Big Data In Oil And Gas Exploration And Production Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

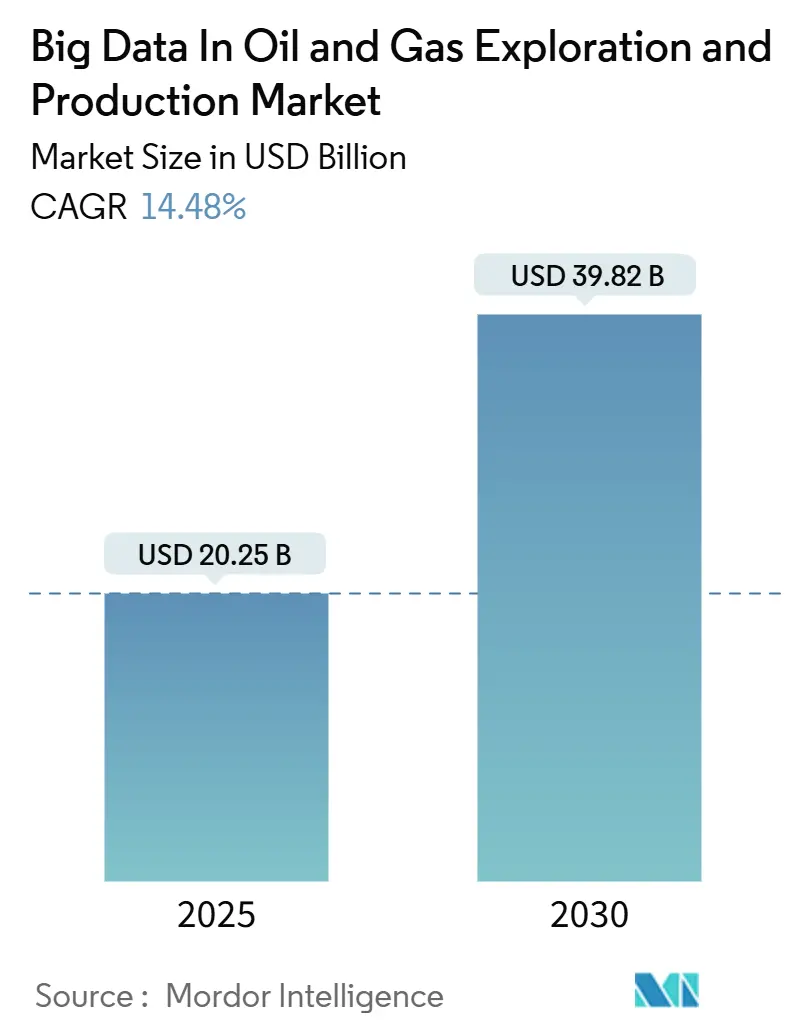

| Market Size (2025) | USD 20.25 Billion |

| Market Size (2030) | USD 39.82 Billion |

| Growth Rate (2025 - 2030) | 14.48% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Big Data In Oil And Gas Exploration And Production Market Analysis by Mordor Intelligence

The Big Data In Oil And Gas Exploration And Production Market size is estimated at USD 20.25 billion in 2025, and is expected to reach USD 39.82 billion by 2030, at a CAGR of 14.48% during the forecast period (2025-2030).

Operators have raised their digital ambitions to capture value from seismic imaging, real-time sensor networks, and edge analytics, which cut decision cycles from hours to minutes. Standardization around the OSDU framework now removes vendor lock-in while supporting seamless cloud migration. Edge processing at remote wellheads already enables continuous methane-leak monitoring that satisfies tightening ESG mandates. Competitive dynamics favour firms that marry domain expertise with data science skills, allowing smaller analytics specialists to secure niche wins in predictive maintenance and emissions tracking.

Key Report Takeaways

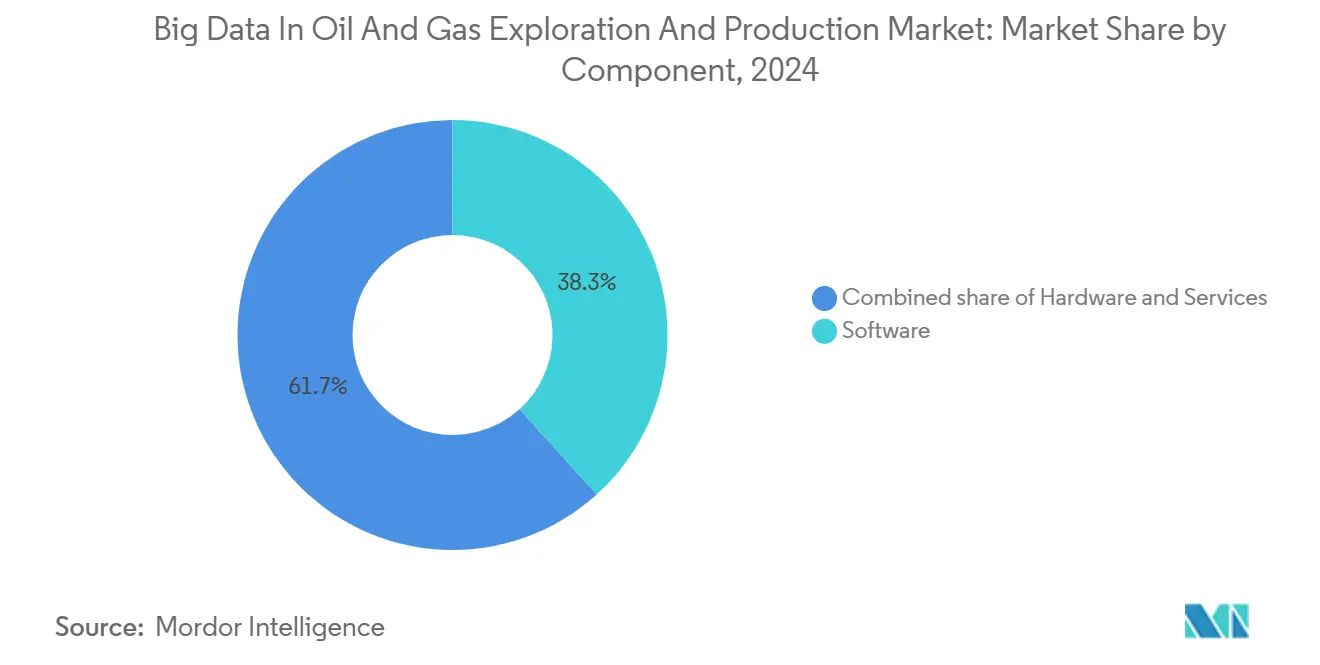

- By component, software accounted for 38.3% of 2024 revenue; the same segment is projected to grow at a 15.9% CAGR through 2030.

- By deployment mode, on-premise installations held 42.5% of the Big Data in oil and gas exploration & production market share in 2024, whereas cloud deployments are advancing at an 18.5% CAGR through 2030.

- By data type, structured data retained a 39.8% share of the Big Data in oil and gas exploration & production market size in 2024, while streaming analytics is expanding at a 19.2% CAGR.

- By application, reservoir management led with a 21.1% share in 2024, whereas drilling and well planning are rising at a 17.7% CAGR.

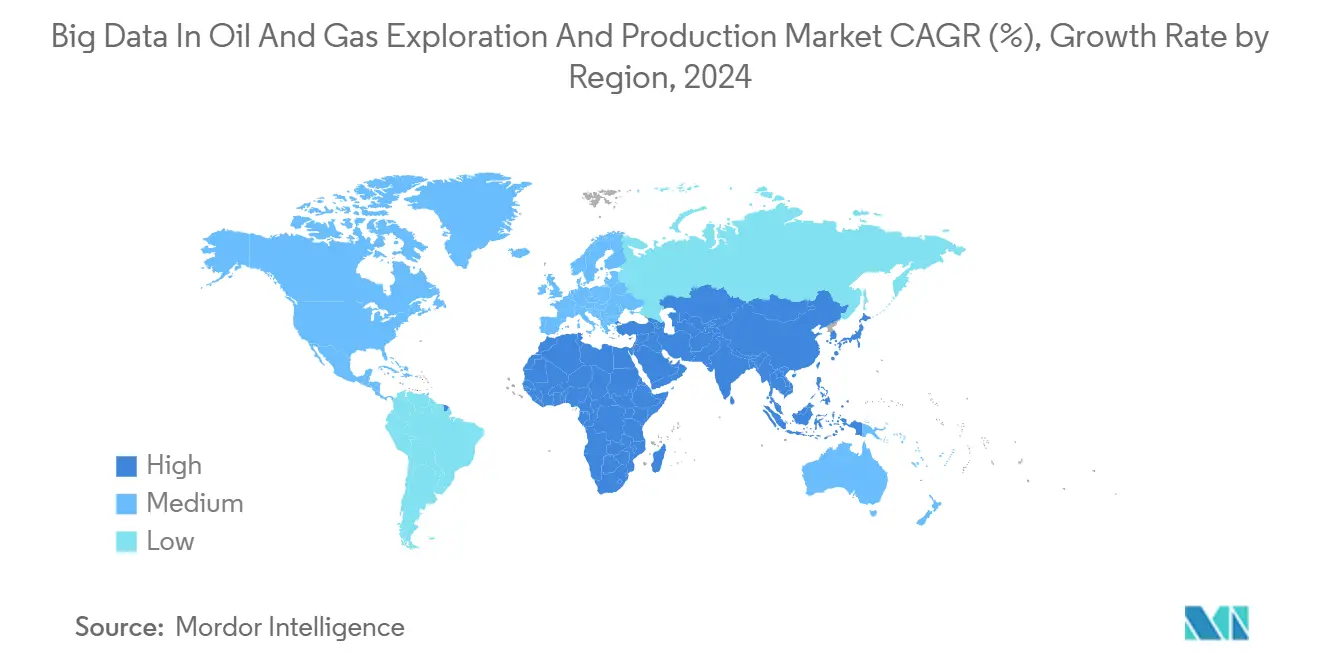

- By geography, North America accounted for 37.6% of the revenue in 2024; the Asia-Pacific region is forecast to post an 18.8% CAGR from 2024 to 2030.

Global Big Data In Oil And Gas Exploration And Production Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of high-frequency E&P sensor data | +2.8% | Global, with concentration in North America & APAC | Medium term (2-4 years) |

| Cost-pressure led demand for production optimization | +2.1% | Global, particularly in mature fields across North America & Europe | Short term (≤ 2 years) |

| Cloud migration of subsurface data workloads | +1.9% | North America & EU leading, APAC following | Medium term (2-4 years) |

| Industry adoption of OSDU open data standard | +1.6% | Global, with early adoption in North America & Middle East | Long term (≥ 4 years) |

| Edge / fog analytics at remote wellheads | +1.2% | Global, with emphasis on remote operations in North America & Middle East | Medium term (2-4 years) |

| ESG-driven methane-leak analytics mandates | +0.8% | North America & EU regulatory focus, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosion of High-Frequency E&P Sensor Data

Modern rigs now carry more than 40,000 sensors that stream over 2 TB per well each day. Edge devices filter this torrent locally and then relay curated sets to cloud clusters for further processing. Real-time optimisation cuts non-productive time by up to 15% while raising wellbore placement accuracy. The International Energy Agency expects AI-linked industrial electricity demand to reach 1,500 TWh by 2030, underscoring the compute load behind these analytics [1]International Energy Agency, “Electricity 2024 – Analysis and Forecasts to 2030,” iea.org. Operators already use multi-sensor correlation to predict equipment faults 72 hours ahead, lowering unplanned downtime by 25%.

Cost-Pressure Led Demand for Production Optimization

Low-margin environments prompt producers to extract every last drop from existing wells. ExxonMobil’s automated gas-lift system delivered a 2.2% production uplift across 1,300 wells and trimmed USD 50 million in yearly costs [2]ExxonMobil, “Advancing Production with Automated Gas Lift,” exxonmobil.com. Machine-learning models review historical production, reservoir pressure, and ESP performance to identify underperforming assets. Vital Energy reported 2-4% lift-pump gains by continuously adjusting motor speed against downhole conditions. Baker Hughes’ InjectRT software predicts chemical-injection needs with 90% accuracy, preventing overdosing and scale build-up.

Cloud Migration of Subsurface Data Workloads

Moving seismic reprocessing and reservoir simulation to cloud platforms unlocks elastic GPU pools, reducing runtimes from weeks to days. Microsoft Azure Data Manager for Energy already hosts more than 500 PB of operator data in OSDU-compliant form [3]Microsoft, “Azure Data Manager for Energy Overview,” microsoft.com. Small independents can obtain supercomputer-level horsepower without capital expenditure, narrowing the technology gap with major companies. Hybrid strategies keep sensitive datasets on-premise while bursting compute to encrypted cloud zones. This flexibility accelerates the adoption of machine learning across drilling and production workflows.

Industry Adoption of OSDU Open Data Standard

OSDU supplies a common schema that enables tools to exchange logs, production histories, and seismic cubes without manual reformatting. Early adopters such as Saudi Aramco, Shell, and TotalEnergies now spin up analytics pilots in weeks rather than months. Open APIs encourage a marketplace of third-party applications, widening operator choice and diluting vendor lock-in. Cloud-native design enables automatic scaling as workloads surge during frontier exploration or mega-field redevelopment programs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security & IP-protection concerns | -1.5% | Global, with heightened concerns in North America & Europe | Short term (≤ 2 years) |

| Legacy IT & data-silo complexity | -1.1% | Global, particularly affecting established operators in North America & Europe | Medium term (2-4 years) |

| Shortage of domain data-science talent | -0.9% | Global, with acute shortages in North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Regulatory-driven investment uncertainty | -0.7% | North America & Europe regulatory focus, with spillover to global operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-security & IP-Protection Concerns

More than half of the top oil and gas firms reported data breaches in 2024, with 69% scoring D or below on external security ratings. The blending of OT and IT networks opens fresh attack surfaces. Operators hesitate to move proprietary subsurface data—often worth billions—to public clouds despite the use of its strong encryption. Regulatory mosaics add extra hurdles; some jurisdictions insist seismic data stay within national borders. Together these issues slow universal adoption of shared analytics platforms.

Legacy IT & Data-Silo Complexity

Years of bolt-on systems have produced a patchwork of proprietary databases and incompatible file formats. Valuable logs often sit inside aging applications with no API access. Integration projects often require custom middleware and lengthy data-cleansing cycles that can strain budgets. Cultural factors also matter: engineers steeped in traditional workflows may be skeptical of algorithmic recommendations. These hurdles extend deployment timeframes and defer returns on analytics investment.

Segment Analysis

By Component: Software Catalyses Advanced Analytics

Software contributed the largest 38.3% share of 2024 revenue, and it is forecast to grow at a 15.9% CAGR, underscoring that algorithm sophistication, not hardware count, drives the competitive edge in the Big Data market for oil and gas exploration & production. Providers bundle seismic interpretation, reservoir modelling, and predictive maintenance within cohesive suites that shorten time-to-value. Managed-service providers complement these offerings by deploying data scientists into field teams to operationalise models quickly.

Hardware retains relevance for high-performance computing and ruggedized edge gateways, yet cloud elasticity removes the need for constant capital expenditure (capex) refresh. Services—ranging from data integration to change-management training—help operators overcome legacy IT friction. As software matures, value migrates toward packaged use cases, such as automated gas-lift tuning or ESP failure prediction, that deliver measurable production gains within weeks.

Note: Segment shares of all individual segments available upon report purchase

By Deployment Mode: Cloud Momentum Builds

On-premise estates still held a 42.5% share in 2024, reflecting perceived security benefits and regulatory mandates for local data storage. Even so, cloud workloads are growing at an 18.5% CAGR, the fastest of any deployment category within the big data market in oil and gas exploration & production. Hybrid architectures dominate: sensitive data sits inside operator firewalls while heavyweight simulations burst to cloud GPU clusters.

Edge computing provides the final layer, executing AI at the wellhead where milliseconds matter. This tiered model trims latency, controls bandwidth costs, and supports autonomous operations in remote basins. Vendors now offer pre-validated blueprints that streamline hybrid deployment, making the transition easier for conservative operators.

By Data Type: Streaming Analytics Gains Traction

Structured datasets—such as production reports and financial ledgers—still account for 39.8% of the Big Data in the oil and gas exploration & production market size. Yet streaming feeds from downhole tools and surface sensors are expanding at a 19.2% CAGR as operators demand real-time optimisation. Edge preprocessors compress and label microsecond readings before cloud ingestion, keeping transport costs viable.

Semi-structured formats, such as WITSML logs, bridge the structured and streaming realms, enabling cross-domain correlations. Unstructured files—including seismic images and maintenance manuals—are finally mined using computer vision and NLP to surface hidden insights. Integrated platforms that handle all four data shapes win favour for reducing hand-offs and governance headaches.

Note: Segment shares of all individual segments available upon report purchase

By Application: Reservoir Focus Meets Drilling Innovation

Reservoir management led with a 21.1% share in 2024, as engineers leveraged simulation engines and data-driven EOR programs to enhance recovery factors. The segment captures nearly one-fifth of the Big Data in oil and gas exploration & production market share, reflecting its central role in value creation. Drilling and well planning, however, hold the fastest 17.7% CAGR, driven by AI-guided geosteering that reduces slide time and improves borehole placement.[4]Halliburton, “DecisionSpace® 365 Capabilities,” halliburton.com

Production and lift optimisation remains a high-ROI arena where incremental gains compound across thousands of wells. Predictive maintenance utilizes vibration and pressure signatures to anticipate pump or compressor failures days in advance. HSE and emissions monitoring benefits from satellite and drone imagery stitched with ground readings to give continuous asset visibility. Together, these advances extend the value of analytics beyond subsurface teams into every workflow.

Geography Analysis

North America generated 37.6% of 2024 revenue, powered by shale players that pioneered horizontal drilling and data-rich completions. The region continues to scale automated gas-lift control and ESP analytics that deliver tangible cost savings. Government support for data-sharing consortia further expands the accessibility of subsurface libraries.

The Asia-Pacific region is the fastest-growing geography, projected to grow at an 18.8% CAGR through 2030. National oil companies in China and India are investing capital in AI-enabled exploration to enhance domestic supply security. Joint research programs between academia and industry accelerate the localization of algorithms for complex geology found in the South China Sea and Indian basins.

The Middle East leverages massive field datasets—Saudi Aramco alone stores 1,500 PB—to run AI models that optimise injection patterns across giant reservoirs. Europe focuses on emissions analytics to meet strict ESG rules, while South America adopts cloud platforms to overcome limited in-house computing capabilities. Collectively, these trends ensure the Big Data in oil and gas exploration & production market remains global in scope, yet locally nuanced in execution.

Competitive Landscape

Market concentration is moderate. Schlumberger leads with 256 digital patents, targeting subsurface analysis and drilling optimisation. Halliburton follows with 136 patents focused on production uplift technologies. Cloud hyperscalers—Microsoft, AWS, Google Cloud—add muscle through scalable infrastructure and AI frameworks, partnering with service majors rather than displacing them.

Strategic alliances shape competition. SLB and Nvidia co-develop GPU-accelerated subsurface workflows, while Baker Hughes teams with Repsol to roll out the Leucipa™ platform for predictive maintenance. These collaborations mix domain insights with AI expertise, shortening adoption cycles.

Niche vendors thrive by solving specific pain points such as methane detection or supply-chain optimisation. Their agility appeals to operators looking for quick wins. Over time, successful start-ups often become acquisition targets for larger service firms seeking to round out digital portfolios.

Big Data In Oil And Gas Exploration And Production Industry Leaders

-

Schlumberger

-

Halliburton

-

IBM

-

Baker Hughes

-

Microsoft

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Baker Hughes, an energy technology firm, and Repsol, a worldwide multi-energy corporation, unveiled a pact to implement advanced digital features via the Leucipa automated field production system, which boasts a generative AI-driven virtual assistant.

- September 2024: SLB expanded its collaboration with Nvidia to shorten seismic-processing turnaround and refine velocity models.

- September 2024: Saudi Aramco partnered with Groq to install edge AI hardware, enabling real-time inference on sensor feeds.

- July 2024: SLB and Aker BP unveiled a strategic long-term alliance. This initiative aims to fast-track innovation and significantly boost efficiency in Aker BP's exploration and production (E&P) operations.

Global Big Data In Oil And Gas Exploration And Production Market Report Scope

Big Data in the Oil and Gas Exploration and Production report includes:

| Hardware |

| Software |

| Services |

| On-premise |

| Cloud |

| Hybrid/Edge-Enabled |

| Structured |

| Unstructured |

| Semi-structured/Streaming |

| Exploration and Seismic Imaging |

| Drilling and Well Planning |

| Production and Lift Optimization |

| Reservoir Management and EOR |

| Predictive Maintenance |

| HSE and Emissions Monitoring |

| Supply-Chain and Logistics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Nigeria | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Deployment Mode | On-premise | |

| Cloud | ||

| Hybrid/Edge-Enabled | ||

| By Data Type | Structured | |

| Unstructured | ||

| Semi-structured/Streaming | ||

| By Application | Exploration and Seismic Imaging | |

| Drilling and Well Planning | ||

| Production and Lift Optimization | ||

| Reservoir Management and EOR | ||

| Predictive Maintenance | ||

| HSE and Emissions Monitoring | ||

| Supply-Chain and Logistics | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Nigeria | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected growth rate for the Big Data in oil and gas exploration & production market?

The market is forecast to expand at a 14.48% CAGR from 2025 to 2030.

Which component segment leads revenue contribution?

Software holds the top position with a 38.3% 2024 share and is forecast to grow at 15.9% CAGR.

Why are operators adopting cloud platforms for subsurface data?

Cloud offers elastic GPU resources that cut seismic re-processing times from weeks to days while lowering capex, driving an 18.5% CAGR in cloud deployments.

Which region shows the fastest market growth?

Asia-Pacific is advancing at an 18.8% CAGR due to large investments by national oil companies in China and India.

How are companies addressing methane-leak regulations?

Operators deploy continuous sensor monitoring and edge analytics that pinpoint leaks in near real time, enabling faster repairs and compliance reporting.

Page last updated on: