Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

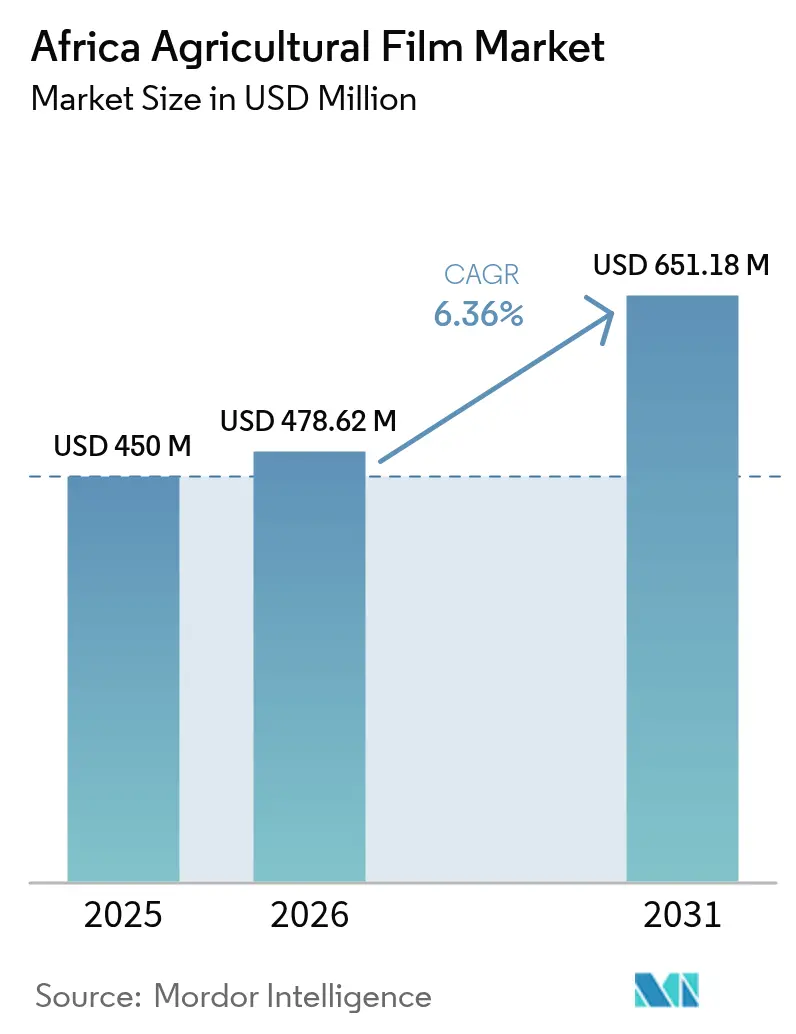

| Base Year Market Size (2025) | USD 450.0 Million |

| Market Size (2026) | USD 478.62 Million |

| Market Size (2031) | USD 651.18 Million |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Africa Agricultural Film Market Analysis by Mordor Intelligence

The Africa agricultural film market size is expected to grow from USD 450.0 million in 2025 to USD 478.62 million in 2026 and is forecast to reach USD 651.18 million by 2031 at 6.36% CAGR over 2026-2031. The market growth is driven by agricultural mechanization, increasing protected cultivation area, and expanded government subsidies supporting both smallholder and commercial farms. South Africa dominates the market with established distribution networks, while Morocco shows the highest growth rate due to greenhouse expansion and export-focused agriculture. The market sees increased demand for advanced products, including multilayer, anti-drip, and recycled-content films. The introduction of biodegradable films compliant with EN17033 standards is influencing material selection. Challenges such as counterfeit products, volatile polymer prices, and inadequate recycling infrastructure affect market growth, though these factors have not significantly impacted the overall agricultural modernization trend.

Key Report Takeaways

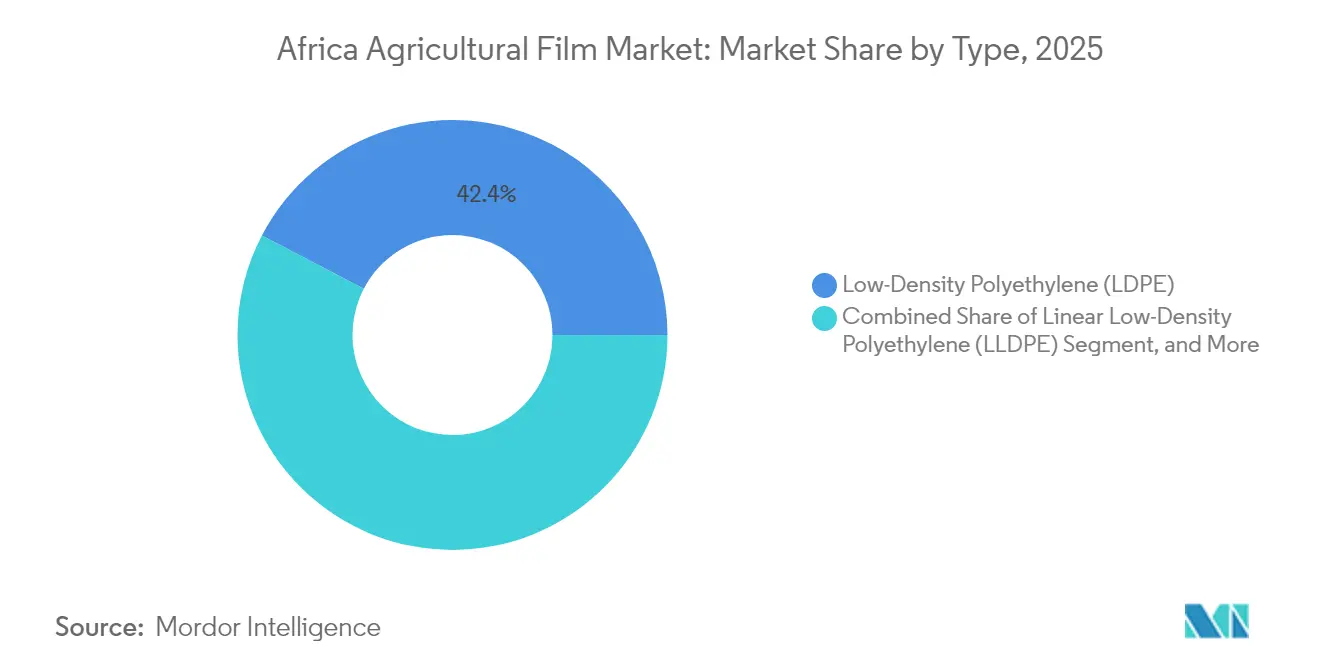

- By type, Low-density Polyethylene (LDPE) accounted for 42.35% of the Africa agricultural film market share in 2025, while biodegradable films registered the highest 10.12% CAGR through 2031.

- By application, mulching captured 44.60% of the Africa agricultural film market size in 2025, while greenhouse films are advancing at a 8.95% CAGR toward 2031.

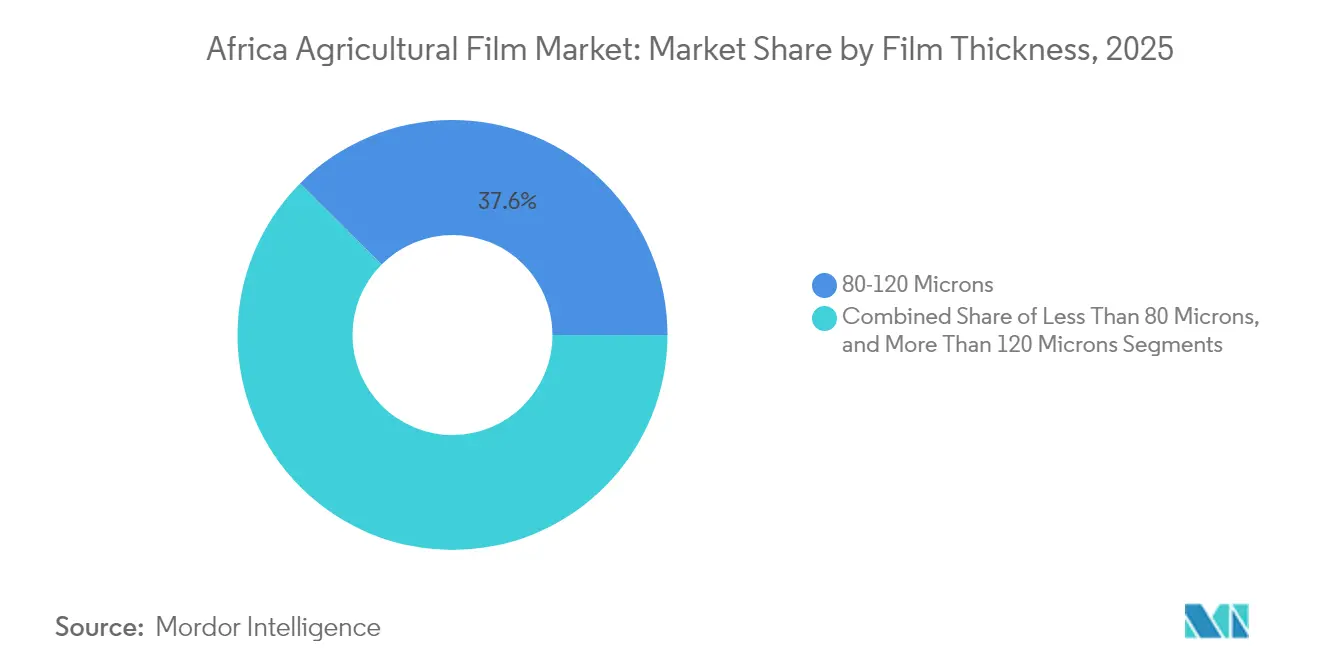

- By film thickness, products with a thickness of 80–120 microns held 37.55% of the market size in 2025, while films with a thickness of less than 80 microns represented the fastest-growing segment at a 10.24% CAGR.

- By geography, South Africa led with a 34.85% market share in 2025, while Morocco is forecast to post the fastest 8.32% CAGR through 2031.

- Berry Global, Inc., Armando Alvarez S.A., Ginegar Plastic Products Ltd., BASF SE, and Mondi PLC, collectively holding 50.12% of the market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Agricultural Film Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raising food demand and need for higher farm productivity | +1.2% | Nigeria, Ethiopia, and Egypt | Medium term (2-4 years) |

| Surging greenhouse cultivation acreage across Africa | +0.9% | Morocco, South Africa, and Kenya | Long term (≥ 4 years) |

| Product innovations in multilayer films and anti-drip additives | +0.7% | South Africa, and Morocco | Medium term (2-4 years) |

| Government subsidies on agricultural film | +0.8% | Uganda, Ghana, and Kenya | Short term (≤ 2 years) |

| Rapid expansion of horticulture export clusters | +0.6% | Morocco, South Africa, and Kenya | Long term (≥ 4 years) |

| Emergence of biodegradable and compostable film standards | +0.5% | South Africa, Morocco, and Kenya | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raising Food Demand and Need for Higher Farm Productivity

In Africa, cereals are staple foods, with maize, wheat, and rice being the most important, and maize leading in consumption. Maize constitutes the primary daily subsistence need for most Kenyans[1]Source: Agriculture and Food Authority, Kenya, "Cereals – Food Directorate", afa.go.ke. While Africa's cereal consumption continues to rise, production remains significantly lower, widening the import gap and increasing the demand for yield-boosting technologies such as mulch and greenhouse covers. The third Comprehensive African Agriculture Development Programme (CAADP) roadmap aligns continental policies to prioritize productivity tools that reduce water stress and shorten growth cycles[2]Source: World Organisation for Animal Health Africa, “AU adopts third CAADP roadmap,” rr-africa.oie.int. Ethiopia's achievement of wheat self-sufficiency, which eliminated USD 1 billion in imports, has encouraged similar adoption programs in Zambia and Mozambique. Agricultural films enhance soil moisture retention and canopy microclimate, enabling farmers to overcome yield deficits during unpredictable weather conditions. This ongoing supply-demand gap establishes agricultural films as essential inputs across food-insecure regions.

Surging Greenhouse Cultivation Acreage Across Africa

Morocco operates 40,000 hectares of greenhouses, producing 2 million metric tons of horticultural output, demonstrating the transition to protected cultivation. Technology partnerships between Dutch and Moroccan companies provide diffusive polyethylene covers that improve yield and water-use efficiency. Research in similar arid regions indicates cucumber yields of 12.3 kg/m² under optimized diffusive films, confirming the agricultural benefits of specialized covers. Kenya and South Africa implement comparable greenhouse systems, driven by the need to adapt to increasing rainfall variability. The expansion of greenhouse area maintains consistent demand for UV-stable, thermally insulated, and high-light-transmission films.

Product Innovations in Multilayer Films and Anti-Drip Additives

Agricultural film manufacturers are developing three- to five-layer structures that incorporate anti-fog, IR, and hydrophobic additives while maintaining mechanical strength. Berry Global increased post-consumer-recycled polyethylene content in its agricultural products by 36% in 2024, showing the viability of large-scale recycling. Films containing stearic-acid-coated sand particles demonstrate enhanced water repellency, helping retain soil moisture for up to four additional days in field tests. The incorporation of biodegradable materials like polyhydroxyalkanoates meets EN17033 standards, reducing film removal costs for farmers. These technological improvements reduce replacement frequency and increase per-hectare productivity, supporting growth in the Africa agricultural film market.

Government Subsidies on Agricultural Film

The National Agricultural Advisory Services program in Uganda and Ghana's mechanization initiatives provide subsidies for agricultural inputs, including greenhouse films, to enhance smallholder farmer access. Kenya's 2025 Finance Bill discussions have highlighted the significance of agricultural inputs, particularly regarding VAT exemptions. The World Bank advocates redirecting fertilizer subsidies toward agricultural innovation and infrastructure development, encompassing protected cultivation systems[3]Source: The World Bank Group, "Getting agriculture policies right is key for the future of food in Africa", worldbank.org. These subsidy programs enable regional film converters to maintain consistent production volumes through established demand patterns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit low-grade films flooding informal markets | -0.8% | Nigeria, Kenya, and Ghana | Short term (≤ 2 years) |

| Low farmer awareness and limited technical training on proper film use | -0.6% | Rural Sub-Saharan Africa | Medium term (2-4 years) |

| Volatility in crude-derived polymer feedstock prices | -0.9% | Import-dependent economies | Short term (≤ 2 years) |

| Sub-scale local recycling infrastructure | -0.4% | Continent-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit Low-Grade Films Flooding Informal Markets

The presence of informal trading routes enables significant volumes of low-quality agricultural films to enter Nigeria and Kenya. This influx of substandard products reduces farmer trust in film effectiveness and damages established brand value. Studies of Nigeria's plastics market indicate persistent regulatory gaps that enable uncertified imports to circumvent quality control measures. The rapid degradation of counterfeit films leads to crop losses, which discourages farmers from making future purchases and limits the sales growth of legitimate manufacturers.

Low Farmer Awareness and Limited Technical Training on Proper Film Use

Field surveys conducted in rural Ethiopia and Tanzania in 2024 revealed that smallholder farmers frequently apply mulch improperly and tension greenhouse covers incorrectly, leading to film deterioration and suboptimal microclimates. The limited availability of agricultural extension services and the concentration of private agronomy support in urban areas impede the dissemination of best practices. These knowledge limitations negatively impact repeat purchase rates and impede the transition from traditional straw mulch to polymer films.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Low-density Polyethylene (LDPE) Dominance Amid Biodegradable Surge

Low-density polyethylene (LDPE) maintains 42.35% of the Africa agricultural film market share in 2025. This dominance stems from established supply chains, proven flexibility, and suitability for low-tension installation methods. Standard LDPE grades support mulching and tunnel applications across diverse regions, from Nigeria's semi-arid maize cultivation areas to South Africa's wine regions. Linear-low and high-density variants address silage and bale wrapping requirements, while ethyl vinyl acetate and ethylene butyl acrylate copolymers provide solutions for greenhouse roofs requiring high light transmission.

Biodegradable films, despite their smaller market presence, are growing at a 10.12% CAGR. This growth is driven by clear regulations under EN17033 and climate-smart pilot programs supported by donor funding. Field trials in maize and tomato cultivation demonstrate yields comparable to LDPE while eliminating collection costs, improving overall cost efficiency. New material formulations combine poly (3-hydroxybutyrate-co-3-hydroxyvalerate) or starch with recycled LDPE to achieve both structural strength and controlled degradation. Manufacturers are developing nanoclay barriers and stearic-acid-surface treatments to improve water retention and soil respiration, reducing transplant stress and accelerating plant growth cycles. Recycled-content films, though experiencing slower growth, appeal to cooperatives focused on creating circular economies through the reuse of agricultural plastic waste.

By Application: Mulching Leads While Greenhouse Accelerates

Mulching accounted for 44.60% of the Africa agricultural film market size in 2025, as moisture conservation and weed suppression remain foundational practices in rain-fed systems. The Comprehensive Africa Agriculture Development Programme (CAADP) demonstrations have shown maize yield increases of up to 35% when low-density polyethylene (LDPE) mulch is combined with minimum tillage. Government extension services in Rwanda and Uganda support farmer-field schools that demonstrate mulch benefits, increasing adoption in districts previously dependent on organic litter.

Greenhouse films represent a smaller but fast-growing segment with a 8.95% CAGR, aligned with Morocco's and Kenya's shift toward export-oriented horticulture. Diffusive and infrared-reflective coverings are now standard in new construction specifications, increasing tomato and cucumber productivity while reducing heating costs during cool seasons. High-clarity three-layer structures with anti-fog additives provide longer service life in humid coastal areas, reducing film replacement frequency and improving financial stability for growers supplying European supermarkets.

By Film Thickness: Thinner Films Drive Innovation

Products in the 80-120 micron range held 37.55% of the Africa agricultural film market share in 2025, providing an optimal balance of tear resistance and cost-effectiveness for mechanized laying equipment. The integrated pigmented layers in these films filter specific light spectrums to regulate soil temperature, particularly benefiting onion and strawberry cultivation. Films above 120 microns primarily serve specialized applications requiring high durability, such as commercial greenhouse operations and export-oriented horticulture.

The below-80 micron segment is growing at a 10.24% CAGR as regional converters use high-melt-strength recycled high-density polyethylene (HDPE) additives to manufacture thin films that reduce material usage while maintaining tensile strength. While these ultra-thin grades attract government subsidy programs aiming to maximize budget allocation, farmers working with rocky soil conditions continue to prefer films exceeding 120 microns for enhanced puncture resistance. Modern polymer processing methods enable thin film production with improved mechanical properties, and multi-layer construction allows functional optimization without increasing thickness.

Geography Analysis

South Africa held 34.85% of the Africa agricultural film market share in 2025, supported by mechanized farming operations and efficient access to resin import terminals. The market recovery in 2025, following drought conditions, increased spending on greenhouse coverings and silage sheets. Non-tariff trade costs within the Southern African Development Community (SADC) continue to impact profit margins. The country's established recycling infrastructure and extended producer responsibility regulations drive the adoption of recycled-content films, positioning South Africa as a potential regional export center for compliant agricultural films.

Morocco is projected to grow at an 8.32% CAGR through 2031, driven by greenhouse expansion to meet European winter vegetable demand. Technical collaborations with Dutch suppliers facilitate advanced film technology adoption, and government irrigation projects encourage farmers to implement water-efficient mulch and low-tunnel systems. The market growth is further supported by cold-chain infrastructure grants that necessitate film-wrapped silage and baleage for dairy feed preservation.

Egypt's land reclamation projects and large-scale corporate farming drive demand for heavy-duty greenhouse films. In contrast, Kenya, Ghana, and Nigeria depend on subsidies and out-grower programs to support film adoption among small-scale farmers. The African Continental Free Trade Area reduces internal tariffs, varying quality standards, and inspection requirements across regions, creating distinct market segments, requiring distributors to adapt certification and labeling for individual customs jurisdictions.

Competitive Landscape

The Africa agricultural film market demonstrates moderate concentration, with the top five companies, Berry Global, Inc., Armando Alvarez S.A., Ginegar Plastic Products Ltd., BASF SE, and Mondi PLC, holding around 50.5% of the market share in 2024. Berry Global maintains its market leadership through increased post-consumer recycled content and the divestment of non-core divisions, focusing on specialty films. Armando Alvarez S.A. and Ginegar Plastic Products Ltd. maintain strong positions by utilizing Spanish and Israeli technology portfolios to expand into Morocco's and Kenya's greenhouse markets.

Companies are prioritizing vertical integration strategies. Film converters are establishing partnerships with polymer suppliers to ensure a stable resin supply while developing agreements with regional distributors that offer local agronomic support. In 2023, BASF SE's investments in fermentation facilities support the future supply of bio-resins to African partners, indicating a long-term commitment to the region. Technology licensing agreements for anti-fog and reflective additives enable local extrusion plants to reduce development time, facilitating technology-backed co-branding initiatives.

Market opportunities exist in developing biodegradable mulch sheets specifically certified for African soil and climate conditions, and silage wraps with oxygen-barrier layers adapted for East and West Africa's higher temperatures. Companies that integrate digital moisture-monitoring systems with film products, similar to Diageo-funded climate-smart initiatives, can generate additional service revenue beyond film sales.

Africa Agricultural Film Industry Leaders

-

Berry Global, Inc. (Amcor plc)

-

Armando Alvarez S.A.

-

Ginegar Plastic Products Ltd.

-

BASF SE

-

Mondi PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Perfect Colourants & Plastics Pvt. Ltd. has rolled out specialized masterbatches tailored for mulch film applications, making their debut in markets across the globe, including Kenya and Tanzania. These innovative masterbatches not only enhance tensile strength and puncture resistance, even in environments laden with pesticides and insecticides, but also offer high opacity and cost-efficiency for superior performance.

- November 2024: Berry Global's Flexibles division has ramped up its use of post-consumer recycled (PCR) polyethylene (PE) in its agricultural film products by 36% year-over-year. The company touts this move as a testament to its commitment to sustainable packaging and aiding customers in achieving their environmental objectives.

- July 2024: BASF SE introduced Tinuvin NOR 211 AR, a heat and light stabilizer designed for agricultural plastics in plasticulture applications. The product improves plastic durability by protecting against UV radiation, thermal stress, and inorganic chemicals, including sulfur and chlorine.

Africa Agricultural Film Market Report Scope

Agricultural films or plastics are used in many innovative agricultural practices to increase the crop output per hectare while enhancing crop quality. Agricultural films are used extensively for soil protection, greenhouse farming, and mulching. The African agricultural films market is segmented by Type (Low-density Polyethylene, Linear Low-density Polyethylene, High-density Polyethylene, Ethyl Vinyl Acetate (EVA)/Ethylene Butyl Acrylate (EBA), Reclaims, and Other Film Types), Application (Silage, Mulching, and Greenhouse), and Geography (South Africa, Morocco, Egypt, and Rest of Africa). The report offers market estimation and forecasts in value (USD) for the above mentioned segments.

By Type

| Low-Density Polyethylene (LDPE) |

| Linear Low-Density Polyethylene (LLDPE) |

| High-Density Polyethylene (HDPE) |

| Ethyl Vinyl Acetate / Ethylene Butyl Acrylate |

| Biodegradable Films |

| Reclaims |

By Application

| Mulching |

| Greenhouse |

| Silage and Ensiling |

By Film Thickness

| Less Than 80 Microns |

| 80-120 Microns |

| More Than 120 Microns |

By Geography

| South Africa |

| Morocco |

| Egypt |

| Rest of Africa |

| By Type | Low-Density Polyethylene (LDPE) |

| Linear Low-Density Polyethylene (LLDPE) | |

| High-Density Polyethylene (HDPE) | |

| Ethyl Vinyl Acetate / Ethylene Butyl Acrylate | |

| Biodegradable Films | |

| Reclaims | |

| By Application | Mulching |

| Greenhouse | |

| Silage and Ensiling | |

| By Film Thickness | Less Than 80 Microns |

| 80-120 Microns | |

| More Than 120 Microns | |

| By Geography | South Africa |

| Morocco | |

| Egypt | |

| Rest of Africa |

Key Questions Answered in the Report

What is the forecast value of the Africa agricultural film market by 2031?

USD 651.18 million, reflecting a 6.36% CAGR over 2026-2031.

Which application segment is expanding fastest across African farms?

Greenhouse covers, growing at a 8.95% CAGR on the back of Morocco's and Kenya's protected-cultivation investment.

Which country presently leads spending on agricultural films?

South Africa, with 34.85% of total 2025 sales due to mechanized operations and mature supply chains.

What is the primary short-term threat to market growth?

Counterfeit low-grade films circulating in informal markets that undermine farmer confidence in legitimate products.

Page last updated on: