Market Overview

| Study Period | 2020 - 2031 |

|---|---|

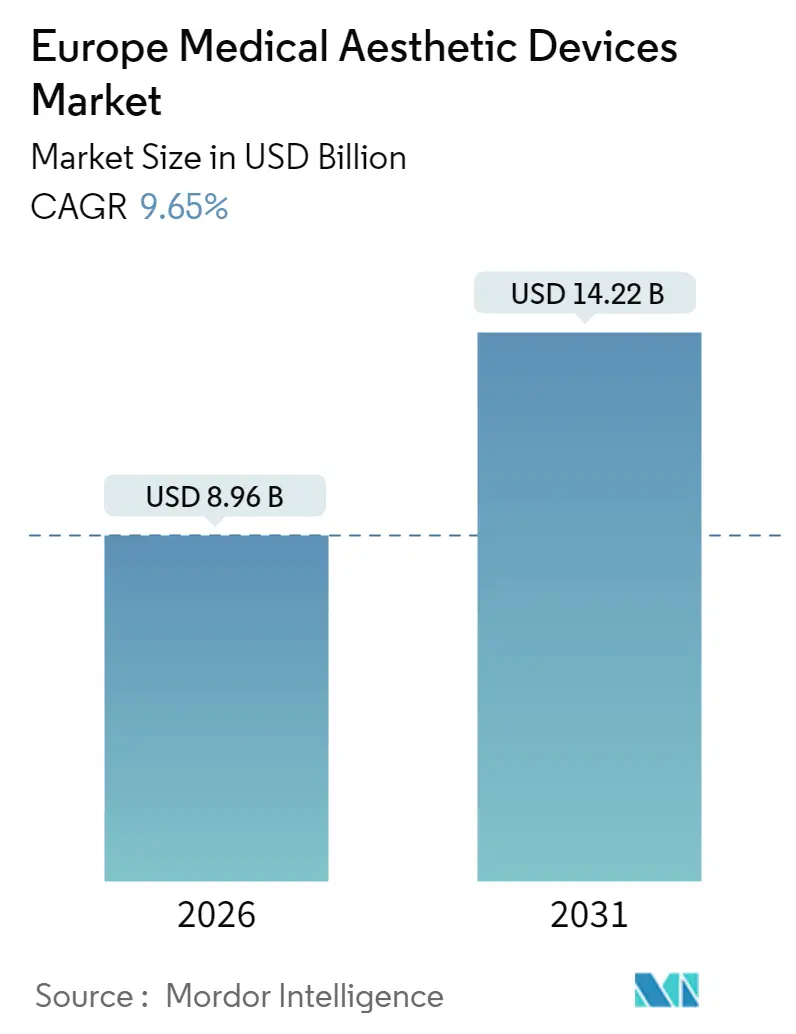

| Market Size (2026) | USD 8.96 Billion |

| Market Size (2031) | USD 14.22 Billion |

| Growth Rate (2026 - 2031) | 9.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Medical Aesthetic Devices Market Analysis by Mordor Intelligence

The Europe medical aesthetic devices market is expected to grow from USD 8.17 billion in 2025 to USD 8.96 billion in 2026 and is forecast to reach USD 14.22 billion by 2031 at 9.65% CAGR over 2026-2031. A well-established healthcare ecosystem, strict but transparent European Union Medical Device Regulation (MDR) rules and a widening consumer shift toward minimally invasive cosmetic care combine to create a growth profile that consistently outpaces traditional device categories. Energy-based platforms remain the anchor of the Europe medical aesthetic devices market, yet continuous product refresh cycles in injectables and threads are broadening the competitive field. Consolidation among suppliers and clinic chains is rising as private equity capital targets scalable service models. Meanwhile, cross-border medical tourism, especially within the Schengen area, reinforces the quality premium attached to compliant European providers even as it exposes gaps in postoperative follow-up care.

Key Report Takeaways

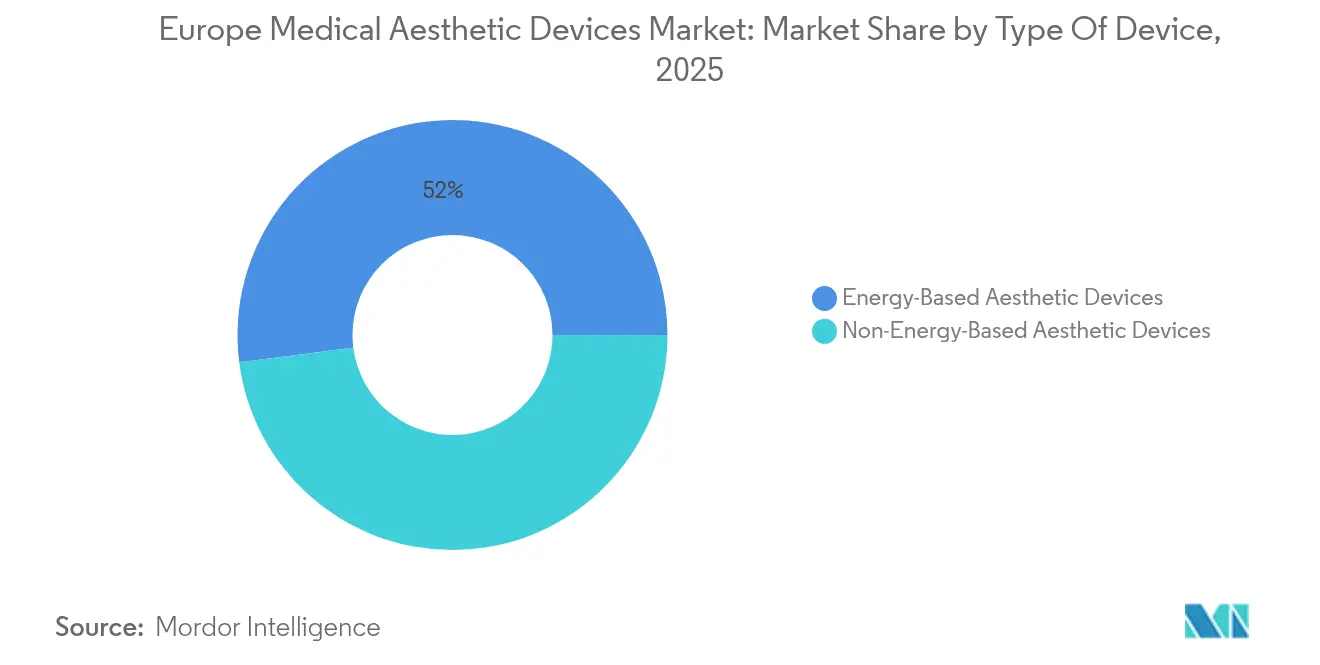

- By type of device, energy-based platforms held 52.02% of the Europe medical aesthetic devices market share in 2025, while non-energy systems are on track for an 11.53% CAGR to 2031.

- By procedure, non-surgical and minimally invasive options accounted for 55.21% of the Europe medical aesthetic devices market size in 2025; surgical interventions are projected to rise at a 10.84% CAGR through 2031.

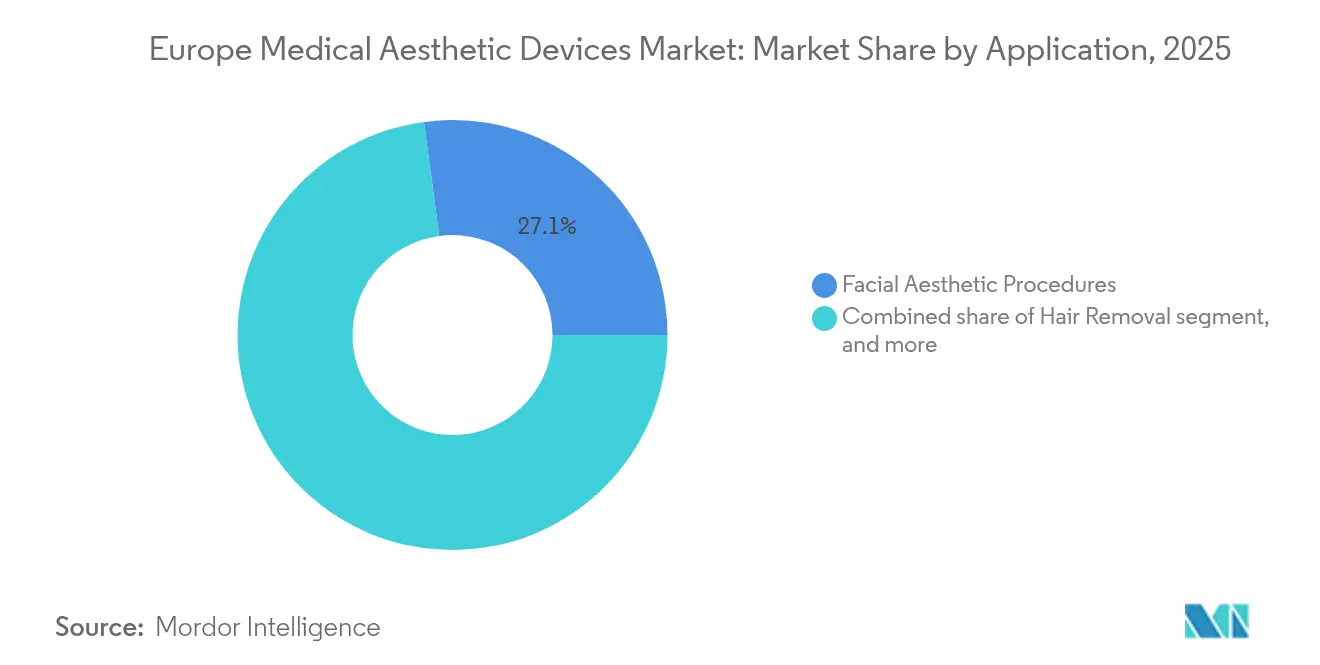

- By application, facial aesthetics represented 27.12% of 2025 revenue, but body contouring shows the fastest trajectory with an 11.62% CAGR toward 2031.

- By end user, clinics and dermatology offices led with 46.05% of revenue in 2025, as medical spas post the strongest forecast growth at 11.75% CAGR.

- By geography, Germany secured 22.07% of regional revenue in 2025, whereas Spain is positioned for a 10.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Medical Aesthetic Devices Market Trends and Insights

Driver Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising obesity prevalence | +1.8% | Germany, UK | Medium term (2-4 years) |

| Growing demand for minimally invasive procedures | +2.4% | France, Italy | Short term (≤ 2 years) |

| Rapid technological advancements in aesthetic devices | +1.9% | Germany, UK | Long term (≥ 4 years) |

| Aging population and increasing disposable income | +2.1% | Western Europe, expanding East | Long term (≥ 4 years) |

| Stringent European regulatory standards encouraging premium devices | +0.8% | EU-wide, UK spillover | Medium term (2-4 years) |

| Expansion of medical aesthetic tourism intra-Europe | +1.2% | Southern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Obesity Prevalence

Adult obesity now tops 25% in several EU states, fueling demand for body-contouring and cellulite-reduction technologies. In Germany, the number of energy-based fat-reduction procedures climbed 190.5% between 2011 and 2024, a change closely linked to the uptake of radiofrequency and cryolipolysis systems[1]Dirk Rolf Smoller et al., “Non-Surgical Body Contouring Trends in Germany,” Springer, springer.com. Clinics leverage this demographic shift by bundling weight-management advice with non-surgical treatments, appealing to patients seeking wellness as much as aesthetics. Germany and France also benefit from intra-European medical travelers who prefer EU safety standards for high-ticket procedures.

Growing Demand for Minimally Invasive Procedures

Reduced downtime and favorable safety profiles continue to pull patients toward injectable and device-based therapies. The International Society of Aesthetic Plastic Surgery reports that neuromodulator and dermal-filler sessions rose for a sixth straight year across Europe[2]International Society of Aesthetic Plastic Surgery, “Global Survey 2024,” pubmed.ncbi.nlm.nih.gov. Device makers respond by rolling out multi-modal energy systems able to combine radiofrequency with pulsed light in one pass, thereby widening the non-surgical toolkit. Medical spas capture a large share of this traffic because they can schedule evening and weekend appointments, satisfying time-pressed professionals.

Rapid Technological Advances in Aesthetic Devices

Artificial-intelligence-guided high-intensity focused ultrasound (HIFU) enables operators to visualize dermal layers in real time for consistent outcomes. Hybrid laser workstations now mix ablative and non-ablative wavelengths, letting practitioners tailor protocols by skin type while keeping discomfort low. Consumer-grade radiofrequency handsets—approved for at-home maintenance—expand the addressable base beyond clinic visitors, though physician oversight remains preferred for first-time treatments.

Aging Population and Increasing Disposable Income

Europe’s 50-65-year-old cohort, the fastest-growing segment of the population, drives steady demand for treatments that correct volume loss and skin laxity. Higher disposable income supports repeat procedures and premium device choices, especially in Western Europe. Eastern European markets are catching up as wage growth improves affordability and social media normalizes cosmetic enhancement, widening the reach of the Europe medical aesthetic devices market.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited reimbursement for elective procedures | -1.4% | Northern Europe | Medium term (2-4 years) |

| High capital and treatment costs | -1.1% | Europe-wide | Short term (≤ 2 years) |

| Sustainability concerns over single-use consumables | -0.6% | Western Europe | Long term (≥ 4 years) |

| Regulatory ambiguity for novel injectable fillers | -0.9% | EU-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement for Elective Procedures

Public health systems rarely cover elective esthetic care, leaving patients to self-finance treatments. This dynamic places a natural ceiling on price points that independent practitioners can charge, particularly in Northern Europe, and encourages the spread of installment payment plans offered directly by clinics. Device makers respond by offering lease and revenue-share models to lower capital hurdles for new entrants.

High Capital and Treatment Costs

An advanced energy platform can cost EUR 500,000, a bar too high for many single-physician practices. Larger clinic chains therefore capture volume discounts and higher margins, a trend that fosters acquisition by private-equity groups hunting scalable roll-up opportunities. Manufacturers are experimenting with modular systems that allow providers to add handpieces over time, reducing initial outlay without diluting treatment breadth.

Segment Analysis

By Type of Device: Energy Platforms Drive Innovation

Energy-based systems generated 52.02% of 2025 revenue, securing the largest Europe medical aesthetic devices market share on the back of lasers, radiofrequency and HIFU platforms that target a broad range of indications. Laser sub-segments are evolving toward fractional and hybrid modes that minimize downtime yet maintain efficacy, supporting repeat-business models for clinics. In parallel, radiofrequency devices leverage temperature-controlled handpieces to promote neocollagenesis without epidermal damage, appealing to patients with higher Fitzpatrick skin scores. The Europe medical aesthetic devices market size for non-energy tools is smaller today yet poised for faster expansion, with an 11.53% CAGR tied to next-generation neuromodulators and cross-linked hyaluronic-acid fillers. Ready-to-use botulinum toxin liquids such as Galderma’s Relfydess offer predictable dosing and quicker turnover times, advantages that resonate in high-volume practices. Mechanical options like microdermabrasion retain a foothold as entry-level services, while newer thread-lift materials improve tensile strength and longevity.

A secondary shift is emerging toward portable fractional laser heads that lower space requirements and broaden mobile-clinic concepts in rural Europe. Suppliers also report rising interest in sustainability features, from recyclable cartridges to software updates that extend device lifespan, reflecting environmental priorities in Western European regulations. Collectively these advances preserve the dominance of energy platforms while ensuring non-energy alternatives keep pace through innovation rather than price competition.

Note: Segment shares of all individual segments available upon report purchase

By Procedure Type: Minimally Invasive Dominance

Non-surgical modalities accounted for 55.21% of 2025 revenue, cementing their role as first-line aesthetic options across Europe. Integration of ultrasound and optical guidance lets operators target sub-dermal layers with millimetric precision, elevating outcomes so that many patients now skip entry-level surgery altogether. Combination packages—such as neuromodulators plus fractional RF—deliver multidimensional rejuvenation in fewer visits, a format that pays off in patient satisfaction scores and clinic occupancy metrics. Price transparency and shorter recovery windows further anchor non-surgical share within the Europe medical aesthetic devices market.

Surgical procedures, though smaller in absolute terms, will climb at a 10.84% CAGR as techniques become less invasive. Examples include micro-textured silicone implants for breast augmentation and energy-assisted liposuction devices that streamline fat emulsification. Surgeons increasingly adopt energy instruments intra-operatively, blending traditional cutting skills with device-based tissue management to speed healing. Collectively, the surgical arena retains its importance for clients seeking dramatic reshaping, but the threshold for choosing surgery over devices continues to rise as non-invasive efficacy improves.

By Application: Facial Treatments Lead Market

Facial indications remained the largest revenue generator at 27.12% in 2025. Social-media visibility and remote-working video calls intensify attention to facial appearance, supporting steady appointment cycles for neuromodulators, fractional lasers and radiofrequency micro-needling. The hybrid-laser class offers simultaneous texture smoothing and pigment correction, helping clinics market single-visit “total face” packages. Within the Europe medical aesthetic devices market size for facial care, providers differentiate on combination sequencing and post-procedure skincare, reinforcing brand loyalty.

Body contouring is the breakout category, projected to grow 11.62% annually. Radiofrequency fat-melting applicators and cryolipolysis paddles that can treat multiple zones simultaneously cut session times and broaden throughput, appealing to busy clinics. Recent obesity statistics bolster patient interest in non-surgical fat reduction, particularly among 30- to 50-year-olds seeking incremental improvements rather than bariatric surgery. Hair-removal devices maintain a mature, replacement-driven cycle, while fractional CO₂ lasers for skin resurfacing find renewed demand among older cohorts looking to correct chronic photodamage.

Note: Segment shares of all individual segments available upon report purchase

By End User: Clinics Maintain Leadership

Clinics and dermatology offices captured 46.05% of 2025 revenue, benefitting from medical credibility and the ability to integrate prescription-grade skincare and regenerative injectables with device services. Dermatologists routinely upsell add-on services, ranging from platelet-rich plasma to topical antioxidants, deepening revenue per visit. The Europe medical aesthetic devices market shows that insurance-funded dermatology units now dedicate separate rooms to elective procedures, ensuring clear separation from reimbursable services.

Medical spas, forecast to expand at 11.75% CAGR, blend hospitality cues with clinical oversight. Extended evening hours, membership plans and wellness add-ons such as IV therapy help spas attract clients who view aesthetics as part of a broader self-care routine. Hospital-based plastic-surgery departments remain active for higher-acuity interventions, while consumer-approved home devices gain share for maintenance between office visits, nudging overall market expansion rather than cannibalizing clinic revenue.

Geography Analysis

Germany led regional sales with a 22.07% share in 2025, powered by robust disposable incomes and a medical-device manufacturing heritage that accelerates technology adoption. German clinics frequently serve as early adopters for CE-marked innovations, giving domestic patients first access to upgraded platforms. Cross-border visitors from Eastern Europe and the Middle East further enlarge addressable procedure volumes, as they perceive German regulatory oversight as a safety guarantee.

The United Kingdom commands strong demand despite post-Brexit certification adjustments. London-based chains see steady international inflows, partly because English remains the lingua franca for medical tourism. However, the National Health Service continues to report resource burdens from complications linked to lower-cost overseas procedures, underlining the need for thorough follow-up protocols. France positions aesthetic care as a lifestyle extension of its luxury brand ecosystem, prompting clinics to emphasize subtle, natural-looking outcomes compatible with local beauty sensibilities. Southern Europe exhibits the fastest growth. Spain is forecast to achieve a 10.09% CAGR through 2031, thanks to clinic clusters along the Mediterranean coast that package procedures with holiday stays. Regulatory clarity and competitive pricing make Spain a magnet for Northern European clients seeking warm-weather recovery. Italy leverages its fashion capital status to sustain high procedure frequencies in Milan and Rome, while smaller cities grow through franchised medical-spa concepts. Eastern European nations, notably Poland and the Czech Republic, display double-digit unit growth as rising salaries intersect with broader social acceptance of cosmetic enhancement.

Competitive Landscape

Competition in the Europe medical aesthetic devices market is moderate but tightening. Large multinationals hold broad multi-modality portfolios that cover lasers, radiofrequency, ultrasound and injectables, allowing cross-selling to existing accounts. Mergers such as the 2024 Cynosure-Lutronic tie-up combine complementary laser and IPL technologies, strengthening negotiating power with pan-European clinic chains. Device suppliers now compete on post-sale services—ranging from marketing toolkits to AI-driven treatment-planning software—rather than hardware alone.

Private-equity interest remains high; annual deal counts exceeded 50 transactions for three straight years. Investors favor regional clinic platforms able to standardize protocols and spread capital expenditure across multiple sites, compressing payback periods for premium systems. Manufacturers court these networks with fleet-pricing contracts and leasing models that tie monthly fees to handpiece usage, aligning incentives between builder and operator.

Clinical-evidence generation is a core differentiator. EU MDR mandates stronger post-market surveillance, prompting suppliers to sponsor long-term safety and efficacy studies. Firms also run physician-training academies, often co-located with flagship clinics in Frankfurt, Paris or Milan, to ensure best-practice adoption and reduce complication rates. An emerging frontier is at-home or “prosumer” devices cleared for maintenance treatments, a space where traditional clinical brands compete with new entrants specializing in connected skincare gadgets.

Europe Medical Aesthetic Devices Industry Leaders

AbbVie Inc (Allergan Aesthetics)

Galderma SA

Johnson & Johnson (Mentor Worldwide LLC)

Merz Pharma GmbH & Co. KGaA

Sisram Medical (Alma Lasers)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Galderma posted Q1 net sales of USD 1.129 billion, up 8.3% year-on-year, driven by injectable aesthetics momentum and the rollout of Nemluvio and Relfydess.

- April 2025: Bausch Health gained Health Canada clearance for Solta Medical’s Thermage FLX, offering 25% faster radiofrequency skin-tightening sessions.

- March 2025: Cutera began a pre-packaged Chapter 11 plan that will cut debt by nearly USD 400 million and inject USD 65 million in new capital.

- January 2025: Allergan Aesthetics introduced the AA Signature Program at IMCAS 2025 to promote holistic facial-assessment protocols using its expanded product line.

- August 2024: L’Oréal acquired a 10% stake in Galderma to deepen collaboration on dermatology innovation

- July 2024: Galderma’s Relfydess became the first ready-to-use liquid neuromodulator to secure a positive EU decision for frown lines and crow’s-feet indications.

Europe Medical Aesthetic Devices Market Report Scope

As per the scope of the report, aesthetic devices refer to all medical devices that are used for various cosmetic procedures, which include plastic surgery, unwanted hair removal, excess fat removal, anti-aging, aesthetic implants, skin tightening, etc., that are used for beautification, correction, and improvement of the body. Aesthetic procedures include both surgical and non-surgical procedures.

The Europe medical aesthetic devices market is segmented by type of devices (energy-based aesthetic devices (laser-based aesthetic devices, radiofrequency (RF)-based aesthetic devices, light-based aesthetic devices, and ultrasound aesthetic devices), non-energy based aesthetic devices (botulinum toxin, dermal fillers and aesthetic threads, chemical peels, microdermabrasion, and implants (facial implants, breast implants, and other imp lants), and other aesthetic devices), application (skin resurfacing and tightening, body contouring and cellulite reduction, hair removal, breast augmentation, and other applications), end-user (hospitals, clinics, and other end-users), and geography (United Kingdom, Germany, France, Italy, Spain, and Rest of Europe).

The report offers the value (in USD million) for the above segments.

By Type Of Device

| Energy-Based Aesthetic Devices | Laser-Based Aesthetic Devices |

| Radiofrequency-Based Aesthetic Devices | |

| Light-Based Aesthetic Devices | |

| Ultrasound-Based Aesthetic Devices | |

| Non-Energy-Based Aesthetic Devices | Botulinum Toxin |

| Dermal Fillers And Threads | |

| Microdermabrasion | |

| Implants | |

| Other Aesthetic Devices |

By Procedure Type

| Non-Surgical / Minimally Invasive |

| Surgical |

By Application

| Skin Resurfacing And Tightening |

| Body Contouring And Cellulite Reduction |

| Hair Removal |

| Facial Aesthetic Procedures |

| Breast Augmentation |

| Other Applications |

By End User

| Hospitals |

| Clinics And Dermatology Offices |

| Medical Spas |

| Home Settings |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Type Of Device | Energy-Based Aesthetic Devices | Laser-Based Aesthetic Devices |

| Radiofrequency-Based Aesthetic Devices | ||

| Light-Based Aesthetic Devices | ||

| Ultrasound-Based Aesthetic Devices | ||

| Non-Energy-Based Aesthetic Devices | Botulinum Toxin | |

| Dermal Fillers And Threads | ||

| Microdermabrasion | ||

| Implants | ||

| Other Aesthetic Devices | ||

| By Procedure Type | Non-Surgical / Minimally Invasive | |

| Surgical | ||

| By Application | Skin Resurfacing And Tightening | |

| Body Contouring And Cellulite Reduction | ||

| Hair Removal | ||

| Facial Aesthetic Procedures | ||

| Breast Augmentation | ||

| Other Applications | ||

| By End User | Hospitals | |

| Clinics And Dermatology Offices | ||

| Medical Spas | ||

| Home Settings | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe medical aesthetic devices market in 2026?

The market is valued at USD 8.96 billion and is projected to reach USD 14.22 billion by 2031.

What segment leads by revenue in Europe?

Energy-based platforms dominate with 52.02% of 2025 revenue.

Which procedure type is growing fastest?

Surgical interventions are forecast to expand at a 10.84% CAGR as technologies reduce invasiveness.

Which country generates the highest sales?

Germany leads with a 22.07% revenue share in 2025.

What is driving body-contouring demand?

Rising obesity prevalence and new non-surgical fat-reduction devices underpin an 11.62% CAGR outlook for body-contouring applications.

Page last updated on: