UK Facilities Management Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

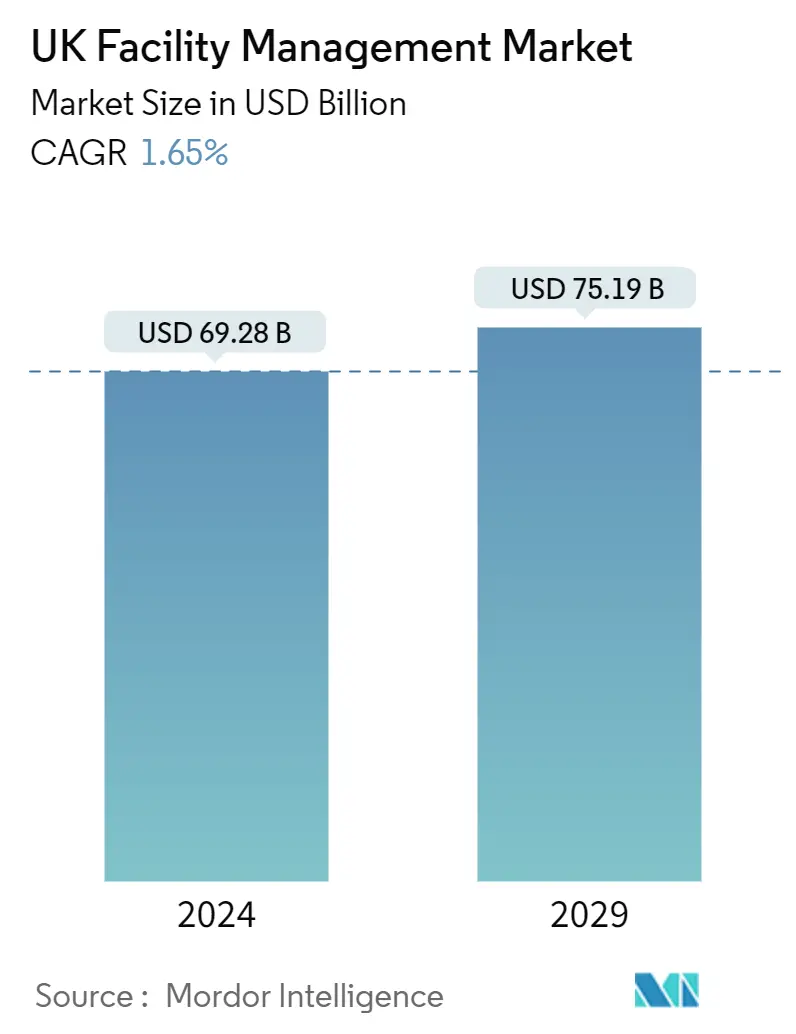

| Market Size (2024) | USD 69.28 Billion |

| Market Size (2029) | USD 75.19 Billion |

| CAGR (2024 - 2029) | 1.65 % |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

UK Facility Management Market Analysis

The UK Facility Management Market size is estimated at USD 69.28 billion in 2024, and is expected to reach USD 75.19 billion by 2029, growing at a CAGR of 1.65% during the forecast period (2024-2029).

- In terms of maturity and sophistication, the United Kingdom is one of Europe's most mature and sophisticated markets for facility management services. Given the increasing penetration of facility management services, providers are actively focusing on specialized services to obtain a foothold in the industry, which also saw many changes due to the region's macroeconomic and social changes.

- Various service providers operating in the country have emphasized growing their presence over the last decade to benefit from the increasing demand for facility management, especially with the current trend favoring outsourcing non-core functions. Given the dynamics across the country, the country is witnessing increased opportunities to leverage facility management and corporate real estate in innovative ways. According to BNP Paribas Real Estate, in 2023, the United Kingdom headed the ranking as the country with the most significant value of commercial real estate investments, amounting to about EUR 43.5 billion.

- The government is also focusing on closing the country's productivity gap for small to medium enterprises. For instance, in the recent past, the British government pledged EUR 56 million to enhance leadership and management skills. The funding also forms part of the Business Productivity Review announced by the Department for Business, Energy, and Industrial Strategy (BEIS) and Strategy, which sets out a 10-point action plan to help UK companies harness technology and boost productivity, thereby driving the market growth.

- Also, the facility management industry is expected to expand due to consumers' shifting preferences toward outsourced facility management services to cut costs. Businesses may save significantly by outsourcing building operations and maintenance while concentrating on their core competencies. Research by the Building Owners & Managers Association (BOMA) found that, on average, private commercial properties spend USD 2.15 on maintenance and repairs per square foot. Expenditures associated with maintaining the facility, such as labor costs for cleaning and upkeep, are not included in this amount. Businesses can save expenses and leverage the time saved by outsourcing to better use their workers in their core operations.

- Moreover, various market vendors are expanding their business operations through multiple contracts. For instance, in January 2023, Sodexo announced that it won a five-year contract to offer integrated facilities management (IFM) for a global bank's London offices. As part of the GBP 2 million-a-year contract, Sodexo would deliver services that connect with employees and make their working environment as engaging as possible. The services include catering, hospitality, cleaning, technical services, reception and guest services, and the management of the in-house gym.

- In September 2023, Apleona, a significant European integrated facilities management company based in Neu-Isenburg near Frankfurt (Main), acquired JCW Group Limited (JCW). The two companies will form a robust platform for integrated facilities management. Their complementary enterprise models, regional footprints, and client portfolios will secure strong organic growth with existing and recent Apleona clients in the United Kingdom and Europe.

- The growing competition in the market impacts the profit margins and growth of existing vendors. The competition level between suppliers is so high that FM services are transitioning to commoditized in the country. However, the country's recovering economic stability is anticipated to improve the market demand gradually and, subsequently, the profit margins of the market players. As suggested by the UK Facilities Management Market Survey by RICS, the profit margins, workloads, and employment opportunities are anticipated to grow over the next couple of years.

- Increasing inflation can affect the growth of the United Kingdom facility management market in several ways. If inflation leads to higher costs for inputs such as labor, materials, and equipment, facility management companies may face increased operating expenses, potentially squeezing profit margins unless they can pass these costs onto clients through higher prices. According to the Office for National Statistics (UK), the UK inflation rate was 3.2% in March 2024, compared with 3.4% in the previous month. Between September 2022 and March 2023, the United Kingdom experienced seven months of double-digit inflation, which peaked at 11.1% in October 2022.

UK Facility Management Market Trends

Single FM Service is Expected to Hold Significant Share

- Delegating task management to separate entities is common when working with a single facility management service provider. It also entails a different service provider for each service the organization needs, such as cleaning, reception, and vending machines. Using the services of specialized service providers includes several advantages.

- It allows customers to focus on their core business, while single-service providers provide adequate customer services and help operational efficiency. Experts handling task management will result in much higher efficiency and service quality. It will also free company employees to focus on the most critical business areas while saving resources for non-core activities.

- Outsourced FM is used significantly in various sectors, including the public sector, professional services, healthcare, technology, logistics, manufacturing, retail, and education. The areas that FM services look after vary widely, primarily depending on its type, the company size, and the sector in which it functions. Some organizations may only require a single service solution provider, further driving the demand for single FM in the country.

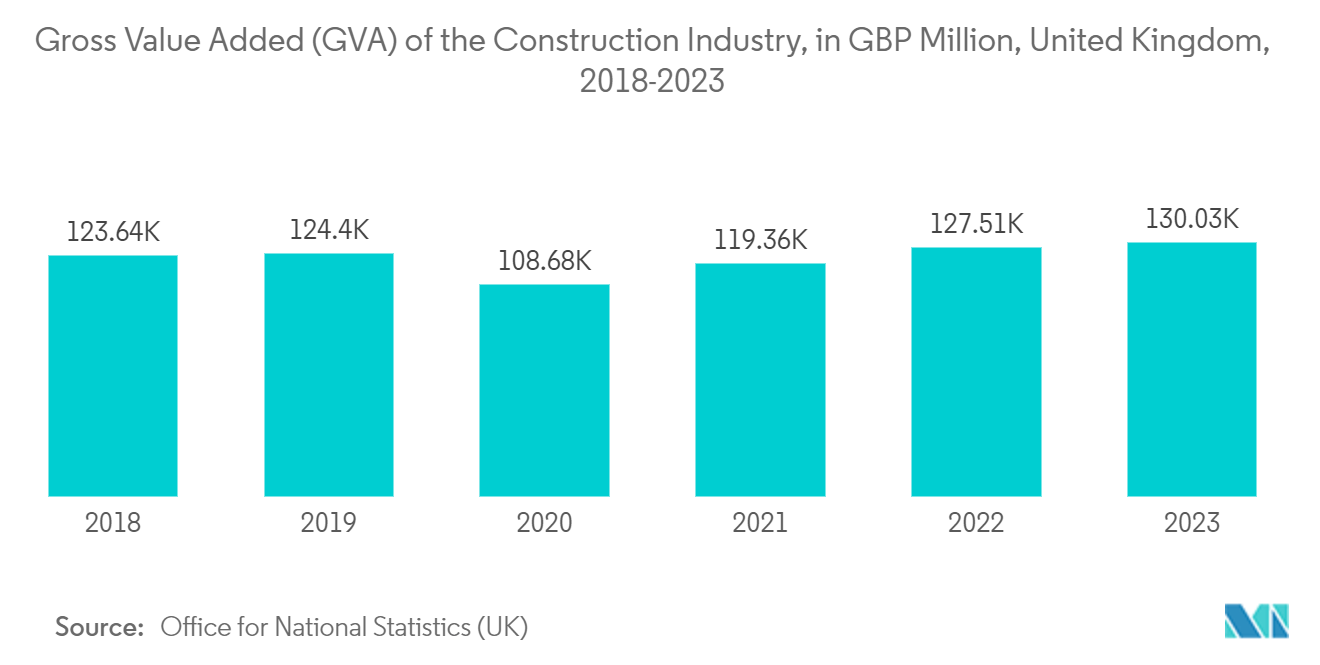

- Increasing the country's construction sector emphasis on sustainable building practices and lifecycle management has increased the demand for facility management services that can support the whole lifecycle of a building, from design and construction to procedure and maintenance. Single facility management systems provide a holistic approach to managing buildings throughout their lifecycle, ensuring sustainability and longevity. According to the Office for National Statistics (UK), in 2023, the gross value added (GVA) of the construction industry in the United Kingdom amounted to almost GBP 108.7 billion, compared with GBP 124.4 billion in the previous year.

- Modern buildings have increasingly complex systems and technologies, including HVAC systems, security systems, energy management systems, and smart building technologies. Single facility management systems offer integrated solutions to manage and optimize these systems effectively, maximizing operational efficiency and cost savings.

- When businesses choose a single service provider, they outsource their day-to-day operations to a specialist provider. They can be assured of superior service quality and efficiency by hiring specialists. Using several service providers is a time-consuming activity that necessitates the management of multiple vendors and the associated hazards. The scale of the developing and developed economies makes working with a single supplier and servicer impossible. Unfortunately, many businesses still operate with a single mindset, relying on a single property management service provider for all their needs.

The Commercial End-user Segment is Expected to Hold a Significant Market Share

- The commercial segment's demand for facility management services continues to grow as businesses prioritize operational efficiency, occupant satisfaction, regulatory compliance, and risk management to maintain competitive advantage and maximize returns on their real estate investments. Office buildings used by providers of business services, including manufacturers' corporate offices, IT & communication companies, and other service providers, are mainly referred to as the commercial end-user sector. Due to this, the overall supply of commercial building decoration, essential interior fittings, and management has grown drastically in importance, pushing the region's commercial sector market.

- Commercial buildings often have complex infrastructure and systems requiring regular maintenance, including HVAC, electrical, plumbing, and security systems. Facility management services help ensure these systems operate efficiently, minimizing downtime and disruptions to business operations.

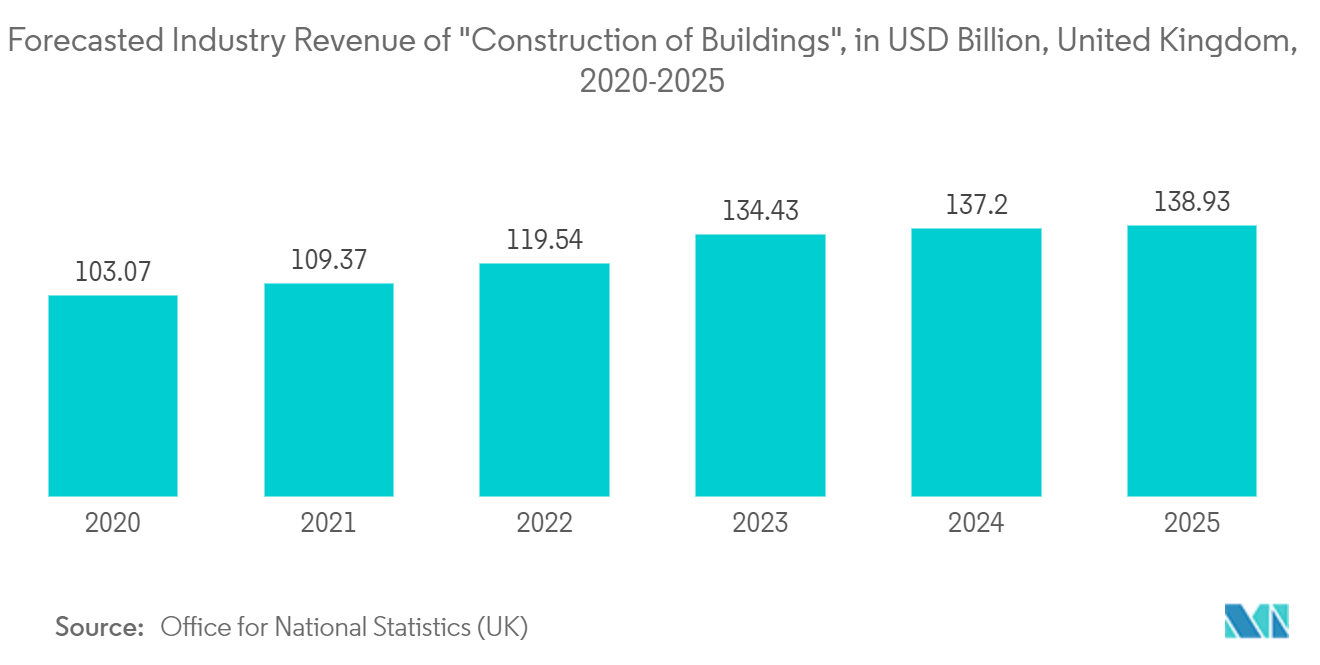

- According to the Construction Industry Training Board, in 2023, output for the construction of commercial facilities in the United Kingdom increased by 4%, and it is predicted to be the same in FY 2024. Further, according to the Office for National Statistics (UK), it is projected that the revenue of construction of residential and non-residential buildings in the United Kingdom will amount to around USD 138.93 billion by 2025. Growth in the commercial construction sector leads to an increase in new buildings, including commercial properties, which may further create demand in the market.

- In addition, commercial properties are exposed to various risks, including security threats, equipment failures, and natural disasters. Facility management services help mitigate these risks by implementing security measures, conducting preventive maintenance, and developing emergency response plans to protect occupants and assets.

- Additionally, the market offers several opportunities for vendors to implement and execute various IoT-based facility management and enhance the development of smart buildings within the United Kingdom. This is due to the rising interest in establishing smart buildings and IoT technologies. Also, the surge in the business acumen among industry providers and the diversification of the economy from various industries is anticipated to maximize the demand for facility management services within the region.

- In January 2023, Fisco UK, the facilities management company, partnered with (MWS) managed workplace services provider Apogee Corporation to expand its overall IT offering and deliver a more automated and integrated solutions portfolio to its client base. Through the partnership, the firm has boosted machinery uptime for its clients by around 28% compared to its previous MWS supplier. Hence, these significant developments are poised to drive the demand for FM services in the commercial space in the United Kingdom.

UK Facility Management Industry Overview

The UK facility management market is fragmented as it is highly competitive, with several players of different sizes. This market is expected to experience several acquisitions, mergers, and partnerships as enterprises continue to invest in strategically offsetting the present slowdowns they are experiencing.

- August 2023: Rolls-Royce appointed real estate group JLL to run global facilities management operations across the company's real estate portfolio, including the United Kingdom. As part of the long-term contract starting February 2024, JLL would operate as Rolls-Royce's strategic global facilities management partner across 15 million square feet of manufacturing, warehouse, and office area at 44 sites in 6 countries.

- July 2023: Porto-based Infraspeak extended Series A with EUR 7.5 million to fuel the global expansion of its intelligent facility management platform. The funding will be utilized to develop the company's team and fuel its international expansion.

UK Facilities Management Market Leaders

CBRE Group, Inc.

Mitie Group PLC

EMCOR Facilities Services Inc.

Atlas FM Ltd

Andron Facilities Management

*Disclaimer: Major Players sorted in no particular order

UK Facility Management Market News

- March 2024: Sodexo Health & Care extended established partnerships for catering, retail, and soft FM services at two hospitals at Stoke-on-Trent in Staffordshire. Under a new 10-year contract worth EUR 38 million a year covering both hospitals as part of a Private Finance Initiative (PFI), Sodexo will continue to deliver catering, retail, and soft FM services throughout the PFI and the retained estate at both hospitals.

- March 2024: Mitie was awarded a place on the Crown Commercial Service’s (CCS) Healthcare Soft Facilities Management (FM) Framework agreement for three years with an option to extend for a year. As a prequalified supplier, the integrated services provider will be able to bid for contracts that support the provision of Healthcare Soft FM services to the NHS and other organizations within the healthcare industry in England, including NHS Hospital Trusts, Community Health Trusts, Mental Health Trusts, and General Practices.

UK Facilities Management Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Assessment of the Impact of Macroeconomic Factors on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Trend Toward Commoditization of FM

5.1.2 Growing Demand for IFM and Outsourcing of Non-core Operations from Emerging Verticals

5.1.3 Renewed Emphasis on Workplace Optimization and Productivity

5.2 Market Restraints

5.2.1 Market Saturation in the Public Sector

5.2.2 Growing Competition Expected to Impact Profit Margins of Existing Vendors

5.3 Analysis of Penetration of Integrated Facility Management Services in the United Kingdom

6. MARKET SEGMENTATION

6.1 By Facility Management Type

6.1.1 In-House Facility Management

6.1.2 Outsourced Facility Management

6.1.2.1 Single FM

6.1.2.2 Bundled FM

6.1.2.3 Integrated FM

6.2 By Offering Type

6.2.1 Hard FM

6.2.1.1 Building Services

6.2.1.2 HVAC Services

6.2.1.3 Mechanical, Electrical, and Plumbing Services

6.2.2 Soft FM

6.3 By End-user Industry

6.3.1 Commercial

6.3.2 Institutional

6.3.3 Public/Infrastructure

6.3.4 Industrial

6.3.5 Retail

6.3.6 Other End-user Industries

6.4 By Region

6.4.1 London and South East England

6.4.2 South West England

6.4.3 Midlands and East England

6.4.4 North of England

6.4.5 Rest of the United Kingdom

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 CBRE Group Inc.

7.1.2 Mitie Group PLC

7.1.3 EMCOR Facilities Services Inc.

7.1.4 Atlas FM Ltd

7.1.5 Andron Facilities Management

7.1.6 ISS UK

7.1.7 JLL Limited

7.1.8 Serco Group PLC

7.1.9 Kier Group PLC

7.1.10 Amey PLC

7.1.11 Atalian Servest

7.1.12 Sodexo Facilities Management Services

7.1.13 Compass Group

7.1.14 Engie Facility Management (Engie SA)

7.1.15 Vinci Facilities Limited

7.1.16 Aramark Facilities Services

7.2 Market Share Analysis

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

UK Facility Management Indsutry Segmentation

Facility management is an organizational function that integrates people, places, and processes within the built environment to improve people's quality of life and the productivity of the core business.

The UK facility management market is segmented by facility management type (in-house FM service, outsourced FM service (single FM, bundled FM, and integrated FM)), offering type (hard FM (building services, HVAC services, mechanical, and electrical & plumbing services), and soft FM), and end users (commercial, institutional, public/infrastructure, industrial, and other end users), and region (London and South East England, South West England, Midlands & East England, North of England, and Rest of the United Kingdom). The market sizes and forecasts are in terms of value USD for all the above segments.

| By Facility Management Type | |||||

| In-House Facility Management | |||||

|

| By Offering Type | |||||

| |||||

| Soft FM |

| By End-user Industry | |

| Commercial | |

| Institutional | |

| Public/Infrastructure | |

| Industrial | |

| Retail | |

| Other End-user Industries |

| By Region | |

| London and South East England | |

| South West England | |

| Midlands and East England | |

| North of England | |

| Rest of the United Kingdom |

UK Facilities Management Market Research FAQs

How big is the UK Facility Management Market?

The UK Facility Management Market size is expected to reach USD 69.28 billion in 2024 and grow at a CAGR of 1.65% to reach USD 75.19 billion by 2029.

What is the current UK Facility Management Market size?

In 2024, the UK Facility Management Market size is expected to reach USD 69.28 billion.

Who are the key players in UK Facility Management Market?

CBRE Group, Inc., Mitie Group PLC, EMCOR Facilities Services Inc., Atlas FM Ltd and Andron Facilities Management are the major companies operating in the UK Facility Management Market.

What years does this UK Facility Management Market cover, and what was the market size in 2023?

In 2023, the UK Facility Management Market size was estimated at USD 68.14 billion. The report covers the UK Facility Management Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the UK Facility Management Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

UK Facilities Management Industry Report

Statistics for the 2024 UK Facility Management market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. UK Facility Management analysis includes a market forecast outlook for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.