Market Size of Europe Residential Real Estate Industry

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

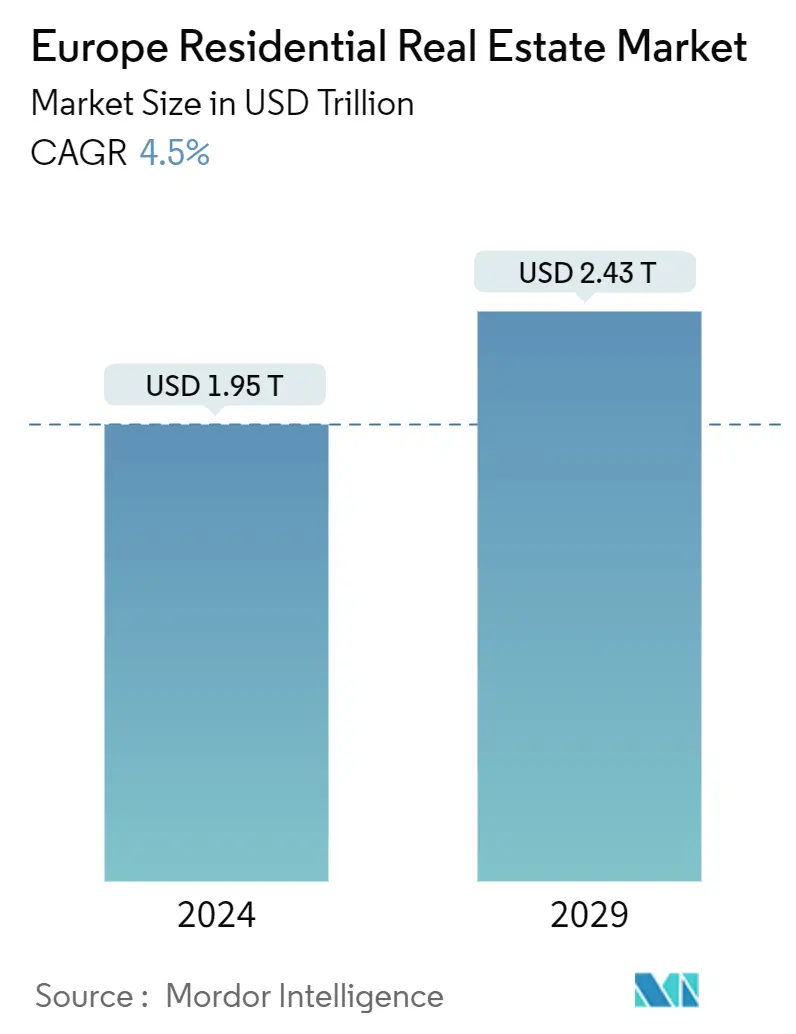

| Market Size (2024) | USD 1.95 Trillion |

| Market Size (2029) | USD 2.43 Trillion |

| CAGR (2024 - 2029) | 4.50 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Europe Residential Real Estate Market Analysis

The Europe Residential Real Estate Market size is estimated at USD 1.95 trillion in 2024, and is expected to reach USD 2.43 trillion by 2029, growing at a CAGR of 4.5% during the forecast period (2024-2029).

- Housing demand in Europe is projected to continue to be driven by a combination of demographic factors. Over the past decade, Europe’s population has grown rapidly, resulting in an increased demand for housing. This growth has been accompanied by a decrease in the average household size as a result of an aging population.

- Housing demand is expected to continue to grow as a result of demographic factors such as an increasing number of households in Europe’s largest urban centers. The number of households in the EU’s capital cities is projected to grow by 3% in the next five years.

- As demand continues to grow, many European cities are already struggling with a lack of new housing developments. Over the past decade, construction activity has been 45% lower than the pre-crisis average, and supply has been unable to keep up.

- In the past 18 months, the pipeline has continued to dry up, and the situation is expected to remain subdued. While construction cost inflation is projected to ease from 2023 and the peak seen in 2022, there will still be upward pressure on costs, mainly driven by wage increases.

- The construction sector faces a number of challenges, including a lack of financing, lengthy planning processes, and uncertainty about exit values, which are expected to further exacerbate the supply and demand imbalance, putting further pressure on affordability.

- The cost of living is anticipated to continue to rise as higher mortgage rates make it less affordable to own a home while a limited new rental supply pushes up rents. Mortgage rates in the euro area and the United Kingdom have been at their highest levels since 2009 and are expected to remain high.

- This makes renting relatively attractive in many markets. However, the rental segment is already oversupplied, and increasing demand is likely to push rents higher. Some markets may see double-digit rent growth, while others are restricted by rent controls. Tightening regulations will reduce supply further. Vacancy is expected to remain low. While regulation remains a concern, rising market rents are set to underpin robust income growth.