Aerospace Adhesives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.17 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

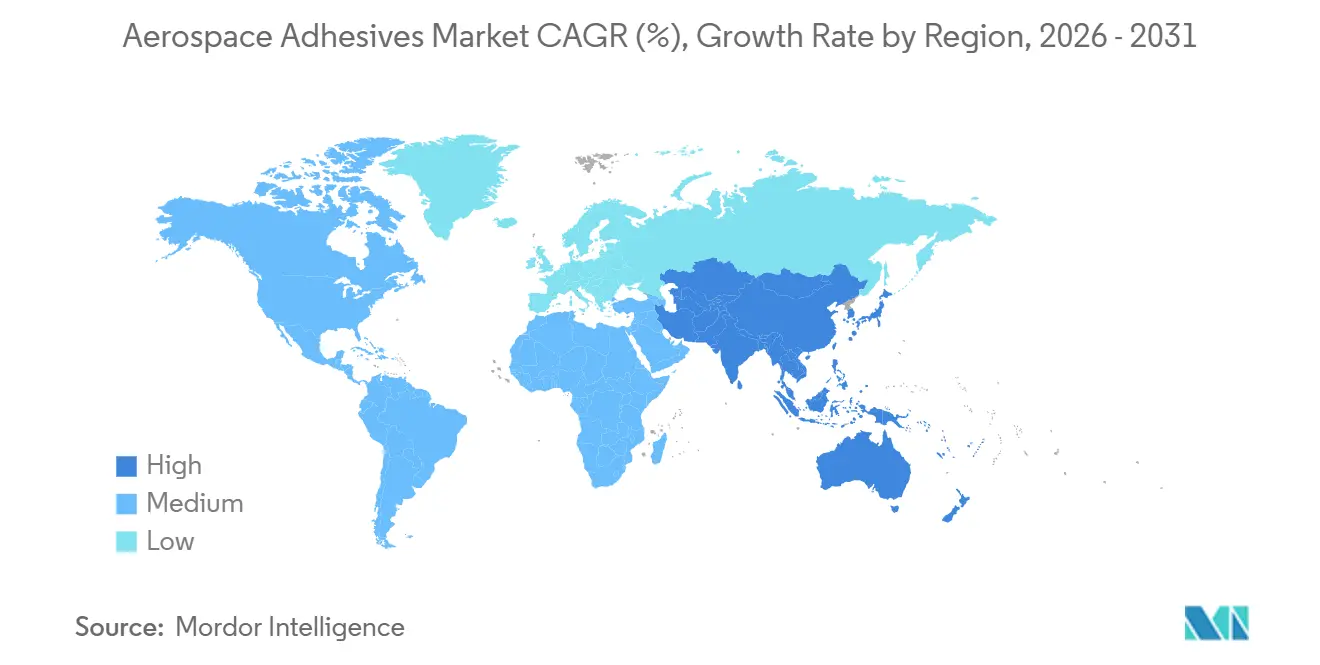

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace Adhesives Market Analysis by Mordor Intelligence

The Aerospace Adhesives Market size is projected to expand from USD 0.89 billion in 2025 and USD 0.93 billion in 2026 to USD 1.17 billion by 2031, registering a CAGR of 4.78% between 2026 to 2031. Key growth drivers include composite-intensive airframes, robotic bonding cells, and cryogenic-ready chemistries that support hydrogen propulsion. While solvent-borne systems maintain a significant revenue share, waterborne formulations are rapidly gaining ground, spurred by tightening VOC level caps from the California Air Resources Board and REACH. Structural grades align closely with original-equipment manufacturers’ consumption share, as they increasingly adopt bonded composite skins and wing boxes. North America, bolstered by Boeing’s 737 MAX and Lockheed Martin’s F-35 programs, dominates adhesive volumes. Yet, with the output of COMAC's C919 and Tata-Airbus's C295, the Asia-Pacific region is poised for the swiftest growth.

Key Report Takeaways

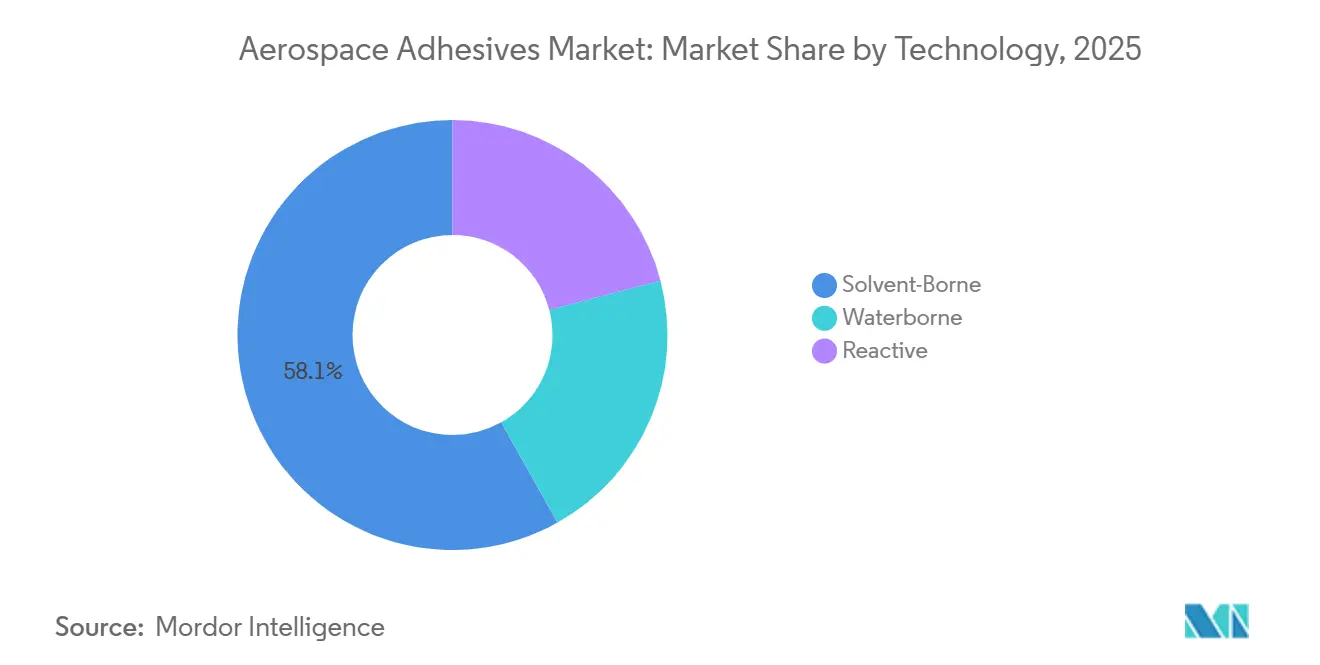

- By technology, solvent-borne formulations led with a 58.12% revenue share in 2025, while waterborne variants are projected to grow at a 4.98% CAGR through 2031.

- By resin type, epoxy captured 50.23% of 2025 sales and is forecast to advance at a 5.12% CAGR to 2031 on the strength of high-temperature composite applications.

- By function, structural adhesives accounted for 59.16% of demand in 2025 and are expected to expand at a 4.91% CAGR as automated robotic bonding lines proliferate.

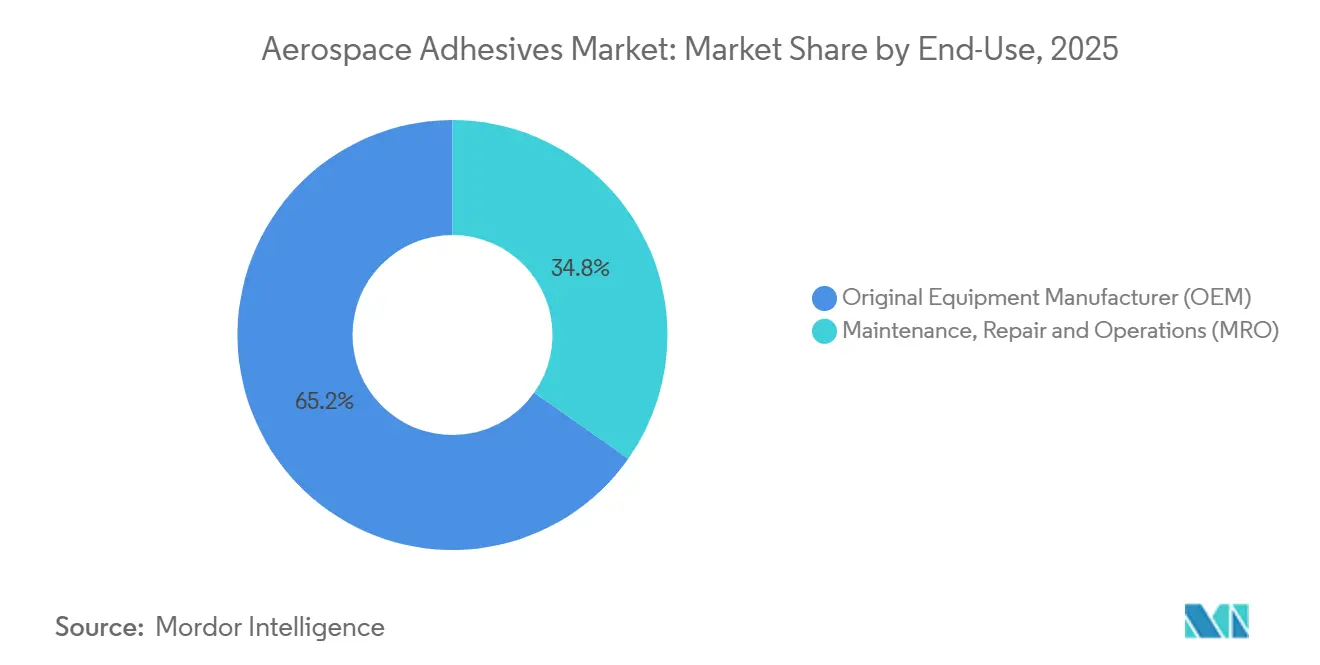

- By end-use, OEMs held 65.23% share in 2025, while the same channel will post the fastest 4.93% CAGR through 2031 because of new-build aircraft programs.

- By geography, North America generated 40.14% of 2025 revenue; Asia-Pacific is forecast to log the highest regional 5.21% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aerospace Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing penetration of composites in aircraft manufacturing | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Automated robotic bonding lines to meet Airbus and Boeing ramp-up | +0.9% | North America, Europe, APAC manufacturing hubs | Short term (≤ 2 years) |

| Expansion of national defense budgets (U.S., China, India) | +1.1% | North America, APAC (China, India, South Korea) | Long term (≥ 4 years) |

| Growth of commercial-space launch and in-orbit-service programs | +0.7% | North America (U.S.), emerging in Europe and APAC | Long term (≥ 4 years) |

| Cryogenic-ready adhesives for hydrogen-propelled aircraft | +0.5% | Europe (Airbus ZEROe), North America research and development clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Penetration of Composites in Aircraft Manufacturing

Carbon-fiber-reinforced polymers now account for a significant portion of the structural weight in both the Boeing 787 and the Airbus A350. This shift has replaced thousands of mechanical fasteners with high-strength adhesive joints, ensuring the integrity of the laminate. NASA's AERoBOND program has confirmed that using barrier-ply film adhesives can reduce surface abrasion, leading to a decrease in fuselage assembly labor[1]Airbus, “ZEROe Hydrogen Aircraft Program,” airbus.com. Similarly, COMAC's C919 wing box utilizes these film systems, achieving a reduction in wing mass compared to traditional aluminum riveting. This advancement bolsters COMAC's ambition of delivering its units by 2030. Epoxy-based structural grades lead the market, thanks to their compatibility with toughened prepreg cycles at cure profiles of 120 °C – 180 °C, and their ability to produce lap-shear strengths exceeding industry standards. While Asian suppliers are expanding their autoclave capacities, qualification delays have solidified the positions of Henkel's LOCTITE EA 9695 and Cytec's FM 300 series in the market.

Automated Robotic Bonding Lines to Meet Airbus and Boeing Ramp-Up

Airbus has earmarked a significant budget for automated cells that apply film and paste adhesives with high accuracy. This investment is pivotal for Airbus's ambition to ramp up production of the A320 family by late 2026. In 2024, Boeing's Fuselage Automated Upright Build line successfully cut the panel cycle time for the 737 MAX and achieved a notable reduction in scrap. Turnkey systems from Electroimpact and MTorres feature infrared pre-heat stations, elevating substrate temperatures to 60 °C, which bolsters wet-out and void control. Spirit AeroSystems reported a reduction in adhesive waste in 2025, translating to substantial cost savings across its Wichita and Prestwick sites. This was achieved using two-part reactive epoxies with open times of 20 to 45 minutes, perfectly aligning with robotic takt cycles.

Expansion of National Defense Budgets (U.S., China, India)

In 2024, the United States allocated a substantial budget for defense, designating a significant portion specifically for aircraft procurement. Each platform in this procurement utilizes adhesives. Meanwhile, India, in its fiscal 2026 budget, increased its defense allocation to support the Tejas Mk2 and AMCA fighters, which utilize film epoxies to bond composite radomes and wings. China officially reported a defense expenditure for 2024. However, external estimates suggest a significantly higher figure. Notably, China's J-20 stealth jet incorporates low-dielectric-loss adhesives under its radar-absorbent skins. Additionally, South Korea's KF-21 program mandates FST-compliant adhesives for 120 units, with a target completion year of 2032. These military contracts not only shield suppliers from the volatility of commercial price fluctuations but also ensure a steady long-term volume.

Growth of Commercial-Space Launch and In-Orbit-Service Programs

In 2024, SpaceX executed multiple Falcon 9 missions and ramped up Starship production, utilizing adhesives for TPS tiles and cryogenic insulation. Blue Origin's New Glenn rocket achieved its inaugural orbital flight in 2024, employing epoxy systems certified for -196 °C, tailored for carbon-fiber tanks. Virgin Galactic, resuming its tourism flights in 2025, mandated cabin adhesives compliant with ASTM E595 outgassing standards. Northrop Grumman's servicing craft in orbit employs adhesive docking collars, potentially extending satellite lifespans and deferring replacements. Due to the stringent space requirements for radiation tolerance and thermal cycling, margins are notably higher than aviation standards.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in epoxy and isocyanate feedstock supply chains | -1.3% | Global, with acute exposure in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Stringent REACH/CARB VOC caps curbing solvent systems | -0.8% | Europe, North America, spill-over to APAC | Medium term (2-4 years) |

| Qualification bottlenecks for bio-based and recycled chemistries | -0.7% | Global, with early impact in EU and US | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Epoxy and Isocyanate Feed-Stock Supply Chains

In 2024, volatility hit bisphenol-A and epichlorohydrin feedstocks as China, holding a significant share of global capacity, faced export quotas amid power rationing. This scenario led to price spikes, compelling European formulators to turn to sources in India and the Middle East. Toluene diisocyanate and methylene diphenyl diisocyanate experienced fluctuations. Major players like BASF, Covestro, and Wanhua declared force majeure, resulting in an extension of adhesive lead times. Meanwhile, fixed-price contracts with OEMs hindered Tier 1 suppliers from passing costs downstream, thereby compressing margins and heightening supply-chain risks.

Stringent REACH/CARB VOC Caps Curbing Solvent Systems

In 2025, the REACH update set a cap on VOCs in adhesives, making older solvent products non-compliant unless they were reformulated with higher solids or water carriers. In the same year, CARB slashed the permissible VOC limit for aerospace adhesives, leading to a wave of product withdrawals. Additionally, restrictions on nonylphenol and certain phthalates under SVHC have added to the regulatory challenges. Now, OEMs are proactively including "future-proof" clauses in their tenders, pushing for compliance by 2028. This shift is benefiting vertically integrated formulators who possess the capability to handle both reformulation and certification in-house.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Waterborne Formulations Outpace Legacy Solvent Systems

Solvent-borne systems retained a 58.12% aerospace adhesives market share in 2025 because of rapid cure and process familiarity. However, their VOC emissions are increasingly at odds with tightening regulations. This has paved the way for waterborne chemistries, which are set to post a 4.98% CAGR through 2031. The market for waterborne aerospace adhesives is anticipated to grow, buoyed by gains in OEM panel assemblies and interior retrofits. Robotic bonding lines, utilizing reactive two-part epoxies and polyurethanes, benefit from open times and heightened initial tack, enhancing takt reliability. While Asia-Pacific has been slow to adopt, primarily due to a lack of investment in humidity-controlled rooms essential for waterborne curing, references in OEM procurement clauses to VOC ceilings are poised to spur accelerated capital spending.

Automation plays a pivotal role in minimizing application variability. Vision-guided robots, with an accuracy of ±5% of the target weight, apply waterborne pastes, ensuring more uniform bond lines compared to manual methods and significantly cutting down rework. Operators have noted reduced inventories, attributing it to the longer pot life of single-component waterborne products and their less stringent hazardous-material shipping classification. Consequently, suppliers lacking expertise in waterborne products face the risk of being sidelined from new-build programs.

By Resin Type: Epoxy Dominates High-Performance Applications

Epoxy resins accounted for 50.23% of revenue in 2025, capturing the largest share by chemistry. With a 5.12% CAGR through 2031, epoxy's ascent is attributed to its elevated Tg, fatigue resistance, and seamless compatibility with carbon-fiber cure cycles, operating between 120 °C and 180 °C. Furthermore, epoxy's prominence extends to cryogenic tank prototypes, where its rubber-modified matrices maintain ductility even at a frigid -180 °C. While polyurethanes lag due to their lower modulus, limiting them to interior applications, hot-melt grades are carving a niche in sidewall panels, facilitating quicker line moves. Silicones, on the other hand, find their forte in nacelle firewalls and avionics bays, offering vibration damping at temperatures exceeding 200 °C, albeit at a premium price that restricts volume.

In response to REACH and CARB restrictions, epoxy suppliers are actively reducing residual amine and free monomer content. Highlighting the industry's innovative spirit, Hexcel secured a patent for a nano-silica-toughened epoxy, showcasing the delicate balance between toughness and low-viscosity film castability[2]United States Patent and Trademark Office, “Nano-Silica Epoxy Patent,” uspto.gov . Looking ahead, resin vendors that integrate low-SVHC chemistry with advanced digital cure-kinetics modeling are poised to outpace traditional players, especially during pivotal platform refresh cycles.

By Function: Structural Grades Drive Value Creation

Structural products contributed 59.16% of demand in 2025. They are projected to expand at 4.91% CAGR on the back of composite fuselage, wing box, and nacelle integration. Baseline requirements include lap-shear strengths exceeding 30 MPa and 24-hour humidity durability. Meanwhile, emerging cryogenic-ready formulations, enhanced with nano-silica and rubber tougheners, are undergoing pressure tests for applications in Airbus ZEROe and reusable launch vehicles. Although non-structural grades are vital for seat tracks, insulation blankets, and quick repairs, they grapple with price pressures and faster reformulation cycles.

Changes in OEM processes further bolster the demand for structural products. The shift to single-piece barrel manufacturing has removed fastener rows, resulting in longer bonded seams for each aircraft. Additionally, robotic spar bonding lines are transitioning to two-part films that cure in under 90 minutes at 140 °C, allowing for wing movement within the same shift. Suppliers who position application engineers at OEM plants to optimize process windows are securing specifications for next-generation platforms.

By End-Use: OEMs Capture the Largest and Fastest-Growing Share

OEMs consumed 65.23% of aerospace adhesives in 2025, and will expand 4.93% annually to 2031, keeping them the most lucrative customer class. The uptick in demand is largely attributed to the Airbus A321XLR, Boeing 777X, and COMAC C929, all of which are integrating wider bonded skin panels and liquid-hydrogen storage assemblies. Automated bonding lines are amplifying adhesive usage; the consistent bead geometry minimizes squeeze-out, enabling designers to expand the bond-line area for added margin. While aftermarket demand in MRO channels remains steady, it's not as brisk. This is due to older fleets opting for grandfathered solvent-borne kits and spot repairs over complete panel replacements.

However, the Asia-Pacific region stands out in MRO volume. The surge is driven by low-cost carriers emphasizing quick turnaround times. This urgency has led to a preference for depot-grade two-part epoxies, which cure at room temperature in just 30 minutes, allowing mechanics to release aircraft on the same day. Suppliers that provide pre-measured dual-cartridge packages, designed to eliminate scaling errors, are not only securing station approvals but also enhancing their presence in the aftermarket.

Geography Analysis

North America produced 40.14% of the 2025 revenue. The robust demand is buoyed by Boeing's production of the 737 MAX and 787, alongside the F-35 and KC-46 defense programs. The region's early adoption of robotic bonding centers, combined with the use of VOC-compliant waterborne products, not only minimizes scrap but also garners sustainability credits. Furthermore, the co-location of OEMs and suppliers in states like Washington, South Carolina, Texas, and Wichita accelerates pilot-line validation, reduces logistics costs, and solidifies the region's dominant position.

Asia-Pacific is the fastest-growing region, forecast to post a 5.21% CAGR through 2031. The region's share of the aerospace adhesives market is set to increase, driven by COMAC's delivery of C919 jets and Tata-Airbus's ramping up of the C295 line. Japan and South Korea are also contributing, with Mitsubishi's SpaceJet making a comeback and KAI's KF-21 fighter gaining traction. While regional regulations on VOCs are currently more lenient, there's a move towards aligning with REACH standards, fueling investments in waterborne products. Additionally, a burgeoning MRO ecosystem in cities like Singapore, Kuala Lumpur, and Guangzhou bolsters the demand for adhesive retrofits.

Europe plays a crucial role, bolstered by Airbus facilities spread across France, Germany, the UK, and Spain. Research into hydrogen propulsion is channeling research and development funds into adhesive cryogenic testing. Meanwhile, the REACH legislation is hastening the phase-out of solvent-borne products. With tight supply chains and collaborative engineering efforts, the industry is witnessing accelerated recertification cycles. Emerging markets in the Middle East, South America, and Africa, though smaller, are gaining momentum, driven by fleet modernization and new composite-part fabrication centers. Suppliers eyeing joint ventures with local entities are strategically positioning themselves for early advantages as these regions ascend the aerospace value chain.

Competitive Landscape

The aerospace adhesives market is moderately consolidated. The top five vendors' multi-site production, cradle-to-gate quality systems, and embedded engineering teams at OEM assembly lines create meaningful entry barriers. Specialty formulators are carving niches in low-outgassing, rapid-cure, and niche temperature windows. DELO and Dymax are leveraging UV-cure and dual-cure hybrids to shorten interior panel takt times. Competitive weaponry increasingly includes digital curve-simulation software that lets OEMs model bond-line stresses during load cases. Suppliers with robust regulatory intelligence and swift reformulation labs outperform peers as REACH, CARB, and EASA requirements evolve. Robotic automation reshuffles positioning as well. Vendors that integrate dispensing robots, inline calorimetry, and vision systems into a turnkey package capture process control data that OEMs crave for statistical quality control. Combined with sustainability reporting, this digital overlay differentiates offers beyond price per kilogram. The competitive field, therefore, tilts toward companies blending chemistry expertise with automation, data analytics, and regulatory agility.

Aerospace Adhesives Industry Leaders

Henkel AG & Co. KGaA

3M

PPG Industries Inc.

Huntsman International LLC.

H.B. Fuller Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hexcel showcased HexPly M51 rapid-cure prepreg and the complementary HexBond family at the Paris Air Show 2025, emphasizing reduced autoclave times and lower scrap rates.

- May 2024: H.B. Fuller has acquired ND Industries, gaining access to its Vibra-Tite thread-locking adhesives. The move strengthens H.B. Fuller’s product portfolio and expands its presence in the aerospace sector.

- February 2024: PPG introduced PR-2940 epoxy syntactic paste adhesive and PR-2936 skin-bonding product, targeting internal structural and fuselage applications respectively.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the aerospace adhesives market as all film, paste, and liquid bonding formulations certified for fixed-wing, rotorcraft, or spaceframe use, whether applied at the original equipment line or during scheduled maintenance. These chemistries include epoxy, polyurethane, silicone, acrylic, cyanoacrylate, anaerobic, and hybrid systems that join or seal structural and non-structural components exposed to flight loads, extreme temperature swings, vibration, and aviation fluids.

Scope exclusion: generic industrial adhesives sold without aerospace qualification are left outside this assessment.

Segmentation Overview

- By Technology

- Waterborne

- Solvent-Borne

- Reactive

- By Resin Type

- Epoxy

- Polyurethane

- Silicone

- Others

- By Function Type

- Structural

- Non-Structural

- By End-Use

- Original Equipment Manufacturer (OEM)

- Maintenance, Repair and Operations (MRO)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed adhesive formulators, tier-one part fabricators, MRO engineers, and certification consultants across North America, Europe, and Asia-Pacific. These discussions validate usage rates, average selling prices, cure cycle preferences, and foreseeable regulatory hurdles, giving us the context needed to fine-tune model assumptions and stress-test early outputs.

Desk Research

We began with public domain datasets from authorities such as the US Federal Aviation Administration, EASA, and Transport Canada that provide yearly fleet additions, retirements, and flight-hour trends. Trade bodies including IATA, GAMA, and the International Council of Aerospace Industries Associations supply traffic, production, and composite-content ratios that anchor consumption coefficients. Additional insight flows from customs statistics on adhesive HS codes, patent analytics (Questel) that flag new resin families, and company 10-K filings that break out aerospace revenue. Subscription tools like Dow Jones Factiva and D&B Hoovers support competitive share checks and price curves. The sources listed illustrate the range only; many others inform data vetting throughout the project.

A second desk pass screens environmental rules (REACH, CARB VOC caps) and defense budget releases that sway regional demand, while press coverage of OEM ramp-up schedules helps time our adoption curves.

Market-Sizing & Forecasting

After mapping aircraft build and in-service stocks, top-down and bottom-up logic converges. Production and trade data reconstruct the total bonding opportunity by aircraft class, which is then corroborated with sampled ASP × volume inputs from supplier roll-ups. Key variables in the model include composite penetration per airframe, grams of adhesive per square meter of skin, average maintenance interval, resin price inflation, and regional defense procurement cycles. Multivariate regression links these drivers to historic spend and feeds an ARIMA forecast that extends through 2030. Where bottom-up estimates lack granularity, gap factors drawn from primary interviews bridge the distance, ensuring totals remain consistent with real-world purchasing patterns.

Data Validation & Update Cycle

Outputs pass a three-layer check: cross-series variance tests, peer review among senior analysts, and follow-back calls when anomalies surface. Reports refresh every twelve months, with interim updates triggered by material events such as OEM rate changes or disruptive regulation.

Why Mordor's Aerospace Adhesives Totals Earn Trust

Published numbers often differ because firms vary resin scope, bundle sealants, or assume distinct adoption speeds for lightweight composites.

Our team locks definition first, keeps sealants separate, applies current exchange rates, and updates models yearly; some publishers rely on older fleet baselines or static pricing, which magnifies divergence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.90 B (2025) | Mordor Intelligence | - |

| USD 1.32 B (2024) | Global Consultancy A | Includes sealants and counts defense offset packages as adhesive revenue |

| USD 1.27 B (2025) | Industry Publisher B | Uses list prices without regional ASP discounts |

| USD 1.75 B (2024) | Trade Journal C | Grafts aggregate chemicals growth rate onto an older 2019 baseline |

Taken together, the comparison shows that when scope, price realism, and refresh cadence are harmonized, our moderate 2025 baseline provides planners with a balanced, transparent point of departure they can audit quickly and replicate with publicly traceable inputs.

Key Questions Answered in the Report

How large will the aerospace adhesives market be by 2031?

It is projected to reach USD 1.17 billion by 2031 on a 4.78% CAGR trajectory from USD 0.93 billion in 2026.

Which chemistry leads demand?

Epoxy accounted for 50.23% of 2025 revenue and is expected to maintain leadership thanks to high-temperature tolerance and composite compatibility.

What drives the fastest regional growth?

Asia-Pacific’s 5.21% CAGR stems from COMAC C919 production, India’s C295 program, and expanding regional MRO capacity.

How are VOC regulations shaping product portfolios?

REACH and CARB caps below 250 g/L and 120 g/L, respectively, are phasing out legacy solvent products and pushing suppliers toward waterborne and reactive chemistries.

What role does automation play in adhesive consumption?

Robotic bonding lines shorten cycle time, cut scrap, and standardize bead geometry, increasing structural adhesive usage per airframe.

Page last updated on: