Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

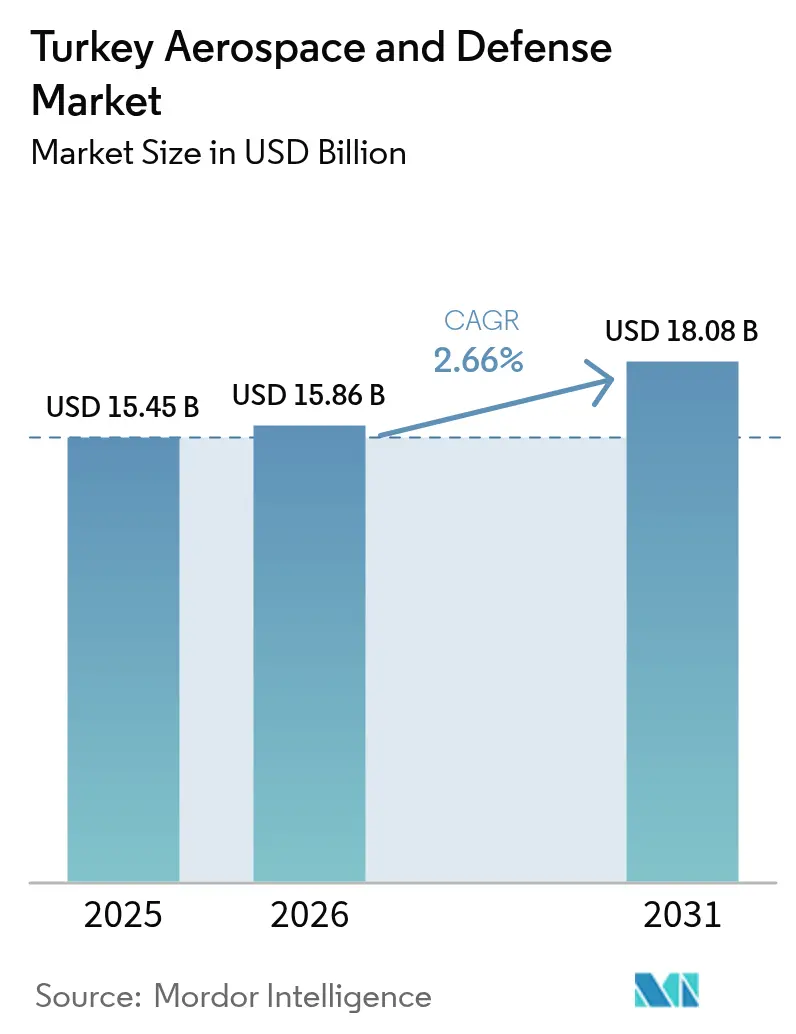

| Base Year Market Size (2025) | USD 15.45 Billion |

| Market Size (2026) | USD 15.86 Billion |

| Market Size (2031) | USD 18.08 Billion |

| Growth Rate (2026 - 2031) | 2.66% CAGR |

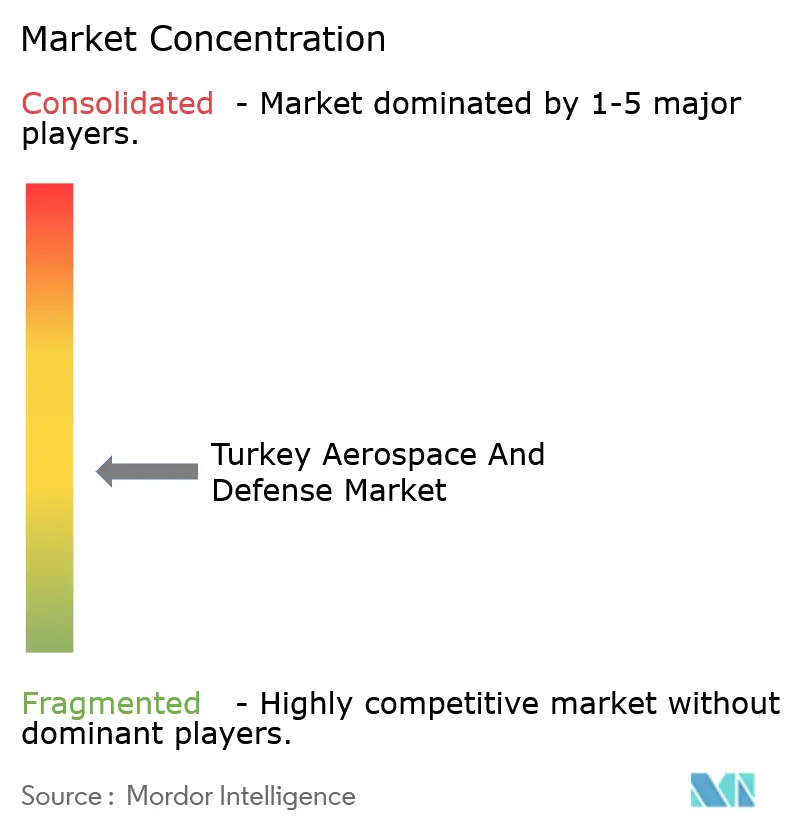

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Aerospace And Defense Market Analysis by Mordor Intelligence

The Turkey aerospace and defense market size is expected to grow from USD 15.45 billion in 2025 to USD 15.86 billion in 2026 and is forecast to reach USD 18.08 billion by 2031 at 2.66% CAGR over 2026-2031. This trajectory stems from the nation’s pivot toward indigenous platform development, resilient export demand, and a supportive defense budget framework that climbed to USD 47 billion in 2025.[1]Source: Middle East Eye, “Turkey’s 2025 Defense Budget Reaches USD 47 Billion,” middleeasteye.net Rising drone, missile, and space-system deliveries reinforce Turkey’s status as a reliable alternative to traditional suppliers. At the same time, the government’s commitment to 80% local content shields the sector from supply-chain shocks. Competitive dynamics emphasize technology sovereignty, demonstrated by the KAAN fifth-generation fighter, Hisar-O air-defense missile, and TB3 naval drone programs, which anchor an ecosystem capable of end-to-end design, prototyping, and serial production.

Key Report Takeaways

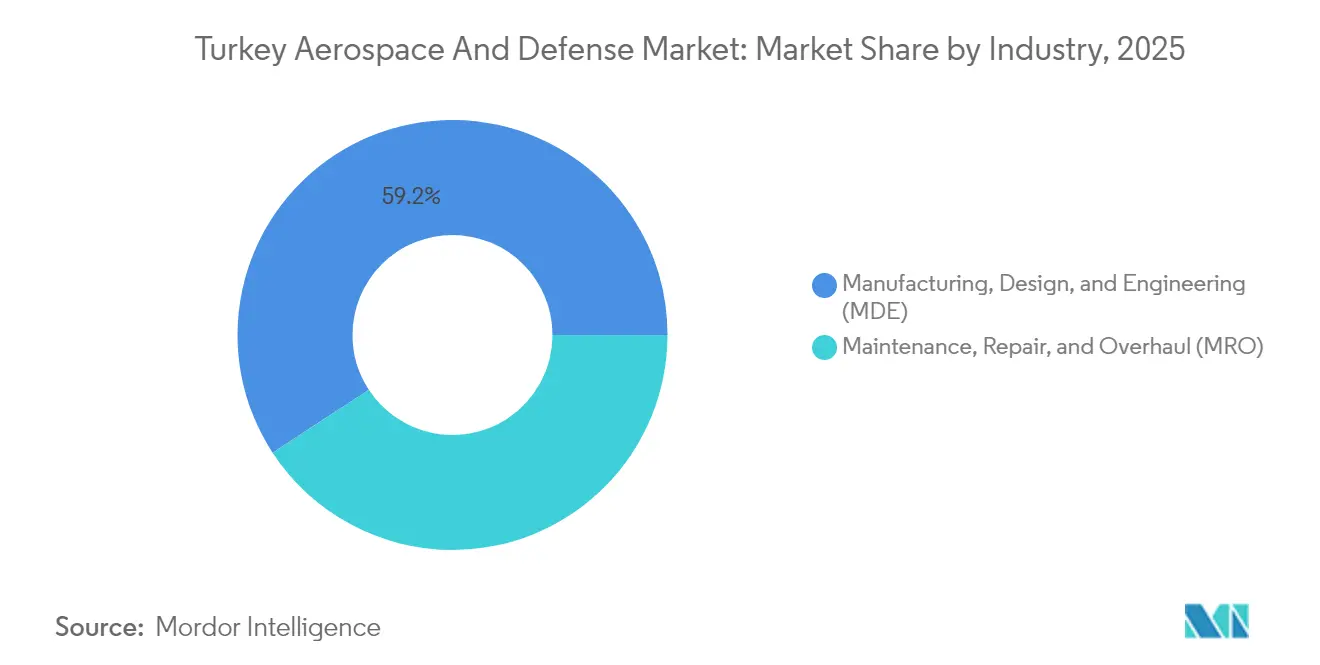

- By industry, manufacturing, design, and engineering (MDE) led with 59.22% of Turkey's aerospace and defense market share in 2025 and is projected to expand at a 2.98% CAGR through 2031.

- By type, defense platforms held a 67.90% share of the Turkish aerospace and defense market size in 2025, while the aerospace segment is forecasted to grow at a 3.24% CAGR to 2031.

- By end user, the military segment accounted for 71.60% share of the Turkish aerospace and defense market size in 2025, with government non-military applications advancing at a 3.62% CAGR through 2031.

- By platform, unmanned aerial vehicles (UAVs) captured 26.27% of the Turkish aerospace and defense market share in 2025 and are projected to grow at a 4.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Turkey Aerospace And Defense Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising defense-budget allocations | +0.8% | National, with spillover to regional partners | Medium term (2-4 years) |

| Surge in UAV and guided-munition exports | +0.6% | Global, with strong penetration in MENA, Eastern Europe | Short term (≤ 2 years) |

| National self-reliance and indigenous-platform targets | +0.5% | National, with technology transfer to allied nations | Long term (≥ 4 years) |

| Commercial-aviation fleet and airport capacity expansion | +0.4% | National, with regional connectivity benefits | Medium term (2-4 years) |

| NATO-interoperability upgrade programs | +0.3% | NATO member states, with focus on Eastern flank | Medium term (2-4 years) |

| Additive-manufacturing and advanced-composites adoption | +0.2% | National, with export potential to emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Defense-Budget Allocations

The 2025 defense budget of USD 47 billion allocates 165 billion Turkish lira to the Defense Industry Support Fund, guaranteeing near-term demand for indigenous air and missile programs and underwriting USD 4.5 billion in domestic R&D. Elevated outlays have already accelerated serial production of the Hisar-O air-defense missile and enabled new engine test stands for the TF35000 turbofan, thereby deepening vertical integration across propulsion, guidance and C4ISR subsystems. Predictable funding streams also entice SMEs into advanced composites, sensors, and additive-manufacturing niches, expanding the supplier base that feeds the Turkish aerospace and defense market. Taken together, these investments reinforce Turkey’s quest for strategic autonomy and broaden its export appeal to partners eager for technology transfer.

Surge in UAV and Guided-Munition Exports

Baykar’s USD 1.76 billion 2024 revenues highlight how performance in Ukraine, Libya, and Nagorno-Karabakh translated into contracts across 34 countries, with locally staffed facilities inaugurated in Ukraine and Indonesia. The TB3’s deck-based sorties from TCG Anadolu illustrate maritime force-multiplication at price points light-carrier navies can afford. Accompanying precision munitions packages and sustainment services create stable annuity revenues, helping firms weather exchange-rate swings while enlarging the Turkish aerospace and defense market footprint.

National Self-Reliance and Indigenous-Platform Targets

The KAAN fighter’s USD 10 billion export contract with Indonesia for over 48 aircraft—with licensed production lines in Bandung—confirms that home-grown designs can win on global tenders even against established Western jets. Turkey reduced foreign dependency from 80% to 20% in two decades, building supply-chain depth in avionics, warheads, and composite structures. Indigenous-content mandates channel procurement toward local suppliers, locking in scale economies that lower unit costs and make Turkish bids more competitive abroad. Once perceived as risks, technology-transfer clauses now function as selling points for governments seeking industrial upskilling, enlarging the Turkish aerospace and defense market.

Commercial-Aviation Fleet and Airport Capacity Expansion

Turkish Airlines operates 458 aircraft and targets 813 by 2033, a plan that requires expanded MRO capacity, domestic interiors, and composite components.[2]Source: Turkish Airlines, “Board Activity Report 2Q 2024,” investor.turkishairlines.com Istanbul Airport’s 120 million-passenger layout cements Turkey’s role as an intercontinental hub, sparking demand for radar, baggage handling, and ground-support systems. Dual-use technologies migrate from military programs into cost-sensitive commercial lines—such as additive-manufactured cabin brackets—shortening development cycles. Thus, the Turkish aerospace and defense market benefits from civil-military technology convergence that diversifies revenue streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency volatility and high input-cost inflation | -0.4% | National, with export competitiveness implications | Short term (≤ 2 years) |

| Export-license/sanctions exposure | -0.3% | Global, particularly affecting Western technology access | Medium term (2-4 years) |

| Skilled-labor shortages in critical disciplines | -0.2% | National, with regional talent competition | Medium term (2-4 years) |

| ESG/geopolitical-risk driven financing constraints | -0.1% | European markets, with limited emerging market impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility and High Input-Cost Inflation

Sharp Turkish-lira swings widen cost baselines for imported engines and aerospace-grade titanium, complicating pricing for long-cycle export contracts. Although 80% of a finished system is now locally sourced, the 20% foreign-supplied share often embodies propulsion or sensor packages that carry disproportionate value. Hard-currency billing and natural-hedge export portfolios provide partial relief, yet material inflation still pressures margins across the Turkish aerospace and defense market.

Export-License/Sanctions Exposure

Western sanctions following the S-400 acquisition evicted Turkey from the F-35 program, blocking planned workshare returns on a USD 1.4 billion sunk cost. License denials for US-origin components complicate subsystem sourcing and restrict sales into NATO markets. Turkish response strategies range from indigenous engine development to supply-chain diversification toward Asian and Middle-Eastern vendors, a pathway that expands design freedom but requires additional qualification testing. Short-term friction thus trims growth in the Turkish aerospace and defense market, even as self-reliance programs lay foundations for long-term resilience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Industry: Manufacturing Drives Indigenous Platform Development

Manufacturing, design, and engineering (MDE) generated 59.22% of 2025 revenue and is on track for a 2.98% CAGR, underscoring how production autonomy underpins the Turkish aerospace and defense market. TUSAŞ’s 4 million m² Kahramankazan campus covers design, assembly, and flight-test operations, enabling simultaneous production of the KAAN fighter, GÖKBEY helicopter, and ANKA-3 UAV on contiguous lines. Serial-production capacity gives Turkish primes negotiating clout on joint-venture bids, while SMEs supply harnesses, 3D-printed ducts, and high-temperature resins, elevating domestic value capture to 80% across major platforms.

The segment’s forward momentum benefits from additive manufacturing breakthroughs that shorten tooling cycles by 40%, allowing for quick pivoting from prototype to low-rate initial production. Integrated digital twins reduce rework costs and align well with export partners’ offset packages, enhancing the appeal of the Turkish aerospace and defense market. Sustained investment in hybrid composite-metallic structures for the TF35000 engine nacelle highlights how Turkey converts R&D budgets into proprietary IP that commands premium margins.

By Type: Defense Platforms Lead While Aerospace Accelerates

Defense platforms accounted for 67.90% of 2025 revenue as the Turkish Armed Forces recapitalized its armored vehicles, air-defense battalions, and naval assets. Combat-tested systems enhance credibility abroad, driving 30% year-over-year export growth that expands the Turkish aerospace and defense market. Yet the Aerospace segment’s 3.24% CAGR is closing the gap, powered by Turkish Airlines’ fleet-doubling plan and the domestic space program’s demand for launch structures and satellite buses.

Turksat 6A, designed in Ankara, extends coverage to 5 billion people and unlocks telecom royalties from emerging Asian markets. Civil-military spillovers, such as space-qualified solar arrays now repurposed for HALE UAVs, illustrate technology cross-pollination that enriches the Turkish aerospace and defense industry while reducing dependence on volatile defense cycles.

By End User: Military Dominance With Government Growth Emerging

Military agencies purchased 71.60% of the 2025 output, absorbing large volumes of precision munitions, tactical UAVs, and naval corvettes under multi-year procurement plans. National forces act as launch customers, validating systems for foreign buyers and cementing robust baseline demand for the Turkish aerospace and defense market. Nonetheless, Government (non-military) applications show a 3.62% CAGR, driven by border security towers, wildfire-monitoring drones, and satellite-enabled e-government connectivity.

Civil-authority adoption of dual-use radars and encrypted radio networks helps amortize R&D across broader volumes, lowering unit costs and improving export competitiveness. Such diversification shields revenue streams against potential slowdowns in defense allocation without diluting core competencies that define the Turkish aerospace and defense market.

By Platform: UAVs Lead Innovation and Export Success

UAVs accounted for 26.27% revenue and paced the field with 4.32% CAGR, reflecting Baykar’s prominent share of global UAV exports and TB2’s milestone of 1 million flight hours. Indigenous EO/IR turrets, SATCOM data links, and smart munitions replace once-imported payloads, keeping value in-country and expanding the Turkish aerospace and defense market. Fixed-wing manned projects such as the KAAN fighter diversify the portfolio, while ATAK-II heavy helicopter programs address regional rotor-craft demand.

Missile and precision-munition lines leverage composite airframes from drone production, cutting cycle times and offering turnkey packages attractive to medium-income nations. Space platforms, catalyzed by Fergani Space’s private-satellite launch, present long-tail upside by positioning Turkey as a regional provider of earth-observation and PNT services. Platform diversity, therefore, undergirds the sustained expansion of the Turkish aerospace and defense market.

Geography Analysis

The Marmara region houses SAHA Istanbul, a 1,300-member cluster that tallied USD 12.59 billion turnover and USD 6.08 billion exports in 2024. Its concentration of system integrators, port logistics, and the new Istanbul Airport places it at the epicenter of the Turkish aerospace and defense market. Collaborative R&D parks link primes with prototyping boutiques, accelerating the transition from concept to series production and enabling quick iterations responding to export customer feedback.

Central Anatolia, anchored by Ankara, centers on Turkish Aerospace’s Kahramankazan plant and the TF35000 engine integration line, reinforcing propulsion self-reliance. Proximity to defense-procurement agencies fosters agile decision-making and rapid contract execution, factors that cultivate new entrants and sustain SME pipelines feeding the Turkish aerospace and defense market.

The Aegean region leverages Izmir’s industrial zones and deep-water ports to support naval-air integration projects, while Mediterranean shipyards diversify into UAV-capable corvette decks. Black Sea hubs focus on radar and EW subsystems, capitalizing on offshore gas security needs. Southeastern and Eastern Anatolia offer cost-competitive facilities and tax incentives, attracting additive-manufacturing startups and broadening geographic risk dispersion for the Turkish aerospace and defense market.

Competitive Landscape

Seven Turkish firms rank in the global defense top-100; ASELSAN leads domestically at USD 2.172 billion revenue and holds heavy positions in radar, EW, and electro-optics. TUSAŞ follows with USD 1.858 billion, integrating airframes and satellites, while Baykar dominates UAVs with a 90% export-revenue ratio. Competitive advantage stems from vertical integration and speed—the time between TB2 baseline certification and first export was three years, far shorter than legacy OEM cycles.

Additive-manufacturing adoption reduces tooling costs by 35% and compresses prototype lead times, giving SMEs leverage to bid for subsystems on next-generation aircraft. Strategic moves in 2025 include Leonardo and Baykar’s joint venture targeting Europe’s unmanned-fighter segment and TUSAŞ’s Airbus partnership on Spain’s trainer program. Disruptors like Fergani Space push satellite-bus prices below USD 4 million, expanding addressable markets beyond state budgets. Collaboration inside SAHA Istanbul allows rapid scaling when export contracts, such as Indonesia’s KAAN order, demand local content. All told, synergistic competition propels global reach for the Turkish aerospace and defense market.

Turkey Aerospace And Defense Industry Leaders

Turkish Aerospace Industries, Inc.

ASELSAN A.Ş.

BMC Otomotiv Sanayi ve Ticaret A.Ş.

BAYKAR MAKİNA SANAYİ VE TİCARET A.Ş.

Roketsan A.Ş.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Rolls-Royce and Turkish Technic announced the establishment of a state-of-the-art MRO center at Istanbul Airport by 2027. This facility will support Trent XWB-97, Trent XWB-84, and Trent 7000 engines, with a capacity of 200 shop visits annually. It will serve Turkish Airlines and third-party Rolls-Royce TotalCare customers, enhancing regional engine maintenance capabilities.

- February 2025: FNSS secured a contract to produce next-gen PARS ALPHA 8×8 and 6×6 armoured vehicles for the Turkish Land Forces (TLF). The initial phase includes 8×8 Anti-Armour Squad and Armoured Recovery variants and 6×6 command post variants equipped with advanced mission systems.

Turkey Aerospace And Defense Market Report Scope

The study on Turkey aerospace and defense industry accounts for the developments in critical systems and components of aircraft, UAVs, armored vehicles, air defense systems, naval vessels, and satellites, among others.

The Turkey aerospace and defense market is segmented by industry and type. Based on industry, the market is segmented into manufacturing, design and engineering, and maintenance, repair, & overhaul (MRO). Based on type, the market is segmented into aerospace and defense. The report provides the market size in USD for all the aforementioned segments.

By Industry

| Manufacturing, Design, and Engineering (MDE) |

| Maintenance, Repair, and Overhaul (MRO) |

By Type

| Aerospace | Aviation |

| Space | |

| Defense |

By End User

| Commercial Aviation |

| Military |

| Government (Non-military) |

| Private and Business Aviation |

By Platform

| Fixed-Wing Aircraft |

| Rotary-Wing Aircraft |

| Unmanned Aerial Vehicles (UAVs) |

| Land Systems |

| Naval Systems |

| Missiles and Precision Munitions |

| Space Platforms and Launchers |

| By Industry | Manufacturing, Design, and Engineering (MDE) | |

| Maintenance, Repair, and Overhaul (MRO) | ||

| By Type | Aerospace | Aviation |

| Space | ||

| Defense | ||

| By End User | Commercial Aviation | |

| Military | ||

| Government (Non-military) | ||

| Private and Business Aviation | ||

| By Platform | Fixed-Wing Aircraft | |

| Rotary-Wing Aircraft | ||

| Unmanned Aerial Vehicles (UAVs) | ||

| Land Systems | ||

| Naval Systems | ||

| Missiles and Precision Munitions | ||

| Space Platforms and Launchers | ||

Key Questions Answered in the Report

What is the current size of the Turkey aerospace and defense market?

The market stands at USD 15.86 billion in 2026 and is projected to reach USD 18.08 billion by 2031, reflecting a 2.66% CAGR.

Which segment holds the largest Turkey aerospace and defense market share?

Manufacturing, Design & Engineering leads with 59.22% share as of 2025, thanks to sustained investment in indigenous platform production.

Why are Turkish UAVs so competitive internationally?

Combat validation, high indigenous content and bundled sustainment services have enabled Baykar to secure contracts in 34 countries and capture 65% of global UAV exports.

How significant is Turkey’s defense budget for industry growth?

The USD 47 billion 2025 defense budget, including substantial R&D allocations, underwrites domestic demand and accelerates technology self-reliance programs.

What regions within Turkey drive aerospace and defense production?

The Marmara region hosts the SAHA Istanbul cluster, Central Anatolia houses major assembly and engine-test facilities, and the Aegean leverages port infrastructure for maritime-air projects.

Which restraints could slow Turkey aerospace and defense market growth?

Currency volatility, export-license hurdles and skilled-labor shortages pose near-term risks, although indigenous development initiatives aim to mitigate these challenges.

Page last updated on: