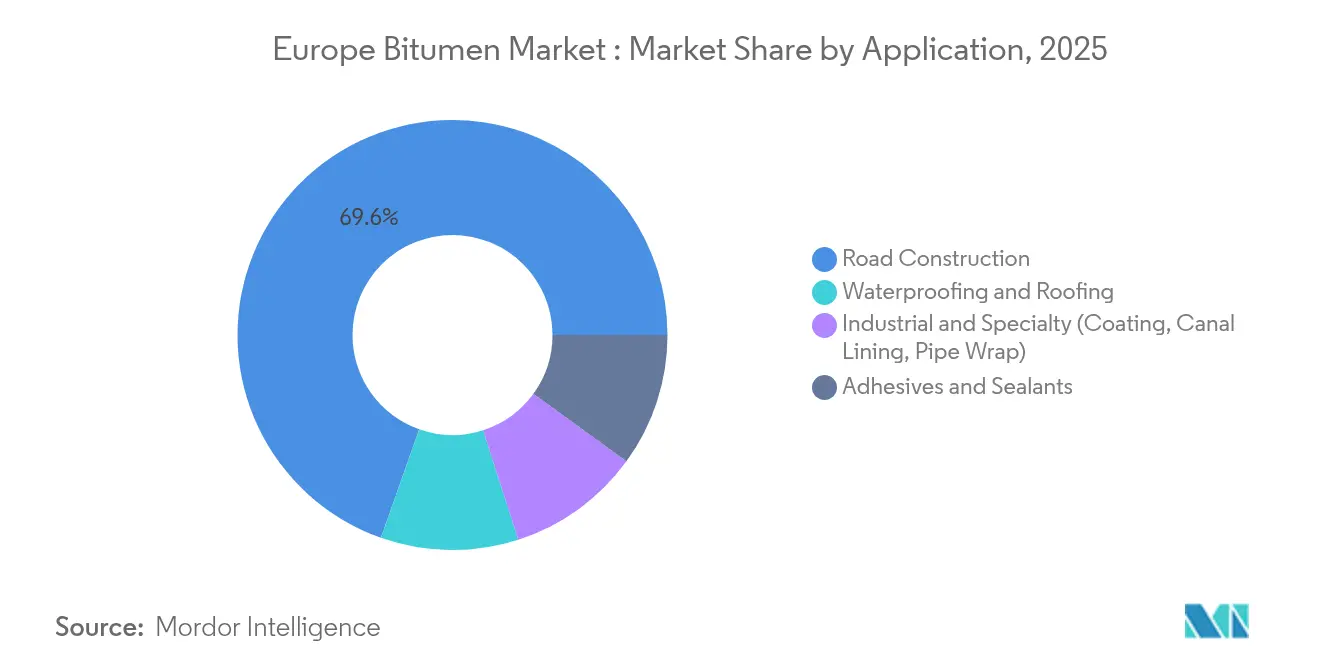

- By application, road construction accounted for 69.60% of the Europe bitumen market size in 2025, while waterproofing and roofing is advancing at a 4.05% CAGR.

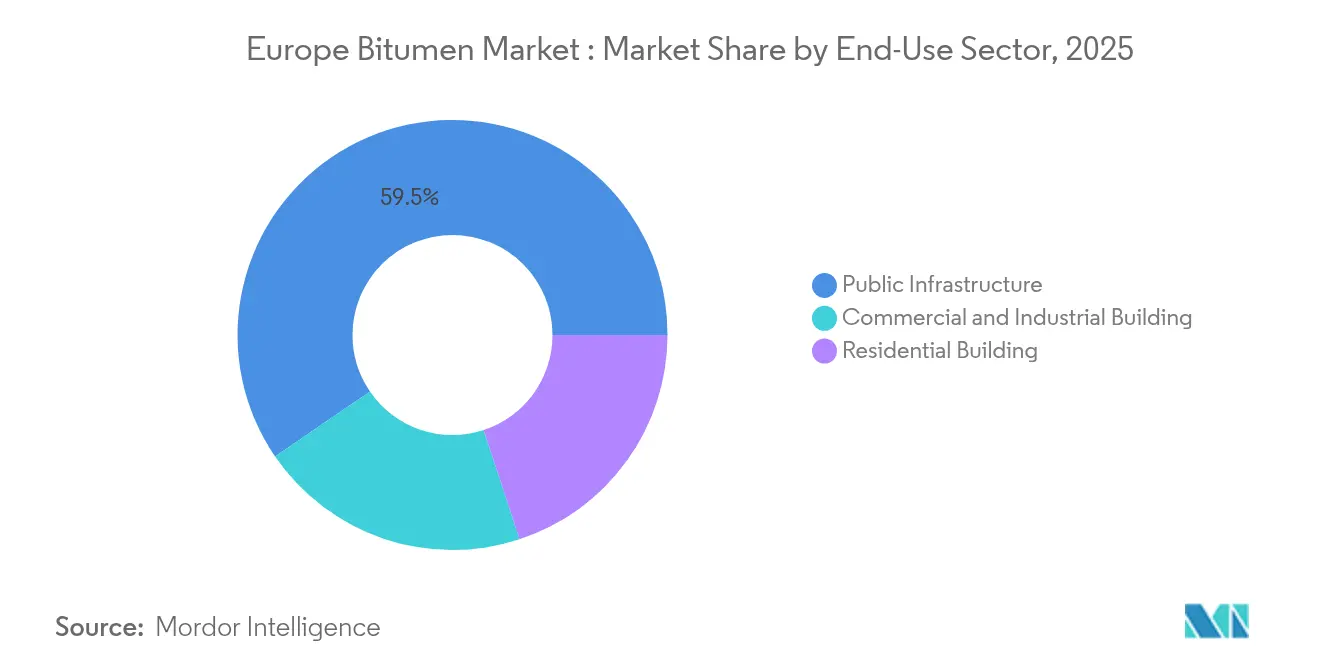

- By end-use sector, public infrastructure commanded 59.55% of 2025 demand; commercial and industrial building is forecast to expand at a 3.88% CAGR.

- By geography, Germany led with an 18.05% Europe bitumen market share in 2025, whereas Central and Eastern Europe is set to post a 3.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple regions, with Europe forming one of the important contributors. Mordor Intelligence's global bitumen market size report represents that cumulative total.

Europe Bitumen Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Road-Rehabilitation and Greenfield Highway Spending Across EU-27 | +1.2% | EU-27 wide, concentrated in Germany, France, Italy | Medium term (2-4 years) |

| Accelerating Adoption of Polymer-Modified Binders for Heavier Truck Loads | +0.8% | Western Europe, expanding to Central Europe | Short term (≤ 2 years) |

| Surging Demand for Premium Waterproofing Membranes in Zero-Energy Buildings | +0.6% | Nordic countries, Germany, Netherlands | Long term (≥ 4 years) |

| Mediterranean Surplus Filling Supply Gap After Russia Ban, Lowering NW Europe Costs | +0.7% | Northwestern Europe, Mediterranean basin | Short term (≤ 2 years) |

| Rapid Shift Toward Warm-Mix Asphalt (WMA) to Meet Fit-For-55 Decarbonisation Targets | +0.5% | EU-27 wide, early adoption in Scandinavia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Road-Rehabilitation and Greenfield Highway Spending Across EU-27

EU transport authorities earmarked EUR 7 billion (USD 7.7 billion) in 2024 for road modernization, with Germany alone spending EUR 2.8 billion (USD 3.08 billion) each year on motorway upgrades[1]European Commission, “Connecting Europe Facility Transport Calls 2024,” europa.eu . Mandates embedded in the revised TEN-T regulation stretch demand visibility to 2050. Tender specifications increasingly call for polymer-modified binders that lengthen maintenance cycles, reinforcing premiumization trends across the Europe bitumen market. Contractors benefit from certainty in multi-year spending plans that lock in baseline tonnage requirements and tilt procurement toward suppliers with robust logistics footprints.

Accelerating Adoption of Polymer-Modified Binders for Heavier Truck Loads

Freight tonnage jumped 23% since 2019 and axle weights now approach the 44-ton limit along major corridors, prompting road agencies to specify SBS-modified binders known to raise rutting resistance by 30-40%. Field trials confirm service‐life gains of up to 80% relative to conventional paving grade, validating price premiums that average 15–20%. EN 14023 provides a harmonized performance benchmark, while Germany and France codify mandatory PMB use on motorways exceeding 10,000 vehicles daily. This structural shift underpins the fastest expansion track for polymer-modified products within the Europe bitumen market.

Surging Demand for Premium Waterproofing Membranes in Zero-Energy Buildings

Nearly zero-energy building rules under the Energy Performance of Buildings Directive elevate moisture-barrier specifications. Kingspan’s roofing and waterproofing revenue reached EUR 568.5 million (USD 625.35 million) in 2024 and rose 15% year-on-year, while its EUR 1.2 billion (USD 1.32 billion) purchase of Nordic Waterproofing amplifies supply scale. SBS-modified sheets offer superior flexibility in sub-zero Nordic climates, pushing premium membranes deeper into the specification stack. The Europe bitumen market therefore tilts toward high-margin downstream systems where quality assurance and integrated insulation packages command pricing power.

Mediterranean Surplus Filling Supply Gap After Russia Ban, Lowering NW Europe Costs

Sanctions erased roughly 2 million tonnes of Russian imports, but Italian and Spanish refineries backfilled volumes while trimming haulage distances into Germany, the Netherlands, and Belgium. Freight savings of 25–30% now underpin more stable delivered pricing, decreasing volatility that previously plagued the Europe bitumen market. TotalEnergies aligned its European refining slate around regional logistics, and Shell redirected its Wesseling site toward higher-value base oils, collectively tightening supply yet refining cost curves in favor of Mediterranean output.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened CO₂ / PAH Emission Regulations on Asphalt Plants | -0.4% | EU-27 wide, strictest in Nordic countries | Medium term (2-4 years) |

| Concrete and Composite Pavements Winning Share in Long-Life Motorway Projects | -0.3% | Germany, Austria, Netherlands | Long term (≥ 4 years) |

| Antitrust Fines on Regional Emulsion Cartels Inflating Compliance Costs | -0.2% | Germany, Italy, Austria | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened CO₂ / PAH Emission Regulations on Asphalt Plants

The revised Industrial Emissions Directive ratcheted PAH limits down 40% and expanded CO₂ reporting duties. Operators estimate EUR 2-5 million (USD 2.2-5.5 million) per facility for oxidation and filtration retrofits[2]U.S. EPA, “Cost Guidelines for Hot-Mix Asphalt Plant Emission Controls,” epa.gov . Smaller batch plants may struggle to fund upgrades, trimming available capacity and pushing some producers out of the Europe bitumen market. Early movers with best-available-technology status leverage compliance as a competitive moat and capture carbon-conscious tender lots.

Concrete and Composite Pavements Winning Share in Long-Life Motorway Projects

Lifecycle studies indicate 5–35% cost savings over 40 years for concrete surfaces, particularly on steep Alpine grades that punish flexible pavements. Austria now lays concrete on two-thirds of new motorways, while Germany pushes the material to 25% share. Composite solutions that marry concrete bases with asphalt toppers stretch service intervals beyond 30 years, diverting part of the Europe bitumen market toward alternative materials where durability trumps up-front cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PMB Commands Premium Growth Despite Paving Grade Dominance

Polymer-modified bitumen underpins the fastest trajectory, charting a 4.27% CAGR through 2031, although conventional paving grade still accounts for 54.85% of the Europe bitumen market share in 2025. Premiumization accelerates because freight corridors demand binders that postpone rutting and fatigue, while EN 14023 assures buyers of cross-border consistency. The Europe bitumen market size tied to PMB climbed in tandem with logistics efficiencies that shorten lead times from Mediterranean hubs. Suppliers with integrated SBS and crumb-rubber modification capacity therefore record superior order backlogs.

Bio-bitumen innovations ride on the warm-mix wave. Lignin substitution rates near 5% in half-warm mixes, and used-cooking-oil epoxidation trials produce binders that hit durability targets. Hard and oxidized grades remain niche yet critical for industrial coatings and waterproofing mats. Bitumen emulsions find relevance in cold recycling and spray seals, especially where road agencies lift reclaimed asphalt pavement (RAP) thresholds to 50%. The Europe bitumen industry thus stretches its product ladder to capture both sustainability and performance premiums.

By Application: Waterproofing Gains Momentum Beyond Road Construction Dominance

Road construction still consumes 69.60% of demand, yet waterproofing and roofing is projected to grow at 4.05% CAGR as zero-energy codes shift value downstream. Rising warehouse construction injects volume into adhesive flashings and SBS cap sheets. Kingspan’s membrane revenues illustrate the commercial pull of high-spec roofs, signaling an addressable sub-sector that outpaces the broader Europe bitumen market.

Industrial coatings and pipe wraps cling to their niche but stable slot. Adhesives and sealants gain from modular building systems that favor bitumen‐based sound attenuation mats. Public subsidy programs for building envelopes amplify retrofit activity, keeping waterproofing lines fully booked. As a result, the Europe bitumen market size dedicated to building solutions is widening relative to its historical baseline, balancing infrastructure cyclicality.

By End-Use Sector: Commercial Building Segment Accelerates Despite Public Infrastructure Leadership

Public infrastructure remains the anchor at 59.55% for 2025, buoyed by an EU road budget that hit USD 7.7 billion. Still, warehousing and logistics hubs in Poland, Czechia, and Hungary are propelling commercial consumption at a 3.88% CAGR. Investors racing to serve same-day e-commerce delivery fit large roofs with reflective waterproofing membranes, intensifying private-sector pull on the Europe bitumen market.

Residential construction faces higher mortgage rates, yet roof retrofit subsidies keep shingles and torch-on sheets moving through distribution. Industrial facilities reshape floor layouts to accommodate robotics, raising requirements for chemical-resistant bituminous screeds. This differential growth pattern forces producers to calibrate batch runs toward smaller-lot specialty grades alongside bulk road binders, adding flexibility to the Europe bitumen industry production mix.

Geography Analysis

Germany anchors the Europe bitumen market with an 18.05% share in 2025, driven by USD 3.08 billion annual motorway allocations and stringent PMB norms for high-traffic lanes. Concrete accounts for a quarter of German motorways, yet bitumen maintains leadership through lifecycle optimized overlay strategies. Antitrust fines totaling USD 11.55 million underscore regulatory vigilance and raise compliance thresholds for local contractors.

Central and Eastern Europe advances at a 3.95% CAGR, powered by cohesion funds funneled into Polish expressways, Czech ring roads, and Hungarian industrial parks. Warehouse clusters around Łódź and Katowice translate directly into waterproofing demand, while newly upgraded asphalt plants in Slovakia adopt warm-mix equipment to comply with EU emission ceilings. This region captures increasing slices of the Europe bitumen market size as infrastructure parity with Western Europe tightens.

Italy leverages Mediterranean surplus to offset lost Russian cargoes, lowering delivered costs into Lombardy projects. France maintains steady growth on the back of its USD 16.5 billion five-year infrastructure plan. The United Kingdom adjusts supply chains post-Brexit but preserves volumes through motorway asset management contracts. Spain benefits from EU recovery grants, and Nordic states pioneer lignin-modified binders that dovetail with their bioeconomy strategies. Collectively, these dynamics reinforce diversified demand pillars that stabilize the Europe bitumen market against single-country shocks.

Coverage of the bitumen market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Asia and Africa.

Competitive Landscape

The producer roster is headlined by integrated majors—TotalEnergies, Shell, and BP—flanked by specialists such as Nynas AB and Bitumina Group. Combined, the top five suppliers control roughly 45% of regional volume, positioning the Europe bitumen market in the moderately concentrated tier. BP is divesting its 12 million-tonne Gelsenkirchen refinery, and Shell transitioned Wesseling into a 300 000-tonne base-oils hub, shifts that squeeze commodity output while lifting margins on upgraded products.

Kingspan’s EUR 1.32 billion Nordic Waterproofing deal crystallizes downstream consolidation where branded membranes out-earn generic binders. Specialty polymer houses such as Kraton and Sika use proprietary SBS and reactive elastomer chemistries to lock in sticky supply agreements with toll blenders. Warm-mix additives and bio-bitumen modifiers emerge as battlegrounds for intellectual property, evidenced by a surge in EU patent filings throughout 2025.

Compliance capability is increasingly a differentiator. Plants fitted with regenerative thermal oxidizers meet PAH rules ahead of schedule, winning procurement bonuses from Scandinavian agencies. Producers failing to retrofit face curtailed operating permits, effectively ceding share to compliant rivals. These strategic pivots collectively re-shape competition and raise the overall sophistication of the Europe bitumen industry.

Europe Bitumen Industry Leaders

Exxon Mobil Corporation

Nynas AB

Shell plc

TotalEnergies

BP Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SAT Reabilitare Reciclare, a subsidiary of Austrian construction group Strabag SE, established Romania's largest bitumen emulsion plant in the northwestern commune of Criseni, Salaj county. The facility, built with an investment of EUR 2.2 million (USD 2.5 million), has a production capacity of 15 tonnes per hour.

- January 2024: Shell converted its Wesseling refinery in Germany into a base oils production facility with an annual capacity of 300,000 tonnes. This transformation reduced the regional bitumen production capacity, creating a supply deficit in the European market and increasing the likelihood of higher import volumes from neighboring regions.

Europe Bitumen Market Report Scope

Bitumen is a black or dark brown non-crystalline soil or viscous material having adhesive properties. It is derived from petroleum crude either naturally or through refinery processes. Bitumen is commonly used as a binder in constructing roads, runways, and platforms and for waterproofing and adhesive applications in residential and commercial construction.

The Europe Bitumen Market is segmented by product type, application, and geography. The market is segmented by product type into paving grade, hard grade, oxidized grade, bitumen emulsions, polymer-modified bitumen, and other product types (cutback bitumen and crystal bitumen). The market is segmented by application into road construction, waterproofing, adhesives, and other applications (coating and canal lining).

The report also covers the market size and forecasts for the Europe bitumen market in 6 countries across the European region. The market sizes and forecasts are provided in volume (tons) for each segment.

| Paving Grade |

| Hard Grade |

| Oxidized Grade |

| Bitumen Emulsions |

| Polymer-Modified Bitumen (PMB) |

| Other Grades (Cutback, Crystal, Bio-bitumen) |

| Road Construction |

| Waterproofing and Roofing |

| Adhesives and Sealants |

| Industrial and Specialty (Coating, Canal Lining, Pipe Wrap) |

| Public Infrastructure |

| Residential Building |

| Commercial and Industrial Building |

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| NORDIC Countries |

| Central and Eastern Europe |

| Rest of Europe |

| By Product Type | Paving Grade |

| Hard Grade | |

| Oxidized Grade | |

| Bitumen Emulsions | |

| Polymer-Modified Bitumen (PMB) | |

| Other Grades (Cutback, Crystal, Bio-bitumen) | |

| By Application | Road Construction |

| Waterproofing and Roofing | |

| Adhesives and Sealants | |

| Industrial and Specialty (Coating, Canal Lining, Pipe Wrap) | |

| By End-Use Sector | Public Infrastructure |

| Residential Building | |

| Commercial and Industrial Building | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| NORDIC Countries | |

| Central and Eastern Europe | |

| Rest of Europe |

Key Questions Answered in the Report

How large is Europe’s bitumen demand today and where is it heading by 2031?

Value reached USD 9.83 billion in 2026 and is projected to climb to USD 11.81 billion by 2031, implying a 3.73% CAGR.

Which bitumen product type is expanding fastest across Europe?

Polymer-modified bitumen leads with a 4.27% CAGR, driven by heavier truck loads and stricter pavement durability standards.

What role do Mediterranean refineries play in supplying Northwest European bitumen?

Additional output from Italian and Spanish plants replaces lost Russian volumes and cuts freight costs into Germany, the Netherlands, and Belgium by up to 30%.

Why are European highway agencies switching to polymer-modified binders?

SBS-modified mixes boost rutting resistance and can extend pavement life 60–80%, offsetting their 15–20% price premium.

Page last updated on: