Aerospace Floor Panels Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

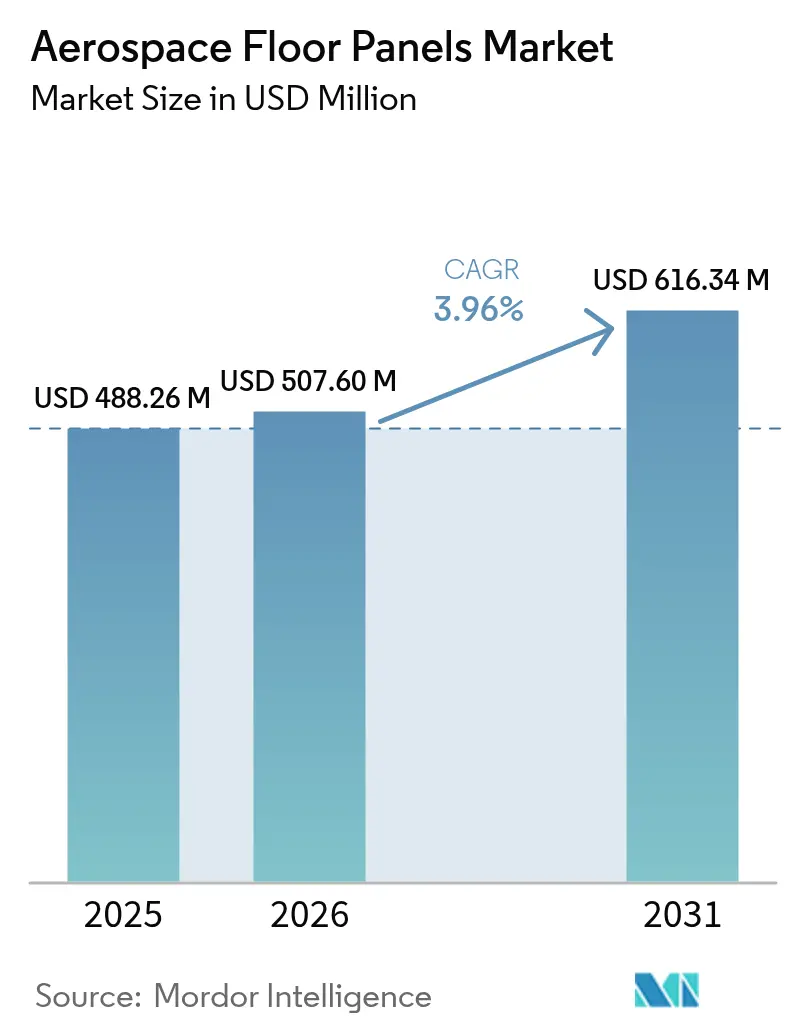

| Market Size (2026) | USD 507.6 Million |

| Market Size (2031) | USD 616.34 Million |

| Growth Rate (2026 - 2031) | 3.96% CAGR |

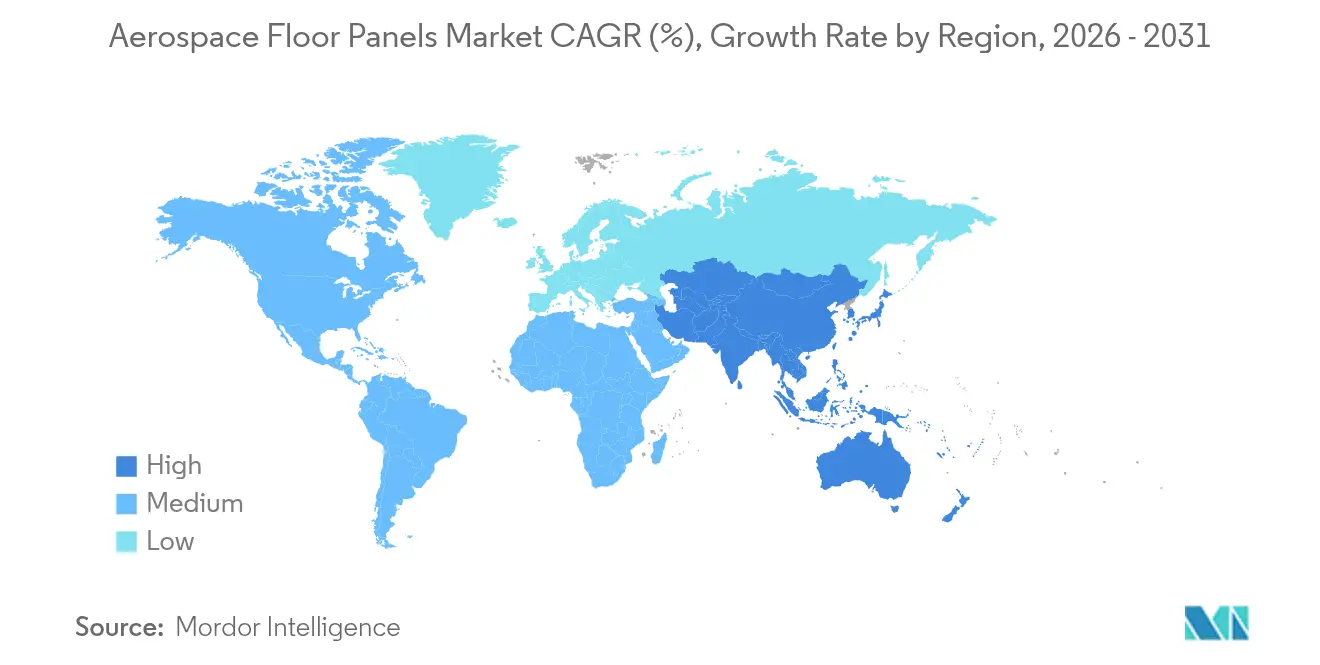

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace Floor Panels Market Analysis by Mordor Intelligence

Aerospace Floor Panels Market size in 2026 is estimated at USD 507.6 million, growing from 2025 value of USD 488.26 million with 2031 projections showing USD 616.34 million, growing at 3.96% CAGR over 2026-2031. Accelerated wide-body and narrow-body aircraft deliveries, stringent fuel-burn regulations, and rapid composite adoption continue to underpin demand. Airlines favour lightweight honeycomb panels that shave 20-30% off structural weight, delivering measurable fuel savings per flight. Strong order backlogs—Boeing alone projects 44,000 new aircraft through 2043—ensure a multiyear production runway. OEMs and tier suppliers are therefore scaling automated thermoplastic lines while investing in regional supply chains that mitigate raw-material uncertainty. Meanwhile, rising retrofit programs create a secondary revenue stream as operators refit legacy cabins to comply with updated FAR 25.853 fire-safety rules.

Key Report Takeaways

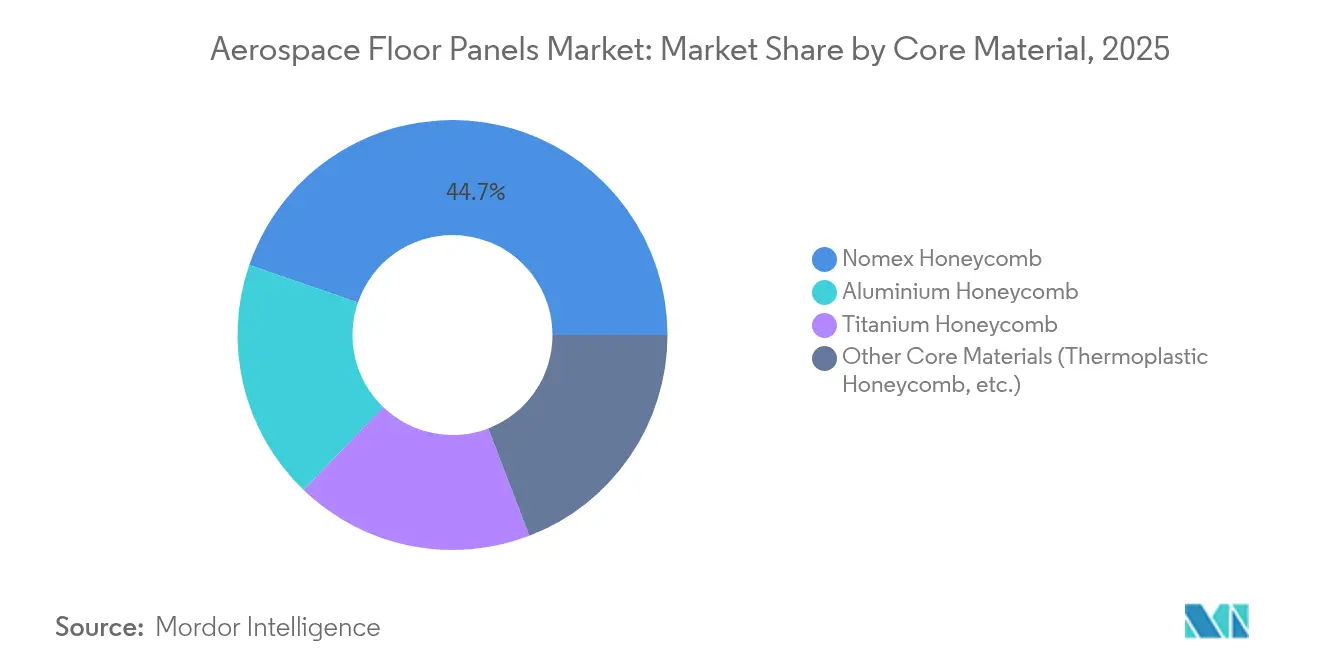

- By core material, Nomex honeycomb led with 44.72% aerospace floor panels market share in 2025, while thermoplastic honeycomb is forecast to expand at a 5.05% CAGR to 2031.

- By installation area, passenger cabin floors accounted for 58.03% of the aerospace floor panels market size in 2025 and are advancing at a 4.98% CAGR through 2031.

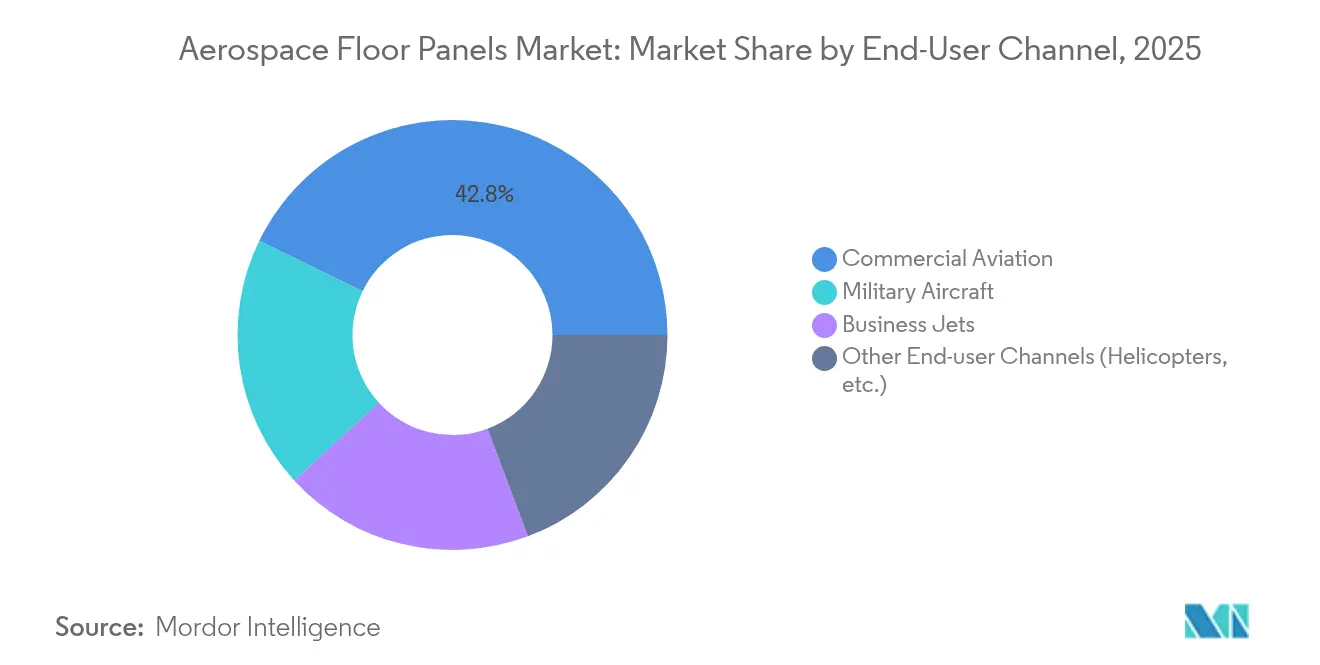

- By end-user channel, commercial aviation held 42.78% revenue share in 2025, whereas other end-user channels post the fastest 5.12% CAGR to 2031.

- By geography, North America commanded 38.21% share of the aerospace floor panels market in 2025, yet Asia-Pacific is set to record the highest 4.72% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aerospace Floor Panels Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing number of new-build & retrofit aircraft deliveries | +1.20% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Stringent fuel-burn & CO₂ regulations accelerating lightweighting | +0.90% | Global, led by EU and North America regulatory frameworks | Long term (≥ 4 years) |

| Rapid adoption of composite honeycomb floor panels | +0.80% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Low-cost carrier (LCC) expansion boosting narrow-body demand | +0.70% | Asia-Pacific core, spill-over to Latin America and MEA | Short term (≤ 2 years) |

| Additive-manufactured titanium honeycomb cores speeding MRO turnaround | +0.50% | North America & Europe, with selective adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Number of New-Build & Retrofit Aircraft Deliveries

Boeing forecasts just under 44,000 aircraft additions over the next two decades, with single-aisle models representing roughly three-quarters of the pipeline[1]Boeing, “Boeing Forecasts Demand for Nearly 44,000 New Airplanes Through 2043,” investors.boeing.com . Airlines increasingly schedule mid-life cabin overhauls that replace legacy aluminum boards with lighter honeycomb alternatives to secure immediate fuel savings. India anticipates 4,000 incremental airframes and 200 new airports within twenty years, amplifying retrofit prospects alongside new builds. China adds another growth vector: COMAC plans to lift C919 output to 75 units annually by 2029 to meet a domestic backlog topping 1,000 jets. Each incremental frame requires 30–50 m² of primary cabin flooring, guaranteeing a persistent demand baseline. Retrofit work also benefits MRO centres, which can install certified thermoplastic panels during heavy-check windows without altering structural load paths.

Stringent Fuel-Burn & CO₂ Regulations Accelerating Lightweighting

The European Fit-for-55 package and similar schemes worldwide obligate airlines to slash per-seat emissions, making cabin weight an actionable lever. Composite floor solutions cut panel mass by up to 30% versus aluminium, improving block fuel by roughly 0.5% on a narrow-body mission. Diehl Aviation’s ECO Sidewall, combining carbon fibre skins and Kepler honeycomb, shows how interior programmes integrate weight and waste reduction; the concept trims 10% mass and 33% scrap. Airlines also link lightweighting to sustainable aviation fuel economics because every kilogram saved extends SAF burn efficiency. Consequently, composite panel upgrades feature prominently in decarbonisation roadmaps filed with regulators or used to negotiate airport carbon charges.

Rapid Adoption of Composite Honeycomb Floor Panels

Thermoplastic advancements are removing historical cost and cycle-time barriers. EconCore’s ThermHex line extrudes continuous PP or PEEK honeycomb from a single sheet, achieving 4-6 × throughput gains while enabling full recyclability. Collins Aerospace mirrors this acceleration via automated fibre placement and fusion bonding on a next-generation nacelle programme slated for technology readiness level 6 by 2026. NASA’s HiCAM initiative corroborates scalability, targeting similar 4-6 × productivity leaps using co-curable thermoset and thermoplastic prepregs. Together, these innovations compress production bottlenecks that once limited composite penetration in high-volume narrow-body programmes.

Additive-Manufactured Titanium Honeycomb Cores Speeding MRO Turnaround

Laser-powder-bed technology is unlocking on-demand titanium honeycomb production for high-temperature floor assemblies in military and rotary platforms. GE Aerospace earmarked nearly USD 1 billion for U.S. additive facilities that include honeycomb prototyping cells targeting 40% cycle-time reductions on spares by 2027[2]GE Aerospace, “GE Aerospace to Invest Nearly USD 1B in U.S. Manufacturing in 2025,” geaerospace.com . While currently niche, printed cores alleviate raw-material bottlenecks and cut the logistical lead times that often ground aircraft awaiting replacement parts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility (aramid fibre, aluminium, titanium) | -0.60% | Global, with acute impact in North America and Europe | Short term (≤ 2 years) |

| Geopolitical supply-chain shocks for aerospace honeycomb cores | -0.40% | Global, concentrated in regions dependent on Eastern European and Russian suppliers | Medium term (2-4 years) |

| Certification delays for next-gen thermoplastic floor systems | -0.30% | North America & Europe regulatory jurisdictions, cascading to global markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Aramid Fibre, Aluminium, Titanium)

Global titanium output slid 12% between 2019 and 2024 as Ukrainian mining disruptions collided with export curbs, pressuring aerospace alloys. Aluminium costs remain sensitive to trade actions; U.S. tariffs of 25% on selected imports keep spot prices elevated relative to pre-trade-war averages. DuPont’s Nomex supply chain has also faced intermittent capacity constraints, triggering double-digit quarterly price swings for aramid paper used in honeycomb cores. OEMs respond by multisourcing, forward-buying, and engineering substitution options, but margin compression persists when contracts lock in catalog prices.

Geopolitical Supply-Chain Shocks for Aerospace Honeycomb Cores

Russia long supplied roughly 30% of commercial-grade titanium sponge used in Western programmes; sanctions now complicate that flow and extend qualification cycles for alternative smelters. Japan and Kazakhstan have ramped investment, yet aerospace certification requires multiyear testing. Meanwhile, honeycomb core conversion often clusters near titanium sources, so any upstream disruption ripples through panel capacity. Government mineral-security initiatives, including stockpiles and low-interest loans for new melt facilities, aim to buffer long-term exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Core Material: Thermoplastic Innovation Challenges Nomex Dominance

Nomex honeycomb retained 44.72% revenue in 2025, reflecting entrenched OEM specifications and a global supplier ecosystem tuned for high-volume output. Despite its lead, the aerospace floor panels market is tilting toward thermoplastic honeycomb, which is forecast to grow at 5.05% CAGR this decade. The performance uplift hinges on continuous-sheet technologies that marry mechanical strength with one-shot forming, thus cutting takt time and scrap. Thermoplastic boards also meet closed-loop recycling targets that regulators increasingly require. Aluminium honeycomb still finds favour in cargo decks where cost metrics trump every kilogram, while titanium cores remain vital for hot-zone floors on military transports. Additive-manufactured titanium promises future cost parity by eradicating machining waste and enabling lattice optimisation. Other experimental cores—ranging from basalt fibres to bio-resins—continue pilot testing with an eye on life-cycle carbon metrics.

Adoption trajectories vary by platform class. Narrow-body programmes lean toward PP and PEI thermoplastic variants because service temperatures rarely exceed 150 °C. Wide-body jets and long-range business aircraft prefer PEKK or PPS cores that withstand higher cabin floor loads and galley heat. Consequently, material suppliers pursue platform-specific qualification roadmaps rather than one-size strategies. Competition is intensifying as Asian compounders seek to undercut Western incumbents on cost while matching flame and smoke performance. Intellectual-property protection around core geometry remains a differentiator; patents on cell size gradients and edge-closure methods help vendors secure sole-source contracts. The aerospace floor panels industry therefore exhibits a dual dynamic: legacy Nomex supply chains deliver price stability at scale, whereas thermoplastic disruptors capture share through speed and sustainability credentials.

By Installation Area: Passenger Cabin Floors Drive Market Expansion

Passenger cabin floors generated 58.03% of 2025 revenue and will post the fastest 4.98% CAGR through 2031 as airlines refit densified layouts. Aircraft interiors teams view the cabin floor as prime territory for energy savings because it spans the entire passenger footprint. Installing a full set of advanced composite boards on a single-aisle jet can remove roughly 80 kg, equating to a lifetime fuel saving of near USD 250,000 under prevailing kerosene prices. Cabin reconfigurations escalate turnover because seat-track patterns must align precisely with floor-beam hard points; each time carriers move rows to tweak pitch, they often replace affected panels.

Cargo deck floors trail but still benefit from a projected need for 2,800 freighters by 2043, many converted from passenger airframes. Cockpit floors, galley zones, and lavatories collectively form a stable replacement market driven by avionics retrofit, food-service upgrades, and lavatory downsizing trends. Modular flooring kits are gaining popularity because line-maintenance crews can swap damaged panels during overnight stops, reducing AOG risk. Looking ahead, eVTOL developers are already specifying thermoplastic honeycomb in prototype cabins, potentially opening a nascent subsegment once urban air mobility certifies.

By End-User Channel: Commercial Aviation Leads as Other Channels Accelerate

Commercial carriers represented 42.78% of 2025 spending as major OEM lines in Renton, Toulouse, and Shanghai continued high monthly rates. The aerospace floor panels market size for commercial aviation is predicted to expand steadily given the multi-year delivery skyline. Yet the strongest 5.12% CAGR momentum comes from other end-user channels. Honeywell foresees 8,500 new business jets valued at USD 280 billion within ten years, with North America absorbing two-thirds of these units. High-net-worth buyers demand bespoke interiors, prompting panel suppliers to offer custom veneer faceskins and rapid-prototype core layouts.

On the defence side, floor panels must survive higher point loads from palletised cargo or armoured troop seats, leading to titanium or hybrid carbon-titanium constructions. Rotorcraft fleets add unique requirements such as anti-slip surfacing and vibration damping for medevac missions. MRO organisations increasingly stock thermoplastic spare panels because they can be trimmed on-site with heat-stapling tools, cutting turnaround during phase inspections. The aerospace floor panels industry therefore captures a broad usage spectrum, from volume-driven airlines to low-volume, high-margin bespoke jets, balancing commodity scale with premium engineering.

Geography Analysis

North America held 38.21% revenue share in 2025, thanks to an established manufacturing base stretching from Wichita through the Carolinas to Québec. Collins Aerospace’s USD 225 million footprint expansion across Fort Worth, Spokane, and Pueblo raised carbon brake and honeycomb capacity by more than 50% and secures long-term panel resin supply. Regional airline fleet renewal, including a 77-aircraft order from ANA Holdings for North American routes, reinforces order stability.

Asia-Pacific, however, is registering the quickest 4.72% CAGR. India’s requirement for 2,500-plus aircraft and aggressive airport expansion is reshaping supply-chain geography, with local composite shops popping up around Hyderabad and Bengaluru. China’s C919 advance, aided by annual rates of 75 units by 2029, accelerates domestic demand for compliant cabin components. Japan and South Korea are also incentivising locally sourced interiors under economic-security statutes, nudging global vendors to license technology or pursue JVs.

Europe leverages deep composites expertise clustered in Germany, France, and the UK. Programmes such as Diehl’s ECO Sidewall feed into Airbus interior packages, keeping the region influential in design authority decisions. Latin America and the Middle East show mixed growth tied to tourism recovery and LCC proliferation; both regions import most panels but could cultivate assembly hubs to sidestep shipping lead times. Collectively, these geographic currents ensure the aerospace floor panels market remains globally diversified while tilting toward Asia-centric volume growth.

Competitive Landscape

The aerospace floor panels industry features a moderately consolidated tier-one layer atop a long tail of regional players. Hexcel reported 11.8% commercial aerospace revenue growth in 2024 and showcased new honeycomb ranges at the 2025 Paris Air Show that boost out-of-plane compression by 15%. Collins, meanwhile, is verticalising thermoplastic nacelle know-how into floorboards, betting on common materials and robotic drilling to accelerate learning curves.

Strategic alliances dominate. Safran Cabin clinched the 2025 Crystal Cabin “IFEC & Digital Services” award for an integrated interior concept that relies on in-house honeycomb floor assemblies, signalling its intent to bundle panels with electrical and IFE routing. Gurit is expanding German prepreg lines while shutting higher-cost Swiss capacity, highlighting a pivot to regional specialisation.

Entry barriers stem from certification cost and knowledge capital. FAR 25.853 fire testing can swallow USD 2 million per material variant and takes nine to twelve months. Digital simulation is lowering trial iterations, yet incumbents still enjoy decades of statistical fire data that new entrants must replicate. Additive manufacturing is the wild card: if GE or similar OEMs prove repeatability at scale, smaller fabricators might leapfrog traditional core cutting, altering the competitive calculus. Patent landscapes around honeycomb geometry and edge sealing remain intense, prompting continuous litigation monitoring.

Aerospace Floor Panels Industry Leaders

Collins Aerospace

Comtek Advanced Structures Ltd.

Hexcel Corporation

The Gill Corporation

The NORDAM Group LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hexcel Corporation presented its latest advancements, including the honeycomb range products, for the Aerospace markets at the Paris Air Show 2025. These innovations are expected to significantly enhance the performance and durability of aerospace floor panels, driving growth in the market.

- April 2025: Safran Cabin, Safran Seats, Safran Passenger Innovations, and Safran Electronics & Defense jointly won the "IFEC & Digital Services" award at the Crystal Cabin Awards, which recognize innovations in aircraft interiors. As a producer of Honeycomb floor panels, this achievement is expected to strengthen Safran's position in the aerospace floor panel market.

Global Aerospace Floor Panels Market Report Scope

The aerospace floor panels market report includes:

| Nomex Honeycomb |

| Aluminium Honeycomb |

| Titanium Honeycomb |

| Other Core Materials (Thermoplastic Honeycomb, etc.) |

| Passenger Cabin Floor |

| Cargo Deck Floor |

| Cockpit Floor |

| Galley and Lavatory Zones |

| Commercial Aviation |

| Military Aircraft |

| Business Jets |

| Other End-user Channels (Helicopters, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Core Material | Nomex Honeycomb | |

| Aluminium Honeycomb | ||

| Titanium Honeycomb | ||

| Other Core Materials (Thermoplastic Honeycomb, etc.) | ||

| By Installation Area | Passenger Cabin Floor | |

| Cargo Deck Floor | ||

| Cockpit Floor | ||

| Galley and Lavatory Zones | ||

| By End-User Channel | Commercial Aviation | |

| Military Aircraft | ||

| Business Jets | ||

| Other End-user Channels (Helicopters, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the aerospace floor panels market?

The aerospace floor panels market size stands at USD 507.6 million in 2026 and is projected to reach USD 616.34 million by 2031.

Which core material holds the largest share?

Nomex honeycomb leads with 44.72% market share, although thermoplastic variants are growing the fastest.

Why are thermoplastic honeycomb panels gaining traction?

They deliver 4-6 × faster production cycles, enable recyclability, and meet emerging sustainability mandates without sacrificing structural performance.

Which region is expanding the fastest?

Asia-Pacific posts the highest 4.72% CAGR, driven by large aircraft backlogs in China and India and expanding local manufacturing capability.

How do fuel-burn regulations influence demand for floor panels?

Weight-saving composite panels help airlines meet CO₂ reduction targets and improve the cost effectiveness of sustainable aviation fuel uptake.

Page last updated on: