Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 10.85 Billion |

| Market Size (2026) | USD 11.14 Billion |

| Market Size (2031) | USD 12.72 Billion |

| Growth Rate (2026 - 2031) | 2.69% CAGR |

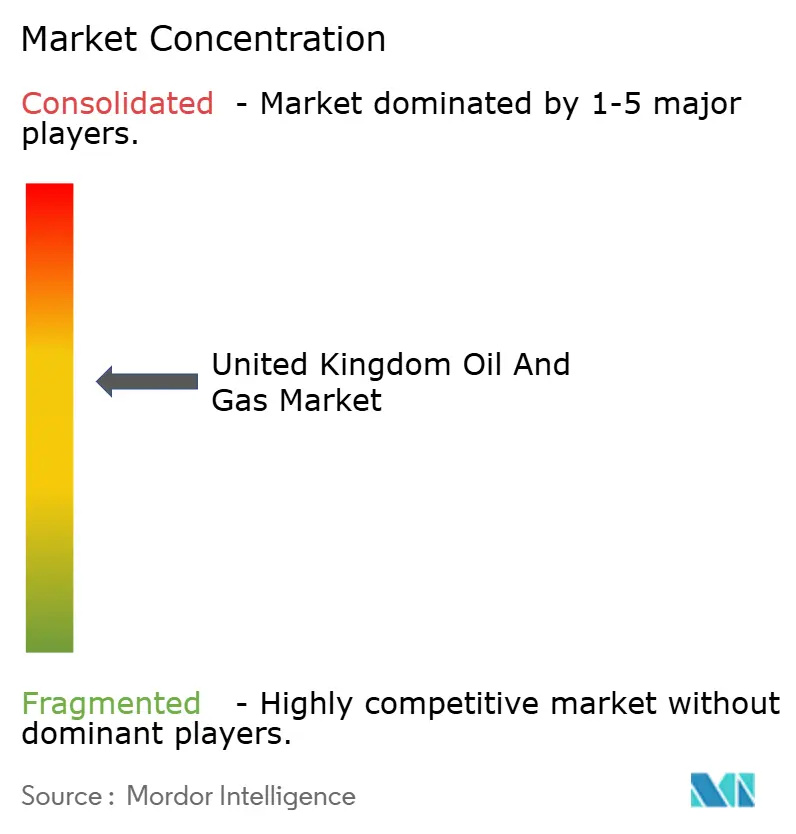

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Oil And Gas Market Analysis by Mordor Intelligence

The United Kingdom Oil And Gas market size is expected to grow from USD 10.85 billion in 2025 to USD 11.14 billion in 2026 and is forecast to reach USD 12.72 billion by 2031 at 2.69% CAGR over 2026-2031.

A strategic shift toward squeezing maximum value from mature North Sea reservoirs, paired with a deliberate slowdown in greenfield exploration, underpins this measured expansion. Operators have reduced lifting costs by 15-20% since 2020, thereby protecting profitability even as fiscal burdens increase.(1)Offshore Energies UK, “Economic Report 2024: UK Oil and Gas Industry Performance,” Offshore Energies UK, oeuk.org.uk The 2024 investment outlay of more than £6 billion, half again above regulator expectations, flowed mainly into life-extension programs and midstream upgrades that support carbon-capture infrastructure.(2)North Sea Transition Authority, “UK Oil and Gas Production and Investment Data,” North Sea Transition Authority, nstauthority.co.uk Consolidation among independents accelerated, with two headline acquisitions totaling more than USD 2 billion, unlocking cost synergies and decommissioning efficiencies.(3)Financial Times, “UK North Sea Oil Industry Consolidation Accelerates,” Financial Times, ft.com At the same time, floating-wind pilots and on-platform electrification cut diesel burn, proving that emissions compliance and production stability can coexist.

Key Report Takeaways

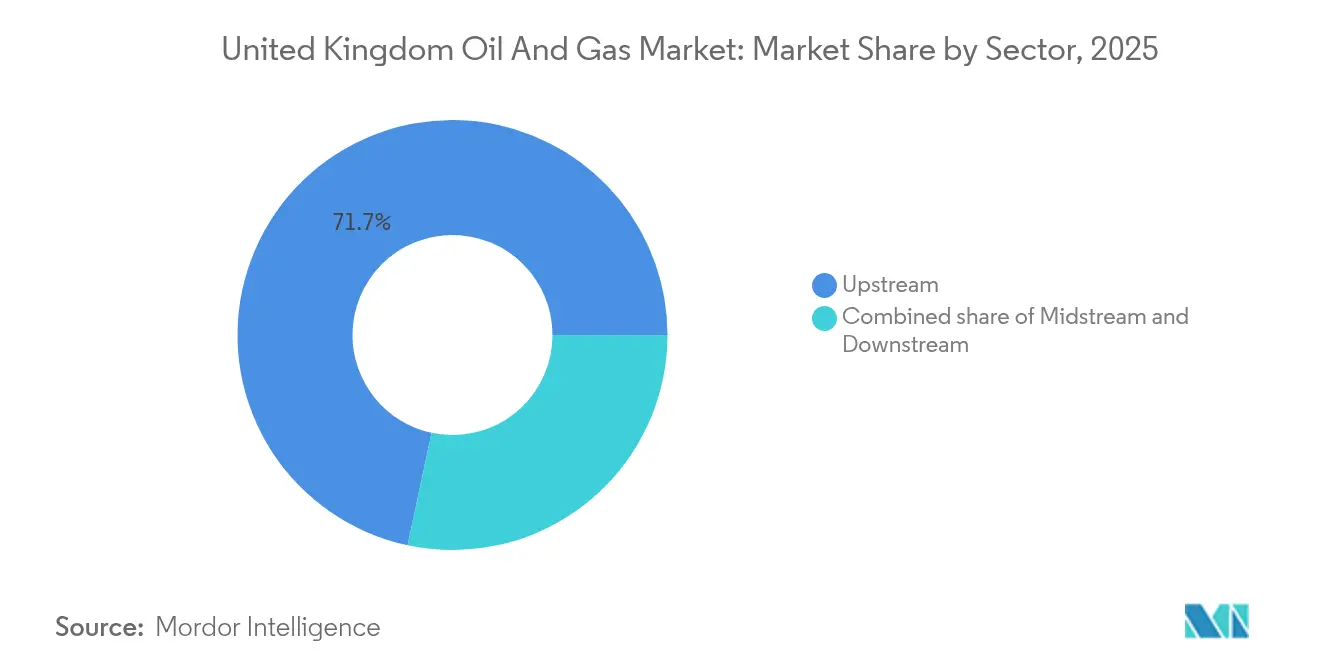

- By sector, upstream operations dominated with 71.65% of the UK oil and gas market share in 2025, while midstream emerged as the fastest-growing segment with 4.18% CAGR through 2031.

- By location, offshore activities commanded 88.35% of the UK oil and gas market size in 2025 and are expected to maintain growth leadership at a 3.02% CAGR through 2031.

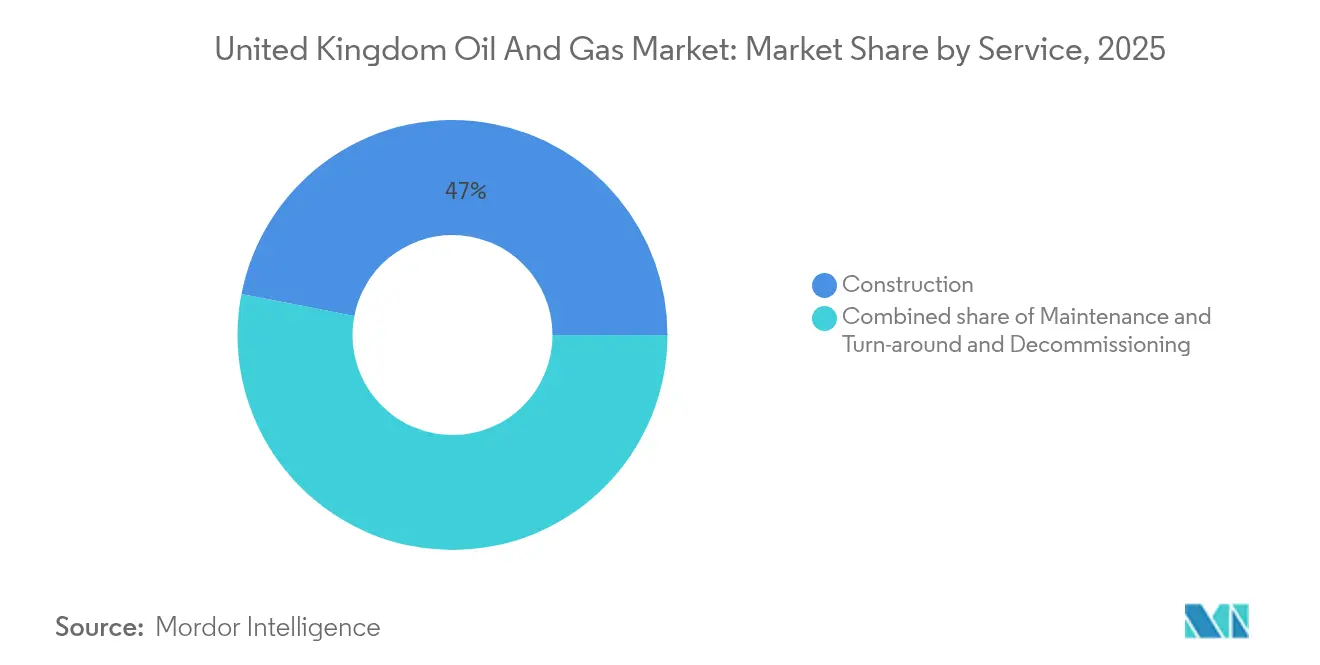

- By service type, construction activities held 46.95% of the UK oil and gas market share in 2025; however, decommissioning services led growth at a 6.05% CAGR, reflecting the basin's maturation.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Oil And Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining North Sea lifting costs | +0.8% | North Sea basins, concentrated in Central and Southern sectors | Medium term (2-4 years) |

| UK North Sea Transition Deal incentives | +0.6% | UK Continental Shelf, particularly new development areas | Long term (≥ 4 years) |

| Surge in floating-wind-powered platforms | +0.4% | North Sea offshore installations, pilot deployments in Scottish waters | Long term (≥ 4 years) |

| Re-industrialisation of Teesside & Humber | +0.3% | Northeast England industrial clusters, extending to Yorkshire | Medium term (2-4 years) |

| AI-enabled seismic imaging success rates | +0.2% | Global application with UK North Sea focus areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining North Sea Lifting Costs Drive Operational Efficiency

North Sea lifting costs have decreased substantially, creating competitive advantages for UK operators amid global energy market challenges. Technological breakthroughs in subsea systems and enhanced drilling techniques have cut per-barrel extraction costs by 15-20% since 2020, sustaining production viability despite heightened fiscal pressures. This cost reduction trajectory positions UK fields favorably against international alternatives, particularly as energy security concerns elevate domestic production value. The efficiency gains result from advanced reservoir management systems and optimized production scheduling, which maximize recovery rates while minimizing operational expenses. Operators leverage these cost improvements to extend field life and justify continued investment in mature assets that might otherwise face early decommissioning.

UK North Sea Transition Deal Incentives Reshape Investment Priorities

The UK North Sea Transition Deal offers structured fiscal incentives to operators demonstrating measurable progress toward net-zero emissions targets, thereby fundamentally altering capital allocation decisions across the sector. Investment allowances and enhanced depletion rates reward companies that integrate carbon capture, utilization, and storage technologies into their operations, with qualifying projects receiving accelerated tax relief worth up to 40% of eligible expenditures.(4)HM Revenue & Customs, “North Sea Transition Deal Tax Incentives Framework,” HM Revenue & Customs, gov.uk This policy framework has catalyzed over £2 billion in committed CCUS investments since 2024, transforming previously uneconomical projects into viable development opportunities. The deal creates competitive advantages for operators demonstrating technological leadership in emissions reduction, effectively subsidizing the transition toward lower-carbon hydrocarbon production. ISO 14001 environmental management certification has become increasingly critical for accessing these incentives, with operators investing heavily in compliance processes.

Floating Wind Platform Integration Reduces Operational Carbon Intensity

Floating wind-powered platforms represent a technological breakthrough addressing both operational costs and emissions compliance simultaneously. TotalEnergies' Culzean pilot project demonstrates the viability of this approach, with a 3 MW floating wind turbine supplying approximately 20% of the platform's power requirements, resulting in an estimated 2,000 tonnes of diesel consumption reduction annually. Crown Estate Scotland's Innovation and Targeted Oil and Gas leasing round has enabled direct power purchase agreements between wind developers and platform operators, creating a new revenue model benefiting both sectors. This integration strategy allows operators to maintain production levels while achieving substantial Scope 1 emissions reductions, addressing regulatory requirements without compromising output. The technology's scalability suggests potential application across 40-50 North Sea platforms by 2030, representing a fundamental shift in offshore energy infrastructure design.

Teesside and Humber Industrial Clusters Create Blue Hydrogen Demand

The re-industrialization of Teesside and Humber regions has generated unprecedented demand for blue hydrogen, creating new market opportunities for natural gas feedstock suppliers. BP's H2Teesside project aims to achieve up to 2 GW of hydrogen production capacity, representing more than 10% of the UK's 2030 hydrogen production target, and will require approximately 1.5 billion cubic meters of natural gas annually. The £21.7 billion government funding commitment over 25 years for carbon capture and storage clusters has de-risked these industrial developments, ensuring long-term off-take agreements for gas suppliers. Net Zero Teesside's 10 million tonnes per year CO2 capture capacity, operational by 2028, will anchor the region's transformation into a low-carbon industrial hub. This industrial renaissance reverses decades of manufacturing decline while creating stable, long-term demand for UK Continental Shelf gas production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated CCS levy on upstream operators | -0.4% | UK Continental Shelf, affecting all production licenses | Short term (≤ 2 years) |

| Grid-connected offshore wind cannibalising peak-time gas demand | -0.3% | UK electricity grid, concentrated impact during high wind periods | Medium term (2-4 years) |

| Heightened decommissioning bond requirements | -0.2% | North Sea installations approaching end-of-life | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated CCS Levy Strains Operator Cash Flows

The introduction of accelerated carbon capture and storage levies on upstream operators has created immediate financial pressure across the UK Continental Shelf, with compliance costs estimated at £150-200 million annually for major producers. This regulatory framework requires operators to contribute to national CCS infrastructure development regardless of their individual project participation, effectively subsidizing broader energy transition objectives through sector-specific taxation. The levy structure disproportionately impacts smaller independents who lack the scale to absorb these additional costs, potentially accelerating consolidation as marginal operators seek larger partners or exit the market entirely. Compliance with the levy requirements demands enhanced monitoring and reporting capabilities, which add operational complexity and further strain resources.

Offshore Wind Grid Integration Reduces Peak Gas Demand

Grid-connected offshore wind capacity has reached levels where peak generation periods significantly reduce natural gas demand for electricity generation, creating revenue volatility for gas-fired power plants and upstream suppliers. Wind generation contributed 35% of the UK electricity supply in 2023, with peak output periods displacing gas-fired generation that traditionally provided grid balancing services. This demand cannibalization is most pronounced during high wind periods when renewable output exceeds baseload requirements, forcing gas plants into increasingly intermittent operating patterns that reduce their economic viability. The grid's growing renewable penetration creates structural demand destruction for natural gas, particularly affecting long-term supply contracts that assume consistent baseload consumption patterns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Upstream Dominance Faces Midstream Growth Surge

The upstream segment's commanding 71.65% market share in 2025 reflects the continued centrality of extraction activities to UK oil and gas operations, yet the midstream segment's 4.18% CAGR through 2031 signals a fundamental shift toward infrastructure and processing investments. Upstream activities benefit from enhanced recovery techniques and extended field life programs that maximize value from existing North Sea assets. Operators like Harbour Energy have invested over USD 1.3 billion in asset acquisitions during 2024 to consolidate production capabilities. The midstream segment's accelerated growth stems from critical infrastructure requirements for carbon capture, utilization, and storage projects, with pipeline networks and processing facilities requiring substantial upgrades to handle CO2 transport and hydrogen production. Downstream operations maintain steady performance through refined product demand, though the segment faces long-term headwinds from electrification trends and renewable fuel mandates.

Midstream infrastructure investments are particularly concentrated in the East Coast Cluster, where Kellas Midstream's H2NorthEast facility represents a 1 GW blue hydrogen production capability that necessitates extensive pipeline modifications and the installation of new compression stations. The UK oil and gas market size for midstream operations reached USD 2.19 billion in 2025, with annual growth rates exceeding the sector average by 1.5 percentage points. The UK's gas transmission system spans over 7,600 km of high-pressure pipelines, with National Grid investing £2.5 billion annually in network maintenance and enhancement projects that support both traditional gas transport and emerging hydrogen applications. Processing capabilities are expanding through the deployment of floating production, storage, and offloading vessels, which enable the development of previously stranded reserves. Meanwhile, storage infrastructure benefits from strategic petroleum reserve requirements and seasonal demand balancing needs.

By Location: Offshore Supremacy Drives Technological Innovation

Offshore operations command an overwhelming 88.35% share UK the UK oil and gas market in 2025, with the same segment maintaining growth leadership at a 3.02% CAGR through 2031, underscoring the North Sea's irreplaceable role in UK hydrocarbon production. The offshore segment's dominance reflects geological advantages and established infrastructure networks that create substantial barriers to onshore development, particularly given the UK's limited unconventional resource base and restrictive hydraulic fracturing policies. Technological innovations in subsea systems and floating production platforms enable the development of previously inaccessible reserves, with water depths exceeding 200 meters becoming economically viable through the use of advanced drilling techniques. Onshore activities are subject to regulatory constraints and public opposition, which limit expansion opportunities, confining growth primarily to existing conventional fields and associated gas processing facilities.

The offshore segment benefits from economies of scale in platform operations and the utilization of shared infrastructure, which reduces per-barrel development costs. Hub-and-spoke production systems enable tie-back developments that extend field life at minimal capital investment. The UK oil and gas market size for offshore operations reached USD 9.58 billion in 2025, representing nearly 90% of the total sector value. Environmental compliance frameworks established by the Offshore Petroleum Regulator for Environment and Decommissioning create standardized operational protocols that facilitate technology transfer and best practice sharing among operators. Floating wind integration projects demonstrate the offshore segment's adaptability to energy transition requirements, with hybrid platforms combining hydrocarbon production and renewable energy generation in a single installation that optimizes infrastructure utilization and reduces environmental footprint.

By Service: Construction Maturity Contrasts Decommissioning Boom

Construction services hold the largest market share at 46.95% in 2025, reflecting ongoing platform modifications and infrastructure upgrades required for extended field operations, while decommissioning services experience an explosive 6.05% CAGR growth through 2031 as North Sea fields reach end-of-life. The construction segment benefits from complex brownfield projects that require specialized engineering capabilities and heavy-lift vessel operations, with operators investing heavily in platform life extension programs that can add 10-15 years to productive capacity. Maintenance and turnaround services provide steady revenue streams through predictable inspection and repair cycles, though digital monitoring systems are reducing intervention requirements and extending service intervals. The decommissioning segment's rapid expansion reflects the approaching end-of-life for fields developed during the 1970s and 1980s North Sea boom, with over 2,200 wellbores potentially becoming inactive between 2025-2029.

Decommissioning activities require specialized capabilities in platform removal, well plugging and abandonment, and environmental remediation, which command premium pricing due to their technical complexity and stringent regulatory requirements. The UK oil and gas market share for decommissioning services reached 18.75% in 2025, with annual growth rates exceeding the sector average by 3.4 percentage points. The UK's total decommissioning liability stands at approximately £ 40 billion, with the North Sea Transition Authority aiming to reduce this to £33.3 billion by 2028 through enhanced planning and improved supply chain efficiency. Supply chain analysis indicates UK companies can capture approximately 70% of domestic decommissioning work, creating substantial opportunities for service providers who develop appropriate technical capabilities and regulatory compliance frameworks. Compliance with ISO 45001 occupational health and safety standards has become mandatory for decommissioning contractors, driving investment in specialized training and equipment that supports the segment's premium pricing structure.

Geography Analysis

The North Sea's geological provinces exhibit distinct production characteristics and development trajectories that shape regional investment patterns and operational strategies. The Central North Sea maintains the highest production density, with established infrastructure networks that support efficient tie-back developments and shared processing facilities. In contrast, the Southern North Sea benefits from proximity to UK gas demand centers and existing pipeline connections, which reduce transportation costs. The Northern North Sea presents the most challenging operating environment but contains the largest remaining reserves, with water depths exceeding 150 meters requiring advanced subsea technologies and floating production systems that command higher development costs but offer substantial resource potential.

Regional emissions performance varies significantly across North Sea sectors, with the Southern North Sea achieving an 11.1% reduction in field emissions during 2023, while the Central North Sea recorded a 6.8% decline, and the Northern North Sea managed a 2.9% decrease. The UK oil and gas market size across these regions reflects both production volumes and operational complexity, with the Central North Sea accounting for the largest share at 42.05% of the total market value. The Eastern Irish Sea experienced an 8.6% increase in emissions, reflecting aging infrastructure and declining production efficiency that may accelerate decommissioning timelines for marginal fields. These regional variations in environmental performance are increasingly influencing investment decisions, as operators prioritize assets that can achieve compliance with tightening emissions regulations while maintaining economic viability.

Onshore activities remain geographically concentrated in established production areas, primarily in southern England and the East Midlands, where conventional fields provide stable but declining output, which reached record quarterly lows of 7.7 million tonnes in Q2 2024. The onshore segment faces structural challenges from regulatory restrictions on hydraulic fracturing and public opposition to new developments that limit expansion opportunities and confine growth to existing licensed areas. Scotland's offshore waters contain the majority of remaining UK hydrocarbon reserves, with the West of Shetland region emerging as a key growth area for floating production systems that can access previously stranded deepwater resources through technological innovations in subsea infrastructure and harsh environment operations.

Regulatory Landscape

The United Kingdom oil and gas sector operates under a multi-agency framework led by the North Sea Transition Authority (NSTA) for licensing and consents, with the Offshore Petroleum Regulator for Environment and Decommissioning (OPRED) handling environmental approvals and decommissioning oversight. The UK Government's North Sea Future Plan (published in November 2025) is the most notable shift, as it focuses basin management on maximizing value from existing fields and stops the issuance of new exploration licenses for new oil and gas fields, redirecting activity toward tie-backs, life extension, and brownfield redevelopment.

Regulatory requirements increasingly link hydrocarbon activity to transition infrastructure, including carbon storage and emissions governance. In 2026, the Oil and Gas Authority (Carbon Storage and Offshore Petroleum) (Specified Periods for Disclosure of Protected Material) Regulations 2026 updated confidentiality and disclosure periods for protected carbon storage information and certain offshore petroleum materials, which affects data access and project development workflows for CCUS and upstream operators. Onshore activity (where applicable) is still governed by environmental regulation and permitting routes such as those set by the Environment Agency, alongside the wider licensing framework administered by the NSTA.

Competitive Landscape

The UK oil and gas market exhibits moderate consolidation with increasing concentration among major independents following the strategic withdrawal of international oil companies from North Sea operations. Market structure has shifted decisively toward specialized regional operators that possess the technical expertise and cost structures necessary for mature basin development. The top three independents—Harbour Energy, Energean, and Ithaca Energy—account for 68% of the total market capitalization among UK-focused producers. This consolidation trend accelerated through 2024 with Harbour Energy's USD 1.3 billion acquisition of Wintershall Dea's UK assets and Ithaca Energy's USD 754 million purchase of Eni's North Sea portfolio, creating larger and more efficient operators capable of managing complex, multi-field developments. Technology adoption patterns reveal competitive advantages for operators who successfully integrate artificial intelligence in reservoir management and predictive maintenance, with companies like BP reducing seismic interpretation timeframes from 6-12 months to 8-12 weeks through machine learning applications.

Strategic positioning is increasingly centered on energy transition capabilities, with operators pursuing dual strategies that maximize cash generation from existing hydrocarbon assets while developing competencies in carbon capture, utilization, and storage technologies. The UK oil and gas market share distribution among service providers reflects specialization trends, with engineering firms like Wood plc capturing premium segments through technical differentiation and digital capabilities. White-space opportunities exist in decommissioning services, where specialized contractors can capture premium margins through technical expertise in platform removal and environmental remediation, as well as in midstream infrastructure development that supports hydrogen production and CO2 transport networks. Emerging disruptors include technology companies that provide digital solutions for operational optimization and emissions monitoring, while traditional service providers face pressure to develop capabilities in renewable energy integration and environmental compliance. Regulatory compliance with Offshore Petroleum Regulator for Environment and Decommissioning standards creates barriers to entry that protect established operators while demanding continuous investment in environmental management systems and safety protocols.

United Kingdom Oil And Gas Industry Leaders

TotalEnergies SE

Shell PLC

BP PLC

Harbour Energy plc

Equinor ASA (UK ops)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The North Sea Future Plan (November 2025) shifts opportunity away from frontier exploration toward monetizing mature infrastructure via tie-backs, incremental projects around existing hubs, and service demand tied to late-life operations. This matches investment patterns, including more than GBP 6 billion of 2024 outlay directed toward life-extension programs and midstream upgrades, and it also supports decommissioning as a fast-growing service area given the scale of North Sea end-of-life activity and the basin's decommissioning liability. In this setting, supply-chain capacity that helps reduce unit costs for brownfield engineering, well interventions, and late-life integrity work becomes a practical lever to keep assets economic under tighter compliance and fiscal burdens.

Midstream and integrated energy-hub buildouts around East Coast industrial clusters also create whitespace where oil and gas infrastructure, CO2 transport and storage, and hydrogen projects overlap. Demand pull is supported by the UK government's long-term funding commitment for CCUS clusters and project pipelines such as BP's H2Teesside and Net Zero Teesside, which connect natural gas feedstock requirements to decarbonization infrastructure. Regulatory requirements that link new gas development to decarbonization readiness, including legislation implemented in 2026 requiring new unabated gas to be future-proofed for carbon capture or hydrogen conversion, further concentrate opportunity in assets and contractors able to carry out electrification, emissions monitoring, and CCUS-enablement upgrades, alongside operators working through NSTA approvals for tie-backs and infrastructure-led developments.

Recent Industry Developments

- July 2026: Adura (Shell and Equinor JV) released updated environmental impact assessments for the Jackdaw gas field and the Rosebank oil field, with OPRED reviewing the submissions after legal and regulatory scrutiny on climate impacts. The updates highlight how consenting timelines and EIA content have become central to progressing large UK upstream projects and associated supply-chain activity.

- March 2026: TotalEnergies completed the merger of its UK North Sea upstream assets with NEO NEXT to form NEO NEXT+, with TotalEnergies holding a 47.5% shareholding. The transaction consolidates mature-basin positions and concentrates capital and operating capability around late-life value extraction and infrastructure-led development in the UK Continental Shelf.

- October 2024: Harbour Energy completed its USD 1.3 billion acquisition of Wintershall Dea's UK North Sea assets, expanding its footprint across additional fields and adding material production capacity. The deal reinforced consolidation among UK-focused independents and strengthened the platform for life-extension spend and decommissioning planning across a larger asset base.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the value of oil and gas activity in the United Kingdom across upstream, midstream, and downstream, as tracked through onshore and offshore operations and related services delivered to operators.

Scope exclusions: Pure-play power generation, retail fuel marketing margins, and renewable-only projects are not counted unless they are directly tied to oil and gas assets (for example, decommissioning or conversion work).

Segmentation Overview

- By Sector

- Upstream

- Midstream

- Downstream

- By Location of Deployment

- Onshore

- Offshore

- By Service

- Construction

- Maintenance and Turn-around

- Decommissioning

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base map of the UK oil and gas system, and to set guardrails for production, infrastructure, and spending cycles. We relied on public datasets and official releases such as government energy statistics, the UK regulator for offshore licensing and field data, trade and customs statistics, and central-bank macro series for inflation and exchange rates.

To keep assumptions realistic, the desk work was complemented with company annual reports, investor presentations, project press releases, and reputable industry media coverage of field developments, maintenance schedules, and decommissioning timelines. In parallel, we used a paid subscription for company financials and news, plus a paid patent database where it helped check technology adoption signals. The sources listed here are illustrative only, and many other public references were also checked during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what is actually being executed in the UK, and then tightening assumptions that desk research cannot fully answer. We interviewed and surveyed a mix of asset operators, EPC and service providers, logistics and midstream participants, and domain experts across major UK activity hubs. Follow-up checks were then used to close gaps in service splits, offshore intensity, and timing of project phases.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 16% | |

| Mid tier: 49% | Functional/Unit leaders: 31% | |

| Smaller Players: 19% | Managers: 53% |

Market-Sizing & Forecasting

Sizing starts from a top-down rebuild of the UK oil and gas demand pool using activity signals that can be traced year to year, and then the totals are stress-tested with selective bottom-up checks. In practice, production and field activity trends, offshore versus onshore intensity, and service demand cycles were converted into value using realistic cost and pricing assumptions. We then corroborated results using sampled supplier revenue direction, channel checks, and sanity checks on implied spend per active asset.

A few inputs that matter in this market include offshore project cadence (including maintenance and turn-around windows), decommissioning schedules, upstream share versus midstream expansion, and the balance between construction versus ongoing services. Where coverage is thin for smaller contracts or bundled service lines, we filled gaps with proxy ratios derived from primary inputs, and then rechecked the implied split so it stays consistent with observable UK activity.

For forecasting, scenario analysis was used so the outlook can reflect different paces of field development, infrastructure upgrades, and policy-led changes to project timing. The forward view was then anchored to expert expectations on how offshore work, midstream upgrades, and decommissioning evolve, which helped keep growth rates within a plausible range.

Data Validation & Update Cycle

Triangulation is applied at multiple steps so no single source or assumption drives the total. Analysts compare model outputs against independent signals such as production direction, announced project pipelines, and service intensity indicators, and then investigate variances before internal sign-off.

When an outlier appears, we re-check scope fit, the unit economics used, and the timing of project execution, and then re-contact relevant interviewees if the change looks material. Reports are refreshed annually, and interim updates are made when major events can shift spend or activity. A final pre-delivery review pass follows to ensure the latest public signals are reflected.

Mordor Intelligence's United Kingdom Oil and Gas Market Size Measured Against Other Published Estimates

Published estimates for the UK oil and gas market can look far apart because the underlying boundaries are not always the same, even when the titles sound similar. Differences usually come from what parts of the value chain are counted, whether figures represent industry revenue versus project and service spend, and how currency timing and inflation are handled.

Production and offshore activity checks, combined with service-line splits taken from interviews, are the evidence trail that keeps Mordor Intelligence aligned to UK oil and gas construction, maintenance and turn-around, and decommissioning value rather than counting the full pass-through value of produced hydrocarbons.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.85 B (2025) | |

| Industry Publisher A | USD 330.50 B (2024) | This figure appears to treat the market as the total industry value across upstream, midstream, and downstream, which can embed commodity value and broad downstream revenue pools that are not tied to UK project and service execution. |

| Industry Publisher B | USD 0.60 B (2025) | This estimate is much smaller, which commonly happens when only a narrow slice is valued, such as select midstream and upstream activities or a limited set of services, with conservative coverage of offshore-heavy work. |

The spread is mainly explained by what is being counted, not by a disagreement on the direction of UK activity. By tying the market total to observable UK service demand signals and then checking the implied spend against real-world execution patterns, the result stays transparent and repeatable for planning and benchmarking.

Key Questions Answered in the Report

What is driving growth in the UK oil and gas sector?

Growth in the UK oil gas market is primarily driven by declining North Sea lifting costs (15-20% reduction since 2020), North Sea Transition Deal incentives providing up to 40% tax relief for qualifying projects, and technological innovations like floating wind-powered platforms that reduce operational carbon intensity.

How large is the UK oil and gas industry?

The UK oil gas market reached USD 10.85 billion in 2025 and is projected to grow at a 2.69% CAGR to reach USD 12.72 billion by 2031, with production averaging 1.09 million barrels of oil equivalent per day in 2024.

Which segment dominates the UK oil and gas market?

The upstream segment dominates with 71.65% market share in 2025, while offshore operations command 88.35% of the market, underscoring the North Sea's central role in UK hydrocarbon production.

What is the fastest growing segment in UK oil and gas?

Decommissioning services are experiencing the most rapid expansion at 6.05% CAGR through 2031, reflecting the sector's maturation phase as fields developed during the 1970s and 1980s approach end-of-life.

How is the energy transition affecting UK oil and gas?

The energy transition is reshaping the UK oil gas market through accelerated CCS levies on operators, increased competition from grid-connected offshore wind that reduces peak-time gas demand, and strategic pivots toward blue hydrogen production and carbon capture projects that create new market opportunities.

Who are the leading companies in the UK oil and gas sector?

The market is increasingly concentrated among specialized regional operators, with Harbour Energy, Energean, and Ithaca Energy accounting for 68% of total market capitalization among UK-focused producers following strategic acquisitions worth over USD 2 billion combined in 2024.

Page last updated on: