Glass Packaging Market Size

| Study Period | 2019 - 2029 |

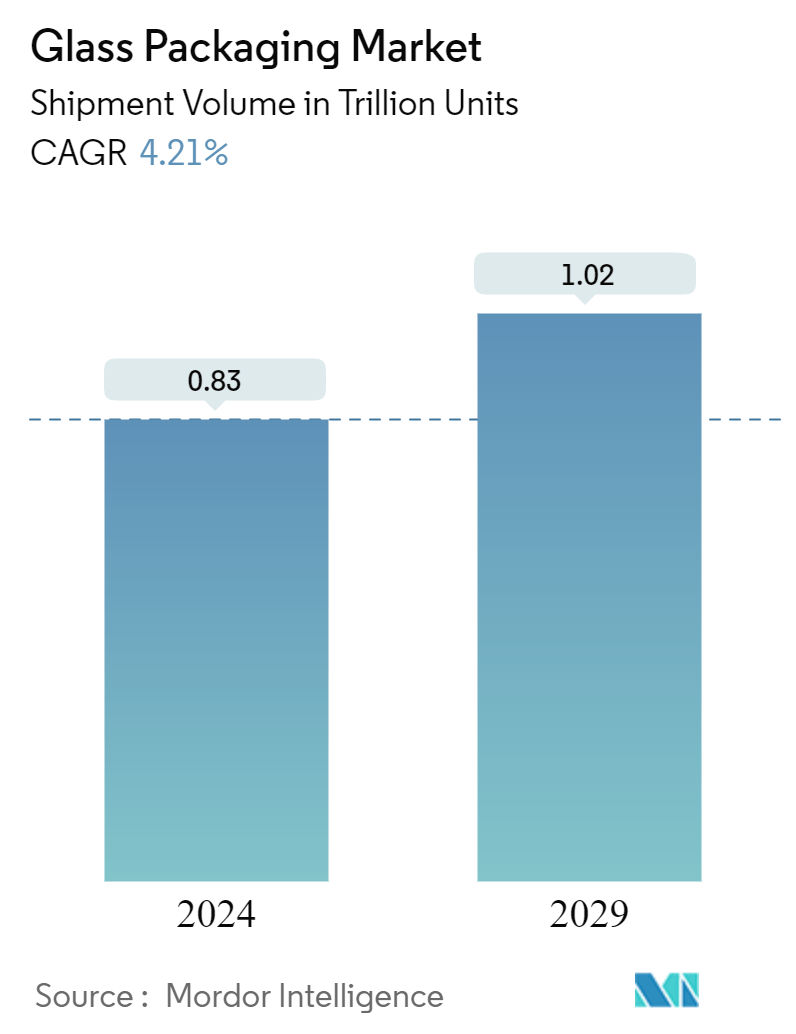

| Market Volume (2024) | 0.83 Trillion units |

| Market Volume (2029) | 1.02 Trillion units |

| CAGR (2024 - 2029) | 4.21 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Glass Packaging Market Analysis

The Glass Packaging Market size in terms of shipment volume is expected to grow from 0.83 Trillion units in 2024 to 1.02 Trillion units by 2029, at a CAGR of 4.21% during the forecast period (2024-2029).

- Glass packaging is considered one of the most trusted forms of packaging for health, taste, and environmental safety. Glass packaging, considered premium, maintains the freshness and safety of the product. This can ensure its continuous usage across various end-user industries despite the heavy competition from other packaging forms.

- Rising consumer demand for safe and healthier packaging helps glass packaging grow in different categories. Also, innovative technologies for embossing, shaping, and adding artistic finishes to glass make glass packaging more desirable among end users. The market is growing due to the increasing demand for eco-friendly products and the rising demand from the food and beverage industry.

- Glass is widely considered the most environmentally friendly packaging type due to its recyclable nature. Lightweight glass has become a significant innovation, offering the same resistance as conventional glass materials and higher stability, reducing the volume of raw materials and CO2 emitted.

- Emerging markets like India and China are witnessing high demand for beer, soft drinks, and ciders due to the consumers' increasing per capita spending and changing lifestyles. However, the increasing operational costs and growing usage of substitute products, such as plastics and tin, are restraining the market growth.

- One of the main challenges for the market is the increased competition from alternative forms of packaging, such as aluminum cans and plastic containers. As these items are lighter in weight than bulky glass, they are gaining popularity among manufacturers and customers because of the lower cost of their carriage and transportation. Moreover, the increasing costs of raw materials and other factors have led to higher expenses, making it economically unfeasible for mass-produced goods.

- With consumers' increasing focus on sustainability concerns, brewing companies are adopting collaboration and partnership strategies with glass bottle and container manufacturers to offer beer products in glass bottles to meet sustainability goals. In May 2023, Ardagh Glass Packaging (Ardagh Group) and Sprecher Brewing Company announced the partnership. The partnership will help the brewery's commitment to stay local and sustainable with the continuous supply of glass beer and beverage bottles from Ardagh Glass Packaging. Also, this will help the brewing company meet the brand and sustainability goals by providing beer in high-quality glass bottles.

Glass Packaging Market Trends

The Beverage Industry to Hold the Highest Market Share

- Premiumization trends have played a role in selecting glass packaging for various beverage categories, including soft drinks. Soft drinks hold a significant market share, owing to the popularity of such drinks worldwide. Soft drinks offer various flavors and formats to suit every drinking occasion.

- The market for glass packaging in the alcoholic beverage industry faces intense competition from the metal packaging segment in the form of cans. However, it is expected to maintain its share during the forecast period due to its usage of premium products. The growth is expected across different beverage products, like juices, coffee, tea, soups, and non-dairy beverages.

- Among alcoholic beverages, beer has witnessed tremendous growth in the past few years. Most beer volume is sold in glass bottles, driving the need for increased production rates in the glass packaging industry. The increasing demand for premium variants of alcoholic drinks is driving the growth of glass bottles.

- Returnable glass bottles are a cost-effective option for companies to deliver their products. This form of packaging is used mainly in the non-alcoholic beverage industry. About 70% of the bottles used for natural mineral water are plastic. The choice of bottled water packaging material is increasing, considering environmental considerations.

- Beverage companies like Coke and PepsiCo also try to avoid plastic packaging. By 2025, PepsiCo aims to eliminate the use of 67 billion plastic bottles, which glass bottles will replace.

- The global dairy industry has been witnessing a shift from plastic to glass bottles, driven by consumer demand for environmentally friendly milk. Dairy companies like Milk & More and Parker Dairies have noticed a significant rise in demand for glass bottles. Consumers are willing to pay more for this service as they attempt to reduce their use of plastic and help the environment.

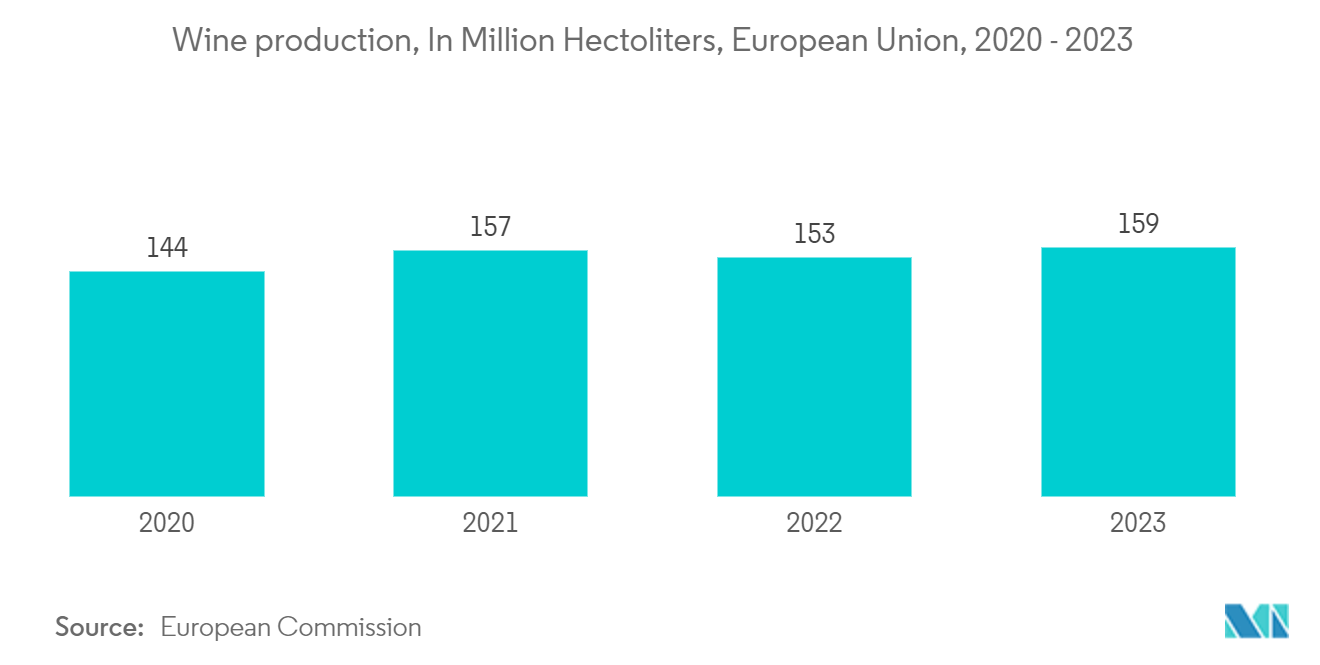

- According to the European Commission, wine production in 2020 was 144 million hectares, which increased to 159 million hectares in 2023. The preferred wine packaging is a colored glass bottle to prevent sunlight from spoiling the wine inside. The increasing consumption of wine is expected to spearhead the demand for glass packaging during the forecast period. Wine manufacturers are becoming increasingly innovative in attracting customers with their packaging and are developing new concepts and designs.

Asia-Pacific to Hold the Largest Market Share

- The escalating need for pharmaceutical drugs and advancements in pharmaceutical technology drive the demand for glass bottles, ampules, and other glass packaging solutions. With an upsurge in chronic illnesses and the substantial production of vaccine doses, the demand for primary packaging, particularly glass containers, is expected to surge.

- The increasing consumption of alcoholic beverages drives market growth in the Asia-Pacific region. The beer packaging industry in the Asia-Pacific region is mainly driven by changing cultural trends, growing populations, urbanization, and the growing popularity of beer among the younger populations.

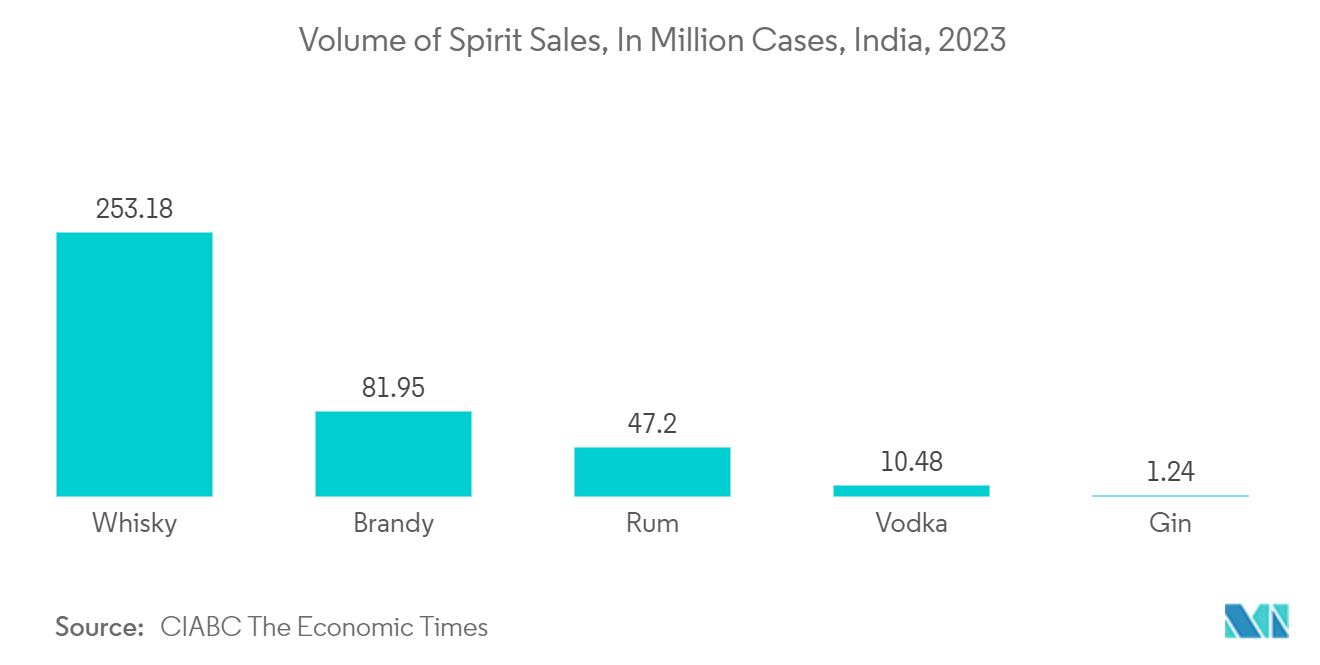

- In India, most spirits, including whiskey, gin, rum, and brandy, are packed in glass bottles. Due to the increasing consumption of spirits, there was an increase in sales in 2023; whiskey had the highest number of cases sold, with 253.18 million cases, followed by 81.95 million cases, and gin at 47.2 million cases, according to Economic Times.

- China is one of the world's largest pharmaceutical markets. Compared to many industrialized countries, healthcare spending is still modest. The Chinese government is improving its ability to research and develop medicines domestically. As a result, it can provide affordable healthcare to more citizens.

- Additionally, alcohol consumption in China has been significantly increasing over the years. As per the Brazil-based bank Banco do Nordeste, the consumption of alcoholic beverages in China is expected to increase the demand for glass packaging in the coming years. Also, many alcoholic beverage companies seek to expand in the country to seize the opportunity.

- Japan has been emphasizing recycling glass containers and bottles to reduce its carbon footprint and has built multiple glass recycling plants nationwide. Over 18 glass recycling plants accept glass bottles and containers to form glass culets and powder. The robust recycling infrastructure promotes glass packaging due to its functional property advantages.

- Also, countries such as India have increased beer consumption. Indian consumers are increasingly opting for glass packaging, particularly bottles, due to health concerns. Glass packaging is preferred over other options as it prevents surface leaching.

- India's pharmaceutical sector places a high value on research and development. In recent years, India achieved global recognition as a medical powerhouse by expanding its R&D ecosystem and boosting pharmaceutical exports, offering growth prospects for various domestic glass packaging providers.

- Increased shipments of glass containers in various end-use sectors are driving market growth in Japan. Glass containers are highly favored for packaging liquid pharmaceuticals, chemicals, and a range of perishable/non-perishable products. The growing preference for eco-friendly packaging solutions positively impacts the adoption of pharmaceutical glass packaging.

Glass Packaging Industry Overview

The global glass packaging market is fragmented due to the strong presence of major players worldwide, like Piramal Glass Private Limited, Owens-Illinois Inc., Westpack LLC, Gerresheimer AG, and Ardagh Group. The competition is also intense due to the presence of substitutes, as many companies in the industry are trying to innovate consistently to retain their market share.

April 2024: O-I Glass Inc. (O-I Glass) significantly refurbished its Zipaquira (Colombia) manufacturing site to improve sustainability, flexibility, and productivity. O-I Glass invested approximately USD 120 million in this refurbishment, which aligns with sustainability strategy, ongoing investments in plant upgrades, and a previously announced capital expenditure plan. The refurbishment included installing a state-of-the-art furnace with proven oxy/fuel combustion and waste heat recovery technology.

February 2024: Telangana announced that it will collaborate with SGD Pharma and Corning Inc. to bring modern technology and manufacturing expertise to this area. This collaboration will combine Corning’s high-quality pharmaceutical tubing technology with SGD Pharma’s glass vial manufacturing and conversion expertise. This will secure SGD Pharma’s tubing capacities to supply primary packaging to its Indian and international customers from Telangana, India.

Glass Packaging Market Leaders

Piramal Glass Private Limited

Owens-Illinois Inc.

Gerresheimer AG

Ardagh Group

SGD S.A. (SGD Pharma)

*Disclaimer: Major Players sorted in no particular order

Glass Packaging Market News

- March 2024: A 75 cl bottle with a carbon footprint and approach to achieving carbon neutrality was launched by O-I Glass, which has been certified by the Carbon Trust.

- February 2024: Vetropack, a European glass manufacturer, launched a returnable bottle of 0.33 liter, the first of its kind in the Austrian brewing sector. The bottle is one-third lighter than the traditional reusable bottle, and over two-thirds of the glass used in the production process is recycled.

Glass Packaging Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

4.4 Industry Policies

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Demand for Eco-friendly Products

5.1.2 Increasing Demand from the Food and Beverage Industries

5.2 Market Restraints

5.2.1 Rising Operational Costs

5.2.2 Growing Usage of Substitute Products (Plastic)

6. MARKET SEGMENTATION

6.1 By End-user Industry

6.1.1 Food

6.1.2 Beverage

6.1.3 Personal Care

6.1.4 Healthcare

6.1.5 Household Care

6.2 By Geography ***

6.2.1 North America

6.2.1.1 United States

6.2.1.2 Canada

6.2.2 Europe

6.2.2.1 United Kingdom

6.2.2.2 Germany

6.2.2.3 France

6.2.2.4 Italy

6.2.2.5 Spain

6.2.3 Asia-Pacific

6.2.3.1 China

6.2.3.2 India

6.2.3.3 Japan

6.2.3.4 Australia and New Zealand

6.2.4 Latin America

6.2.4.1 Brazil

6.2.4.2 Mexico

6.2.4.3 Argentina

6.2.5 Middle East and Africa

6.2.5.1 Saudi Arabia

6.2.5.2 United Arab Emirates

6.2.5.3 South Africa

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Piramal Glass Private Limited

7.1.2 Owens-Illinois Inc.

7.1.3 WestPack LLC

7.1.4 Gerresheimer AG

7.1.5 Hindustan National Glass & Industries Ltd

7.1.6 Ardagh Group

7.1.7 HEINZ-GLAS GmbH & Co. KGaA

7.1.8 Agrado Sa

7.1.9 SGD SA (SGD Pharma)

7.1.10 AAPL Solutions Pvt. Ltd

7.1.11 Crestani Srl

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

Glass Packaging Industry Segmentation

Glass is one of the most preferred packaging materials for consumers who are concerned about their health and the environment. It is made from all-natural, sustainable raw materials. Glass packaging preserves the product's taste or flavor and maintains the integrity or healthiness of food and beverages. In addition to extending the shelf life, the high glass barrier helps prevent cross-contamination of odors and flavors between products. This is especially important for foods with unique flavors or smells. Glass packaging ensures that the tantalizing tastes and aromas of the brand's food products remain unchanged from manufacturing to consumption.

The glass packaging market is segmented by end-user industry (food, beverage, personal care, healthcare, and household care) and geography (North America [United States and Canada], Europe [United Kingdom, Germany, France, and Rest of Europe], Asia-Pacific [China, India, Japan, Australia and New Zealand, and Rest of Asia-Pacific], Latin America [Brazil, Mexico, and Rest of Latin America], and Middle East and Africa [Saudi Arabia, United Arab Emirates, South Africa, and the Rest of Middle East and Africa]. The report offers market forecasts and size in volume (units) and value (USD) for all the above segments.

| By End-user Industry | |

| Food | |

| Beverage | |

| Personal Care | |

| Healthcare | |

| Household Care |

| By Geography *** | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Glass Packaging Market Research FAQs

How big is the Glass Packaging Market?

The Glass Packaging Market size is expected to reach 0.83 trillion units in 2024 and grow at a CAGR of 4.21% to reach 1.02 trillion units by 2029.

What is the current Glass Packaging Market size?

In 2024, the Glass Packaging Market size is expected to reach 0.83 trillion units.

Who are the key players in Glass Packaging Market?

Piramal Glass Private Limited, Owens-Illinois Inc., Gerresheimer AG, Ardagh Group and SGD S.A. (SGD Pharma) are the major companies operating in the Glass Packaging Market.

Which is the fastest growing region in Glass Packaging Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Glass Packaging Market?

In 2024, the Asia-Pacific accounts for the largest market share in Glass Packaging Market.

What years does this Glass Packaging Market cover, and what was the market size in 2023?

In 2023, the Glass Packaging Market size was estimated at 0.80 trillion units. The report covers the Glass Packaging Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Glass Packaging Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

What are the regulations and recycling initiatives impacting the Glass Packaging Industry?

The regulations and recycling initiatives impacting the Glass Packaging Industry are a) Recycling infrastructure b) Regulations on recycled content in glass c) Potential for a circular economy

Glass Packaging Industry Report

The glass packaging market is witnessing remarkable growth, fueled by increasing demand from sectors like food and beverages, pharmaceuticals, personal care, and cosmetics. This surge is driven by the material's health, safety, premium quality, and sustainability attributes, with glass being infinitely recyclable. Innovations such as lightweight designs and artistic finishes are boosting its appeal. The beverage industry, in particular, is seeing a rise in glass usage due to growing alcohol consumption and a shift towards sustainable packaging. The cosmetics sector also favors glass for its impermeability and inertness, enhancing product safety and longevity. Market growth is further supported by a global focus on recycling, with Europe leading in recycling rates. Despite challenges from alternative materials and higher costs, the glass packaging market thrives, offering eco-friendly solutions. For detailed insights, Mordor Intelligence™ provides an in-depth analysis, including market share, size, revenue growth rate, and a forecast outlook, available as a free report PDF download, highlighting the sector's potential and opportunities for growth.