Titanium Alloy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

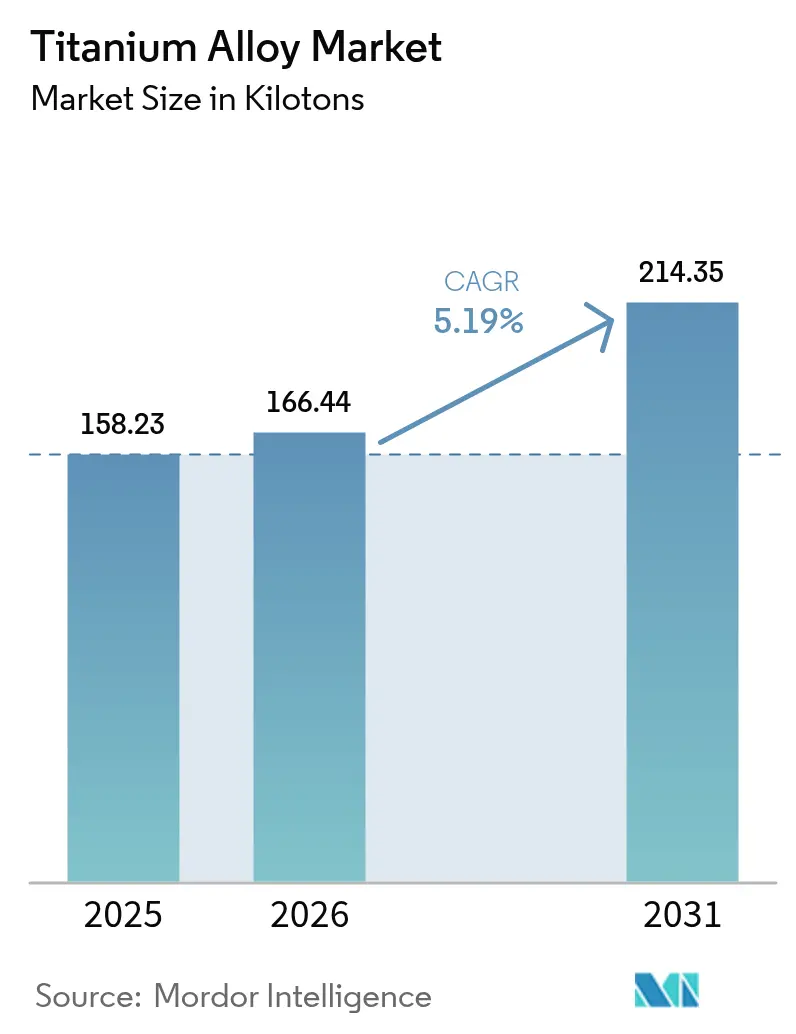

| Market Volume (2026) | 166.44 kilotons |

| Market Volume (2031) | 214.35 kilotons |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

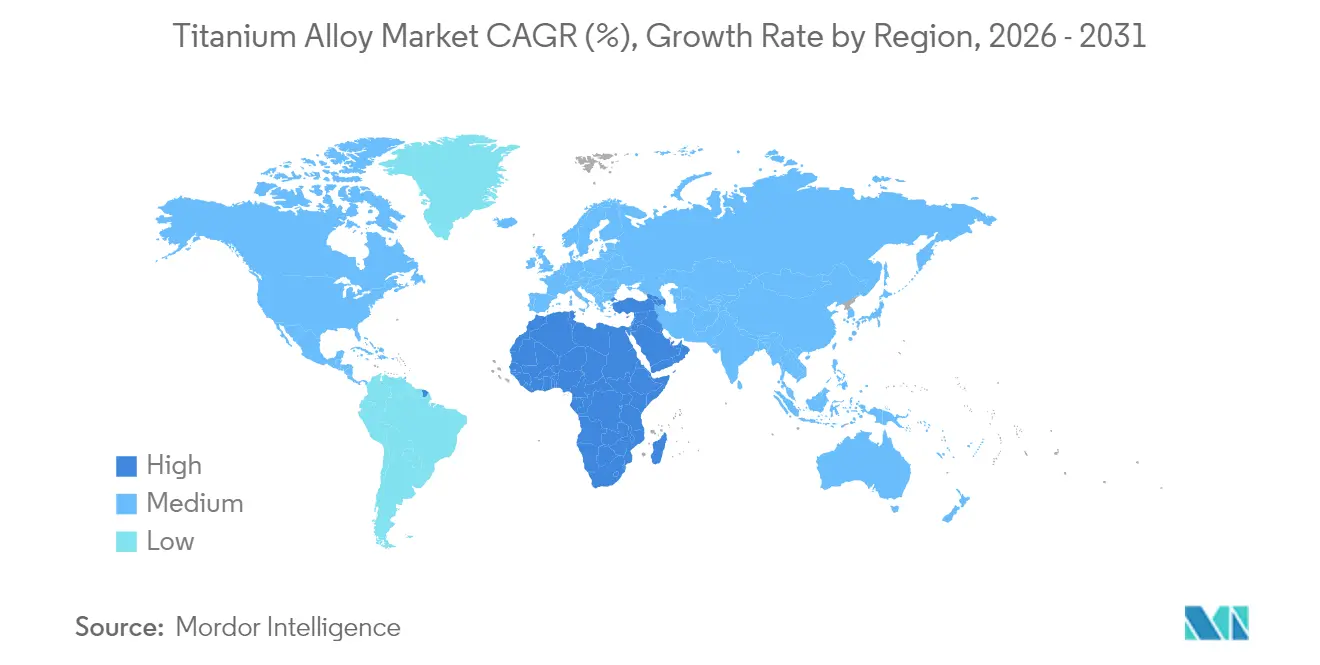

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Titanium Alloy Market Analysis by Mordor Intelligence

The Titanium Alloy Market size is expected to grow from 158.23 kilotons in 2025 to 166.44 kilotons in 2026 and is forecast to reach 214.35 kilotons by 2031 at 5.19% CAGR over 2026-2031. Consistent order backlogs at Boeing and Airbus, revived defense procurement cycles, and a widening medical-implant customer base anchor demand. Sustained performance hinges on titanium’s high strength-to-weight ratio, corrosion resistance, and biocompatibility, traits that continue to outweigh its higher production cost in critical applications. Producers are adding melt capacity, often through hydrogen-assisted reduction or additive manufacturing, to alleviate supply bottlenecks, while customers diversify sourcing to mitigate geopolitical risk. Cost-down innovation and regulatory push for fuel-efficient aircraft further reinforce the growth narrative of the titanium alloy market.

Key Report Takeaways

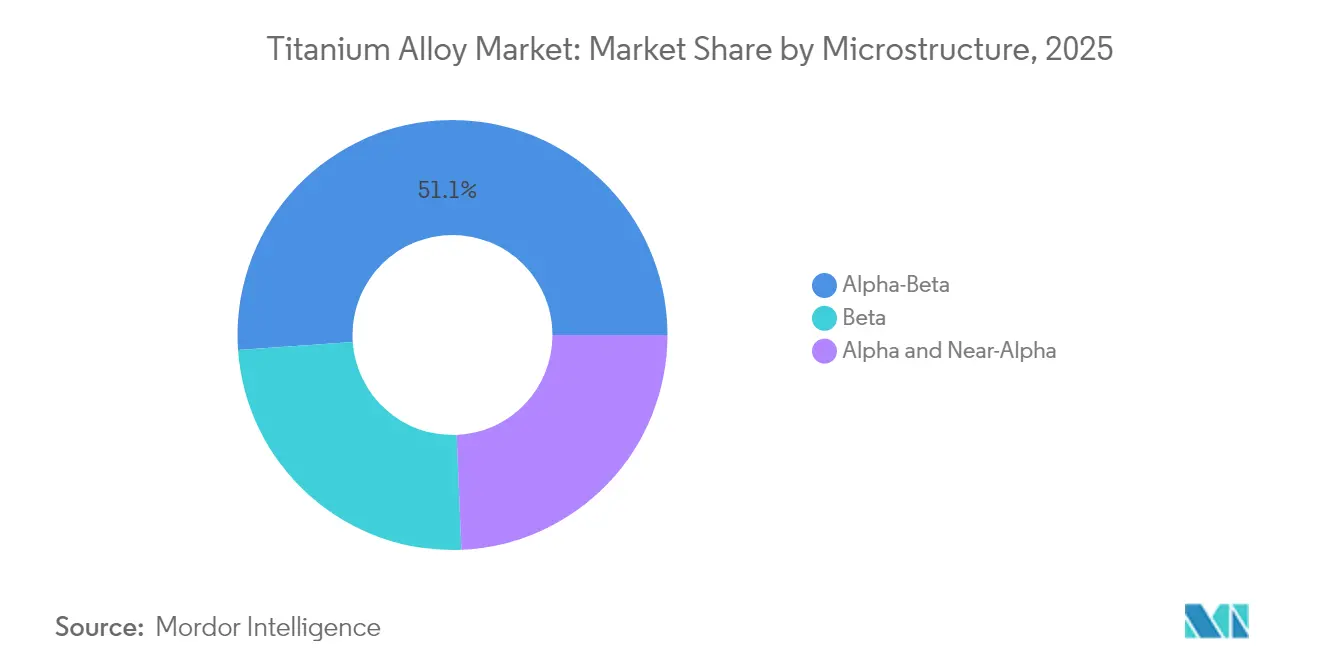

- By microstructure, Alpha-Beta grades led with 51.12% share of the titanium alloy market size in 2025; Beta alloys are projected to expand at 6.02% CAGR to 2031.

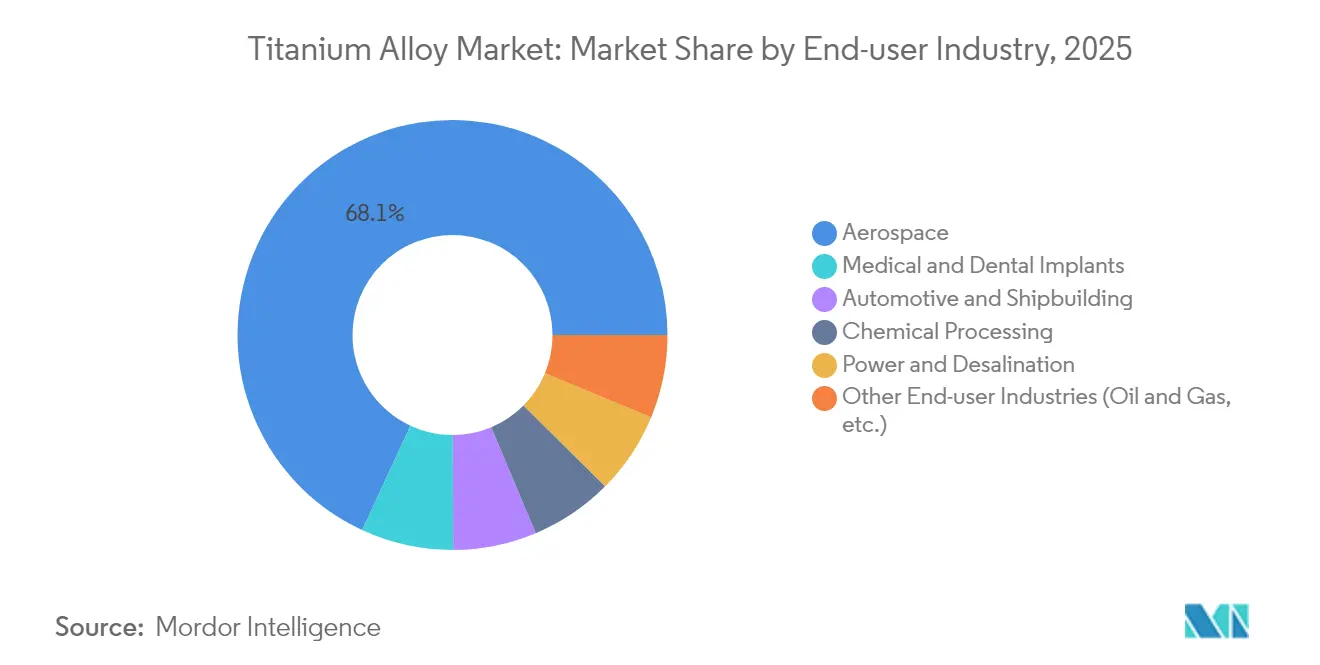

- By end-user industry, aerospace commanded 68.10% of the titanium alloy market share in 2025, whereas medical and dental implants are advancing at a 7.12% CAGR through 2031.

- By geography, Asia-Pacific held 41.02% of the titanium alloy market in 2025, while the Middle East and Africa region exhibits the fastest growth at 5.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Titanium Alloy Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing aerospace and defense airframe demand | +1.8% | Global (North America, Europe core) | Medium term (2-4 years) |

| Military ground-vehicle light-weighting | +0.9% | North America and Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Expansion of medical and dental procedures | +1.2% | Global, strongest in Asia-Pacific and MEA | Short term (≤ 2 years) |

| Additive manufacturing unlocking new grades | +0.7% | North America and Europe, Asia-Pacific | Medium term (2-4 years) |

| Hydrogen-economy heat-exchanger uptake | +0.4% | Europe and North America, pilots in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Aerospace and Defense Airframe Demand

Orders exceeding 15,000 commercial aircraft place titanium squarely in structural, landing-gear, and engine components, where weight reduction translates into fuel savings. ATI drew 66% of Q1 2025 revenue from aerospace and defense and locked in a five-year USD 1 billion supply pact with Airbus. Howmet Aerospace recorded 17% commercial-aerospace sales growth in Q3 2024 on surging engine demand. Titanium intensity now reaches 15-25% of a jet engine’s weight, while defense programs specify the alloy for stealth and durability. Diversification away from Russian feedstock is driving new partnerships with Japanese and Middle Eastern suppliers, reinforcing the titanium alloy market’s production realignment.

Military Ground-Vehicle Light-Weighting Programs

Defense planners increasingly swap steel for titanium in armor, drivetrains, and suspensions to boost range and payload without sacrificing protection. The U.S. Department of Defense’s USD 47.1 million award to IperionX underscores a national push for secure, low-cost titanium capacity. NATO standards that harmonize material specifications amplify cross-border demand, and field data show 15-20% fuel savings when titanium components replace steel. Advanced manufacturing shortens part lists, easing maintenance burden for deployed vehicle fleets and fueling long-run momentum in the titanium alloy market.

Expansion of Medical and Dental Implant Procedures

Titanium’s biocompatibility keeps it the implant metal of choice as global populations age. Selective laser melting now delivers patient-specific knee, hip, and dental fixtures with lattice structures that promote osseointegration while cutting waste. Research into Ti-Ta-Cu systems shows elastic moduli closer to natural bone, widening clinical applicability. Revised ISO 5832-11:2024 criteria for Ti-6Al-7Nb tighten quality benchmarks. Rising surgical volumes in Asia-Pacific and MEA funnel steady demand into the titanium alloy market.

Additive Manufacturing Unlocking Novel Grades

3D printing unlocks alloy chemistries that were once uneconomical or impossible. RMIT researchers produced a 29% cheaper grade by swapping vanadium for cost-effective elements while improving strength. MIT and ATI advanced lattice-distortion strategies to upend the classic strength-ductility compromise. Powder-atomization upgrades cut electricity use by 50% and argon by 98%, bringing unit costs down. Greater design freedom shortens ramp-up for aerospace and medical programs, injecting incremental growth into the titanium alloy market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost and complex metallurgy | -1.4% | Global (sharpest in emerging markets) | Medium term (2-4 years) |

| Limited global sponge capacity | -0.8% | North America and Europe | Short term (≤ 2 years) |

| Geopolitical dependence on Russian feedstock | -0.6% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Cost and Complex Metallurgy

The legacy Kroll route burns 11-13 MWh per ton, making titanium 3-4 times pricier than aluminum and 10-15 times pricier than steel. Reactive metallurgy demands inert atmospheres and specialized cutting fluids, hampering productivity in downstream machining. Hydrogen-assisted reduction pathways promise lower temperatures but remain pre-commercial. University of Tokyo techniques for oxygen removal via yttrium reactions offer potential cost savings, yet industrial scaling is several years. Until new processes mature, elevated conversion costs cap the full potential of the titanium alloy market.

Geopolitical Dependence on Russian Feedstock

VSMPO-AVISMA accounted for most Western jet-grade supply before sanctions, forcing OEMs to scramble for Japanese and Middle Eastern alternatives. Airlines continue to accept limited waivers for legacy contracts, reflecting the narrow pool of certified providers. Strategic reserves cushion the short run, but fresh geopolitical shocks could reverberate quickly through the titanium alloy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Microstructure: Beta Alloys Drive Innovation

Beta alloys are projected to register a 6.02% CAGR through 2031, while Alpha-Beta grades retained 51.12% of the titanium alloy market share in 2025. Ti-5553 demonstrates superior castability, delivering high strength-to-weight ratios vital for wing-carry-throughs and landing-gear structures. Research into high-entropy intermetallics incorporating zirconium and hafnium achieves yield strengths of 1.5 GPa with 8% plastic strain, expanding options for hypersonic applications.

Ongoing additive-manufacturing deployments enable near-net-shape production, slashing buy-to-fly ratios by up to 60% and supporting intricate cooling-channel architectures in turbine blades. Beta alloys' titanium alloy market size is on track to close the decade at roughly 25% of overall volume, supported by synergistic gains in powder-atomization capacity and qualification tests for critical flight hardware. Parallel interest in Alpha and Near-Alpha alloys for temperatures above 500 °C preserves demand in gas turbines and space-propulsion contexts. As producers standardize vacuum-arc-remelting parameters, alloy chemistries stabilize, improving confidence among aerospace and defense primes.

By End-User Industry: Medical Applications Accelerate

Aerospace maintained 68.10% of the titanium alloy market in 2025, but medical implants are slated for the highest growth at a 7.12% CAGR through 2031. Patient-specific hip and knee replacements are moving from pilot programs to mainstream adoption as hospital systems invest in point-of-care 3D-printing suites. Surgeons value titanium’s osseointegration and low allergic response rates, ensuring long-term demand despite pricing premiums. Dental implants follow a similar trajectory, driven by cosmetic dentistry in emerging economies. Automotive uptake remains niche, exemplified by Nippon Steel’s Super-TIX connecting rods, which deliver 50% higher specific strength than steel while trimming rotational mass.

Stronger government mandates on vehicle emissions could unlock broader mobility applications, but present cost differentials constrain large-scale penetration. Meanwhile, titanium’s dominance in orthopedic screws, plates, and spinal cages accelerates as healthcare access widens in Asia-Pacific.

Geography Analysis

Asia-Pacific commanded 41.02% of the titanium alloy market in 2025, anchored by China’s 60% share of global metal output. However, the region’s aerospace certification gap curtails immediate penetration into high-value jet programs. India collaborates with HAL and DRDO on indigenous sponge capacity, while Australian miners explore downstream alloying to capture margin farther along the value chain. These initiatives collectively support robust volume gains, although quality hurdles remain.

The Middle East and Africa region, expanding at a 5.85% CAGR, benefits from Saudi Arabia’s USD 46 billion mining strategy, which aims to lift mining GDP share to 75 billion by 2030 and position the kingdom as a neutral titanium supplier. North American consumption stays high despite minimal sponge output. Cumberland County, North Carolina, secured a USD 867 million plant to rebuild domestic capacity with hydrogen-assisted reduction that could supply 10,000 tons annually once fully operational. In Canada, Quebec’s hydro-powered ilmenite operations explore vertically integrating into low-carbon sponge.

Across the Atlantic, European OEMs juggle sanction compliance and production continuity, prompting joint-venture discussions with Kazakh and Japanese suppliers; the EU’s Critical Raw Materials Act expedites permitting for sponge projects in Norway and Spain. South America remains largely a raw-ore exporter, but Brazil’s state development bank signals interest in co-financing downstream alloy plants near existing ilmenite mines. Overall, shifting supply footprints continue to reshape the titanium alloy market.

Value Chain Analysis

The titanium alloy value chain starts with mineral feedstocks (ilmenite and rutile), moves through beneficiation into titanium slag and TiCl4, and then uses the Kroll route to produce titanium sponge. From there, producers convert sponge into titanium ingot via primary melting (VIM/VAR), shape it into mill products (plate, sheet, bar, billet, wire), and finish parts through machining, forging, casting, and additive manufacturing (powder or wire feedstock). The main constraints tend to sit upstream in chloride-route feedstock quality and aerospace-qualified sponge availability, and midstream in specialized melt capacity and qualification. EU reference points continue to show aerospace as the dominant pull on titanium metal consumption, which tightens qualification requirements and raises switching costs across the chain.

Recent capacity and localization moves show how participants are trying to de-risk supply outside traditional certified sources. In April 2025, Pangang Group reached full production on a 35,000 mt titanium sponge expansion, lifting total annual capacity above 60,000 mt and reinforcing China-focused vertical integration. In December 2024, Indian Rare Earths Limited partnered with Kazakhstan-based UKTMP JSC to develop ilmenite-to-slag capability for sponge, and in March 2025, PTC Industries (Aerolloy Technologies) commissioned a 1,500 t/yr VAR furnace and signed a sponge supply agreement with Amic Toho Titanium Metal (ATTM) to support aerospace-grade ingot production. On the downstream side, OEM and Tier suppliers are leaning more on near-net-shape routes (AM and advanced casting) to improve lead times and lower buy-to-fly ratios. As certified material stays constrained, scrap recycling and closed-loop programs are also becoming more visible in customer qualification planning.

Competitive Landscape

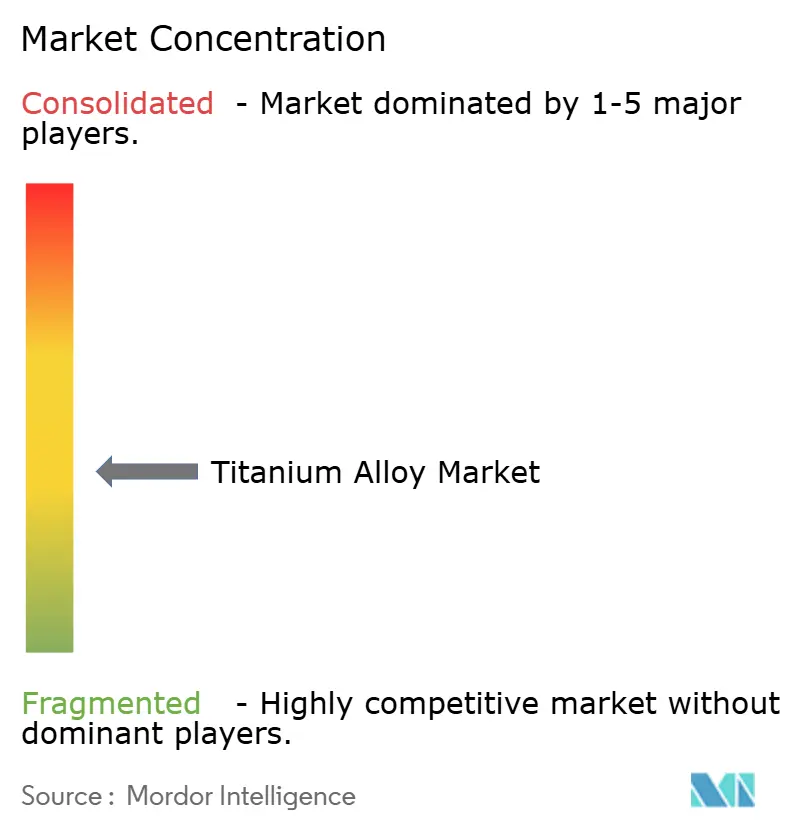

The titanium alloy market is moderately fragmented. Incumbents maintain technological and contractual moats, yet the field is far from oligopolistic. ATI closed a multi-year expansion that lifts titanium melt capacity 80% by 2025, anchoring long-term contracts with Airbus and Boeing. Mergers and specialized joint ventures target vertical integration. Powder suppliers partner with aerospace primes for closed-loop recycling, while medical-implant OEMs invest in captive printing farms to lock in powder supply. Competitive intensity therefore remains moderate, with process patents, customer qualification, and capacity scale serving as key differentiators in the titanium alloy market.

Titanium Alloy Industry Leaders

ATI

Howmet Aerospace

PJSC VSMPO-AVISMA Corporation

TIMET (Precision Castparts Corp.)

Toho Titanium Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is tied to shortening qualification-to-production cycles for aerospace structures, while also reducing the material penalty associated with traditional forging and machining. In April 2026, GKN Aerospace and the U.S. Air Force Research Laboratory launched the USD 8.4 million TITAN-AM program to industrialize wire-based laser metal deposition for aerospace structural components, which indicates a shift from demonstrators toward repeatable process windows. In May 2026, Norsk Titanium outlined an approach to embed Rapid Plasma Deposition machines at Airbus facilities, starting with the Varel site in Germany, reflecting a model where titanium near-net-shape capability moves closer to final assembly and supplier logistics.

Supply-chain localization and downstream conversion capacity can also translate into buyer opportunities where aerospace-qualified inputs and conversion steps are constrained. In July 2025, ATI expanded its long-term titanium supply agreement with Boeing to include flat-rolled titanium sheet from its Pageland, South Carolina facility, supporting a move toward more domestic sheet availability for airframe and engine-adjacent applications. In Europe, financing is aimed at reducing dependence on external large-scale conversion: in July 2025, Aubert and Duval secured EUR 51.1 million in state-backed financing for a new 6,000-ton forging press at Pamiers, addressing a conversion choke point for critical titanium parts. New entry efforts in emerging supply hubs add further whitespace, including the Bahrain Titanium (BTI) project announced with a staged plan (4,000 t/yr commercially pure slabs, followed by 10,000 t/yr titanium alloy billets), which would give aerospace, defense, and industrial buyers additional non-traditional sourcing options once qualified.

Recent Industry Developments

- June 2026: ATI extended its agreement with BWX Technologies under a five-year strategic materials arrangement supporting the U.S. Naval Nuclear Propulsion Program through 2030. The scope includes titanium among other advanced materials, reinforcing defense-linked demand visibility and long-horizon planning for melt and conversion capacity.

- February 2026: JX Advanced Metals announced a share exchange agreement to acquire Toho Titanium Co., Ltd. as a wholly owned subsidiary, with an effective date of June 1, 2026. The consolidation tightens integration between upstream titanium materials and downstream customer needs, with potential to streamline investment and qualification priorities within the combined group.

- July 2024: MIT researchers and ATI Specialty Materials disclosed titanium alloy developments aimed at overcoming the traditional strength-ductility trade-off through targeted composition and processing. The work supports a broader pipeline of higher-performance alloys for aerospace and other critical applications where properties and manufacturability are jointly constrained.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the titanium alloy market is counted as the demand and supply of titanium alloy materials sold in standard product forms (such as mill products, castings, and powders) across end-use industries worldwide, measured as volume shipped/consumed.

Scope exclusions: We exclude commercially pure titanium, titanium sponge traded as a standalone commodity, titanium dioxide pigment, and finished end-products that merely contain titanium alloy parts.

Segmentation Overview

- By Microstructure

- Alpha and Near-Alpha

- Alpha-Beta

- Beta

- By End-User Industry

- Aerospace

- Automotive and Shipbuilding

- Chemical Processing

- Power and Desalination

- Medical and Dental Implants

- Other End-user Industries (Oil and Gas, etc.)

- Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the factual base for the model, before any assumptions are applied. We leaned on public sources such as the USGS for titanium supply context, UN Comtrade for trade flows, IEA for power and energy indicators that affect industrial demand, and the FAA and EASA for aircraft production and fleet signals that influence aerospace pull-through.

Alongside this, company filings and investor presentations were reviewed to understand capacity additions, alloy mix shifts, and expansion timelines, which are then reflected as constraints in the supply side. Patent databases and peer reviewed materials journals were also scanned to understand where alloy grades and processing routes are moving, which helps sanity-check the pace of adoption in medical and industrial uses. For deal activity and shipment visibility, we also referenced a paid subscription focused on import and export shipments, but only as a check and not as a single point of truth. The desk sources cited here are illustrative, and many other public references were used to collect, cross-check, and clarify inputs.

Primary Interviews and Surveys

Primary work was used to pressure-test the model where public data is either delayed or reported at an aggregated level. We spoke with participants across alloy production, conversion, and distribution, and we also included buyers and technical stakeholders from aerospace, medical, chemical processing, and power related applications to confirm volume trends, alloy preferences, and pricing logic.

Coverage was balanced across APAC, EMEA, and the Americas so regional mix shifts, qualification cycles, and lead time changes were reflected consistently, and then our assumptions were adjusted where multiple respondents pointed to the same variance.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 14% | APAC: 51% |

| Mid tier: 47% | Functional/Unit leaders: 40% | EMEA: 31% |

| Smaller Players: 15% | Managers: 46% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where aircraft production and delivery schedules, medical implant procedure growth, and industrial corrosion resistant equipment demand are translated into an alloy demand pool, which is then reconciled to regional supply availability and trade movements. To keep the numbers realistic, results were corroborated with selective bottom-up approximations such as sampled producer and converter volume roll-ups, channel checks with distributors, and simple volume by typical conversion yield checks.

A few inputs that mattered in the model were aerospace build rates and backlog release timing, defense procurement tempo, the mix shift between alpha, alpha-beta, and beta alloys in key applications, conversion yields from melt to mill product, and regional import reliance for titanium alloy semi-finished forms. Where bottom-up coverage was incomplete, gaps were handled by using conservative penetration rates by end-use and then re-checking totals against trade balances and capacity utilization signals.

For forecasting, we used scenario analysis anchored to end-use demand drivers, followed by smoothing to avoid unrealistic year-to-year jumps. The demand cases were refined using what interviewees shared on qualification lead times, new melt capacity ramp-up, and the pace of supply chain normalization, and then a single base case was selected for the published outlook.

Data Validation & Update Cycle

Outputs are validated through multiple checks so one noisy input does not drive the final number. We compare totals against independent signals such as regional trade direction, stated capacity additions, and end-use production indicators, and then any large variance is investigated and corrected with a clear reason logged in the model.

Before sign-off, the work is reviewed in steps, starting with consistency checks on units, definitions, and regional splits, followed by an internal review for assumption logic and year-over-year movement. If a mismatch appears or a material event occurs (for example, a major capacity change or a sharp aerospace delivery revision), experts are re-contacted so the assumption set is refreshed. Reports are refreshed annually, and a final pre-delivery scan is done so clients receive the latest updated view.

Mordor Intelligence's Titanium Alloy Market Sizing Compared With Other Published Estimates

It is common to see different market sizes for titanium alloys because researchers do not always count the same thing, even when the title looks identical. The biggest differences usually come from whether a study is counting value or volume, which product forms are included, and how price assumptions are updated across years.

By tracking end-use demand signals and reconciling them with trade and capacity checks, Mordor Intelligence keeps the titanium alloy estimate tied to shipped material volumes, while many external studies express the market in USD and may also mix in adjacent titanium products or different form factors.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 166.44 B (2026) | |

| Global Consultancy A | USD 5.40 B (2025) | Reported in USD value terms, which can move mainly due to price and FX assumptions, and scope may include broader titanium alloy revenue pools beyond shipped volume totals. |

| Industry Publisher B | USD 6.90 B (2025) | Uses a value-based definition and often counts additional product forms like powders and castings with differing price points, which can lift the total versus a strict volume-only yardstick. |

The table shows that the widest spread comes from unit choice and scope boundaries, rather than one side being simply right or wrong. When the market is modeled from observable demand drivers and then checked against supply and trade constraints, the final number becomes easier to repeat, explain, and update as new signals appear.

Key Questions Answered in the Report

How large is the titanium alloy market in 2026 and what CAGR is expected to 2031?

The titanium alloy market size stands at 166.44 kilotons in 2026 and is set to grow at a 5.19% CAGR, reaching 214.35 kilotons by 2031.

Which application segment is expanding the fastest?

Medical and dental implants show the fastest growth, projected at a 7.12% CAGR through 2031 due to rising surgical volumes and 3D-printed patient-specific solutions.

Which microstructure segment holds the largest share today?

Alpha-Beta grades lead, accounting for 51.12% of titanium alloy market share in 2025, thanks to their balance of strength and formability for aerospace structures.

Which region is expected to record the highest growth?

The Middle East and Africa region is forecast to be the fastest-growing geography at a 5.85% CAGR, bolstered by Saudi mining investments and neutral supplier positioning.

What is the primary supply-side challenge facing titanium producers?

Limited aerospace-qualified sponge capacity and high energy costs from the Kroll process constrain output, creating a supply bottleneck for downstream alloy production.

Page last updated on: