Automotive MLCC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

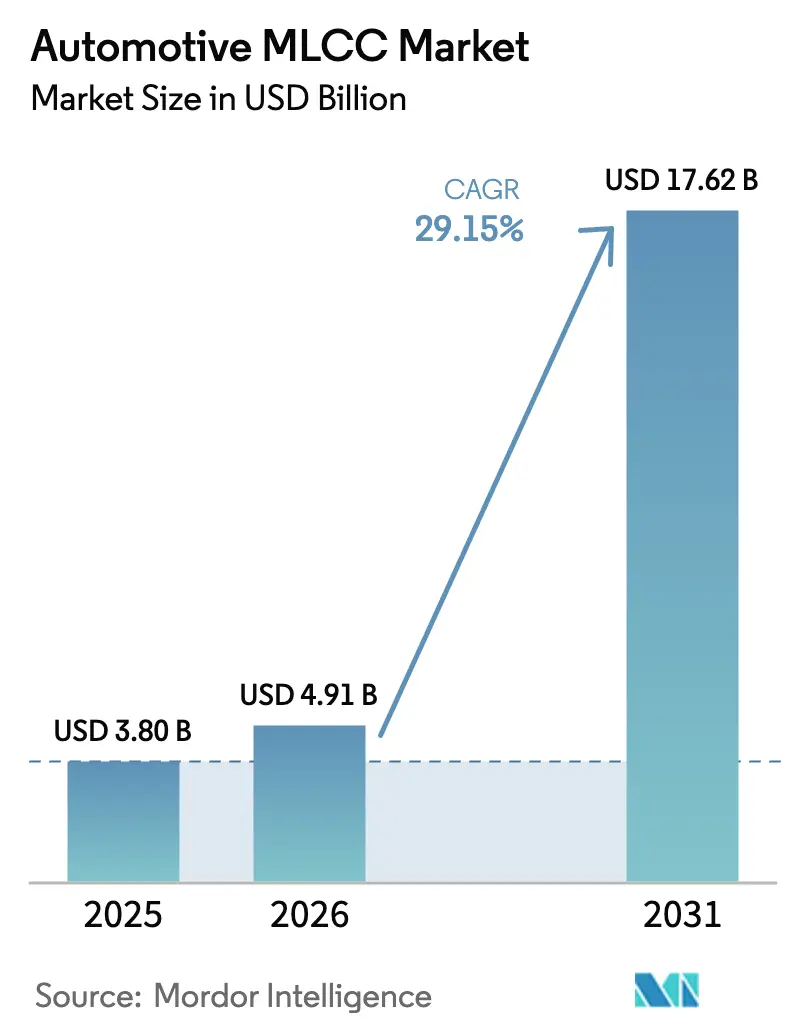

| Market Size (2026) | USD 4.91 Billion |

| Market Size (2031) | USD 17.62 Billion |

| Growth Rate (2026 - 2031) | 29.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive MLCC Market Analysis by Mordor Intelligence

The automotive MLCC market size is expected to grow from USD 3.80 billion in 2025 to USD 4.91 billion in 2026 and is forecast to reach USD 17.62 billion by 2031 at 29.15% CAGR over 2026-2031. Accelerating electrification, deep ADAS penetration, and the migration to 800 V electrical systems keep lifting content per vehicle, while large-scale investments by Murata, TDK, and Samsung Electro-Mechanics focus on substrate miniaturization, high-voltage endurance, and soft-termination reliability to secure automotive qualification.[1]Investor Relations Team, “TDK Investor Day 2024 Speech,” TDK, tdk.com Battery electric vehicles consume more than three times the MLCC count of internal-combustion platforms because traction inverters, onboard chargers, and advanced thermal-management circuits each demand dense decoupling and EMI suppression. The continuous shift from distributed ECUs to domain and zonal controllers intensifies power-delivery requirements in fewer, but dramatically more powerful, modules, thereby expanding per-unit MLCC value even as module counts decline. Volatile capacity allocation between smartphones and automotive, plus ceramic material cost inflation for nickel and palladium, injects short-term supply risk, yet long-horizon growth visibility remains high thanks to mandated functional-safety upgrades and the global policy drive toward zero-emission fleets.

Key Report Takeaways

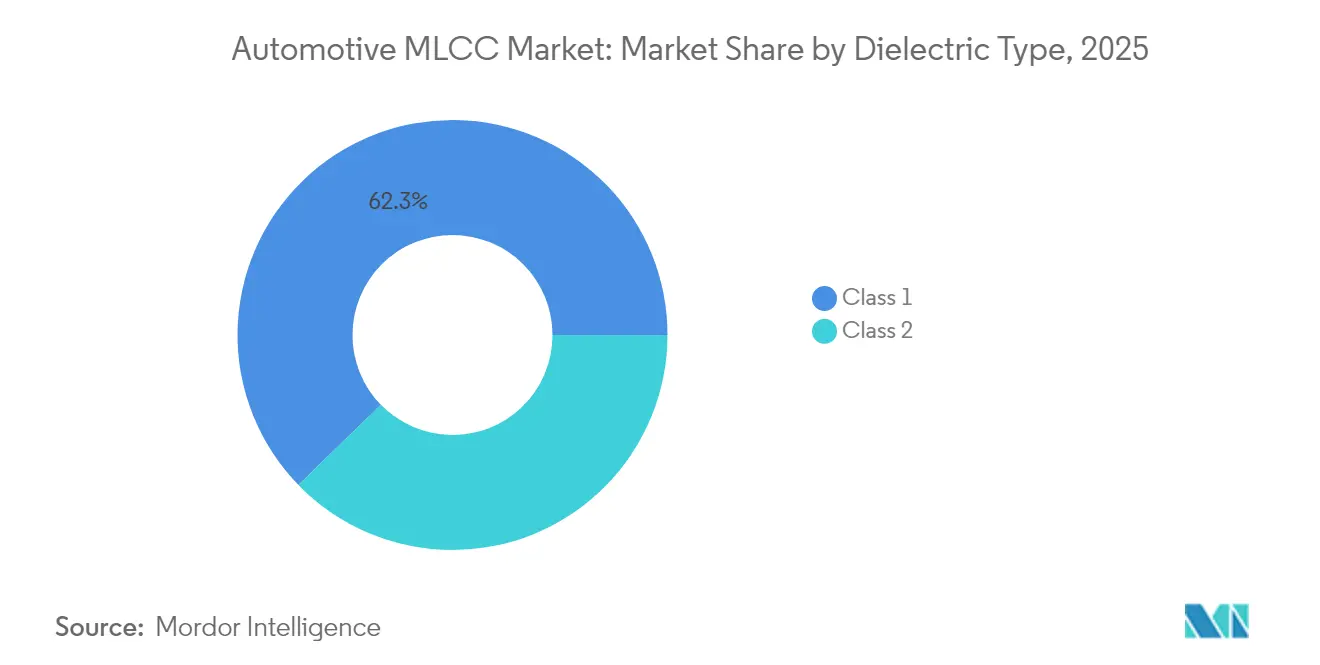

- By dielectric class, class 1 devices captured 62.28% of automotive MLCC market share in 2025, while Class 2 devices are projected to post the quickest 30.25% CAGR through 2031.

- By case size, 201 components led with 55.91% revenue share in 2025 in the automotive MLCC market; the 402 format is forecast to expand at a 30.05% CAGR to 2031.

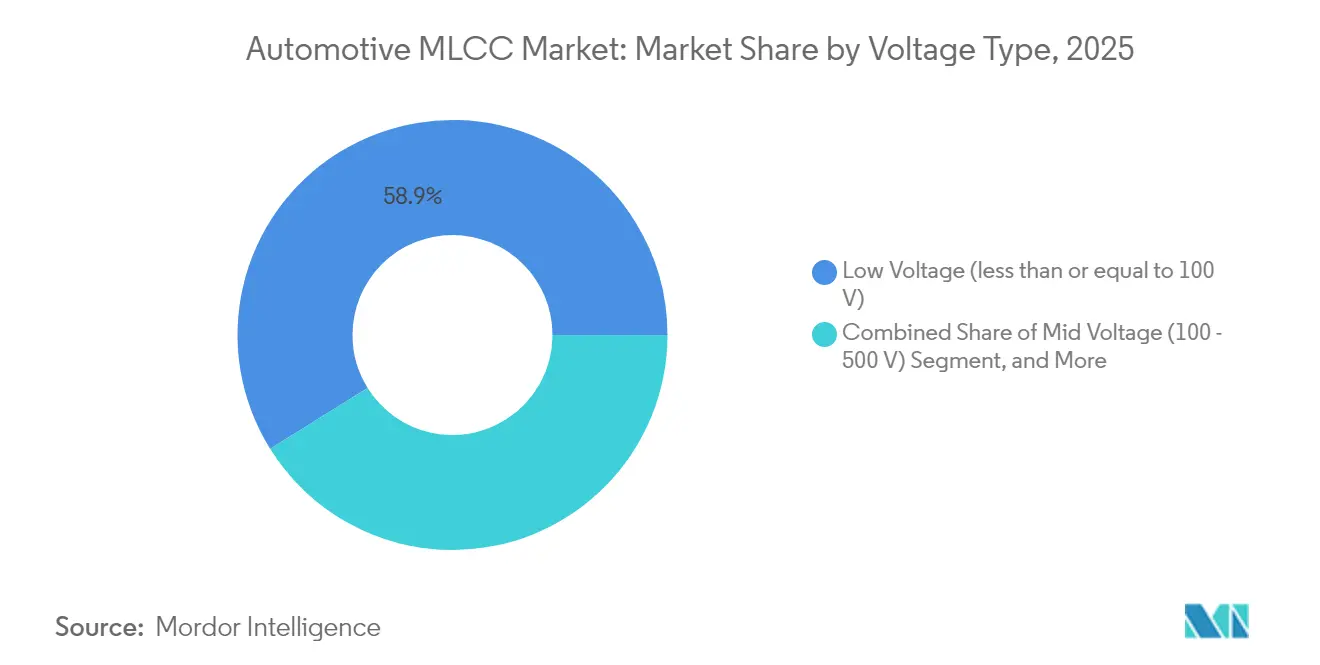

- By voltage rating, low-voltage (less than or equal to 100 V) units accounted for 58.88% of the automotive MLCC market size in 2025 and remain the fastest-growing sub-segment at 30.20% through 2031.

- By mounting type, surface-mount commanded 41.05% share in 2025 in the automotive MLCC market; metal-cap solutions record the highest projected CAGR at 29.95% through 2031.

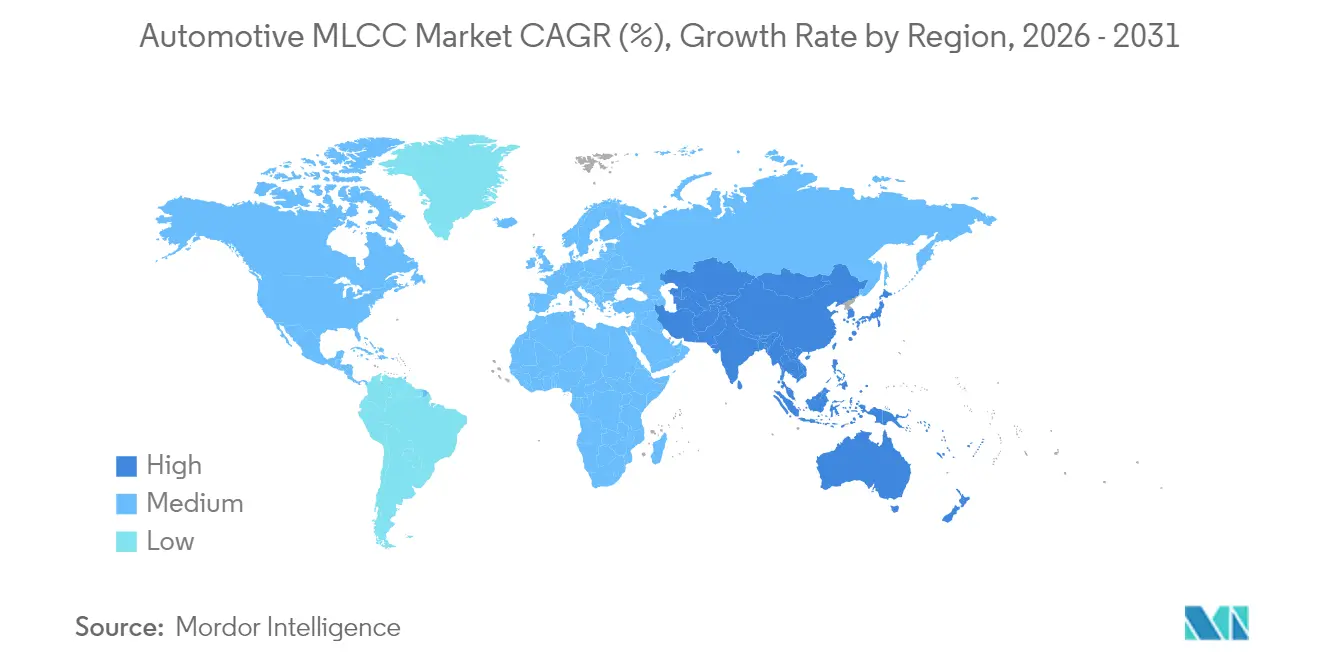

- By geography, Asia-Pacific dominated with 57.12% share in 2025 in the automotive MLCC market; North America delivers the sharpest 31.25% CAGR on reshoring and EV stimulus programs to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive MLCC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technology-intensive ADAS architecture requires higher capacitance density | +8.5% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Rapid electrification of powertrain and 800-V platforms | +9.2% | Asia-Pacific core, spill-over to North America and EU | Long term (≥ 4 years) |

| OEM shift to domain and zonal E/E architectures | +6.8% | Global, led by premium OEMs in Germany and Japan | Medium term (2-4 years) |

| Stricter OEM derating guidelines driving higher-class MLCC demand | +4.1% | Global, with stringent requirements in EU and Japan | Short term (≤ 2 years) |

| Adoption of SiC power modules boosting high-voltage MLCC sockets | +7.3% | Asia-Pacific and North America, following SiC adoption curves | Long term (≥ 4 years) |

| Insurance-driven mandate for predictive-maintenance telematics ECUs | +3.2% | North America and EU, driven by regulatory frameworks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technology-Intensive ADAS Architecture Requires Higher Capacitance Density

ADAS stacks now integrate LiDAR, high-resolution cameras, radar, and neural-network processors, each demanding rigorous power-delivery-network stability across broad frequency spectra. Consolidation into centralized compute domains concentrates switching noise, so decoupling capacitors must exhibit lower equivalent series resistance and inductance while fitting confined footprints. Murata’s forthcoming 0.4 × 0.2 mm, ~100 nF parts sustain sensor miniaturization without sacrificing reliability, and volume ramp in 2025 will unlock board-area savings for Tier 1 camera modules. Automotive EMC norms, especially CISPR 25 Class 5, drive MLCC counts upward because every serializer-deserializer lane and high-speed-interface PHY needs localized bypassing. As automakers push Level 3 autonomy into mid-segment vehicles, total ADAS MLCC sockets per car are projected to rise another 40% by 2028, cementing this driver’s medium-term influence.

Rapid Electrification of Powertrain and 800 V Platforms

The migration from 400 V to 800 V packs halves peak charge time and trims copper weight, yet subjects passive components to steeper dv/dt and corona stress.[2]Investor Relations Team, “TDK Investor Day 2024 Speech,” TDK, tdk.com Silicon-carbide MOSFET inverters switch at higher frequencies, so decoupling schemes demand MLCCs with tighter dielectric strength, low dissipation factor, and minimal acoustic resonance. TDK’s 3225-case, 100 V MLCCs deliver industry-leading capacitance while staying within AEC-Q200 temperature cycles, enabling compact DC-link arrays in traction inverters. High-voltage on-board chargers similarly require clusters of 100–470 nF parts for common-mode filtering. The push toward megawatt-class heavy-duty EV platforms further scales voltage stress, ensuring this driver remains potent throughout the decade.

OEM Shift to Domain and Zonal E/E Architectures

Premium automakers restructure networks around six to ten zonal controllers linked by 10 Gb Ethernet backbones, replacing ~100 legacy ECUs. The consolidation trims harness weight yet forces remaining boards to host mixed-signal power domains that service multiple subsystems simultaneously. Every additional rail compels sets of input-filter, bulk-storage, and high-frequency MLCCs, so content per controller climbs even though board count falls. Murata’s soft-termination variants protect these larger assemblies against board flexure induced by cabin structural resonance. Over-the-air software updates intensify current slew during flash programming, further amplifying the need for dense bypass networks. Consequently, the architecture shift bolsters near-term volume resilience despite future ASIC integration.

Stricter OEM Derating Guidelines Driving Higher-Class MLCC Demand

After the inverter field returns in 2024, European and Japanese OEMs tightened derating rules, capping continuous voltage at 50% of the rating and limiting operating temperature to two-thirds of the component's maximum. Engineers now up-select Class 1 X8G or X9G dielectrics instead of Class 2 X7R to preserve capacitance under load. Samsung Electro-Mechanics employs copper–epoxy soft terminations that arrest board-flex-induced cracking, satisfying Volkswagen’s VW80808 safety requirement.[3]Product Marketing, “25 V MLCC Solution for Memory Voltage Regulators,” Samsung Electro-Mechanics, samsungsem.com Derating reduces the usable capacitance window, so designers offset losses by installing more, or higher-value, parts per rail, thereby increasing demand for premium-grade MLCCs. Although the policy shifts are already in effect, compliance audits scheduled through 2027 keep this driver impactful in the short to medium term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-demand volatility due to smartphone-automotive capacity clash | -4.7% | Global, with acute impact in Asia-Pacific manufacturing hub | Short term (≤ 2 years) |

| Rising ceramic material costs (nickel, palladium) | -3.8% | Global, with cost pass-through challenges in price-sensitive regions | Medium term (2-4 years) |

| Quality-related field failures in EV inverters (AEC-Q200 rev-D) | -2.9% | Global, with stricter enforcement in EU and Japan | Short term (≤ 2 years) |

| OEM preference for film capacitors in above 1 µF/1 kV traction inverters | -2.1% | Global, concentrated in high-voltage EV applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Demand Volatility Due to Smartphone–Automotive Capacity Clash

Consumer-electronics launches soak up high-volume MLCC lines because phone builds often exceed 1.5 billion units annually, dwarfing automotive volumes. Foundries prioritize the shorter design cycles and cash-conversion velocity of flagship phones, sidelining longer qualification automotive runs during Q3–Q4 ramp peaks. Despite automakers locking 12-month forecasts, sudden handset pull-ins can stretch lead times for Class 1 parts from 16 to 34 weeks, forcing Tier 1s to activate contingency allocations. The tension should moderate as vendors carve out dedicated automotive capacity, yet near-term schedule risk stays material.

Rising Ceramic Material Costs (Nickel, Palladium)

Dielectric layers rely on nickel electrodes while soft terminations use palladium-rich pastes; both metals experienced double-digit price swings through 2024–2025 amid geopolitical supply squeezes. Automotive contracts often lock prices for three-year windows, so manufacturer margins compress when spot surges outpace hedging. Though substitution with copper and silver alloys is progressing, performance tradeoffs limit immediate relief for high-voltage SKUs. Therefore, input-cost inflation will likely dampen profitability over the medium term even as unit volumes rise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dielectric Type: Class 1 Leadership Prevails Under Reliability Mandates

Class 1 devices captured 62.28% of the 2025 automotive MLCC market share, reflecting the industry’s insistence on stable capacitance across -55 °C to 150 °C cycles. The segment is projected to grow at 29.85% CAGR through 2031, outpacing overall automotive MLCC market growth as OEM derating rules elevate Class 1 demand. While Class 2 parts deliver higher volumetric efficiency, their capacitance drop under bias impedes usage in safety-critical ADAS, steering, and braking domains. Automakers thus allocate Class 2 primarily to infotainment or cabin-comfort rails, shielding mission-critical circuits behind Class 1 clusters. As EV traction and zonal controllers proliferate, the automotive MLCC market size contribution of Class 1 parts is forecast to reach USD 10.85 billion by 2031, up from USD 2.37 billion in 2025.

Concurrent R&D focuses on X8G and X9G formulations to push temperature endurance beyond 150 °C, widening the moat against polymer film substitutes. Because AEC-Q200 rev-D intensifies life-test cycles, suppliers with proprietary nano-crystal dopants and sintering control, such as Murata, fortify leadership while late entrants struggle to pass qualification.

By Case Size: 201 Dominance Meets 402 Acceleration

At 55.91% share in 2025, the 201 footprint remains the workhorse form factor, balancing solder-joint reliability, pick-and-place yield, and capacitance density. However, 402 parts record a 30.05% CAGR to 2031 as ADAS cameras and radar units demand ultra-tight packaging. The automotive MLCC market size for 402 components is set to surpass USD 2.69 billion by 2031, reflecting OEM pressure to reclaim PCB real estate for high-speed SerDes routing. Meanwhile, 603 and larger footprints persist in power inverters because thicker dielectric stacks manage above 150 V stress with superior self-heating characteristics. Industry roadmaps target sub-0402 codes by 2027, yet automotive adoption will lag consumer uptake until vibration survivability proofs mature.

By Voltage: Low-Voltage Supremacy with High-Voltage Upside

Low-voltage (less than or equal to 100 V) units held 58.88% of the automotive MLCC market in 2025, anchored by 12 V body control, infotainment, and sensor rails. The slice expands at a 30.20% CAGR, yet high-voltage (above 500 V) SKUs lose strategic mindshare as 800 V EV architectures proliferate. The 100-V segment alone could triple by 2030 as silicon-carbide gate-drivers adopt 48 V isolation rings. For now, design wins cluster under 25 V X8L parts, which support Ethernet PHYs and camera serial interfaces. Multiple OEMs explore hybrid stacks pairing MLCCs with thin-film polymer to smooth high-energy spikes, suggesting cross-technology complementarity rather than outright replacement.

By MLCC Mounting Type: Metal-Cap Emergence Under Harsh-Duty Cycles

Surface-mount technology still commands 41.05% of 2025 revenues due to automated line efficiency and fine-pitch PCB evolution. Yet metal-cap mounting accelerates at 29.95% CAGR because EV drivetrain vibration, torque shudder, and elevated temperatures stress standard terminations. Metal-cap designs encase the chip in a conductive cap soldered to heavy copper tabs, decoupling ceramic bodies from bending forces and doubling current-carrying capacity. Radial-lead MLCCs remain viable for under-hood fuse boxes but cede share to metal-cap and flexible-termination SMDs as OEMs chase higher reliability scores on VDA239-011 tests. Over the forecast, automotive MLCC market size for metal-cap parts could eclipse USD 1.62 billion, transforming a niche format into a mainstream solution for traction inverter filters.

Geography Analysis

Asia-Pacific retained 57.12% automotive MLCC market share in 2025 on the back of China’s 7 million-unit EV output and Japan’s high-value component ecosystem. Regional CAGR of 29.75% to 2031 remains aligned with global averages, yet the sheer production scale magnifies absolute growth. Chinese OEMs such as BYD and SAIC increasingly source domestic X8G MLCCs to satisfy local content rules, pressuring multinational suppliers to open Suzhou- and Wuxi-based automotive lines. Meanwhile, Japanese incumbents leverage superior sintering and material science to stay ahead in Class 1 reliability metrics, ensuring export relevance even as Chinese quality levels rise.

North America captured 19.74% of 2025 revenue and exhibits the steepest 31.25% CAGR through 2031, driven by the Inflation Reduction Act’s EV incentives and OEM reshoring mandates. General Motors and Ford now stipulate dual-source MLCC procurement with at least one U.S. or Mexican fab, stimulating projects in Arizona and Querétaro. Government loan guarantees offset capital intensity, while proximity cuts logistics lead time for high-mix, low-volume runs. Canada’s nickel reserves attract cell and passive-component ventures, creating a vertically integrated corridor for 800 V power-train modules.

Europe accounted for 16.54% market share in 2025, anchored by Germany’s premium OEM cluster that demands top-tier Class 1 MLCCs for Level 3 driver-assistance rollouts. EU battery regulations incentivize local passive-component production, though high energy costs challenge competitiveness against Asian fabs. The automotive MLCC market size uplift in Europe is nonetheless underwritten by a legal requirement that all new cars be zero-emission by 2035, guaranteeing sustained content growth. Rest-of-World regions, such as Latin America and the Middle East, add marginal volumes today but present future upside as CKD assembly plants adopt global BEV platforms.

Competitive Landscape

The automotive MLCC market remains highly concentrated: Murata holds an estimated 40–50% share, while TDK and Samsung Electro-Mechanics collectively exceed 30%. High entry barriers stem from proprietary ceramic powders, multi-year AEC-Q200 qualifications, and tier-one customer audits that favor entrenched suppliers. Murata commands leadership through vertically integrated nickel paste and in-house soft-termination lines, enabling rapid transfer to high-voltage SKUs. TDK earmarked roughly 30% of its 2025-2027 CAPEX for passive components, expanding Akita and Yamagata facilities to dedicate clean rooms for 100V automotive MLCCs. Samsung Electro-Mechanics leverages flip-chip packaging expertise from its smartphone lineage to pioneer metal-cap automotive variants launched in 2025.

Strategic playbooks center on capacity ring-fencing, soft-termination patent portfolios, and localized ceramic powder sintering to reduce geopolitical shipping risk. Joint ventures with SiC module makers are emerging: Murata collaborates with Cree to co-design snubber arrays optimized for Wolfspeed’s Gen-4 MOSFET gate drive. Niche suppliers like Yageo target second-tier EV makers with price-competitive X6S parts, yet still rely on foundry subcontracting for Class 1. Market incumbents guard share by bundling MLCCs with complementary inductors and EMC filters, locking in multi-component awards at the platform RFI stage.

Technological differentiation now hinges on miniaturization and acoustic noise suppression. Murata’s 0.4 × 0.2 mm launch slashes board area for forward-facing radar, while TDK’s resin-coated, stress-relief MLCCs exceed 3,000 thermal cycles without crack initiation, double the AEC-Q200 requirement. Samsung Electro-Mechanics introduced copper-epoxy soft terminations rated to survive 10 k cycles of 2,000 G mechanical shock, opening design wins in heavy-duty off-road EVs. Such innovations consolidate pricing power despite nickel and palladium volatility, preserving gross margins in the high-teens percentage range.

Automotive MLCC Industry Leaders

Kyocera AVX Components Corporation (Kyocera Corporation)

TDK Corporation

Walsin Technology Corporation

Yageo Corporation

Murata Manufacturing Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Yageo raised its tender offer for Shibaura Electronics to JPY 6,200 per share, eyeing sensor portfolio expansion to complement automotive MLCC lines.

- April 2025: TDK released MLCCs delivering the industry’s highest capacitance at 100 V in 3225 case size, targeting traction inverter decoupling.

- February 2025: Samsung Electro-Mechanics rolled out 25 V, 22 µF X6S MLCCs in 0805 format, with automotive power-train qualification underway.

- October 2024: TDK showcased AI-centric passive components for e-mobility and ADAS platforms at electronica 2024 in Munich.

Global Automotive MLCC Market Report Scope

Heavy Commercial Vehicle, Light Commercial Vehicle, Passenger Vehicle, Two-Wheeler are covered as segments by Vehicle Type. Electric Vehicle, Non-Electric Vehicle are covered as segments by Fuel Type. BEV - Battery Electric Vehicle, FCEV - Fuel Cell Electric Vehicle, HEV - Hybrid Electric Vehicle, ICEV - Internal Combustion Engine Vehicle, PHEV - Plug-in Hybrid Electric Vehicle, Others are covered as segments by Propulsion Type. ADAS, Infotainment, Powertrain, Safety System, Others are covered as segments by Component Type. 0 603, 0 805, 1 206, 1 210, 1 812, Others are covered as segments by Case Size. 50V to 200V, Less than 50V, More than 200V are covered as segments by Voltage. 10 µF to 1000 µF, Less than 10 µF, More than 1000µF are covered as segments by Capacitance. Class 1, Class 2 are covered as segments by Dielectric Type. Asia-Pacific, Europe, North America are covered as segments by Region.| Class 1 |

| Class 2 |

| 201 |

| 402 |

| 603 |

| 1005 |

| 1210 |

| Other Case Sizes |

| Low Voltage (less than or equal to 100 V) |

| Mid Voltage (100 – 500 V) |

| High Voltage (above 500 V) |

| Metal Cap |

| Radial Lead |

| Surface Mount |

| North America | United States |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Dielectric Type | Class 1 | |

| Class 2 | ||

| By Case Size | 201 | |

| 402 | ||

| 603 | ||

| 1005 | ||

| 1210 | ||

| Other Case Sizes | ||

| By Voltage | Low Voltage (less than or equal to 100 V) | |

| Mid Voltage (100 – 500 V) | ||

| High Voltage (above 500 V) | ||

| By MLCC Mounting Type | Metal Cap | |

| Radial Lead | ||

| Surface Mount | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Market Definition

- MLCC (Multilayer Ceramic Capacitor) - A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits.

- Voltage - The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V)

- Capacitance - The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor

- Case Size - The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height

| Keyword | Definition |

|---|---|

| MLCC (Multilayer Ceramic Capacitor) | A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits. |

| Capacitance | The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor |

| Voltage Rating | The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V) |

| ESR (Equivalent Series Resistance) | The total resistance of a capacitor, including its internal resistance and parasitic resistances. It affects the capacitor's ability to filter high-frequency noise and maintain stability in a circuit. |

| Dielectric Material | The insulating material used between the conductive layers of a capacitor. In MLCCs, commonly used dielectric materials include ceramic materials like barium titanate and ferroelectric materials |

| SMT (Surface Mount Technology) | A method of electronic component assembly that involves mounting components directly onto the surface of a printed circuit board (PCB) instead of through-hole mounting. |

| Solderability | The ability of a component, such as an MLCC, to form a reliable and durable solder joint when subjected to soldering processes. Good solderability is crucial for proper assembly and functionality of MLCCs on PCBs. |

| RoHS (Restriction of Hazardous Substances) | A directive that restricts the use of certain hazardous materials, such as lead, mercury, and cadmium, in electrical and electronic equipment. Compliance with RoHS is essential for automotive MLCCs due to environmental regulations |

| Case Size | The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height |

| Flex Cracking | A phenomenon where MLCCs can develop cracks or fractures due to mechanical stress caused by bending or flexing of the PCB. Flex cracking can lead to electrical failures and should be avoided during PCB assembly and handling. |

| Aging | MLCCs can experience changes in their electrical properties over time due to factors like temperature, humidity, and applied voltage. Aging refers to the gradual alteration of MLCC characteristics, which can impact the performance of electronic circuits. |

| ASPs (Average Selling Prices) | The average price at which MLCCs are sold in the market, expressed in USD million. It reflects the average price per unit |

| Voltage | The electrical potential difference across an MLCC, often categorized into low-range voltage, mid-range voltage, and high-range voltage, indicating different voltage levels |

| MLCC RoHS Compliance | Compliance with the Restriction of Hazardous Substances (RoHS) directive, which restricts the use of certain hazardous substances, such as lead, mercury, cadmium, and others, in the manufacturing of MLCCs, promoting environmental protection and safety |

| Mounting Type | The method used to attach MLCCs to a circuit board, such as surface mount, metal cap, and radial lead, which indicates the different mounting configurations |

| Dielectric Type | The type of dielectric material used in MLCCs, often categorized into Class 1 and Class 2, representing different dielectric characteristics and performance |

| Low-Range Voltage | MLCCs designed for applications that require lower voltage levels, typically in the low voltage range |

| Mid-Range Voltage | MLCCs designed for applications that require moderate voltage levels, typically in the middle range of voltage requirements |

| High-Range Voltage | MLCCs designed for applications that require higher voltage levels, typically in the high voltage range |

| Low-Range Capacitance | MLCCs with lower capacitance values, suitable for applications that require smaller energy storage |

| Mid-Range Capacitance | MLCCs with moderate capacitance values, suitable for applications that require intermediate energy storage |

| High-Range Capacitance | MLCCs with higher capacitance values, suitable for applications that require larger energy storage |

| Surface Mount | MLCCs designed for direct surface mounting onto a printed circuit board (PCB), allowing for efficient space utilization and automated assembly |

| Class 1 Dielectric | MLCCs with Class 1 dielectric material, characterized by a high level of stability, low dissipation factor, and low capacitance change over temperature. They are suitable for applications requiring precise capacitance values and stability |

| Class 2 Dielectric | MLCCs with Class 2 dielectric material, characterized by a high capacitance value, high volumetric efficiency, and moderate stability. They are suitable for applications that require higher capacitance values and are less sensitive to capacitance changes over temperature |

| RF (Radio Frequency) | It refers to the range of electromagnetic frequencies used in wireless communication and other applications, typically from 3 kHz to 300 GHz, enabling the transmission and reception of radio signals for various wireless devices and systems. |

| Metal Cap | A protective metal cover used in certain MLCCs (Multilayer Ceramic Capacitors) to enhance durability and shield against external factors like moisture and mechanical stress |

| Radial Lead | A terminal configuration in specific MLCCs where electrical leads extend radially from the ceramic body, facilitating easy insertion and soldering in through-hole mounting applications. |

| Temperature Stability | The ability of MLCCs to maintain their capacitance values and performance characteristics across a range of temperatures, ensuring reliable operation in varying environmental conditions. |

| Low ESR (Equivalent Series Resistance) | MLCCs with low ESR values have minimal resistance to the flow of AC signals, allowing for efficient energy transfer and reduced power losses in high-frequency applications. |

Research Methodology

Mordor Intelligence has followed the following methodology in all our MLCC reports.

- Step 1: Identify Data Points: In this step, we identified key data points crucial for comprehending the MLCC market. This included historical and current production figures, as well as critical device metrics such as attachment rate, sales, production volume, and average selling price. Additionally, we estimated future production volumes and attachment rates for MLCCs in each device category. Lead times were also determined, aiding in forecasting market dynamics by understanding the time required for production and delivery, thereby enhancing the accuracy of our projections.

- Step 2: Identify Key Variables: In this step, we focused on identifying crucial variables essential for constructing a robust forecasting model for the MLCC market. These variables include lead times, trends in raw material prices used in MLCC manufacturing, automotive sales data, consumer electronics sales figures, and electric vehicle (EV) sales statistics. Through an iterative process, we determined the necessary variables for accurate market forecasting and proceeded to develop the forecasting model based on these identified variables.

- Step 3: Build a Market Model: In this step, we utilized production data and key industry trend variables, such as average pricing, attachment rate, and forecasted production data, to construct a comprehensive market estimation model. By integrating these critical variables, we developed a robust framework for accurately forecasting market trends and dynamics, thereby facilitating informed decision-making within the MLCC market landscape.

- Step 4: Validate and Finalize: In this crucial step, all market numbers and variables derived through an internal mathematical model were validated through an extensive network of primary research experts from all the markets studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 5: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platform