Cat Food Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Market Size (2026) | USD 66.48 Billion |

| Market Size (2031) | USD 88.65 Billion |

| Growth Rate (2026 - 2031) | 5.93% CAGR |

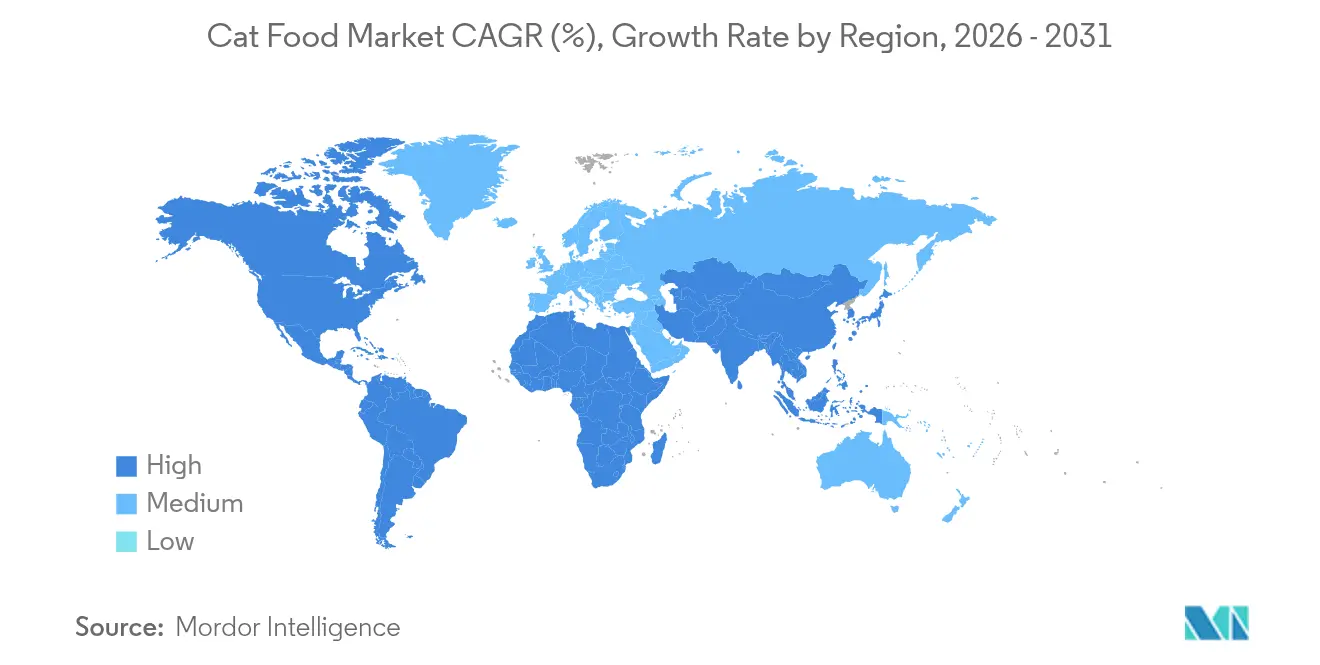

| Fastest Growing Market | South America |

| Largest Market | North America |

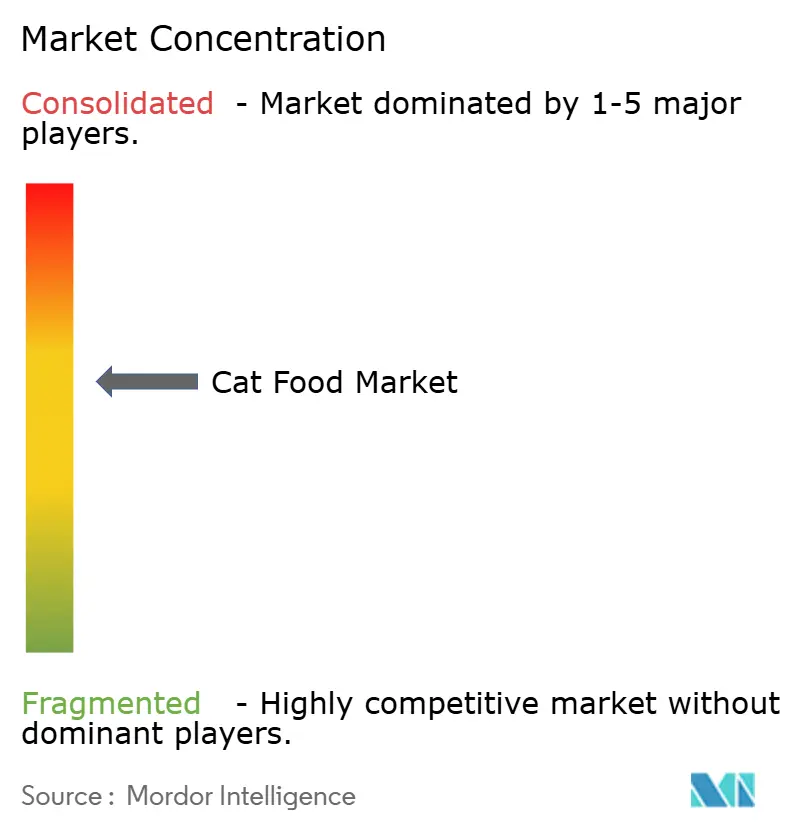

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cat Food Market Analysis by Mordor Intelligence

Cat food market size in 2026 is estimated at USD 66.48 billion, growing from 2025 value of USD 62.76 billion with 2031 projections showing USD 88.65 billion, growing at 5.93% CAGR over 2026-2031. The sustained upswing reflects how owners increasingly view feline nutrition as part of household health spending. Premium formats, subscription-based delivery, and nutraceutical add-ons are outpacing staples as urban, single-person, and senior households channel discretionary income toward cats’ perceived wellness needs. Competitive pressure is rising as direct-to-consumer entrants use data analytics to tailor recipes while incumbents defend shelf presence through brand extensions and acquisitions. Ingredient cost swings, especially for meat and fish, and tightening label rules temper profit visibility but also accelerate protein innovation cycles.

Key Report Takeaways

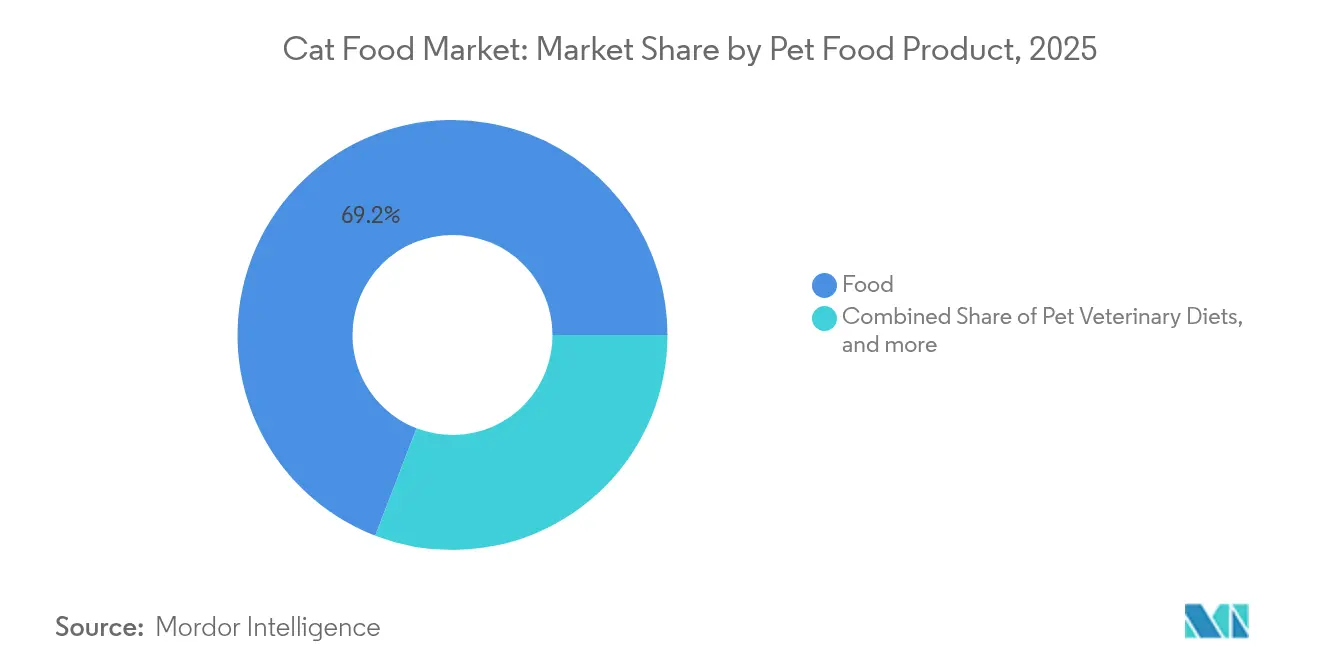

- By pet food product category, food led with a 69.15% revenue share of the cat food market in 2025, and nutraceuticals and supplements are projected to expand at an 7.85% CAGR to 2031.

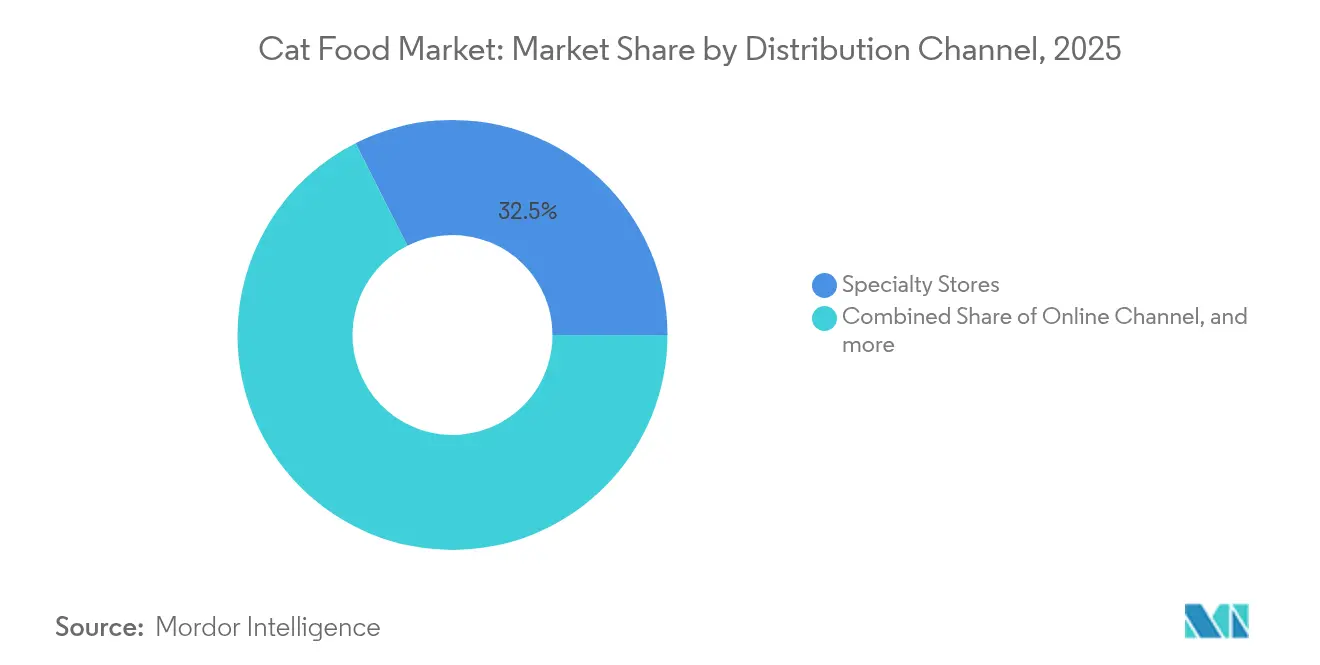

- By distribution channel, specialty stores held a 32.45% market share in the cat food market in 2025, while online channels were projected to have the highest CAGR of 8.05% through 2031.

- By geography, North America accounted for 39.85% of the cat food market size in 2025, and South America is projected to advance at an 7.9% CAGR through 2031.

- The Cat food market exhibits a moderate consolidated structure dominated by global multinational corporations with diverse product portfolios. Mars, Incorporated, Nestle (Purina), Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.), General Mills Inc., and The J.M. Smucker Company are major players, accounting for a 33.1% share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cat Food Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dry-food affordability and shelf-life advantages | +1.2% | Global, with a stronger impact in emerging markets | Long term (≥ 4 years) |

| Rising cat ownership in single-person and senior households | +0.9% | North America and Europe core, expanding to urban Asia-Pacific | Medium term (2-4 years) |

| Premiumization of wet and soft-natural formats | +1.1% | North America and Europe, early adoption in Japan and Australia | Medium term (2-4 years) |

| Surge in e-commerce and DTC subscription models | +0.8% | Global, led by North America and urban Asia-Pacific markets | Short term (≤ 2 years) |

| Novel-protein adoption (insect and single-cell) | +0.4% | Europe and North America are early adoption, gradual global expansion | Long term (≥ 4 years) |

| AI-driven personalization of feline nutrition plans | +0.3% | North America and Europe, tech-forward urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Dry-Food Affordability and Shelf-Life Advantages

Inflationary budgets accentuate dry formulations’ cost-per-serving edge, often lower than wet equivalents. Long shelf life reduces waste and supports bulk buying, a priority for multi-cat homes. Emerging-market retailers use vacuum-seal packaging and nitrogen flushing to keep kibble fresh, narrowing the sensory gap versus premium wet fare. Flavor-coated kibbles now feature poultry-fat drizzle technology that lifts palatability scores in in-house trials, reinforcing value and taste in a single proposition.

Rising Cat Ownership in Single-Person and Senior Households

Demographic shifts toward smaller household sizes and aging populations are creating distinct consumption patterns that favor premium cat food categories. Senior citizens exhibit similar premium purchasing behaviors while showing a preference for wet food formats that align with their cats' changing nutritional needs. This demographic convergence is reshaping product development priorities toward smaller package sizes, enhanced digestibility, and age-specific formulations. The trend is particularly evident in urban markets where apartment living and delayed family formation extend the period of intensive pet investment.

Premiumization of Wet and Soft-Natural Formats

Consumer willingness to pay premium prices for wet and soft-natural cat food formats reflects deeper shifts in pet care philosophy in 2024, with 67% of cat owners now viewing nutrition as preventive healthcare rather than basic sustenance [1]Source: “Premium pet food market grows as owners prioritize health,” Wall Street Journal, wsj.com. Hydration benefits, recognizable ingredients, and grain-free labels justify price premiums. Manufacturers secure a supply of cage-free poultry and line-caught fish to satisfy traceability audits, while adopting retortable recyclable pouches that lower carbon footprint claims.

Surge in E-Commerce and DTC Subscription Models

Direct-to-consumer brands are leveraging subscription economics to offer personalized nutrition plans, automated delivery schedules, and premium positioning at competitive price points through the elimination of traditional retail margins. This channel shift is particularly pronounced among millennial and Gen Z pet owners who prioritize convenience and are comfortable with recurring payment models. Established manufacturers are responding through hybrid strategies that combine traditional retail presence with proprietary e-commerce platforms and strategic partnerships with subscription services. The trend is supported by improved cold-chain logistics and packaging technologies that maintain product integrity during direct shipment.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile meat and ocean-fish input costs | -0.7% | Global, with a higher impact in import-dependent regions | Short term (≤ 2 years) |

| Stringent global labeling and FSMA-style regulations | -0.4% | North America and Europe core, expanding globally | Medium term (2-4 years) |

| Premium price sensitivity during inflationary periods | -0.6% | Global, with a higher impact in emerging markets | Short term (≤ 2 years) |

| High carbon-footprint scrutiny on beef-based recipes | -0.2% | Europe and North America, early concerns in Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Meat and Ocean-Fish Input Costs

Chicken meal prices swung in 2024 as avian flu disrupted supply chains, while tuna and salmon faced quota limits tied to climate-driven stock declines. Smaller brands without hedging tools suffered margin compressions, fueling consolidation talk. Ingredient substitution with poultry by-products steadied costs but raised palatability concerns that required intensified flavor system investment. The volatility is most acute for smaller manufacturers lacking procurement scale and hedging capabilities, potentially accelerating industry consolidation as cost pressures mount.

Premium Price Sensitivity During Inflationary Periods

This price sensitivity is most pronounced in emerging markets and among lower-income demographics, where pet food represents a larger share of discretionary spending. Premium brands are responding through value-engineering initiatives, including smaller package sizes, promotional pricing, and loyalty programs designed to maintain customer relationships during economic stress. The challenge is particularly acute for super-premium segments where price elasticity is higher and switching costs are lower compared to prescription or veterinary diet categories.

Segment Analysis

By Pet Food Product: Food Dominates Despite Nutraceutical Surge

Food products generated 69.15% of 2025 revenue, giving them the largest slice of the cat food market. Nutraceuticals and supplements are projected to expand at an 7.85% CAGR to 2031. Within this base, dry kibble provided scale, but wet formats captured higher per-unit spend as owners embraced hydration narratives. Pet nutraceuticals, although smaller in scale, are increasing their contribution to the cat food market size and influencing cross-merchandising with main meals. Digestive supplements combining probiotics and omega-3 gels demonstrate the convergence of therapeutic benefits and consumer treats, challenging traditional categorizations. Treats are increasingly used as training aids, with freeze-dried poultry dice priced significantly higher per ounce compared to average kibble. Despite the premium pricing, these products maintain a strong sales performance in specialty aisles that emphasize natural offerings.

Veterinary diets, a niche of the broader cat food market, deliver premium margins under digestive and urinary care lines that veterinarians prescribe, making them resilient to general trade-down pressures. Dry recipes utilize twin-screw extrusion efficiency, resulting in lower energy consumption per pound compared to retort wet lines, which supports ESG reporting goals. Conversely, wet lines innovate around recyclable aluminum trays and reclosable plastic cups, aligning with consumer demands for waste reduction. Brands that integrate functional botanicals cranberry for urinary tract support or turmeric for joint health, add a second layer of value capture without cannibalizing base feeding occasions.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Specialty Stores Lead While Digital Accelerates

Specialty outlets secured 32.45% of 2025 sales and remain consultative hubs where trained staff hand-sell novel proteins and breed-specific SKUs, deepening consumer knowledge and loyalty. Yet online’s 8.05% CAGR outruns all other channels, funneling growth to the cat food market through subscription engines that automate basket replenishment. Supermarkets and hypermarkets maintain reach for impulse and price-sensitive purchases but lose premium share due to constrained shelf sets. Convenience stores gain relevance in urban cores by carrying single-serve pouches that fit micro-kitchens and address just-in-time consumption.

E-commerce platforms employ AI to suggest cross-sell items such as litter delivered in the same box, raising average order values. Successful omnichannel models let owners order heavy kibble online for doorstep drop while still visiting specialists for treat sampling and nutrition advice. Retail media networks monetize search placement fees, creating a new battleground for visibility between legacy brands and DTC challengers.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America captured 39.85% of the 2025 value. United States households display high spending per cat and early adoption of subscription services, boosting the cat food market size ahead of other regions. Canada mirrors the trend with rapid natural and organic uptake, while Mexico’s rising middle class and cross-border e-commerce inflows pull premium cans into supermarkets.

South America posts the fastest growth rate of 7.9%. Brazil anchors growth by pairing its domestic protein supply with improved logistics networks that transport chilled products to interior cities. Argentine consumers tend to lean toward European-style pâtés and grain-free recipes, reflecting cultural palate preferences. Currency volatility prompts manufacturers to localize inputs whenever possible, thereby stabilizing pricing and safeguarding volumes.

Asia-Pacific occupies a dynamic middle ground. China’s urban households transition from table scraps to complete diets, making it the largest incremental contributor to the cat food market. Local factories co-pack for global players, lowering tariff exposure. Japan and Australia focus on innovations in single-source protein claims, while India explores early-stage growth with entry-level kibble products positioned for value but gradually targeting premium segments as incomes rise.

Competitive Landscape

The Cat food market exhibits a moderate consolidated structure dominated by global multinational corporations with diverse product portfolios. Mars, Incorporated, Nestle (Purina), Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.), General Mills Inc., and The J.M. Smucker Company are major players, accounting for a 33.5% share in 2024. Each leverages multi-brand portfolios that span economy to prescription lines, securing shelf breadth and veterinary trust. Acquisitions such as Purina’s 2024 purchase of Tailored Pet bring AI personalization assets into traditional factories, blending mass scale with niche agility[2]Source: “Pet food startups challenge big brands with personalized nutrition,” Wall Street Journal, wsj.com.

Blue Buffalo, Wellness Pet Company, and Unicharm are challenging established players by promoting limited-ingredient or raw-inspired offerings that align with the trend toward premiumization. Technology is driving the next phase of development. Patent filings covering hydrolyzed insect meal extrusion and time-release kibble coatings indicate a race for differentiation[3]Source: “Patent database search results for pet food innovations,” USPTO, uspto.gov. Supply-chain digital twins help major companies hedge against raw material swings and reduce lead times.

Sustainability metrics enter brand valuation, firms publicize water-use reductions or recyclable-pack targets to court eco-minded customers and regulators. Barriers to entry persist. Meeting AAFCO nutrient sufficiency and FSMA hazard-analysis mandates requires laboratory investment that raises start-up thresholds. Yet digital storytelling lowers marketing costs, letting niche DTC newcomers gain awareness quickly, pressuring legacy advertising budgets.

Cat Food Industry Leaders

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

Mars Incorporated

Nestle (Purina)

The J. M. Smucker Company

General Mills Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Mars invested USD 2 billion to expand its food and pet care manufacturing facilities in the United States. The expansion includes a USD 240 million Nature's Bakery facility in Utah and a USD 450 million Royal Canin manufacturing site in Ohio.

- February 2025: Colgate-Palmolive Company acquired Care TopCo Pty Ltd, the owner of Australian pet food brand Prime100. The acquisition aligns with Colgate's strategy to expand its Hill's Pet Nutrition division into the fresh pet food segment, including cat food. This purchase enhances Hill's existing specialty pet food portfolio and expands its market presence in Australia.

- November 2024: General Mills acquired the North American assets of Whitebridge, which includes premium cat food brands Tiki Pets and Cloud Star, for USD 1.45 billion.

Global Cat Food Market Report Scope

Food, Pet Nutraceuticals/Supplements, Pet Treats, Pet Veterinary Diets are covered as segments by Pet Food Product. Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets are covered as segments by Distribution Channel. Africa, Asia-Pacific, Europe, North America, South America are covered as segments by Region.| Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | ||||

| Wet Pet Food | ||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | ||

| Omega-3 Fatty Acids | ||||

| Probiotics | ||||

| Proteins and Peptides | ||||

| Vitamins and Minerals | ||||

| Other Nutraceuticals | ||||

| Pet Treats | By Sub Product | Crunchy Treats | ||

| Dental Treats | ||||

| Freeze-dried and Jerky Treats | ||||

| Soft & Chewy Treats | ||||

| Other Treats | ||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | ||

| Diabetes | ||||

| Digestive Sensitivity | ||||

| Obesity Diets | ||||

| Oral Care Diets | ||||

| Renal | ||||

| Urinary tract disease | ||||

| Other Veterinary Diets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| Africa | By Country | South Africa |

| Rest of Africa | ||

| Asia-Pacific | By Country | Australia |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Malaysia | ||

| Philippines | ||

| Taiwan | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Europe | By Country | France |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Poland | ||

| Russia | ||

| Spain | ||

| United Kingdom | ||

| Rest of Europe | ||

| North America | By Country | Canada |

| Mexico | ||

| United States | ||

| Rest of North America | ||

| South America | By Country | Argentina |

| Brazil | ||

| Rest of South America |

| By Pet Food Product | Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | |||||

| Wet Pet Food | |||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | |||

| Omega-3 Fatty Acids | |||||

| Probiotics | |||||

| Proteins and Peptides | |||||

| Vitamins and Minerals | |||||

| Other Nutraceuticals | |||||

| Pet Treats | By Sub Product | Crunchy Treats | |||

| Dental Treats | |||||

| Freeze-dried and Jerky Treats | |||||

| Soft & Chewy Treats | |||||

| Other Treats | |||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | |||

| Diabetes | |||||

| Digestive Sensitivity | |||||

| Obesity Diets | |||||

| Oral Care Diets | |||||

| Renal | |||||

| Urinary tract disease | |||||

| Other Veterinary Diets | |||||

| By Distribution Channel | Convenience Stores | ||||

| Online Channel | |||||

| Specialty Stores | |||||

| Supermarkets/Hypermarkets | |||||

| Other Channels | |||||

| By Geography | Africa | By Country | South Africa | ||

| Rest of Africa | |||||

| Asia-Pacific | By Country | Australia | |||

| China | |||||

| India | |||||

| Indonesia | |||||

| Japan | |||||

| Malaysia | |||||

| Philippines | |||||

| Taiwan | |||||

| Thailand | |||||

| Vietnam | |||||

| Rest of Asia-Pacific | |||||

| Europe | By Country | France | |||

| Germany | |||||

| Italy | |||||

| Netherlands | |||||

| Poland | |||||

| Russia | |||||

| Spain | |||||

| United Kingdom | |||||

| Rest of Europe | |||||

| North America | By Country | Canada | |||

| Mexico | |||||

| United States | |||||

| Rest of North America | |||||

| South America | By Country | Argentina | |||

| Brazil | |||||

| Rest of South America | |||||

Market Definition

- FUNCTIONS - Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. The scope includes the food and supplements consumed by pets including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

- RESELLERS - Companies engaged in reselling of pet food without value addition have been excluded from the market scope, in order to avoid double counting.

- END CONSUMERS - Pet owners are considered to be the end-consumers in the market studied.

- DISTRIBUTION CHANNELS - Supermarkets/hypermarkets, specialty stores, convenience stores, online channels and other channels are considered within the scope. The stores which are exclusively providing pet related basic and custom products are considered within the scope of specialty stores.

| Keyword | Definition |

|---|---|

| Pet Food | The scope of pet food includes the food that is eatable by pets including food, treats, veterinary diets, and nutraceuticals/supplements. |

| Food | Food is animal feed intended for consumption by pets. It is formulated to provide essential nutrients and meet the dietary needs of various types of pets, including dogs, cats, and other animals. These are generally segmented into dry and wet pet foods. |

| Dry Pet Food | Dry pet foods may be extruded/baked (kibbles) or flaked. They have a lower moisture content, typically around 12-20%. |

| Wet Pet Food | Wet pet food, also known as canned pet food or moist pet food, generally has a higher moisture content compared to dry pet food, often ranging from 70-80%. |

| Kibbles | Kibbles are dry, processed pet food in small, bite-sized pieces or pellets. They are specifically formulated to provide balanced nutrition for various domestic animals, such as dogs, cats, and other animals. |

| Treats | Pet Treats are special food items or rewards given to pets, to show affection, and encourage good behavior. They are especially used during training. Pet treats are made from various combinations of meat or meat-derived materials with other ingredients. |

| Dental Treats | Pet dental treats are specialized treats that are formulated to promote good oral hygiene in pets. |

| Crunchy Treats | It is a type of pet treat that has a firm and crispy texture which can be a good source of nutrition for pets. |

| Soft and chewy treats | Soft and Chewy pet treats are a type of pet food product that is formulated to be easy to chewy and digest. They are usually made from soft and pliable ingredients, such as meat, poultry, or vegetables, that have been blended and formed into bite-sized pieces or strips. |

| Freeze-dried & Jerky Treats | Freeze-dried and jerky treats are snacks given to pets, that are prepared through a special preservation process, without damaging the nutritional content, resulting in long-lasting, nutrient-rich treats. |

| Urinary Tract Disease Diets | These are commercial diets that are specifically formulated to promote urinary health and reduce the risk of urinary tract infections and other urinary problems. |

| Renal Diets | These are specialized pet foods formulated to support the health of pets with kidney disease or renal insufficiency. |

| Digestive Sensitivity Diets | Digestive-sensitive diets are specially formulated to meet the nutritional needs of pets with digestive issues such as food intolerances, allergies, and sensitivities. These diets are designed to be easily digestible and to reduce the symptoms of digestive problems in pets. |

| Oral Care Diets | Oral care diets for pets are specially formulated diets produced to promote oral health and hygiene in pets. |

| Grain-Free Pet Food | Pet food that does not contain common grains like wheat, corn, or soy. Grain-free diets are often preferred by pet owners seeking alternative options or if their pets have specific dietary sensitivities. |

| Premium Pet Food | High-quality pet food formulated with superior ingredients often offers additional nutritional benefits compared to standard pet food. |

| Natural Pet Food | Pet food made from natural ingredients, with minimal processing and without artificial preservatives. |

| Organic Pet Food | Pet food is produced using organic ingredients, free from synthetic pesticides, hormones, and genetically modified organisms (GMOs). |

| Extrusion | A manufacturing process used to produce dry pet food, where ingredients are cooked, mixed, and shaped under high pressure and temperature. |

| Other Pets | Other pets include birds, fish, rabbits, hamsters, ferrets, and reptiles. |

| Palatability | The taste, texture, and aroma of pet food influence its appeal and acceptance by pets. |

| Complete and Balanced Pet Food | Pet food that provides all essential nutrients in appropriate proportions to meet the nutritional needs of pets without additional supplementation. |

| Preservatives | These are the substances that are added to pet food to extend its shelf life and prevent spoilage. |

| Nutraceuticals | Food products that offer health benefits beyond basic nutrition, often contain bioactive compounds with potential therapeutic effects. |

| Probiotics | Live beneficial bacteria that promote a healthy balance of gut flora, supporting digestive health and immune function in pets. |

| Antioxidants | Compounds that help neutralize harmful free radicals in the body, promoting cellular health and supporting the immune system in pets. |

| Shelf-Life | The duration of which pet food remains safe and nutritionally viable for consumption after its production date. |

| Prescription diet | Specialized pet food formulated to address specific medical conditions under veterinary supervision. |

| Allergen | A substance that can cause allergic reactions in some pets, leading to food allergies or sensitivities. |

| Canned food | Wet pet food that is packed in cans and contains higher moisture content than dry food. |

| Limited ingredient diet (LID) | Pet food formulated with a reduced number of ingredients to minimize potential allergens. |

| Guaranteed Analysis | The minimum or maximum levels of certain nutrients present in pet food. |

| Weight management | Pet food designed to help pets maintain a healthy weight or support weight loss efforts. |

| Other Nutraceuticals | It includes prebiotics, antioxidants, digestive fiber, enzymes, essential oils and herbs. |

| Other Veterinary Diets | It includes weight management diets, skin and coat health, cardiac care, and joint care. |

| Other Treats | It includes rawhides, mineral blocks, lickables, and catnips. |

| Other Dry Foods | It includes cereal flakes, mixers, meal toppers, freeze-dried foods, and air-dried foods. |

| Other Animals | It includes birds, fish, reptiles, and small animals (rabbits, ferrets, hamsters). |

| Other Distribution Channels | It includes veterinary clinics, local unregulated stores, and feed and farm stores. |

| Proteins and Peptides | Proteins are large molecules composed of basic units called amino acids which help in the growth and development of pets. Peptides are the short string of 2 to 50 amino acids. |

| Omega-3 fatty acids | Omega-3 fatty acids are essential polyunsaturated fats that play a crucial role in the overall health and well-being of Pets |

| Vitamins | Vitamins are the essential organic compounds that are essential for vital physiological functioning. |

| Minerals | Minerals are naturally occurring inorganic substances that are essential for various physiological functions in pets. |

| CKD | Chronic Kidney Disease |

| DHA | Docosahexaenoic Acid |

| EPA | Eicosapentaenoic Acid |

| ALA | Alpha-linolenic Acid |

| BHA | Butylated Hydroxyanisol |

| BHT | Butylated Hydroxytoluene |

| FLUTD | Feline Lower Urinary Tract Disease |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms