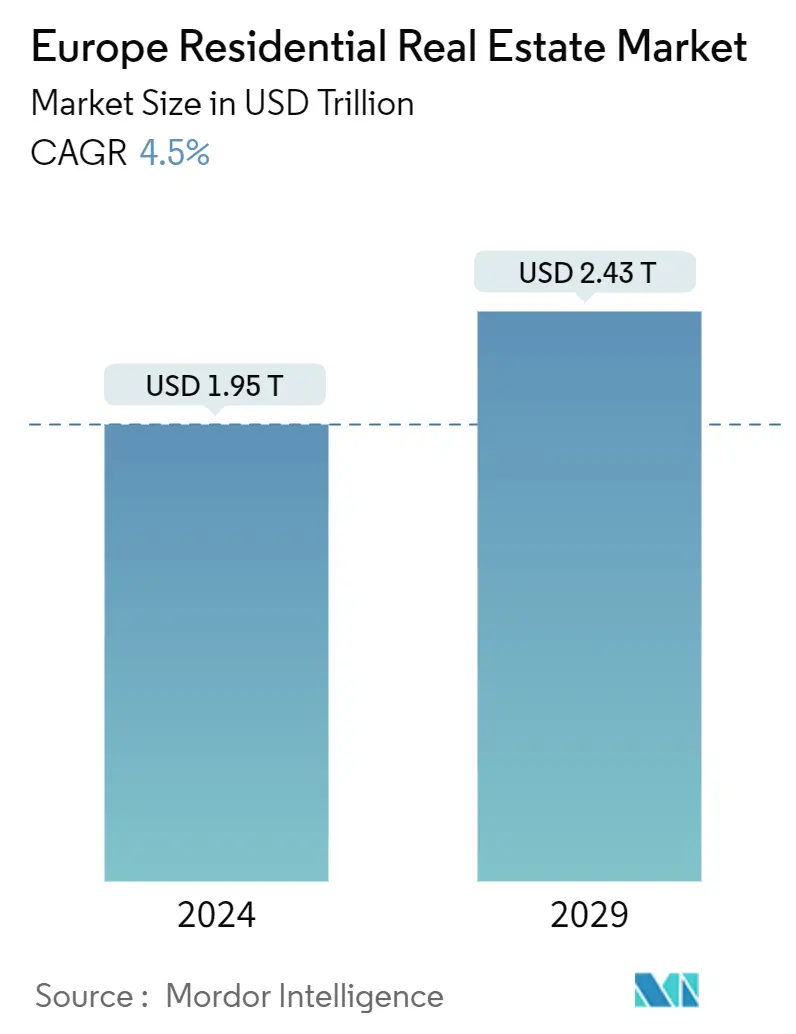

Europe Residential Real Estate Market Size

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| Market Size (2024) | USD 1.95 Trillion |

| Market Size (2029) | USD 2.43 Trillion |

| CAGR (2024 - 2029) | 4.50 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Europe Residential Real Estate Market Analysis

The Europe Residential Real Estate Market size is estimated at USD 1.95 trillion in 2024, and is expected to reach USD 2.43 trillion by 2029, growing at a CAGR of 4.5% during the forecast period (2024-2029).

- Housing demand in Europe is projected to continue to be driven by a combination of demographic factors. Over the past decade, Europe’s population has grown rapidly, resulting in an increased demand for housing. This growth has been accompanied by a decrease in the average household size as a result of an aging population.

- Housing demand is expected to continue to grow as a result of demographic factors such as an increasing number of households in Europe’s largest urban centers. The number of households in the EU’s capital cities is projected to grow by 3% in the next five years.

- As demand continues to grow, many European cities are already struggling with a lack of new housing developments. Over the past decade, construction activity has been 45% lower than the pre-crisis average, and supply has been unable to keep up.

- In the past 18 months, the pipeline has continued to dry up, and the situation is expected to remain subdued. While construction cost inflation is projected to ease from 2023 and the peak seen in 2022, there will still be upward pressure on costs, mainly driven by wage increases.

- The construction sector faces a number of challenges, including a lack of financing, lengthy planning processes, and uncertainty about exit values, which are expected to further exacerbate the supply and demand imbalance, putting further pressure on affordability.

- The cost of living is anticipated to continue to rise as higher mortgage rates make it less affordable to own a home while a limited new rental supply pushes up rents. Mortgage rates in the euro area and the United Kingdom have been at their highest levels since 2009 and are expected to remain high.

- This makes renting relatively attractive in many markets. However, the rental segment is already oversupplied, and increasing demand is likely to push rents higher. Some markets may see double-digit rent growth, while others are restricted by rent controls. Tightening regulations will reduce supply further. Vacancy is expected to remain low. While regulation remains a concern, rising market rents are set to underpin robust income growth.

Europe Residential Real Estate Market Trends

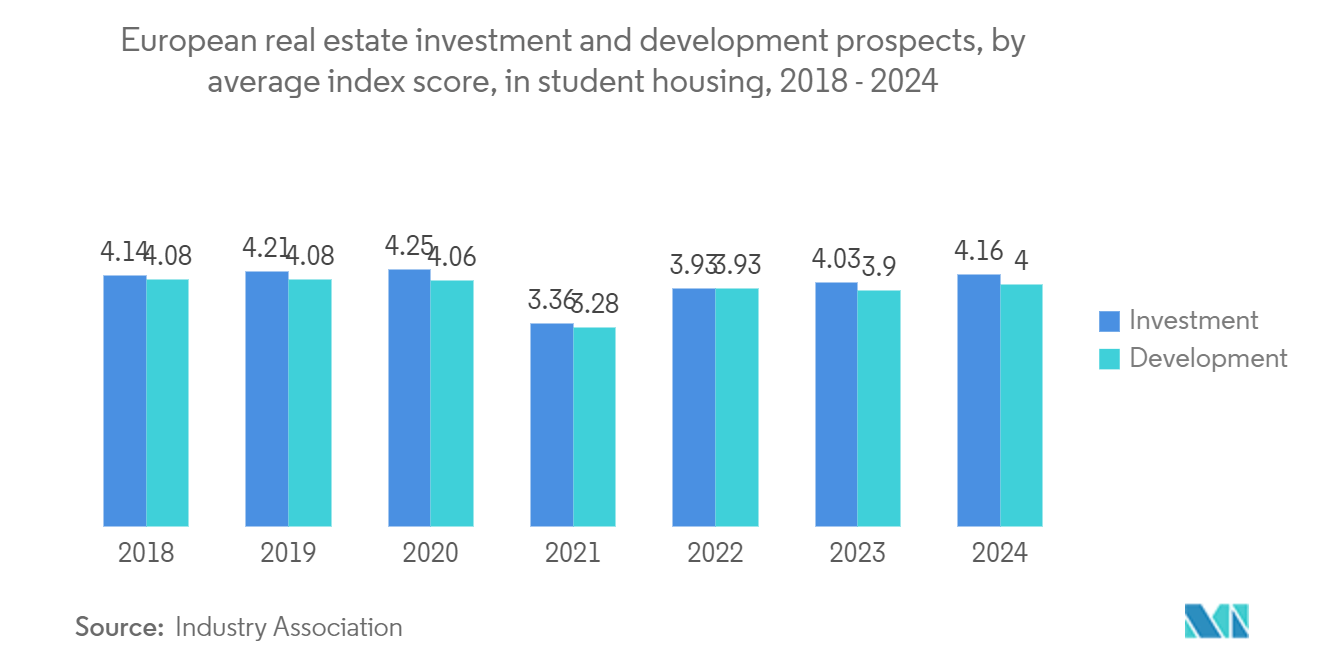

Student Housing to Gain Traction

- The demand for student housing in Europe is set to continue to grow, driven by the increasing number of international students. In addition, the aging population is also putting pressure. As a result, occupier fundamentals in all subsectors are expected to remain strong, underpinning rental growth in 2024.

- With a student population of 1.2 million, Poland is the 6th largest potential market in Europe for student accommodation operators, second only to Spain and Italy. The market potential for student accommodation operators in Poland is 2 to 3 times that of the Netherlands.

- There is an unmet demand of 200 to 400 thousand beds for student housing in Poland, driven mainly by domestic mobile students who move to other cities to study, as well as the growing number of international students. The student housing market is still in its early stages in Poland, providing investors with attractive opportunities for yield and capital value growth.

- On the other hand, rental rates for operational projects within Poland’s student accommodation sector have increased by 30% to 60% over the last three years, depending on the city and the asset. Warsaw saw a 50% increase in rental rates. In the city of Skopje, rents increased by around 30%. In the city of Tri-City, rents increased by 50%. In Wrocław, rents increased by 30-50%, and in the city of Krakow, rents increased by 40-60%. It is clear that the new supply cannot keep up with the increasing demand.

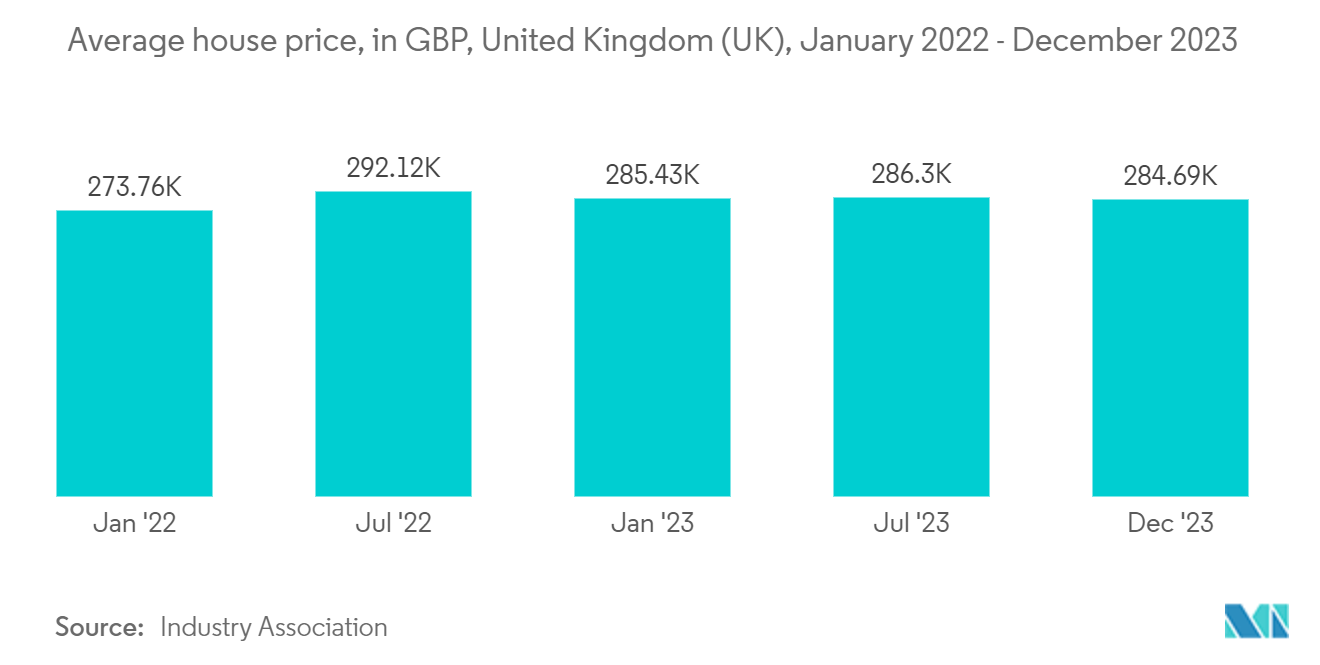

United Kingdom Holds a Prominent Position in the Market

- The living sector is benefitting from structural and demographic tailwinds, which means that sentiment toward the sector remains strong despite broader macroeconomic headwinds. Occupational demand in the private rented sector and the demand for purpose-built student accommodation in the face of an acute supply shortage have contributed to strong rental-value growth across all subsectors. This rental growth, in combination with more flexible asset pricing, has attracted investors into the sector.

- Year-on-year transaction volumes have fallen significantly. This is largely due to asset holders remaining reluctant sellers rather than a general softening in investor appetite toward the sector. An estimated 82,940 sales were completed in February 2024, which was 1.2% more than the sales recorded in January. This was the second consecutive monthly increase. However, sales still remain 5.6% below the same time last year and 15.5% below pre-pandemic levels.

- Investors are continuing to focus on well-positioned, high-quality schemes with robust environmental, social, and governance credentials – all key factors in attracting tenants. Student accommodation schemes affiliated with world-class universities are expected to remain at the top of investors' priorities.

- The living sector is expected to continue to deliver positive results, supported by an increase in rental values, albeit at more normalized levels, as affordability concerns constrain investors’ capacity to drive up rental values. Increased investor attention to the long-term cost-effectiveness of schemes is critical to underpinning asset-income profiles with certainty and stability.

Europe Residential Real Estate Industry Overview

Europe's residential real estate market is moderately consolidated, with a few players dominating the market. Major real estate players in the market are Elm Group, Places for People Group Limited, LEG Immobilien AG, Consus Real Estate AG, and CPI Property Group. The proportion of residential real estate property sales through online channels has consistently grown due to the rising internet penetration, growing demand, increasing personal disposable incomes, surging middle-class youth population, and opportunities offered by government infrastructure investments.

Europe Residential Real Estate Market Leaders

Elm Group

Places for People Group Limited

LEG Immobilien AG

Consus Real Estate AG

CPI Property Group

*Disclaimer: Major Players sorted in no particular order

Europe Residential Real Estate Market News

- November 2023: DoorFeed, a Proptech company, raised EUR 12 million (USD 13.24 million) in seed funding, led by Motive Ventures and Stride and supported by renowned investors, including Seedcamp. Founded by veteran proptech entrepreneur and ex-Uber employee James Kirimi, DoorFeed aims to be the first choice for institutional investors seeking to invest in residential real estate. The company is looking to expand its footprint across Europe, with a focus on Spain, Germany, and the United Kingdom.

- October 2023: H.I.G, a global alternative investment firm with over USD 59 billion in assets under management, invested in the real estate development company, The Grounds Real Estate Development AG (“the Transaction”), which is listed on the alternative stock exchange. The proceeds of the transaction are expected to be utilized to fund the capital expenditures of the current projects of The Grounds. The Grounds, based in Berlin, specializes in the acquisition and development of German residential properties located in large metropolitan areas. In the transaction, the major shareholders of The Grounds, which currently hold 73% of the company’s shares, have agreed to grant H. I.G. the right to share in future rights issues.

Europe Residential Real Estate Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

2.1 Analysis Methodology

2.2 Research Phases

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Current Economic Scenario and Consumer Sentiment

4.2 Residential Real Estate Buying Trends - Socioeconomic and Demographic Insights

4.3 Government Initiatives and Regulatory Aspects Pertaining to the Residential Real Estate Sector

4.4 Insights into the Size of Real Estate Lending and Loan-to-value Trends

4.5 Insights into the Interest Rates for the General Economy and Real Estate Lending

4.6 Insights into the Rental Yields in the Residential Real Estate Sector

4.7 Insights into the Capital Market Penetration and REIT Presence in the Residential Real Estate Sector

4.8 Insights into the Support Provided by the Government and Public-Private Partnerships for Affordable Housing

4.9 Insights into the Tech and Startups Active in the Real Estate Sector (Broking, Social Media, Facility Management, and Property Management)

4.10 Impact of COVID-19 on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Developments in the Residential Segment

5.1.2 Investments in the Senior Living Units

5.2 Restraints

5.2.1 Limited Availability of Land Hindering the Market

5.3 Opportunities

5.3.1 Sustainable and Eco-Friendly Methods

5.4 Industry Attractiveness - Porter's Five Forces Analysis

5.4.1 Bargaining Power of Suppliers

5.4.2 Bargaining Power of Consumers / Buyers

5.4.3 Threat of New Entrants

5.4.4 Threat of Substitute Products

5.4.5 Intensity of Competitive Rivalry

6. MARKET SEGMENTATION

6.1 By Type

6.1.1 Condominiums and Apartments

6.1.2 Villas and Landed Houses

6.2 By Countries

6.2.1 Germany

6.2.2 United Kingdom

6.2.3 France

6.2.4 Rest of Europe

7. COMPETITIVE LANDSCAPE

7.1 Overview

7.2 Company Profiles

7.2.1 Elm Group

7.2.2 Places for People Group Limited

7.2.3 LEG Immobilien AG

7.2.4 Consus Real Estate AG

7.2.5 CPI Property Group

7.2.6 Aroundtown Property Holdings

7.2.7 Segro

7.2.8 Covivio

7.2.9 Unibail-Rodamco

7.2.10 Gecina*

- *List Not Exhaustive

7.3 Other Companies

8. FUTURE OF THE MARKET

9. APPENDIX

Europe Residential Real Estate Industry Segmentation

Real estate (land and any buildings on it) used for residential purposes is commonly referred to as residential real estate. Single-family dwellings are the most prevalent type of residential real estate.

The residential real estate market in Europe is segmented by type (condominiums & apartments and villas & landed houses) and country (Germany, United Kingdom, France, and the Rest of Europe).

The report offers market sizes and forecasts in value (USD) for all the above segments.

| By Type | |

| Condominiums and Apartments | |

| Villas and Landed Houses |

| By Countries | |

| Germany | |

| United Kingdom | |

| France | |

| Rest of Europe |

Europe Residential Real Estate Market Research FAQs

How big is the Europe Residential Real Estate Market?

The Europe Residential Real Estate Market size is expected to reach USD 1.95 trillion in 2024 and grow at a CAGR of 4.5% to reach USD 2.43 trillion by 2029.

What is the current Europe Residential Real Estate Market size?

In 2024, the Europe Residential Real Estate Market size is expected to reach USD 1.95 trillion.

Who are the key players in Europe Residential Real Estate Market?

Elm Group, Places for People Group Limited, LEG Immobilien AG, Consus Real Estate AG and CPI Property Group are the major companies operating in the Europe Residential Real Estate Market.

What years does this Europe Residential Real Estate Market cover, and what was the market size in 2023?

In 2023, the Europe Residential Real Estate Market size was estimated at USD 1.86 trillion. The report covers the Europe Residential Real Estate Market historical market size for years: 2020, 2021, 2022 and 2023. The report also forecasts the Europe Residential Real Estate Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

What are the key drivers of the European Residential Real Estate Market?

The key drivers of the European Residential Real Estate Market are a) Increasing demand for affordable housing b) Rise of co-living and co-working spaces c) Demand for sustainable and energy-efficient homes d) Shift towards smaller, more compact homes

Europe Residential Real Estate Industry Report

The European Residential Real Estate market is experiencing significant transformations, driven by customer preferences, local circumstances, and macroeconomic factors. There's a growing demand for sustainable, energy-efficient, and compact homes, leading to a shift towards environmentally conscious living and affordable housing. This trend is prompting real estate companies in Europe to innovate and adapt their offerings, exploring new business models to cater to the changing needs of freelancers, digital nomads, and young professionals, especially in urban areas with high housing costs. The market is also influenced by the scarcity of land, leading to vertical expansions in densely populated areas and a trend towards countryside living in rural areas. The market is expected to grow, fueled by low-interest rates, economic growth, and a significant increase in transaction prices and rental segment growth. These factors present a promising outlook for real estate companies in Europe, which must navigate these diverse demands with adaptability and innovation. The market's diversity, shaped by trends like the return to nature and the popularity of multifamily real estate models, reflects the complex interplay of factors influencing the market and the strategic approaches of real estate companies in Europe. Mordor Intelligence™ Industry Reports offer a comprehensive market forecast and historical overview. Get a sample of this industry analysis as a free report PDF download.