Market Overview

| Study Period | 2019 - 2030 |

|---|---|

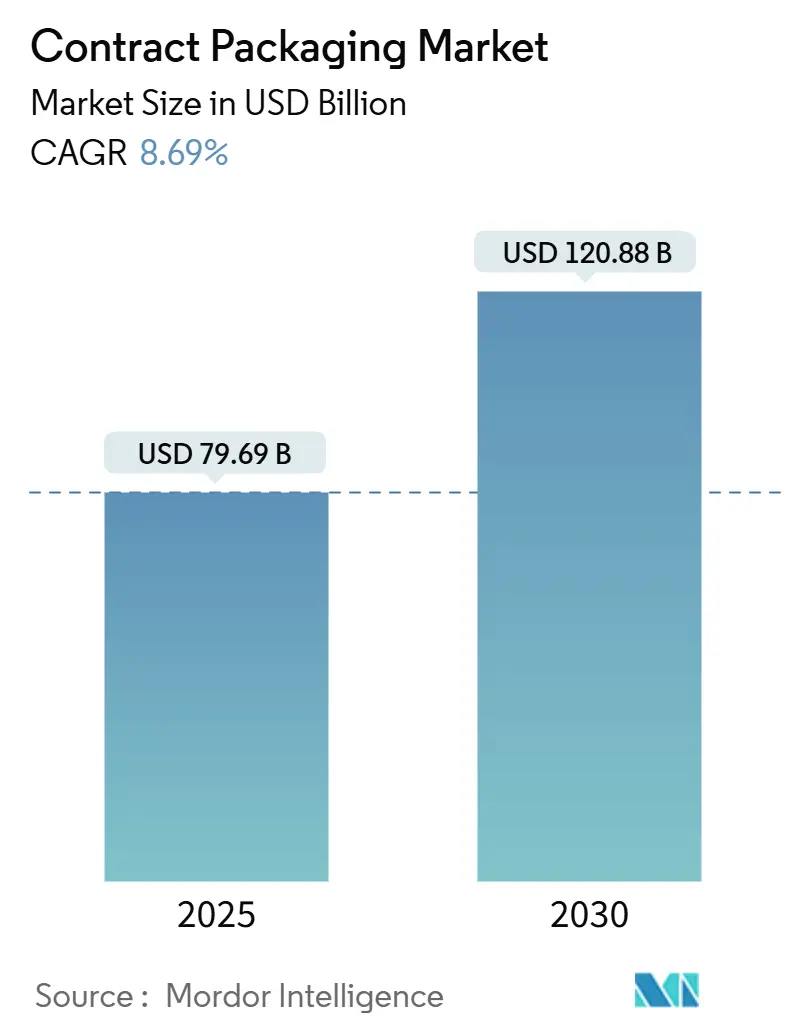

| Market Size (2025) | USD 79.69 Billion |

| Market Size (2030) | USD 120.88 Billion |

| Growth Rate (2025 - 2030) | 8.69% CAGR |

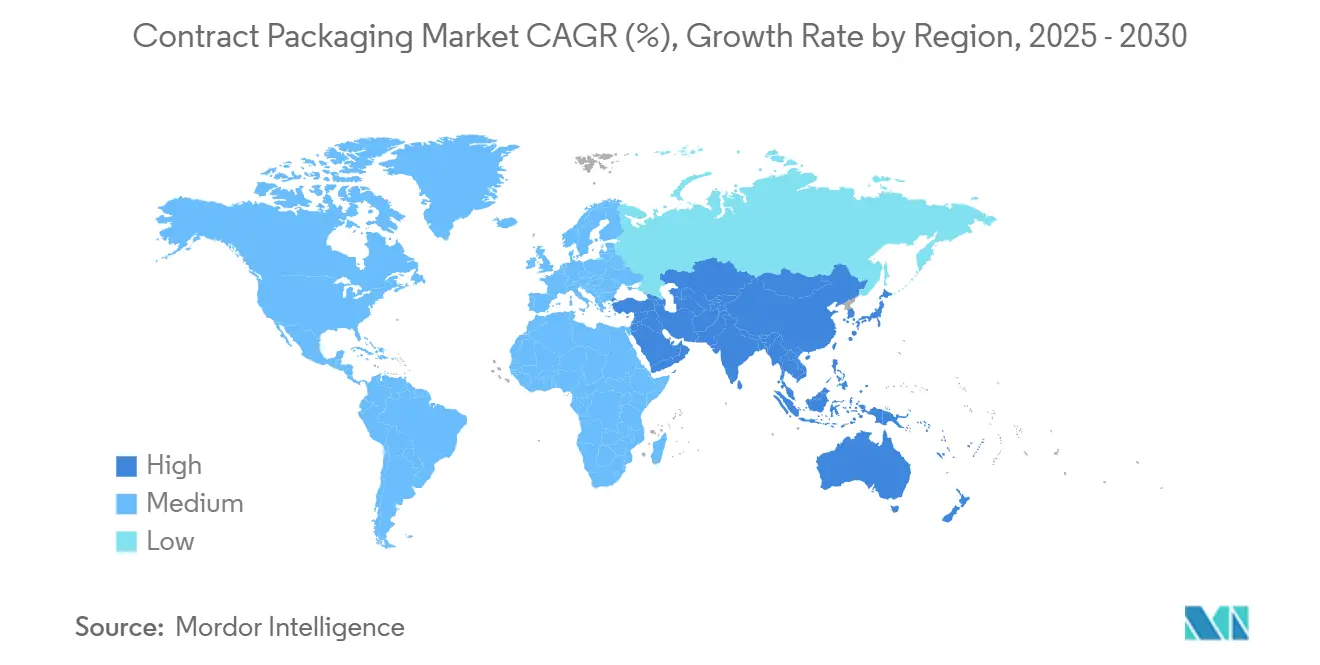

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Contract Packaging Market Analysis by Mordor Intelligence

The contract packaging market size stands at USD 79.69 billion in 2025 and is forecast to reach USD 120.88 billion by 2030, advancing at an 8.69% CAGR during the period. Regulatory mandates from agencies such as the U.S. Food and Drug Administration (FDA) and the European Commission are the primary catalyst for outsourcing decisions, especially in pharmaceutical applications where combination product guidelines and recycled-content rules have raised the technical bar.[1]U.S. Food and Drug Administration, “Packaging & Food Contact Substances (FCS),” FDA.gov E-commerce fueled SKU proliferation, raw material cost volatility, and rapid automation adoption are reshaping service models and cost structures, prompting brand owners to engage providers with flexible lines and digital workflow capabilities. Consolidation-illustrated by Novo Holdings’ USD 16.5 billion Catalent purchase and Amcor’s USD 8.43 billion Berry Global deal-signals a race to scale, geographic reach, and advanced material science competence, giving larger players the edge in serving multinational customers with harmonized quality standards.

Key Report Takeaways

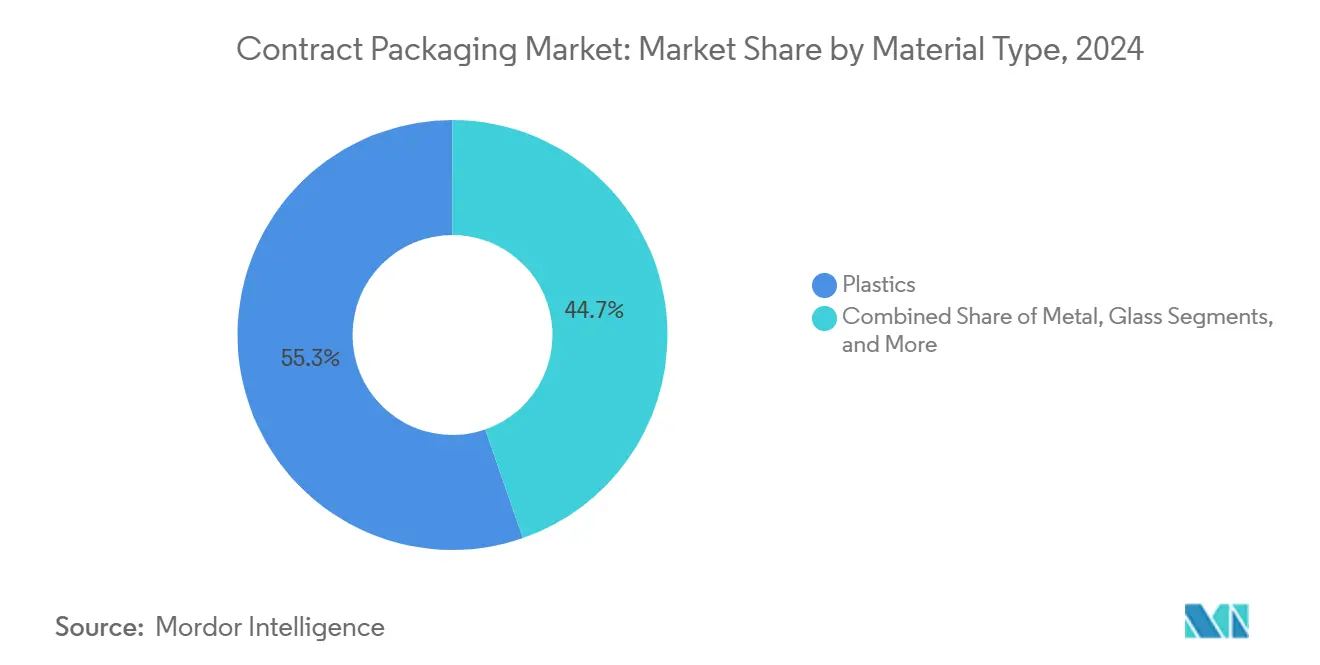

- By material type, plastics commanded 55.32% of the contract packaging market share in 2024; bio-based and composite materials are projected to grow at a 9.65% CAGR through 2030.

- By packaging type, primary packaging captured 57.43% of the contract packaging market size in 2024 and is set to expand at a 9.32% CAGR to 2030.

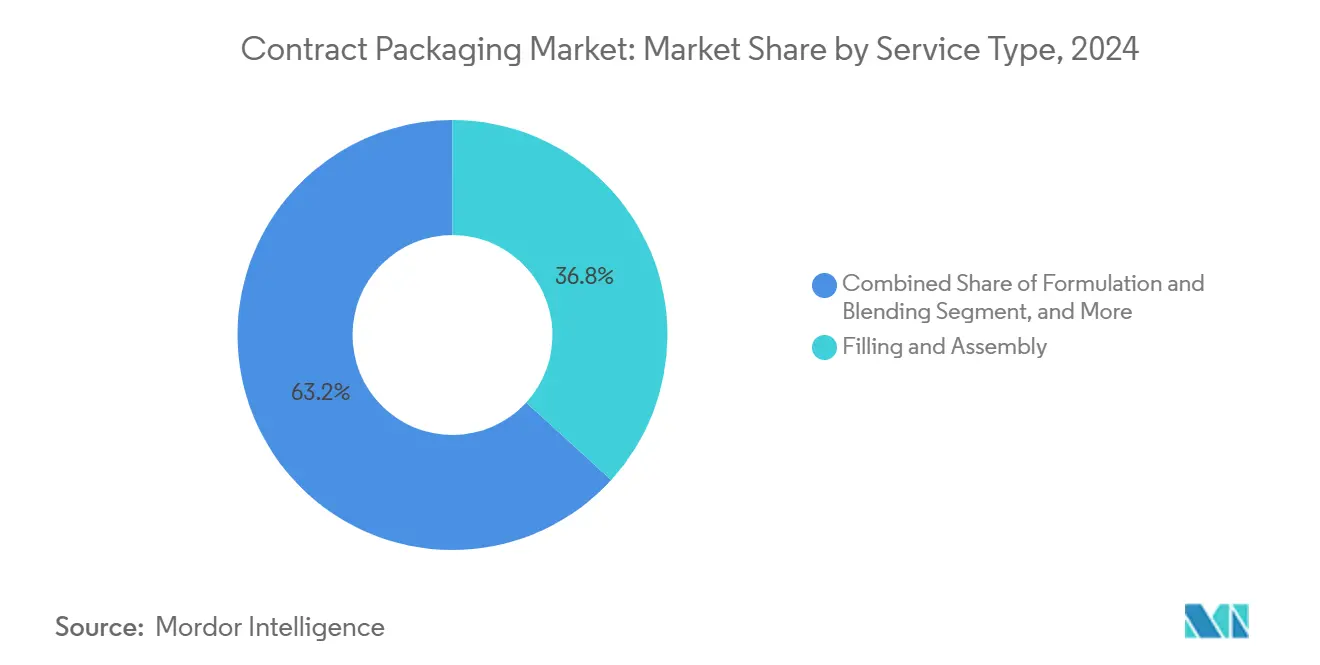

- By service type, filling and assembly held 36.78% of revenue in 2024, whereas fulfillment and logistics are advancing at a 10.34% CAGR through 2030.

- By end-user industry, the food segment led with 35.13% revenue share in 2024, while pharmaceuticals are forecast to record a 10.98% CAGR to 2030.

- By geography, North America retained 38.98% of 2024 revenue, and Asia-Pacific is on track for an 11.52% CAGR to 2030.

Global Contract Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing to gain competitive advantage | +2.3% | Global, highest in North America and Europe | Medium term (2-4 years) |

| Explosive SKU proliferation from e-commerce | +1.9% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Pharma outsourcing for novel biologics | +1.6% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Automation and robotics lowering per-unit cost | +1.4% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Sustainability-led substrate shifts | +1.1% | Europe leading, followed by North America | Long term (≥ 4 years) |

| Near-shoring to mitigate geopolitical risk | +0.6% | North America to Mexico, Europe to Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Outsourcing to Gain Competitive Advantage

Pharmaceutical manufacturers increasingly direct capital toward drug discovery while relying on external partners for highly regulated packaging tasks. FDA guidance on combination products released in 2024 intensified validation, container-closure integrity, and documentation demands, encouraging biologics producers to outsource to specialists such as Catalent, which invested EUR 23 million (USD 27.13 million) in an automated clinical-supply line in Germany. European Medicines Agency rules for advanced therapy medicinal products heighten the complexity further, prompting contract packagers to shoulder compliance risk and technology refresh, shortening launch timelines for sponsors and freeing them from costly facility upgrades.

Explosive SKU Proliferation from E-commerce

Direct-to-consumer channels require shorter runs, frequent artwork variations, and protective designs tuned for parcel networks rather than palletized retail. Flexible manufacturing cells and digital job tickets allow contract packagers to execute more changeovers per shift without inflating set-up costs. Food brands exploit this agility for seasonal flavors and limited editions, while the same lines accommodate eco-friendly substrates that align with online retailers’ emissions goals. Modern workflow software captures traceability data and routes it into enterprise resource planning systems, meeting audit requirements and reducing recall risk.

Pharma Outsourcing for Novel Biologics Packaging

Biologics demand sterile barriers, temperature integrity, and drug-device pairing. Drug delivery patents climbed 28% in 2024, underlining relentless innovation.[2]United States Patent and Trademark Office, “Patent Activity Report – Packaging Technologies 2024,” uspto.gov PCI Pharma Services earmarked USD 365 million for global biologics-ready lines capable of assembling autoinjectors and on-body pumps. Sponsors lacking such infrastructure turn to external partners for speed-to-market and regulatory expertise, with service agreements often spanning clinical and commercial stages.

Automation and Robotics Lowering Per-unit Cost

Collaborative robots, vision systems, and predictive maintenance reduce labor exposure and scrap. Packaging automation patent activity rose 31% in 2024, confirming widespread investment. Continuous operation improves overall equipment effectiveness, allowing providers to quote competitive unit costs yet retain margin integrity. Automated lines generate process data streams that assist FDA and EMA inspections, further differentiating technologically advanced suppliers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent cross-border regulatory compliance | -1.6% | Global, highest in pharma and food sectors | Long term (≥ 4 years) |

| Competition from in-house packaging lines | -1.1% | Developed markets with established infrastructure | Medium term (2-4 years) |

| Volatile resin and energy prices | -0.9% | Global, highest in energy-intensive operations | Short term (≤ 2 years) |

| Mismatch between recycled-content goals and supply | -0.7% | Europe and North America leading sustainability initiatives | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Cross-border Regulatory Compliance

Divergent FDA and European rules compel providers to duplicate validation protocols, label formats, and audit trails. PPWR design standards occasionally clash with U.S. food-contact thresholds, obliging dual inventory or reformulation. Smaller firms struggle to fund the necessary quality teams, enterprise resource planning modules, and serialization infrastructure, limiting their participation in global bids.

Competition from In-house Packaging Lines

High-volume manufacturers, notably in consumer staples, amortize automated lines over large runs, narrowing the price gap with outsourced alternatives. While complexity and sustainability demands still nudge niche products toward specialists, mainstream SKUs remain viable internally, especially when intellectual property protection outweighs outsourcing’s flexibility benefits.

Segment Analysis

By Material Type: Bio-based Polymers Gain Momentum

Plastics retained 55.32% of revenue in 2024 thanks to entrenched supply chains, but recycled-content quotas and brand commitments accelerate a 9.65% CAGR for bio-based and composite materials. The shift calls for extrusion upgrades, compatibilizer know-how, and barrier coatings that preserve shelf life without multilayer laminates. Contract packaging market size allocations to plant-based polymers will expand as PPWR deadlines near, giving providers with formulary expertise a pricing premium.[3]European Commission, “Packaging and Packaging Waste Regulation (PPWR),” environment.ec.europa.eu

Technical complexity widens competitive gaps. Providers with on-site laboratories conduct migration, seal-strength, and shelf-life tests swiftly, shortening approval cycles. Patent filings for biodegradable solutions rose 34% in 2024, underscoring rapid innovation and signaling that material leadership will be pivotal for margin defense.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Packaging Type: Primary Formats Dominate Compliance-Driven Spend

Primary packaging accounted for 57.43% of 2024 revenue and is set for a 9.32% CAGR owing to stringent contact-surface validations required by the FDA and EMA. The contract packaging market share premium arises from container-closure integrity, extractables, and leachables testing, which smaller in-house teams often cannot execute economically.

Secondary packs face margin compression as corrugate and carton converting capacities rise globally, yet remain critical for tamper evidence, brand messaging, and serialization. Tertiary packs evolve with automation; robotic palletizers and warehouse robots drive ergonomic redesigns that improve cube utilization.

By Service Type: Fulfillment Adds End-to-End Value

Filling and assembly represented 36.78% of 2024 spend, reflecting high-volume production runs in food and beverage. Yet fulfillment and logistics will grow 10.34% annually as e-commerce sellers seek single-provider solutions. Providers integrate warehouse management systems, pick-to-light technology, and last-mile carrier APIs, enabling just-in-time runs and postponement strategies that cut client inventory holding costs.

Formulation and blending services advance steadily in pharmaceuticals and personal care, bundling active-ingredient handling with downstream packaging. Serialization, temperature monitoring, and real-time inventory dashboards differentiate partners competing for long-term contracts.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Pharma Leads Value Creation

Pharmaceutical spending, while lower volume than food, delivers a 10.98% CAGR through 2030 as biologics pipelines mature. Contract packaging market size gains reflect specialized needs-sterile environments, cold chain, and device integration-that command premium pricing. Catalent’s German expansion and PCI’s USD 365 million program illustrate the capex scale required to compete.

Food maintained 35.13% revenue in 2024, emphasizing scale and cost efficiency, yet sustainability regulations shift material choice toward fiber-based and mono-PE solutions. Cosmetics and personal care innovate with airless pumps and sensory-driven closures that enhance consumer experience.

Geography Analysis

North America contributed 38.98% of 2024 sales, underpinned by mature pharmaceutical outsourcing and advanced automation adoption. The contract packaging market size in Asia-Pacific is accelerating at 11.52% CAGR, propelled by China’s 8.7% packaging output growth and pro-manufacturing policies.[4]China National Bureau of Statistics, “Industrial Production Statistics – Packaging Manufacturing,” stats.gov.cn India’s vaccine output surge and Japan’s reform of medical device approvals further lift regional demand.

Europe’s growth centers on PPWR compliance, spurring investment in recyclable substrates and digital traceability infrastructure. South America and the Middle East and Africa represent long-horizon opportunities contingent on logistics upgrades and regulatory harmonization.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Mega-mergers reshape the playing field. Novo Holdings’ Catalent deal and Amcor’s Berry Global acquisition create vertically integrated entities wielding expanded R&D, procurement leverage, and cross-regional footprints, making them preferred partners for global launches. Technology investment differentiates contenders: patent filings in packaging automation jumped 31% in 2024, demonstrating the arms race for robotics, machine learning, and vision-guided inspection.

Smaller specialists thrive in niches-high-potency drug filling, eco-design, or connected packaging-yet must form alliances or accept acquisition risk as capital intensity and data requirements escalate. Providers able to pair advanced material science with digital supply chain tools will capture an outsized share of margin expansion.

Contract Packaging Industry Leaders

-

Amcor plc

-

Sonoco Products Company

-

Aaron Thomas Company, Inc.

-

Jones Healthcare Group Inc.

-

Sharp Packaging Services LLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Aptar Group opened a CSP Technologies clinical packaging site in New Jersey, adding cGMP cleanrooms and Activ-Polymer moisture-scavenging technology for drug stability.

- December 2024: Novo Holdings finalized its USD 16.5 billion Catalent acquisition, expanding biologics and drug delivery capacity across 50+ facilities.

- November 2024: Amcor closed a USD 8.43 billion all-stock purchase of Berry Global, targeting USD 650 million annual synergies.

- October 2024: PCI Pharma Services committed USD 365 million to expand drug-device combination packaging in the U.S. and EU.

Global Contract Packaging Market Report Scope

Contract packaging is the process of assembling a product and putting it into its final finished packaging. Depending on the product, the final packaging constitutes a variety of forms, such as thermoformed/plastic clamshell/blister packaging, a plastic bag, a standing corrugated retail point-of-sale display, or a transport tray.

The contract packaging market is segmented by packaging (primary, secondary, and tertiary), end-user industry (food, beverage, pharmaceutical, household and personal care, and other end-user industries), and geography (North America (United States and Canada), Europe (United Kingdom, Germany, France, Netherlands, Italy, Spain, and Rest of Europe), Asia-Pacific (China, India, Japan, and Rest of Asia-Pacific), Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Material Type

| Plastics |

| Paper and Paperboard |

| Metal |

| Glass |

| Bio-based and Composites |

By Packaging Type

| Primary |

| Secondary |

| Tertiary |

By Service Type

| Formulation and Blending |

| Filling and Assembly |

| Packaging and Labeling |

| Fulfillment and Logistics |

| Other Service Types |

By End-User Industry

| Food |

| Beverage |

| Pharmaceutical |

| Cosmetics and Personal Care |

| Industrial |

| Other End-user Industries |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Material Type | Plastics | ||

| Paper and Paperboard | |||

| Metal | |||

| Glass | |||

| Bio-based and Composites | |||

| By Packaging Type | Primary | ||

| Secondary | |||

| Tertiary | |||

| By Service Type | Formulation and Blending | ||

| Filling and Assembly | |||

| Packaging and Labeling | |||

| Fulfillment and Logistics | |||

| Other Service Types | |||

| By End-User Industry | Food | ||

| Beverage | |||

| Pharmaceutical | |||

| Cosmetics and Personal Care | |||

| Industrial | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the contract packaging market in 2025?

The market is valued at USD 79.69 billion in 2025, on a path to USD 120.88 billion by 2030 at an 8.69% CAGR.

Which segment contributes the highest revenue?

Primary packaging leads with 57.43% of 2024 sales due to strict contact-surface compliance requirements.

Which region is growing the fastest?

Asia-Pacific is advancing at an 11.52% CAGR through 2030, fueled by Chinese manufacturing expansion and pharmaceutical outsourcing.

Why are brands outsourcing packaging?

Regulations, SKU complexity, and automation investment needs make specialized providers more cost-effective and compliant than in-house lines.

What drives material innovation in packaging?

PPWR recycled-content mandates and corporate sustainability goals accelerate adoption of bio-based and recyclable substrates.

How is consolidation shaping the competitive landscape?

Mega-mergers such as Novo Holdings–Catalent and Amcor–Berry Global create scale advantages in R&D, procurement, and global service delivery.

Page last updated on: