Saudi Arabia Waste Management Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

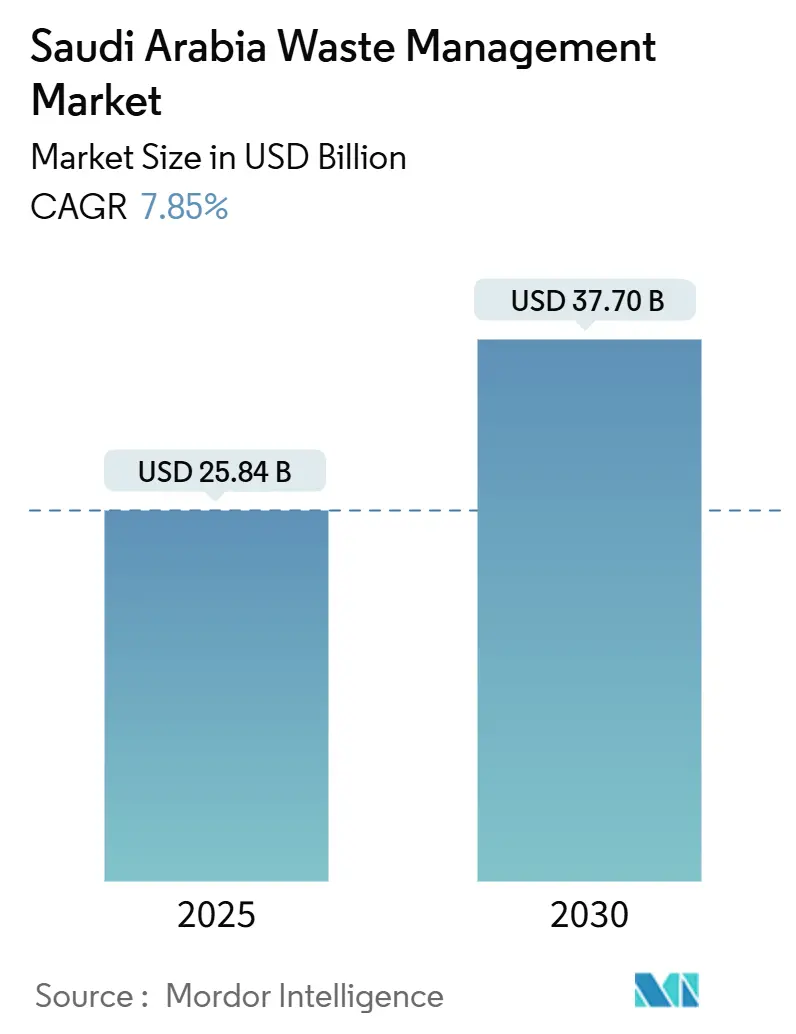

| Market Size (2025) | USD 25.84 Billion |

| Market Size (2030) | USD 37.70 Billion |

| Growth Rate (2025 - 2030) | 7.85% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Waste Management Market Analysis by Mordor Intelligence

The Saudi Arabia Waste Management Market size stands at USD 25.84 billion in 2025 and is forecast to reach USD 37.70 billion by 2030, reflecting a robust 7.85% CAGR. Vision 2030’s circular-economy mandate, rising urbanization, and the National Center for Waste Management’s 94% landfill-diversion target are propelling capital into advanced treatment technologies. Construction mega-projects, mandatory source segregation beginning in 2025, and carbon-credit eligibility for waste-to-energy facilities after 2027 are widening the revenue base across collection, recycling, and recovery services. Private-sector public-private partnerships (PPPs) totaling more than 200 projects are accelerating infrastructure rollout, while international operators leverage joint ventures to localize technology and meet Saudi standards. Competitive differentiation is quickly shifting from landfilling capacity to integrated resource-recovery models that unlock value from municipal solid, construction, and e-waste streams[1]Ministry of Environment, Water and Agriculture, “National Waste Strategy Updates,” mewa.gov.sa.

Key Report Takeaways

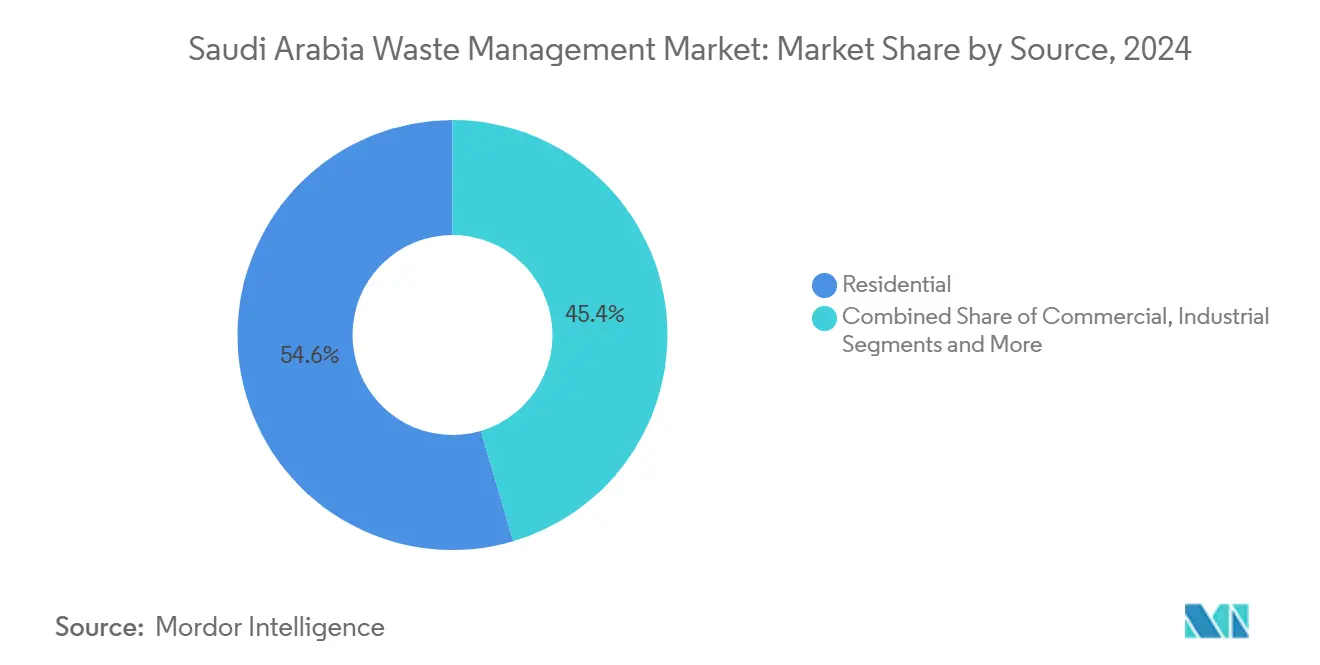

- By source, residential waste commanded 54.56% of Saudi Arabia's waste management market share in 2024, whereas commercial waste is advancing at a 9.60% CAGR through 2030.

- By service type, disposal and treatment captured 52.34% of revenues in 2024, while recycling and resource recovery are projected to accelerate at a 9.70% CAGR to 2030.

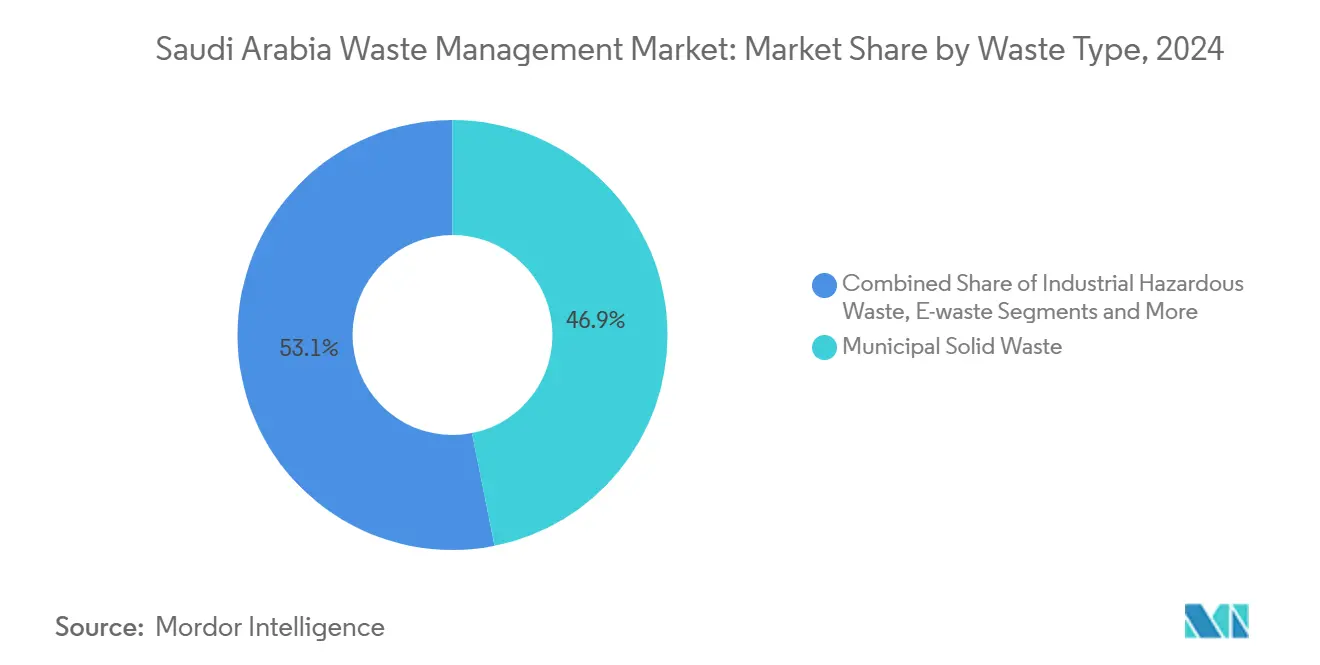

- By waste type, municipal solid waste led with 46.87% share of the Saudi Arabia waste management market size in 2024, and e-waste is expanding at an 8.49% CAGR to 2030.

- By region, Riyadh Province held 40.43% revenue share in 2024, whereas the Eastern Province is on track for the fastest 8.19% CAGR through 2030.

Saudi Arabia Waste Management Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 zero-landfill milestones | +1.8% | Nationwide, early uptake in major cities | Long term (≥ 4 years) |

| Private-sector PPP pipeline | +1.5% | National, strongest in Eastern Province and Makkah | Medium term (2-4 years) |

| Economic growth & urban migration | +1.2% | National focus on Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Mandatory source segregation 2025-2027 | +1.0% | National, phased from urban centers | Short term (≤ 2 years) |

| Construction giga-project waste surge | +0.8% | NEOM, Red Sea Project, Qiddiya, Riyadh Central | Medium term (2-4 years) |

| Carbon-credit upside for waste-to-energy | +0.7% | Industrial zones nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Zero-Landfill Targets Reshape Investment Priorities

The Kingdom’s pledge to divert 94% of waste from landfills by 2035 is triggering a wholesale shift from disposal toward recycling, composting, and waste-to-energy. Over 840 new facilities are planned within 25 regional clusters, reducing logistics costs and ensuring balanced geographic coverage. Operators that establish integrated hubs early in Riyadh and Jeddah secure first-mover advantages before compliance deadlines tighten. Clear liability assignment under the Waste Management Law and eligibility of waste-to-energy carbon credits after 2027 de-risk capital commitments. Consequently, the Saudi Arabian waste management market is aligning investment flows with long-term regulatory certainty[2]National Center for Waste Management, “Waste Management Law,” ncwm.gov.sa.

Private-Sector PPP Pipeline Accelerates Infrastructure Development

A PPP pipeline exceeding USD 700 million is unlocking private capital for collection fleets, sorting lines, and waste-to-energy plants. The National Center for Privatization standardizes tender documents, trimming transaction costs and shortening bid cycles. Flagship deals such as SIRC–Veolia joint ventures demonstrate how international technology is localized through Saudi majority ownership structures. In water services, similar PPP frameworks have already slashed delivery timelines by 25%, offering a playbook for waste infrastructure. Competitive concession awards and 20-year offtake agreements further strengthen bankability across the Saudi Arabian waste management market.

Economic Growth & Urban Migration Drive Infrastructure Demand

Accelerating GDP diversification is channeling population inflows into Riyadh, Jeddah, and Dammam, lifting per-capita waste volumes and stretching collection grids. Annual municipal solid waste has already reached 15 million tonnes and is forecast to double by 2033, creating scale for automated sorting and real-time fleet monitoring. Municipalities are rolling out digital platforms such as Jeddah’s Madinati to optimize routing and boost citizen engagement. The Ministry of Environment, Water, and Agriculture estimates waste-circularity initiatives could contribute USD 32 billion to GDP by 2035, underpinning investor confidence in advanced treatment plants. These converging economic and demographic trends cement a stable demand base for the Saudi Arabian waste management market[3]Riyadh Municipality, “Madīnatī Platform Launch,” riyadhmun.gov.sa.

Mandatory Source Segregation Creates Operational Transformation

From 2025, households nationwide must separate organic and dry recyclables, with Riyadh’s pilot targeting 81% diversion of 3.4 million tonnes per year. Dual-bin systems spawn fresh demand for color-coded containers, RFID tags, and route-optimization software. Real-time dashboards allow municipalities to issue penalties for non-compliance, speeding behavioral change. Higher material purity lifts plant yields and cuts operating costs in downstream recovery facilities. Early adopters equipped with optical sorters and AI-powered robotics will capture premium processing contracts across the Saudi Arabian waste management market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CapEx for integrated facilities | -1.1% | National, sharper in secondary cities | Medium term (2-4 years) |

| Fragmented collection in secondary cities | -0.8% | Smaller municipalities outside top metros | Short term (≤ 2 years) |

| Low household participation in recycling | -0.6% | Nationwide, rural areas are most affected | Medium term (2-4 years) |

| Thin domestic market for secondary materials | -0.5% | National, limited industrial demand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CapEx Requirements Constrain Market Entry

Waste-to-energy lines often exceed USD 150 million in capital cost, limiting participation to well-capitalized conglomerates or foreign utilities. Financing cycles of three to five years prolong payback horizons, deterring smaller tech innovators. In secondary cities, lower waste volumes erode economies of scale, making it hard to service debt covenants. Although PPP structures offer viability-gap funding, local banks’ limited track record with waste assets inflates risk premiums. As a result, market consolidation around SIRC, Veolia, and SUEZ is likely to intensify within the Saudi Arabian waste management market.

Fragmented Collection Systems Limit Operational Efficiency

Outside Riyadh and Jeddah, more than 40 municipalities run discrete fleets with divergent container sizes, scheduling windows, and fee structures. This patchwork lifts cost per tonne by up to 30% versus unified systems and hampers data integration for route optimization. Incomplete curbside coverage also depresses recycling yields, complicating feedstock forecasts for new recovery plants. The Ministry is piloting regional consortiums to pool procurement and harmonize standards, yet full rollout may take several budget cycles. Until alignment happens, inefficiencies will trim margins across the Saudi Arabian waste management market.

Segment Analysis

By Source: Residential Volumes Anchor Growth While Commercial Waste Accelerates

Residential streams supplied 54.56% of Saudi Arabia's waste management market share in 2024, underscoring the enduring influence of household behavior on collection routes and service design. Urban households generate an average of 1.4 kg per capita daily, creating predictable tonnage that underpins baseline revenues for fleet operators. Yet commercial generators—shopping malls, office complexes, and logistics hubs are raising output by 9.60% CAGR, adding premium opportunities for source-segregated pickups and after-hours service windows. The Saudi Arabia waste management market size for commercial waste is projected to add more than USD 2.6 billion by 2030 as mixed-use property pipelines in Riyadh Front and Jeddah Corniche reach completion.

Industrial sources remain significant in absolute tonnage, particularly in the Eastern Province, where petrochemical complexes supply hazardous streams that demand specialized permits and command fees two to three times higher than municipal waste. Healthcare and pharmaceutical facilities contribute a smaller but high-margin biomedical niche requiring licensed incineration operators. Construction and demolition (C&D) debris from mega-projects like NEOM and Red Sea Destination creates seasonal surges, encouraging players to deploy mobile crushing units that convert concrete into certified aggregates. Integrated service providers that bridge residential reliability with commercial customization are poised to capture outsized wallet share in the Saudi Arabia waste management market.

Note: Segment shares of all individual segments available upon report purchase

By Service Type: Disposal Dominance Gives Way to Recycling-Led Value Creation

Disposal and treatment accounted for 52.34% of 2024 revenues, yet the growth spotlight now rests on recycling and resource recovery, moving at a 9.70% CAGR. Municipal tenders increasingly bundle collection with material-recovery guarantees, forcing bidders to integrate optical sorters, AI robotics, and refuse-derived-fuel lines. The Saudi Arabia waste management market size for recycling is forecast to top USD 9 billion by 2030 as diversion targets tighten. Collection and transportation still form the logistical backbone, but margins improve when operators pair route density with transfer-station drop points that lower haul distances.

Landfill operators face declining gate fees as diversion mandates bite, incentivizing conversions into engineered cells for inert C&D waste or low-carbon energy hubs capturing methane for grid injection. Waste-to-energy plants within economic zones such as Jubail Industrial City are securing 20-year feedstock agreements that underpin project financing. Consulting, audit, and training services—classified as “Others” are quietly expanding as municipalities seek expertise on compliance, digital twins, and carbon accounting. As the regulatory bar rises, technology-enabled, multi-service platforms will secure pricing power throughout the Saudi Arabian waste management market.

By Waste Type: Municipal Solid Waste Leads but E-Waste Shows Highest Momentum

Municipal solid waste (MSW) delivered 46.87% of revenue in 2024, marking it the anchor stream for most recovery infrastructure. However, e-waste is the fastest-growing category at 8.49% CAGR, propelled by government digitization and short device replacement cycles within corporate IT refresh programs. Pilot dismantling centers in Riyadh recover copper, gold, and rare-earth elements, achieving gross margins above 30%. The Saudi Arabia waste management market size for e-waste is expected to double to nearly USD 1.5 billion by 2030, attracting specialized investors.

Industrial hazardous waste offers high unit profits but requires ISO-certified storage, transport manifests, and advanced thermal treatment. Plastic recycling gains strategic heft from SABIC’s circular polymer offtake, creating end-market certainty that derisks supply contracts. Biomedical waste growth aligns with hospital expansions under the Health Sector Transformation Program, requiring catalytic-oxidation incinerators equipped with flue-gas scrubbing. C&D debris retains volume dominance in giga-project zones; over 25 million tonnes of concrete will be recycled into road base by 2028. Operators that diversify feedstock portfolios while maintaining compliance excellence will lead in the Saudi Arabian waste management market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Riyadh Province generated 40.43% of national revenue in 2024, supported by population density, consistent municipal budgets, and the Riyadh Green Initiative that directs public funding toward advanced sorting and composting. Technology pilots run here often become national templates, giving local operators early learning curves that translate into tender wins elsewhere.

The Eastern Province is projected to post the fastest 8.19% CAGR through 2030 as petrochemical and gas investments multiply hazardous and industrial waste streams. National Water Company’s USD 586 million capital program to integrate water and waste infrastructure further widens the addressable market. Dammam’s industrial clients sign multi-year take-or-pay contracts for specialized treatment, underpinning bankable cash flows and encouraging deployment of higher-specification incinerators.

Makkah Province, anchored by Jeddah’s commercial expansion and religious tourism, experiences seasonal waste peaks that necessitate flexible fleet deployment and dynamic routing. The USD 19.9 billion Jeddah Central Project enriches C&D volumes and spurs investments in on-site recycling hubs. Outside top metros, secondary cities and rural districts confront fragmented collection, presenting first-mover advantages for regional aggregators that introduce scalable, mobile treatment platforms across the Saudi Arabia waste management market.

Competitive Landscape

The Saudi Arabian waste management market is witnessing moderate fragmentation as domestic champion SIRC accelerates consolidation through minority-controlled joint ventures with Veolia and SUEZ that inject technology while safeguarding local employment. Digitalization is now a core strategy: operators deploy IoT sensors for bin-fill monitoring and AI vision systems to cut sort-line labor by 40%. Compliance with National Center for Waste Management licenses and ISO 14001 certification is a must-have for municipal bid prequalification.

International entrants vie for differentiation via niche expertise. Veolia is piloting hazardous-waste vitrification, while SUEZ is introducing AI-driven predictive maintenance for fleet uptime. BEEAH Group is diversifying into hydrogen-from-waste pathways through Chinook collaborations, anticipating future demand for low-carbon transport fuels. Specialized newcomers like Edama Organic Solutions secure a share by turning organic fractions into value-added compost for desert agriculture, delivering both environmental and economic returns.

Competitive intensity is set to rise as carbon-credit monetization reshapes project economics. Early signatories to the Saudi Voluntary Carbon Market gain upside beyond tipping and energy fees. Simultaneously, margin compression in basic collection pushes incumbents toward vertical integration, from curb to commodity, across the Saudi Arabian waste management market.

Saudi Arabia Waste Management Industry Leaders

-

Saudi Investment Recycling Co. (SIRC)

-

BEEAH Group

-

Veolia Middle East

-

Averda

-

SUEZ Middle East

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Saudi Aramco launched a 12-tonne Direct Air Capture pilot in partnership with Siemens Energy to advance net-zero ambitions.

- February 2025: NEOM and DataVolt agreed to build a USD 5 billion net-zero AI factory powered by renewable energy, reinforcing circular principles.

- December 2024: NEOM and Samsung C&T formed a SAR 1.3 billion robotics joint venture expected to cut material waste by 40%.

- December 2024: Aramco, TotalEnergies, and SIRC advanced plans for a sustainable aviation-fuel plant using local waste oils.

Saudi Arabia Waste Management Market Report Scope

Waste management is the complete process of collecting, hauling, treating, and disposing of waste materials in a method that minimizes their impact on the environment and human health. It encloses various activities and practices to reduce waste generation and manage waste materials efficiently and sustainably.

The report provides a comprehensive background analysis of the market, covering the current market trends, restraints, technological updates, and detailed information on various segments and the competitive landscape of the industry.

The Saudi Arabian waste management market is segmented by waste type (industrial waste, municipal solid waste, e-waste, plastic waste, and biomedical and other waste types [including construction waste]), disposal method (landfill, incineration, recycling, and other disposal methods), and region (Riyadh, Jeddah, Dammam, Yanbu, and Other Regions). The report offers market sizes and forecasts for all the above segments in terms of value (USD).

| Residential |

| Commercial (retail, office, etc.) |

| Industrial |

| Medical (Health and Pharmaceutical) |

| Construction & Demolition |

| Others (institutional, agricultural, etc) |

| Collection, Transportation, Sorting & Segregation | |

| Disposal / Treatment | Landfill |

| Recycling & Resource Recovery | |

| Incineration & Waste-to-Energy | |

| Others (Chemical Treatment, Composting, etc.) | |

| Others (Consulting, Audit & Training, etc.) |

| Municipal Solid Waste |

| Industrial Hazardous Waste |

| E-waste |

| Plastic Waste |

| Biomedical Waste |

| Construction & Demolition Waste |

| Agricultural Waste |

| Other Specialized Waste (radio active, etc) |

| Riyadh |

| Makkah Province (incl. Jeddah) |

| Eastern Province (Dammam, Khobar) |

| Rest of Saudi Arabia |

| By Source | Residential | |

| Commercial (retail, office, etc.) | ||

| Industrial | ||

| Medical (Health and Pharmaceutical) | ||

| Construction & Demolition | ||

| Others (institutional, agricultural, etc) | ||

| By Service Type | Collection, Transportation, Sorting & Segregation | |

| Disposal / Treatment | Landfill | |

| Recycling & Resource Recovery | ||

| Incineration & Waste-to-Energy | ||

| Others (Chemical Treatment, Composting, etc.) | ||

| Others (Consulting, Audit & Training, etc.) | ||

| By Waste Type | Municipal Solid Waste | |

| Industrial Hazardous Waste | ||

| E-waste | ||

| Plastic Waste | ||

| Biomedical Waste | ||

| Construction & Demolition Waste | ||

| Agricultural Waste | ||

| Other Specialized Waste (radio active, etc) | ||

| By Region | Riyadh | |

| Makkah Province (incl. Jeddah) | ||

| Eastern Province (Dammam, Khobar) | ||

| Rest of Saudi Arabia | ||

Key Questions Answered in the Report

How large is the Saudi Arabia waste management market today?

The sector is valued at USD 25.84 billion in 2025 and is projected to climb to USD 37.70 billion by 2030.

Which segment holds the highest Saudi Arabia waste management market share?

Residential waste leads with 54.56% share as of 2024, anchored by dense urban households.

What area shows the fastest growth within the industry?

Commercial waste is expanding at a 9.60% CAGR thanks to retail and office development across major metros.

Why is recycling gaining momentum?

Vision 2030’s 94% landfill-diversion mandate and rising carbon-credit incentives are shifting investment from disposal toward material recovery.

Which region offers the strongest growth prospects?

The Eastern Province is forecast to grow at 8.19% CAGR through 2030 due to petrochemical and utility expansions.

How are companies differentiating themselves?

Leading operators integrate digital tracking, AI-powered sorting, and waste-to-energy solutions while forming joint ventures to access advanced technologies.

Page last updated on: