Tamaño y Participación del Mercado de Proteína Vegetal de India

Visión General del Mercado

| Período de Estudio | 2021 - 2031 |

|---|---|

| Período de Datos Pronosticados | 2026 - 2031 |

| Período de Datos Históricos | 2021 - 2024 |

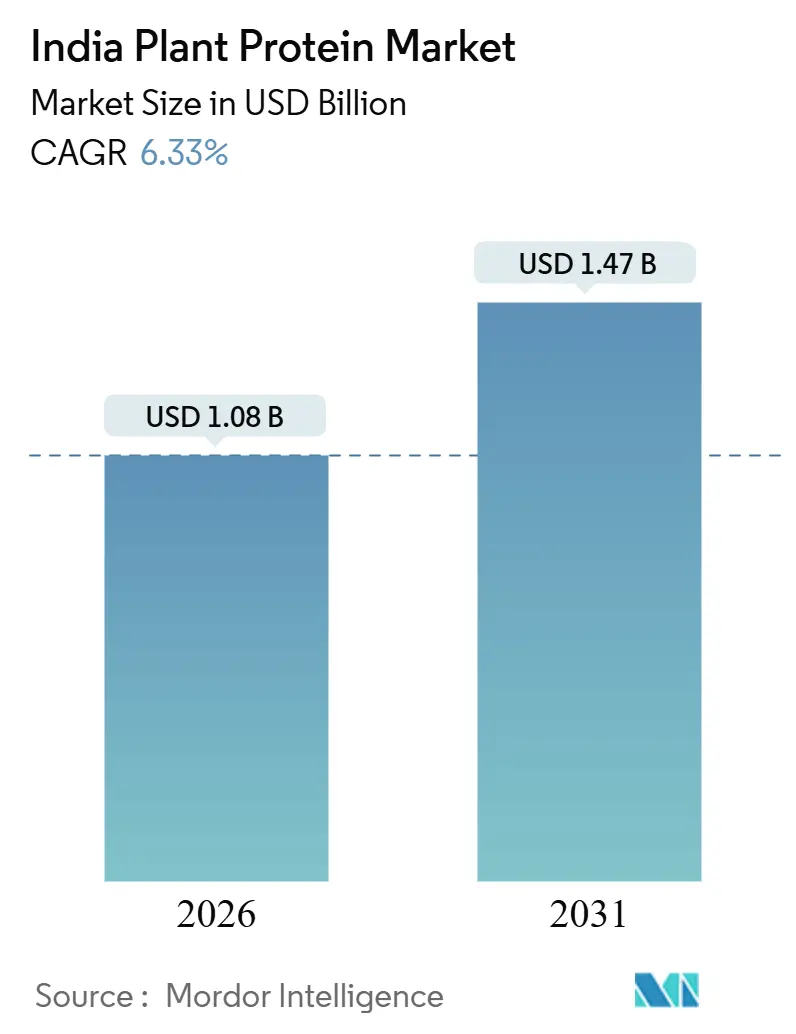

| Tamaño del Mercado (2026) | 1.08 Mil millones de dólares |

| Tamaño del Mercado (2031) | 1.47 Mil millones de dólares |

| Tasa de crecimiento (2026 - 2031) | 6.33% CAGR |

| Concentración del Mercado | Alto |

Jugadores principales *Nota aclaratoria: los principales jugadores no se ordenaron de un modo en especial Imagen © Mordor Intelligence. El uso requiere atribución según CC BY 4.0. | |

Análisis del Mercado de Proteína Vegetal de India por Mordor Intelligence

El tamaño del mercado de proteína vegetal de India se situó en USD 1,08 mil millones en 2026 y se proyecta que alcance USD 1,47 mil millones en 2031, registrando una CAGR del 6,33% durante el período. Los hábitos flexitarianos en aumento en las metrópolis, el impulso de políticas sobre legumbres domésticas y las expansiones de capacidad por parte de procesadores integrados continúan reconfigurando los patrones de abastecimiento, procesamiento y consumo. Los incentivos gubernamentales como la Misión para la Aatmanirbharta en Legumbres, con un presupuesto de INR 11.440 crore, garantizan un suministro confiable de materias primas, mientras que los aumentos en los aranceles de importación sobre los guisantes amarillos impulsan a los fabricantes a localizar el suministro de proteína de guisante. Los consumidores urbanos están cada vez más orientados hacia la salud, y el 84% declara priorizar opciones alimentarias más seguras, lo que crea espacio para productos fortificados y análogos de carne híbridos. Las inversiones de conglomerados como Adani Wilmar y grandes proveedores de ingredientes como ADM mejoran la eficiencia de extracción doméstica y reducen los costos unitarios. La volatilidad de precios en las materias primas de soya y guisante, el cumplimiento del etiquetado y la limitada conciencia del consumidor fuera de las ciudades de primer nivel siguen siendo puntos de atención, aunque el mercado de proteína vegetal de India continúa ampliándose a medida que los procesadores diversifican hacia proteínas de garbanzo, frijol mungo y arroz.

Conclusiones Clave del Informe

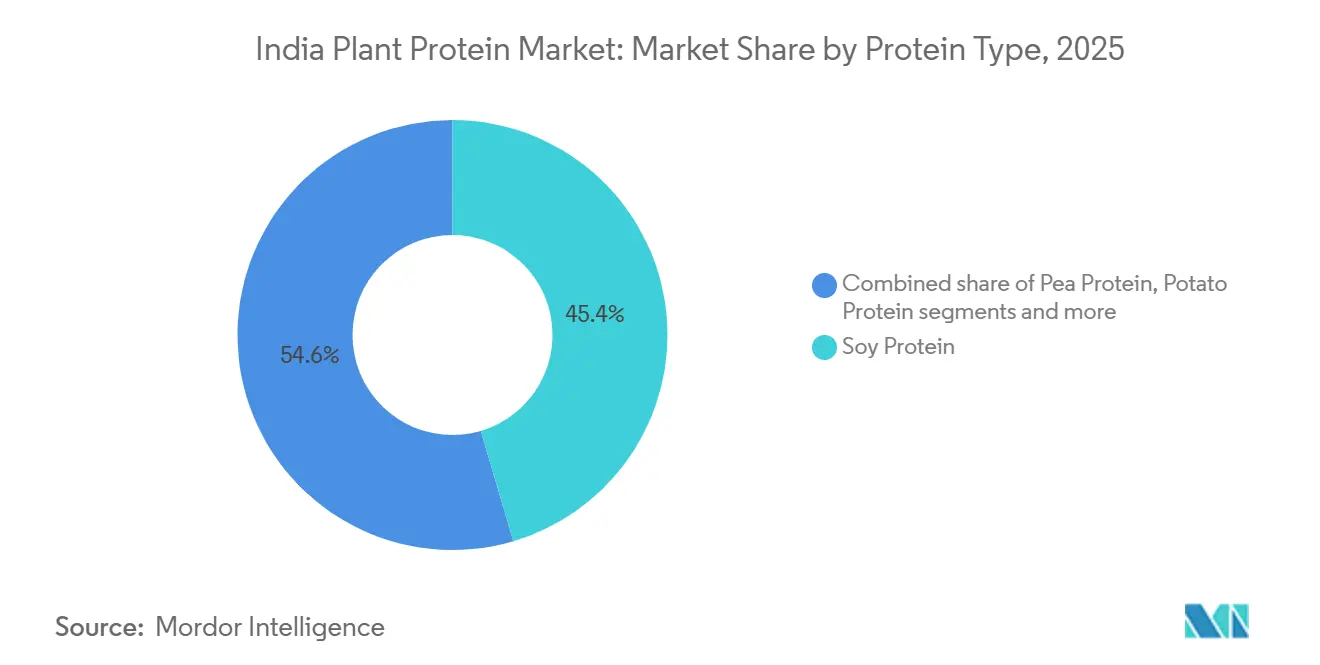

Por tipo de proteína, la soya representó el 45,43% de la participación del mercado de proteína vegetal de India en 2025, y se prevé que la proteína de guisante se expanda a una CAGR del 7,65% hasta 2031.

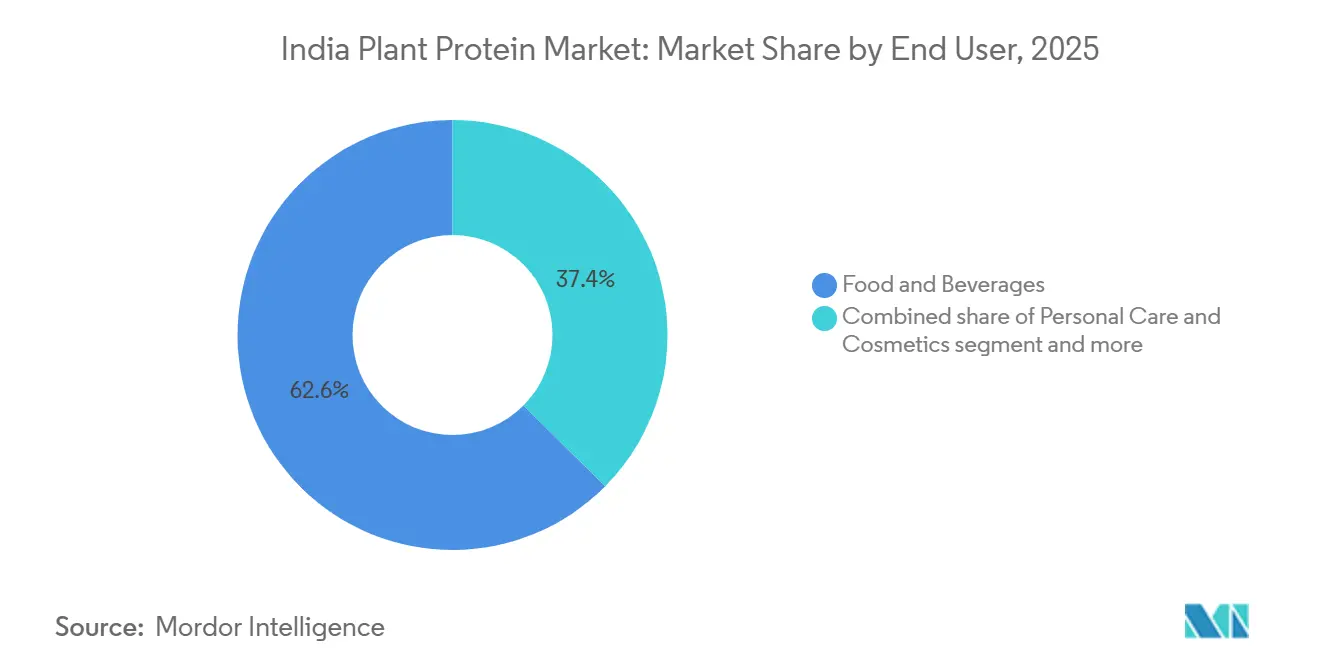

Por usuario final, los alimentos y bebidas representaron el 62,57% de los ingresos en 2025, y se proyecta que los suplementos registren una CAGR del 6,94% hasta 2031.

Nota: Las cifras del tamaño del mercado y los pronósticos de este informe se generan utilizando el marco de estimación patentado de Mordor Intelligence, actualizado con los datos y conocimientos más recientes disponibles a partir de enero de 2026.

Tendencias e Información del Mercado de Proteína Vegetal de India

Análisis del Impacto de los Impulsores*

| Impulsor | (~) % de Impacto en el Pronóstico de CAGR | Relevancia Geográfica | Horizonte Temporal del Impacto |

|---|---|---|---|

| Crecimiento de las dietas basadas en plantas y flexitarianas | +1.2% | Nacional, concentrado en metrópolis (Bombay, Delhi, Bengaluru, Chennai) con expansión hacia ciudades de segundo nivel | Mediano plazo (2-4 años) |

| Aumento de la demanda de alternativas proteicas sin lactosa | +0.9% | Nacional, particularmente en áreas urbanas y semiurbanas con mayor conciencia sobre la intolerancia a los lácteos | Corto plazo (≤ 2 años) |

| Iniciativas gubernamentales de nutrición y apoyo a cultivos | +1.5% | Nacional, con enfoque de producción en Madhya Pradesh, Maharashtra, Rajastán, Uttar Pradesh | Largo plazo (≥ 4 años) |

| Expansión de los sectores de alimentos procesados, bebidas y suplementos | +1.3% | Nacional, impulsado por el comercio minorista organizado y el comercio electrónico en centros urbanos | Mediano plazo (2-4 años) |

| Preferencias del consumidor por productos de etiqueta limpia y fáciles de digerir | +0.8% | Segmentos urbanos y de alto poder adquisitivo a nivel nacional | Corto plazo (≤ 2 años) |

| Innovaciones tecnológicas en el desarrollo de proteínas | +0.6% | Nacional, con centros de I+D en Bengaluru, Pune, Hyderabad | Largo plazo (≥ 4 años) |

| Fuente: Mordor Intelligence | |||

Crecimiento de las Dietas Basadas en Plantas y Flexitarianas

El panorama dietético de la India urbana está experimentando una silenciosa recalibración, con la adopción flexitariana —la sustitución parcial de la proteína animal en lugar de su eliminación total— emergiendo como el patrón de consumo dominante entre los grupos generacionales de millennials y la Generación Z. Este matizado cambio favorece los formatos híbridos, kebabs de origen vegetal, análogos de paneer y snacks tradicionales enriquecidos con proteínas, por encima de los sustitutos directos de la carne, lo que obliga a los fabricantes a localizar las formulaciones en torno a perfiles de especias y métodos de cocción familiares. La nota de prensa de julio de 2025 del Ministerio de Estadística e Implementación de Programas sobre la ingesta nutricional en India documentó una deficiencia proteica persistente en distintos segmentos de la población, generando impulso político para la incorporación de productos de proteína vegetal fortificada en los esquemas de comidas escolares y en los sistemas de distribución pública. Esta brecha estructural de proteínas es un catalizador clave en todo el mercado de proteínas de India, donde la creciente conciencia sobre la salud está impulsando a los consumidores hacia diversas fuentes de proteínas. El comercio minorista organizado y los restaurantes de servicio rápido están acelerando la prueba de estos productos al ofrecer opciones de origen vegetal junto a las ofertas convencionales, reduciendo la fricción del cambio de categoría para los consumidores sensibles al precio.

Aumento de la Demanda de Alternativas Proteicas sin Lactosa

La prevalencia de la intolerancia a la lactosa en India, que se estima afecta a una parte significativa de la población adulta, ha sido históricamente desatendida por los lácteos convencionales, lo que abre una oportunidad estructural para la leche a base de plantas, el yogur y los análogos de paneer. La leche de soya y las bebidas de proteína de guisante están ganando terreno en los hogares urbanos como sustitutos funcionales, con fabricantes que enfatizan la fortificación con calcio, vitamina D y B12 para abordar las brechas nutricionales asociadas con la evitación de los lácteos. Las directrices de etiquetado nutricional de la FSSAI exigen una declaración clara del contenido de proteínas por cada 100 gramos y por porción, lo que permite la comparación directa con los lácteos de origen animal y apoya la confianza del consumidor en la adecuación proteica[1]Fuente: Autoridad de Seguridad e Inocuidad Alimentaria de India, "Directrices sobre Etiquetado Nutricional," fssai.gov.in. El requisito regulatorio de declaración de alérgenos, en particular para la soya —un alérgeno importante—, garantiza la transparencia, pero también exige una formulación cuidadosa y controles de la cadena de suministro para prevenir la contaminación cruzada. Las empresas emergentes están aprovechando el comercio electrónico y los modelos de suscripción para llegar a los primeros adoptantes, evitando los intermediarios minoristas tradicionales y captando retroalimentación directa del consumidor para perfeccionar el sabor y la textura.

Iniciativas Gubernamentales de Nutrición y Apoyo a Cultivos

La aprobación del Gabinete de la Unión en octubre de 2025 de la Misión para la Aatmanirbharta en Legumbres, con un presupuesto de seis años de INR 11.440 crore (aproximadamente USD 1,37 mil millones), representa la intervención política más significativa en el suministro doméstico de legumbres en una década. La misión tiene como objetivo aumentar el área, la productividad y la infraestructura poscosecha para el garbanzo, la paloma de campo, la lenteja y el frijol mungo, abordando directamente las restricciones de materias primas para los concentrados y aislados de proteínas derivados de legumbres. El informe de septiembre de 2025 del NITI Aayog sobre estrategias para acelerar el crecimiento de las legumbres subrayó la necesidad de mejorar los sistemas de semillas, la extensión agronómica y las inversiones en la cadena de valor para reducir la dependencia de las importaciones y estabilizar los precios[2]Fuente: NITI Aayog, "Estrategias y Vías para Acelerar el Crecimiento en Legumbres," pib.gov.in. Para los procesadores de proteína vegetal, este impulso político señala una disponibilidad predecible de materias primas y una posible presión a la baja sobre los precios de las legumbres a mediano plazo, mejorando la competitividad de las proteínas de legumbres domésticas frente a los aislados de guisante o soya importados. El énfasis de la misión en el procesamiento y la agregación de valor crea oportunidades de coinversión para instalaciones privadas de fraccionamiento y plantas piloto de extracción de proteínas.

Expansión de los Sectores de Alimentos Procesados, Bebidas y Suplementos

El sector de procesamiento de alimentos organizado de India está experimentando una actualización estructural, con inversiones en logística de cadena de frío, envases modernos y redes de distribución minorista que permiten que los productos de proteína vegetal estables en estantería lleguen a las ciudades de segundo y tercer nivel. El informe anual 2023-24 de la APEDA detalló subvenciones de infraestructura y esquemas de promoción de exportaciones que reducen las cargas de gasto de capital para los procesadores de proteína vegetal, mientras que los programas de asistencia técnica apoyan a las MIPYMES en el cumplimiento de los estándares internacionales de calidad e inocuidad[3]Fuente: Autoridad de Desarrollo de Exportaciones de Productos Alimentarios Agrícolas y Procesados, "Legumbres," apeda.gov.in . El segmento de suplementos, que abarca la nutrición deportiva, la fórmula infantil y la nutrición para adultos mayores, está experimentando una evolución regulatoria, con las Regulaciones de Alimentos Infantiles de enero de 2024 de la FSSAI (Versión II) que establecen requisitos estrictos de composición y etiquetado de alérgenos para la inclusión de proteína vegetal en productos para la primera infancia. Los fabricantes deben demostrar la calidad de la proteína mediante PDCAAS o métricas equivalentes y garantizar la complementación de aminoácidos cuando las proteínas vegetales reemplazan a los lácteos, elevando el estándar de experiencia en formulación y sustanciación clínica. Las plataformas de comercio electrónico y las marcas de venta directa al consumidor están evitando el comercio minorista tradicional aprovechando el marketing digital y las asociaciones con influenciadores para educar a los consumidores sobre el contenido de proteínas, las etiquetas limpias y las afirmaciones de sostenibilidad.

Análisis del Impacto de las Restricciones*

| Restricción | (~) % de Impacto en el Pronóstico de CAGR | Relevancia Geográfica | Horizonte Temporal del Impacto |

|---|---|---|---|

| Prima de precio sobre la proteína animal | -0.8% | Nacional, más aguda en áreas rurales y semiurbanas con alta sensibilidad al precio | Corto plazo (≤ 2 años) |

| Volatilidad de los precios de las materias primas de guisante y soya | -0.6% | Nacional, con riesgo de producción concentrado en Madhya Pradesh, Maharashtra | Mediano plazo (2-4 años) |

| Baja conciencia y barreras sensoriales más allá de las metrópolis | -0.5% | Zonas rurales y ciudades de tercer nivel, donde el consumo tradicional de proteína animal está arraigado | Mediano plazo (2-4 años) |

| Obstáculos regulatorios relacionados con las declaraciones de contenido proteico y los estándares de etiquetado | -0.4% | Nacional, que afecta los plazos de desarrollo de productos y la entrada al mercado | Corto plazo (≤ 2 años) |

| Fuente: Mordor Intelligence | |||

Prima de Precio sobre la Proteína Animal

Los productos de proteína a base de plantas en India generalmente se venden con primas del 20-40% sobre las proteínas animales convencionales, una brecha que limita la adopción masiva y confina el crecimiento a los segmentos urbanos de alto poder adquisitivo. Los precios mayoristas de la soya promediaron Rs 4.825 por quintal en septiembre de 2024, mientras que los márgenes de los trituradores permanecieron comprimidos debido a la competencia de la harina de soya argentina más barata y el aceite de soya importado con descuento, según el Centro de Inteligencia de Mercados Agrícolas de la PJTSAU[4]Fuente: Centro de Inteligencia de Mercados Agrícolas de la PJTSAU, "Perspectivas de la Soya – Octubre de 2024," pjtau.edu.in. Estas presiones sobre los costos de insumos se traducen en precios minoristas más altos para los concentrados y aislados de proteína de soya, socavando la competitividad frente al pollo, los huevos y los lácteos en los hogares sensibles al precio. La decisión del gobierno de mayo de 2025 de aumentar el precio mínimo de apoyo para la soya en un 9% a Rs 5.328 por quintal tenía como objetivo incentivar a los agricultores, pero inadvertidamente elevó los costos de materias primas para los procesadores, ajustando los márgenes y limitando su capacidad de reducir los precios al consumidor, según el Servicio Agrícola Exterior del Departamento de Agricultura de los Estados Unidos. Lograr la paridad de precios requerirá economías de escala en el fraccionamiento, el abastecimiento localizado de legumbres bajo la Misión de Legumbres, e innovaciones en formulación que combinen proteínas de arroz o trigo de menor costo con aislados premium de guisante o soya para optimizar las compensaciones entre costo y rendimiento.

Volatilidad de los Precios de las Materias Primas de Guisante y Soya

La producción de soya en el año comercial 2025/26 disminuyó un 12% a 10,7 millones de toneladas debido a lluvias inoportunas, retrasos en la resiembra y la diversificación de los agricultores hacia el arroz, la caña de azúcar y el maíz, lo que tensó el suministro doméstico de harina de soya y aumentó la incertidumbre de materias primas para los fabricantes de proteína vegetal, según el Servicio Agrícola Exterior del Departamento de Agricultura de los Estados Unidos (USDA FAS). Los volúmenes de trituración cayeron un 6% a 9,5 millones de toneladas, y la producción de harina de soya descendió a 7,6 millones de toneladas, con las existencias finales recortadas en un 52% a 455.000 toneladas, lo que señala tensión en el lado de la oferta. El aumento de India en noviembre de 2025 de los aranceles de importación sobre los guisantes amarillos —una materia prima clave para los aislados de proteína de guisante— restringió aún más las opciones de abastecimiento alternativo, obligando a los procesadores domésticos a absorber costos de desembarque más altos o trasladarlos a los clientes intermedios, según el USDA FAS. La participación combinada del 82% de Madhya Pradesh y Maharashtra en el área nacional de soya concentra el riesgo de producción en dos estados, amplificando la vulnerabilidad a los choques climáticos localizados y los brotes de plagas. Diversificar las carteras de materias primas para incluir proteínas de garbanzo, frijol mungo y arroz, junto con el almacenamiento estratégico de reservas y la contratación a plazo, será esencial para mitigar la volatilidad de precios y garantizar la continuidad del suministro.

*Nuestras previsiones consideran los impactos de impulsores y restricciones como direccionales, no aditivos. Las previsiones de impacto reflejan el crecimiento base, los efectos de mezcla y las interacciones entre variables.

Análisis de Segmentos

Por Tipo de Proteína: El Dominio de la Soya se Encuentra con el Impulso de la Proteína de Guisante

La Proteína de Soya mantuvo una participación de mercado del 45,43% en 2025, anclada en el establecido cultivo de soya de India en Madhya Pradesh y Maharashtra —estados que en conjunto representan el 82% del área nacional de soya— y en la infraestructura de trituración madura capaz de producir harina de soya, harina de soya y proteína vegetal texturizada a escala, según la PJTSAU. La trituración doméstica de soya alcanzó 9,5 millones de toneladas en el año comercial 2025/26, produciendo 7,6 millones de toneladas de harina de soya, una parte de la cual se destina a aplicaciones de grado alimentario, incluidos concentrados y aislados de proteína de soya para análogos de carne, alternativas lácteas y productos de panadería fortificados, según el USDA FAS. Se prevé que la Proteína de Guisante se expanda a una CAGR del 7,65% hasta 2031, impulsada por los incentivos de sustitución de importaciones tras el aumento de India en noviembre de 2025 de los aranceles de importación de guisantes amarillos, que elevaron los costos de desembarque de la proteína de guisante importada y estimularon el interés doméstico en el cultivo de guisantes de campo y la inversión en capacidad de fraccionamiento. El perfil de sabor neutro y las propiedades hipoalergénicas de la proteína de guisante la posicionan favorablemente en los segmentos de fórmula infantil y nutrición deportiva, donde las preocupaciones sobre la alergenicidad y los fitoestrógenos de la soya pueden limitar su adopción.

La Proteína de Arroz y la Proteína de Trigo ocupan nichos más pequeños pero en crecimiento, con la proteína de arroz atrayendo a los consumidores sin gluten y sensibles a los alérgenos, y el gluten de trigo (gluten de trigo vital) sirviendo como texturizante en análogos de carne a base de plantas y aplicaciones de panadería. La Proteína de Cáñamo y la Proteína de Papa siguen siendo incipientes en India, limitadas por el cultivo doméstico restringido de cáñamo industrial —las aprobaciones regulatorias para el cultivo de cáñamo son específicas de cada estado e incompletas— y la ausencia de instalaciones de extracción de proteína de papa a gran escala. Otras Proteínas Vegetales, incluidas las proteínas de garbanzo, frijol mungo y lenteja, se benefician del estatus de India como el mayor productor mundial de legumbres (25,238 millones de toneladas en 2024-25) y ofrecen oportunidades para el desarrollo de ingredientes localizados alineados con los patrones dietéticos tradicionales, según la APEDA. Los estándares de mayo de 2023 de la FSSAI para la harina de soya extraída con solvente (mínimo 48% de proteína en base seca, residuo de hexano ≤10 ppm) y la harina de trigo enriquecida con proteínas (mínimo 15% de proteína) proporcionan puntos de referencia de composición que guían la formulación y el control de calidad para los fabricantes. Los avances tecnológicos en la extracción alcalina y la hidrólisis enzimática están mejorando los rendimientos de proteínas y las propiedades funcionales, lo que permite a los procesadores domésticos competir con los aislados importados en costo y rendimiento.

Por Usuario Final: Alimentos y Bebidas Lideran, los Suplementos se Aceleran

Alimentos y Bebidas representó el 62,57% de la participación de usuarios finales en 2025, reflejando una demanda arraigada en alternativas lácteas (leche de soya, yogur de proteína de guisante, análogos de paneer), alternativas cárnicas (kebabs a base de plantas, hamburguesas, salchichas), productos de panadería (pan enriquecido con proteínas, galletas), comidas listas para consumir y bebidas (batidos de proteínas, bebidas fortificadas). Los Lácteos y Alternativas Lácteas representan el subsegmento más grande, impulsado por la prevalencia de la intolerancia a la lactosa y la preferencia del consumidor por formatos familiares —leche, cuajada y paneer— que se integran perfectamente en las dietas diarias. Las Alternativas de Carne/Aves/Mariscos están ganando terreno en los restaurantes de servicio rápido urbanos y el comercio minorista moderno, con empresas emergentes como GoodDot, Imagine Meats y Blue Tribe Foods aprovechando los canales de venta directa al consumidor y los sabores localizados (tikka, keema, biryani) para superar las barreras sensoriales. Las aplicaciones de panadería se benefician de la autorización regulatoria de la FSSAI para hasta el 15% de harina de proteína vegetal (soya, maní) en harina de trigo y maida enriquecidas con proteínas, lo que permite que los alimentos básicos fortificados lleguen a los mercados masivos a través del comercio minorista tradicional y los sistemas de distribución pública.

Se prevé que los Suplementos crezcan a una CAGR del 6,94% hasta 2031, impulsados por la creciente conciencia sobre la salud, la adopción de la nutrición deportiva entre los millennials y la claridad regulatoria sobre las declaraciones de contenido proteico. Los Suplementos Deportivos y Dietéticos —polvos de proteínas alternativos al suero de leche, batidos listos para beber y barras de proteínas— están captando participación de la proteína de suero de leche importada a medida que los aislados domésticos de guisante y soya mejoran en sabor y solubilidad. La guía de la FSSAI sobre nutrición deportiva y suplementos alimenticios para deportistas, emitida en 2025, estableció estándares para el contenido de proteínas, los perfiles de aminoácidos y los aditivos permitidos, reduciendo la ambigüedad regulatoria y fomentando el lanzamiento de productos. Los Alimentos para Bebés y la Fórmula Infantil enfrentan obstáculos regulatorios estrictos bajo las Regulaciones de Alimentos Infantiles de enero de 2024 de la FSSAI, que exigen métricas de calidad proteica (umbrales de PDCAAS), etiquetado de alérgenos y sustanciación clínica para la inclusión de proteína vegetal, lo que limita la adopción a corto plazo pero crea oportunidades para formulaciones especializadas dirigidas a lactantes con intolerancia a la lactosa. Los productos de Nutrición para Adultos Mayores y Nutrición Médica —formulaciones de alta proteína y fácil digestión para poblaciones geriátricas y en convalecencia— están emergiendo como un segmento de nicho, con fabricantes que fortifican las bases de proteína vegetal con calcio, vitamina D y B12 para abordar las deficiencias nutricionales relacionadas con la edad.

Las aplicaciones de Alimento para Animales consumen una parte significativa de la producción de harina de soya (6,15 millones de toneladas en 2025/26), con los sectores avícola y acuícola impulsando la demanda de ingredientes de alimento ricos en proteínas, según el USDA FAS. Sin embargo, la sustitución en el sector de alimento hacia granos de destilería secos (DDG) y salvado de arroz desgrasado —subproductos de la expansión de la producción de etanol a base de granos— está reduciendo la demanda de harina de soya, lo que podría liberar suministro para el procesamiento de proteína vegetal de grado alimentario. El Cuidado Personal y los Cosméticos representan una aplicación incipiente, con proteínas vegetales (soya, trigo, arroz) utilizadas como agentes acondicionadores, formadores de película y emulsionantes en formulaciones de cuidado del cabello y la piel, aunque este segmento sigue siendo marginal en relación con los usos alimentarios y de alimento animal.

Análisis Geográfico

El mercado de proteína vegetal de India está geográficamente anclado en Madhya Pradesh y Maharashtra, que en conjunto representaron el 82% del área nacional de soya en 2024-25 y albergan la mayoría de las instalaciones de trituración a gran escala operadas por Ruchi Soya, Sonic Biochem y cooperativas regionales, según la PJTSAU. Madhya Pradesh por sí solo representó el 42,14% del área de soya (53,48 lakh de hectáreas), con producción concentrada en distritos como Indore, Ujjain y Dewas, donde las redes de adquisición establecidas y los clústeres de procesamiento permiten la conversión eficiente de oleaginosas en harina de soya y harina de soya. La participación del 40,47% del área de Maharashtra (51,36 lakh de hectáreas) apoya un ecosistema de procesamiento paralelo, con instalaciones en Nagpur, Akola y Latur que sirven a los fabricantes de alimentos domésticos y los mercados de exportación. Rajastán, Karnataka, Guyarat y Telangana representan colectivamente el 18% restante, con Rajastán contribuyendo el 8,87% del área de soya y emergiendo como un centro de producción secundario. La producción de legumbres está más dispersa geográficamente, con Madhya Pradesh, Maharashtra, Rajastán, Uttar Pradesh, Guyarat, Karnataka, Jharkhand, Andhra Pradesh, Chhattisgarh y Bengala Occidental contribuyendo a las 25,238 millones de toneladas cosechadas en 2024-25, proporcionando diversidad de materias primas para proteínas de garbanzo, paloma de campo, lenteja y frijol mungo, según la APEDA.

El consumo urbano está concentrado en las metrópolis —Bombay, Delhi, Bengaluru, Chennai, Hyderabad y Pune— donde la penetración del comercio minorista moderno, la adopción del comercio electrónico y la exposición a las tendencias alimentarias internacionales impulsan la adopción temprana de análogos de carne a base de plantas, alternativas lácteas y suplementos proteicos. Las ciudades de segundo nivel —Ahmedabad, Jaipur, Lucknow, Coimbatore, Visakhapatnam— están experimentando una difusión gradual a medida que el comercio minorista organizado se expande y crece la conciencia del consumidor, aunque la sensibilidad al precio y la infraestructura limitada de cadena de frío siguen siendo restricciones. Las áreas rurales y semiurbanas, que representan la mayoría de la población de India, exhiben menor conciencia y adopción, con patrones de consumo tradicional de proteína animal y redes minoristas fragmentadas que limitan la penetración de la proteína vegetal. La dinámica de exportación está evolucionando, con India exportando 793.291,51 toneladas métricas de legumbres valoradas en USD 854,89 millones en el año fiscal 2024-25, principalmente a Bangladesh, China, Emiratos Árabes Unidos, Estados Unidos y Sri Lanka, lo que señala el potencial para exportaciones de proteína de legumbres con valor agregado si la capacidad doméstica de fraccionamiento escala. El informe anual 2023-24 de la APEDA destacó subvenciones de infraestructura y esquemas de promoción de exportaciones que apoyan las mejoras de calidad, las pruebas y el acceso al mercado para los procesadores de proteína vegetal que apuntan a los mercados internacionales.

Las iniciativas de política a nivel estatal están comenzando a configurar la competitividad regional, con Madhya Pradesh y Maharashtra ofreciendo subsidios para el procesamiento de oleaginosas y la infraestructura de valor agregado, mientras que Karnataka y Telangana —sede de centros de biotecnología y procesamiento de alimentos en Bengaluru y Hyderabad— están atrayendo inversiones en I+D en tecnologías novedosas de extracción y proteínas basadas en fermentación. Se espera que la aprobación del Gabinete de la Unión en octubre de 2025 de la Misión para la Aatmanirbharta en Legumbres, con un presupuesto de seis años de INR 11.440 crore, fortalezca la producción de legumbres en múltiples estados, reduciendo los desequilibrios regionales de suministro y estabilizando los precios de materias primas para los fabricantes de proteína vegetal. La infraestructura logística —redes de cadena de frío, almacenamiento y conectividad portuaria— sigue siendo un cuello de botella, particularmente para los análogos de lácteos y carne a base de plantas perecederos, con el enfoque del gobierno en las zonas de procesamiento de alimentos y los proyectos integrados de cadena de frío bajo el Ministerio de Industrias de Procesamiento de Alimentos orientados a abordar estas brechas.

Panorama Competitivo

El mercado de proteína vegetal de India se está consolidando, con actores clave como Ruchi Soya (bajo Patanjali Ayurved), Sonic Biochem, ADM y Cargill controlando una capacidad significativa de trituración de soya y producción de harina de soya, mientras que una creciente cohorte de empresas emergentes y actores de tamaño mediano apunta a segmentos de nicho con productos diferenciados y estrategias de venta directa al consumidor. Ruchi Soya, el mayor productor integrado de proteína de soya y alimentos de soya de India, opera instalaciones de trituración, unidades de refinación y líneas de productos de consumo de marca, aprovechando la integración vertical para gestionar los costos de materias primas y los riesgos de la cadena de suministro.

Sonic Biochem, un fabricante líder de proteínas funcionales de soya no modificada genéticamente, se enfoca en los mercados de exportación y el suministro doméstico de ingredientes alimentarios, enfatizando las certificaciones de calidad y la trazabilidad para cumplir con los estándares internacionales. Las multinacionales como ADM y Cargill suministran ingredientes de soya y proteína vegetal a los fabricantes de alimentos y alimento animal de India, con el anuncio de ADM en enero de 2025 de programas de producción sostenible de soya en India que señala un compromiso estratégico con el abastecimiento local y las credenciales de sostenibilidad. PROWISE India, el primer y único fabricante del país de proteína de soya aislada (PSA), apunta a los mercados premium de ingredientes de proteína vegetal, compitiendo en pureza y propiedades funcionales. Las empresas emergentes —GoodDot Enterprises, Imagine Meats, Blue Tribe Foods y Shaka Harry— están disrumpiendo los canales tradicionales al lanzar análogos de carne a base de plantas adaptados a los paladares indios, utilizando el comercio minorista moderno, el comercio electrónico y las asociaciones con el sector de servicios de alimentos para evitar las redes de distribución establecidas. Estos actores aprovechan los conocimientos del consumidor, la iteración rápida de productos y el marketing digital para capturar los segmentos de primeros adoptantes, aunque la escalabilidad sigue siendo limitada por los altos costos de adquisición de clientes y el acceso limitado a aislados de proteínas competitivos en costo.

La puesta en marcha en enero de 2025 por parte de Adani Wilmar de una planta de procesamiento de alimentos de Rs 1.300 crore en Sonepat ejemplifica la expansión de capacidad por parte de conglomerados diversificados que buscan integrar la trituración de oleaginosas aguas arriba con productos de proteína vegetal con valor agregado aguas abajo, intensificando potencialmente la competencia por materias primas y espacio en estantería. Las oportunidades de espacio en blanco incluyen los aislados de proteínas a base de legumbres (garbanzo, frijol mungo, lenteja), que se alinean con las fortalezas de producción doméstica de India y la familiaridad cultural, pero que siguen subdesarrollados debido a la capacidad de fraccionamiento limitada y la experiencia técnica. La adopción de tecnología —fraccionamiento húmedo, hidrólisis enzimática y fermentación— determinará el posicionamiento competitivo, con los primeros en adoptar tecnologías de extracción verde potencialmente capturando ventajas de costo y sostenibilidad a medida que la iniciativa de estandarización de marzo de 2025 de GFI India gana impulso.

Líderes de la Industria de Proteína Vegetal de India

Ruchi Soya Industries Ltd.

Sonic Biochem Extractions Pvt Ltd.

Archer Daniels Midland Company (ADM)

Cargill, Incorporated

PROWISE India

- *Nota aclaratoria: los principales jugadores no se ordenaron de un modo en especial

Desarrollos Recientes de la Industria

- Julio de 2025: Prot ha lanzado Prot Block, un ingrediente a base de proteína de guisante diseñado como una solución versátil y libre de alérgenos que cierra la brecha entre los análogos de carne altamente procesados y las proteínas vegetales convencionales limitadas, permitiendo la fácil integración de proteína vegetal en los platos cotidianos.

- Enero de 2025: ADM anunció programas para apoyar la producción sostenible de soya en India, asociándose con agricultores, cooperativas y ONG para mejorar los rendimientos, la salud del suelo y la trazabilidad, con el objetivo de asegurar un suministro de materias primas sostenible a largo plazo para la fabricación de ingredientes de proteína vegetal.

- Enero de 2025: Adani Wilmar puso en marcha una planta de procesamiento de alimentos de Rs 1.300 crore (aproximadamente USD 156 millones) en Sonepat, Haryana, ampliando la capacidad de procesamiento doméstico y señalando la entrada de conglomerados diversificados en la fabricación de productos de proteína vegetal con valor agregado.

Alcance del Informe del Mercado de Proteína Vegetal de India

La proteína vegetal se refiere a la proteína extraída o derivada de fuentes vegetales como legumbres, granos, semillas y nueces, utilizada como ingrediente nutricional en alimentos, bebidas y suplementos. Este informe define el Mercado de Proteína Vegetal de India como la industria enfocada en la producción, procesamiento y aplicación de proteínas derivadas de fuentes vegetales, y examina su alcance por tipo de proteína (cáñamo, guisante, papa, arroz, soya, trigo y otras proteínas vegetales) y por usuario final, incluido el alimento para animales; alimentos y bebidas (panadería, bebidas, cereales de desayuno, condimentos/salsas, confitería, lácteos y alternativas lácteas, carne/aves/mariscos y sus alternativas, alimentos listos para consumir/listos para cocinar y aperitivos); cuidado personal y cosméticos; y suplementos (alimentos para bebés y fórmula infantil, nutrición para adultos mayores y nutrición médica, y suplementos deportivos y dietéticos).

| Proteína de Cáñamo |

| Proteína de Guisante |

| Proteína de Papa |

| Proteína de Arroz |

| Proteína de Soya |

| Proteína de Trigo |

| Otras Proteínas Vegetales |

| Alimento para Animales | |

| Alimentos y Bebidas | Panadería |

| Bebidas | |

| Cereales de Desayuno | |

| Condimentos/Salsas | |

| Confitería | |

| Lácteos y Alternativas Lácteas | |

| Carne/Aves/Mariscos y Alternativas | |

| Alimentos Listos para Consumir/Listos para Cocinar | |

| Aperitivos | |

| Cuidado Personal y Cosméticos | |

| Suplementos | Alimentos para Bebés y Fórmula Infantil |

| Nutrición para Adultos Mayores y Nutrición Médica | |

| Suplementos Deportivos y Dietéticos |

| Por Tipo de Proteína | Proteína de Cáñamo | |

| Proteína de Guisante | ||

| Proteína de Papa | ||

| Proteína de Arroz | ||

| Proteína de Soya | ||

| Proteína de Trigo | ||

| Otras Proteínas Vegetales | ||

| Por Usuario Final | Alimento para Animales | |

| Alimentos y Bebidas | Panadería | |

| Bebidas | ||

| Cereales de Desayuno | ||

| Condimentos/Salsas | ||

| Confitería | ||

| Lácteos y Alternativas Lácteas | ||

| Carne/Aves/Mariscos y Alternativas | ||

| Alimentos Listos para Consumir/Listos para Cocinar | ||

| Aperitivos | ||

| Cuidado Personal y Cosméticos | ||

| Suplementos | Alimentos para Bebés y Fórmula Infantil | |

| Nutrición para Adultos Mayores y Nutrición Médica | ||

| Suplementos Deportivos y Dietéticos | ||

Definición de mercado

- Usuario Final - El Mercado de Ingredientes Proteicos opera sobre una base B2B. Los fabricantes de Alimentos, Bebidas, Suplementos, Alimento para Animales y Cuidado Personal y Cosméticos se consideran usuarios finales en el mercado estudiado. El alcance excluye a los fabricantes que compran suero de leche líquido/seco para su uso como agente aglutinante, espesante u otras aplicaciones no proteicas.

- Tasa de Penetración - La Tasa de Penetración se define como el porcentaje del Volumen del Mercado de Usuario Final Fortificado con Proteínas en el Volumen Total del Mercado de Usuario Final.

- Contenido Proteico Promedio - El contenido proteico promedio es el contenido proteico promedio presente por cada 100 g de producto fabricado por todas las empresas de usuarios finales consideradas en el alcance de este informe.

- Volumen del Mercado de Usuario Final - El volumen del mercado de usuario final es el volumen consolidado de todos los tipos y formas de productos de usuario final en el país o región.

| Palabra clave | Definición |

|---|---|

| Alfa-lactoalbúmina (α-Lactoalbúmina) | Es una proteína que regula la producción de lactosa en la leche de casi todas las especies de mamíferos. |

| Aminoácido | Es un compuesto orgánico que contiene grupos funcionales tanto amino como de ácido carboxílico, necesarios para la síntesis de proteínas corporales y otros compuestos importantes que contienen nitrógeno, como la creatina, las hormonas peptídicas y algunos neurotransmisores. |

| Escaldado | Es el proceso de calentar brevemente las verduras con vapor o agua hirviendo. |

| BRC | Consorcio Minorista Británico |

| Mejorador de pan | Es una mezcla a base de harina de varios componentes con propiedades funcionales específicas diseñadas para modificar las características de la masa y dar atributos de calidad al pan. |

| BSF | Mosca Soldado Negro |

| Caseinato | Es una sustancia producida al añadir un álcali a la caseína ácida, un derivado de la caseína. |

| Enfermedad celíaca | La enfermedad celíaca es una reacción inmune a la ingesta de gluten, una proteína que se encuentra en el trigo, la cebada y el centeno. |

| Calostro | Es un fluido lácteo que liberan los mamíferos que han dado a luz recientemente, antes de que comience la producción de leche materna. |

| Concentrado | Es la forma menos procesada de proteína y tiene un contenido proteico que oscila entre el 40-90% en peso. |

| Base de proteína seca | Se refiere al porcentaje de "proteína pura" presente en un suplemento después de que el agua que contiene se elimina completamente mediante calor. |

| Suero de leche seco | Es el producto resultante del secado del suero de leche fresco que ha sido pasteurizado y al que no se le ha añadido nada como conservante. |

| Proteína de huevo | Es una mezcla de proteínas individuales, que incluye ovoalbúmina, ovomucoides, ovoglobulinas, conalbúmina, vitelina y vitelenina. |

| Emulsionante | Es un aditivo alimentario que facilita la mezcla de alimentos que son inmiscibles entre sí, como el aceite y el agua. |

| Enriquecimiento | Es el proceso de adición de micronutrientes que se pierden durante el procesamiento del producto. |

| ERS | Servicio de Investigación Económica del USDA |

| Extrusión | Es el proceso de forzar ingredientes mezclados blandos a través de una abertura en una placa perforada o troquel diseñado para producir la forma requerida. El alimento extruido se corta luego a un tamaño específico mediante cuchillas. |

| Fava | También conocida como Faba, es otra palabra para los frijoles amarillos partidos. |

| FDA | Administración de Alimentos y Medicamentos |

| Laminado | Es un proceso en el que típicamente un grano de cereal (como maíz, trigo o arroz) se descompone en sémola, se cocina con sabores y jarabes, y luego se prensa en copos entre rodillos enfriados. |

| Agente espumante | Es un ingrediente alimentario que hace posible formar o mantener una dispersión uniforme de una fase gaseosa en un alimento líquido o sólido. |

| Servicios de alimentación | Se refiere a la parte de la industria alimentaria que incluye empresas, instituciones y compañías que preparan comidas fuera del hogar. Incluye restaurantes, cafeterías escolares y hospitalarias, operaciones de catering y muchos otros formatos. |

| Fortificación | Es la adición deliberada de micronutrientes que no se encuentran en ellos de forma natural o que se pierden durante el procesamiento, para mejorar el valor nutricional de un producto alimentario. |

| FSANZ | Normas Alimentarias de Australia y Nueva Zelanda |

| FSIS | Servicio de Inspección e Inocuidad Alimentaria |

| FSSAI | Autoridad de Seguridad e Inocuidad Alimentaria de India |

| Agente gelificante | Es un ingrediente que funciona como estabilizador y espesante para proporcionar espesor sin rigidez mediante la formación de gel. |

| GHG | Gas de Efecto Invernadero |

| Gluten | Es una familia de proteínas que se encuentran en los granos, incluidos el trigo, el centeno, la espelta y la cebada. |

| Cáñamo | Es una clase botánica de cultivares de Cannabis sativa cultivados específicamente para uso industrial o medicinal. |

| Hidrolizado | Es una forma de proteína fabricada exponiendo la proteína a enzimas que pueden romper parcialmente los enlaces entre los aminoácidos de la proteína y descomponer proteínas grandes y complicadas en piezas más pequeñas. Su procesamiento facilita y acelera su digestión. |

| Hipoalergénico | Se refiere a una sustancia que causa menos reacciones alérgicas. |

| Aislado | Es la forma más pura y procesada de proteína que ha sido sometida a separación para obtener una fracción proteica pura. Típicamente contiene ≥ 90% de proteína en peso. |

| Queratina | Es una proteína que ayuda a formar el cabello, las uñas y la capa exterior de la piel. |

| Lactoalbúmina | Es la albúmina contenida en la leche y obtenida del suero de leche. |

| Lactoferrina | Es una glicoproteína de unión al hierro que está presente en la leche de la mayoría de los mamíferos. |

| Lupino | Son las semillas de leguminosas amarillas del género Lupinus. |

| Millennial | También conocido como Generación Y o Gen Y, se refiere a las personas nacidas entre 1981 y 1996. |

| Monogástrico | Se refiere a un animal con un estómago de un solo compartimento. Ejemplos de monogástricos incluyen humanos, aves de corral, cerdos, caballos, conejos, perros y gatos. La mayoría de los monogástricos generalmente son incapaces de digerir muchos materiales alimenticios de celulosa, como los pastos. |

| MPC | Concentrado de proteína de leche |

| MPI | Aislado de proteína de leche |

| MSPI | Aislado de proteína de soya metilada |

| Micoproteína | La micoproteína es una forma de proteína unicelular, también conocida como proteína fúngica, derivada de hongos para el consumo humano. |

| Nutricosmética | Es una categoría de productos e ingredientes que actúan como suplementos nutricionales para el cuidado de la belleza natural de la piel, las uñas y el cabello. |

| Osteoporosis | Es una condición médica en la que los huesos se vuelven frágiles y quebradizos por la pérdida de tejido, típicamente como resultado de cambios hormonales o deficiencia de calcio o vitamina D. |

| PDCAAS | La puntuación de aminoácidos corregida por digestibilidad proteica (PDCAAS) es un método para evaluar la calidad de una proteína basado tanto en los requisitos de aminoácidos de los humanos como en su capacidad para digerirla. |

| Consumo per cápita de proteína animal | Es la cantidad promedio de proteína animal (como leche, suero de leche, gelatina, colágeno y proteínas de huevo) que está disponible para el consumo de cada persona en una población real. |

| Consumo per cápita de proteína vegetal | Es la cantidad promedio de proteína vegetal (como proteínas de soya, trigo, guisante, avena y cáñamo) que está disponible para el consumo de cada persona en una población real. |

| Quorn | Es una proteína microbiana fabricada utilizando micoproteína como ingrediente, en la que el cultivo de hongos se seca y se mezcla con albúmina de huevo o proteína de papa, que actúa como aglutinante, y luego se ajusta en textura y se prensa en diversas formas. |

| Listo para Cocinar (LPC) | Se refiere a productos alimentarios que incluyen todos los ingredientes, donde se requiere alguna preparación o cocción a través de un proceso que se indica en el envase. |

| Listo para Consumir (LPC) | Se refiere a un producto alimentario preparado o cocinado con anticipación, sin necesidad de cocción o preparación adicional antes de ser consumido. |

| LPB | Listo para Beber |

| LPS | Listo para Servir |

| Grasa saturada | Es un tipo de grasa en la que las cadenas de ácidos grasos tienen todos enlaces simples. Generalmente se considera poco saludable. |

| Salchicha | Es un producto cárnico elaborado con carne finamente picada y sazonada, que puede ser fresca, ahumada o en escabeche, y que generalmente se rellena en una tripa. |

| Seitán | Es un sustituto de carne a base de plantas elaborado con gluten de trigo. |

| Cápsula blanda | Es una cápsula a base de gelatina con relleno líquido. |

| SPC | Concentrado de proteína de soya |

| SPI | Aislado de proteína de soya |

| Espirulina | Es una biomasa de cianobacterias que puede ser consumida por humanos y animales. |

| Estabilizador | Es un ingrediente añadido a los productos alimentarios para ayudar a mantener o mejorar su textura original y sus características físicas y químicas. |

| Suplementación | Es el consumo o provisión de fuentes concentradas de nutrientes u otras sustancias que tienen como objetivo complementar los nutrientes en la dieta y están destinadas a corregir deficiencias nutricionales. |

| Texturizante | Es un tipo específico de ingrediente alimentario que se utiliza para controlar y alterar la sensación en boca y la textura de los productos alimentarios y de bebidas. |

| Espesante | Es un ingrediente que se utiliza para aumentar la viscosidad de un líquido o masa y hacerlo más espeso, sin cambiar sustancialmente sus otras propiedades. |

| Grasa trans | También llamada ácidos grasos trans insaturados o ácidos grasos trans, es un tipo de grasa insaturada que se produce naturalmente en pequeñas cantidades en la carne. |

| TSP | Proteína de soya texturizada |

| TVP | Proteína vegetal texturizada |

| WPC | Concentrado de proteína de suero de leche |

| WPI | Aislado de proteína de suero de leche |

Metodología de Investigación

Mordor Intelligence sigue una metodología de cuatro pasos en todos nuestros informes.

- Paso 1: Identificar las Variables Clave: Las variables clave cuantificables (de la industria y externas) relacionadas con el segmento de producto específico y el país se seleccionan de un grupo de variables y factores relevantes basados en investigación documental y revisión bibliográfica, junto con aportes de expertos primarios. Estas variables se confirman posteriormente mediante modelos de regresión (cuando corresponde).

- Paso 2: Construir un Modelo de Mercado: Con el fin de desarrollar una metodología de pronóstico sólida, las variables y factores identificados en el Paso 1 se prueban contra los números históricos de mercado disponibles. A través de un proceso iterativo, se establecen las variables necesarias para el pronóstico del mercado y el modelo se construye sobre la base de estas variables.

- Paso 3: Validar y Finalizar: En este importante paso, todos los números de mercado, variables y criterios de los analistas se validan a través de una extensa red de expertos en investigación primaria del mercado estudiado. Los encuestados se seleccionan en todos los niveles y funciones para generar una imagen holística del mercado estudiado.

- Paso 4: Resultados de la Investigación: Informes Sindicados, Asignaciones de Consultoría Personalizada, Bases de Datos y Plataformas de Suscripción