Aerospace And Defense Robotic Automation Actuators Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

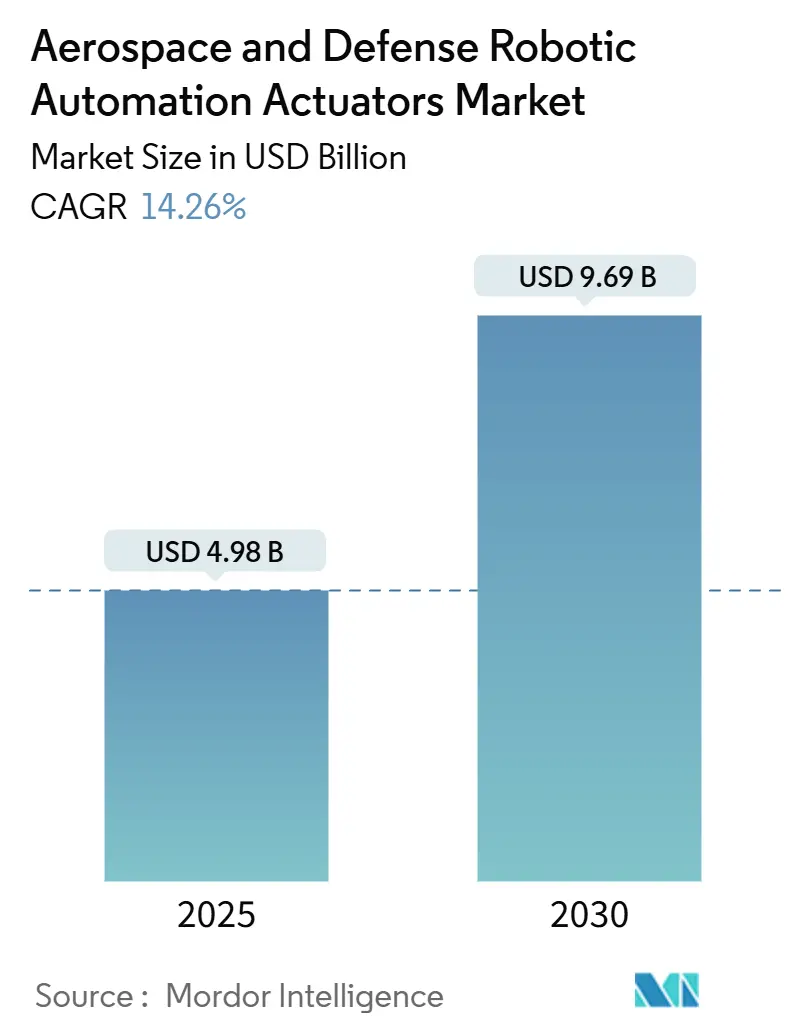

| Market Size (2025) | USD 4.98 Billion |

| Market Size (2030) | USD 9.69 Billion |

| Growth Rate (2025 - 2030) | 14.26% CAGR |

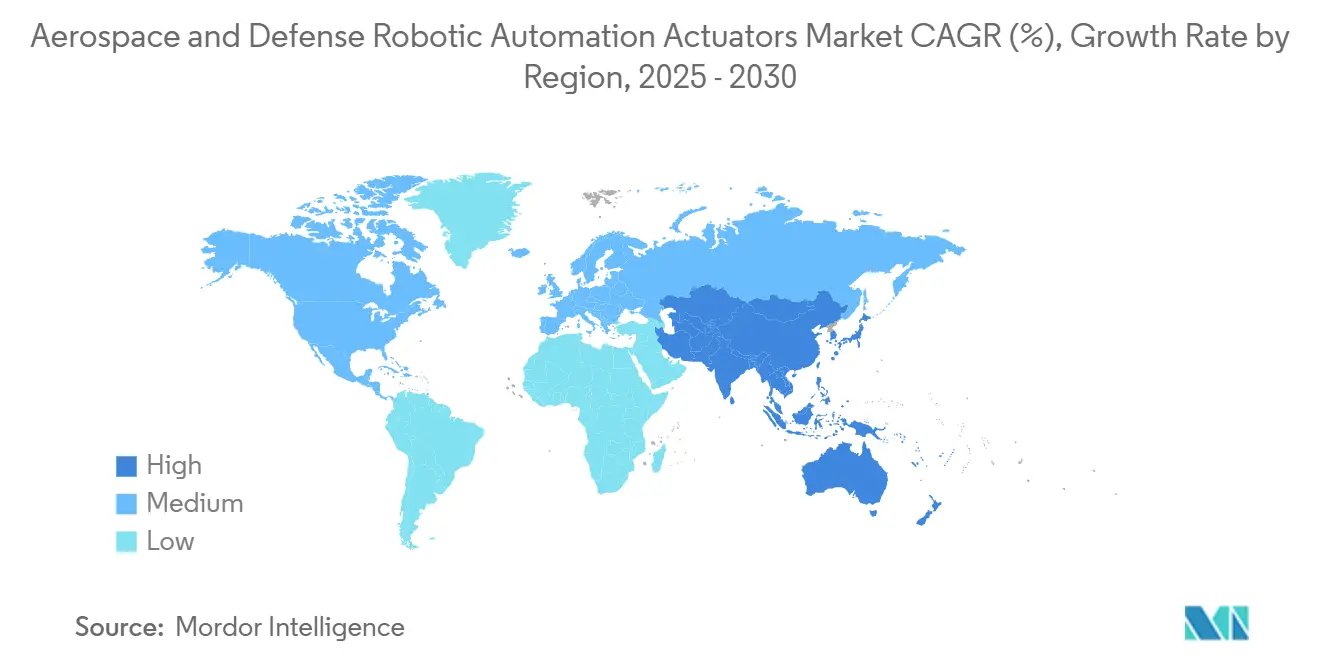

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace And Defense Robotic Automation Actuators Market Analysis by Mordor Intelligence

The aerospace and defense robotic automation actuators market size is USD 4.98 billion in 2025 and is forecasted to hit USD 9.69 billion by 2030, expanding at a 14.26% CAGR through the period. Demand accelerates as next-generation aircraft, spacecraft, and unmanned platforms replace fluid-power systems with lighter electro-mechanical solutions, pursue autonomous operations, and embed real-time health monitoring. Commercial jet programs sustain volume, while defense modernization and the rise of new-space ventures layer additional opportunities. Consolidation is reshaping supply lines, with large suppliers buying niche specialists to secure electric-actuation know-how and certification capabilities. Persistent supply-chain vulnerability around rare-earth magnets and the cost of cyber-hardening embedded networks temper growth but do not derail the long-term shift to digital, fault-tolerant motion control.

Key Report Takeaways

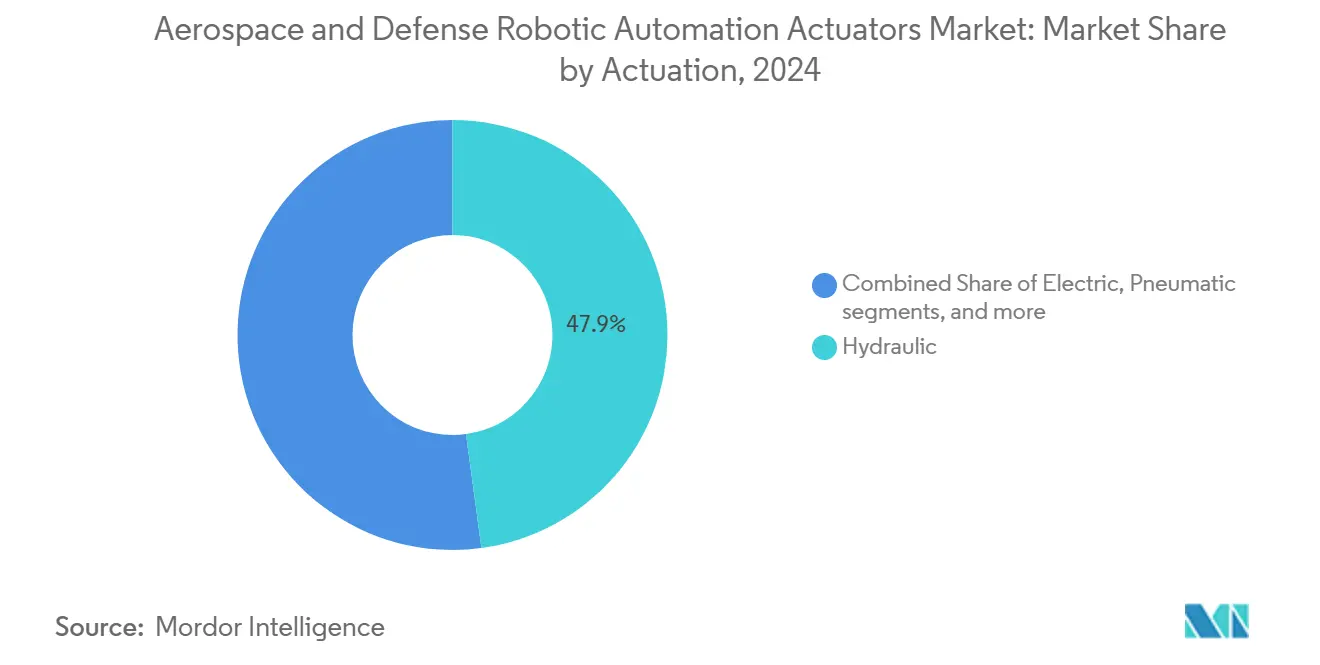

- By actuation type, hydraulic systems held 47.85% of the aerospace and defense robotic automation actuators market share in 2024, while electro-mechanical designs are set to grow at a 13.76% CAGR to 2030.

- By component, sensors and encoders commanded a 39.68% share of the aerospace and defense robotic automation actuators market size in 2024; controllers and software are projected to climb at a 14.87% CAGR through 2030.

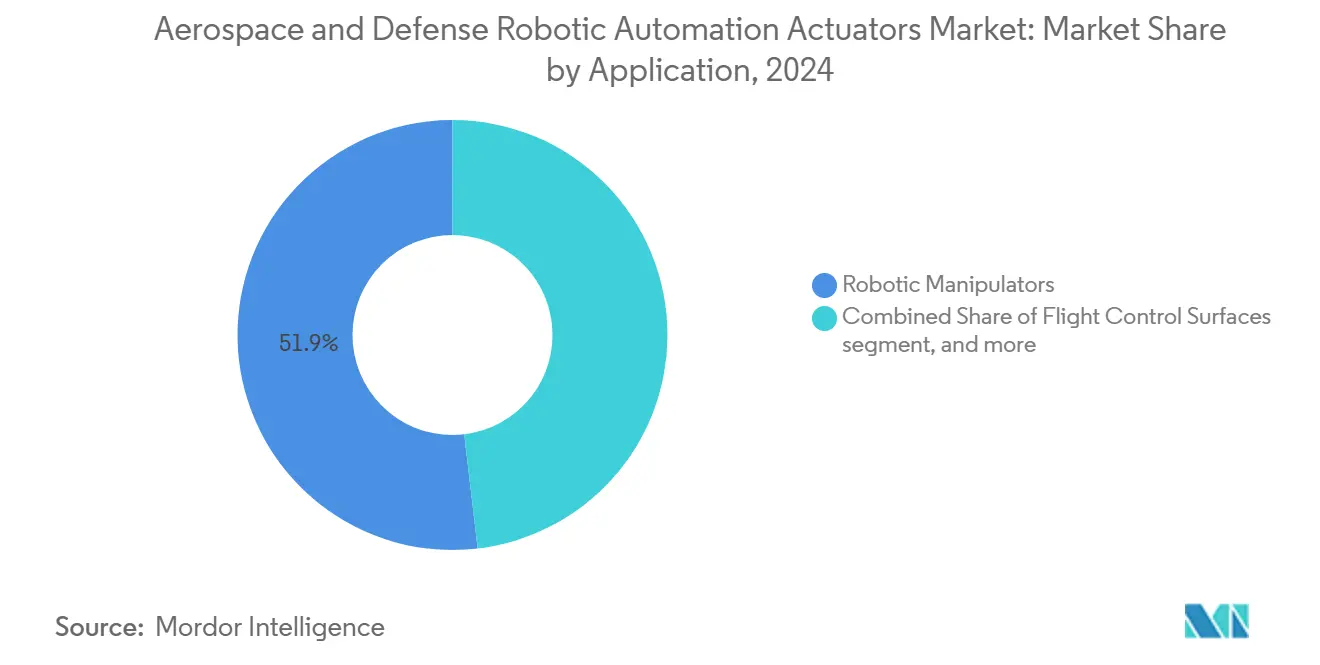

- By application, robotic manipulators led with 51.87% revenue share in 2024; satellite and space robotics is advancing at a 15.84% CAGR during the forecast window.

- By end user, commercial aerospace OEMs accounted for a 60.49% share of the aerospace and defense robotic automation actuators market in 2024. In contrast, space agencies and new-space firms posted the strongest 14.92% CAGR outlook.

- By geography, North America captured 40.21% of the aerospace and defense robotic automation actuators market in 2024, and Asia-Pacific is on track for a 14.38% CAGR to 2030.

Global Aerospace And Defense Robotic Automation Actuators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for fault-tolerant electric flight-control actuators | +2.80% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rapid defense adoption of robotic unmanned ground vehicle (UGV) actuators | +2.10% | North America, APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Lightweight composite gear-train innovations lowering SWaP | +1.90% | Global, concentrated in aerospace hubs | Medium term (2-4 years) |

| DoD “Zero Hydraulic Lines” mandate for next-gen aircraft | +2.30% | North America, with NATO alignment | Long term (≥ 4 years) |

| SpaceX-style vertically integrated actuator production models | +1.40% | North America, expanding to APAC | Long term (≥ 4 years) |

| Rising call-off contracts for modular maintenance-free UAV servos | +1.70% | Global, defense-focused regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Fault-Tolerant Electric Flight-Control Actuators

Commercial and military programs are migrating to triple-redundant electromechanical actuators that tolerate single-point failures, incorporate real-time health sensors, and enable graceful degradation during flight.[1]787 Dreamliner Systems Architecture, Boeing Company, boeing.com Health-aware algorithms predict failures before they occur and re-route loads across redundant channels, cutting unplanned maintenance and lifting dispatch reliability. The feature set aligns with autonomous flight ambitions in defense and advanced air mobility. As major airframers lock in “all-electric” architectures, suppliers can certify multi-lane safety electronics and integrated power drives, and gain preferential linefit positions.

Rapid Defense Adoption of Robotic Unmanned Ground Vehicle Actuators

Armed forces fielding robotic combat vehicles specify actuators that combine high torque density with electromagnetic-pulse shielding and secure command links.[2]Robotic Combat Vehicle Program, U.S. Army, army.mil The US Army’s tracked RCV prototypes require precise gimbal motion for turrets and manipulators under cyber attack. Similar demands surface in Australia, South Korea, and Poland, translating to accelerated procurement cycles and long-tail spares agreements. Civil-origin robotics firms now pivot to hardened variants, fragmenting incumbent defense supply chains and compressing margins.

Lightweight Composite Gear-Train Innovations Lowering SWaP

Carbon-fiber reinforced gear sets can shave 40-50% mass while sustaining aerospace-grade torque, directly improving aircraft range and satellite delta-V budgets.[3]Advanced Actuator Technologies, Curtiss-Wright Corporation, curtisswright.com Advanced resin‐transfer molding lifts batch consistency, permitting inclusion in safety-critical listings. Electric vertical-takeoff-and-landing (VTOL) developers place composite gearboxes high on bill-of-materials lists to offset battery weight, giving material science a competitive edge. As acceptance test procedures mature, composite internals are forecast to permeate landing gear and thrust-vectoring systems.

DoD “Zero Hydraulic Lines” Mandate for Next-Gen Aircraft

US defense planners have instructed platform primes to eliminate on-board hydraulics to cut infrared signatures, fire risk, and maintenance hours. The directive underpins future fighter and rotorcraft roadmaps and is echoed by European partners. Vendors must deliver electro-mechanical units that rival 5,000 psi hydraulic force levels without overheating or electromagnetic interference. Qualification programs on legacy F-35 flight-control channels offer data, yet mass adoption hinges on next-generation power-dense motors and fault-tolerant power electronics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Qualification bottlenecks for safety-critical electro-mechanical drives | -1.80% | Global, stringent in North America and Europe | Medium term (2-4 years) |

| Rare-earth magnet supply-chain vulnerability | -2.10% | Global, acute in Western markets | Short term (≤ 2 years) |

| Defense export‐control compliance delays (ITAR, EAR) | -1.30% | North America and allied nations | Medium term (2-4 years) |

| Cyber-hardening costs for networked robotic joints | -1.10% | Global, priority in defense applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Qualification Bottlenecks for Safety-Critical Electromechanical Drives

Regulators demand multi-year test campaigns, hardware-in-loop simulation, and extensive failure-mode analysis before electric drives can replace hydraulics on primary flight surfaces. Smaller firms struggle to fund the required test rigs and documentation, so primes often dual-source with incumbents. Laboratory certification slots remain scarce, creating backlogs that slow market entry and extend program schedules.

Rare-Earth Magnet Supply-Chain Vulnerability

Neodymium and dysprosium supplies remain concentrated in China, exposing Western actuator programs to political risk and price spikes. Hedge strategies include recycling scrap magnets, qualifying heavy-rare-earth-free motor designs, and stockpiling. Each path raises procurement cost or technical complexity, and none eliminates exposure until alternate refining capacity matures in the US or Australia.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Actuation: Electromechanical Systems Drive Future Growth

Hydraulic devices retained a 47.85% share of the aerospace and defense robotic automation actuators market in 2024, supported by entrenched use on legacy fleets. Electro-mechanical units, helped by integrated power electronics and improved torque density, are posting a 13.76% CAGR and will erode hydraulic dominance well before 2030. Adoption is strongest on new commercial widebodies and reusable launch vehicles, where maintenance-free operation outweighs absolute force headroom. The aerospace and defense robotic automation actuators market size for electro-mechanical products is forecasted to climb rapidly as DoD zero-hydraulic mandates mature and new entrants replicate vertical integration economics. Electro-hydrostatic modules offer a bridging option for refit programs that cannot yet power fully electric spools but still aim to shed centralized pipes.

The performance leap rests on rare-earth magnet brushless motors, dual-redundant position feedback, and compact harmonic drives. Qualification testbeds run environmental cycles from –55 °C to 125 °C and 15 g vibration. Moog reports its aerospace electro-mechanical line as its fastest-growing, gaining USD 1.2 billion in revenue in 2024 and targeting commercial narrowbody refreshes from 2027 onward. Field data show 30% maintenance-hour savings versus legacy hydraulics, reinforcing the payback case for airline retrofit even absent a regulatory push.

By Component: Software Integration Reshapes Value Chains

Sensors and encoders represented 39.68% of the aerospace and defense robotic automation actuators market share in 2024, underlining how precision feedback is foundational to closed-loop control. Yet controllers and software register the quickest 14.87% CAGR as AI-enabled edge compute bloats code bases and elevates cybersecurity requirements. Suppliers bundle dedicated safety processors that monitor torque balance and drive phase currents in real time, automatically reconfiguring operating modes when anomalies trip thresholds. The aerospace and defense robotic automation actuators market size attached to software expands faster than hardware alone, pulling margins higher for vendors with embedded-systems depth.

Motors and drives consume significant revenue but face material-cost swings tied to magnet pricing. Gearboxes evolve through additive manufacturing of lattice structures and composite meshes that drop inertial mass. Curtiss-Wright’s purchase of a niche sensor house in 2024 signals intent to lock down vertical stacks that stretch from Hall-effect arrays to prognostic dashboards. Integration simplifies certification packages and appeals to OEMs that want single-throat support for linefit.

By Application: Space Robotics Accelerates Beyond Traditional Aerospace

Robotic manipulators dominated with 51.87% revenue share in 2024, thanks to entrenched use in aircraft assembly, missile handling, and ground-vehicle turrets. However, satellite and space robotics applications hold a 15.84% CAGR, transforming the opportunity profile by pushing extreme thermal and radiation‐hardening requirements. The aerospace and defense robotic automation actuators market size attached to orbital use will more than double by 2030 as multi-sat megaconstellations and lunar logistics assets proliferate.

Space-grade mechanisms demand dry-lubricated joints, micro-stepping motors, and out-gassing-controlled harnesses. Heritage aerospace vendors extend product certs from the International Space Station era, but new-space firms favor rapid iteration and in-house build. NASA’s Artemis lander robot arms illustrate the jump in torque per kilogram achievable with carbon-composite geartrains, demonstrating 45 Nm output at under 1 kg package mass.[4]Artemis Program Actuator Requirements, NASA, nasa.gov High-rate launch cadence from reusable rockets further normalizes off-the-shelf avionics and actuators, shrinking lead times from years to months.

By End User: Commercial Aerospace OEMs Lead as New-Space Players Surge

Commercial aerospace OEMs captured 60.49% of the aerospace and defense robotic automation actuators market share in 2024, reflecting sustained narrowbody and widebody production lines alongside ongoing fleet upgrades. The dominance stems from airframers’ push for lighter, maintenance-free electro-mechanical units that improve dispatch reliability and cut hydraulic fluid handling. Volume contracts with Boeing and Airbus anchor baseline demand and create high entry barriers for smaller suppliers that lack comprehensive certification libraries. Defense OEMs remain a sizeable but slower-growing cohort as modernization cycles align with fiscal budgets and stringent export-control timelines. MRO and retrofit organizations provide a steady aftermarket pull by installing drop-in electric actuators on legacy fleets to extend service life and reduce maintenance labor.

Space agencies and new-space firms are expanding at a 14.92% CAGR, positioning them as the fastest-growing customer group through 2030. The aerospace and defense robotic automation actuators market size tied to these entities is climbing as satellite megaconstellations, lunar logistics programs, and reusable launch vehicles demand radiation-hardened, lightweight motion systems with integrated diagnostics. Vertical integration strategies pioneered by SpaceX compress lead times and favor suppliers that can deliver modular, software-rich actuators in high volumes. National space organizations in China, India, and Japan are broadening local supply chains, further diversifying end-user demand beyond traditional Western agencies. Together, these trends redistribute revenue streams across the aerospace and defense robotic automation actuators industry while reinforcing the long-term pivot toward intelligent, networked, and fully electric motion control.

Geography Analysis

North America, holding a 40.21% share in 2024, benefits from Tier 1 OEM concentration, the US DoD zero-hydraulic roadmap, and NASA's Artemis lunar campaign. Several vertically integrated new-space builders source actuators domestically, bolstering the region's supply-chain resilience despite rare-earth concerns. Canada leverages composite materials know-how in Quebec and Ontario hubs, while Mexico's Baja California cluster continues to absorb labor-intensive machining.

Asia-Pacific posts the highest 14.38% CAGR, powered by China's heavy investment in reusable launchers and stealth fighters, India's focus on indigenous satellite buses, and Japan's digital mainstreaming of defense production. Government mandates for local content encourage joint ventures with Western actuator specialists, phasing in technology transfer and building regional ecosystem depth. South Korea's K-drone and armoured-vehicle programs add a steady pull, and Australia's naval and air force upgrades drive long-cycle retrofit orders.

Europe maintains strategic weight through Airbus, BAE Systems, Safran, and a dense network of precision-motion SMEs. The European Union's (EU's) "Green Deal" prompts flight-control electrification to curb cabin hydraulic leaks and spill risks. Sanctions undermine Russia's supply relationships, forcing local industry to substitute imported electronics. The Middle East and Africa remain nascent but show promise as Gulf carriers modernize fleets and regional defense forces add UAV capacity, importing actuators alongside airframes.

Competitive Landscape

The field displays a high concentration where the top five firms control a significant revenue share. Moog Inc., Curtiss-Wright Corporation, Rockwell Automation Inc., Honeywell International Inc., and Emerson Electric Co. anchor the breadth of offerings and leverage extensive certification libraries. Woodward vaulted into the electro-mechanical vanguard with its USD 1.8 billion acquisition of Safran’s linefit actuator unit in 2024. Moog plows USD 150 million into US and Polish capacity to supply booming narrowbody backlogs. Honeywell pushes electric landing gear, chasing win-rates on retrofit packages for mature fleets.

New-space actors such as SpaceX, Rocket Lab, and Blue Origin design and build in-house units to cut turnaround cost, occasionally spinning out products to the defense market. European challenger companies explore hollow-rotor direct-drive actuators that bypass gearboxes, while Japanese consortia co-develop indigenous units to reduce import dependence. Patent activity clusters around digital twin prognostics, composite gears, and secure deterministic network stacks.

Cyber resilience and export-license agility increasingly sway bid outcomes, pushing suppliers to create multilevel product families segmented by ITAR status. The shift forces globalized design centers and mirror production lines outside the US so that controlled firmware stays local yet commercial derivatives ship freely.

Aerospace And Defense Robotic Automation Actuators Industry Leaders

Moog Inc.

Curtiss-Wright Corporation

Rockwell Automation Inc.

Honeywell International Inc.

Emerson Electric Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Momentus Inc., a US commercial space company providing satellites, satellite components, and in-space transportation services, received a NASA contract to study deploying essential robotics technologies in space.

- April 2025: RISE Robotics, which developed the Beltdraulic™ Systems for industrial actuation, has joined the US Air Force's Eglin Wide Agile Acquisition Contract (EWAAC) On-Ramp IV. This selection allows RISE to compete for future USAF delivery orders within the USD 46 billion Indefinite Delivery/Indefinite Quantity (IDIQ) contract vehicle.

Global Aerospace And Defense Robotic Automation Actuators Market Report Scope

| Electric |

| Hydraulic |

| Pneumatic |

| Electro-mechanical |

| Electro-hydrostatic |

| Motors and Drives |

| Gearboxes |

| Sensors and Encoders |

| Power Electronics |

| Controllers and Software |

| Flight Control Surfaces |

| Landing Gear and Braking |

| Robotic Manipulators |

| Weapon and Payload Handling |

| Satellite/Space Robotics |

| Other Applications |

| Commercial Aerospace OEM |

| Defense OEM |

| MRO and Retrofit |

| Space Agencies and New-Space |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Middle East | ||

| By Actuation | Electric | ||

| Hydraulic | |||

| Pneumatic | |||

| Electro-mechanical | |||

| Electro-hydrostatic | |||

| By Component | Motors and Drives | ||

| Gearboxes | |||

| Sensors and Encoders | |||

| Power Electronics | |||

| Controllers and Software | |||

| By Application | Flight Control Surfaces | ||

| Landing Gear and Braking | |||

| Robotic Manipulators | |||

| Weapon and Payload Handling | |||

| Satellite/Space Robotics | |||

| Other Applications | |||

| By End User | Commercial Aerospace OEM | ||

| Defense OEM | |||

| MRO and Retrofit | |||

| Space Agencies and New-Space | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Middle East | |||

Key Questions Answered in the Report

What is the aerospace and defense robotic automation actuators market size projected for 2025 and 2030, and what compound annual growth rate links the two values?

The aerospace and defense robotic automation actuators market is valued at USD 4.98 billion in 2025 and is forecasted to reach USD 9.69 billion by 2030, a trajectory that equates to a 14.26% CAGR.

Which actuator technology is phasing out hydraulics on next-generation aircraft?

Electro-mechanical systems posting a 13.76% CAGR are meeting the DoD goal of zero hydraulic lines by combining high torque density with built-in redundancy.

Why are rare-earth magnets a strategic risk for actuator programs?

China commands about 80% of global supply and recent disruptions triggered price spikes, forcing Western OEMs to explore alternative motor topologies and stockpiling strategies.

What component segment is expanding quickest due to embedded intelligence?

Controllers and software, forecasted at 14.87% CAGR, are integrating AI for predictive maintenance and cyber-secure networking.

Which region shows the highest growth potential through 2030?

Asia-Pacific leads with a 14.38% CAGR, driven by defense modernization, commercial aviation expansion, and ambitious national space programs.

How fast will actuator demand grow in autonomous military ground vehicles?

The category is on a 2.1% positive CAGR contribution, propelled by near-term fielding of robotic combat vehicles, particularly in North America and Asia-Pacific.

Page last updated on: