Aerospace Pressure Gauge Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.03 Million |

| Market Size (2031) | USD 25.43 Million |

| Growth Rate (2026 - 2031) | 2.02% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

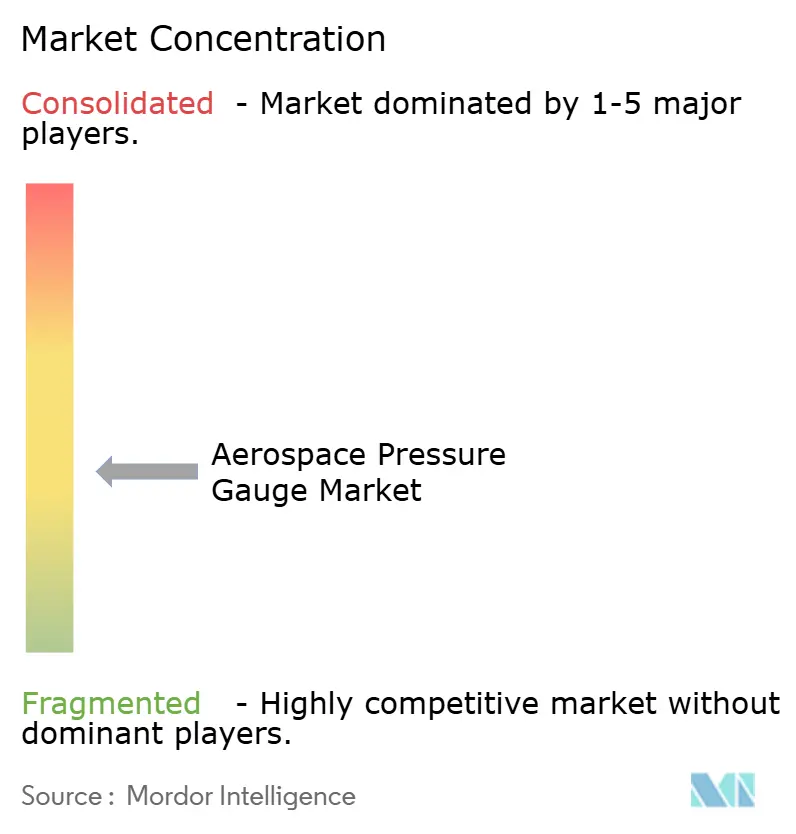

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace Pressure Gauge Market Analysis by Mordor Intelligence

The aerospace pressure gauge market size in 2026 is estimated at USD 23.03 million, growing from 2025 value of USD 22.57 million with 2031 projections showing USD 25.43 million, growing at 2.02% CAGR over 2026-2031. Digital retrofits on legacy cockpits, tighter sensor tolerances in new-build airframes, and expanding fleet renewal programs are moderating the growth profile yet steadily orienting demand toward miniaturized, software-enabled instrumentation. Analog gauges still dominate installed bases, but airframers are specifying digital interfaces for predictive maintenance tie-ins, driving incremental revenue opportunities in connected spares, data services, and calibration equipment. Capacity expansions at The Boeing Company, Airbus, and COMAC are shortening design cycles and compressing delivery schedules, raising the urgency for multi-year sensor supply agreements and localized manufacturing footprints. Meanwhile, regulatory emphasis on wireless monitoring and cybersecurity compliance is increasing certification costs but strengthening aftermarket pull for qualified digital variants. Suppliers that can synchronize MEMS innovation with global production ramp-ups and national content rules are best placed to capture share as the aircraft mix tilts toward newer, more instrumented platforms.

Key Report Takeaways

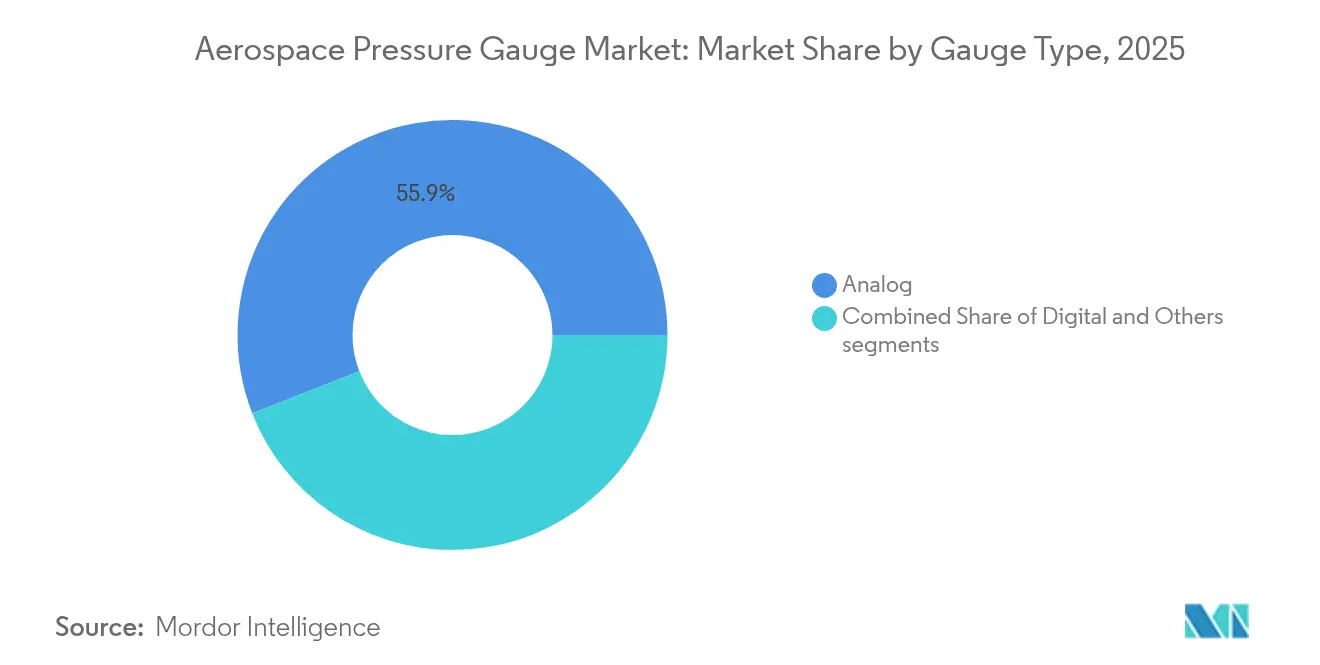

- By gauge type, analog instruments led with a 55.92% share in 2025, while digital variants are projected to expand at a 3.12% CAGR to 2031.

- By pressure sensor technology, piezoresistive devices accounted for 47.25% of the aerospace pressure gauge market share in 2025, while capacitive designs are advancing at a 4.4% CAGR through 2031.

- By application, commercial and military aviation accounted for 92.85% of 2025 revenue; unmanned systems represented the fastest expansion, with a 4.05% CAGR driven by drone fleet growth.

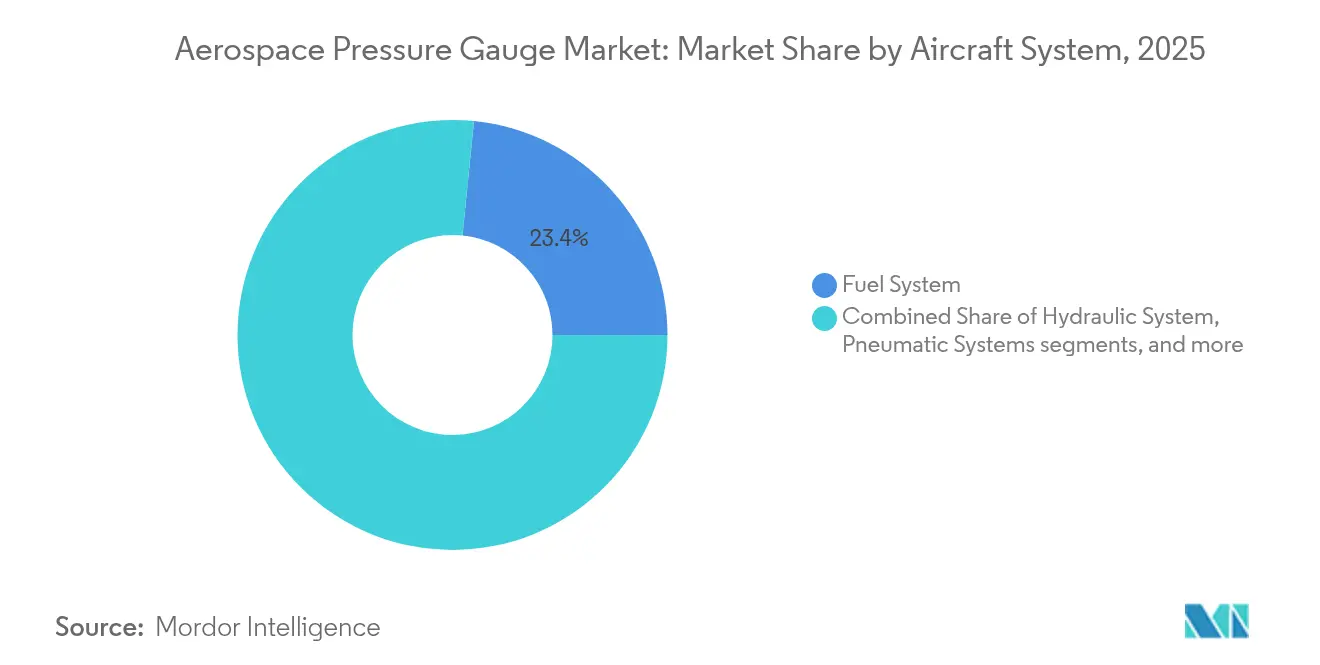

- By aircraft system, fuel monitoring captured 23.41% of the 2025 demand, whereas landing-gear and tire pressure sensing showed the quickest pace at a 2.54% CAGR to 2031.

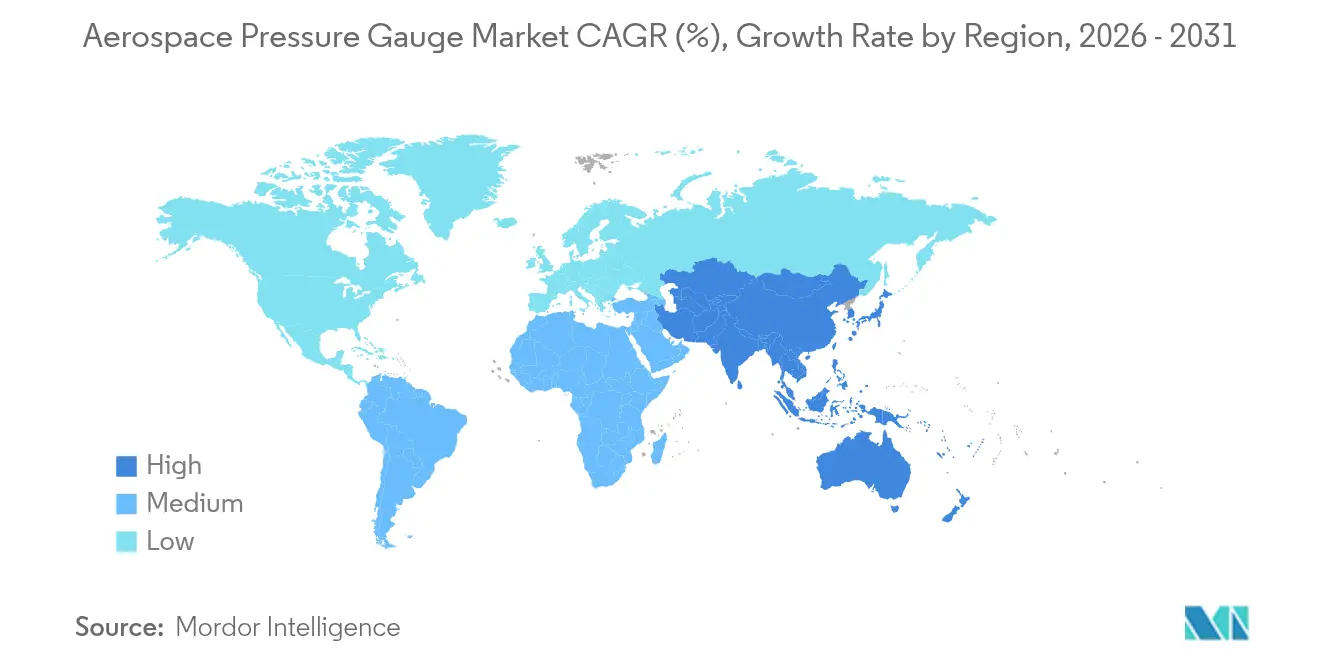

- By geography, North America retained a 37.25% share in 2025; the Asia-Pacific region is set to grow the fastest at a 5.59% CAGR, buoyed by COMAC C919 build rates and Indian defense programs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aerospace Pressure Gauge Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acceleration in digital cockpit modernization initiatives | +0.4% | Global, led by North America and Europe | Medium term (2–4 years) |

| Increasing integration of wireless pressure monitoring systems in commercial fleets | +0.3% | North America and Asia-Pacific | Medium term (2–4 years) |

| Expansion in global aerospace manufacturing and assembly capacity | +0.3% | Global, concentrated in North America, Europe, Asia-Pacific | Short term (≤2 years) |

| Regulatory compliance mandates enforcing strict calibration and maintenance cycles | +0.2% | Global, strongest in North America and Europe | Long term (≥4 years) |

| Technological advancements in MEMS-based miniaturized pressure sensors | +0.3% | Global, R&D hubs in North America, Europe, Asia-Pacific | Long term (≥4 years) |

| Growth in unmanned aerial systems requiring compact and high-precision instrumentation | +0.2% | Global, early adoption in North America, Asia-Pacific, Middle East | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Acceleration In Digital Cockpit Modernization Initiatives

Airframers are migrating from mechanical dials toward integrated flight decks that consolidate pressure data on glass displays. Honeywell’s Avianca A320neo retrofit replaced 14 analog gauges with six digital units, reducing cockpit weight by 8 kg and enabling health monitoring through Skywise analytics.[1]Honeywell, “Avianca A320neo Retrofit,” honeywell.com The B787 and B777X require digital sensors across fuel, hydraulic, and environmental systems, pressuring MROs to carry electronic spares. Embraer’s E2 jets demand sub-0.1% full-scale accuracy delivered via CAN bus, which mechanical Bourdon tubes cannot maintain over wide thermal ranges. Lessors are funding mid-life narrowbody upgrades to sustain lease rates, accelerating the retirement of analog aircraft even on those with 10-year service lives. FAA Advisory Circular 25-11B now streamlines approval of digital instrumentation, further reinforcing the adoption cycle.

Increasing Integration Of Wireless Pressure Monitoring Systems In Commercial Fleets

Teledyne’s 2024 Bluetooth Low Energy module eliminated 200 m of wiring per aircraft and cut installation labor by 40 hours. Weight savings of roughly 12 kg per narrowbody translate into fuel burn reductions and lower carbon charges. Airbus Skywise aggregates real-time sensor data from more than 10,000 aircraft, and early anomaly alerts prevented three in-flight shutdowns on an Asian A330 fleet in 2024.[2]Airbus, “Skywise Health Monitoring,” airbus.com EASA requires DO-160G emission compliance and fail-safe modes for wireless links, which can add up to nine months to certification, but ensures reliability. Operators prioritize tire-pressure modules that shorten ground checks by up to 20 minutes and reduce incidents of tread separation.

Expansion In Global Aerospace Manufacturing And Assembly Capacity

Boeing enhanced the B737 MAX output to 38 units per month by late 2024, and South Carolina’s B787 line now produces ten airframes monthly. Airbus added an A320 line in Mobile, Alabama, and raised Tianjin throughput to six per month, lifting the family’s rate to 65. COMAC delivered 39 C919 jets in 2024 and aims to reach 150 per year by 2028, driving domestic demand for localized sensors under the “Made in China 2025” policy. India’s Tata-Airbus venture has begun C295 assembly, with each airframe requiring approximately 50 pressure transducers. These ramps squeeze lead times for aerospace-grade piezoresistive parts beyond 52 weeks, forcing OEMs into multi-year supply contracts.

Regulatory Compliance Mandates Enforcing Strict Calibration And Maintenance Cycles

FAA AC 43-13-1B requires annual calibration with NIST traceability for critical pressure instruments, sustaining recurring aftermarket sales. EASA Part-M obliges operators to keep lifetime records and replace sensors that drift out of tolerance. The US Air Force Technical Order 33B-1-1 halves the interval to six months for fighter power plants, magnifying demand for certified replacements. Cybersecurity standards DO-326A and ED-202A add software validation costs and require secure boot functionality, which can increase certification budgets by up to USD 300,000 per sensor family. Operators view compliance as non-negotiable, given that a single pressure-sensor failure can ground an aircraft and cost airlines between USD 50,000 and USD 150,000 per day.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Performance limitations associated with mechanical gauge reliability | -0.3% | Global, legacy fleets in North America, Europe, emerging markets | Short term (≤2 years) |

| Elevated certification and regulatory approval costs for advanced sensor technologies | -0.2% | Global, most acute in North America and Europe | Medium term (2–4 years) |

| Material sourcing challenges impacting high-grade sensor component availability | -0.2% | Global, supply concentrated in North America, Asia-Pacific | Short term (≤2 years) |

| Cybersecurity compliance requirements delaying deployment of connected gauge systems | -0.1% | Global, regulatory focus in North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Performance Limitations Associated With Mechanical Gauge Reliability

Analog Bourdon-tube gauges drift 0.5% to 1.0% per year and contributed 18% of unscheduled maintenance events on regional turboprops in 2024. Temperature sensitivity can cause errors exceeding 3% at cruise altitude, whereas digital sensors compensate algorithmically. Complete retrofits cost between USD 15,000 and USD 25,000 per aircraft, deterring operators of older assets. Mechanical units also require 500-hour inspections, compared to 2,000 hours for digital equivalents, which increases lifecycle expenses by roughly 40%. Operators weigh known shortcomings against capital outlay, slowing the fleet-wide update pace.

Elevated Certification And Regulatory Approval Costs For Advanced Sensor Technologies

FAA TSO approval can exceed USD 800,000 once DO-178C, DO-160G, and DO-326A test regimes are met. EASA rules add up to USD 300,000 and nine months of dual-lab verification. Mid-tier suppliers, such as Kulite, report that certification expenses equal to 12% of their revenue limit their product pipeline. Annual cybersecurity audits increase recurring costs, prompting 40% of surveyed vendors to delay launches by more than a year.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Gauge Type: Digital Variants Gain On Integration Mandates

Analog instruments accounted for 55.92% of the aerospace pressure gauge market share in 2025, reflecting their legacy footprint across older narrowbodies and turboprops. Digital gauges, supported by airframe policies on integrated avionics, are forecast to grow at a rate of 3.12% annually to 2031, progressively displacing mechanical units in both linefit and retrofit channels.

Digital architectures simplify wiring, enable remote diagnostics, and meet new cybersecurity rules, tipping total cost-of-ownership in their favor by delivering a three-year payback through reduced calibration labor and fewer unscheduled interventions. The growth in market share of digital pressure gauges is envisioned to be aided by FAA incentives for software-based displays. Analog remains relevant in military programs that still specify mechanical backups, but its revenue pool steadily narrows as fleets modernize.

By Application: Aviation Dominance Masks Space Segment Potential

Aviation accounted for 92.85% of 2025 revenue, with commercial air transport leading unit demand as Airbus and Boeing boost single-aisle production. Military and business aviation add volume through modernization programs that embed digital sensors for condition-based maintenance. The aerospace pressure gauge market size in aviation applications is expected to grow at a 4.05% CAGR by 2031.

Spacecraft and satellite platforms, although smaller in dollars, display above-average growth as Artemis lunar missions, LEO constellations, and JAXA’s exploration projects adopt radiation-hardened gauges. Redundant capacitive sensors on SpaceX Dragon capsules set new performance benchmarks and guide specifications for future orbital stations. While space represents under 7% of current sales, its higher margins and technology spillovers give suppliers a strategic incentive to invest.

By Aircraft System: Fuel Monitoring Leads, Landing Gear Accelerates

Fuel systems retained 23.41% of demand in 2025 because regulations require dual-redundant measurement across tanks and feed lines. Hydraulics and cabin-pressure loops follow, each becoming more sensor-intensive as fly-by-wire and bleedless architectures expand. The aerospace pressure gauge market share for landing-gear and tire monitoring systems is growing at the fastest rate, with a 2.54% CAGR through 2031, driven by wireless TPMS approvals from the EASA and FAA.

Landing gear modules save operators up to 20 minutes per turnaround and cut unscheduled events tied to under-inflation, justifying rapid airline uptake. High-temperature SiC sensors are winning engine and APU positions once reserved for remotely mounted mechanical units, trimming weight and simplifying maintenance. Over the forecast period, wireless systems will continue to redistribute value toward connected ground operations, tooling, and data analytics.

By Pressure Sensor Technology: Piezoresistive Maturity, Capacitive Momentum

Piezoresistive devices held a 47.25% share in 2025, valued for linearity and heritage qualifications across pressure ranges up to 15,000 psi. Capacitive MEMS parts, however, are growing at a rate of 4.4% annually due to their superior drift performance and low-power traits, which are attractive for wireless and battery-powered use cases.

Capacitive share gains are most visible in cabin-pressure and TPMS modules, where milli-watt consumption extends sensor life within sealed housings. Piezoresistive units remain indispensable for high-pressure hydraulic circuits and cryogenic propellant lines. Piezoelectric designs remain niche but command premium prices in turbine blade and combustion pressure mapping applications.

Geography Analysis

North America led with 37.25% revenue in 2025, supported by Boeing’s production hubs, Airbus’s Alabama line, and a dense network of Tier 1 suppliers. Proximity to the FAA and RTCA accelerates certification, giving domestic vendors early access to new standards and program slots. US defense projects such as the KC-46 tanker and B-21 bomber sustain demand for 40-G shock-qualified, 10,000-hour mean time between failures (MTBF) sensors. Canada contributes through Bombardier upgrades, while Mexico’s low-cost sub-assembly capability supports local growth.

The Asia-Pacific is the fastest-growing cluster, with a 5.59% CAGR, driven by COMAC’s C919 ramp, India’s C295 transport line, and high-tempo fleet expansion at low-cost carriers. China’s 70% domestic content mandate catalyzes joint ventures such as Safran-AVIC Jonhon’s Luoyang plant for piezoresistive output. India’s Tejas and HTT-40 programs intensify indigenous demand; meanwhile, Japan’s JAXA drives the development of cryogenic and radiation-hardened sensors. South Korea and Southeast Asian nations add incremental volume through urban air mobility (UAM) pilots.

Europe maintains a robust share, anchored by Airbus assemblies in Toulouse, Hamburg, and Seville, as well as suppliers such as Safran and Parker Meggitt. EASA’s stringent Part-21 requirements lengthen the time-to-market yet ensure high-quality thresholds that favor established players. Sustainability themes, including Airbus’s ZEROe hydrogen demonstrator, spur requests for gauges capable of operating at -253 °C. The Middle East is leveraging the growth of MRO hubs in Dubai and Abu Dhabi. In contrast, Africa and South America remain comparatively small due to limited manufacturing of high-reliability sensors.

Competitive Landscape

Competitive intensity is moderate. Honeywell International Inc., TE Connectivity plc, Ahlers Aerospace, Inc., UMA, Inc., and Parker Meggitt (Parker-Hannifin Corporation) collectively hold a prominent market share, leaving a runway for niche innovators. Honeywell expanded its Arizona MEMS facility by 30% in 2025 to meet demand for the B737 MAX and A320neo aircraft, utilizing automated die-bonding to reduce unit costs by 15%. AMETEK’s acquisition of Crank Software folds rich graphical interfaces into sensor bundles, elevating value propositions for glass-cockpit programs.

TE Connectivity advances low-power capacitive designs, such as the MS5837-02BA, for UAVs, capitalizing on lightweight urban air mobility craft. Safran’s joint venture with AVIC Jonhon meets Chinese content rules, granting local access to the C919. Parker Meggitt’s USD 120 million Next Generation Air Dominance (NGAD) contract demonstrates incumbents’ leverage in defense niches that require 5,000 psi, 50-G-rated devices.

White space exists in wireless TPMS and deep-space probes, where fewer than five qualified suppliers operate. Patent filings underscore the innovation race: Honeywell lodged 14 pressure-sensor applications in 2024, covering fabrication and predictive algorithms, while TE Connectivity’s patents center on ultra-low-power telemetry. Cybersecurity compliance is emerging as a tie-breaker as airlines insist on DO-326A credentials for connected cockpit components.

Aerospace Pressure Gauge Industry Leaders

Honeywell International Inc.

UMA, Inc.

TE Connectivity plc

Ahlers Aerospace, Inc.

Parker Meggitt (Parker-Hannifin Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2023: Parker Meggitt (Parker-Hannifin Corporation) announced that it has been awarded a Supplemental Type Certificate (STC) for iPRESSTM, a long-range wireless tire pressure gauge for aviation. iPRESS is available for various aircraft.

- November 2022: DLA Aviation issued a solicitation for dial pressure gauges used in the HH-60 aircraft. The gauge is NSN 6685-00-074-2288, made of anodized aluminum with a Beryllium copper element. It ranges from 0 to 20 psi, marked in 5 psi increments. It measures 4 inches in diameter and has a depth of 3.6 inches.

Global Aerospace Pressure Gauge Market Report Scope

A pressure gauge measures the intensity of gas, fluid, water, or steam in a pressure-powered machine to ensure that no leaks or pressure changes occur.

The aerospace pressure gauge market is segmented based on gauge type, application, aircraft system, pressure sensor technology, and geography. By gauge type, the market is segmented into analog, digital, and others. By application, the market is classified into aviation and space. By aircraft system, the market is segmented into fuel system, hydraulics system, cabin pressure and ECS, engine and APU monitoring system, landing-gear and tire pressure monitoring system, avionics/pitot-static, and pneumatic systems.

The report also covers the market sizes and forecasts for the aerospace pressure gauge market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Analog |

| Digital |

| Others |

| Aviation | Commercial Aviation |

| Military Aviation | |

| General Aviation | |

| Unmannned Aerial Systems | |

| Space | Satellite |

| Spacecraft |

| Fuel System |

| Hydraulics System |

| Cabin Pressure and ECS |

| Engine and APU Monitoring System |

| Landing-Gear and Tire Pressure Monitoring System |

| Avionics/Pitot-Static |

| Pneumatic Systems |

| Piezoresistive |

| Capacitive |

| Piezoelectric |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Gauge Type | Analog | ||

| Digital | |||

| Others | |||

| By Application | Aviation | Commercial Aviation | |

| Military Aviation | |||

| General Aviation | |||

| Unmannned Aerial Systems | |||

| Space | Satellite | ||

| Spacecraft | |||

| By Aircraft System | Fuel System | ||

| Hydraulics System | |||

| Cabin Pressure and ECS | |||

| Engine and APU Monitoring System | |||

| Landing-Gear and Tire Pressure Monitoring System | |||

| Avionics/Pitot-Static | |||

| Pneumatic Systems | |||

| By Pressure Sensor Technology | Piezoresistive | ||

| Capacitive | |||

| Piezoelectric | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the aerospace pressure gauge market?

The aerospace pressure gauge market size is USD 23.03 million in 2026 and is forecasted to reach USD 25.43 million by 2031, growing at a 2.02% CAGR.

Which gauge type holds the largest share?

Analog instruments hold 55.92% of 2025 revenue, although digital units are growing faster at 3.12% CAGR.

Which region is expanding the quickest?

Asia-Pacific is the fastest-growing region, projected at a 5.59% CAGR through 2031 due to COMAC C919 and Indian defense programs.

What technology is gaining ground over piezoresistive sensors?

Capacitive MEMS sensors are advancing at a 4.4% CAGR because of superior temperature stability and lower power draw.

How are wireless TPMS modules affecting airline operations?

Certified wireless tire-pressure systems cut ground inspection time by up to 20 minutes per turnaround and reduce unscheduled maintenance events.

What is the main hurdle for new sensor entrants?

High certification costs, often exceeding USD 800,000 per variant, and extended approval timelines create significant barriers for newcomers.

Page last updated on: