India Steel Market Size and Share

Market Overview

| Study Period | 2024 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

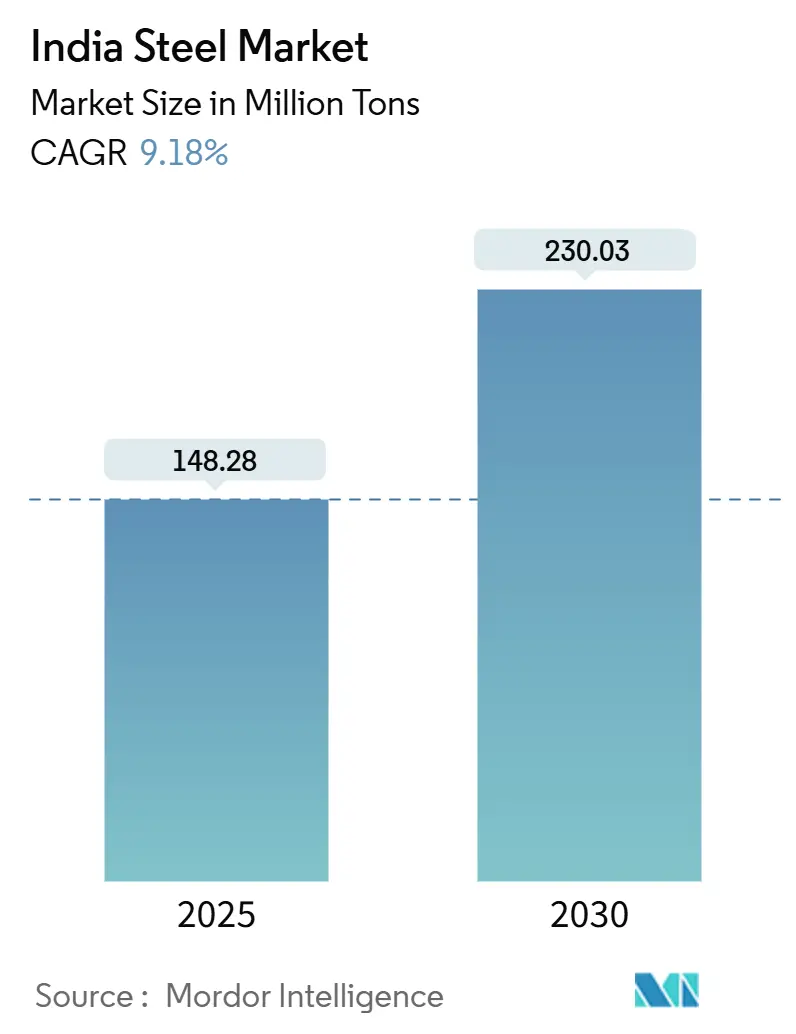

| Market Volume (2025) | 148.28 Million tons |

| Market Volume (2030) | 230.03 Million tons |

| Growth Rate (2025 - 2030) | 9.18% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Steel Market Analysis by Mordor Intelligence

The India Steel Market size is estimated at 148.28 million tons in 2025, and is expected to reach 230.03 million tons by 2030, at a CAGR of 9.18% during the forecast period (2025-2030). Expanding capacity targets of 300 million tons by 2030, accelerating infrastructure spending, and policy incentives together anchor this trajectory, positioning the India steel industry as the world’s second-largest producer cohort. Government-backed megaprojects such as Bharatmala’s 34,800 km highway build-out, PM-AWAS’s large-scale housing programs, and Smart Cities 2.0 create durable domestic offtake, while an emerging green-steel policy ecosystem channels investment toward low-carbon technologies. Competitive intensity remains high, as leading producers race to secure brown- and green-field capacity, hedge against import surges, and comply with export-linked environmental mandates, such as the EU’s CBAM. Simultaneously, state-level advantages in raw material availability and logistics connectivity spur an eastward production shift, supporting regional economic development and optimizing supply chain costs. Despite rising decarbonization outlays, capital efficiency gains, and value-added product strategies, these help shield operating margins amid volatile raw-material prices, thereby strengthening the overall resilience of the India steel industry.

Key Report Takeaways

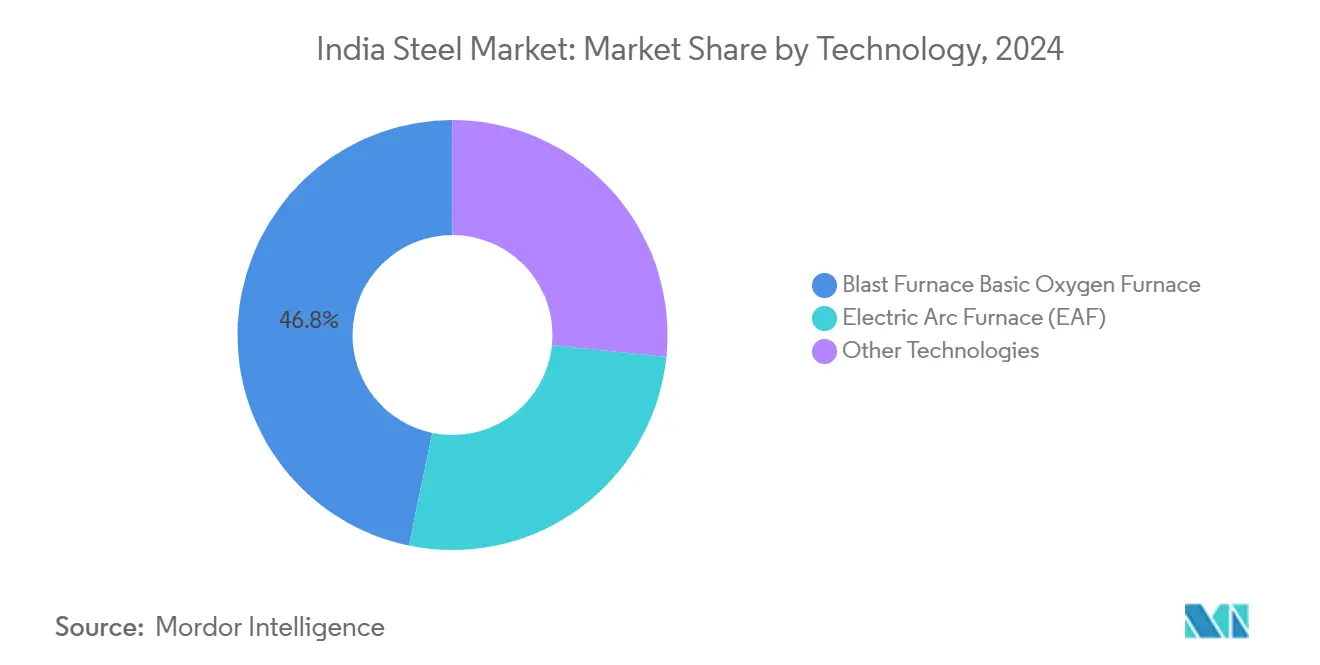

- By technology, the Blast Furnace-Basic Oxygen Furnace (BF-BOF) route held 46.76% of India Steel market share in 2024 and is expected to expand at an 8.88% CAGR through 2030.

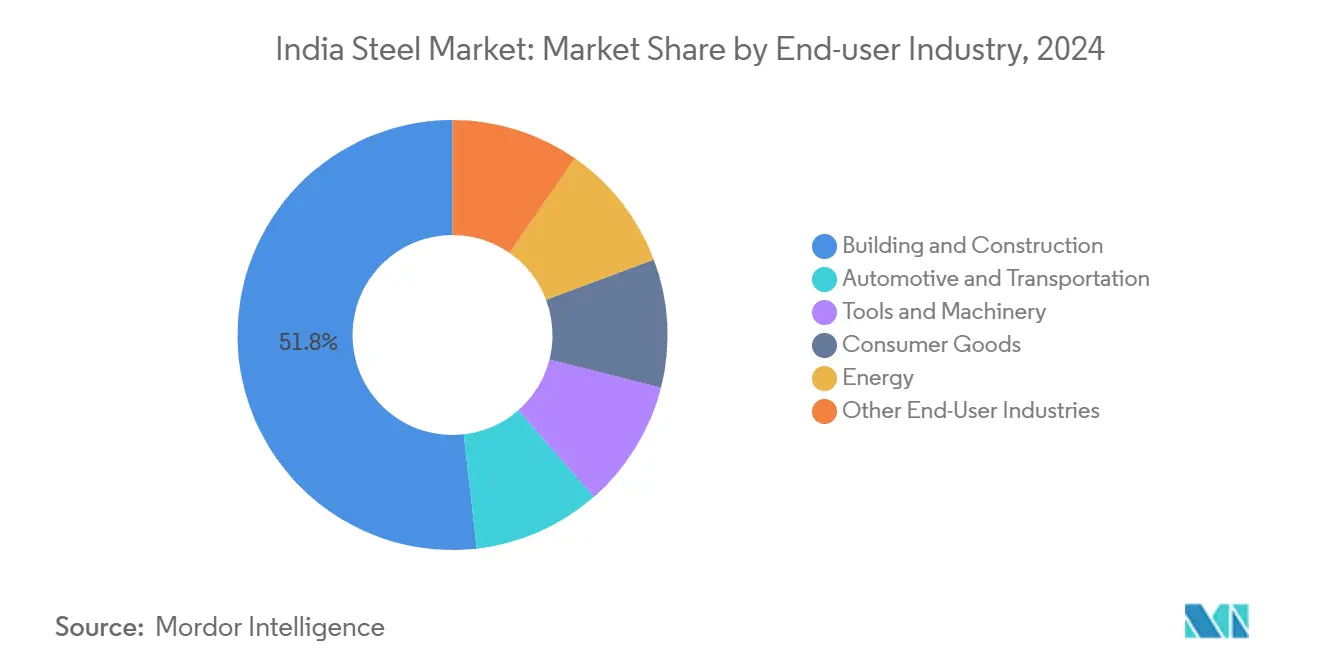

- By end-user industry, building and construction led with 51.79% of India Steel industry share in 2024 while also registering the fastest 10.01% CAGR through 2030.

India Steel Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong policy support | +2.1% | National; Odisha, Jharkhand, Chhattisgarh | Medium term (2-4 years) |

| Domestic and foreign CAPEX surge | +1.8% | APAC focus; eastern states | Long term (≥ 4 years) |

| Large infrastructure pipeline | +2.4% | National; Maharashtra, Uttar Pradesh, Gujarat | Medium term (2-4 years) |

| Automotive pivot to AHSS and EV-grade steels | +1.2% | National; automotive hubs | Long term (≥ 4 years) |

| Hydrogen-based DRI pilots ad scrap substitution | +0.9% | Odisha, Maharashtra | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong Policy Support

A comprehensive framework, combining the National Steel Policy’s 300 million ton capacity target, the PLI scheme for specialty steel, and the mandate for domestically manufactured iron and steel products, underpins demand certainty across the India steel industry. Production-linked incentives worth INR 27,106 crore have already unlocked 7.9 million tons of specialty capacity and nearly 15,000 jobs. Preferential procurement thresholds of 15–50% value-added bolster domestic suppliers in government tenders, while real-time import monitoring via the Steel Import Monitoring System refines trade remedy decisions. Infrastructure integration through PM-Gati Shakti lowers logistics costs by up to 15%, sharpening competitiveness for producers in mineral-rich regions. Finally, the Bureau of Indian Standards enforces quality compliance, ensuring that new capacity delivers globally acceptable product grades that align with export market requirements.

Surge in Domestic and Foreign CAPEX for Brown-/Green-field Capacity

Private and public commitments exceeding USD 25 billion have amplified the India Steel investment cycle, drawing marquee entrants and expanding incumbents. ArcelorMittal Nippon Steel’s INR 1.5 lakh crore Andhra Pradesh complex exemplifies technology-transfer driven upgrades in advanced high-strength grades. SAIL’s trajectory from 20 million tons to 35.65 million tons capacity by 2031, supported by incremental FY25 capex allocations, highlights public-sector alignment with national targets. Strategic FDI flows embed knowledge of low-carbon technologies, while mineral-rich eastern clusters shorten raw material supply lines and enable economies of scale. Employment multipliers reinforce state support, creating virtuous cycles of skill development and industrial growth across the India Steel industry.

Large Infrastructure Pipeline (Bharatmala, PM-AWAS, Smart Cities 2.0)

Central government infrastructure outlays rose fivefold since 2014, culminating in a record INR 11.11 trillion capital commitment for FY 2024-25[1]Ministry of Information & Broadcasting, “Building India – 10 Years of Infrastructure Development,” pib.gov.in . Bharatmala alone requires 15–20 million tons of steel for highway development, generating multi-year visibility for producers as Phase I nears completion in 2027-28. PM-AWAS envisions 3 crore new homes using steel-intensive precast systems that consume 20–30% more steel per unit than conventional methods. Smart Cities 2.0 drives demand for seismic-grade structural sections, while the National Infrastructure Pipeline mandates specialized long-product grades for bridges, ports, and rails. The Institute for Steel Development and Growth disseminates design templates that optimize steel utilization, reinforcing embedded demand through standardized specifications, further strengthening the India steel industry.

Hydrogen-Based DRI Pilots and Scrap Substitution Push

Pilot projects under the National Green Hydrogen Mission aim to validate 100% hydrogen-based DRI at a commercial scale, positioning India among early adopters[2]Ministry of New and Renewable Energy, “Scheme Guidelines for Pilot Projects for Use of Green Hydrogen in the Steel Sector,” mnre.gov.in. Tata Steel’s hydrogen injection trials at Jamshedpur achieved a 7–10% CO₂ reduction per ton of hot metal, setting proof-of-concept for hybrid BF-DRI operations. Jindal Steel’s blast-furnace syngas retrofit and Matrix Gas’s sponge iron pilot in Raipur expand the technology envelope. Concurrently, the Steel Scrap Recycling Policy aims to achieve a global benchmark scrap utilization rate of up to 70% by 2030, thereby creating pathways to reduce energy intensity and production costs. Together, hydrogen adoption and scrap substitution underpin the long-term decarbonization roadmap of the India steel industry.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Below-average per-capita consumption | -1.4% | Nation-wide; rural-urban gap | Medium term (2-4 years) |

| Volatile raw-material and energy costs | -1.8% | National; higher impact on coastal sites | Short term (≤ 2 years) |

| ESG-linked export carbon tariffs (EU CBAM) | -1.1% | Export-oriented producers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Per-Capita Steel Consumption Still Below Global Average

At 93.44 kg in 2023, India’s per-capita steel usage remains far below the 230 kg global mean, signaling untapped potential but also revealing structural bottlenecks. Rural markets, which account for 65% of the population, have disproportionately low demand due to limited infrastructure penetration and income constraints. Consumption disparities complicate capacity-planning decisions, as producers must balance supply expansion with realistic regional demand curves. These patterns underline the need for parallel investments in rural infrastructure to unlock the full potential of the India Steel industry.

ESG-Linked Export Carbon Tariffs (EU CBAM)

The EU’s Carbon Border Adjustment Mechanism, effective 2026, could add USD 80-397 per ton cost to Indian steel exports, jeopardizing competitiveness. High exposure to European customers necessitates rapid investments in decarbonization, such as hydrogen DRI, renewable power integration, and carbon capture retrofits. Compliance reporting increases administrative burden and working capital needs, particularly for mid-sized exporters. While domestic demand growth buffers volume risk, profit margins face new headwinds unless producers secure green steel premiums or diversify their export destinations. State and federal incentives for low-carbon technology adoption thus become pivotal in maintaining export viability for the India Steel industry.

Segment Analysis

By Technology: BF-BOF Dominance Drives Transition Dominance Drives Transition

The BF-BOF route held 46.76% India Steel industry share in 2024, a level underscoring the entrenched integrated-plant footprint that still delivers cost advantages on large volumes. The India steel market size for BF-BOF output is forecast to compound at an 8.88% CAGR as producers sweat existing assets even while charting decarbonization roadmaps. Declining unit emissions through incremental efficiency gains and partial hydrogen injection illustrate pragmatic transition pacing. Electric-arc furnaces are gaining traction in scrap-rich urban clusters, signaling a future redistribution of capacity toward low-carbon hubs. Emerging hydrogen DRI pilot plants introduce a third vector, although commercial uptake hinges on green-hydrogen cost parity, which is expected only beyond 2030.

In the medium term, BF-BOF complexes evolve through the use of hot-blast stoves, top-pressure recovery turbines, and slag granulation upgrades, thereby enhancing energy recovery and product quality. Technology partnerships accelerate process-control digitalization, widening yield spreads between best- and average-practice plants. Meanwhile, secondary producers leverage EAF flexibility to nimbly supply specialty grades and meet evolving construction standards. The coexistence of multiple routes reflects the India Steel market size and varied regional scrap-availability profiles, suggesting a gradual rather than abrupt technology realignment.

Note: Segment shares of all individual segments available upon report purchase

By Basic Form: Crude Steel Foundation

Crude steel constitutes the entire basic-form segment and is forecast to climb at a 7.81% CAGR, mirroring upstream capacity additions across integrated and secondary mills. High utilization rates of roughly 80% underscore latent headroom before extensive green-field builds are required. Iron-ore self-sufficiency across Odisha, Chhattisgarh, and Karnataka grants crude-steel producers a sustained raw-material edge compared with import-dependent peers in Southeast Asia, strengthening the india steel industry position in the region.

Enabling policies, such as captive mine allocations and express environmental clearances for expansion projects, expedite throughput gains in the India steel market. Simultaneously, the Steel Scrap Recycling Policy aims to lift scrap use from 25% to 70%, driving process efficiency. Crude steel players are increasingly integrating predictive maintenance analytics and process optimization software, narrowing the gap to best performance and trimming energy intensity. These moves collectively solidify the segment’s centrality within the India steel industry.

By Final Form: Finished Steel Market Leadership

Finished products occupy the complete final-form share and are projected to grow at a 9.18% CAGR to 2030, outpacing upstream output due to value-added mix upgrades, highlighting trends in the India steel industry. Structural long products feed infrastructure builds, while coated flat-steel demand accelerates from consumer durables and solar panel frame applications. Value-added products already account for 60% of revenue at leading mills, underscoring the success of premiumization strategies.

By End-User Industry: Construction Sector Supremacy

Building and construction accounted for 51.79% India's Steel market share in 2024 and retains the top growth slot with a 10.01% CAGR through 2030. The India steel market size for construction applications expands alongside highway, metro-rail, and port upgrades, with budget allocations at record levels. Pre-engineered buildings and modular housing accelerate steel intensity, while seismic-code revisions raise grade and tonnage requirements.

Automotive and transportation rank second, buttressed by EV penetration and tightened crash-safety norms that necessitate AHSS, reflecting growth in the India steel industry. Energy projects, from transmission towers to offshore wind foundations, create a new demand frontier. Tools and machinery benefit from the government’s Production-Linked Incentive schemes for capital-goods localization, whereas consumer-goods grade demand grows with rising disposable incomes. Regulatory oversight via IS standards guarantees consistent quality, enhancing structural integrity and safety across use cases.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Capacity investments such as Tata Steel’s INR 27,000 crore Kalinganagar expansion leverage proximity to raw materials, reducing inbound logistics costs and anchoring regional clusters in the India steel industry. Chhattisgarh, Jharkhand, and West Bengal complement this axis, collectively providing the bulk of indigenous ore and coal linkages.

Maharashtra is underpinned by industrial hubs and urban infrastructure outlays, while Gujarat’s export-oriented manufacturing base pulls specialty grades, reinforcing demand diversity within the India Steel market. Northern states capture highway and defense allocations, whereas southern coastal states exploit port infrastructure for import substitution and export dispatch. The National Highway network’s growth to 146,145 km in 2023 reduced inland freight time, converged regional transaction prices, and broadened supplier reach in the india steel industry.

The PM-Gati Shakti plan integrates rail, road, and port connectivity, promising 15–20% logistics cost savings and thereby increasing the size of the India Steel market accessible to interior producers. Dedicated freight corridors nearing completion offer predictable haulage for bulk steel, mitigating seasonal bottlenecks. Coastal shipping policy incentives further align with emission-reduction goals by shifting heavy cargo from highways to sea routes. Collectively, geographic synergies widen competitive options for India Steel market participants.

Competitive Landscape

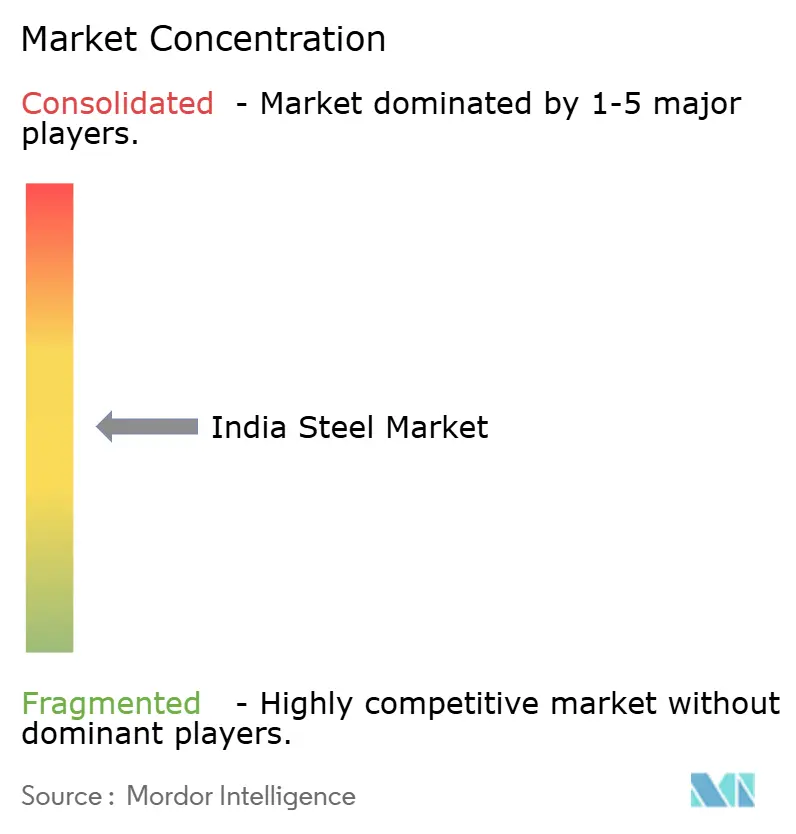

The market is moderately fragmented. Raw-material backward integration, proprietary rail sidings, and captive power plants provide scale economies and shield leading mills from input volatility. Secondary EAF-based producers, although smaller, service regional requirements with flexible melt capacities and quicker grade turnover, supporting customer-centric niches. Import pressures from China and Vietnam prompted anti-dumping investigations into hot-rolled coils, leading to provisional duties that shield domestic mills from margin erosion. However, compliance with the forthcoming EU CBAM re-orders cost structures, compelling accelerated decarbonization investments across the India Steel market. Firms that secure renewable-power PPAs and develop green-hydrogen sourcing are expected to command premium export lanes, reinforcing a twin-track competitive paradigm of scale and sustainability leadership.

India Steel Industry Leaders

-

Steel Authority of India Limited (SAIL)

-

AM/NS INDIA

-

Jindal Steel & Power Limited

-

JSW Steel Limited

-

Tata Steel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: JSW Group announced a INR 1 lakh crore (USD 12 billion) investment to construct a steel plant in Gadchiroli, Maharashtra, with 25 million tonnes annual capacity.

- November 2024: ArcelorMittal Nippon Steel India announced an INR 1.5 lakh crore (~USD 18 billion) integrated plant at Anakapalle, Andhra Pradesh, with a 24 million ton capacity and 70,000 job creation.

India Steel Market Report Scope

Steel is an iron alloy with additional carbon to increase its strength and fracture resistance. It is utilized in structures, infrastructure, tools, ships, trains, cars, machinery, electrical appliances, weaponry, and rockets.

India Steel Market is segmented by form (basic form (crude steel), and final form (finished steel)), technology (Blast Furnace-Basic Oxygen Furnace (BF-BOF), electric arc furnace, and other technologies), and end-user industry (automotive and transportation, building and construction, tools and machinery, energy, consumer goods, and other end-user industry (oil and gas extraction equipment, furniture, pipes, barrels, drums, packaging, semiconductors)). The report also includes market sizes and forecasts for the volume market in India. For each segment, market size and forecasts are based on volume.

| Blast Furnace-Basic Oxygen Furnace (BF-BOF) |

| Electric Arc Furnace (EAF) |

| Other Technologies |

| Crude Steel |

| Finished Steel |

| Automotive and Transportation |

| Building and Construction |

| Tools and Machinery |

| Consumer Goods |

| Energy |

| Other End-User Industries |

| By Technology | Blast Furnace-Basic Oxygen Furnace (BF-BOF) |

| Electric Arc Furnace (EAF) | |

| Other Technologies | |

| By Basic Form | Crude Steel |

| By Final Form | Finished Steel |

| By End-user Industry | Automotive and Transportation |

| Building and Construction | |

| Tools and Machinery | |

| Consumer Goods | |

| Energy | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the projected volume of steel production in India by 2030?

The India Steel market is forecast to reach 230.03 million tons by 2030, up from 148.28 million tons in 2025.

How fast is the domestic construction segment expanding?

Building and construction steel demand is growing at a 10.01% CAGR through 2030, supported by record infrastructure budgets.

Which technology route currently dominates Indian steelmaking?

The BF-BOF route holds 46.76% share, though electric-arc furnaces and hydrogen DRI pilots are gaining traction.

How will the EU’s CBAM affect Indian steel exporters?

The CBAM could add USD 80-397 per ton in costs from 2026, pressing exporters to accelerate decarbonization strategies.

Page last updated on: