Tamaño y Participación del Mercado de Proteína de Canadá

Visión General del Mercado

| Período de Estudio | 2021 - 2031 |

|---|---|

| Período de Datos Pronosticados | 2026 - 2031 |

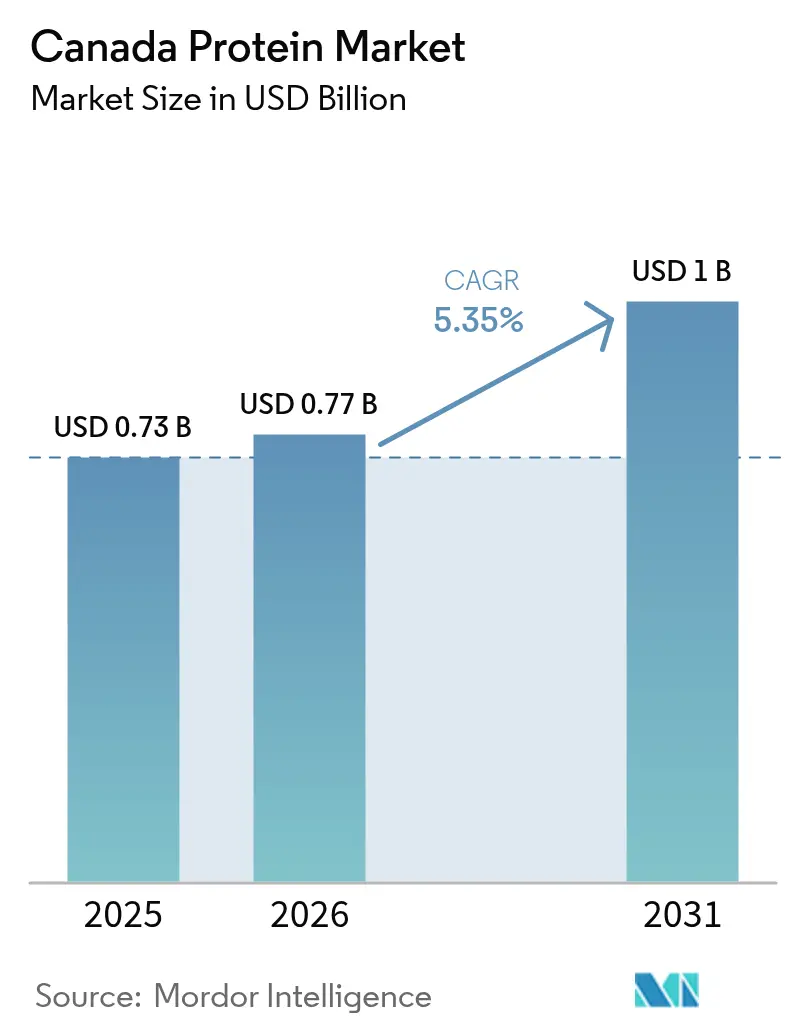

| Tamaño del mercado en el año base (2025) | 0.73 Mil millones de dólares |

| Tamaño del Mercado (2026) | 0.77 Mil millones de dólares |

| Tamaño del Mercado (2031) | 1 Mil millones de dólares |

| Tasa de crecimiento (2026 - 2031) | 5.35% CAGR |

| Concentración del Mercado | Medio |

Jugadores principales *Nota aclaratoria: los principales jugadores no se ordenaron de un modo en especial Imagen © Mordor Intelligence. El uso requiere atribución según CC BY 4.0. | |

Análisis del Mercado de Proteína de Canadá por Mordor Intelligence

Se proyecta que el tamaño del mercado de proteína de Canadá sea de USD 0,73 mil millones en 2025, USD 0,77 mil millones en 2026, y alcance USD 1,00 mil millones para 2031, creciendo a una CAGR del 5,35% de 2026 a 2031. El financiamiento federal de superclústeres, los grandes centros de procesamiento en las Praderas y un cambio nacional hacia hábitos alimenticios flexitarianos están orientando la demanda hacia proteínas vegetales y microbianas. Los proveedores multinacionales de ingredientes están ampliando sus instalaciones en las Praderas para aprovechar la energía hidroeléctrica de bajo carbono y el acceso directo por ferrocarril a las terminales de exportación, mientras que los innovadores regionales licencian tecnologías de extracción propietarias para competir en funcionalidad más que en volumen. La dinámica de los bienes comercializados es igualmente importante: los procesadores cubren las fluctuaciones de divisas y precios de cultivos mediante contratos a largo plazo con productores y carteras de proteínas diversificadas, amortiguando así las ganancias frente a la volatilidad inducida por sequías en los precios de guisantes y lentejas. La claridad regulatoria para las proteínas novedosas y el creciente escrutinio de las emisiones de Alcance 3 entre los compradores globales refuerzan aún más la ventaja competitiva de Canadá en ingredientes proteicos de bajo carbono y trazables.

Conclusiones Clave del Informe

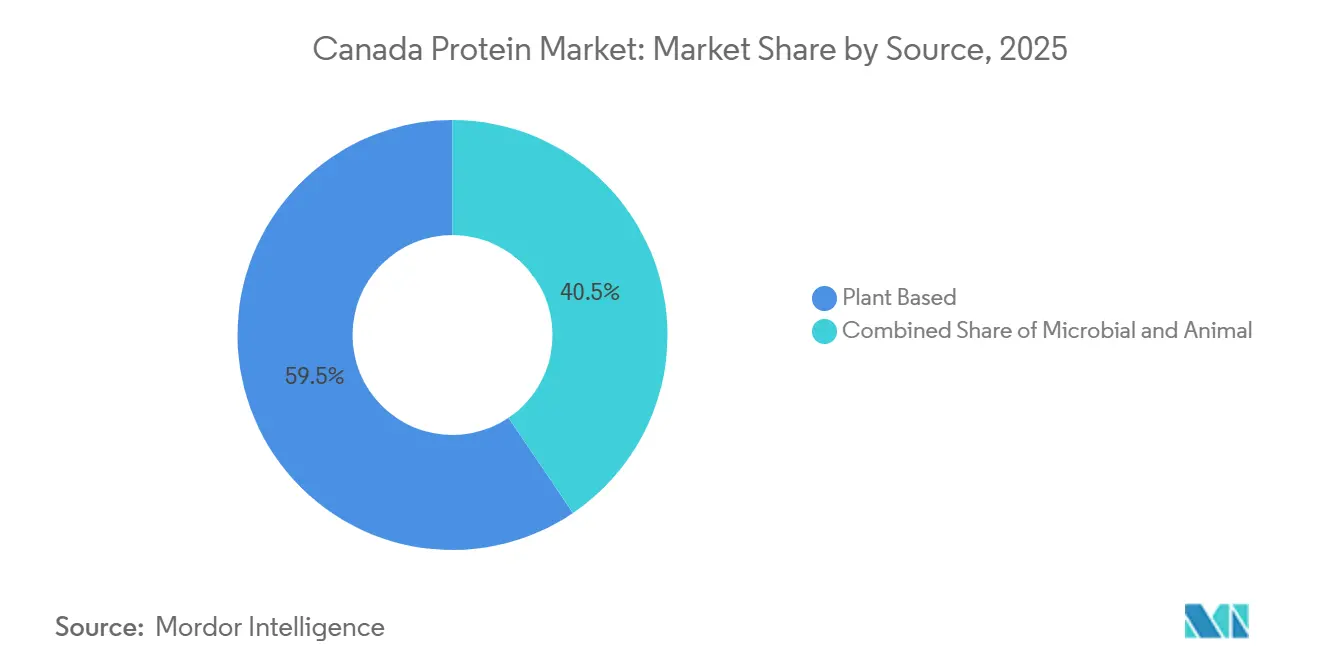

- Por fuente, las proteínas vegetales lideraron con el 59,48% de la participación del mercado de proteína de Canadá en 2025, mientras que las proteínas microbianas están proyectadas para registrar el crecimiento más rápido con una CAGR del 6,99% hasta 2031.

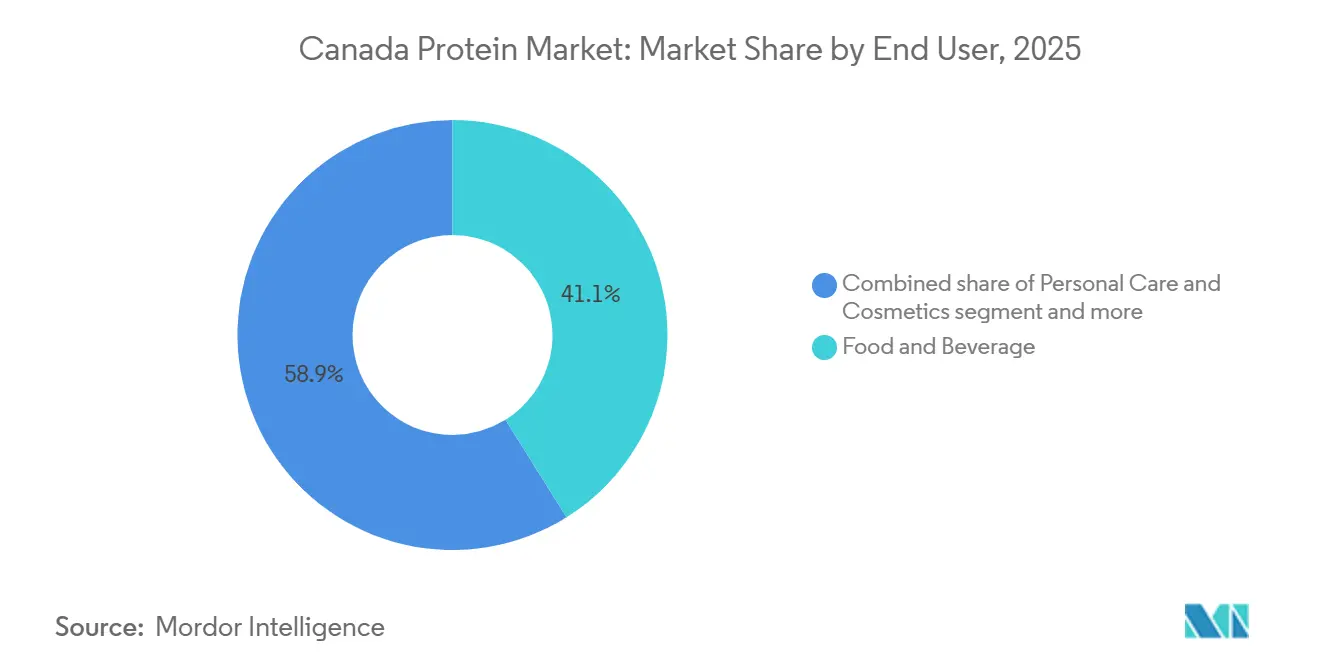

- Por usuario final, los alimentos y bebidas representaron el 41,05% del tamaño del mercado de proteína de Canadá en 2025, mientras que el alimento para animales está proyectado para registrar una CAGR del 5,75% durante 2026-2031.

Nota: Las cifras de tamaño del mercado y previsión de este informe se generan utilizando el marco de estimación propietario de Mordor Intelligence, actualizado con los últimos datos e información disponibles a partir de 2026.

Tendencias e Información del Mercado de Proteína de Canadá

Análisis del Impacto de los Impulsores*

| Impulsor | Impacto (~) % en el Pronóstico de CAGR | Relevancia Geográfica | Horizonte Temporal del Impacto |

|---|---|---|---|

| Demanda creciente de alimentos de salud y bienestar con alto contenido proteico | +1.2% | Nacional, con concentración en centros urbanos (Toronto, Vancouver, Montreal) | Mediano plazo (2-4 años) |

| Crecimiento de las dietas basadas en plantas y flexitarianas | +1.5% | Nacional, más fuerte en Columbia Británica y Ontario | Mediano plazo (2-4 años) |

| Financiamiento federal de superclústeres (Protein Industries Canada) | +0.9% | Provincias de las Praderas (Manitoba, Saskatchewan, Alberta) | Largo plazo (≥ 4 años) |

| Megainstalaciones de las Praderas que reducen los costos de producción | +1.0% | Manitoba y Saskatchewan, los beneficios de exportación son nacionales | Largo plazo (≥ 4 años) |

| Avances en el procesamiento de proteínas de canola y haba | +0.6% | Producción nacional, acceso al mercado global | Largo plazo (≥ 4 años) |

| Ventaja energética provincial de bajo carbono (p. ej., hidroeléctrica de Manitoba) | +0.4% | Manitoba, ventaja competitiva para instalaciones orientadas a la exportación | Largo plazo (≥ 4 años) |

| Fuente: Mordor Intelligence | |||

Demanda creciente de alimentos de salud y bienestar con alto contenido proteico

Los canadienses conscientes de su salud están incorporando proteínas en partes cotidianas de su dieta, desde cereales de desayuno fortificados con aislado de guisante hasta bebidas listas para consumir que aportan 20 gramos por porción, un cambio que los fabricantes de alimentos están monetizando mediante precios premium. La encuesta de la Universidad de Dalhousie de 2025 reveló que el 51% de los canadienses están dispuestos a reducir el consumo de carne, con la calidad de la proteína y la saciedad impulsando las decisiones de compra por encima del recuento calórico[1]Fuente: Universidad de Dalhousie, "Encuesta de Tendencias de Consumo Alimentario Canadiense 2025," dal.ca. Este cambio de comportamiento es más pronunciado entre los consumidores millennials y de la Generación Z, quienes ven la proteína como un ingrediente funcional más que como un macronutriente, lo que lleva a las marcas a reformular aperitivos, condimentos y alternativas lácteas con declaraciones de 8-12 gramos de proteína. Los marcos regulatorios bajo las Regulaciones de Alimentos y Medicamentos de Health Canada permiten declaraciones de contenido proteico cuando los productos cumplen umbrales mínimos, lo que permite a los fabricantes diferenciar los mensajes en el envase y obtener precios premium en estantes en categorías competitivas. La convergencia de la demografía envejecida, los adultos mayores que buscan nutrición para preservar la masa muscular, y las poblaciones atléticas que persiguen mejoras en el rendimiento, está expandiendo los mercados direccionables más allá de los suplementos deportivos tradicionales hacia la nutrición para personas mayores y los alimentos médicos, segmentos donde las proteínas de suero y caseína retienen ventajas funcionales a pesar de la competencia de las proteínas vegetales.

Crecimiento de las dietas basadas en plantas y flexitarianas

El flexitarianismo está superando al veganismo como la tendencia dietética dominante en Canadá, creando una demanda sostenida de productos híbridos que combinan proteínas animales y vegetales para optimizar el sabor, la textura y el costo. Aproximadamente el 15% de los canadienses siguen dietas basadas en plantas, pero la mayor oportunidad reside en el 40% que se identifica como flexitariano, comprando alternativas de carne de origen vegetal 2-3 veces al mes mientras mantiene hábitos omnívoros, según el estudio de la Universidad de Dalhousie. Este patrón de consumo dual está reformando el desarrollo de productos: procesadores lácteos como Saputo y Agropur están lanzando yogures combinados que mezclan suero con proteína de guisante para mantener la cremosidad mientras reducen las grasas saturadas, una estrategia de formulación que atrae a consumidores enfocados en la salud que no están dispuestos a sacrificar la experiencia sensorial. El segmento flexitariano es menos sensible al precio que los compradores de valor, pero más exigente en cuanto a la transparencia de los ingredientes, lo que impulsa a las marcas a obtener proteínas no transgénicas y certificadas como orgánicas y a divulgar el país de origen en las etiquetas, una tendencia que favorece las legumbres cultivadas en Canadá sobre la soja importada, según la Agencia Canadiense de Inspección de Alimentos.

Financiamiento federal de superclústeres (Protein Industries Canada)

El financiamiento federal de Canadá prioriza proyectos que integran el procesamiento de canola, el fraccionamiento de legumbres y la fermentación en operaciones de un solo sitio, reduciendo la logística entre instalaciones y permitiendo la valorización de coproductos. La harina de canola, por ejemplo, está siendo transformada en concentrados de proteína en lugar de venderse como alimento para animales de bajo margen. Las iniciativas cofinanciadas incluyen la planta de proteína de canola y guisante de Merit Functional Foods por CAD 310 millones (USD 232 millones) en Winnipeg, que alcanzó producción comercial en 2024 y tiene como objetivo 20.000 toneladas de producción anual para 2026. El modelo de superclúster también financia investigación precompetitiva en universidades y laboratorios gubernamentales, acelerando innovaciones de proceso, como el fraccionamiento en seco y la filtración por membrana, que reducen el consumo de agua y energía por kilogramo de proteína producida, un factor crítico a medida que el precio del carbono aumenta bajo la política climática federal. Al concentrar las inversiones en Manitoba y Saskatchewan, el programa está creando ecosistemas regionales donde los proveedores de ingredientes, los fabricantes de equipos y las organizaciones de investigación por contrato colaboran, reduciendo el tiempo de comercialización de proteínas novedosas de 5-7 años a 3-4 años.

Megainstalaciones de las Praderas que reducen los costos de producción

Las plantas de fraccionamiento a gran escala están logrando economías unitarias que hacen que las proteínas de guisante y canola canadienses sean competitivas en costos con los aislados de soja importados, un umbral que desbloquea la adopción masiva en categorías sensibles al precio como panadería y aperitivos. La instalación de Roquette en Portage la Prairie, que comenzó a duplicar su capacidad en 2024 para alcanzar 250.000 toneladas anuales, se beneficia de la automatización y el procesamiento continuo que reducen los costos laborales por tonelada en un 35% en comparación con las operaciones por lotes. La planta de Louis Dreyfus Company en Yorkton, puesta en marcha en 2025 con 75.000 toneladas de capacidad de proteína de guisante, integra la recuperación de almidón y la valorización de fibra, generando ingresos de tres flujos de productos en lugar de uno y mejorando la rentabilidad general de la planta. Estas megainstalaciones también negocian contratos a largo plazo con productores de legumbres, fijando los precios de las materias primas y reduciendo la exposición a la volatilidad del mercado spot, una estrategia que resultó esencial durante la sequía de 2024, cuando los precios del guisante se dispararon un 18% en Saskatchewan según Statistics Canada. La proximidad a las tierras de cultivo de las Praderas minimiza el flete entrante, mientras que los operadores orientados a la exportación envían aislados de proteína a granel en buques cisterna a clientes de Estados Unidos y Asia, evitando la dilución de márgenes de la distribución minorista en pequeños envases. La ventaja de costos es más pronunciada en Manitoba, donde la energía hidroeléctrica ofrece tarifas industriales un 25% por debajo de la red dependiente del gas natural de Alberta, un diferencial que se acumula a lo largo de la vida útil de las plantas de varias décadas.

Análisis del Impacto de las Restricciones*

| Restricción | Impacto (~) % en el Pronóstico de CAGR | Relevancia Geográfica | Horizonte Temporal del Impacto |

|---|---|---|---|

| Complejidad del etiquetado de la CFIA y las aprobaciones de alimentos novedosos | -0.5% | Nacional, afecta a todas las fuentes de proteínas novedosas | Mediano plazo (2-4 años) |

| Volatilidad del precio de los cultivos de legumbres impulsada por el clima | -0.7% | Provincias de las Praderas (Saskatchewan, Alberta, Manitoba) | Corto plazo (≤ 2 años) |

| Cuellos de botella en la capacidad ferroviaria desde las Praderas hasta los puertos | -0.4% | Manitoba, Saskatchewan, Alberta (instalaciones dependientes de la exportación) | Corto plazo (≤ 2 años) |

| Barreras culturales de sabor para proteínas de insectos/microbianas | -0.3% | Nacional, mayor resistencia en demografías rurales y de mayor edad | Largo plazo (≥ 4 años) |

| Fuente: Mordor Intelligence | |||

Complejidad del etiquetado de la CFIA y las aprobaciones de alimentos novedosos

El proceso de aprobación de alimentos novedosos de la Agencia Canadiense de Inspección de Alimentos requiere expedientes de seguridad exhaustivos y puede extenderse de 18 a 24 meses desde la presentación hasta la autorización, retrasando la entrada al mercado de proteínas microbianas y de insectos que carecen de un historial de uso seguro en Canadá. La CFIA clasifica las proteínas derivadas de la fermentación de precisión, el cultivo de algas y las larvas de insectos como alimentos novedosos bajo la División 28 del Reglamento de Alimentos y Medicamentos, lo que desencadena una notificación previa a la comercialización y una evaluación toxicológica, una vía que las proteínas vegetales convencionales como el guisante y la soja eluden porque se derivan de alimentos con registros de seguridad establecidos[2]Fuente: Agencia Canadiense de Inspección de Alimentos, "Alimentos Novedosos," inspection.canada.ca. Esta asimetría regulatoria perjudica a los innovadores: Enterra Corporation tardó 3 años en obtener la aprobación de la CFIA para la proteína de larvas de mosca soldado negro en alimento para acuicultura, un plazo que consumió capital de trabajo y permitió a los competidores estadounidenses capturar la ventaja de ser los primeros en los mercados norteamericanos. Los requisitos de etiquetado añaden complejidad; la CFIA exige que las proteínas novedosas sean identificadas por su organismo fuente en los paneles de ingredientes, lo que puede disuadir a los consumidores no familiarizados con términos como "micoproteína de Aspergillus oryzae" o proteína de Spirulina platensis,

obligando a las marcas a invertir en educación del consumidor y reformulación para enmascarar los ingredientes novedosos dentro de mezclas. El marco de alimentos suplementados bajo la División 29 restringe aún más los niveles de fortificación proteica en ciertas categorías, limitando la cantidad de proteína añadida en bebidas y aperitivos para evitar declaraciones nutricionales engañosas, una norma que limita la flexibilidad de formulación para las marcas que buscan diferenciarse con un posicionamiento de alto contenido proteico.

Volatilidad del precio de los cultivos de legumbres impulsada por el clima

Saskatchewan y Alberta experimentaron una disminución del 15% en los rendimientos de guisante durante la temporada de cultivo de 2024 debido a la sequía y el estrés por calor, lo que desencadenó picos de precios spot que comprimieron los márgenes de los procesadores y obligó a algunas plantas a obtener legumbres de mayor costo de Montana y Dakota del Norte. Los cultivos de legumbres, guisantes, lentejas y garbanzos son sensibles al estrés hídrico durante la floración, y los modelos climáticos proyectan una mayor frecuencia de sequías plurianuales en las Praderas canadienses, introduciendo una volatilidad estructural en los costos de las materias primas. Los procesadores con contratos de precio fijo con los fabricantes de alimentos no pueden trasladar la inflación de los costos de insumos, erosionando la rentabilidad; Roquette y Louis Dreyfus mitigan este riesgo contratando directamente con cooperativas de productores para entregas plurianuales a precios basados en fórmulas, pero los operadores más pequeños carecen de la solidez financiera para ofrecer tales condiciones. La sequía de 2024 también redujo el contenido proteico de los guisantes cosechados de los niveles típicos del 21-23% al 19-20%, lo que requirió que los procesadores mezclaran múltiples lotes para cumplir con las especificaciones de los clientes y aumentó los costos de manipulación, según Agriculture and Agri-Food Canada. Los programas de seguro de cultivos administrados por los gobiernos provinciales brindan protección parcial de ingresos a los productores, pero no estabilizan los precios para los procesadores aguas abajo, creando una discrepancia entre los mecanismos de distribución de riesgos y la exposición de la cadena de valor. Las estrategias de adaptación a largo plazo incluyen el desarrollo de variedades de guisante y haba tolerantes a la sequía a través de asociaciones público-privadas financiadas por Protein Industries Canada, aunque el despliegue comercial de tales cultivares no ocurrirá hasta 2027-2028.

*Nuestras previsiones consideran los impactos de impulsores y restricciones como direccionales, no aditivos. Las previsiones de impacto reflejan el crecimiento base, los efectos de mezcla y las interacciones entre variables.

Análisis de Segmentos

Por Fuente: Las Proteínas Vegetales Anclan el Mercado, el Segmento Microbiano se Acelera

Las proteínas vegetales tuvieron una participación de mercado del 59,48% en 2025, con la proteína de guisante dominando debido a la capacidad de procesamiento en las Praderas que ahora supera las 200.000 toneladas anuales en las instalaciones de Roquette, Louis Dreyfus y Merit Functional Foods. La plataforma de extracción enzimática de Burcon NutraScience está permitiendo que la proteína de canola desafíe al guisante en las formulaciones de nutrición deportiva, donde el perfil de sabor neutro e hipoalergénico justifica precios premium a pesar de una menor penetración de mercado. La proteína de soja mantiene una posición en panadería y alternativas cárnicas, aunque la producción canadiense es limitada y la mayor parte del suministro se importa de procesadores del Medio Oeste de Estados Unidos, creando una vulnerabilidad estratégica ya que las fricciones comerciales interrumpen periódicamente los flujos transfronterizos. La proteína de trigo, principalmente gluten extraído de la molienda de harina, sirve para aplicaciones de nicho en productos horneados y alimentos para mascotas, pero enfrenta una demanda estancada a medida que las tendencias sin gluten erosionan su mercado direccionable. La proteína de cáñamo está emergiendo en canales orgánicos y naturales, respaldada por los cambios regulatorios de Health Canada en 2018 que legalizaron los ingredientes alimentarios de cáñamo, aunque la producción sigue siendo a pequeña escala y los precios son 2-3 veces más altos que los del guisante, lo que limita la adopción masiva. La proteína de arroz, obtenida en gran medida de proveedores asiáticos, ocupa una participación menor en fórmulas infantiles hipoalergénicas y nutrición médica, donde su baja alergenicidad compensa los mayores costos de importación.

Las proteínas microbianas, algas y micoproteína, se están expandiendo a una CAGR del 6,99% hasta 2031, la tasa más rápida entre los segmentos de fuente, impulsadas por plataformas de fermentación de precisión que producen proteínas completas con perfiles de aminoácidos superiores a la mayoría de las fuentes vegetales. La proteína de algas, particularmente de Spirulina y Chlorella, está ganando terreno en suplementos deportivos y bebidas funcionales, donde su alto contenido de leucina apoya la síntesis de proteínas musculares de manera más efectiva que el guisante o el arroz. Las empresas emergentes canadienses están pilotando sistemas de fotobiorreactores de circuito cerrado que eliminan la variabilidad estacional y permiten la producción durante todo el año, aunque la intensidad de capital sigue siendo una barrera para la escala. La micoproteína, derivada de la fermentación fúngica, está siendo comercializada por actores internacionales con producción canadiense limitada hasta la fecha, aunque la aprobación de la CFIA en 2024 de la micoproteína de Fusarium venenatum como ingrediente alimentario novedoso abre la puerta a la fabricación doméstica. Las proteínas animales, suero, caseína, huevo, colágeno, gelatina, representan colectivamente una participación significativa, con cooperativas lácteas como Agropur y Saputo invirtiendo en capacidad de concentrado y aislado de proteína de suero para servir a los mercados de nutrición deportiva y fórmula infantil; la expansión de la planta de Lethbridge de Agropur por CAD 200 millones (USD 150 millones), completada en 2025, añadió 15.000 toneladas de capacidad de aislado de proteína de suero. La proteína de insectos, liderada por las larvas de mosca soldado negro de Enterra Corporation, está aprobada para alimento de acuicultura y raciones avícolas, con aplicaciones limitadas en alimentos humanos debido a barreras de aceptación cultural, aunque las vías regulatorias son más claras en alimento que en alimentos para consumo humano.

Por Usuario Final: El Alimento para Animales Supera el Crecimiento de Alimentos y Bebidas

Las aplicaciones de alimentos y bebidas representaron el 41,05% de la participación de mercado en 2025, sin embargo, se proyecta que el alimento para animales crezca a una CAGR del 5,75% hasta 2031, superando a todos los demás segmentos de usuarios finales a medida que los productores de ganado y acuicultura buscan fuentes de proteína sostenibles y rentables. Dentro de alimentos y bebidas, los productos lácteos y las alternativas lácteas son el subsegmento más grande, impulsado por formulaciones de leche, yogur y queso de origen vegetal que combinan proteínas de guisante, avena y almendra para optimizar el sabor y la textura; Saputo y Agropur están lanzando productos lácteos híbridos que combinan suero con proteína de guisante para mantener la cremosidad mientras reducen las grasas saturadas. Los productos de carne, aves, mariscos y alternativas cárnicas representan la segunda aplicación más grande, con marcas de hamburguesas y salchichas de origen vegetal que obtienen proteínas de guisante y haba de procesadores canadienses para cumplir con las declaraciones de etiqueta limpia y no transgénico. Los operadores de acuicultura están sustituyendo el 30-40% de la harina de pescado con proteína de larvas de insectos y concentrados de legumbres, un cambio impulsado por certificaciones de sostenibilidad como el Consejo de Administración de la Acuicultura, que penaliza la dependencia de peces forrajeros capturados en la naturaleza. Las aplicaciones de panadería, pan, muffins y barras de proteína utilizan gluten de trigo y proteína de guisante para aumentar el contenido proteico y mejorar la resistencia de la masa, aunque persisten desafíos de formulación en torno a la retención de humedad y la vida útil. Las bebidas, incluidos los batidos listos para beber y las aguas proteicas, demandan aislados altamente solubles con sabor neutro, una especificación que favorece las proteínas de canola y arroz sobre el guisante. Los cereales de desayuno, aperitivos y productos alimenticios RTE/RTC están incorporando proteínas para captar a los consumidores conscientes de su salud, con marcas que reformulan para lograr declaraciones de 8-12 gramos de proteína que activan llamadas en la parte frontal del envase.

Los suplementos, que abarcan nutrición deportiva, nutrición para personas mayores y fórmula infantil, son un segmento de alto margen donde las proteínas de suero y caseína retienen ventajas funcionales, aunque las alternativas de origen vegetal están ganando participación entre los consumidores veganos e intolerantes a la lactosa. Los productos de nutrición deportiva y de rendimiento favorecen el aislado de proteína de suero por su rápida digestión y alto contenido de leucina, aunque las mezclas de proteínas de guisante y arroz están capturando el 25-30% del segmento al ofrecer perfiles de aminoácidos comparables a precios más bajos. Los productos de nutrición para personas mayores y nutrición médica requieren proteínas con alta digestibilidad y baja alergenicidad, impulsando la demanda de proteínas de suero e arroz hidrolizadas que cumplen con los estándares de nutrición clínica. Los alimentos para bebés y la fórmula infantil representan un subsegmento estrictamente regulado donde las proteínas lácteas dominan debido a los perfiles de seguridad establecidos, aunque la aprobación de la CFIA de proteínas vegetales novedosas para uso infantil podría abrir oportunidades para formulaciones hipoalergénicas para 2027. Las aplicaciones de cuidado personal y cosméticos utilizan colágeno, gelatina y proteínas hidrolizadas para el acondicionamiento del cabello y la piel, un segmento de nicho con potencial de crecimiento limitado pero demanda estable de marcas de belleza premium. El alimento para animales, el usuario final de más rápido crecimiento, se beneficia de la aprobación de la CFIA en 2024 de la proteína de insectos para raciones de aves de corral y porcinos, expandiendo el mercado direccionable más allá de la acuicultura; Enterra Corporation está escalando la producción para satisfacer la demanda de integradores que buscan reducir la dependencia de las importaciones de harina de soja.

Análisis Geográfico

El mercado de proteína de Canadá está geográficamente concentrado en las provincias de las Praderas, Manitoba, Saskatchewan y Alberta, que en conjunto albergan capacidad de procesamiento debido a la proximidad a las tierras de cultivo de legumbres y el acceso a energía de bajo costo, aunque Ontario y Quebec siguen siendo centros de demanda críticos donde ocurre el 60% del consumo de usuarios finales. La red eléctrica renovable al 97% de Manitoba ha atraído CAD 1,4 mil millones (USD 1,05 mil millones) en inversiones de procesamiento de proteínas desde 2020, incluido el complejo de proteína de guisante de Roquette en Portage la Prairie y la planta de canola y guisante de Merit Functional Foods en Winnipeg, ambas de las cuales comercializan credenciales de bajo carbono a compradores europeos y norteamericanos que enfrentan objetivos de emisiones de Alcance 3. Saskatchewan lidera en la producción de cultivos de legumbres, suministrando el 50% de la cosecha de guisantes y lentejas de Canadá, y alberga la planta de Louis Dreyfus Company por CAD 500 millones (USD 375 millones) en Yorkton, que comenzó la producción comercial en 2025 y tiene como objetivo los mercados de exportación asiáticos donde los pulsos canadienses obtienen primas por cumplimiento de no transgénico y residuos de pesticidas. El sector proteico de Alberta es más pequeño pero se está diversificando, con la propuesta de instalación de proteína de guisante de Phytokana por CAD 225 millones (USD 169 millones) en Strathmore recibiendo una subvención de CAD 10 millones de Emissions Reduction Alberta, lo que señala el apoyo provincial a la agricultura de valor agregado. Columbia Británica y Ontario son importadores netos de ingredientes proteicos, con demanda impulsada por fabricantes de alimentos y bebidas en el área metropolitana de Vancouver y el Área Metropolitana de Toronto; estas provincias también albergan instituciones de investigación como la Universidad de Columbia Británica y la Universidad de Guelph que están avanzando en tecnologías de extracción y funcionalización de proteínas a través de asociaciones con Protein Industries Canada.

La dinámica de exportación está reformando las trayectorias de crecimiento regional: los aislados de proteína de guisante canadienses están desplazando a los proveedores europeos y chinos en los mercados de nutrición deportiva y carne de origen vegetal de Estados Unidos, donde los compradores priorizan la trazabilidad y el abastecimiento no transgénico. El Puerto de Vancouver maneja el 70% de las exportaciones de ingredientes proteicos de Canadá, con envíos a granel a Japón, Corea del Sur y Taiwán, mientras que Thunder Bay sirve como puerta de entrada para las cargas con destino a Europa a través de las rutas de los Grandes Lagos y la Vía Marítima del San Lorenzo[3]Fuente: Puerto de Vancouver, "Estadísticas de Carga," portvancouver.com. Las restricciones de capacidad ferroviaria durante las temporadas de cosecha retrasan periódicamente los envíos de proteínas, lo que obliga a los procesadores a construir inventarios más grandes y aumenta los requisitos de capital de trabajo; CN Rail y CP Kansas City están invirtiendo CAD 500 millones anuales en mejoras del corredor de las Praderas, aunque los cuellos de botella persisten en cruces clave cerca de Winnipeg y Saskatoon. El sector de proteínas lácteas de Quebec, anclado por Agropur y Saputo, está pivotando hacia aislados de proteína de suero e hidrolizados de alto valor para fórmula infantil y nutrición clínica, mercados donde las barreras regulatorias de entrada y las especificaciones técnicas limitan la competencia de las proteínas vegetales. El Canadá Atlántico sigue siendo un actor menor en la producción de proteínas, aunque las operaciones de acuicultura de Cooke Inc. en Nuevo Brunswick están impulsando la demanda de proteínas de insectos y legumbres como sustitutos de la harina de pescado, creando oportunidades localizadas para los proveedores de ingredientes para alimento. El programa AgriInnovate del gobierno federal de 2024 asignó CAD 75 millones para apoyar las expansiones del procesamiento de proteínas en regiones desatendidas, con el objetivo de Ontario y Quebec para reducir la dependencia de las cadenas de suministro de las Praderas y mejorar la seguridad alimentaria según Agriculture and Agri-Food Canada.

La divergencia de políticas provinciales está creando asimetrías competitivas: Manitoba ofrece créditos fiscales sobre el capital para inversiones en procesamiento de proteínas, Saskatchewan proporciona períodos de exención de regalías en arrendamientos de tierras de la Corona para productores de legumbres, y el fondo de Innovación Tecnológica y Reducción de Emisiones de Alberta cofinancia equipos de procesamiento de bajo carbono. Estos incentivos, combinados con el financiamiento federal de superclústeres, están concentrando las inversiones en las Praderas y ampliando la brecha con las provincias centrales y orientales, donde los mayores costos de energía y la disponibilidad limitada de materias primas restringen la competitividad. El sector de procesamiento de alimentos de Ontario está presionando por un apoyo comparable, argumentando que la proximidad al 40% de la población de Canadá justifica la producción doméstica de proteínas para reducir las emisiones de transporte y mejorar la resiliencia de la cadena de suministro, un debate que dará forma a la política agrícola federal hasta 2027. La concentración geográfica de la capacidad de procesamiento en Manitoba y Saskatchewan crea riesgos de punto único de falla: una huelga ferroviaria prolongada o una sequía severa podría interrumpir el suministro nacional, destacando el argumento estratégico a favor de una capacidad distribuida en múltiples provincias.

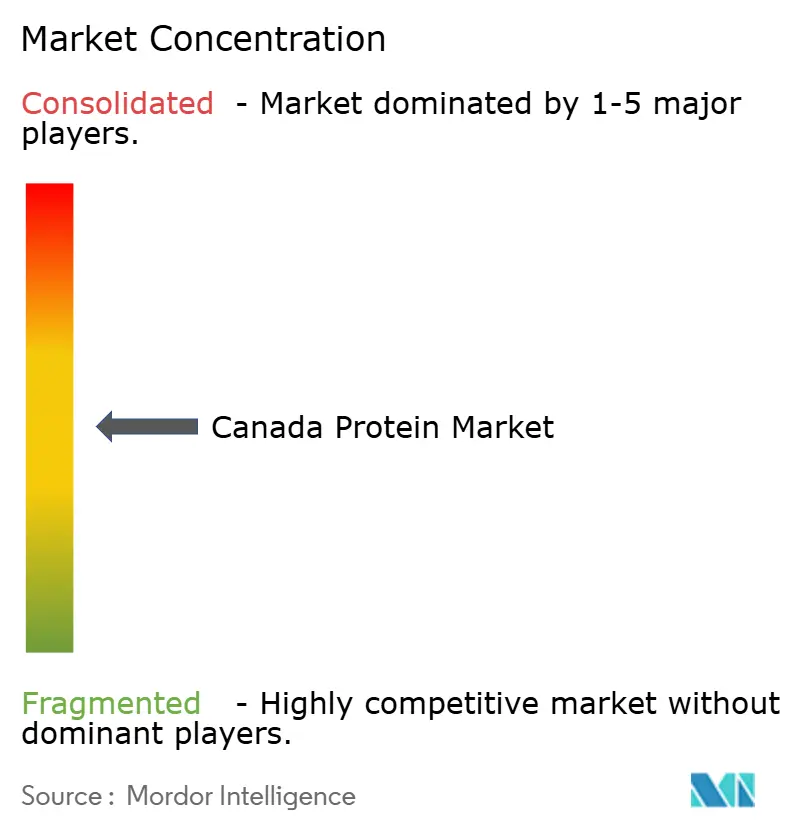

Panorama Competitivo

El mercado de proteína de Canadá exhibe una fragmentación moderada, con los cinco principales actores, Agropur Dairy Cooperative, Archer Daniels Midland, Saputo, Roquette Frères y Lactalis, representando colectivamente la mayor parte de la participación de mercado, dejando un espacio sustancial para que los especialistas regionales y los disruptores impulsados por la tecnología capturen segmentos de nicho a través de plataformas de extracción propietarias y estrategias de integración vertical. Los proveedores multinacionales de ingredientes están desplegando megainstalaciones de capital intensivo para lograr ventajas de costo unitario, mientras que los innovadores de origen canadiense como Burcon NutraScience y AGT Food & Ingredients están licenciando tecnologías de fraccionamiento novedosas a fabricantes por contrato, monetizando efectivamente la propiedad intelectual sin asumir riesgos operativos. Las cooperativas lácteas están defendiendo sus franquicias de suero y caseína invirtiendo en capacidades de ultrafiltración e hidrólisis que producen aislados de alta pureza para los mercados de fórmula infantil y nutrición clínica, donde las proteínas vegetales enfrentan barreras regulatorias y funcionales. La expansión de Lethbridge de Agropur por CAD 200 millones (USD 150 millones), completada en 2025, ejemplifica esta estrategia defensiva.

Están surgiendo oportunidades de espacio en blanco en proteínas microbianas, donde las plataformas de fermentación de precisión pueden producir proteínas completas con perfiles de aminoácidos personalizados, aunque los requisitos de capital de CAD 100-200 millones por planta y los plazos de aprobación de la CFIA de varios años disuaden a todos menos a los participantes con mayor capitalización. La intensidad competitiva es más alta en la proteína de guisante de commodities, donde Roquette, Louis Dreyfus y Merit Functional Foods compiten en costo y huella de carbono, impulsando la compresión de márgenes que favorece la escala y la eficiencia operativa sobre la diferenciación. La adopción de tecnología se está convirtiendo en un factor decisivo: el despliegue de optimización de procesos impulsada por inteligencia artificial de Roquette en su planta de Portage la Prairie redujo el consumo de energía por kilogramo de proteína en un 12% en 2024, un logro que se traduce en CAD 3 millones en ahorros anuales y fortalece su posición frente a los proveedores asiáticos de menor costo.

Los disruptores emergentes incluyen a Enterra Corporation, que posee patentes en sistemas de cría de larvas de mosca soldado negro que convierten residuos alimentarios en proteína, creando una narrativa de economía circular que resuena con los compradores enfocados en la sostenibilidad; la expansión de capacidad de la empresa en 2025 a 10.000 toneladas anuales la posiciona como una alternativa creíble a la harina de soja en acuicultura y alimento avícola. Los competidores más pequeños como Avena Foods y Nutri-Pea están apuntando a los segmentos orgánicos y no transgénicos, donde las primas de certificación compensan los mayores costos de producción y la escala limitada, aunque las restricciones del tamaño del mercado limitan el potencial de ingresos por debajo de CAD 50 millones anuales. El cumplimiento regulatorio es una ventaja competitiva: las empresas que navegan eficientemente el proceso de aprobación de alimentos novedosos de la CFIA obtienen ventajas de ser los primeros en actuar de 18-24 meses, una dinámica que favorece a los actores bien capitalizados con equipos internos de asuntos regulatorios sobre las empresas emergentes con financiamiento insuficiente que dependen de consultores.

Líderes de la Industria de Proteína de Canadá

Agropur Dairy Cooperative

Archer Daniels Midland Company

Saputo Inc.

Roquette Frères

Lactalis Group

- *Nota aclaratoria: los principales jugadores no se ordenaron de un modo en especial

Desarrollos Recientes de la Industria

- Junio de 2025: Hiton Foods reforzó su presencia en el mercado con una inversión de USD 192 millones en una instalación de procesamiento de alimentos ubicada en Brantford. Se anticipa que esta expansión fortalecerá las capacidades de producción de la empresa y satisfará la creciente demanda de productos alimenticios procesados en la región.

- Abril de 2024: Wamame Foods se unió a AGT Food para crear alternativas cárnicas de alto contenido proteico en Canadá, apuntando a mercados globales y aprovechando nuevos ingredientes proteicos canadienses. Esta asociación tiene como objetivo satisfacer la creciente demanda de productos proteicos sostenibles y de origen vegetal en todo el mundo.

- Febrero de 2024: Louis Dreyfus Company presentó planes para una planta de aislado de proteína de guisante en Saskatchewan, prevista para su debut a finales de 2025, enfatizando la alta funcionalidad y la neutralidad del sabor. Se espera que la instalación mejore la cartera de productos de la empresa y atienda la creciente preferencia de los consumidores por soluciones proteicas de origen vegetal.

- Abril de 2023: Sunnydale Foods, una empresa canadiense, anunció un progreso significativo en sus esfuerzos de desarrollo de productos, particularmente en la creación de ingredientes de alto contenido proteico a base de legumbres. Presentaron con orgullo un concentrado de proteína de haba con un contenido proteico del 65% y están buscando activamente mejoras adicionales para alcanzar niveles de proteína de hasta el 80%.

Alcance del Informe del Mercado de Proteína de Canadá

La proteína es un macronutriente esencial que desempeña un papel crucial en el organismo, incluyendo la construcción y reparación de tejidos, la producción de hormonas y enzimas, y el apoyo a la función inmunológica. El mercado de proteína de Canadá está segmentado por fuente y usuario final. Según la fuente, el mercado está segmentado en animal, microbiano y vegetal. Según las fuentes animales, el mercado se segmenta adicionalmente en caseína y caseinatos, colágeno, proteína de huevo, gelatina, proteína de insectos, proteína de leche, proteína de suero y otras proteínas animales. Según las fuentes microbianas, el mercado se segmenta adicionalmente en proteína de algas y micoproteína. Según las fuentes vegetales, el mercado se segmenta adicionalmente en proteína de cáñamo, proteína de avena, proteína de guisante, proteína de papa, proteína de arroz, proteína de soja, proteína de trigo y otras proteínas vegetales. Según los usuarios finales, el mercado está segmentado en alimento para animales, cuidado personal y cosméticos, alimentos y bebidas, y suplementos. El segmento de usuario final de alimentos y bebidas se subsegmenta adicionalmente en panadería, bebidas, cereales de desayuno, condimentos/salsas, confitería, productos lácteos y alternativas lácteas, productos de carne/aves/mariscos y alternativas cárnicas, productos alimenticios RTE/RTC y aperitivos. El segmento de usuario final de suplementos se subsegmenta adicionalmente en alimentos para bebés y fórmula infantil, nutrición para personas mayores y nutrición médica, y nutrición deportiva/de rendimiento. Para cada segmento, el informe proporciona el tamaño del mercado en valor (USD) y volumen (toneladas).

| Animal | Caseína y Caseinatos |

| Colágeno | |

| Proteína de Huevo | |

| Gelatina | |

| Proteína de Insectos | |

| Proteína de Leche | |

| Proteína de Suero | |

| Otras Proteínas Animales | |

| Microbiano | Proteína de Algas |

| Micoproteína | |

| Vegetal | Proteína de Cáñamo |

| Proteína de Guisante | |

| Proteína de Arroz | |

| Proteína de Soja | |

| Proteína de Trigo | |

| Otras Proteínas Vegetales |

| Alimentos y Bebidas | Panadería |

| Bebidas | |

| Cereales de Desayuno | |

| Condimentos/Salsas | |

| Confitería | |

| Productos Lácteos y Alternativas Lácteas | |

| Productos de Carne/Aves/Mariscos y Alternativas Cárnicas | |

| Productos Alimenticios RTE/RTC | |

| Aperitivos | |

| Otras Aplicaciones de Alimentos y Bebidas | |

| Cuidado Personal y Cosméticos | |

| Alimento para Animales | |

| Suplementos | Alimentos para Bebés y Fórmula Infantil |

| Nutrición para Personas Mayores y Nutrición Médica | |

| Nutrición Deportiva/de Rendimiento |

| Por Fuente | Animal | Caseína y Caseinatos |

| Colágeno | ||

| Proteína de Huevo | ||

| Gelatina | ||

| Proteína de Insectos | ||

| Proteína de Leche | ||

| Proteína de Suero | ||

| Otras Proteínas Animales | ||

| Microbiano | Proteína de Algas | |

| Micoproteína | ||

| Vegetal | Proteína de Cáñamo | |

| Proteína de Guisante | ||

| Proteína de Arroz | ||

| Proteína de Soja | ||

| Proteína de Trigo | ||

| Otras Proteínas Vegetales | ||

| Por Usuario Final | Alimentos y Bebidas | Panadería |

| Bebidas | ||

| Cereales de Desayuno | ||

| Condimentos/Salsas | ||

| Confitería | ||

| Productos Lácteos y Alternativas Lácteas | ||

| Productos de Carne/Aves/Mariscos y Alternativas Cárnicas | ||

| Productos Alimenticios RTE/RTC | ||

| Aperitivos | ||

| Otras Aplicaciones de Alimentos y Bebidas | ||

| Cuidado Personal y Cosméticos | ||

| Alimento para Animales | ||

| Suplementos | Alimentos para Bebés y Fórmula Infantil | |

| Nutrición para Personas Mayores y Nutrición Médica | ||

| Nutrición Deportiva/de Rendimiento | ||

Preguntas Clave Respondidas en el Informe

¿Qué tan grande es el mercado de proteína de Canadá hoy?

Está valorado en USD 0,77 mil millones en 2026 y se prevé que alcance USD 1,00 mil millones para 2031.

¿Qué fuente de proteína lidera la producción canadiense?

Las proteínas vegetales, principalmente guisante y canola, tuvieron una participación del 59,48% en 2025.

¿Cuál es el segmento de fuente de proteína de más rápido crecimiento?

Las proteínas microbianas, incluidas las algas y la micoproteína, están proyectadas para crecer a una CAGR del 6,99% hasta 2031.

¿Por qué las provincias de las Praderas son centrales para el procesamiento?

La proximidad a las tierras de cultivo de legumbres, la energía hidroeléctrica de bajo carbono y los enlaces ferroviarios crean ventajas de costo y sostenibilidad.

¿Qué segmento de usuario final crecerá más rápido?

El alimento para animales, impulsado por la acuicultura y la avicultura, está proyectado para expandirse a una CAGR del 5,75% durante 2026-2031.

¿Qué obstaculiza la comercialización de proteínas novedosas?

Los prolongados plazos de aprobación de la CFIA y los requisitos de etiquetado ralentizan la velocidad de comercialización de las proteínas microbianas y de insectos.

Última actualización de la página el: