Market Overview

| Study Period | 2021 - 2031 |

|---|---|

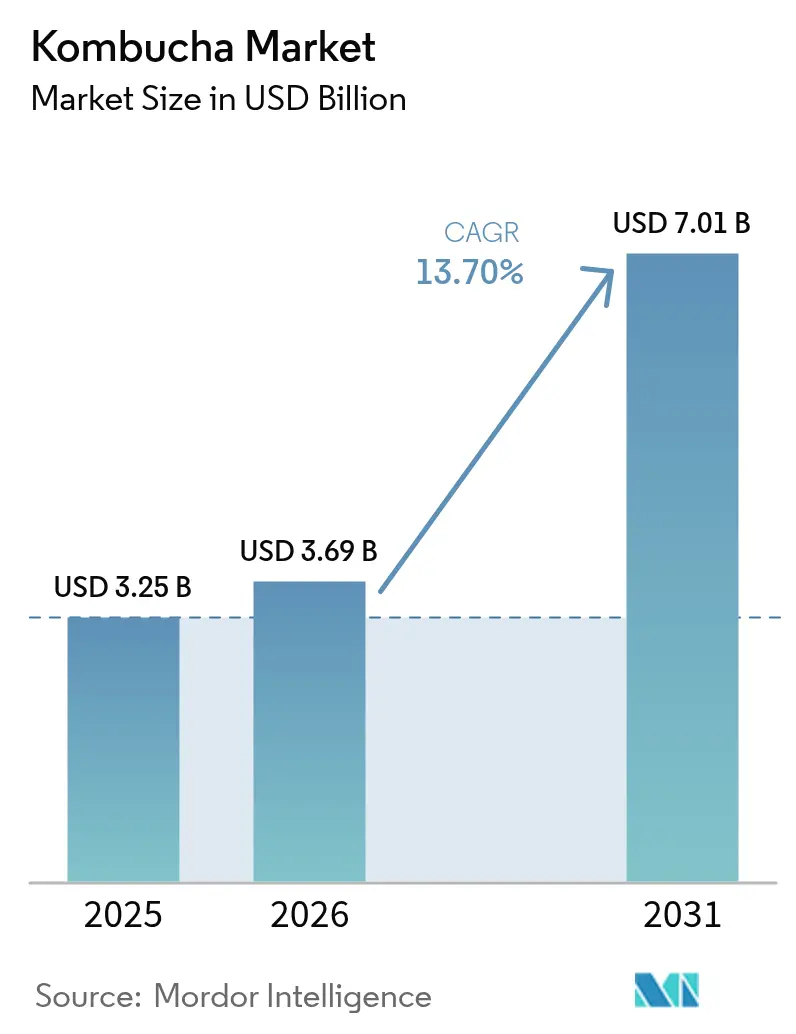

| Market Size (2026) | USD 3.69 Billion |

| Market Size (2031) | USD 7.01 Billion |

| Growth Rate (2026 - 2031) | 13.70% CAGR |

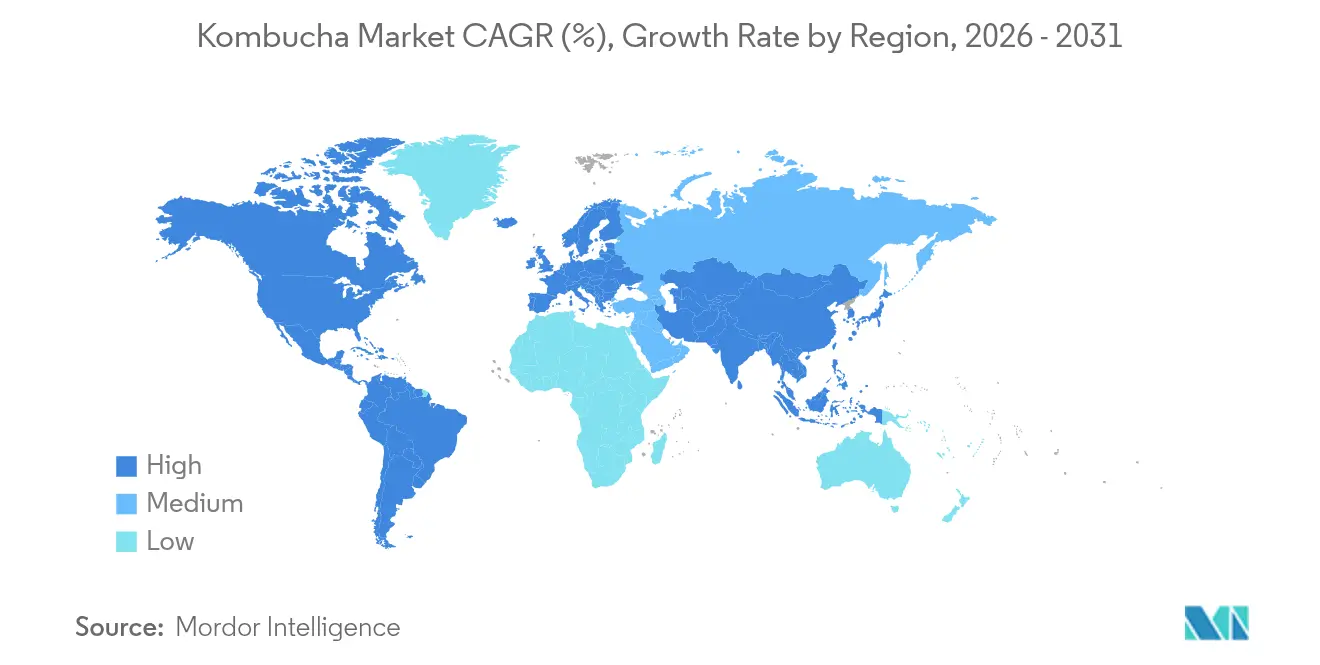

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Kombucha Market Analysis by Mordor Intelligence

The kombucha market size is expected to grow from USD 3.25 billion in 2025 to USD 3.69 billion in 2026 and is forecast to reach USD 7.01 billion by 2031 at 13.7% CAGR over 2026-2031. The increasing popularity of probiotic-rich and functional beverages is driving this demand, as more consumers seek healthier drink options. The growing availability of kombucha in retail stores is helping it transition from being a niche wellness product to a widely consumed mainstream beverage. Flavored kombucha remains the most popular choice among consumers; however, traditional brews are gaining traction at a faster rate. This trend highlights a premium segment of the market where consumers value authenticity in their choices. Organic certification is another key factor influencing consumer preferences, as it serves as a major differentiator in the market. The shift toward aluminum packaging reflects the rising importance of sustainability among consumers. Geographically, the Asia-Pacific region is emerging as a key growth area for the kombucha market, while North America continues to be the largest revenue contributor. The market is moderately concentrated. Established players like GT’s Living Foods, which has over three decades of brewing experience, are leveraging their heritage to maintain their position and uphold claims of authenticity.

Key Report Takeaways

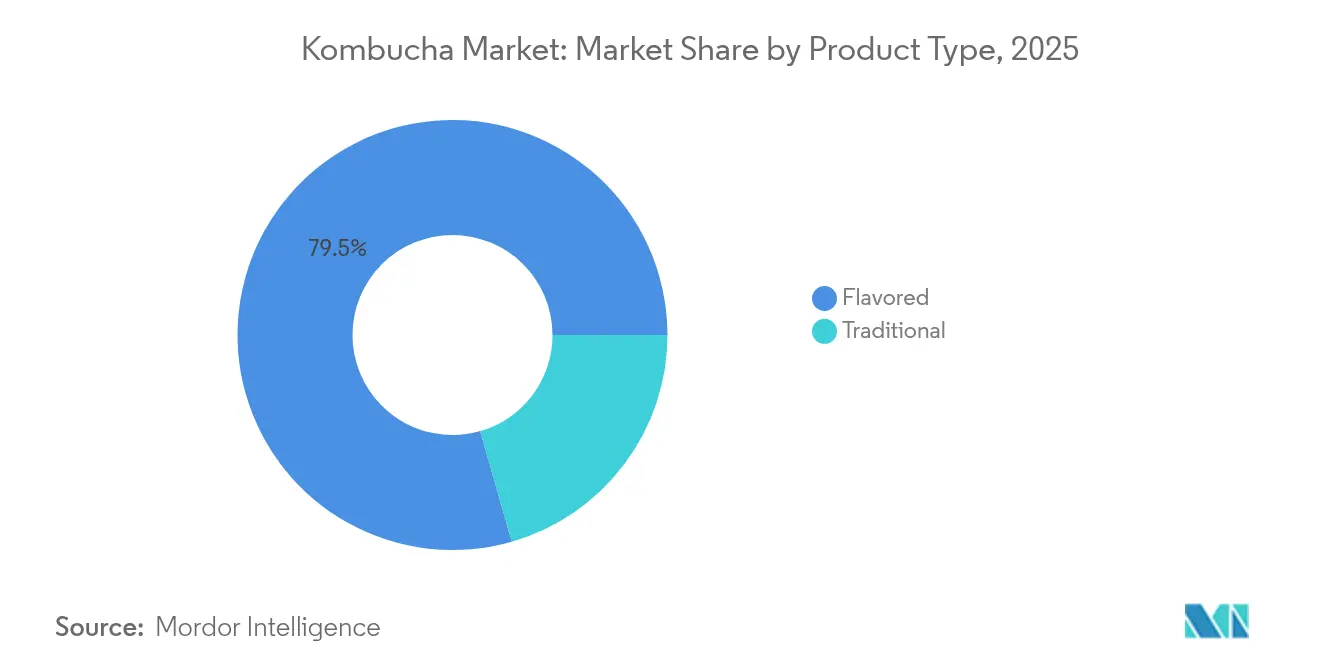

- By product type, flavored variants commanded 79.45% of the kombucha market share in 2025; traditional products are advancing at a 13.95% CAGR to 2031.

- By nature, organic offerings held 70.05% share of the kombucha market size in 2025 and are forecast to grow at 14.55% through 2031.

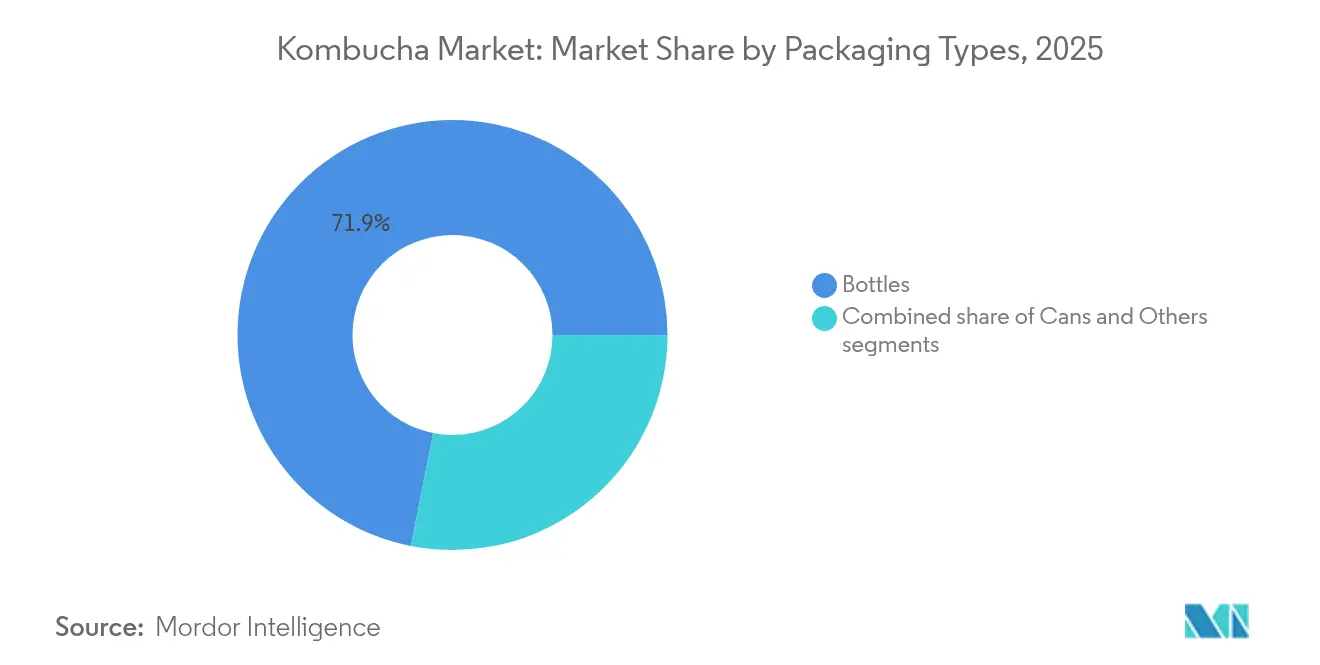

- By packaging, bottles retained 71.90% of the kombucha market share in 2025, but cans are projected to post a 15.6% CAGR to 2031.

- By distribution channel, off-trade formats delivered 54.80% of 2025 revenue, while on-trade is set to expand at 15.65% CAGR through 2031.

- By geography, North America led with 33.70% kombucha market share in 2025; Asia-Pacific is forecast to accelerate at 14.2% CAGR, the fastest among regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Kombucha Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising health awareness drives probiotic beverage demand | +3.2% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Growing vegan trend supports kombucha product adoption | +2.1% | North America and Europe, expanding to Asia-Pacific urban centers | Long term (≥ 4 years) |

| Expanding retail shelves promote wider kombucha availability | +2.8% | Global, with accelerated penetration in Asia-Pacific and Middle East and Africa | Short term (≤ 2 years) |

| Product innovation boosts appeal among young consumers | +2.4% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Celebrity endorsements enhance kombucha brand recognition globally | +1.8% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Functional drinks gain popularity over carbonated options | +2.6% | Global, with highest impact in health-conscious markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing vegan trend supports kombucha product adoption

With the growing popularity of vegan and plant-based diets, kombucha has become a favored functional beverage due to its naturally plant-based composition. According to the World Animal Foundation, by 2025, there will be approximately 88 million vegans globally, with 67% of them being women [1]Source: World Animal Foundation, "How Many Vegans Are in the World in 2025? Latest Vegan Stats," worldanimalfoundation.org. Unlike traditional dairy-based probiotics, kombucha provides gut health benefits without using animal-derived ingredients, making it appealing to both vegans and those who are lactose-intolerant. Ethical consumers seeking transparency and sustainability particularly prefer clean-label and organic kombucha options. In 2024, brands like Remedy Drinks and GT’s Living Foods introduced zero-sugar, organic product lines specifically designed for plant-based consumers. Rapid urbanization in Asia-Pacific cities such as Jakarta, Manila, and Bengaluru is driving kombucha’s popularity among vegan and flexitarian communities. According to UN-Habitat, 54% of the global urban population, or over 2.2 billion people, reside in Asia, highlighting the region's significant potential for kombucha market growth [2]Source: UN-Habitat, "Asia and the Pacific Region," unhabitat.org.

Rising health awareness drives probiotic beverage demand

As more people focus on wellness, they are choosing drinks that help improve digestion and boost immunity. In 2024, a report by Food Insights showed that 62% of Americans consider the health benefits of food and drinks when making a purchase [3]Source: Food Insights, "2024 IFIC Food and Health Survey," foodinsight.org. Fermented beverages like kombucha are becoming popular because healthcare experts and nutritionists recommend them for maintaining a healthy gut. Younger consumers, especially Gen Z, are particularly interested in drinks with functional benefits like probiotics. To cater to this demand, companies like Humm Kombucha have introduced products such as Humm Probiotic+, which contains 10 billion CFUs and clinically proven probiotic strains to support daily health. These scientific claims not only build trust among consumers but also allow brands to sell their products at higher prices. Furthermore, retailers in regions like North America and Western Europe are dedicating more shelf space in refrigerated sections to probiotic drinks in the kombucha market.

Product innovation boosts appeal among young consumers

Unique flavors and creative packaging are helping kombucha stay popular, especially with Gen Z and millennials. Brands are introducing exciting flavor combinations like chili mango, lavender melon, and blends with botanical adaptogens to cater to changing tastes and wellness trends. Seasonal limited-edition flavors, such as Brew Dr. Kombucha’s “Love” hibiscus-rose variety, are gaining attention on social media platforms like TikTok and Instagram, creating buzz and building customer loyalty. Packaging is also evolving, with recyclable aluminum bottles and sleek, minimalist cans appealing to Gen Z’s focus on sustainability and stylish designs. Collaborations with influencers and celebrities, such as Health-Ade teaming up with Ryan Seacrest and GT’s working with wellness creators, are helping kombucha expand its reach beyond health stores into mainstream lifestyle culture. These ongoing innovations in flavors and packaging encourage people to try kombucha and ensure it remains a key player in the kombucha market.

Celebrity endorsements enhance kombucha brand recognition globally

Celebrity partnerships are becoming an important way for kombucha brands to grow their popularity and connect with more people. By teaming up with well-known figures, these brands can reach audiences who might not usually focus on wellness products. For instance, Health-Ade worked with Ryan Seacrest to bring their brand into mainstream media, while companies like Olipop and GT’s Living Foods have collaborated with fitness influencers and athletes to attract more customers. In Asia, kombucha brands are partnering with local celebrities and yoga instructors to appeal to younger, urban consumers. These partnerships not only make the brands more relatable but also highlight the health benefits of kombucha, building trust and encouraging people to try the product. This approach is especially effective with younger generations, like Gen Z and Gen Alpha, who value recommendations from trusted figures in the kombucha market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High product cost limits adoption in price-sensitive markets | -2.1% | Asia-Pacific emerging markets, Latin America, rural regions globally | Medium term (2-4 years) |

| Limited awareness affects demand in rural regions | -1.4% | Rural areas globally, with highest impact in Asia-Pacific and Middle East and Africa | Long term (≥ 4 years) |

| Competition from other functional drinks slows market growth | -1.8% | Global, with intensified competition in developed markets | Short term (≤ 2 years) |

| Short shelf life restricts large-scale distribution logistics | -1.2% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High product cost limits adoption in price-sensitive markets

Kombucha’s higher retail price, often 3–4 times more expensive than regular soft drinks, remains a major challenge for its widespread adoption in price-sensitive markets. This higher cost is mainly due to the complex production process, which involves small-batch fermentation, careful handling of live cultures, and the need for refrigerated supply chains to maintain product quality. In many developing markets, where consumers are more budget-conscious, such pricing makes it difficult for people to try or regularly purchase kombucha, even though interest in health-focused beverages is growing. Meeting regulatory requirements, such as controlling alcohol content and providing accurate sugar labeling, adds to production costs. For instance, recent regulatory actions in regions like the U.S. and EU have increased compliance expenses for brands [4]Source: Federal Register, "Alcohol Facts Statements in the Labeling of Wines, Distilled Spirits, and Malt Beverages," federalregister.gov. These combined costs often lead companies to focus on premium urban markets, leaving rural and smaller towns underserved in the kombucha market.

Competition from other functional drinks slows market growth

Kombucha is now facing tough competition in the functional beverages market, as new categories like probiotic sodas, adaptogenic tonics, prebiotic waters, and nootropic drinks are gaining popularity. Brands such as Olipop, Poppi, and Recess are attracting younger consumers by offering gut-health or mood-enhancing benefits in more convenient and appealing formats. These alternatives often have lower sugar content, longer shelf life, and milder flavors, making them more accessible to people who might not enjoy kombucha’s tangy taste or the idea of live cultures. Additionally, many of these drinks do not require refrigeration, which adds to their convenience. As more options crowd store shelves and compete for consumer attention, kombucha is finding it harder to secure retail space and maintain customer loyalty in the kombucha market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Traditional Variants Drive Authenticity Premium

In 2025, flavored kombucha, which made up 79.45% of the total volume, dominated the category but showed signs of maturity with its decelerating growth. Its widespread appeal can be attributed to its palatable taste profiles, often enhanced with fruits, botanicals, and spices. Brands are pushing boundaries, introducing functional blends like ginger-turmeric and pairing them with exotic fruits to appeal to a broader audience. Thanks to technological strides like hot-fill processing, brands can now preserve probiotics while also offering bolder flavors. Established brands leverage their scale, but up-and-coming brands are making waves with their limited-edition and seasonal launches. With competition heating up, the key to success lies in curating a portfolio that marries novelty with a wellness focus in the kombucha market.

Traditional kombucha is set to outstrip the overall category growth, boasting a projected 13.95% CAGR, fueled by a growing consumer appetite for purity and artisanal craftsmanship. Heritage brands are spotlighting their unflavored, raw formulations and artisanal fermentation methods, allowing them to command premium prices. Buyers with a wellness focus regard these traditional offerings as genuine sources of live cultures. Take GT’s Living Foods, for instance; they’ve cultivated a dedicated following by spotlighting their time-honored brewing methods. As consumers become more discerning, these traditional offerings are gaining traction, especially for their touted microbiome benefits, solidifying their presence on premium shelves in the kombucha market.

By Nature: Organic Certification Drives Premium Positioning

Organic kombucha made up 70.05% of the market revenue in 2025 and is projected to grow at an annual rate of 14.55%. Consumers are increasingly drawn to organic products because they are seen as healthier, purer, and better for the environment. Retailers prominently showcase organic certifications, which help justify higher prices and build trust among buyers. These certifications also address common concerns about sugar content and alcohol traces, making organic kombucha a preferred choice for health-conscious individuals. As a result, organic kombucha continues to lead the market, attracting loyal customers who value clean ingredients and sustainable practices.

In contrast, conventional kombucha appeals more to budget-conscious consumers, especially in developing markets. However, its growth has been slower due to the rising demand for clean-label products and environmentally friendly practices. Transitioning to organic production can be challenging for brands because of supply chain complexities and higher costs, but the benefits often outweigh these challenges. Organic certifications allow brands to charge premium prices and strengthen their position in the kombucha market. Initiatives like TRUE Gold zero-waste certification demonstrate a commitment to broader environmental and social goals, further boosting the reputation and appeal of organic kombucha brands.

By Packaging Type: Can Innovation Challenges Bottle Dominance

In 2025, bottle packaging accounted for 71.90% of the kombucha market share, primarily due to its premium appearance and ability to showcase the product clearly. Glass is also favored for its inert properties, which help preserve the flavor and maintain the probiotic content of kombucha. However, challenges such as high shipping costs and the fragility of glass are encouraging brands to explore alternative packaging options. Aluminum cans are gaining popularity, with a growth rate of 15.6% CAGR, driven by their recyclability, lightweight nature, and alignment with sustainability goals. Younger consumers, in particular, are drawn to these eco-friendly and convenient packaging solutions, as seen with Mortal’s 16-oz aluminum bottle launch.

Brands adopting aluminum cans are expanding kombucha consumption to more on-the-go occasions, such as outdoor events, gym visits, and travel, moving beyond traditional at-home use. Innovations like resealable lids and light-blocking liners are helping address concerns about carbonation loss and UV exposure, ensuring product quality. While glass packaging will likely remain a preferred choice for premium segments, aluminum offers a practical and efficient alternative for brands looking to tap into broader consumer markets in the kombucha market. This shift not only supports sustainability efforts but also provides a cost-effective way to meet the growing demand for kombucha in diverse settings.

By Distribution Channel: On-Trade Surge Signals Premium Positioning Success

In 2025, off-trade outlets like supermarkets and specialty stores accounted for 54.80% of kombucha sales volume. These retail stores play a key role in introducing customers to kombucha, as they provide easy access and visibility on cold shelves, which also enhances the product's credibility. Supermarkets and specialty stores allow consumers to explore different flavors and brands, making them a popular choice for first-time buyers. These outlets often run promotions and discounts, encouraging more purchases. However, the on-trade segment, including restaurants and cafés, is growing rapidly at an annual rate of 15.65%. These establishments position kombucha as a premium, health-conscious alternative to traditional beverages like soda or wine, often pairing it with meals to enhance the dining experience.

Meanwhile, e-commerce platforms are gaining traction by offering the convenience of home delivery, often with chilled cases and subscription options that encourage repeat purchases. This channel is particularly appealing to busy consumers who prefer to stock up on their favorite kombucha flavors without visiting a store. Convenience stores also play a role by targeting impulse buyers looking for a quick, functional refreshment option. These stores cater to consumers who want kombucha on the go, making it a practical choice for busy lifestyles. By leveraging multiple sales channels, kombucha brands can reach a wider audience, reduce risks associated with relying on a single channel, and strengthen their presence in the kombucha market.

Geography Analysis

North America led the kombucha market in 2025, accounting for 33.70% of the market share. The region's strong focus on health and wellness, along with clear labeling regulations and well-established retail networks, has supported this growth.. Retailers like Whole Foods promote exclusive, limited-edition kombucha products, while celebrity endorsements help bring the drink into the mainstream. Although the market in North America continues to grow steadily, the pace is slowing as the market becomes more saturated and mature.

The Asia-Pacific region is the fastest-growing kombucha market, with a projected CAGR of 14.2% through 2031. Factors such as rising middle-class incomes, improved retail infrastructure, and a cultural acceptance of fermented foods are driving this growth. Local companies are innovating by introducing flavors that cater to regional tastes, such as lemongrass and lychee. However, challenges like price sensitivity and differing regulations across countries remain significant. To address these issues, companies are offering smaller, more affordable pack sizes and running educational campaigns to increase consumer awareness. If these strategies succeed, the region could see substantial market growth by the end of the decade.

Europe is taking a sustainability-driven approach to the kombucha market. Consumers in this region are highly influenced by factors like organic certification and recyclable packaging when making purchasing decisions. While strict EU labeling laws add complexity for producers, the familiarity of European consumers with fermented products like kefir makes it easier for kombucha to gain acceptance. Initiatives such as carbon footprint disclosures and zero-waste goals resonate strongly with environmentally conscious shoppers and policymakers. In contrast, South America and the Middle East, and Africa are still emerging markets for kombucha. At the same time, economic growth and urbanization present opportunities, but challenges such as limited cold-chain infrastructure and low consumer awareness hinder kombucha market expansion.

Regulatory Landscape

Kombucha regulation is shaped by alcohol-by-volume (ABV) thresholds and food-safety controls for live, unpasteurized fermented beverages. In the United States, products at or below 0.5% ABV are generally treated as non-alcoholic foods under FDA oversight, while products exceeding 0.5% ABV can fall under Alcohol and Tobacco Tax and Trade Bureau (TTB) jurisdiction as beverage alcohol, affecting labeling and tax compliance. At the state level, retail or on-site brewing can trigger additional approvals such as variances or Special Process Approval (SPA) requirements from health authorities, typically tied to validated process controls (for example, HACCP-based documentation) and routine monitoring of fermentation parameters such as pH and temperature.

In Europe, kombucha marketed as a fermented beverage must comply with the EU general food hygiene framework, including Regulation (EC) No 852/2004, which reinforces a farm-to-fork food safety approach. Country-level guidance for unpasteurized fermented plant-based products, such as the Food Safety Authority of Ireland (FSAI) GMP guidance, emphasizes pathogen-control measures including pH management (for example, keeping pH below 4.4) and robust hygiene practices. For innovation-led formulations, market access can also be influenced by the EU Novel Food framework (Regulation (EU) 2015/2283) when new ingredients or processes require additional safety assessment before commercialization.

Competitive Landscape

The kombucha market is moderately concentrated, with established brands like GT’s Living Foods using their decades of brewing experience to maintain their reputation for authenticity. Their "Real Kombucha" campaign highlights their raw and unpasteurized brewing methods, appealing to consumers who value traditional production techniques. Similarly, Health-Ade has expanded its production and distribution across the United States. By leveraging celebrity endorsements, the brand has successfully increased its visibility and appeal to a broader audience.

Innovation plays a key role in differentiating products within the kombucha market. Companies are introducing functional ingredients, such as zinc or L-theanine, to enhance the health benefits of probiotics, as seen in Humm’s Probiome line. Sustainability is also becoming a critical factor, with brands like GT’s achieving TRUE Gold zero-waste certification, which strengthens their environmental, social, and governance (ESG) credentials in the kombucha industry. Start-ups are addressing gaps in the market by offering low-sugar options or alcohol-free variants, catering to consumers who are mindful of sugar intake or alcohol consumption regulations.

Interest in mergers and acquisitions is growing as large beverage companies look to enter the rapidly expanding functional beverage category. Emerging kombucha brands are attracting investments to scale their operations, improve cold-chain infrastructure, and enhance brand visibility across the kombucha industry. While larger companies benefit from their ability to secure shelf space, smaller, agile brands are gaining traction by offering unique, locally inspired flavors and engaging directly with consumers through storytelling. This balanced competition fosters innovation and diversity in the market, keeping consumers interested and driving the long-term growth of the kombucha industry.

Kombucha Industry Leaders

-

GT’s Living Foods

-

PepsiCo Inc.

-

Health-Ade, LLC

-

Rowdy Mermaid

-

Cathy's Kombucha

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Scaling production while maintaining compliance around ABV and labeling remains a core opportunity area, pushing brands toward tighter fermentation control and more industrialized infrastructure. In April 2026, US lawmakers introduced the KOMBUCHA Act (Rep. Salinas, Rep. Smith, and Sen. Wyden) proposing to raise the ABV threshold relevant to federal alcohol rules from 0.5% to 1.25%, illustrating how regulatory classification can affect product design, testing frequency, and route-to-market decisions. Alongside regulation, producers are investing in customized fermentation systems and larger facilities to improve consistency and throughput, which supports broader distribution and more competitive unit economics.

Geographic expansion also stands out as a practical route for connecting maturing core markets with newer demand centers, particularly in Asia-Pacific and parts of Europe. In June 2026, MOMO Kombucha moved into a 16,000-square-foot facility in Brixton, London, and reported a step-up in capacity from about 60,000 to 300,000 bottles per week using custom fermentation vessels, reflecting a shift from small-batch methods to scaled, engineered production. Cross-border growth is also being pursued by emerging brands, including Spraga announcing expansion into Poland backed by a EUR 700,000 investment (March 2026), while Southeast Asia remains a target for capacity-linked plans such as WonderBrew's stated goal to double production in 2026 to support entry into Singapore and Indonesia. At the same time, enforcement actions, including the April 2026 Taiwan case involving halted production and sales tied to alleged relabeling of expired ingredients, point to the value of traceability, QA, and compliant labeling as volumes increase.

Recent Industry Developments

- June 2026: GT’s Living Foods (SYNERGY The Real Kombucha) launched UNITY x Cheribundi: Shirley Temple, a limited-edition collaboration combining kombucha with tart cherry juice. The release extends the brand's collaboration-led flavor strategy and uses co-branding to broaden trial beyond core kombucha shoppers.

- June 2025: Rowdy Mermaid announced a strategic partnership with Next in Natural, backed by KarpReilly and Luke Comer, positioning the brand under a platform designed to add shared operational and commercial capabilities. The move supports scaling across supply chain, distribution, and innovation while keeping a dedicated kombucha brand in a consolidating functional beverage set.

- August 2024: Tata Consumer Products launched Tetley Kombucha in Ginger Lemon and Peach, a tea-based kombucha positioned with added prebiotic fiber. The entry by a large tea player increased competitive pressure in functional beverages and helped normalize kombucha as a mainstream extension within established beverage portfolios.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the kombucha market is defined as ready-to-drink kombucha beverages sold through retail and on-trade channels, measured in value terms across major consuming regions. The sizing reflects packaged product sales linked to commercial production and branded distribution.

Scope exclusions: Home-brewed kombucha, kombucha used only as an ingredient in other foods, and related probiotic drinks that are not sold as kombucha are excluded.

Segmentation Overview

-

By Product Type

- Traditional

- Flavored

-

By Nature

- Conventional

- Organic

-

By Packaging Types

- Bottle

- Can

- Others

-

By Distribution Channel

-

Off-Trade

- Supermarkets/Hypermarkets

- Specialist Stores

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

- On-Trade

-

Off-Trade

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the base structure of the model and to collect stable data series we could reuse year after year. We typically review government and customs statistics such as UN Comtrade and national trade portals to understand import and export flows for fermented and functional beverages where relevant. To ground consumer demand signals, we also use sources such as USDA and other national agriculture and food agencies, alongside World Bank macro indicators (population, income, and inflation) for regional context.

To cross-check category trends, we also reference association and standards materials such as the Alcohol and Tobacco Tax and Trade Bureau (for markets where hard kombucha labeling rules apply), plus public health and food safety authorities and peer-reviewed food science journals on fermentation, sugar content, and shelf life. Company filings, investor presentations, and trusted press coverage are then used to understand route-to-market shifts and pricing actions. Where needed, our internal paid subscriptions for company financials, news, patent lookups, and shipment-level trade visibility are used only to fill gaps and sanity-check outliers. These desk research sources are illustrative and not exhaustive, since many other public and paid references were used during data collection and validation.

Primary Interviews and Surveys

Primary work was carried out through expert interviews and structured surveys with kombucha brand teams, ingredient suppliers, packaging partners, distributors, and channel stakeholders across APAC, EMEA, and the Americas. The discussions focused on what sells in practice by pack type and channel, how pricing is being adjusted, and how organic and conventional mixes are changing, which helped confirm assumptions that were not directly observable in public sources.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 20% | APAC: 46% |

| Mid tier: 48% | Functional/Unit leaders: 23% | EMEA: 30% |

| Smaller Players: 20% | Managers: 57% | Americas: 24% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where beverage category totals and country consumption signals are reconstructed into a kombucha demand pool, and then filtered by channel availability and product mix. To keep the totals realistic, we corroborated the outputs with selective bottom-up checks, such as sampled brand price points by pack format, observed volume proxies by channel, and supplier and distributor checks on shipment momentum.

Key model inputs (illustrative) included kombucha penetration within functional beverages, on-trade versus off-trade split, price per liter progression by packaging (bottles versus cans), organic share direction, and regional growth differences connected to modern retail expansion and online availability. When direct splits were not available for a country, a proxy was applied using a close market with a similar channel structure, followed by an interview-based adjustment. Forecasts were produced using scenario analysis, with the base case tied to expected pricing, channel expansion, and repeat purchase behavior, and then stress-tested with more conservative and more aggressive adoption paths.

Data Validation & Update Cycle

Model outputs were checked against independent signals such as trade movement, public pricing trends, and channel expansion announcements, and any sharp year-to-year swings were flagged for a second pass. Variances were reviewed step by step, first at the country level and then rolled up to region level, before the final global number was signed off.

Reports are refreshed annually, and interim adjustments are made when there are material events that can affect alcohol or beverage classification, sudden pricing shocks, or major distribution changes. Before delivery, we run a fresh review pass so clients receive an updated view reflecting the latest information available at the time of publication.

Mordor Intelligence's Kombucha Market Size Compared With Other Published Estimates

Published kombucha market numbers can look far apart because each publisher chooses its own year, product definition, and way of treating on-trade versus off-trade sales. Differences also come from how pricing is converted to USD, and whether growth is projected from a stable base case or from a more aggressive adoption curve.

The table shows a spread for the 2025 value, and in Mordor Intelligence's model the scope is limited to kombucha sold as a finished beverage across traditional and flavored types, with explicit splits by nature, packaging, and channel to avoid folding adjacent probiotic drinks into the total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.25 B (2025) | |

| Global Consultancy A | USD 2.90 B (2025) | Uses a different base-year framing with a narrower type definition and less explicit channel treatment, which can undercount on-trade volumes and smaller pack formats in certain markets. |

| Regional Consultancy B | USD 5.51 B (2025) | Often reflects a broader functional beverage scope and a different pricing and currency timing assumption, which can lift the 2025 value when adjacent fermented drinks and higher ASP paths are included. |

Taken together, the comparison mainly points to scope control and pricing logic as the drivers of the gap. By keeping the inputs tied to observable channel splits, packaging mix, and realistic price per liter movements, the estimate stays traceable and can be repeated when new country data and interview signals become available.

Key Questions Answered in the Report

How big is the kombucha market in 2026?

The kombucha market stands at USD 3.69 billion in 2026.

What is the expected kombucha market size by 2031?

It is projected to reach USD 7.01 billion by 2031, growing at a 13.7% CAGR.

Which product type is growing fastest?

Traditional kombucha is forecast to expand at a 13.95% CAGR, outpacing flavored variants.

Which region offers the strongest growth potential?

Asia-Pacific leads in growth with a projected 14.2% CAGR to 2031, thanks to rising health awareness and modernizing retail.

Page last updated on: