Graphite Anode For LIB Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

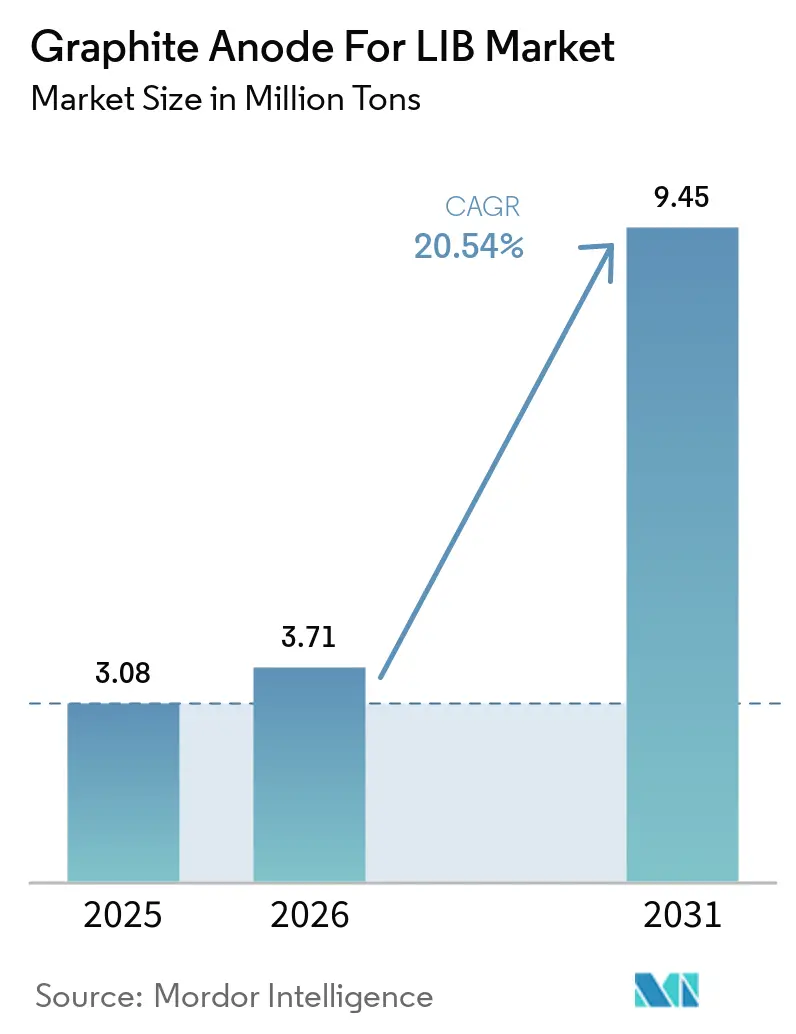

| Market Volume (2026) | 3.71 Million tons |

| Market Volume (2031) | 9.45 Million tons |

| Growth Rate (2026 - 2031) | 20.54% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Graphite Anode For LIB Market Analysis by Mordor Intelligence

The Graphite Anode For LIB Market size was valued at 3.08 million tons in 2025 and is estimated to grow from 3.71 million tons in 2026 to reach 9.45 million tons by 2031, at a CAGR of 20.54% during the forecast period (2026-2031). Global automakers and cell manufacturers are entering into long-term offtake contracts, marking a significant shift in commercial terms, capital allocation, and technical standards. While synthetic materials hold a first-mover edge in fast-charging and high-energy applications, natural graphite is gaining momentum, supported by the rising adoption of lithium-iron-phosphate in electric vehicles (EVs) and stationary storage. Tariffs, export controls, and inflation-linked subsidies are driving investments beyond China, pushing production closer to end markets, even as Chinese suppliers dominate the reference price curve. Producers are now compelled to address emerging demand pools and technology hedges, such as long-duration energy-storage systems, silicon-blended anodes, and low-emission purification routes, to secure multi-year offtake commitments.

Key Report Takeaways

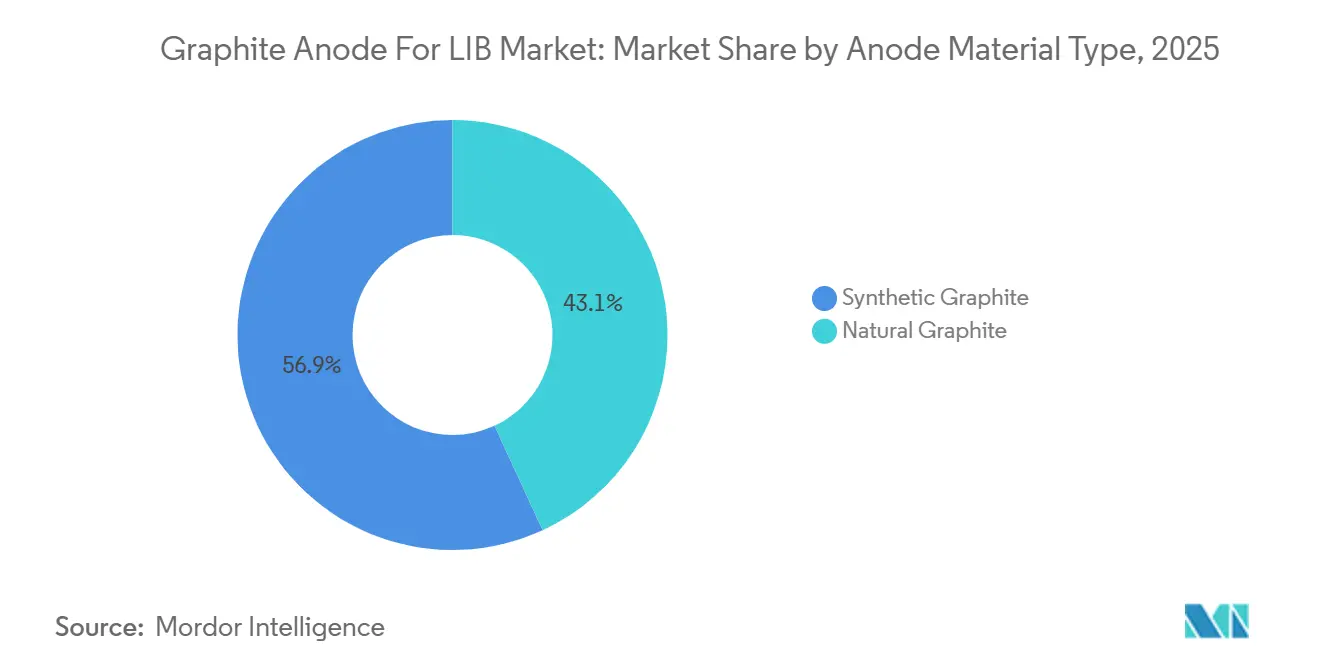

- By anode material type, synthetic graphite accounted for 56.89% of the graphite anode market share in 2025; natural graphite is projected to expand at a 25.21% CAGR through 2031.

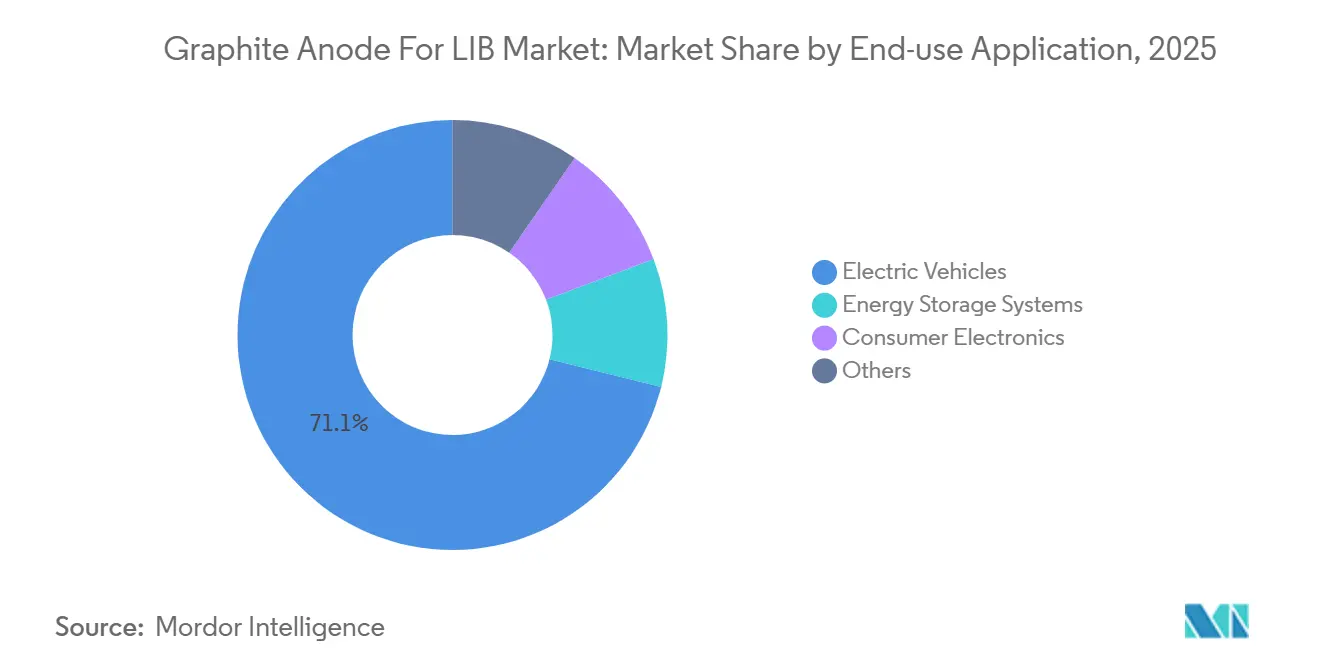

- By end-use application, electric vehicles dominated the 2025 market with 71.12% of the volume, while energy storage systems are forecast to grow at a 22.23% CAGR through 2031.

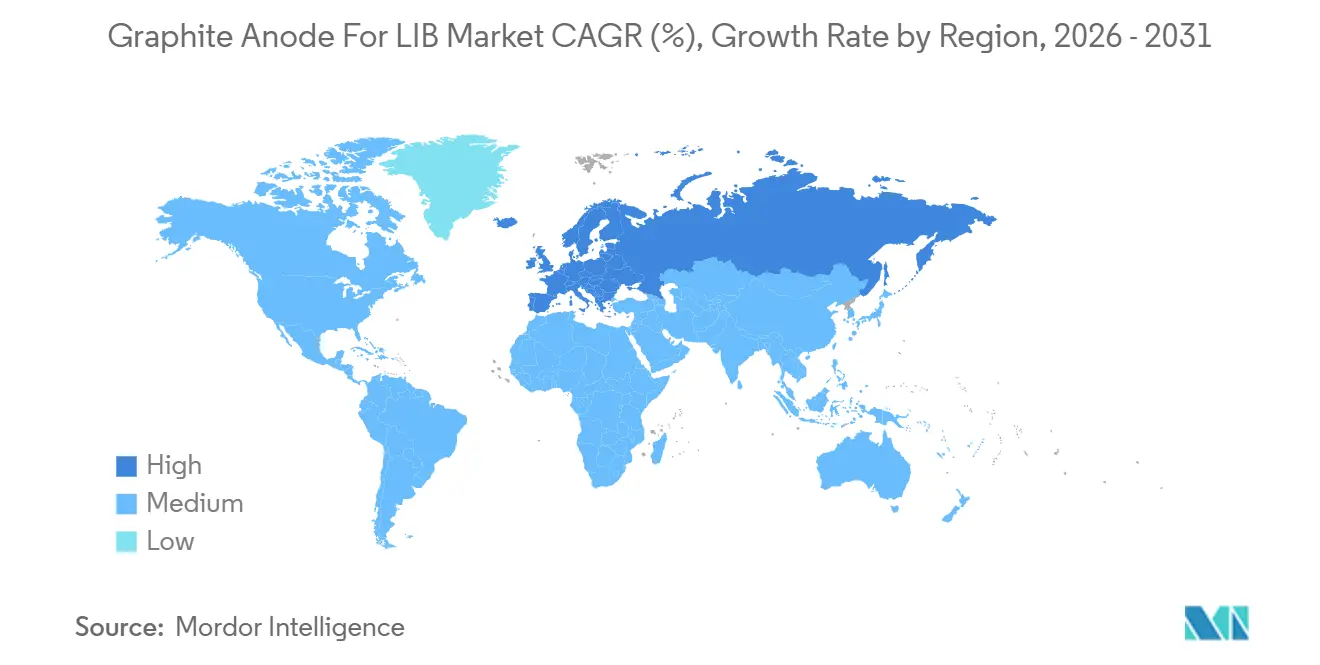

- By geography, the Asia-Pacific region accounted for 74.22% of 2025 shipments, whereas Europe is set to register the fastest growth of 28.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Graphite Anode For LIB Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EV-driven Li-ion cell capacity expansions | +6.5% | Global, with concentration in China, EU, North America | Medium term (2-4 years) |

| Cost decline of synthetic graphite from Chinese scale-ups | +4.2% | APAC core, spill-over to North America and EU | Short term (≤ 2 years) |

| Government incentives for domestic battery supply chains | +3.8% | North America, EU, India | Long term (≥ 4 years) |

| Adoption of high-rate pouch and prismatic architectures in ESS micro-grids | +2.5% | Global, early gains in China, US, Australia | Medium term (2-4 years) |

| Industrialization of fluorine-free coating and thermal purification | +1.8% | Global, led by Japan, South Korea, emerging in EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging EV-Driven Li-Ion Cell Capacity Expansions

From 2026 to 2031, the announcement of numerous new cell projects is expected to lead to a notable uptick in anode demand. Each GWh of capacity requires the active material, prompting OEMs to secure multi-year offtake agreements instead of relying on spot procurement, in an effort to stabilize pricing and volumes. Prismatic and blade cell formats accommodate more anode material per unit volume compared to cylindrical counterparts, driving a surge in graphite demand even as vehicle production stabilizes. Furthermore, the industry’s push for rapid charging - targeting a 10%-to-80% charge in under 15 minutes - underscores the importance of precise particle-size control. While this focus increases capital intensity, it simultaneously offers a unique product differentiation edge in the graphite anode market for lithium-ion batteries (LIBs).

Cost Decline of Synthetic Graphite from Chinese Scale-Ups

By 2025, Chinese producers reduced factory costs by strategically placing graphitization furnaces next to captive power sources and needle-coke feedstock. This approach significantly widened the cost gap with Western competitors. Additionally, reusing waste heat reduced electricity consumption, while long-term feedstock contracts protected margins from market fluctuations. Starting in 2026, European carbon border adjustment tariffs are expected to increase costs for imported synthetic graphite. This change reduces the cost advantage for imports and enhances the value of local low-carbon initiatives. Consequently, non-Chinese suppliers are focusing on monetizing the sustainability attributes of their products rather than relying solely on pricing. This shift underscores the growing importance of sustainability in the graphite anode segment of the lithium-ion battery market during the forecast period of 2026–2031.

Government Incentives for Domestic Battery Supply Chains

Section 30D of the Inflation Reduction Act stipulates that by 2026, a specified percentage of a battery component's value must derive from North America, with this requirement tightening in the subsequent year. This regulation effectively redirects anode sourcing away from China. Loan guarantees and advanced manufacturing credits are making it easier to establish new production capacities. For instance, projects in Tennessee and Alaska-Ohio are expected to achieve a significant combined output in the near future. Concurrently, India's production-linked incentive, in tandem with the EU Innovation Fund, is channeling considerable grants and concessions. This strategy is cultivating regional champions who prioritize supply security over mere cost considerations. Such policy shifts are strengthening the graphite anode market for lithium-ion batteries across multiple continents.

Adoption of High-Rate Pouch and Prismatic Architectures in ESS Micro-Grids

Regions with significant photovoltaic (PV) installations are increasingly adopting batteries for daily cycling, which is essential for grid balancing. Pouch and prismatic cells not only simplify rack design but also reduce interconnects, leading to a reduction in the balance-of-system costs[1]Tesla, “Megapack Cost and Volume Update,” ir.tesla.com. The demand for longer discharge windows of 4 to 8 hours necessitates thicker electrodes, which, in turn, increases the anode mass per cell and aligns it with the cost profile of natural graphite. Chinese producers, closely monitoring market trends, are expanding their spheroidization lines with ambitious annual capacity targets. This strategic move highlights how specifications for Energy Storage Systems (ESS) can influence decisions regarding upstream materials. As a result, utility procurement is increasingly reinforcing the graphite anode's significance in the Lithium-Ion Battery (LIB) market, reducing its dependence on the fluctuations of electric vehicle (EV) cycles.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emissions scrutiny on graphitisation furnaces | -2.3% | Global, most acute in EU and China | Short term (≤ 2 years) |

| Shift toward Si-rich and Li-metal anodes | -1.8% | North America, EU, Japan (premium segments) | Medium term (2-4 years) |

| Volatility in needle-coke pricing amid steel decarbonisation | -1.2% | Global, supply concentrated in China, Japan, US | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Emissions Scrutiny on Graphitization Furnaces

The graphitization process, essential for producing synthetic graphite, demands a considerable amount of energy and can emit significant CO₂, particularly when reliant on coal-fired grids. The increase in EU carbon tariffs has raised the landed costs of materials imported from China. Automakers are now mandating Scope 1-3 disclosures, with the risk of exclusion from RFQ shortlists for non-compliance. In late 2024, regulatory shocks were highlighted when inspections in China prompted the temporary shutdown of multiple sites, tightening supply. The estimated capital expenditure for a typical plant to establish renewable power connections remains a substantial financial challenge. This issue is especially pronounced for smaller producers, dampening the growth outlook for the graphite anode market in lithium-ion batteries.

Shift Toward Si-Rich and Li-Metal Anodes

Silicon-graphite blends enhance energy density, allowing premium EVs to extend their range without increasing the pack volume. By 2025, both Mercedes-Benz and BMW had incorporated silicon content into their high-end models[2]Sila Nanotechnologies, “Titan Silicon in Series Production,” silanano.com. Although solid-state lithium-metal prototypes have achieved significant milestones, they remain considerably more expensive than traditional chemistries. While the premium vehicle segment can accommodate higher costs, this is not feasible for mass-market vehicles. These technological advancements may reduce the pure graphite share in luxury segments. However, with scale-up timelines extending beyond 2028, graphite continues to play a central role in mainstream battery designs. This trend reinforces graphite's pivotal role in the medium-term landscape of the LIB market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Anode Material Type: Cost-Focused Natural Growth against Performance-Driven Synthetic

In 2025, premium EV platforms, seeking first-cycle efficiency rates above a certain threshold, propelled synthetic graphite to a 56.89% market share. On the other hand, natural graphite is projected to post a 25.21% CAGR through 2031, fueled by the growing adoption of lithium-iron-phosphate chemistries in budget-conscious sectors. BYD’s Blade Battery, which harnesses natural graphite, made significant inroads into the domestic EV market in 2025, highlighting a pathway to competitive pricing. While China retains a stronghold over spheroidization capacity, the United States made its mark with the 2024 debut of the Vidalia line in Louisiana, the nation's first large-scale facility, which has already inked an offtake agreement with Tesla. Synthetic producers, enjoying the benefits of vertical integration and meticulous control over fine particle distribution, grapple with pressures from Scope 3 emissions. This challenge has spurred automakers to co-invest in more sustainable, low-carbon natural alternatives. As the landscape shifts, the once-accelerating growth of synthetic materials in graphite anodes for the LIB market is now slowing, while natural materials are witnessing a swift ascent, suggesting a potential balance in their distribution.

By End-Use Application: EV Dominance Meets ESS Acceleration

Electric vehicles captured 71.12% of 2025 demand thanks to multi-year subsidy programs in China and early adoption in Europe. Energy-storage systems are compounding at 22.23% through 2031, driven by utility mandates for renewable integration and a decline in pack-level costs. Tesla increased its shipments of Megapack units, while CATL’s Tener container set new benchmarks for energy density per rack. The consumer electronics sector contracted significantly, primarily due to extended product cycles for handsets and laptops. Regulatory traceability rules, scheduled to take effect by 2027, are expected to increase compliance costs for smaller mobility devices. This development is likely to accelerate industry consolidation and redirect some production capacity toward grid applications. Collectively, these factors ensure that the graphite anode market for lithium-ion batteries maintains a diversified demand base, providing resilience against downturns in specific sectors during the forecast period of 2026–2031.

Geography Analysis

In 2025, Asia-Pacific accounted for a 74.22% share of the global market, underscoring the depth of China's integrated supply chains, which stretch from needle-coke production to cell assembly. In response to export controls on spheroidized natural graphite and rising domestic tariffs, OEMs have begun dual-sourcing from emerging plants in the United States, Europe, and India. After a leading producer in Japan rationalized its capacity, the nation's shipments saw a decline in 2025. Meanwhile, South Korea is shifting its focus to silicon blends to sidestep direct price competition. Marking a significant milestone, India is set to introduce a substantial volume into the graphite anode market for lithium-ion batteries (LIB) by 2027, thanks to its incentive program.

Europe is poised for a 28.12% CAGR through 2031, buoyed by a modest base in 2025 and bolstered by the Innovation Fund and national strategic autonomy initiatives. France and Germany spearhead most projects, with key players benefiting from grants and power price guarantees, significantly reducing their venture risks. The EU Battery Regulation mandates complete supply-chain traceability starting in 2027, a move likely to centralize production within the bloc. While Italy and the United Kingdom are currently honing in on cathode production and cell assembly, it is indicative that intra-EU cross-border flows will soon become standard in the graphite anode market for LIBs.

In North America, the expansion is primarily fueled by subsidies rather than market prices. Projects in Tennessee, Ontario, and Ohio are on track to surpass a combined nameplate capacity sufficient to satisfy a substantial portion of the region's demand. Canada's investment tax credit enhances the economic appeal, while long-term contracts for renewable power help in reducing Scope 2 emissions. However, Mexico's concentration on cell assembly, coupled with its limited upstream graphite capabilities, underscores a vulnerability in the continent's supply resilience.

Competitive Landscape

The graphite anode market for LIBs is moderately consolidated. The graphite anode market for lithium-ion batteries (LIBs) is undergoing a notable transformation. Western companies are capitalizing on subsidies and prepayments from the automotive sector, reshaping the market dynamics. Chinese suppliers, who have long held a dominant position, are utilizing vertical integration and economies of scale to maintain their cost leadership. In contrast, newly established Western plants are prioritizing carbon-footprint transparency, making them more appealing to customers aiming for incentive eligibility. Following the footsteps of CATL, leading automakers are increasing their equity stakes in upstream producers, securing volume allocations during potential shortages. The race for process innovation is intensifying: advancements such as water-based binders, purification at lower temperatures, and the use of silicon-carbon composites are not only reducing capital costs but also attracting buyers with a focus on sustainability.

Graphite Anode For LIB Industry Leaders

Beterui New Materials Group Co. Ltd

Shanghai Putailai New Energy Technology Co. Ltd

Shanshan Co. Ltd

POSCO CHEMICAL

Guangdong Kaijin New Energy Technology Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Northern Graphite and Al Obeikan Group for Investment Company signed a term sheet for a USD 200 million battery anode material (BAM) plant in the Kingdom of Saudi Arabia. Phase I of the BAM production is projected to have a capacity of 25,000 tons per year by 2028.

- July 2025: POSCO Future M signed an anode material supply contract with a Japanese battery company. The company plans to produce natural graphite anode materials at its Sejong plant and supply them for electric vehicle batteries manufactured in Japan.

Global Graphite Anode For LIB Market Report Scope

Graphite anodes are the most common anode material in lithium-ion batteries (LIBs), where layers of carbon atoms provide a stable structure for lithium ions to be stored during charging and released during discharging.

The graphite anode for the LIB market is segmented by anode material type, end-use application, and geography. By anode material type, the market is segmented into synthetic graphite and natural graphite. By end-use application, the market is segmented into electric vehicles, energy storage systems, consumer electronics, and others (including power tools and e-mobility). The report also covers the market size and forecasts for the market in 12 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD) and volume (Tons).

| Synthetic Graphite |

| Natural Graphite |

| Electric Vehicles |

| Energy Storage Systems |

| Consumer Electronics |

| Others (Power Tools and e-Mobility) |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Rest of the World |

| By Anode Material Type | Synthetic Graphite | |

| Natural Graphite | ||

| By End-use Application | Electric Vehicles | |

| Energy Storage Systems | ||

| Consumer Electronics | ||

| Others (Power Tools and e-Mobility) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Rest of the World | ||

Key Questions Answered in the Report

How large will global demand for graphite anodes be by 2031?

The Graphite Anode for LIB Market size was valued at 3.08 million tons in 2025 and is estimated to grow from 3.71 million tons in 2026 to reach 9.45 million tons by 2031, at a CAGR of 20.54% during the forecast period (2026-2031).

Which end-use segment is expanding the quickest?

Energy-storage systems lead growth at a 22.23% CAGR through 2031 as utilities deploy long-duration batteries.

Why are automakers seeking local anode suppliers?

Tariff structures and clean-vehicle tax credits require North American or European content to unlock buyer incentives, driving regional capacity investments.

What share does natural graphite hold today?

Natural graphite accounted for 43.11% of volume in 2025 and is on track to achieve a 25.21% CAGR through 2031.

Are silicon-rich anodes a near-term threat to graphite?

Silicon-graphite blends are gaining traction in luxury models but remain cost-prohibitive for mass-market EVs, so graphite will stay dominant through 2031.

Page last updated on: